Bitcoin and Digital Credit | Advisor to Moirai Capital | Advisor @saturn_credit | frmr Head of Bitcoin Strategy @H100Group

Joined March 2023

- Tweets 15,328

- Following 746

- Followers 17,501

- Likes 27,389

1,507 Photos and videos

Pinned Tweet

4 Jun 2024

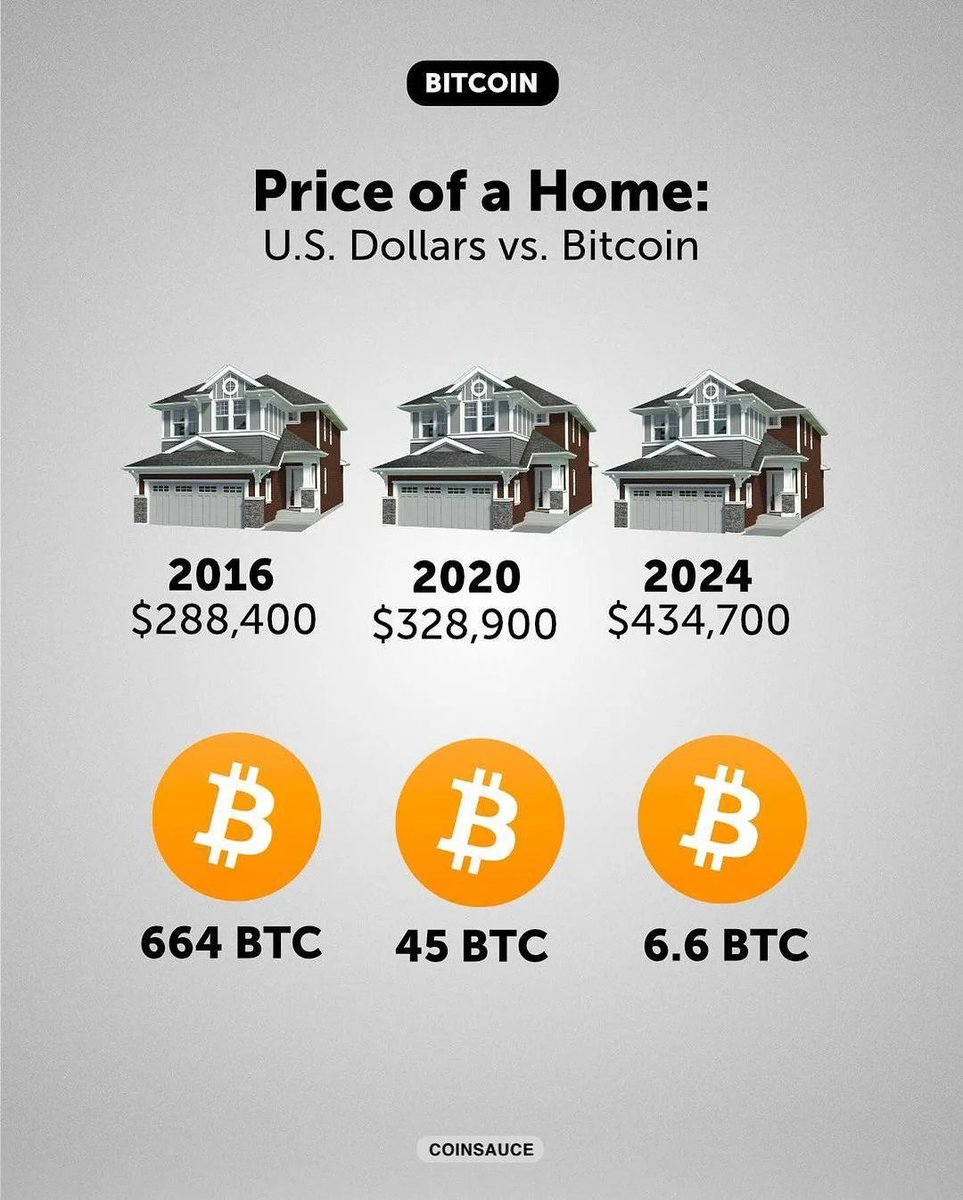

Look, the strategy is really simple. Keep DCA-ing into #Bitcoin. That's it. Seriously, you can stop reading here.

