Bitfinex is the leading digital asset trading platform offering deep liquidity, advanced tools, and zero trading fees.

Joined October 2012

- Tweets 11,288

- Following 62

- Followers 926,408

- Likes 1,824

5,619 Photos and videos

Bitfinex retweeted

Jun 11

Can Fable 5 trade vol?

Someone had to find out, so we handed it a BTC 7d IV/RV series and a full export of the 19JUN26 Thalex options chain.

It was eager to summarize the data but stopped making eye contact when asked, "what's the trade?"

Ultimately, we got it to open up, reminding it that risk management is the most important of all safeguards.

Below are its market thoughts and top three positional option trade ideas.

---

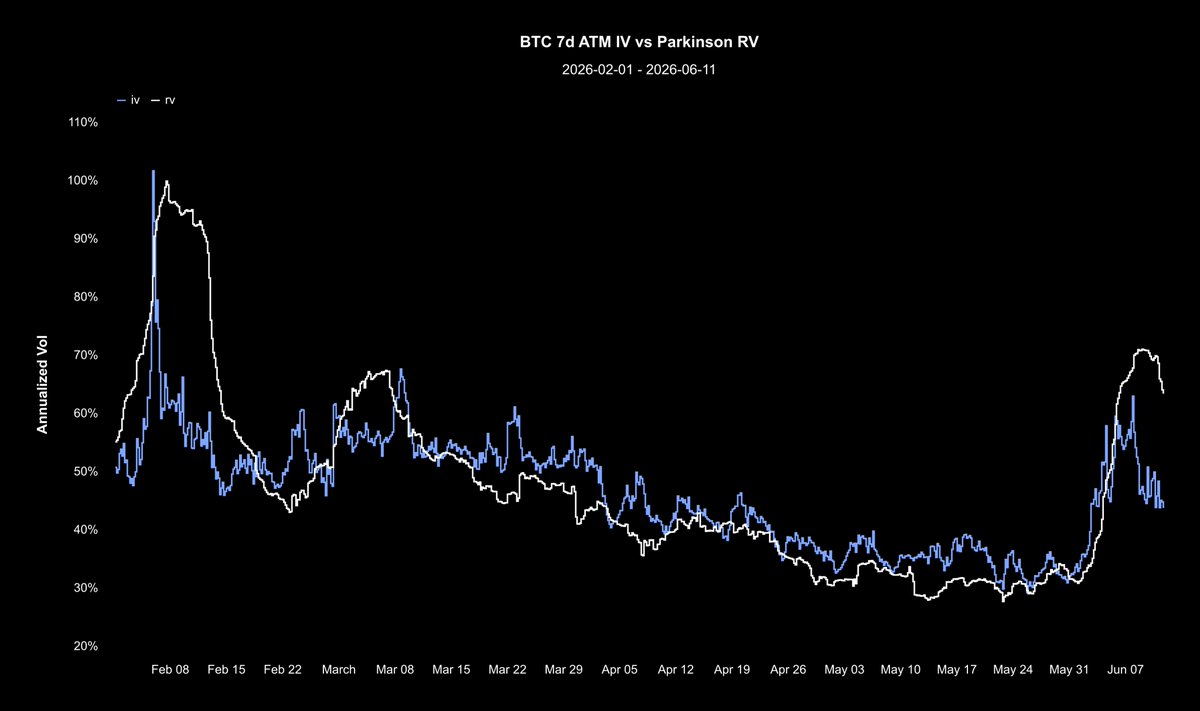

𝗩𝗼𝗹 𝗶𝘀 𝗺𝗮𝗿𝗸𝗲𝗱 𝟮𝟬 𝗽𝗼𝗶𝗻𝘁𝘀 𝘂𝗻𝗱𝗲𝗿 𝘄𝗵𝗮𝘁 𝗶𝘁 𝗷𝘂𝘀𝘁 𝗿𝗲𝗮𝗹𝗶𝘇𝗲𝗱.

• BTC 7d ATM IV closes Jun 11 near 44% against trailing 7d Parkinson RV near 64%, off a ~70% peak: the widest implied-under-realized gap of the Feb–Jun window.

• Part of the gap is a Parkinson lookback artifact: the realized series still carries the spike days and decays on its own as they roll off, no new move required.

• Strip that before sizing a long-vol bet. The true premium is narrower than the headline, and the gap is an edge only if movement persists.

