Bridget™ by @BridgeWiseAI is an AI chat for investments, providing regulatory-compliant insights & recommendations on 50K global securities.

Joined September 2025

- Tweets 427

- Following 67

- Followers 48

- Likes 44

173 Photos and videos

Pinned Tweet

30 Oct 2025

Hello X👋

Welcome to the official account for Bridget™ by @BridgeWiseAI.

Bridget™ is the first compliant conversational AI tool tailored for the investment industry. It provides insights and recommendations on more than 50,000 global securities, with reliable, multilingual responses that institutions can trust.

On this account, we’ll share selected 📊 market perspectives, 💡 investment insights, and 🔎 in-depth analysis powered by Bridget™, making expert-level knowledge accessible to everyone.

This space is for 🏦 bank advisors, 💻 trading platforms, 📈 financial professionals, and investment enthusiasts who want to see how AI is transforming investment intelligence.

Follow along and join the conversation. ✨

#AIFinance #Fintech #FinancialMarkets #InvestorEducation #FinanceTwitter

1

445

Jun 12

💬: What are the key factors behind Vanguard overtaking BlackRock as the largest ETF issuer in the U.S., and is this likely to be a lasting shift?

#BridgetPerspective 👇

🤖: Vanguard overtook BlackRock as the largest ETF issuer in the U.S. thanks to several clear drivers. Vanguard’s relentless focus on low-cost, core index products and a deliberately narrow product lineup has resonated with long-term investors, fueling massive inflows. In 2026 alone, Vanguard attracted approximately 291 billion USD in ETF inflows—more than double BlackRock’s nearly 120 billion USD—helping it reach 4.39 trillion USD in U.S.-listed ETF assets, just ahead of BlackRock’s 4.36 trillion USD. This shift follows years of Vanguard steadily closing the gap, with its ETF assets rising from about 52% of BlackRock’s in 2018 to nearly 97% by late 2024. Milestones like Vanguard S&P 500 ETF (VOO) surpassing 1 trillion USD in assets, outpacing BlackRock’s iShares Core S&P 500 ETF (IVV), highlight this momentum.

The competitive dynamic is shaped by Vanguard’s streamlined, investor-friendly approach versus BlackRock’s broader, more innovative lineup. Vanguard’s strategy—minimizing costs and focusing on simple, scalable index funds—has been a magnet for fee-sensitive, buy-and-hold investors. Meanwhile, BlackRock continues to push product innovation and global reach, as seen with its expansion into crypto ETFs and specialty offerings, but its more diverse and higher-fee product mix hasn’t matched Vanguard’s inflow growth in the current environment.

Whether this leadership change is permanent depends on market trends and investor preferences. Vanguard’s edge in cost efficiency and brand trust gives it staying power, especially as investors gravitate toward simplicity and low fees. However, BlackRock’s scale, global presence, and ability to innovate across asset classes mean the rivalry is far from over. The baton may have passed for now, but the competition at the top of the ETF world remains fierce and dynamic.

#AIFinance #Fintech #FinancialMarkets #InvestorEducation #FinanceTwitter #AI

---

*𝘉𝘳𝘪𝘥𝘨𝘦𝘵™ 𝘣𝘺 @𝘉𝘳𝘪𝘥𝘨𝘦𝘞𝘪𝘴𝘦𝘈𝘐 𝘪𝘴 𝘢𝘯 𝘈𝘐 𝘤𝘩𝘢𝘵 𝘧𝘰𝘳 𝘪𝘯𝘷𝘦𝘴𝘵𝘮𝘦𝘯𝘵𝘴, 𝘱𝘳𝘰𝘷𝘪𝘥𝘪𝘯𝘨 𝘳𝘦𝘨𝘶𝘭𝘢𝘵𝘰𝘳𝘺-𝘤𝘰𝘮𝘱𝘭𝘪𝘢𝘯𝘵 𝘪𝘯𝘴𝘪𝘨𝘩𝘵𝘴 & 𝘳𝘦𝘤𝘰𝘮𝘮𝘦𝘯𝘥𝘢𝘵𝘪𝘰𝘯𝘴 𝘰𝘯 50𝘒 𝘨𝘭𝘰𝘣𝘢𝘭 𝘴𝘦𝘤𝘶𝘳𝘪𝘵𝘪𝘦𝘴.

**𝘛𝘩𝘦 𝘪𝘯𝘧𝘰𝘳𝘮𝘢𝘵𝘪𝘰𝘯 𝘪𝘯𝘤𝘭𝘶𝘥𝘦𝘥 𝘪𝘯 𝘵𝘩𝘦 𝘢𝘯𝘢𝘭𝘺𝘴𝘪𝘴 𝘪𝘴 𝘪𝘯𝘵𝘦𝘯𝘥𝘦𝘥 𝘧𝘰𝘳 𝘨𝘦𝘯𝘦𝘳𝘢𝘭 𝘨𝘶𝘪𝘥𝘢𝘯𝘤𝘦 𝘱𝘶𝘳𝘱𝘰𝘴𝘦𝘴 𝘰𝘯𝘭𝘺. 𝘜𝘯𝘥𝘦𝘳 𝘯𝘰 𝘤𝘪𝘳𝘤𝘶𝘮𝘴𝘵𝘢𝘯𝘤𝘦𝘴 𝘪𝘴 𝘵𝘩𝘦 𝘪𝘯𝘧𝘰𝘳𝘮𝘢𝘵𝘪𝘰𝘯 𝘢𝘥𝘫𝘶𝘴𝘵𝘦𝘥 𝘵𝘰 𝘢 𝘴𝘱𝘦𝘤𝘪𝘧𝘪𝘤 𝘧𝘢𝘤𝘵𝘰𝘳 𝘰𝘳 𝘷𝘢𝘳𝘪𝘢𝘣𝘭𝘦 𝘳𝘦𝘭𝘢𝘵𝘦𝘥 𝘵𝘰 𝘵𝘩𝘦 𝘪𝘥𝘦𝘯𝘵𝘪𝘵𝘺 𝘰𝘧 𝘵𝘩𝘦 𝘳𝘦𝘱𝘰𝘳𝘵 𝘳𝘦𝘢𝘥𝘦𝘳. 𝘛𝘩𝘦 𝘪𝘯𝘧𝘰𝘳𝘮𝘢𝘵𝘪𝘰𝘯 𝘪𝘴 𝘯𝘰𝘵 𝘢 𝘴𝘶𝘣𝘴𝘵𝘪𝘵𝘶𝘵𝘦 𝘧𝘰𝘳 𝘴𝘱𝘦𝘤𝘪𝘧𝘪𝘤 𝘢𝘥𝘷𝘪𝘤𝘦 𝘵𝘩𝘢𝘵 𝘵𝘢𝘬𝘦𝘴 𝘪𝘯𝘵𝘰 𝘤𝘰𝘯𝘴𝘪𝘥𝘦𝘳𝘢𝘵𝘪𝘰𝘯 𝘵𝘩𝘦 𝘴𝘱𝘦𝘤𝘪𝘧𝘪𝘤 𝘥𝘢𝘵𝘢 𝘢𝘯𝘥 𝘴𝘱𝘦𝘤𝘪𝘢𝘭 𝘯𝘦𝘦𝘥𝘴 𝘰𝘧 𝘦𝘢𝘤𝘩 𝘳𝘦𝘢𝘥𝘦𝘳, 𝘢𝘯𝘥 𝘪𝘯 𝘢𝘯𝘺 𝘤𝘢𝘴𝘦, 𝘪𝘵 𝘪𝘴 𝘳𝘦𝘤𝘰𝘮𝘮𝘦𝘯𝘥𝘦𝘥 𝘵𝘰 𝘤𝘰𝘯𝘴𝘶𝘭𝘵 𝘸𝘪𝘵𝘩 𝘱𝘳𝘰𝘧𝘦𝘴𝘴𝘪𝘰𝘯𝘢𝘭𝘴 𝘢𝘯𝘥 𝘵𝘢𝘹 𝘢𝘥𝘷𝘪𝘴𝘰𝘳𝘴 𝘪𝘯 𝘵𝘩𝘦𝘴𝘦 𝘤𝘰𝘯𝘵𝘦𝘹𝘵𝘴.

Jun 12

Vanguard is now the biggest ETF issuer in the United States overtaking BlackRock

22

Jun 12

💬: What factors likely drove @SPGlobalRatings to upgrade @NVIDIA to AA, and what does the upgrade signal about the company's financial strength and competitive position?

#BridgetPerspective 👇

🤖: S&P Global Ratings upgraded NVIDIA Corporation [NasdaqGS:NVDA] to AA primarily due to its exceptional revenue growth, robust profitability, and dominant position in the AI and semiconductor markets. The upgrade reflects several concrete drivers:

▶️ NVIDIA’s revenue is projected to surge to approximately 394 billion USD in fiscal 2027 and 544 billion USD in fiscal 2028, representing explosive growth rates of 82% and 38% year-over-year, respectively.

▶️ Free operating cash flow is expected to reach 196 billion USD in fiscal 2027 and 276 billion USD in fiscal 2028, more than doubling from 97 billion USD in fiscal 2026, highlighting outstanding cash generation.

▶️ The company’s EBITDA margins are forecasted to strengthen to about 68% over the next two years, up from 65% in fiscal 2026, underscoring efficient operations and high profitability.

▶️ NVIDIA maintains an extremely strong liquidity profile, with 81 billion USD in cash and marketable securities against just 8.5 billion USD of funded debt as of April 26, 2026.

▶️ The upgrade was also supported by NVIDIA’s decisive capital allocation moves, including an 80 billion USD increase in share repurchase authorization and a dividend hike to 0.25 USD per share (about 24 billion USD annually).

The AA rating signals that NVIDIA is viewed as having very strong financial strength, with ample liquidity, low leverage, and resilient cash flows. It also highlights the company’s leadership and competitive edge in AI infrastructure, driven by successful product transitions (like Blackwell GPUs) and a clear roadmap for next-generation innovations (Rubin architecture). The upgrade suggests confidence in NVIDIA’s ability to capture outsized market opportunities, withstand market volatility, and maintain its pole position in the rapidly evolving tech landscape.

#AIFinance #Fintech #FinancialMarkets #InvestorEducation #FinanceTwitter #AI

---

*𝘉𝘳𝘪𝘥𝘨𝘦𝘵™ 𝘣𝘺 @𝘉𝘳𝘪𝘥𝘨𝘦𝘞𝘪𝘴𝘦𝘈𝘐 𝘪𝘴 𝘢𝘯 𝘈𝘐 𝘤𝘩𝘢𝘵 𝘧𝘰𝘳 𝘪𝘯𝘷𝘦𝘴𝘵𝘮𝘦𝘯𝘵𝘴, 𝘱𝘳𝘰𝘷𝘪𝘥𝘪𝘯𝘨 𝘳𝘦𝘨𝘶𝘭𝘢𝘵𝘰𝘳𝘺-𝘤𝘰𝘮𝘱𝘭𝘪𝘢𝘯𝘵 𝘪𝘯𝘴𝘪𝘨𝘩𝘵𝘴 & 𝘳𝘦𝘤𝘰𝘮𝘮𝘦𝘯𝘥𝘢𝘵𝘪𝘰𝘯𝘴 𝘰𝘯 50𝘒 𝘨𝘭𝘰𝘣𝘢𝘭 𝘴𝘦𝘤𝘶𝘳𝘪𝘵𝘪𝘦𝘴.

**𝘛𝘩𝘦 𝘪𝘯𝘧𝘰𝘳𝘮𝘢𝘵𝘪𝘰𝘯 𝘪𝘯𝘤𝘭𝘶𝘥𝘦𝘥 𝘪𝘯 𝘵𝘩𝘦 𝘢𝘯𝘢𝘭𝘺𝘴𝘪𝘴 𝘪𝘴 𝘪𝘯𝘵𝘦𝘯𝘥𝘦𝘥 𝘧𝘰𝘳 𝘨𝘦𝘯𝘦𝘳𝘢𝘭 𝘨𝘶𝘪𝘥𝘢𝘯𝘤𝘦 𝘱𝘶𝘳𝘱𝘰𝘴𝘦𝘴 𝘰𝘯𝘭𝘺. 𝘜𝘯𝘥𝘦𝘳 𝘯𝘰 𝘤𝘪𝘳𝘤𝘶𝘮𝘴𝘵𝘢𝘯𝘤𝘦𝘴 𝘪𝘴 𝘵𝘩𝘦 𝘪𝘯𝘧𝘰𝘳𝘮𝘢𝘵𝘪𝘰𝘯 𝘢𝘥𝘫𝘶𝘴𝘵𝘦𝘥 𝘵𝘰 𝘢 𝘴𝘱𝘦𝘤𝘪𝘧𝘪𝘤 𝘧𝘢𝘤𝘵𝘰𝘳 𝘰𝘳 𝘷𝘢𝘳𝘪𝘢𝘣𝘭𝘦 𝘳𝘦𝘭𝘢𝘵𝘦𝘥 𝘵𝘰 𝘵𝘩𝘦 𝘪𝘥𝘦𝘯𝘵𝘪𝘵𝘺 𝘰𝘧 𝘵𝘩𝘦 𝘳𝘦𝘱𝘰𝘳𝘵 𝘳𝘦𝘢𝘥𝘦𝘳. 𝘛𝘩𝘦 𝘪𝘯𝘧𝘰𝘳𝘮𝘢𝘵𝘪𝘰𝘯 𝘪𝘴 𝘯𝘰𝘵 𝘢 𝘴𝘶𝘣𝘴𝘵𝘪𝘵𝘶𝘵𝘦 𝘧𝘰𝘳 𝘴𝘱𝘦𝘤𝘪𝘧𝘪𝘤 𝘢𝘥𝘷𝘪𝘤𝘦 𝘵𝘩𝘢𝘵 𝘵𝘢𝘬𝘦𝘴 𝘪𝘯𝘵𝘰 𝘤𝘰𝘯𝘴𝘪𝘥𝘦𝘳𝘢𝘵𝘪𝘰𝘯 𝘵𝘩𝘦 𝘴𝘱𝘦𝘤𝘪𝘧𝘪𝘤 𝘥𝘢𝘵𝘢 𝘢𝘯𝘥 𝘴𝘱𝘦𝘤𝘪𝘢𝘭 𝘯𝘦𝘦𝘥𝘴 𝘰𝘧 𝘦𝘢𝘤𝘩 𝘳𝘦𝘢𝘥𝘦𝘳, 𝘢𝘯𝘥 𝘪𝘯 𝘢𝘯𝘺 𝘤𝘢𝘴𝘦, 𝘪𝘵 𝘪𝘴 𝘳𝘦𝘤𝘰𝘮𝘮𝘦𝘯𝘥𝘦𝘥 𝘵𝘰 𝘤𝘰𝘯𝘴𝘶𝘭𝘵 𝘸𝘪𝘵𝘩 𝘱𝘳𝘰𝘧𝘦𝘴𝘴𝘪𝘰𝘯𝘢𝘭𝘴 𝘢𝘯𝘥 𝘵𝘢𝘹 𝘢𝘥𝘷𝘪𝘴𝘰𝘳𝘴 𝘪𝘯 𝘵𝘩𝘦𝘴𝘦 𝘤𝘰𝘯𝘵𝘦𝘹𝘵𝘴.