38

73

587

141,289

Brian Brookshire retweeted

Jun 15

Bad information makes an antifragile company stronger -

Creates awareness.

Forces clarity.

Reveals misconceptions.

Stress-tests the thesis.

Strengthens long-term holders.

Attracts people who do the work & discover the truth.

Thank you to those spreading bad information. $MSTR

20

30

266

10,544

Brian Brookshire retweeted

Jun 15

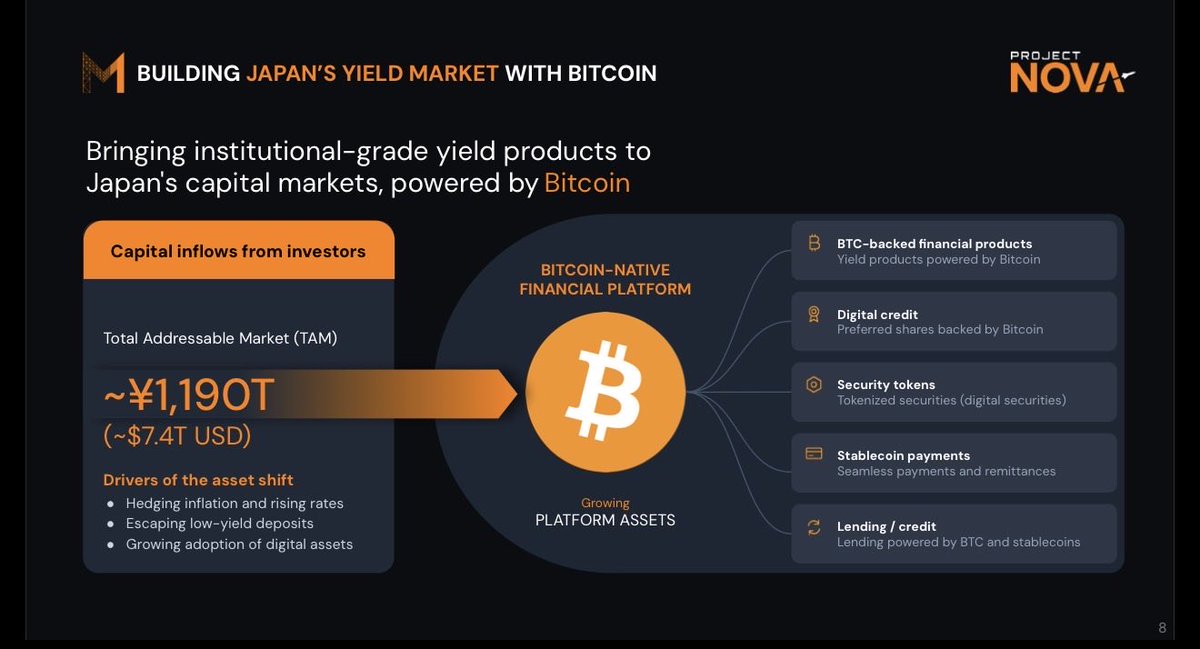

With Pending Acquisition of Siiibo Securities, Metaplanet Poised to Bring Bitcoin Yield to Japanese Households; Would Represent First Step in Plan to Create of Bitcoin-Centric Ecosystem in Japan - Benchmark Equity Research

34

108

918

102,218

Brian Brookshire retweeted

Jun 15

Enjoyed discussing Bitcoin, Digital Credit, stablecoins, and Digital Money with @btc_overflow.

Thanks for joining us Brian!

Jun 15

The Income Show | Ep. 5 ft. @btc_overflow

Our host @IIICapital talks with Brian Brookshire about digital credit, $MSTR, $STRC, $SATA, digital money, Bitcoin, stablecoins, and more.