𝗧𝗵𝗲 𝟲𝟰𝗸 𝗹𝗶𝗻𝗲 𝗶𝘀 𝘁𝗵𝗲 𝗰𝗲𝗻𝘁𝗲𝗿 𝗼𝗳 𝘁𝗵𝗲 𝗯𝗼𝗮𝗿𝗱, 𝗮𝗻𝗱 𝘁𝗵𝗲 𝘀𝘁𝗿𝗮𝗱𝗱𝗹𝗲 𝘁𝗵𝗲𝗿𝗲 𝗶𝘀 𝗮 𝗿𝗲𝗮𝗹𝗶𝘇𝗲𝗱-𝗽𝗲𝗿𝘀𝗶𝘀𝘁𝗲𝗻𝗰𝗲 𝗯𝗲𝘁.

• ATM marks 41 to 42% at the 63k and 64k strikes, forward near $63.6k from the deltas (64k call 0.46, put −0.54).

• The 64k straddle (~$3,023) is the cleanest ATM vehicle and needs more than ~2.1% daily realized to beat decay. Recent tape cleared that bar; the April to May tape did not.

• It is a bet on movement persisting, not on direction.

𝗣𝘂𝘁𝘀 𝗮𝗿𝗲 𝗲𝘅𝗽𝗲𝗻𝘀𝗶𝘃𝗲, 𝗰𝗮𝗹𝗹𝘀 𝗮𝗿𝗲 𝗻𝗼𝘁: 𝘀𝗲𝗹𝗹 𝘁𝗵𝗲 𝗿𝗶𝗰𝗵 𝘄𝗶𝗻𝗴, 𝗯𝘂𝘆 𝘁𝗵𝗲 𝗰𝗵𝗲𝗮𝗽 𝗼𝗻𝗲.

• The put wing climbs from 45% at 61k to 47% at 60k and 51% at 58k, while the call wing sits flat at 41 to 43% out to 70k: ~4 points of 25-delta put skew.

• The put wing is the richest premium to short, but the dollar credits are thin. Harvest the skew differential, not raw theta, and pair it against the call wing so the downside is never naked.

• The 67k call at ~41% sits at the floor of the surface and is the best upside-asymmetry leg. With the 72k marked at 45% to sell against it, a defined-risk vertical is the efficient way to own a breakout.

𝗘𝘃𝗲𝗿𝘆𝘁𝗵𝗶𝗻𝗴 𝗿𝗲𝗱𝘂𝗰𝗲𝘀 𝘁𝗼 𝗼𝗻𝗲 𝗾𝘂𝗲𝘀𝘁𝗶𝗼𝗻: 𝗱𝗼 𝘁𝗵𝗲 𝗻𝗲𝘅𝘁 𝗲𝗶𝗴𝗵𝘁 𝗱𝗮𝘆𝘀 𝗿𝗲𝗮𝗹𝗶𝘇𝗲 𝗻𝗲𝗮𝗿𝗲𝗿 𝟰𝟬 𝗼𝗿 𝗻𝗲𝗮𝗿𝗲𝗿 𝟲𝟬?

• February's precedent favors the seller. Realized fell from ~100% to the 40s in under two weeks, and the snap-back in this regime is fast.

• Pick that side first; every strike and structure follows from the answer.

---

𝗟𝗼𝗻𝗴 𝟭𝘅 𝗕𝗧𝗖-𝟭𝟵𝗝𝗨𝗡𝟮𝟲-𝟲𝟰𝟬𝟬𝟬-𝗖, 𝗟𝗼𝗻𝗴 𝟭𝘅 𝗕𝗧𝗖-𝟭𝟵𝗝𝗨𝗡𝟮𝟲-𝟲𝟰𝟬𝟬𝟬-𝗣

• 𝗖𝗼𝗻𝘀𝘁𝗿𝘂𝗰𝘁𝗶𝗼𝗻: Long 64,000 call (~$1,270, 41% IV) and put (~$1,752, 41% IV), net debit ~$3,023. Net Δ −0.08. Defined risk, long convexity.

• 𝗧𝗵𝗲𝘀𝗶𝘀: Long the IV–RV gap. The front end is priced ~20 vol points under last week's realized, the steepest discount since February, and the straddle owns that gap with no directional view. Long gamma and vega, betting June's regime persists over reversion to the April to May 30s; danger zone is a pin at 64,000 into expiry.

• 𝗘𝗻𝘁𝗿𝘆 𝗰𝗼𝘀𝘁: ~$3,023 net debit (~4.8% of forward).