28

Jun 11

💬: Which publicly traded companies stand to benefit the most from the U.S. becoming the world's largest oil exporter?

#BridgetPerspective 👇

🤖: With the U.S. now leading as the world’s largest oil exporter, certain publicly traded oil & gas explorers in the U.S. are well positioned to benefit from the shift in global energy trade. Here are some standouts:

Green Plains Inc. [NasdaqGS:GPRE] is in the top 10% of Energy companies, backed by very strong balance sheet and income statement scores. Its strong EBITDA metrics and focus on low-carbon fuels make it a cash engine in the current export-driven market. The company has a Buy recommendation.

@ValeroEnergy Corporation [NYSE:VLO] also lands in the top 10% of its sector, boasting very strong financials across the board and a strong cash flow profile. Its leadership in net change in cash and basic EPS signals resilience and opportunity as U.S. exports surge. The company has a Buy recommendation.

EOG Resources, Inc. [NYSE:EOG] stands out for its very strong balance sheet and strong cash flow, ranking in the top 30% of Energy peers. Its asset turnover and book value per share are bright spots, marking it as a solid player for those eyeing U.S. oil export growth. The company has an Outperform recommendation.

Viper Energy, Inc. [NasdaqGS:VNOM] is also in the top 30% of the sector, with a strong balance sheet and very strong cash flow. Its performance in total liabilities and shares outstanding highlights operational discipline—an asset in a booming export environment. The company has an Outperform recommendation.

Major integrated oil companies like @ExxonMobil, @Chevron, and @ConocoPhillips are also commonly recognized as beneficiaries, but @BridgeWiseAI does not provide ratings for these companies in the current analysis.

The analysis and recommendations presented are based on artificial intelligence and do not constitute, and should not be considered, personalized investment advice.

#AIFinance #Fintech #FinancialMarkets #InvestorEducation #FinanceTwitter #AI

---

*𝘉𝘳𝘪𝘥𝘨𝘦𝘵™ 𝘣𝘺 @𝘉𝘳𝘪𝘥𝘨𝘦𝘞𝘪𝘴𝘦𝘈𝘐 𝘪𝘴 𝘢𝘯 𝘈𝘐 𝘤𝘩𝘢𝘵 𝘧𝘰𝘳 𝘪𝘯𝘷𝘦𝘴𝘵𝘮𝘦𝘯𝘵𝘴, 𝘱𝘳𝘰𝘷𝘪𝘥𝘪𝘯𝘨 𝘳𝘦𝘨𝘶𝘭𝘢𝘵𝘰𝘳𝘺-𝘤𝘰𝘮𝘱𝘭𝘪𝘢𝘯𝘵 𝘪𝘯𝘴𝘪𝘨𝘩𝘵𝘴 & 𝘳𝘦𝘤𝘰𝘮𝘮𝘦𝘯𝘥𝘢𝘵𝘪𝘰𝘯𝘴 𝘰𝘯 50𝘒 𝘨𝘭𝘰𝘣𝘢𝘭 𝘴𝘦𝘤𝘶𝘳𝘪𝘵𝘪𝘦𝘴.

**𝘛𝘩𝘦 𝘪𝘯𝘧𝘰𝘳𝘮𝘢𝘵𝘪𝘰𝘯 𝘪𝘯𝘤𝘭𝘶𝘥𝘦𝘥 𝘪𝘯 𝘵𝘩𝘦 𝘢𝘯𝘢𝘭𝘺𝘴𝘪𝘴 𝘪𝘴 𝘪𝘯𝘵𝘦𝘯𝘥𝘦𝘥 𝘧𝘰𝘳 𝘨𝘦𝘯𝘦𝘳𝘢𝘭 𝘨𝘶𝘪𝘥𝘢𝘯𝘤𝘦 𝘱𝘶𝘳𝘱𝘰𝘴𝘦𝘴 𝘰𝘯𝘭𝘺. 𝘜𝘯𝘥𝘦𝘳 𝘯𝘰 𝘤𝘪𝘳𝘤𝘶𝘮𝘴𝘵𝘢𝘯𝘤𝘦𝘴 𝘪𝘴 𝘵𝘩𝘦 𝘪𝘯𝘧𝘰𝘳𝘮𝘢𝘵𝘪𝘰𝘯 𝘢𝘥𝘫𝘶𝘴𝘵𝘦𝘥 𝘵𝘰 𝘢 𝘴𝘱𝘦𝘤𝘪𝘧𝘪𝘤 𝘧𝘢𝘤𝘵𝘰𝘳 𝘰𝘳 𝘷𝘢𝘳𝘪𝘢𝘣𝘭𝘦 𝘳𝘦𝘭𝘢𝘵𝘦𝘥 𝘵𝘰 𝘵𝘩𝘦 𝘪𝘥𝘦𝘯𝘵𝘪𝘵𝘺 𝘰𝘧 𝘵𝘩𝘦 𝘳𝘦𝘱𝘰𝘳𝘵 𝘳𝘦𝘢𝘥𝘦𝘳. 𝘛𝘩𝘦 𝘪𝘯𝘧𝘰𝘳𝘮𝘢𝘵𝘪𝘰𝘯 𝘪𝘴 𝘯𝘰𝘵 𝘢 𝘴𝘶𝘣𝘴𝘵𝘪𝘵𝘶𝘵𝘦 𝘧𝘰𝘳 𝘴𝘱𝘦𝘤𝘪𝘧𝘪𝘤 𝘢𝘥𝘷𝘪𝘤𝘦 𝘵𝘩𝘢𝘵 𝘵𝘢𝘬𝘦𝘴 𝘪𝘯𝘵𝘰 𝘤𝘰𝘯𝘴𝘪𝘥𝘦𝘳𝘢𝘵𝘪𝘰𝘯 𝘵𝘩𝘦 𝘴𝘱𝘦𝘤𝘪𝘧𝘪𝘤 𝘥𝘢𝘵𝘢 𝘢𝘯𝘥 𝘴𝘱𝘦𝘤𝘪𝘢𝘭 𝘯𝘦𝘦𝘥𝘴 𝘰𝘧 𝘦𝘢𝘤𝘩 𝘳𝘦𝘢𝘥𝘦𝘳, 𝘢𝘯𝘥 𝘪𝘯 𝘢𝘯𝘺 𝘤𝘢𝘴𝘦, 𝘪𝘵 𝘪𝘴 𝘳𝘦𝘤𝘰𝘮𝘮𝘦𝘯𝘥𝘦𝘥 𝘵𝘰 𝘤𝘰𝘯𝘴𝘶𝘭𝘵 𝘸𝘪𝘵𝘩 𝘱𝘳𝘰𝘧𝘦𝘴𝘴𝘪𝘰𝘯𝘢𝘭𝘴 𝘢𝘯𝘥 𝘵𝘢𝘹 𝘢𝘥𝘷𝘪𝘴𝘰𝘳𝘴 𝘪𝘯 𝘵𝘩𝘦𝘴𝘦 𝘤𝘰𝘯𝘵𝘦𝘹𝘵𝘴.

Jun 11

The United States has become the world's largest oil exporter, per Reuters

33

Jun 11

💬: What are the key risks that could prevent SpaceX from justifying its IPO valuation, and which metrics should investors monitor over the next 2–3 years?

#BridgetPerspective 👇

🤖: SpaceX is entering the public market with a headline-grabbing valuation between $1.75 trillion and $2 trillion, aiming to raise $75 billion through its Nasdaq debut. The company’s financials show impressive top-line growth, with 2025 revenue hitting $18.7 billion—a 33% jump from the previous year. Starlink, its satellite internet segment, is the main engine, contributing $11.4 billion (61% of total revenue) and boasting over 12 million subscribers as of June 2026.

The biggest risks to justifying this lofty valuation revolve around profitability, cash flow, and execution. Despite strong revenue momentum, SpaceX posted a 2025 GAAP net loss of $4.94 billion and a Q1 2026 net loss of $4.28 billion, with an accumulated deficit of $41.3 billion. These figures highlight the challenge of scaling revenue into sustainable profits, especially as the average revenue per Starlink user has declined.

To gauge whether SpaceX can live up to its valuation, investors should closely track annual revenue growth, the pace of Starlink subscriber additions, and any progress toward positive net income or free cash flow. Watching the trend in Starlink’s ARPU and operating margins will also be key, as these will reveal how well SpaceX can monetize its core business and manage costs while pursuing ambitious expansion plans.

#AIFinance #Fintech #FinancialMarkets #InvestorEducation #FinanceTwitter #AI

---

*𝘉𝘳𝘪𝘥𝘨𝘦𝘵™ 𝘣𝘺 @𝘉𝘳𝘪𝘥𝘨𝘦𝘞𝘪𝘴𝘦𝘈𝘐 𝘪𝘴 𝘢𝘯 𝘈𝘐 𝘤𝘩𝘢𝘵 𝘧𝘰𝘳 𝘪𝘯𝘷𝘦𝘴𝘵𝘮𝘦𝘯𝘵𝘴, 𝘱𝘳𝘰𝘷𝘪𝘥𝘪𝘯𝘨 𝘳𝘦𝘨𝘶𝘭𝘢𝘵𝘰𝘳𝘺-𝘤𝘰𝘮𝘱𝘭𝘪𝘢𝘯𝘵 𝘪𝘯𝘴𝘪𝘨𝘩𝘵𝘴 & 𝘳𝘦𝘤𝘰𝘮𝘮𝘦𝘯𝘥𝘢𝘵𝘪𝘰𝘯𝘴 𝘰𝘯 50𝘒 𝘨𝘭𝘰𝘣𝘢𝘭 𝘴𝘦𝘤𝘶𝘳𝘪𝘵𝘪𝘦𝘴.

**𝘛𝘩𝘦 𝘪𝘯𝘧𝘰𝘳𝘮𝘢𝘵𝘪𝘰𝘯 𝘪𝘯𝘤𝘭𝘶𝘥𝘦𝘥 𝘪𝘯 𝘵𝘩𝘦 𝘢𝘯𝘢𝘭𝘺𝘴𝘪𝘴 𝘪𝘴 𝘪𝘯𝘵𝘦𝘯𝘥𝘦𝘥 𝘧𝘰𝘳 𝘨𝘦𝘯𝘦𝘳𝘢𝘭 𝘨𝘶𝘪𝘥𝘢𝘯𝘤𝘦 𝘱𝘶𝘳𝘱𝘰𝘴𝘦𝘴 𝘰𝘯𝘭𝘺. 𝘜𝘯𝘥𝘦𝘳 𝘯𝘰 𝘤𝘪𝘳𝘤𝘶𝘮𝘴𝘵𝘢𝘯𝘤𝘦𝘴 𝘪𝘴 𝘵𝘩𝘦 𝘪𝘯𝘧𝘰𝘳𝘮𝘢𝘵𝘪𝘰𝘯 𝘢𝘥𝘫𝘶𝘴𝘵𝘦𝘥 𝘵𝘰 𝘢 𝘴𝘱𝘦𝘤𝘪𝘧𝘪𝘤 𝘧𝘢𝘤𝘵𝘰𝘳 𝘰𝘳 𝘷𝘢𝘳𝘪𝘢𝘣𝘭𝘦 𝘳𝘦𝘭𝘢𝘵𝘦𝘥 𝘵𝘰 𝘵𝘩𝘦 𝘪𝘥𝘦𝘯𝘵𝘪𝘵𝘺 𝘰𝘧 𝘵𝘩𝘦 𝘳𝘦𝘱𝘰𝘳𝘵 𝘳𝘦𝘢𝘥𝘦𝘳. 𝘛𝘩𝘦 𝘪𝘯𝘧𝘰𝘳𝘮𝘢𝘵𝘪𝘰𝘯 𝘪𝘴 𝘯𝘰𝘵 𝘢 𝘴𝘶𝘣𝘴𝘵𝘪𝘵𝘶𝘵𝘦 𝘧𝘰𝘳 𝘴𝘱𝘦𝘤𝘪𝘧𝘪𝘤 𝘢𝘥𝘷𝘪𝘤𝘦 𝘵𝘩𝘢𝘵 𝘵𝘢𝘬𝘦𝘴 𝘪𝘯𝘵𝘰 𝘤𝘰𝘯𝘴𝘪𝘥𝘦𝘳𝘢𝘵𝘪𝘰𝘯 𝘵𝘩𝘦 𝘴𝘱𝘦𝘤𝘪𝘧𝘪𝘤 𝘥𝘢𝘵𝘢 𝘢𝘯𝘥 𝘴𝘱𝘦𝘤𝘪𝘢𝘭 𝘯𝘦𝘦𝘥𝘴 𝘰𝘧 𝘦𝘢𝘤𝘩 𝘳𝘦𝘢𝘥𝘦𝘳, 𝘢𝘯𝘥 𝘪𝘯 𝘢𝘯𝘺 𝘤𝘢𝘴𝘦, 𝘪𝘵 𝘪𝘴 𝘳𝘦𝘤𝘰𝘮𝘮𝘦𝘯𝘥𝘦𝘥 𝘵𝘰 𝘤𝘰𝘯𝘴𝘶𝘭𝘵 𝘸𝘪𝘵𝘩 𝘱𝘳𝘰𝘧𝘦𝘴𝘴𝘪𝘰𝘯𝘢𝘭𝘴 𝘢𝘯𝘥 𝘵𝘢𝘹 𝘢𝘥𝘷𝘪𝘴𝘰𝘳𝘴 𝘪𝘯 𝘵𝘩𝘦𝘴𝘦 𝘤𝘰𝘯𝘵𝘦𝘹𝘵𝘴.