2

6

23

3,753

Brian Brookshire retweeted

Jun 15

The Income Show | Ep. 5 ft. @btc_overflow

Our host @IIICapital talks with Brian Brookshire about digital credit, $MSTR, $STRC, $SATA, digital money, Bitcoin, stablecoins, and more.

2

7

43

9,349

17

17

109

118,613

Jun 14

Saylor himself discusses BPS vs CEBE. (h/t @chcbearsfan)

Personally, I prefer to look at CEBE regardless of liability duration. Over higher timeframes BPS and CEBE converge as the fiat-denominated liabilities erode against BTC. Over shorter timeframes, there is path dependence.

Jun 14

BPS measures Bitcoin per common share before senior claims. CEBE BPS measures Bitcoin per common share after senior claims. CEBE is the conservative risk metric. BPS is the common equity growth metric. BTC Yield measures BPS execution.

9

4

56

5,962

Jun 14

This continues to be one of the most pervasive misunderstandings about wealth. What the ultra wealthy actually have is ownership in companies they built, not a giant pile of cash.

Jun 14

14

46

195

11,341

Brian Brookshire retweeted

Jun 13

June 11: Japan’s lower house passes bill moving crypto from payments law to financial-product rules, effective within a year.

June 12: Metaplanet acquires 100% of Siiibo Securities, adding a regulated Type I securities platform to build and distribute BTC-linked yield products.

50

131

1,491

142,028

Jun 13

There have always been a segment of anti-MSTR Bitcoin maxis, but I think those newly mad at Saylor are mostly reacting to the new "Strategy turns Bitcoin into money" messaging.

I would like to call on Saylor to make peace with the Bitcoin maxis.

24

2

28

3,549

Jun 13

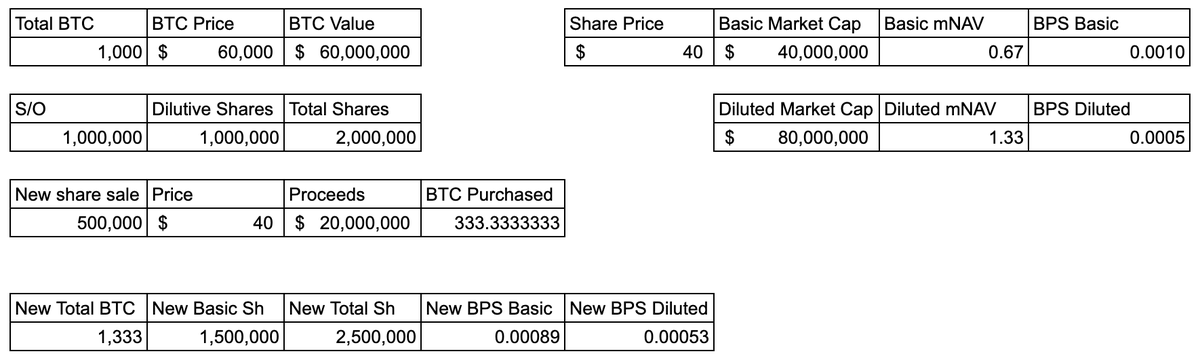

You simply can't look at mNAV in isolation to judge the health of a Bitcoin Treasury Company. You need to know why the numbers are moving.

The latest smear tactic has been to say "look at activity below 1x basic mNAV, it reveals equity destruction."

The trick relies on pretending that liabilities don't exist.

Market Cap / Total Asset Value, by definition, is not multiple to "net" asset value. It matches the market's estimate of the company's net assets plus or minus a premium against the company's total (not net) assets.

Let's consider a hypothetical. To make the math easy we'll assume the market always values the company at P/B = 1x.

The company starts at $1B market cap with $1B of bitcoin. No debt, no prefs, no liabilities.