• 𝗠𝗮𝘅𝗶𝗺𝘂𝗺 𝗽𝗿𝗼𝗳𝗶𝘁: Unbounded past either breakeven; delta-hedged, accrues whenever realized clears ~41%.

• 𝗠𝗮𝘅𝗶𝗺𝘂𝗺 𝗿𝗶𝘀𝗸: Full debit on a 64,000 expiry print.

• 𝗕𝗿𝗲𝗮𝗸𝗲𝘃𝗲𝗻 𝗮𝘁 𝗲𝘅𝗽𝗶𝗿𝗮𝘁𝗶𝗼𝗻: 60,977 and 67,023.

• 𝗧𝗶𝗺𝗲 𝗮𝗻𝗱 𝘃𝗼𝗹𝗮𝘁𝗶𝗹𝗶𝘁𝘆 𝗶𝗺𝗽𝗮𝗰𝘁: Short Θ, heaviest at the strike. Long ν re-rates the book before spot moves; long Γ at 64,000. A crush to the 30s is the adverse path.

• 𝗣𝗼𝘀𝗶𝘁𝗶𝗼𝗻 𝗺𝗮𝗻𝗮𝗴𝗲𝗺𝗲𝗻𝘁: Bank a fast break through either breakeven or an IV re-rate to the high-40s or 50s; if hedging, take gamma daily. Sub-1.5% days with IV sliding toward the 30s kill it: cut to a strangle or close half.

---

𝗦𝗵𝗼𝗿𝘁 𝟭𝘅 𝗕𝗧𝗖-𝟭𝟵𝗝𝗨𝗡𝟮𝟲-𝟲𝟭𝟬𝟬𝟬-𝗣, 𝗟𝗼𝗻𝗴 𝟭𝘅 𝗕𝗧𝗖-𝟭𝟵𝗝𝗨𝗡𝟮𝟲-𝟲𝟳𝟬𝟬𝟬-𝗖

• 𝗖𝗼𝗻𝘀𝘁𝗿𝘂𝗰𝘁𝗶𝗼𝗻: Short 61,000 put (~$635, 45% IV), long 67,000 call (~$380, 41% IV), net credit ~$255. Net Δ 0.44. Short downside, long upside, flat between.

• 𝗧𝗵𝗲𝘀𝗶𝘀: Sell the skew. The book pays ~4 vol points more for downside than upside, and the cheapest call on the surface funds the position that collects it. Wins on up or flat spot as the put decays, pays in three of four spot paths, and bets downside fear overstates the odds of a break lower.

• 𝗘𝗻𝘁𝗿𝘆 𝗰𝗼𝘀𝘁: ~$255 net credit.

• 𝗠𝗮𝘅𝗶𝗺𝘂𝗺 𝗽𝗿𝗼𝗳𝗶𝘁: Unbounded above 67,000; flat ~$255 between strikes.

• 𝗠𝗮𝘅𝗶𝗺𝘂𝗺 𝗿𝗶𝘀𝗸: Undefined; synthetically long spot from ~60,745, point-for-point below.

• 𝗕𝗿𝗲𝗮𝗸𝗲𝘃𝗲𝗻 𝗮𝘁 𝗲𝘅𝗽𝗶𝗿𝗮𝘁𝗶𝗼𝗻: 60,745.

• 𝗧𝗶𝗺𝗲 𝗮𝗻𝗱 𝘃𝗼𝗹𝗮𝘁𝗶𝗹𝗶𝘁𝘆 𝗶𝗺𝗽𝗮𝗰𝘁: Modestly long Θ. Short ν in the put wing, where a downside vol spike compounds the delta loss. Skew flattening is the clean win.

• 𝗣𝗼𝘀𝗶𝘁𝗶𝗼𝗻 𝗺𝗮𝗻𝗮𝗴𝗲𝗺𝗲𝗻𝘁: Buy back the decayed put or close on skew flattening; above 67,000, take profit or roll the call up. A break below 61,000 with rising IV invalidates it: roll the put down-and-out before the strike breaks, not after.

---

𝗟𝗼𝗻𝗴 𝟭𝘅 𝗕𝗧𝗖-𝟭𝟵𝗝𝗨𝗡𝟮𝟲-𝟲𝟳𝟬𝟬𝟬-𝗖, 𝗦𝗵𝗼𝗿𝘁 𝟭𝘅 𝗕𝗧𝗖-𝟭𝟵𝗝𝗨𝗡𝟮𝟲-𝟳𝟮𝟬𝟬𝟬-𝗖

• 𝗖𝗼𝗻𝘀𝘁𝗿𝘂𝗰𝘁𝗶𝗼𝗻: Long 67,000 call (~$380, 41% IV), short 72,000 call (~$43, 45% IV), net debit ~$338. Defined-risk vertical, net Δ long.