SpaceX $SPCX is worth a max of $63 per share, warns Morningstar Research, far less than its IPO offering price of $135 🚨🚨

91

Jun 10

💬: How does @Rivian's decision to use lidar and radar sensors, rather than a vision-only approach, affect its cost structure and competitive positioning against $TSLA?

#BridgetPerspective 👇

🤖: Rivian Automotive, Inc. [NasdaqGS:RIVN] is taking a multi-sensor approach by integrating cameras, radar, and lidar into its vehicles, while Tesla, Inc. [NasdaqGS:TSLA] relies on a vision-only system using just cameras. This fundamental difference shapes both companies' cost structures and their competitive positioning in the electric vehicle and autonomous driving markets.

For Rivian, adding lidar and radar increases the upfront hardware costs per vehicle, although recent advances have made lidar much more affordable—dropping from tens of thousands of dollars to just a few hundred dollars per unit. The upcoming R2 models will feature this sensor suite, and Rivian is also investing in proprietary in-house AI chips to support its autonomy platform. This approach means Rivian faces a higher bill of materials and more complex supply chain management, impacting margins in the near term. However, the company believes the richer sensor fusion offers better safety and reliability, especially in challenging conditions, and provides a continuous stream of high-quality data to improve its autonomous systems.

In contrast, Tesla’s vision-only strategy keeps hardware costs lower and simplifies manufacturing and maintenance, helping protect margins and scale faster. But it may face limitations in certain driving scenarios where additional sensor redundancy could enhance safety or performance.

In terms of competitive positioning, Rivian’s sensor-rich vehicles are marketed as safer and more robust in diverse environments, directly challenging Tesla’s approach. This could appeal to customers prioritizing advanced driver-assistance features and may differentiate Rivian in the premium EV space. However, the added costs and complexity mean Rivian must prove it can scale production efficiently and reach profitability, a challenge Tesla has worked to overcome with its leaner design philosophy.

#AIFinance #Fintech #FinancialMarkets #InvestorEducation #FinanceTwitter #AI

---

*𝘉𝘳𝘪𝘥𝘨𝘦𝘵™ 𝘣𝘺 @𝘉𝘳𝘪𝘥𝘨𝘦𝘞𝘪𝘴𝘦𝘈𝘐 𝘪𝘴 𝘢𝘯 𝘈𝘐 𝘤𝘩𝘢𝘵 𝘧𝘰𝘳 𝘪𝘯𝘷𝘦𝘴𝘵𝘮𝘦𝘯𝘵𝘴, 𝘱𝘳𝘰𝘷𝘪𝘥𝘪𝘯𝘨 𝘳𝘦𝘨𝘶𝘭𝘢𝘵𝘰𝘳𝘺-𝘤𝘰𝘮𝘱𝘭𝘪𝘢𝘯𝘵 𝘪𝘯𝘴𝘪𝘨𝘩𝘵𝘴 & 𝘳𝘦𝘤𝘰𝘮𝘮𝘦𝘯𝘥𝘢𝘵𝘪𝘰𝘯𝘴 𝘰𝘯 50𝘒 𝘨𝘭𝘰𝘣𝘢𝘭 𝘴𝘦𝘤𝘶𝘳𝘪𝘵𝘪𝘦𝘴.

**𝘛𝘩𝘦 𝘪𝘯𝘧𝘰𝘳𝘮𝘢𝘵𝘪𝘰𝘯 𝘪𝘯𝘤𝘭𝘶𝘥𝘦𝘥 𝘪𝘯 𝘵𝘩𝘦 𝘢𝘯𝘢𝘭𝘺𝘴𝘪𝘴 𝘪𝘴 𝘪𝘯𝘵𝘦𝘯𝘥𝘦𝘥 𝘧𝘰𝘳 𝘨𝘦𝘯𝘦𝘳𝘢𝘭 𝘨𝘶𝘪𝘥𝘢𝘯𝘤𝘦 𝘱𝘶𝘳𝘱𝘰𝘴𝘦𝘴 𝘰𝘯𝘭𝘺. 𝘜𝘯𝘥𝘦𝘳 𝘯𝘰 𝘤𝘪𝘳𝘤𝘶𝘮𝘴𝘵𝘢𝘯𝘤𝘦𝘴 𝘪𝘴 𝘵𝘩𝘦 𝘪𝘯𝘧𝘰𝘳𝘮𝘢𝘵𝘪𝘰𝘯 𝘢𝘥𝘫𝘶𝘴𝘵𝘦𝘥 𝘵𝘰 𝘢 𝘴𝘱𝘦𝘤𝘪𝘧𝘪𝘤 𝘧𝘢𝘤𝘵𝘰𝘳 𝘰𝘳 𝘷𝘢𝘳𝘪𝘢𝘣𝘭𝘦 𝘳𝘦𝘭𝘢𝘵𝘦𝘥 𝘵𝘰 𝘵𝘩𝘦 𝘪𝘥𝘦𝘯𝘵𝘪𝘵𝘺 𝘰𝘧 𝘵𝘩𝘦 𝘳𝘦𝘱𝘰𝘳𝘵 𝘳𝘦𝘢𝘥𝘦𝘳. 𝘛𝘩𝘦 𝘪𝘯𝘧𝘰𝘳𝘮𝘢𝘵𝘪𝘰𝘯 𝘪𝘴 𝘯𝘰𝘵 𝘢 𝘴𝘶𝘣𝘴𝘵𝘪𝘵𝘶𝘵𝘦 𝘧𝘰𝘳 𝘴𝘱𝘦𝘤𝘪𝘧𝘪𝘤 𝘢𝘥𝘷𝘪𝘤𝘦 𝘵𝘩𝘢𝘵 𝘵𝘢𝘬𝘦𝘴 𝘪𝘯𝘵𝘰 𝘤𝘰𝘯𝘴𝘪𝘥𝘦𝘳𝘢𝘵𝘪𝘰𝘯 𝘵𝘩𝘦 𝘴𝘱𝘦𝘤𝘪𝘧𝘪𝘤 𝘥𝘢𝘵𝘢 𝘢𝘯𝘥 𝘴𝘱𝘦𝘤𝘪𝘢𝘭 𝘯𝘦𝘦𝘥𝘴 𝘰𝘧 𝘦𝘢𝘤𝘩 𝘳𝘦𝘢𝘥𝘦𝘳, 𝘢𝘯𝘥 𝘪𝘯 𝘢𝘯𝘺 𝘤𝘢𝘴𝘦, 𝘪𝘵 𝘪𝘴 𝘳𝘦𝘤𝘰𝘮𝘮𝘦𝘯𝘥𝘦𝘥 𝘵𝘰 𝘤𝘰𝘯𝘴𝘶𝘭𝘵 𝘸𝘪𝘵𝘩 𝘱𝘳𝘰𝘧𝘦𝘴𝘴𝘪𝘰𝘯𝘢𝘭𝘴 𝘢𝘯𝘥 𝘵𝘢𝘹 𝘢𝘥𝘷𝘪𝘴𝘰𝘳𝘴 𝘪𝘯 𝘵𝘩𝘦𝘴𝘦 𝘤𝘰𝘯𝘵𝘦𝘹𝘵𝘴.

Rivian CEO @RJScaringe says the company plans to launch hands-off driving later this year, eyes-off driving in 2027, and fully autonomous vehicles that never require human intervention in 2028.

"Getting to Level 4, which is the idea of the vehicle driving empty, you sitting in the backseat, picking up groceries for you, or dropping you at the airport, our timeline for that is 2028.

"We have point-to-point capabilities launching later this year. That's when you're in the driver's seat, you type in the address, and the car will completely navigate to that address. Your hands are not on the wheel, you're still alert and aware of what's happening, but you're not driving the car. We call that hands off, eyes on."

"Next year we'll go to Level 3, which is hands off, eyes off. So you do all that, but you no longer have to look at the road at all. You can be on your phone, reading a book, etc."

"Level 4 is where the car won't ask you to take over in any situation. It's fully on its own."

1

136

Jun 9

💬: Which sectors stand to gain the most if China's AI strategy succeeds?

#BridgetPerspective 👇

🤖: China’s AI strategy is fueling growth across several key sectors. Autonomous vehicles are a standout, grabbing 22% of total AI investment in 2026, followed by computer vision with 18% and natural language processing (NLP) at 11%. Healthcare AI is also a major focus, with the government rolling out AI-assisted diagnosis in hospitals and making AI capacity more accessible and affordable for healthcare enterprises.

Industrial automation and manufacturing are seeing large-scale integration of AI into production and operations, while finance, logistics, and smart city infrastructure are set to benefit from more affordable AI solutions. The chip development and semiconductor sector is another strategic priority, with China aiming to source at least 80% of essential technologies domestically. Robotics is also getting targeted support, especially for industrial and real-world deployment. If China’s AI strategy hits its marks, these sectors are positioned to see the biggest gains.

#AIFinance #Fintech #FinancialMarkets #InvestorEducation #FinanceTwitter #AI

---

*𝘉𝘳𝘪𝘥𝘨𝘦𝘵™ 𝘣𝘺 @𝘉𝘳𝘪𝘥𝘨𝘦𝘞𝘪𝘴𝘦𝘈𝘐 𝘪𝘴 𝘢𝘯 𝘈𝘐 𝘤𝘩𝘢𝘵 𝘧𝘰𝘳 𝘪𝘯𝘷𝘦𝘴𝘵𝘮𝘦𝘯𝘵𝘴, 𝘱𝘳𝘰𝘷𝘪𝘥𝘪𝘯𝘨 𝘳𝘦𝘨𝘶𝘭𝘢𝘵𝘰𝘳𝘺-𝘤𝘰𝘮𝘱𝘭𝘪𝘢𝘯𝘵 𝘪𝘯𝘴𝘪𝘨𝘩𝘵𝘴 & 𝘳𝘦𝘤𝘰𝘮𝘮𝘦𝘯𝘥𝘢𝘵𝘪𝘰𝘯𝘴 𝘰𝘯 50𝘒 𝘨𝘭𝘰𝘣𝘢𝘭 𝘴𝘦𝘤𝘶𝘳𝘪𝘵𝘪𝘦𝘴.

**𝘛𝘩𝘦 𝘪𝘯𝘧𝘰𝘳𝘮𝘢𝘵𝘪𝘰𝘯 𝘪𝘯𝘤𝘭𝘶𝘥𝘦𝘥 𝘪𝘯 𝘵𝘩𝘦 𝘢𝘯𝘢𝘭𝘺𝘴𝘪𝘴 𝘪𝘴 𝘪𝘯𝘵𝘦𝘯𝘥𝘦𝘥 𝘧𝘰𝘳 𝘨𝘦𝘯𝘦𝘳𝘢𝘭 𝘨𝘶𝘪𝘥𝘢𝘯𝘤𝘦 𝘱𝘶𝘳𝘱𝘰𝘴𝘦𝘴 𝘰𝘯𝘭𝘺. 𝘜𝘯𝘥𝘦𝘳 𝘯𝘰 𝘤𝘪𝘳𝘤𝘶𝘮𝘴𝘵𝘢𝘯𝘤𝘦𝘴 𝘪𝘴 𝘵𝘩𝘦 𝘪𝘯𝘧𝘰𝘳𝘮𝘢𝘵𝘪𝘰𝘯 𝘢𝘥𝘫𝘶𝘴𝘵𝘦𝘥 𝘵𝘰 𝘢 𝘴𝘱𝘦𝘤𝘪𝘧𝘪𝘤 𝘧𝘢𝘤𝘵𝘰𝘳 𝘰𝘳 𝘷𝘢𝘳𝘪𝘢𝘣𝘭𝘦 𝘳𝘦𝘭𝘢𝘵𝘦𝘥 𝘵𝘰 𝘵𝘩𝘦 𝘪𝘥𝘦𝘯𝘵𝘪𝘵𝘺 𝘰𝘧 𝘵𝘩𝘦 𝘳𝘦𝘱𝘰𝘳𝘵 𝘳𝘦𝘢𝘥𝘦𝘳. 𝘛𝘩𝘦 𝘪𝘯𝘧𝘰𝘳𝘮𝘢𝘵𝘪𝘰𝘯 𝘪𝘴 𝘯𝘰𝘵 𝘢 𝘴𝘶𝘣𝘴𝘵𝘪𝘵𝘶𝘵𝘦 𝘧𝘰𝘳 𝘴𝘱𝘦𝘤𝘪𝘧𝘪𝘤 𝘢𝘥𝘷𝘪𝘤𝘦 𝘵𝘩𝘢𝘵 𝘵𝘢𝘬𝘦𝘴 𝘪𝘯𝘵𝘰 𝘤𝘰𝘯𝘴𝘪𝘥𝘦𝘳𝘢𝘵𝘪𝘰𝘯 𝘵𝘩𝘦 𝘴𝘱𝘦𝘤𝘪𝘧𝘪𝘤 𝘥𝘢𝘵𝘢 𝘢𝘯𝘥 𝘴𝘱𝘦𝘤𝘪𝘢𝘭 𝘯𝘦𝘦𝘥𝘴 𝘰𝘧 𝘦𝘢𝘤𝘩 𝘳𝘦𝘢𝘥𝘦𝘳, 𝘢𝘯𝘥 𝘪𝘯 𝘢𝘯𝘺 𝘤𝘢𝘴𝘦, 𝘪𝘵 𝘪𝘴 𝘳𝘦𝘤𝘰𝘮𝘮𝘦𝘯𝘥𝘦𝘥 𝘵𝘰 𝘤𝘰𝘯𝘴𝘶𝘭𝘵 𝘸𝘪𝘵𝘩 𝘱𝘳𝘰𝘧𝘦𝘴𝘴𝘪𝘰𝘯𝘢𝘭𝘴 𝘢𝘯𝘥 𝘵𝘢𝘹 𝘢𝘥𝘷𝘪𝘴𝘰𝘳𝘴 𝘪𝘯 𝘵𝘩𝘦𝘴𝘦 𝘤𝘰𝘯𝘵𝘦𝘹𝘵𝘴.

Jun 9

The plan fuels Beijing’s ambition to propel the domestic AI sector and surpass the US in a potentially game-changing technology. yhoo.it/49Szx1g

1

25

Jun 8

💬: $GOOGL manufactures its own TPU chips in-house. How does shifting some production to Intel affect Google's cost structure and its competitive advantage in AI infrastructure?

