Global agriculture & commodity market insights | Ex-FAO | Data-driven analysis on food security, prices & trends

Joined April 2026

- Tweets 7

- Following 24

- Followers 0

- Likes 0

2 Photos and videos

May 18

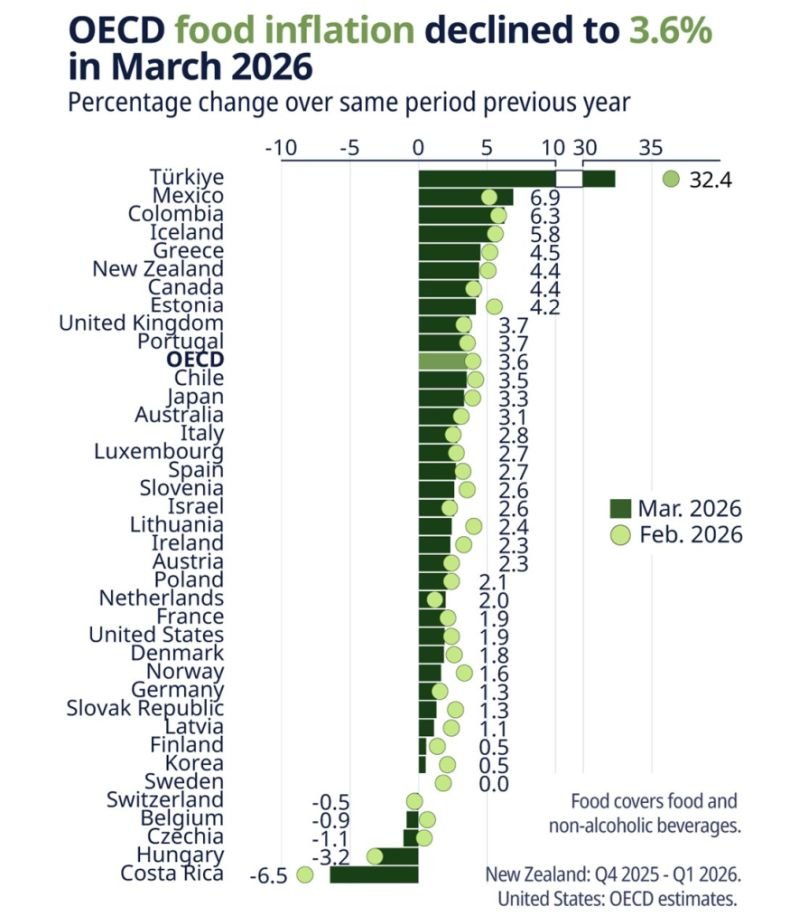

OECD food inflation eased to 3.6% YoY in March 2026, but the picture remains highly uneven across countries. Türkiye continues to stand out at 32.4%, far above the OECD average, while several economies are already seeing flat or negative food inflation. Divergence remains the story. #FoodInflation #OECD

6

May 14

Supply is tightening across virtually every major commodity. Production is pulling back from 2025/26 records while consumption keeps climbing, squeezing stocks and pushing prices higher.

Wheat — Most ConcerningU.S. production collapses 424 million bushels on drought-hit Hard Red Winter, sending the farm price up $1.50 to $6.50/bushel. Every major global exporter is cutting production. Russia holds its position as top exporter on strong carryover stocks, but global ending stocks are falling. Watch this space.

Corn — Tightest in Over a DecadeThe U.S. crop is down 6%, and global ending stocks would hit their lowest since 2013/14. Consumption is set to outpace production by 19.4 million tons. China's corn stockpile is quietly shrinking — a slow-burning risk worth monitoring.

Rice — First Production Drop Since 2015Global output falls for the first time in a decade, yet consumption hits a new record. India's massive reserves keep it firmly as the world's top exporter at ~40% of global trade, effectively acting as a global buffer.

Soybeans — The Bright SpotFarmers are shifting acres from corn and wheat into soybeans, lifting the U.S. crop to 4.435 billion bushels. Biofuel demand is a growing structural driver — soybean oil for biofuels jumps 3.6 billion pounds. Global production rises nearly 14 million tons.

The Bigger Risk Nobody's Pricing InThis WASDE assumes near-record Brazilian corn and soybean crops. But with the Strait of Hormuz closure driving up fertilizer costs, and IFPRI modeling potential Brazilian urea import declines of up to 27%, those projections may prove too optimistic. If Southern Hemisphere harvests disappoint this fall, already-thin grain stocks could turn from manageable to critical fast.

Source: USDA WASDE-671, May 12, 2026

14

May 14

The Strait of Hormuz closure is squeezing South American farmers at the worst possible time. Brazil sources 28% of its nitrogen fertilizer from the Persian Gulf, and Argentina about 9% — with disruptions already pushing input costs higher in a low crop-price environment.

If the closure lasts through end of 2026, Brazil's urea imports could fall by as much as 27.3%, according to recent analysis. Farmers may respond by cutting fertilizer application rates or shifting toward less input-intensive crops like soybeans — echoing what happened during the 2022 fertilizer price spike, when Brazil cut phosphate use by 12.4% and Argentina slashed potash use by 50% in 2023.