• 𝗧𝗵𝗲𝘀𝗶𝘀: Buy the cheap wing. The flattest vol on the surface sits in the calls, and the vertical turns it into ~14:1 convex upside without touching elevated put-side vol. The short 72,000 leg sells the only lifted call point to subsidize entry; bets the expansion resolves higher.

• 𝗘𝗻𝘁𝗿𝘆 𝗰𝗼𝘀𝘁: ~$338 net debit.

• 𝗠𝗮𝘅𝗶𝗺𝘂𝗺 𝗽𝗿𝗼𝗳𝗶𝘁: ~$4,662 at or above 72,000 (5,000 width less debit).

• 𝗠𝗮𝘅𝗶𝗺𝘂𝗺 𝗿𝗶𝘀𝗸: Full debit below 67,000 at expiry.

• 𝗕𝗿𝗲𝗮𝗸𝗲𝘃𝗲𝗻 𝗮𝘁 𝗲𝘅𝗽𝗶𝗿𝗮𝘁𝗶𝗼𝗻: 67,338 (~ 5.9% from forward).

• 𝗧𝗶𝗺𝗲 𝗮𝗻𝗱 𝘃𝗼𝗹𝗮𝘁𝗶𝗹𝗶𝘁𝘆 𝗶𝗺𝗽𝗮𝗰𝘁: Short Θ, lighter than an outright call. Net long ν at 67,000, convexity capped at 72,000. Skew favorable: cheapest wing bought, richest call sold.

• 𝗣𝗼𝘀𝗶𝘁𝗶𝗼𝗻 𝗺𝗮𝗻𝗮𝗴𝗲𝗺𝗲𝗻𝘁: Monetize as spot nears 72,000 or the spread reaches most of max value. A stall below 67,000 into expiry is the failure path: the debit is the stop; do not average a fade.

2

5

43

4,380

Quantum computing is a real issue. It is also overstated for Bitcoin specifically.

@paoloardoino on @CRYPTO101Pod explains why the broader internet is the more immediate concern.