#BridgetPerspective 👇

#AIFinance #Fintech #FinancialMarkets #InvestorEducation #FinanceTwitter #AI

57

Jun 8

💬: With CPI data due this week and oil prices still elevated, how does the Iran ceasefire change the inflation outlook — and what does that mean for rate-sensitive growth stocks in the Nasdaq?

#BridgetPerspective 👇

🤖: Based on Bridgewise's analysis:

- Crude Oil / WTI [NYMEX:CL] prices have been highly volatile, primarily due to ongoing geopolitical tensions in the Middle East. The recent escalation between Iran and Israel pushed WTI prices up to 94.80 USD/Bbl, and Brent crude to 97.85 USD/Bbl, with the Strait of Hormuz remaining largely closed since late February.

Based on recent news reports and various information sources:

- The Iran ceasefire had previously triggered a sharp drop in oil prices, but renewed conflict quickly reversed that trend. Elevated oil prices have directly contributed to higher US inflation, with CPI rising to 3.8% in April 2026 (the highest since May 2023), largely driven by a 17.9% surge in energy costs.

- If the Iran ceasefire holds and tensions ease, oil prices could stabilize or even decline, potentially alleviating some upward pressure on inflation. However, with the situation still fragile and the Strait of Hormuz closed, energy prices remain a key risk for further inflation spikes.

- For rate-sensitive growth stocks in the Nasdaq, persistent inflation and elevated oil prices increase the likelihood that the Federal Reserve will keep interest rates higher for longer. This tends to weigh on valuations for growth stocks, as higher rates reduce the present value of their expected future earnings and can lead to increased volatility in the sector.

#AIFinance #Fintech #FinancialMarkets #InvestorEducation #FinanceTwitter #AI

---

*𝘉𝘳𝘪𝘥𝘨𝘦𝘵™ 𝘣𝘺 @𝘉𝘳𝘪𝘥𝘨𝘦𝘞𝘪𝘴𝘦𝘈𝘐 𝘪𝘴 𝘢𝘯 𝘈𝘐 𝘤𝘩𝘢𝘵 𝘧𝘰𝘳 𝘪𝘯𝘷𝘦𝘴𝘵𝘮𝘦𝘯𝘵𝘴, 𝘱𝘳𝘰𝘷𝘪𝘥𝘪𝘯𝘨 𝘳𝘦𝘨𝘶𝘭𝘢𝘵𝘰𝘳𝘺-𝘤𝘰𝘮𝘱𝘭𝘪𝘢𝘯𝘵 𝘪𝘯𝘴𝘪𝘨𝘩𝘵𝘴 & 𝘳𝘦𝘤𝘰𝘮𝘮𝘦𝘯𝘥𝘢𝘵𝘪𝘰𝘯𝘴 𝘰𝘯 50𝘒 𝘨𝘭𝘰𝘣𝘢𝘭 𝘴𝘦𝘤𝘶𝘳𝘪𝘵𝘪𝘦𝘴.

**𝘛𝘩𝘦 𝘪𝘯𝘧𝘰𝘳𝘮𝘢𝘵𝘪𝘰𝘯 𝘪𝘯𝘤𝘭𝘶𝘥𝘦𝘥 𝘪𝘯 𝘵𝘩𝘦 𝘢𝘯𝘢𝘭𝘺𝘴𝘪𝘴 𝘪𝘴 𝘪𝘯𝘵𝘦𝘯𝘥𝘦𝘥 𝘧𝘰𝘳 𝘨𝘦𝘯𝘦𝘳𝘢𝘭 𝘨𝘶𝘪𝘥𝘢𝘯𝘤𝘦 𝘱𝘶𝘳𝘱𝘰𝘴𝘦𝘴 𝘰𝘯𝘭𝘺. 𝘜𝘯𝘥𝘦𝘳 𝘯𝘰 𝘤𝘪𝘳𝘤𝘶𝘮𝘴𝘵𝘢𝘯𝘤𝘦𝘴 𝘪𝘴 𝘵𝘩𝘦 𝘪𝘯𝘧𝘰𝘳𝘮𝘢𝘵𝘪𝘰𝘯 𝘢𝘥𝘫𝘶𝘴𝘵𝘦𝘥 𝘵𝘰 𝘢 𝘴𝘱𝘦𝘤𝘪𝘧𝘪𝘤 𝘧𝘢𝘤𝘵𝘰𝘳 𝘰𝘳 𝘷𝘢𝘳𝘪𝘢𝘣𝘭𝘦 𝘳𝘦𝘭𝘢𝘵𝘦𝘥 𝘵𝘰 𝘵𝘩𝘦 𝘪𝘥𝘦𝘯𝘵𝘪𝘵𝘺 𝘰𝘧 𝘵𝘩𝘦 𝘳𝘦𝘱𝘰𝘳𝘵 𝘳𝘦𝘢𝘥𝘦𝘳. 𝘛𝘩𝘦 𝘪𝘯𝘧𝘰𝘳𝘮𝘢𝘵𝘪𝘰𝘯 𝘪𝘴 𝘯𝘰𝘵 𝘢 𝘴𝘶𝘣𝘴𝘵𝘪𝘵𝘶𝘵𝘦 𝘧𝘰𝘳 𝘴𝘱𝘦𝘤𝘪𝘧𝘪𝘤 𝘢𝘥𝘷𝘪𝘤𝘦 𝘵𝘩𝘢𝘵 𝘵𝘢𝘬𝘦𝘴 𝘪𝘯𝘵𝘰 𝘤𝘰𝘯𝘴𝘪𝘥𝘦𝘳𝘢𝘵𝘪𝘰𝘯 𝘵𝘩𝘦 𝘴𝘱𝘦𝘤𝘪𝘧𝘪𝘤 𝘥𝘢𝘵𝘢 𝘢𝘯𝘥 𝘴𝘱𝘦𝘤𝘪𝘢𝘭 𝘯𝘦𝘦𝘥𝘴 𝘰𝘧 𝘦𝘢𝘤𝘩 𝘳𝘦𝘢𝘥𝘦𝘳, 𝘢𝘯𝘥 𝘪𝘯 𝘢𝘯𝘺 𝘤𝘢𝘴𝘦, 𝘪𝘵 𝘪𝘴 𝘳𝘦𝘤𝘰𝘮𝘮𝘦𝘯𝘥𝘦𝘥 𝘵𝘰 𝘤𝘰𝘯𝘴𝘶𝘭𝘵 𝘸𝘪𝘵𝘩 𝘱𝘳𝘰𝘧𝘦𝘴𝘴𝘪𝘰𝘯𝘢𝘭𝘴 𝘢𝘯𝘥 𝘵𝘢𝘹 𝘢𝘥𝘷𝘪𝘴𝘰𝘳𝘴 𝘪𝘯 𝘵𝘩𝘦𝘴𝘦 𝘤𝘰𝘯𝘵𝘦𝘹𝘵𝘴.

BREAKING: Nasdaq 100 futures surge over 1.5% as Iran announces it is halting military operations against Israel and President Trump says he is working toward a "final deal" with Iran.

156

Jun 6

💬: Could the market be starting to view SpaceX's supplier ecosystem similarly to how investors once viewed key suppliers to Apple, and what would that mean for STM's upside potential?

#BridgetPerspective 👇

🤖: The market is indeed drawing parallels between SpaceX’s emerging supplier ecosystem and the way investors historically valued key suppliers to Apple Inc. [NasdaqGS:AAPL], but the implications for STMicroelectronics N.V. [ENXTPA:STMPA] are nuanced.

For SpaceX, suppliers like STM are gaining attention because SpaceX’s anticipated IPO and its dominant Starlink business are spotlighting companies that provide critical components—much like how Apple’s supply chain partners have been prized for their access to high-growth product cycles. STM has a 90% market share in Low Earth Orbit satellite semiconductors, and its revenue from SpaceX’s Starlink segment has grown from about 175 million USD in 2021 to nearly 1 billion USD in 2026, with a public commitment to over 3 billion USD in cumulative revenue through 2028. This association has already powered a substantial rally in STM’s shares—up 147% year-to-date and 34% in the past month as of late May 2026.

However, while investor excitement is running high—mirroring the “Apple supplier premium” seen in past cycles—STM’s upside potential faces headwinds. Bridgewise’s analysis assigns STM an Underperform recommendation, citing weak income statement and balance sheet fundamentals, significant cash outflows, and a target price of 40.5 EUR (46.68 USD), which is notably below the current market price of 62.82 EUR (72.41 USD). This suggests that, despite the market’s enthusiasm for STM’s SpaceX exposure, its financial profile does not currently support sustained outperformance.

In short, while STM is benefiting from the “SpaceX supplier effect” in the market narrative—much like Apple’s key suppliers did in the past—the company’s actual upside may be limited unless it can translate this strategic positioning into stronger, more sustainable financial results.

The analysis and recommendations presented are based on artificial intelligence and do not constitute, and should not be considered, personalized investment advice.

#AIFinance #Fintech #FinancialMarkets #InvestorEducation #FinanceTwitter #AI

---

*𝘉𝘳𝘪𝘥𝘨𝘦𝘵™ 𝘣𝘺 @𝘉𝘳𝘪𝘥𝘨𝘦𝘞𝘪𝘴𝘦𝘈𝘐 𝘪𝘴 𝘢𝘯 𝘈𝘐 𝘤𝘩𝘢𝘵 𝘧𝘰𝘳 𝘪𝘯𝘷𝘦𝘴𝘵𝘮𝘦𝘯𝘵𝘴, 𝘱𝘳𝘰𝘷𝘪𝘥𝘪𝘯𝘨 𝘳𝘦𝘨𝘶𝘭𝘢𝘵𝘰𝘳𝘺-𝘤𝘰𝘮𝘱𝘭𝘪𝘢𝘯𝘵 𝘪𝘯𝘴𝘪𝘨𝘩𝘵𝘴 & 𝘳𝘦𝘤𝘰𝘮𝘮𝘦𝘯𝘥𝘢𝘵𝘪𝘰𝘯𝘴 𝘰𝘯 50𝘒 𝘨𝘭𝘰𝘣𝘢𝘭 𝘴𝘦𝘤𝘶𝘳𝘪𝘵𝘪𝘦𝘴.

**𝘛𝘩𝘦 𝘪𝘯𝘧𝘰𝘳𝘮𝘢𝘵𝘪𝘰𝘯 𝘪𝘯𝘤𝘭𝘶𝘥𝘦𝘥 𝘪𝘯 𝘵𝘩𝘦 𝘢𝘯𝘢𝘭𝘺𝘴𝘪𝘴 𝘪𝘴 𝘪𝘯𝘵𝘦𝘯𝘥𝘦𝘥 𝘧𝘰𝘳 𝘨𝘦𝘯𝘦𝘳𝘢𝘭 𝘨𝘶𝘪𝘥𝘢𝘯𝘤𝘦 𝘱𝘶𝘳𝘱𝘰𝘴𝘦𝘴 𝘰𝘯𝘭𝘺. 𝘜𝘯𝘥𝘦𝘳 𝘯𝘰 𝘤𝘪𝘳𝘤𝘶𝘮𝘴𝘵𝘢𝘯𝘤𝘦𝘴 𝘪𝘴 𝘵𝘩𝘦 𝘪𝘯𝘧𝘰𝘳𝘮𝘢𝘵𝘪𝘰𝘯 𝘢𝘥𝘫𝘶𝘴𝘵𝘦𝘥 𝘵𝘰 𝘢 𝘴𝘱𝘦𝘤𝘪𝘧𝘪𝘤 𝘧𝘢𝘤𝘵𝘰𝘳 𝘰𝘳 𝘷𝘢𝘳𝘪𝘢𝘣𝘭𝘦 𝘳𝘦𝘭𝘢𝘵𝘦𝘥 𝘵𝘰 𝘵𝘩𝘦 𝘪𝘥𝘦𝘯𝘵𝘪𝘵𝘺 𝘰𝘧 𝘵𝘩𝘦 𝘳𝘦𝘱𝘰𝘳𝘵 𝘳𝘦𝘢𝘥𝘦𝘳. 𝘛𝘩𝘦 𝘪𝘯𝘧𝘰𝘳𝘮𝘢𝘵𝘪𝘰𝘯 𝘪𝘴 𝘯𝘰𝘵 𝘢 𝘴𝘶𝘣𝘴𝘵𝘪𝘵𝘶𝘵𝘦 𝘧𝘰𝘳 𝘴𝘱𝘦𝘤𝘪𝘧𝘪𝘤 𝘢𝘥𝘷𝘪𝘤𝘦 𝘵𝘩𝘢𝘵 𝘵𝘢𝘬𝘦𝘴 𝘪𝘯𝘵𝘰 𝘤𝘰𝘯𝘴𝘪𝘥𝘦𝘳𝘢𝘵𝘪𝘰𝘯 𝘵𝘩𝘦 𝘴𝘱𝘦𝘤𝘪𝘧𝘪𝘤 𝘥𝘢𝘵𝘢 𝘢𝘯𝘥 𝘴𝘱𝘦𝘤𝘪𝘢𝘭 𝘯𝘦𝘦𝘥𝘴 𝘰𝘧 𝘦𝘢𝘤𝘩 𝘳𝘦𝘢𝘥𝘦𝘳, 𝘢𝘯𝘥 𝘪𝘯 𝘢𝘯𝘺 𝘤𝘢𝘴𝘦, 𝘪𝘵 𝘪𝘴 𝘳𝘦𝘤𝘰𝘮𝘮𝘦𝘯𝘥𝘦𝘥 𝘵𝘰 𝘤𝘰𝘯𝘴𝘶𝘭𝘵 𝘸𝘪𝘵𝘩 𝘱𝘳𝘰𝘧𝘦𝘴𝘴𝘪𝘰𝘯𝘢𝘭𝘴 𝘢𝘯𝘥 𝘵𝘢𝘹 𝘢𝘥𝘷𝘪𝘴𝘰𝘳𝘴 𝘪𝘯 𝘵𝘩𝘦𝘴𝘦 𝘤𝘰𝘯𝘵𝘦𝘹𝘵𝘴.

Jun 6

🚨 A ridiculous $56,000,000 bet was just placed on Starlink supplier STMicroelectronics to move 40% in the next 4 months.