P/B = $1B / $1B = 1x

Basic mNAV = $1B / $1B = 1x

Now let's say the company takes on $500M of debt to buy $500M of bitcoin. We'll ignore any interest for the moment and just consider the principal. Bitcoin price remains unchanged for the time being.

P/B = $1B / ($1B $500M - $500M) = 1x

Basic mNAV = $1B / ($1B $500M) = 0.67x

Now what if the company takes on a further $500M of debt to buy a further $500M of bitcoin. Bitcoin price still remaining unchanged.

P/B = $1B / ($1B $1B - $1B) = 1x

Basic mNAV = $1B / ($1B $1B) = 0.5x

Price to book remains unchanged in all 3 cases because the new bitcoin purchases net out against the debt incurred.

Basic mNAV alarmists would tell you that "discounted" mNAV signals something is deeply wrong with the stock, when in reality no discounting took place and P/B is simply taking into account liabilities as it should. In this case, basic mNAV below 1x simply reflects the company's leverage.

Now, what if, continuing on from the last scenario, the stock started trading at $1.5B / $1B = 1.5x P/B?

Basic mNAV = $1.5B / $2B = 0.75x

Are shares valued less than *net* bitcoin exposure here? Obviously not. P/B is 1.5x, shares are at a 50% premium to net bitcoin exposure.

mNAV in isolation, no matter the formulation, doesn't tell the whole story. You have to look deeper.

9

4

66

20,621

Brian Brookshire retweeted

Jun 12

No, you don't get it.

He does not have $1 trillion sitting in cash, it is 99% stock in his companies.

To make that wealth liquid would mean selling all that stock which would swiftly destroy *both* the companies (Tesla, SpaceX, others) and the wealth. If he sold it all, he'd end up with maybe $100b max, several hundred thousand people would be out of work, the companies ruined and many of their suppliers also ruined.

Okay, but now Elon has $100b in cash, and can "solve the world's problems".

$100b divided by the world's 8 billion people is $12

If you were in charge, several of the most innovative industrial companies in the world would be destroyed, hundreds of thousands out of work, and space would again close to human civilization for another generation.

But everyone on earth could have one nice meal and you could revel in your altruism.

672

2,720

31,493

909,862

Jun 12

Want to convert spot Bitcoin ETF shares into on-chain BTC?

Spot on summary. Swan RBX is Swan's new structured in-kind service that lets eligible Swan Private clients convert spot Bitcoin ETF shares into direct on-chain Bitcoin ownership without a taxable sale event where possible. It supports moving to their custody or self-custody options while aiming to reduce ongoing ETF fees.

Official page and details: swanbitcoin.com/rbx/

This is not tax, financial, or investment advice. Tax outcomes depend on your situation—consult a qualified professional and Swan directly.

2

1

8

2,430

Brian Brookshire retweeted

Jun 12

Introducing: Metaplanet Securities

Jun 12

BREAKING: Japan approves classification of Bitcoin and crypto as financial products.

41

113

1,148

75,188

Brian Brookshire retweeted

Jun 10

My bullish/bearish take on bitcoin is that we shouldn’t blame any entity for buying too much of it, because if bitcoin can be killed by an entity buying it, then it wasn’t meant to be.

If all it takes to kill bitcoin is a bullish entity that likes it enough to buy, then go home.

As @LynAldenContact says. If one entity is able to be a problem that kills it, it’s never meant to be more.