4

4

44

4,928

Bitfinex retweeted

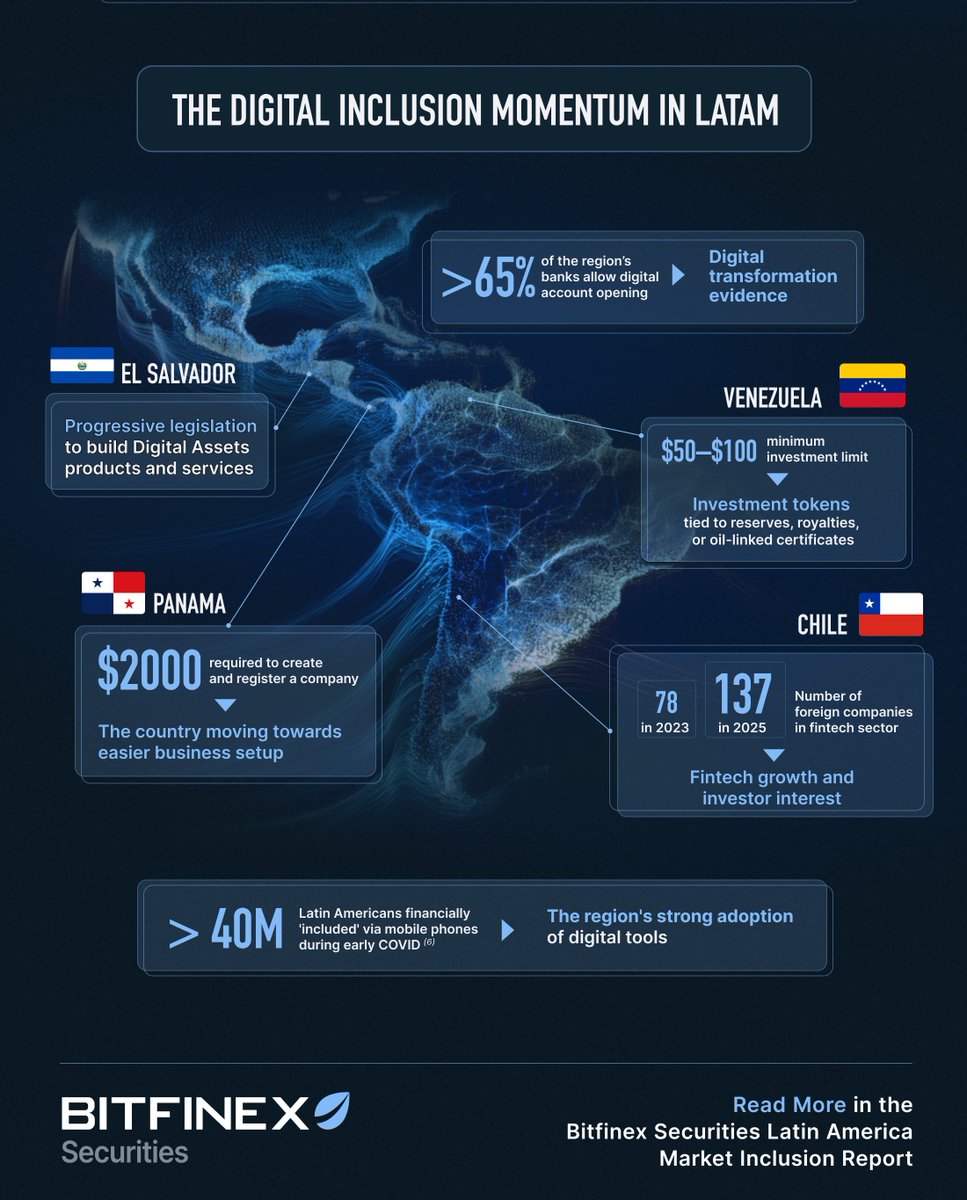

Latin America’s financial inclusion gap remains significant, with limited access to credit, shallow capital markets, and low financial education restricting growth across the region.

But momentum is building.

1

1

19

1,618

A critical flaw in Zcash's shielded pool survived years of expert scrutiny. An AI-assisted researcher found it in days.

How many similar vulnerabilities still remain hidden across crypto?

blog.bitfinex.com/industry-n…

1

1

12

1,510

What is your monthly trading volume costing you in fees?

Run the numbers: bitfinex.com/zero-fee-tradin…

1

16

1,622

$BTC fell from above $82,000 to $59,200, one of the sharpest corrections of the year.

Parabolic SAR is one of the tools traders use to identify when a trend may be reversing. 👇

blog.bitfinex.com/education/…

2

24

1,893

Bitfinex retweeted

The shock arrest of Nicolás Maduro marked a turning point for Venezuela. Political uncertainty gave way to an emerging opportunity: a long-constrained economy beginning to open up.

Tokenisation may be the fastest route to connecting Venezuelan assets with global capital. 🧵