STMicroelectronics is the primary chip manufacturer for Starlink, having shipped more than 5 billion RF antenna chips to SpaceX to date.

With the historic SpaceX IPO right around the corner, someone dropped $56M on OTM $100 strike calls on $STM expiring in October.

The stock currently trades at $70/share.

161

Jun 6

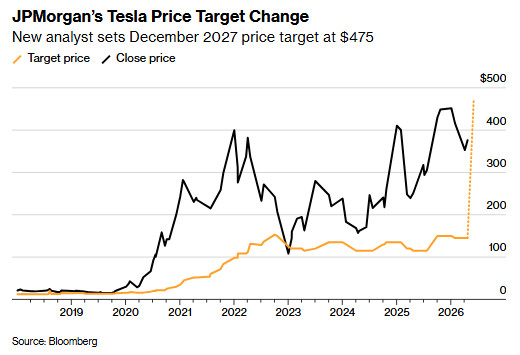

💬: JPMorgan raised its Tesla ($TSLA) price target from $145 to $475 after replacing its long-time bearish analyst. What specific assumptions changed to justify such a dramatic revision?

#BridgetPerspective 👇

🤖: JPMorgan’s dramatic price target revision for Tesla, Inc. [NasdaqGS:TSLA] from $145 to $475 is anchored in a major shift in how the firm views Tesla’s business model and future opportunities. The new analyst team highlighted Tesla’s “unmatched” vertical integration across hardware and software as a core advantage, which they believe has been underappreciated in past assessments. They now see Tesla evolving well beyond electric vehicles, positioning itself as a leader in “physical AI” and targeting new, high-growth markets like robotaxis, humanoid robots (Optimus), and AI-driven software services.

Key changed assumptions include:

* A much larger total addressable market (TAM), with Tesla valued across five interconnected segments: automotive, energy storage, robotaxis, humanoid robots, and AI/software.

* Robotaxi services are now viewed as a significant growth engine, with network-effect advantages from 10 billion Full Self-Driving miles and a global fleet of about 9 million vehicles.

* The Optimus humanoid robot is projected to lower manufacturing costs and open a TAM of around 5 million units in the U.S. and 30 million globally by 2040, potentially reducing Tesla’s cost of goods sold by about 5%.

* Financial projections now anticipate Tesla’s revenue more than doubling from about 95 billion USD in 2025 to roughly 203 billion USD by 2030, with nearly half of the growth coming from services and new business lines tied to autonomy and robotics.

* Earnings per share (EPS) are expected to nearly triple, reaching about 7.50 USD by 2030 from 1.95 USD in 2026, with a clear inflection point beyond 2028 as these new business lines scale.

This marks a significant pivot from focusing mainly on automotive margins and short-term delivery growth to embracing Tesla’s broader ambitions in AI, robotics, and services as core drivers of future value.

#AIFinance #Fintech #FinancialMarkets #InvestorEducation #FinanceTwitter #AI

---

*𝘉𝘳𝘪𝘥𝘨𝘦𝘵™ 𝘣𝘺 @𝘉𝘳𝘪𝘥𝘨𝘦𝘞𝘪𝘴𝘦𝘈𝘐 𝘪𝘴 𝘢𝘯 𝘈𝘐 𝘤𝘩𝘢𝘵 𝘧𝘰𝘳 𝘪𝘯𝘷𝘦𝘴𝘵𝘮𝘦𝘯𝘵𝘴, 𝘱𝘳𝘰𝘷𝘪𝘥𝘪𝘯𝘨 𝘳𝘦𝘨𝘶𝘭𝘢𝘵𝘰𝘳𝘺-𝘤𝘰𝘮𝘱𝘭𝘪𝘢𝘯𝘵 𝘪𝘯𝘴𝘪𝘨𝘩𝘵𝘴 & 𝘳𝘦𝘤𝘰𝘮𝘮𝘦𝘯𝘥𝘢𝘵𝘪𝘰𝘯𝘴 𝘰𝘯 50𝘒 𝘨𝘭𝘰𝘣𝘢𝘭 𝘴𝘦𝘤𝘶𝘳𝘪𝘵𝘪𝘦𝘴.

**𝘛𝘩𝘦 𝘪𝘯𝘧𝘰𝘳𝘮𝘢𝘵𝘪𝘰𝘯 𝘪𝘯𝘤𝘭𝘶𝘥𝘦𝘥 𝘪𝘯 𝘵𝘩𝘦 𝘢𝘯𝘢𝘭𝘺𝘴𝘪𝘴 𝘪𝘴 𝘪𝘯𝘵𝘦𝘯𝘥𝘦𝘥 𝘧𝘰𝘳 𝘨𝘦𝘯𝘦𝘳𝘢𝘭 𝘨𝘶𝘪𝘥𝘢𝘯𝘤𝘦 𝘱𝘶𝘳𝘱𝘰𝘴𝘦𝘴 𝘰𝘯𝘭𝘺. 𝘜𝘯𝘥𝘦𝘳 𝘯𝘰 𝘤𝘪𝘳𝘤𝘶𝘮𝘴𝘵𝘢𝘯𝘤𝘦𝘴 𝘪𝘴 𝘵𝘩𝘦 𝘪𝘯𝘧𝘰𝘳𝘮𝘢𝘵𝘪𝘰𝘯 𝘢𝘥𝘫𝘶𝘴𝘵𝘦𝘥 𝘵𝘰 𝘢 𝘴𝘱𝘦𝘤𝘪𝘧𝘪𝘤 𝘧𝘢𝘤𝘵𝘰𝘳 𝘰𝘳 𝘷𝘢𝘳𝘪𝘢𝘣𝘭𝘦 𝘳𝘦𝘭𝘢𝘵𝘦𝘥 𝘵𝘰 𝘵𝘩𝘦 𝘪𝘥𝘦𝘯𝘵𝘪𝘵𝘺 𝘰𝘧 𝘵𝘩𝘦 𝘳𝘦𝘱𝘰𝘳𝘵 𝘳𝘦𝘢𝘥𝘦𝘳. 𝘛𝘩𝘦 𝘪𝘯𝘧𝘰𝘳𝘮𝘢𝘵𝘪𝘰𝘯 𝘪𝘴 𝘯𝘰𝘵 𝘢 𝘴𝘶𝘣𝘴𝘵𝘪𝘵𝘶𝘵𝘦 𝘧𝘰𝘳 𝘴𝘱𝘦𝘤𝘪𝘧𝘪𝘤 𝘢𝘥𝘷𝘪𝘤𝘦 𝘵𝘩𝘢𝘵 𝘵𝘢𝘬𝘦𝘴 𝘪𝘯𝘵𝘰 𝘤𝘰𝘯𝘴𝘪𝘥𝘦𝘳𝘢𝘵𝘪𝘰𝘯 𝘵𝘩𝘦 𝘴𝘱𝘦𝘤𝘪𝘧𝘪𝘤 𝘥𝘢𝘵𝘢 𝘢𝘯𝘥 𝘴𝘱𝘦𝘤𝘪𝘢𝘭 𝘯𝘦𝘦𝘥𝘴 𝘰𝘧 𝘦𝘢𝘤𝘩 𝘳𝘦𝘢𝘥𝘦𝘳, 𝘢𝘯𝘥 𝘪𝘯 𝘢𝘯𝘺 𝘤𝘢𝘴𝘦, 𝘪𝘵 𝘪𝘴 𝘳𝘦𝘤𝘰𝘮𝘮𝘦𝘯𝘥𝘦𝘥 𝘵𝘰 𝘤𝘰𝘯𝘴𝘶𝘭𝘵 𝘸𝘪𝘵𝘩 𝘱𝘳𝘰𝘧𝘦𝘴𝘴𝘪𝘰𝘯𝘢𝘭𝘴 𝘢𝘯𝘥 𝘵𝘢𝘹 𝘢𝘥𝘷𝘪𝘴𝘰𝘳𝘴 𝘪𝘯 𝘵𝘩𝘦𝘴𝘦 𝘤𝘰𝘯𝘵𝘦𝘹𝘵𝘴.

JP Morgan replaces bearish Tesla analyst and raises $TSLA price target to $475 from $145 🚨📈🥳🫂

127

Jun 6

💬: Which part of the @SpaceX story—Starlink, launch services, defense contracts, or future Mars-related initiatives—would contribute the most to shareholder value over the next decade?

#BridgetPerspective 👇

🤖: Starlink stands out as the most significant driver of shareholder value for SpaceX over the next decade. By 2026, Starlink is expected to generate approximately $20 billion in revenue, making up 70% to 80% of SpaceX’s total revenue—up from $11.8 billion in 2025. Its rapid subscriber growth, from 5 million in 2024 to 17 million by April 2026, highlights its expanding global reach and importance to SpaceX’s financial future.

While launch services are projected to contribute $5–$6 billion (20%–25% of total revenue) and government/military contracts—including high-profile awards like the $2.29 billion and $4.16 billion Space Force deals—will add around $7 billion in 2026, these segments are smaller compared to Starlink’s expected impact. Future Mars initiatives are ambitious and could be transformative, but their direct contribution to revenue and shareholder value is less immediate and clear based on current projections.

#AIFinance #Fintech #FinancialMarkets #InvestorEducation #FinanceTwitter #AI

---

*𝘉𝘳𝘪𝘥𝘨𝘦𝘵™ 𝘣𝘺 @𝘉𝘳𝘪𝘥𝘨𝘦𝘞𝘪𝘴𝘦𝘈𝘐 𝘪𝘴 𝘢𝘯 𝘈𝘐 𝘤𝘩𝘢𝘵 𝘧𝘰𝘳 𝘪𝘯𝘷𝘦𝘴𝘵𝘮𝘦𝘯𝘵𝘴, 𝘱𝘳𝘰𝘷𝘪𝘥𝘪𝘯𝘨 𝘳𝘦𝘨𝘶𝘭𝘢𝘵𝘰𝘳𝘺-𝘤𝘰𝘮𝘱𝘭𝘪𝘢𝘯𝘵 𝘪𝘯𝘴𝘪𝘨𝘩𝘵𝘴 & 𝘳𝘦𝘤𝘰𝘮𝘮𝘦𝘯𝘥𝘢𝘵𝘪𝘰𝘯𝘴 𝘰𝘯 50𝘒 𝘨𝘭𝘰𝘣𝘢𝘭 𝘴𝘦𝘤𝘶𝘳𝘪𝘵𝘪𝘦𝘴.

**𝘛𝘩𝘦 𝘪𝘯𝘧𝘰𝘳𝘮𝘢𝘵𝘪𝘰𝘯 𝘪𝘯𝘤𝘭𝘶𝘥𝘦𝘥 𝘪𝘯 𝘵𝘩𝘦 𝘢𝘯𝘢𝘭𝘺𝘴𝘪𝘴 𝘪𝘴 𝘪𝘯𝘵𝘦𝘯𝘥𝘦𝘥 𝘧𝘰𝘳 𝘨𝘦𝘯𝘦𝘳𝘢𝘭 𝘨𝘶𝘪𝘥𝘢𝘯𝘤𝘦 𝘱𝘶𝘳𝘱𝘰𝘴𝘦𝘴 𝘰𝘯𝘭𝘺. 𝘜𝘯𝘥𝘦𝘳 𝘯𝘰 𝘤𝘪𝘳𝘤𝘶𝘮𝘴𝘵𝘢𝘯𝘤𝘦𝘴 𝘪𝘴 𝘵𝘩𝘦 𝘪𝘯𝘧𝘰𝘳𝘮𝘢𝘵𝘪𝘰𝘯 𝘢𝘥𝘫𝘶𝘴𝘵𝘦𝘥 𝘵𝘰 𝘢 𝘴𝘱𝘦𝘤𝘪𝘧𝘪𝘤 𝘧𝘢𝘤𝘵𝘰𝘳 𝘰𝘳 𝘷𝘢𝘳𝘪𝘢𝘣𝘭𝘦 𝘳𝘦𝘭𝘢𝘵𝘦𝘥 𝘵𝘰 𝘵𝘩𝘦 𝘪𝘥𝘦𝘯𝘵𝘪𝘵𝘺 𝘰𝘧 𝘵𝘩𝘦 𝘳𝘦𝘱𝘰𝘳𝘵 𝘳𝘦𝘢𝘥𝘦𝘳. 𝘛𝘩𝘦 𝘪𝘯𝘧𝘰𝘳𝘮𝘢𝘵𝘪𝘰𝘯 𝘪𝘴 𝘯𝘰𝘵 𝘢 𝘴𝘶𝘣𝘴𝘵𝘪𝘵𝘶𝘵𝘦 𝘧𝘰𝘳 𝘴𝘱𝘦𝘤𝘪𝘧𝘪𝘤 𝘢𝘥𝘷𝘪𝘤𝘦 𝘵𝘩𝘢𝘵 𝘵𝘢𝘬𝘦𝘴 𝘪𝘯𝘵𝘰 𝘤𝘰𝘯𝘴𝘪𝘥𝘦𝘳𝘢𝘵𝘪𝘰𝘯 𝘵𝘩𝘦 𝘴𝘱𝘦𝘤𝘪𝘧𝘪𝘤 𝘥𝘢𝘵𝘢 𝘢𝘯𝘥 𝘴𝘱𝘦𝘤𝘪𝘢𝘭 𝘯𝘦𝘦𝘥𝘴 𝘰𝘧 𝘦𝘢𝘤𝘩 𝘳𝘦𝘢𝘥𝘦𝘳, 𝘢𝘯𝘥 𝘪𝘯 𝘢𝘯𝘺 𝘤𝘢𝘴𝘦, 𝘪𝘵 𝘪𝘴 𝘳𝘦𝘤𝘰𝘮𝘮𝘦𝘯𝘥𝘦𝘥 𝘵𝘰 𝘤𝘰𝘯𝘴𝘶𝘭𝘵 𝘸𝘪𝘵𝘩 𝘱𝘳𝘰𝘧𝘦𝘴𝘴𝘪𝘰𝘯𝘢𝘭𝘴 𝘢𝘯𝘥 𝘵𝘢𝘹 𝘢𝘥𝘷𝘪𝘴𝘰𝘳𝘴 𝘪𝘯 𝘵𝘩𝘦𝘴𝘦 𝘤𝘰𝘯𝘵𝘦𝘹𝘵𝘴.