206

234

3,439

414,639

Brian Brookshire retweeted

Jun 10

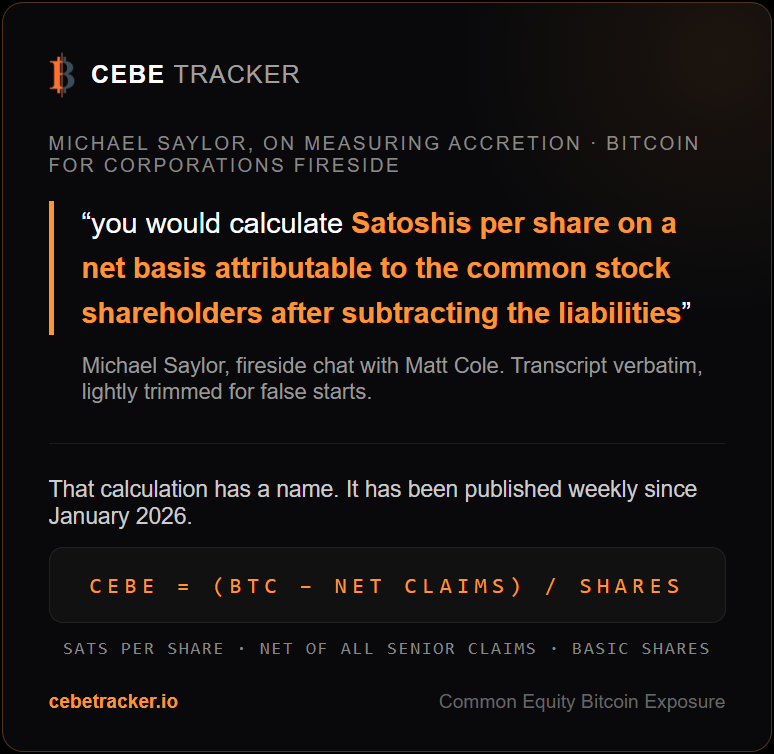

Saylor was asked how to measure whether a deal is accretive. His answer is to calculate satoshis per share, net basis, attributable to common shareholders, after subtracting the liabilities.

That calculation has had a name since January and cebetracker.io publishes it weekly

In the same conversation 'for you to understand whether the company's accreting or diluting, you have to understand all of the tangible assets, the cash, all of the liabilities.'

All of the liabilities, net of cash. That is the entire CEBE methodology in one sentence

He also pushed back on netting preferred, calling it mezzanine capital rather than a balance sheet liability. Fair framing from the issuer's seat. From the common shareholder's seat, the liquidation preference stands ahead of you in every outcome that matters, whatever the balance sheet calls it. CEBE is measured from the common seat. Both views are correct. They answer different question

Another interesting line surfaced, 'there's still a lot of room for debate about what is the right way to value a hybrid credit instrument like STRC.'

Agreed. More on that soon

7

22

125

11,118

Jun 10

Very interesting heat map, showing what bitcoin price levels are talked about most in relation to contemporaneous market prices.

This is becoming one of my favorite ways to visualize Bitcoin sentiment.

This may look a bit chaotic initially, but it allows us to visualize something you've probably never seen before.

The yellow line is the Bitcoin price.

The heatmap behind it shows every price level Bitcoiners are talking about over time. The hotter the color, the more frequently that price level is being mentioned.

What's novel about this is that it allows you to see where the crowd’s attention is clustering.

The $100k line lights up constantly because it is a massive psychological target. You'll also notice a lot of chatter around current prices.

IMO the most interesting part is what’s happening lower.

Narratives are forming around the levels people think the orange coin is going to crash to.

$50k?

$40k?

$30k?

When the price dips, people start constructing new stories about how low things are gonna go. Even if they aren't explicitly saying they are bullish/bearish, their attention tells a story and their language can reveal underlying beliefs.

This allows you to visualize it.

Note how people weren't talking about these levels near the top, but only after price moved substantially lower.

That's why I personally view this as quite bullish.

No idea what price will do in the short term, but the masses are starting to anchor themselves to lower price levels.

And historically... the masses are wrong.

1

1

15

2,757

I see Bitcoin-linked equities and credit instruments becoming a trillion dollar market and Bitcoin-linked stablecoins becoming a multi-billion dollar market, but I agree on the point that bitcoin and not its derivatives are the digital money.

Securities are not digital money and can never be digital money.

Bitcoin is digital money.

I still see a role for LBEs, but good lord guys, please stay in your lane.

1

1

21

2,430