1

9

20

2,986

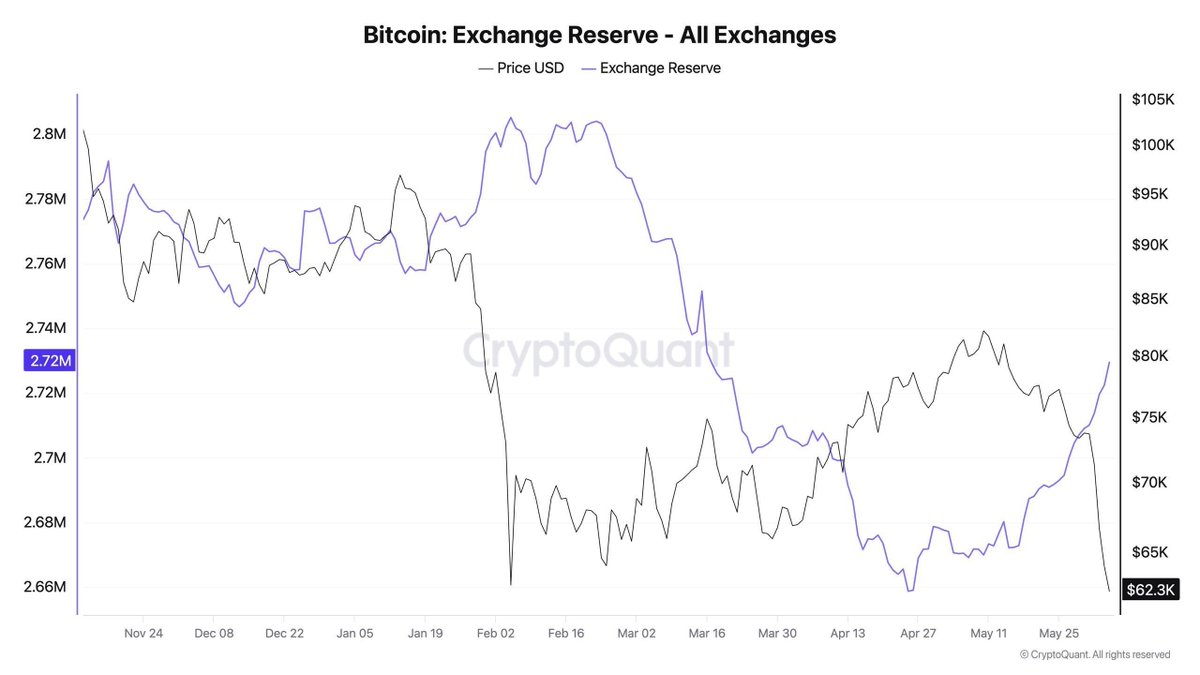

No accumulation signal on $BTC yet.

Price is near the lows but exchange reserves are still elevated at 2.71m.

At the Feb bottom, coins were leaving exchanges. Now they are not.

Seller exhaustion without accumulation to follow leaves another leg down on the table.

2

2

35

2,351

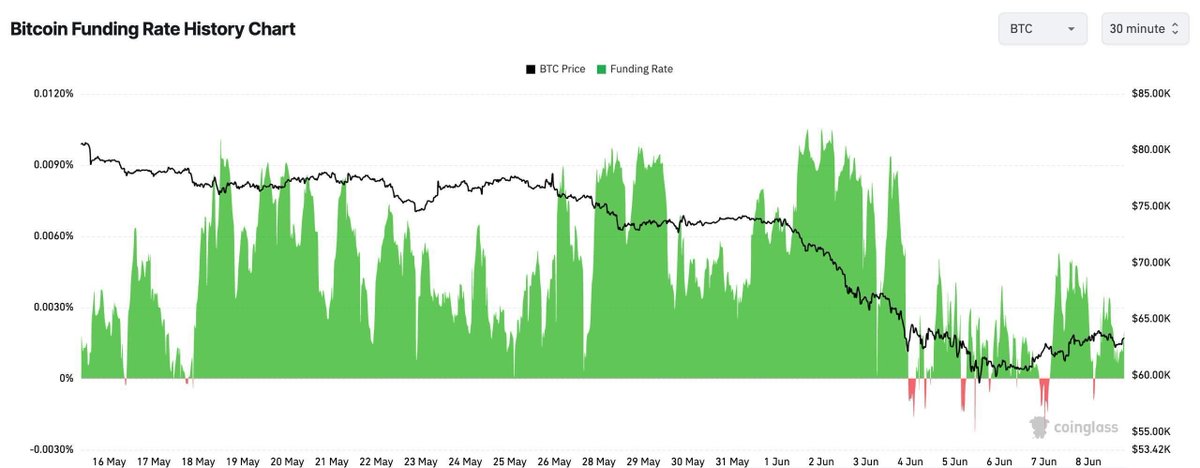

The perp positioning that compounded $BTC’s decline from $72k to $59k has reset.

Funding stayed positive with longs adding into the slow bleed. On 4 June it flipped negative as leveraged OI was likely flushed.

One of the conditions for a bottom is now in place.

7

14

91

8,088

▫️$BTC printed its first sub-$60k level since 2024

▫️$5.9bn in futures liquidated

▫️$4.3bn drained from ETFs

The long positions that drove the cascade have been cleared, and Strategy has re-entered with 1,550 BTC.

We look at what comes next ⤵️

go.bitfinex.com/theairgapclo…

2

24

1,977

$BTC is in distribution, not acquisition. Spot CVD negative, short-term holders underwater, ETF outflows at $4.2bn over three weeks. We told @TheBlockCo why: yields are rising for the wrong reason.

theblock.co/amp/post/404082/…

1

1

25

2,607

“Rallies are increasingly being sold rather than accumulated, signalling that the market remains in a structurally defensive phase until spot demand meaningfully returns,” Bitfinex Alpha describes how fragile $BTC markets have become to @wsj

wsj.com/business/tech-media-…

1

2

17

2,019

What does the payment infrastructure for an AI agent economy actually look like?

@paoloardoino went deep on @CRYPTO101Pod. He explains how Bitcoin and Lightning payments hold the key.

2

1

26

5,550

Full episode via Crypto 101 Podcast. 🎙️ youtu.be/RPjCia3XrYs

1

4

6,908