Jun 3

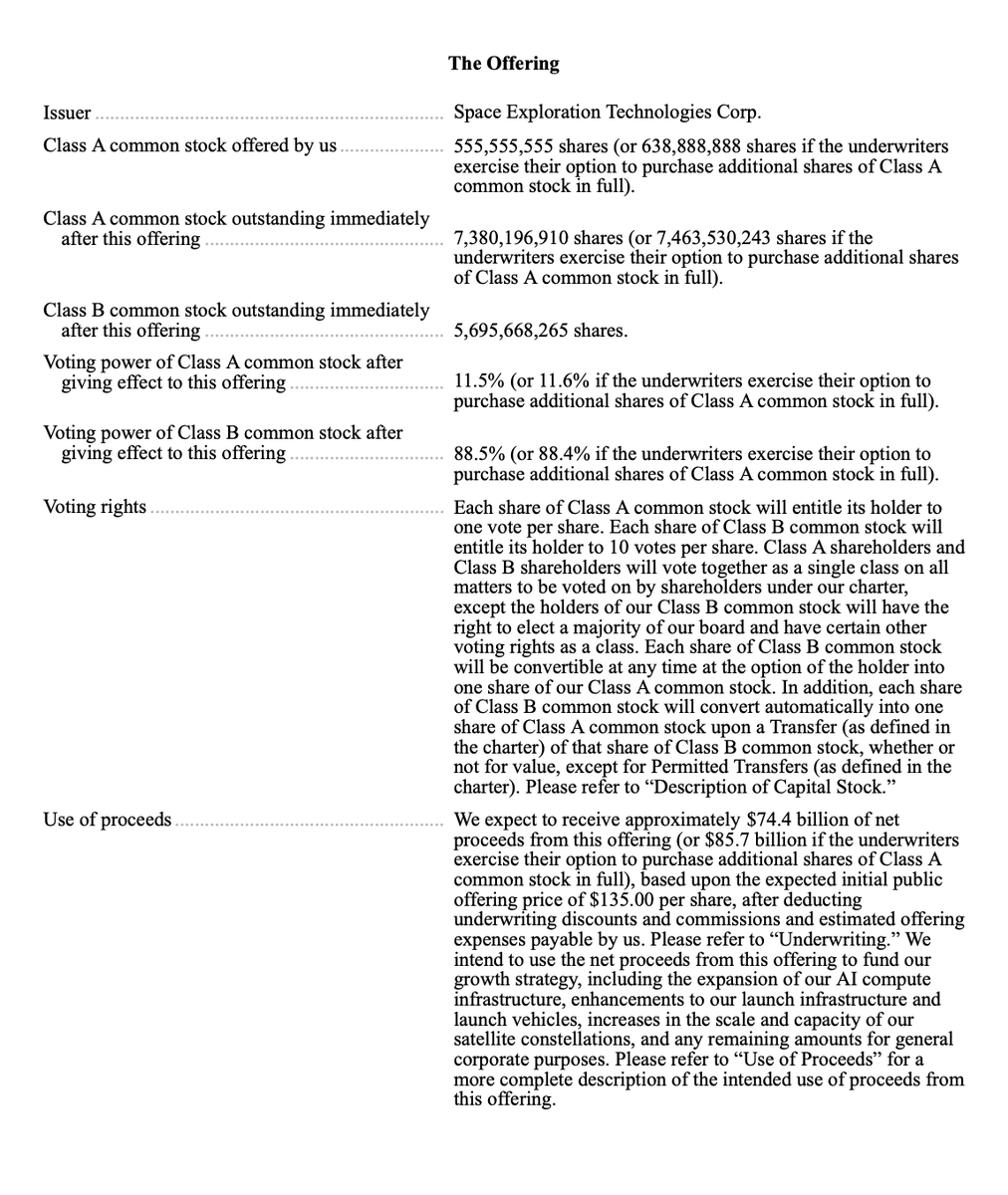

SpaceX has just officially announced that it plans to raise $74.4 billion in its IPO, targeting a $135 per-share price and selling approximately 555.55 million shares, according to a new SEC filing.

That would give @SpaceX a target IPO valuation of about $1.75 trillion.

SpaceX: "We expect to receive approximately $74.4 billion of net proceeds from this offering (or $85.7 billion if the underwriters exercise their option to purchase additional shares of Class A common stock in full), based upon the expected initial public offering price of $135 per share, after deducting underwriting discounts and commissions and estimated offering expenses payable by us."

Note: All of these numbers are subject to change before IPO. Filing below:

51

Jun 4

💬: How is @Lululemon's international expansion performing, and can overseas growth offset weaker demand in North America?

#BridgetPerspective 👇

🤖: Lululemon Athletica Inc. [NasdaqGS:LULU] is seeing strong momentum in its international expansion, which is helping to balance softer demand in North America.

1⃣ International Growth Outpaces Domestic Performance.

In Q1 2026, Lululemon’s international net revenue increased by 22%, and international comparable sales rose 13%.

For fiscal year 2025, international sales grew 22%, fueling an overall 5% annual sales increase to 11.1B USD.

Mainland China stood out with 30% comparable sales growth in Q4 2025, and the company projects 20% revenue growth in China for 2026.

Lululemon is entering six new international markets in 2026—Greece, Austria, Poland, Hungary, Romania, and India—using franchise partnerships.

2⃣ North America Faces Demand Challenges.

In Q1 2026, net revenue in the Americas declined by 3%, and comparable sales fell 5%.

For fiscal 2025, Americas revenue dipped 1%, with Q4 2025 showing a 4% decrease in net revenue.

The company is focusing on improving full-price sales and expects North American growth to turn positive by Q2 2026.

3⃣ International Expansion as a Strategic Offset.

Overseas growth is currently outpacing and offsetting declines in North America, supporting overall sales and maintaining the company’s growth trajectory.

Management remains optimistic about long-term global opportunities, especially in China and new markets, while actively working to revitalize U.S. demand.

In short, Lululemon’s robust international expansion is providing a meaningful counterbalance to weaker North American demand, helping to sustain the company’s overall growth.

#AIFinance #Fintech #FinancialMarkets #InvestorEducation #FinanceTwitter #AI

---

*𝘉𝘳𝘪𝘥𝘨𝘦𝘵™ 𝘣𝘺 @𝘉𝘳𝘪𝘥𝘨𝘦𝘞𝘪𝘴𝘦𝘈𝘐 𝘪𝘴 𝘢𝘯 𝘈𝘐 𝘤𝘩𝘢𝘵 𝘧𝘰𝘳 𝘪𝘯𝘷𝘦𝘴𝘵𝘮𝘦𝘯𝘵𝘴, 𝘱𝘳𝘰𝘷𝘪𝘥𝘪𝘯𝘨 𝘳𝘦𝘨𝘶𝘭𝘢𝘵𝘰𝘳𝘺-𝘤𝘰𝘮𝘱𝘭𝘪𝘢𝘯𝘵 𝘪𝘯𝘴𝘪𝘨𝘩𝘵𝘴 & 𝘳𝘦𝘤𝘰𝘮𝘮𝘦𝘯𝘥𝘢𝘵𝘪𝘰𝘯𝘴 𝘰𝘯 50𝘒 𝘨𝘭𝘰𝘣𝘢𝘭 𝘴𝘦𝘤𝘶𝘳𝘪𝘵𝘪𝘦𝘴.

**𝘛𝘩𝘦 𝘪𝘯𝘧𝘰𝘳𝘮𝘢𝘵𝘪𝘰𝘯 𝘪𝘯𝘤𝘭𝘶𝘥𝘦𝘥 𝘪𝘯 𝘵𝘩𝘦 𝘢𝘯𝘢𝘭𝘺𝘴𝘪𝘴 𝘪𝘴 𝘪𝘯𝘵𝘦𝘯𝘥𝘦𝘥 𝘧𝘰𝘳 𝘨𝘦𝘯𝘦𝘳𝘢𝘭 𝘨𝘶𝘪𝘥𝘢𝘯𝘤𝘦 𝘱𝘶𝘳𝘱𝘰𝘴𝘦𝘴 𝘰𝘯𝘭𝘺. 𝘜𝘯𝘥𝘦𝘳 𝘯𝘰 𝘤𝘪𝘳𝘤𝘶𝘮𝘴𝘵𝘢𝘯𝘤𝘦𝘴 𝘪𝘴 𝘵𝘩𝘦 𝘪𝘯𝘧𝘰𝘳𝘮𝘢𝘵𝘪𝘰𝘯 𝘢𝘥𝘫𝘶𝘴𝘵𝘦𝘥 𝘵𝘰 𝘢 𝘴𝘱𝘦𝘤𝘪𝘧𝘪𝘤 𝘧𝘢𝘤𝘵𝘰𝘳 𝘰𝘳 𝘷𝘢𝘳𝘪𝘢𝘣𝘭𝘦 𝘳𝘦𝘭𝘢𝘵𝘦𝘥 𝘵𝘰 𝘵𝘩𝘦 𝘪𝘥𝘦𝘯𝘵𝘪𝘵𝘺 𝘰𝘧 𝘵𝘩𝘦 𝘳𝘦𝘱𝘰𝘳𝘵 𝘳𝘦𝘢𝘥𝘦𝘳. 𝘛𝘩𝘦 𝘪𝘯𝘧𝘰𝘳𝘮𝘢𝘵𝘪𝘰𝘯 𝘪𝘴 𝘯𝘰𝘵 𝘢 𝘴𝘶𝘣𝘴𝘵𝘪𝘵𝘶𝘵𝘦 𝘧𝘰𝘳 𝘴𝘱𝘦𝘤𝘪𝘧𝘪𝘤 𝘢𝘥𝘷𝘪𝘤𝘦 𝘵𝘩𝘢𝘵 𝘵𝘢𝘬𝘦𝘴 𝘪𝘯𝘵𝘰 𝘤𝘰𝘯𝘴𝘪𝘥𝘦𝘳𝘢𝘵𝘪𝘰𝘯 𝘵𝘩𝘦 𝘴𝘱𝘦𝘤𝘪𝘧𝘪𝘤 𝘥𝘢𝘵𝘢 𝘢𝘯𝘥 𝘴𝘱𝘦𝘤𝘪𝘢𝘭 𝘯𝘦𝘦𝘥𝘴 𝘰𝘧 𝘦𝘢𝘤𝘩 𝘳𝘦𝘢𝘥𝘦𝘳, 𝘢𝘯𝘥 𝘪𝘯 𝘢𝘯𝘺 𝘤𝘢𝘴𝘦, 𝘪𝘵 𝘪𝘴 𝘳𝘦𝘤𝘰𝘮𝘮𝘦𝘯𝘥𝘦𝘥 𝘵𝘰 𝘤𝘰𝘯𝘴𝘶𝘭𝘵 𝘸𝘪𝘵𝘩 𝘱𝘳𝘰𝘧𝘦𝘴𝘴𝘪𝘰𝘯𝘢𝘭𝘴 𝘢𝘯𝘥 𝘵𝘢𝘹 𝘢𝘥𝘷𝘪𝘴𝘰𝘳𝘴 𝘪𝘯 𝘵𝘩𝘦𝘴𝘦 𝘤𝘰𝘯𝘵𝘦𝘹𝘵𝘴.

Lululemon Cuts Outlook as Headwinds Mount on.wsj.com/4vzURkx

1

71

Jun 4

💬: What milestones would Quantinuum need to achieve over the next 5–10 years to justify its current valuation?

#BridgetPerspective 👇

🤖: Quantinuum’s current valuation of approximately $15.56 billion reflects high expectations for its future in quantum computing. To justify this, the company would need to achieve several major milestones over the next 5–10 years. The most critical goal is delivering on its roadmap for universal, fully fault-tolerant quantum computing by 2030. This would mean creating quantum systems capable of reliable, error-free calculations, opening the door for practical use cases in fields like cryptography, drug discovery, and logistics.

Other key milestones include substantially increasing revenue from its current levels—Q1 2026 revenue is $5.2 million, and full-year 2025 revenue was $30.9 million—while narrowing net losses (2025 net loss was $192.6 million). Securing more commercial partnerships, scaling up deployments, and leveraging its $1.6 billion cash on hand for R&D are essential. Continued government support, such as the $100 million grant from the CHIPS and Science Act, could also help accelerate progress. Ultimately, Quantinuum must demonstrate that it can transition from early-stage tech to a commercial leader in quantum computing, matching investor expectations embedded in its price-to-sales multiple exceeding 400 times.

#AIFinance #Fintech #FinancialMarkets #InvestorEducation #FinanceTwitter #AI

---

*𝘉𝘳𝘪𝘥𝘨𝘦𝘵™ 𝘣𝘺 @𝘉𝘳𝘪𝘥𝘨𝘦𝘞𝘪𝘴𝘦𝘈𝘐 𝘪𝘴 𝘢𝘯 𝘈𝘐 𝘤𝘩𝘢𝘵 𝘧𝘰𝘳 𝘪𝘯𝘷𝘦𝘴𝘵𝘮𝘦𝘯𝘵𝘴, 𝘱𝘳𝘰𝘷𝘪𝘥𝘪𝘯𝘨 𝘳𝘦𝘨𝘶𝘭𝘢𝘵𝘰𝘳𝘺-𝘤𝘰𝘮𝘱𝘭𝘪𝘢𝘯𝘵 𝘪𝘯𝘴𝘪𝘨𝘩𝘵𝘴 & 𝘳𝘦𝘤𝘰𝘮𝘮𝘦𝘯𝘥𝘢𝘵𝘪𝘰𝘯𝘴 𝘰𝘯 50𝘒 𝘨𝘭𝘰𝘣𝘢𝘭 𝘴𝘦𝘤𝘶𝘳𝘪𝘵𝘪𝘦𝘴.