While global grain supplies remain relatively robust for now, a prolonged crisis — especially if compounded by a potential El Niño event in late 2026 — could turn today's input squeeze into a full-blown agricultural supply crisis, with ripple effects on food prices worldwide.

Source: Glauber, Piñeiro & Gianatiempo, IFPRI, 2026

11

May 14

USDA's latest grain outlook: Global corn & wheat production declining in 2026/27, but consumption keeps growing. Corn stocks down primarily in China 🇨🇳 & the US 🇺🇸. India 🇮🇳 set to account for ~40% of global rice exports — a new record!

Source: USDA Foreign Agricultural Service, Grain: World Markets and Trade, May 2026

11

May 14

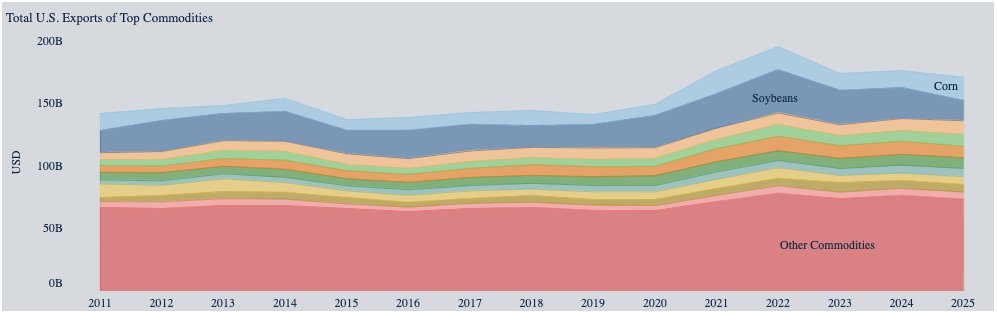

The USDA’s 2025 agricultural export report shows how concentrated U.S. ag trade still is.

Top export drivers:

• Corn

• Soybeans

• Dairy products

• Wheat

• Beef

• Poultry

• Tree nuts

Key numbers:

• $171.4B total U.S. agricultural exports in 2025

• Export growth: -2.9% YoY

• 5-year average exports still near $179B

Interesting takeaway:

Despite all the discussion around diversification, a relatively small number of commodity groups still dominate U.S. agricultural exports. Corn and soybeans alone continue to represent a massive share of global food/feed trade flows.

This also means:

Weather shocks matter more

Fertilizer and energy prices matter more

China demand still matters enormously

Trade policy shifts can ripple through global food markets very quickly

Another important detail is the growing role of value-added exports:

processed foods, bakery products, distillers grains, pet food, and meat products are becoming increasingly important alongside raw commodities.

Agriculture is no longer just “farm exports.”

It’s increasingly an integrated food, energy, logistics, and manufacturing story.

12

May 14

Food inflation is quietly heating up again.

FAO’s Food Price Index rose for the third straight month in April 2026, led by sharp increases in vegetable oils, meat, and cereals. Vegetable oil prices alone surged nearly 6% in a single month, reaching the highest level since July 2022.

What’s driving it?

• Higher energy prices

• Fertilizer cost pressures

• Drought risks in major agricultural regions

• Biofuel demand pulling edible oils into energy markets

• Supply tightness across Black Sea exports and livestock markets

• Logistics disruptions linked to the Strait of Hormuz and Red Sea routes

Some notable details from the report:

Wheat prices increased due to drought concerns in the U.S. and potential lower plantings in 2026.

Corn prices climbed on tighter supply and weather concerns in Brazil and the U.S.

Palm oil rose for the fifth consecutive month.

Meat prices hit a new record high.

Sugar was one of the few commodities moving lower thanks to stronger supply expectations from Brazil, China, and Thailand.

This matters beyond agriculture.

Food prices affect:

Global inflation expectations

Central bank policy

Emerging market stability

Consumer spending

Political and social stability in import-dependent countries

One of the biggest underappreciated themes right now is the connection between energy and food.

When oil prices rise:

→ fertilizer costs increase

→ transportation costs rise

→ biofuel demand strengthens

→ agricultural input costs surge

And eventually, food inflation follows.

Markets often focus on CPI after it happens.

Commodity markets usually signal it earlier.

fao.org/worldfoodsituation/f…

4

Apr 30

One of the less discussed impacts of the current energy shock is what’s happening in agriculture.

Fertilizer prices are expected to rise ~31% in 2026, with urea up nearly 60% due to natural gas constraints. At the same time, food prices are projected to increase only around 2%, thanks to relatively strong grain supply.

But that’s not the full picture. Oils like palm and soybean are expected to rise ~8%, partly due to biofuel dynamics linking energy and agriculture markets again.

The key issue: input costs are rising much faster than output prices. That puts pressure on farmers’ margins and creates potential yield risks going forward.

Source: World Bank Commodity Outlook

openknowledge.worldbank.org/…

18