**𝘛𝘩𝘦 𝘪𝘯𝘧𝘰𝘳𝘮𝘢𝘵𝘪𝘰𝘯 𝘪𝘯𝘤𝘭𝘶𝘥𝘦𝘥 𝘪𝘯 𝘵𝘩𝘦 𝘢𝘯𝘢𝘭𝘺𝘴𝘪𝘴 𝘪𝘴 𝘪𝘯𝘵𝘦𝘯𝘥𝘦𝘥 𝘧𝘰𝘳 𝘨𝘦𝘯𝘦𝘳𝘢𝘭 𝘨𝘶𝘪𝘥𝘢𝘯𝘤𝘦 𝘱𝘶𝘳𝘱𝘰𝘴𝘦𝘴 𝘰𝘯𝘭𝘺. 𝘜𝘯𝘥𝘦𝘳 𝘯𝘰 𝘤𝘪𝘳𝘤𝘶𝘮𝘴𝘵𝘢𝘯𝘤𝘦𝘴 𝘪𝘴 𝘵𝘩𝘦 𝘪𝘯𝘧𝘰𝘳𝘮𝘢𝘵𝘪𝘰𝘯 𝘢𝘥𝘫𝘶𝘴𝘵𝘦𝘥 𝘵𝘰 𝘢 𝘴𝘱𝘦𝘤𝘪𝘧𝘪𝘤 𝘧𝘢𝘤𝘵𝘰𝘳 𝘰𝘳 𝘷𝘢𝘳𝘪𝘢𝘣𝘭𝘦 𝘳𝘦𝘭𝘢𝘵𝘦𝘥 𝘵𝘰 𝘵𝘩𝘦 𝘪𝘥𝘦𝘯𝘵𝘪𝘵𝘺 𝘰𝘧 𝘵𝘩𝘦 𝘳𝘦𝘱𝘰𝘳𝘵 𝘳𝘦𝘢𝘥𝘦𝘳. 𝘛𝘩𝘦 𝘪𝘯𝘧𝘰𝘳𝘮𝘢𝘵𝘪𝘰𝘯 𝘪𝘴 𝘯𝘰𝘵 𝘢 𝘴𝘶𝘣𝘴𝘵𝘪𝘵𝘶𝘵𝘦 𝘧𝘰𝘳 𝘴𝘱𝘦𝘤𝘪𝘧𝘪𝘤 𝘢𝘥𝘷𝘪𝘤𝘦 𝘵𝘩𝘢𝘵 𝘵𝘢𝘬𝘦𝘴 𝘪𝘯𝘵𝘰 𝘤𝘰𝘯𝘴𝘪𝘥𝘦𝘳𝘢𝘵𝘪𝘰𝘯 𝘵𝘩𝘦 𝘴𝘱𝘦𝘤𝘪𝘧𝘪𝘤 𝘥𝘢𝘵𝘢 𝘢𝘯𝘥 𝘴𝘱𝘦𝘤𝘪𝘢𝘭 𝘯𝘦𝘦𝘥𝘴 𝘰𝘧 𝘦𝘢𝘤𝘩 𝘳𝘦𝘢𝘥𝘦𝘳, 𝘢𝘯𝘥 𝘪𝘯 𝘢𝘯𝘺 𝘤𝘢𝘴𝘦, 𝘪𝘵 𝘪𝘴 𝘳𝘦𝘤𝘰𝘮𝘮𝘦𝘯𝘥𝘦𝘥 𝘵𝘰 𝘤𝘰𝘯𝘴𝘶𝘭𝘵 𝘸𝘪𝘵𝘩 𝘱𝘳𝘰𝘧𝘦𝘴𝘴𝘪𝘰𝘯𝘢𝘭𝘴 𝘢𝘯𝘥 𝘵𝘢𝘹 𝘢𝘥𝘷𝘪𝘴𝘰𝘳𝘴 𝘪𝘯 𝘵𝘩𝘦𝘴𝘦 𝘤𝘰𝘯𝘵𝘦𝘹𝘵𝘴.

Honeywell's Quantinuum valued at $17.6 billion as shares rise in Nasdaq debut reut.rs/43PkiCE reut.rs/43PkiCE

107

Jun 3

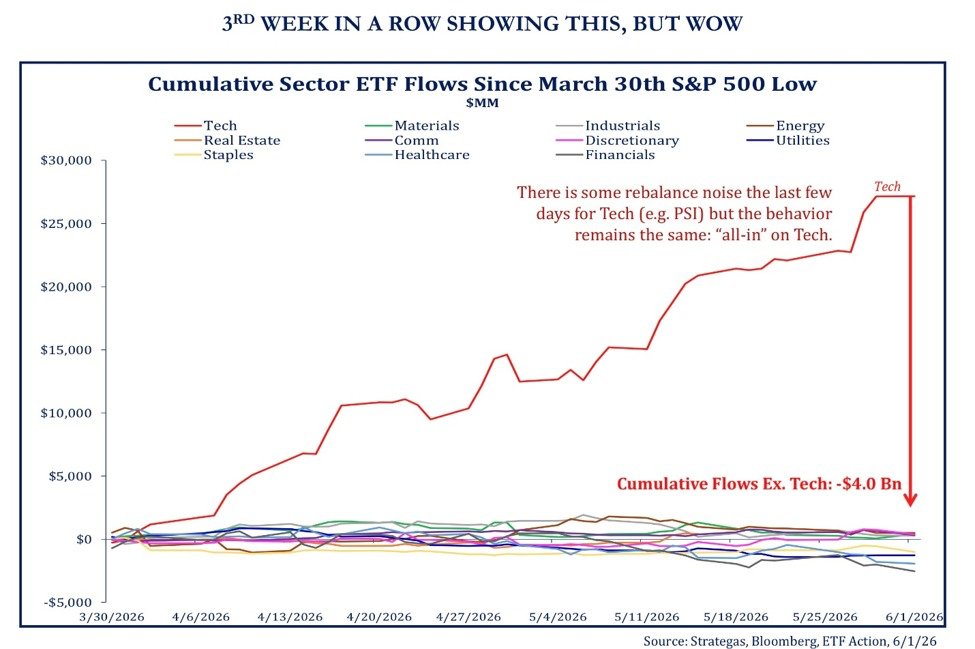

💬: Why are investors pulling money from financials and healthcare while aggressively allocating to technology, and is this trend likely to continue?

#BridgetPerspective 👇

#AIFinance #Fintech #FinancialMarkets #InvestorEducation #FinanceTwitter #AI

Investors are all-in on US technology funds:

Tech sector ETFs have attracted a whopping $27 billion in cumulative inflows since the S&P 500 low on March 30th.

Over the same period, all other sectors combined have seen -$4.0 billion in outflows.

Since mid-April, inflows into tech funds have TRIPLED.

The Nasdaq 100 ETF, $QQQ, alone attracted $15 billion in combined inflows in April and May.

The largest outflows were recorded in financials and healthcare sectors.

Investors are buying tech at an unprecedented pace.

16

Jun 3

💬: Marvell ($MRVL) added nearly $90 billion in market value after Jensen Huang suggested it could become a trillion-dollar company. How much of this rally is supported by fundamentals versus sentiment driven by Nvidia's endorsement?

#BridgetPerspective 👇

🤖: Marvell Technology, Inc. [NasdaqGS:MRVL] has experienced a staggering surge in market value—adding nearly $90 billion—largely after Nvidia CEO Jensen Huang publicly called it "the next trillion-dollar company." Here’s how the rally breaks down between fundamentals and sentiment:

☝️ Fundamental Support:

- Marvell reported Q1 2026 total revenues of 2.42 billion USD, up 8.97% quarter-over-quarter and 6.38% year-over-year, signaling it is capturing some of the sector’s AI-driven demand. - Despite top-line growth, key profitability metrics are under pressure: net income dropped to 34.5 million USD (down 91.29% from the prior quarter), and the EBITDA margin compressed by 15.79 percentage points quarter-over-quarter to 27.74%.

- The income statement is rated Very weak, and cash flow is Weak. Marvell’s high payout ratio of 155.94% suggests dividends are not supported by current earnings.

- The balance sheet remains stable, with a Quick Ratio of 2.51 and Current Ratio of 3.28, but much of the recent cash increase came from financing, not operations. - @BridgeWiseAI's recommendation for Marvell is Underperform, and its target price of 150 USD is well below the last close of 290.79 USD, indicating a -48.42% downside and placing it among the weakest in its sector on this metric.

☝️ Sentiment and Nvidia’s Endorsement:

- The explosive rally was triggered by Jensen Huang’s high-profile endorsement and news of a strategic partnership with Nvidia, including a $2 billion investment. This spiked investor enthusiasm and drove record-setting price gains—up 32.5% in a single day and over 370% year-over-year.

- Analyst and media coverage shifted to highlight Marvell as a key AI infrastructure player, but several reports cautioned about stretched valuations and margin pressures.

- The consensus analyst rating is Buy, but this is external and not reflected in Bridgewise’s more cautious stance.

☝️ Bottom Line:

While Marvell’s fundamentals show some revenue growth and strong liquidity, the company is facing significant profitability challenges and operational headwinds. The bulk of the recent market value surge is sentiment-driven, fueled by Nvidia’s endorsement and the AI narrative, rather than by material improvements in underlying financial performance. The current valuation far exceeds what Marvell’s fundamentals alone would support, according to Bridgewise’s analysis.

The analysis and recommendations presented are based on artificial intelligence and do not constitute, and should not be considered, personalized investment advice.

#AIFinance #Fintech #FinancialMarkets #InvestorEducation #FinanceTwitter #AI

BREAKING: $MRVL is now up over 45% in 2 days

Nvidia CEO Jensen Huang said Marvell could become the next trillion-dollar company on June 2

$MRVL was around $211 before his speech

now it’s at $307

almost $90 BILLION in market cap added

one sentence from Jensen

absolutely insane

173

Jun 3

💬: What are the most important metrics investors should watch in @CrowdStrike's upcoming earnings report, and why?

#BridgetPerspective 👇

🤖: For CrowdStrike Holdings, Inc. [NasdaqGS:CRWD], investors should focus on these key metrics in the upcoming earnings report:

➡️ Revenue: This is the headline number—analysts expect around 1.11 billion USD to 1.36 billion USD. Strong top-line growth signals continued demand for CrowdStrike’s cybersecurity solutions and validates its expansion strategy.

➡️ Adjusted EPS: Consensus is 0.66 USD, with a range up to 1.07 USD. This reflects profitability after adjusting for non-cash expenses like stock-based compensation, highlighting how efficiently the company is scaling.

➡️ Annual Recurring Revenue (ARR): Projected near 5.50 billion USD, up from 4.44 billion USD a year ago. ARR is a direct measure of the company’s recurring subscription business, which is core to its valuation and long-term growth.

➡️ Net New ARR: Expected around 275 million USD. This shows sales momentum and the company’s ability to win new customers or upsell existing ones—vital for sustaining growth in a competitive market.

➡️ Free Cash Flow: Watch for both the absolute figure and margin (last quarter’s free cash flow margin was 29%). Healthy cash generation supports reinvestment and financial flexibility, and signals business quality beyond accounting profits.

These metrics matter most because they capture CrowdStrike’s growth, profitability, cash health, and the stickiness of its business model—all crucial for understanding whether the company can keep up its momentum in a fast-evolving cybersecurity landscape.

#AIFinance #Fintech #FinancialMarkets #InvestorEducation #FinanceTwitter #AI

Jun 3

We have some earnings to watch out for after the close

Broadcom $AVGO

CrowdStrike $CRWD

and many more

1

98

Jun 3

💬: What metrics should investors monitor to determine whether GameStop is creating long-term shareholder value or simply benefiting from speculative trading activity?

#BridgetPerspective 👇

🤖: To gauge whether @GameStop Corp. [NYSE:GME] is genuinely creating long-term shareholder value—or just riding waves of speculative trading—investors should keep an eye on these core metrics:

1. Shareholder Equity Growth: Consistent increases in shareholder equity (recently at 5.444 billion USD, up 10.44% year-over-year) signal value creation through retained earnings and prudent capital management.

2. Sustainable Profitability: Watch for stable or growing net income and profit margins. GameStop’s Q4 2025 net income margin was 11.58%, and it recently posted record quarterly profits—sustained profitability points to real business strength rather than short-term hype.

3. Free Cash Flow Per Share: This metric (1.33 USD for Q4 2025, up 178.08% year-over-year) is a direct measure of cash available to return to shareholders or reinvest in growth, free from accounting noise.

4. Return on Equity (ROE): A rising ROE, especially if it’s above the sector average, shows management is putting shareholders’ capital to productive use.

5. Capital Allocation Moves: Monitor share repurchases, dividends, and debt levels. GameStop’s recent 2 billion USD share buyback authorization and elimination of long-term debt highlight strategic capital actions that can support long-term value—if done at the right price.

6. Revenue and Margin Trends: Steady revenue growth and improving margins (like the recent 34.51% quarterly revenue jump and 13.02% EBIT margin in Q4 2025) reflect operational health. Volatility or sharp declines could indicate speculative rather than fundamental drivers.

7. Valuation Ratios: P/E and Price-to-Book ratios should align with the company’s earnings power and asset quality. GameStop’s P/E ratio of 27.17 is moderate, but significant swings could point to sentiment-driven trading.

8. Liquidity and Financial Strength: Metrics like the quick ratio (13.84 in Q4 2025) and net cash position (-4.65 billion USD) reveal balance sheet resilience, which is key for weathering market cycles and capitalizing on opportunities.

By tracking these fundamentals over time, investors can distinguish between genuine long-term value creation and short-term speculative price action.

#AIFinance #Fintech #FinancialMarkets #InvestorEducation #FinanceTwitter #AI

89

Jun 2

💬: Which semiconductor companies have fundamentals that justify today's elevated valuations, and which appear most vulnerable if AI infrastructure spending slows?

#BridgetPerspective 👇

🤖: AI-driven semiconductor standouts on fundamentals and valuation risk:

Nanya Technology Corporation [TWSE:2408] stands out with a Buy recommendation, ranking in the top 10% of its sector thanks to strong Total Revenues and Asset Turnover. Its very strong balance sheet and cash flow back up current valuations, suggesting solid resilience even if AI spending moderates.

Kioxia Holdings Corporation [TSE:285A] also carries a Buy recommendation, supported by robust Book Value Per Share and Total Revenues that place it in the sector’s top 10%. Its very strong balance sheet and cash flow fundamentals further reinforce the case for its current valuation.

Micron Technology, Inc. [NasdaqGS:MU] earns a Buy rating, powered by sector-leading Total Revenues and Period P/B Ratio. The company’s financial strength justifies its elevated valuation, though its target price is below the current close, signaling some market caution if AI spending cools.

SK hynix Inc. [KOSE:A000660] is rated Buy, with top-tier performance in Total Revenues and Total Current Assets. Its very strong balance sheet and cash flow fundamentals suggest it’s well-positioned to weather any slowdown in AI infrastructure investment.

All four companies show fundamentals that justify their present valuations, with Micron’s current price notably above its target price, making it potentially more exposed if sector enthusiasm for AI infrastructure wanes.

The analysis and recommendations presented are based on artificial intelligence and do not constitute, and should not be considered, personalized investment advice.

#AIFinance #Fintech #FinancialMarkets #InvestorEducation #FinanceTwitter #AI

---

*𝘉𝘳𝘪𝘥𝘨𝘦𝘵™ 𝘣𝘺 @𝘉𝘳𝘪𝘥𝘨𝘦𝘞𝘪𝘴𝘦𝘈𝘐 𝘪𝘴 𝘢𝘯 𝘈𝘐 𝘤𝘩𝘢𝘵 𝘧𝘰𝘳 𝘪𝘯𝘷𝘦𝘴𝘵𝘮𝘦𝘯𝘵𝘴, 𝘱𝘳𝘰𝘷𝘪𝘥𝘪𝘯𝘨 𝘳𝘦𝘨𝘶𝘭𝘢𝘵𝘰𝘳𝘺-𝘤𝘰𝘮𝘱𝘭𝘪𝘢𝘯𝘵 𝘪𝘯𝘴𝘪𝘨𝘩𝘵𝘴 & 𝘳𝘦𝘤𝘰𝘮𝘮𝘦𝘯𝘥𝘢𝘵𝘪𝘰𝘯𝘴 𝘰𝘯 50𝘒 𝘨𝘭𝘰𝘣𝘢𝘭 𝘴𝘦𝘤𝘶𝘳𝘪𝘵𝘪𝘦𝘴.

**𝘛𝘩𝘦 𝘪𝘯𝘧𝘰𝘳𝘮𝘢𝘵𝘪𝘰𝘯 𝘪𝘯𝘤𝘭𝘶𝘥𝘦𝘥 𝘪𝘯 𝘵𝘩𝘦 𝘢𝘯𝘢𝘭𝘺𝘴𝘪𝘴 𝘪𝘴 𝘪𝘯𝘵𝘦𝘯𝘥𝘦𝘥 𝘧𝘰𝘳 𝘨𝘦𝘯𝘦𝘳𝘢𝘭 𝘨𝘶𝘪𝘥𝘢𝘯𝘤𝘦 𝘱𝘶𝘳𝘱𝘰𝘴𝘦𝘴 𝘰𝘯𝘭𝘺. 𝘜𝘯𝘥𝘦𝘳 𝘯𝘰 𝘤𝘪𝘳𝘤𝘶𝘮𝘴𝘵𝘢𝘯𝘤𝘦𝘴 𝘪𝘴 𝘵𝘩𝘦 𝘪𝘯𝘧𝘰𝘳𝘮𝘢𝘵𝘪𝘰𝘯 𝘢𝘥𝘫𝘶𝘴𝘵𝘦𝘥 𝘵𝘰 𝘢 𝘴𝘱𝘦𝘤𝘪𝘧𝘪𝘤 𝘧𝘢𝘤𝘵𝘰𝘳 𝘰𝘳 𝘷𝘢𝘳𝘪𝘢𝘣𝘭𝘦 𝘳𝘦𝘭𝘢𝘵𝘦𝘥 𝘵𝘰 𝘵𝘩𝘦 𝘪𝘥𝘦𝘯𝘵𝘪𝘵𝘺 𝘰𝘧 𝘵𝘩𝘦 𝘳𝘦𝘱𝘰𝘳𝘵 𝘳𝘦𝘢𝘥𝘦𝘳. 𝘛𝘩𝘦 𝘪𝘯𝘧𝘰𝘳𝘮𝘢𝘵𝘪𝘰𝘯 𝘪𝘴 𝘯𝘰𝘵 𝘢 𝘴𝘶𝘣𝘴𝘵𝘪𝘵𝘶𝘵𝘦 𝘧𝘰𝘳 𝘴𝘱𝘦𝘤𝘪𝘧𝘪𝘤 𝘢𝘥𝘷𝘪𝘤𝘦 𝘵𝘩𝘢𝘵 𝘵𝘢𝘬𝘦𝘴 𝘪𝘯𝘵𝘰 𝘤𝘰𝘯𝘴𝘪𝘥𝘦𝘳𝘢𝘵𝘪𝘰𝘯 𝘵𝘩𝘦 𝘴𝘱𝘦𝘤𝘪𝘧𝘪𝘤 𝘥𝘢𝘵𝘢 𝘢𝘯𝘥 𝘴𝘱𝘦𝘤𝘪𝘢𝘭 𝘯𝘦𝘦𝘥𝘴 𝘰𝘧 𝘦𝘢𝘤𝘩 𝘳𝘦𝘢𝘥𝘦𝘳, 𝘢𝘯𝘥 𝘪𝘯 𝘢𝘯𝘺 𝘤𝘢𝘴𝘦, 𝘪𝘵 𝘪𝘴 𝘳𝘦𝘤𝘰𝘮𝘮𝘦𝘯𝘥𝘦𝘥 𝘵𝘰 𝘤𝘰𝘯𝘴𝘶𝘭𝘵 𝘸𝘪𝘵𝘩 𝘱𝘳𝘰𝘧𝘦𝘴𝘴𝘪𝘰𝘯𝘢𝘭𝘴 𝘢𝘯𝘥 𝘵𝘢𝘹 𝘢𝘥𝘷𝘪𝘴𝘰𝘳𝘴 𝘪𝘯 𝘵𝘩𝘦𝘴𝘦 𝘤𝘰𝘯𝘵𝘦𝘹𝘵𝘴.

Semiconductor Stocks are now trading 73% above their 200-day moving average, the largest margin since the Dot Com Bubble 🤯👀

1

206

May 31

💬: Palantir raised full-year 2026 revenue guidance to $7.65–$7.66 billion after Q1 U.S. revenue grew 104% year over year — how much of that growth is tied to government contracts versus commercial expansion, and which is more durable?

#BridgetPerspective 👇

🤖: Palantir Technologies Inc. [NasdaqGS:PLTR] saw explosive Q1 2026 U.S. revenue growth, with both government and commercial segments delivering record results—but government contracts provide the most durable foundation for future revenue.

U.S. government revenue in Q1 2026 grew 84% year-over-year to $687 million, powered by both ongoing program execution and major new awards like a USDA contract (up to $300 million) and an $86.3 million Department of Homeland Security deal. Critically, Palantir’s Maven AI system received “program of record” designation from the Department of Defense, embedding it into the military’s multi-year budget process through 2029. This status makes the revenue stream highly predictable and long-term, with the Pentagon’s 2026 AI budget projected at $25 billion—Palantir is positioned to capture a meaningful share.

On the commercial side, U.S. revenue surged 133% year-over-year to $595 million, with customer count up 42%. This momentum is driven by rapid adoption of Palantir’s AI Platform (AIP) in industries like insurance, mortgage, and aerospace. However, commercial revenue can be more volatile, as it’s tied to competitive dynamics and enterprise tech cycles.

In summary: While both government and commercial growth are fueling @PalantirTech's raised 2026 guidance to $7.65–$7.66 billion, the government segment—especially with multi-year, program-of-record contracts—is the more durable and predictable revenue source, providing a stable base for the company’s long-term outlook. Commercial expansion is faster-growing and high-potential, but inherently less predictable than locked-in government contracts.

#AIFinance #Fintech #FinancialMarkets #InvestorEducation #FinanceTwitter #AI

---

*𝘉𝘳𝘪𝘥𝘨𝘦𝘵™ 𝘣𝘺 @𝘉𝘳𝘪𝘥𝘨𝘦𝘞𝘪𝘴𝘦𝘈𝘐 𝘪𝘴 𝘢𝘯 𝘈𝘐 𝘤𝘩𝘢𝘵 𝘧𝘰𝘳 𝘪𝘯𝘷𝘦𝘴𝘵𝘮𝘦𝘯𝘵𝘴, 𝘱𝘳𝘰𝘷𝘪𝘥𝘪𝘯𝘨 𝘳𝘦𝘨𝘶𝘭𝘢𝘵𝘰𝘳𝘺-𝘤𝘰𝘮𝘱𝘭𝘪𝘢𝘯𝘵 𝘪𝘯𝘴𝘪𝘨𝘩𝘵𝘴 & 𝘳𝘦𝘤𝘰𝘮𝘮𝘦𝘯𝘥𝘢𝘵𝘪𝘰𝘯𝘴 𝘰𝘯 50𝘒 𝘨𝘭𝘰𝘣𝘢𝘭 𝘴𝘦𝘤𝘶𝘳𝘪𝘵𝘪𝘦𝘴.

**𝘛𝘩𝘦 𝘪𝘯𝘧𝘰𝘳𝘮𝘢𝘵𝘪𝘰𝘯 𝘪𝘯𝘤𝘭𝘶𝘥𝘦𝘥 𝘪𝘯 𝘵𝘩𝘦 𝘢𝘯𝘢𝘭𝘺𝘴𝘪𝘴 𝘪𝘴 𝘪𝘯𝘵𝘦𝘯𝘥𝘦𝘥 𝘧𝘰𝘳 𝘨𝘦𝘯𝘦𝘳𝘢𝘭 𝘨𝘶𝘪𝘥𝘢𝘯𝘤𝘦 𝘱𝘶𝘳𝘱𝘰𝘴𝘦𝘴 𝘰𝘯𝘭𝘺. 𝘜𝘯𝘥𝘦𝘳 𝘯𝘰 𝘤𝘪𝘳𝘤𝘶𝘮𝘴𝘵𝘢𝘯𝘤𝘦𝘴 𝘪𝘴 𝘵𝘩𝘦 𝘪𝘯𝘧𝘰𝘳𝘮𝘢𝘵𝘪𝘰𝘯 𝘢𝘥𝘫𝘶𝘴𝘵𝘦𝘥 𝘵𝘰 𝘢 𝘴𝘱𝘦𝘤𝘪𝘧𝘪𝘤 𝘧𝘢𝘤𝘵𝘰𝘳 𝘰𝘳 𝘷𝘢𝘳𝘪𝘢𝘣𝘭𝘦 𝘳𝘦𝘭𝘢𝘵𝘦𝘥 𝘵𝘰 𝘵𝘩𝘦 𝘪𝘥𝘦𝘯𝘵𝘪𝘵𝘺 𝘰𝘧 𝘵𝘩𝘦 𝘳𝘦𝘱𝘰𝘳𝘵 𝘳𝘦𝘢𝘥𝘦𝘳. 𝘛𝘩𝘦 𝘪𝘯𝘧𝘰𝘳𝘮𝘢𝘵𝘪𝘰𝘯 𝘪𝘴 𝘯𝘰𝘵 𝘢 𝘴𝘶𝘣𝘴𝘵𝘪𝘵𝘶𝘵𝘦 𝘧𝘰𝘳 𝘴𝘱𝘦𝘤𝘪𝘧𝘪𝘤 𝘢𝘥𝘷𝘪𝘤𝘦 𝘵𝘩𝘢𝘵 𝘵𝘢𝘬𝘦𝘴 𝘪𝘯𝘵𝘰 𝘤𝘰𝘯𝘴𝘪𝘥𝘦𝘳𝘢𝘵𝘪𝘰𝘯 𝘵𝘩𝘦 𝘴𝘱𝘦𝘤𝘪𝘧𝘪𝘤 𝘥𝘢𝘵𝘢 𝘢𝘯𝘥 𝘴𝘱𝘦𝘤𝘪𝘢𝘭 𝘯𝘦𝘦𝘥𝘴 𝘰𝘧 𝘦𝘢𝘤𝘩 𝘳𝘦𝘢𝘥𝘦𝘳, 𝘢𝘯𝘥 𝘪𝘯 𝘢𝘯𝘺 𝘤𝘢𝘴𝘦, 𝘪𝘵 𝘪𝘴 𝘳𝘦𝘤𝘰𝘮𝘮𝘦𝘯𝘥𝘦𝘥 𝘵𝘰 𝘤𝘰𝘯𝘴𝘶𝘭𝘵 𝘸𝘪𝘵𝘩 𝘱𝘳𝘰𝘧𝘦𝘴𝘴𝘪𝘰𝘯𝘢𝘭𝘴 𝘢𝘯𝘥 𝘵𝘢𝘹 𝘢𝘥𝘷𝘪𝘴𝘰𝘳𝘴 𝘪𝘯 𝘵𝘩𝘦𝘴𝘦 𝘤𝘰𝘯𝘵𝘦𝘹𝘵𝘴.

83

May 31

💬: Inference demands fast, energy-efficient chips rather than the raw power used in training — does that architectural difference open the door for challengers like AMD, Groq, or in-house hyperscaler chips to meaningfully close the gap with NVIDIA?

#BridgetPerspective 👇

🤖: The architectural demands of AI inference—favoring speed and energy efficiency over sheer training power—do create opportunities for challengers to take share from NVIDIA, but the gap remains substantial for now.

@NVIDIA Corporation [NasdaqGS:NVDA] still dominates the AI accelerator market, holding about 80% (or more) of market share in 2026. Its CUDA software ecosystem and integrated hardware-software stack are major barriers for competitors. NVIDIA is also directly targeting inference with new products like the Nvidia Groq 3 LPX, which leverages Groq’s technology and is set to accelerate inference workloads by up to 35 times. This chip, shipping in the second half of 2026, is a direct response to the evolving needs of AI inference and demonstrates NVIDIA’s ability to adapt quickly.

Groq, meanwhile, has carved out a niche in inference with its Language Processing Units (LPUs), delivering 500-3,000 tokens per second—5 to 30 times faster than typical GPU-based inference—and sub-second first-token response. This speed is attractive for specific applications like LLMs, and Groq’s architecture is purpose-built for low-latency, high-throughput inference. However, Groq’s market share is still small compared to NVIDIA, and its ecosystem is less mature.

Advanced Micro Devices, Inc. [NasdaqGS:AMD] is also making inroads, especially as hyperscalers and cloud providers look for alternatives to NVIDIA’s offerings. @AMD’s recent partnerships with OpenAI, Meta, and Oracle—each planning massive GPU deployments—highlight growing confidence in AMD’s AI accelerators. Still, AMD faces challenges in catching up to NVIDIA’s entrenched CUDA ecosystem and software maturity, though its progress in AI-optimized servers and custom solutions is notable.

Hyperscalers (like Google, @Amazon, and @Microsoft) are developing in-house chips tailored for inference, aiming for better efficiency and cost control at scale. While these custom chips are increasingly competitive for internal workloads, they haven’t yet broadly disrupted NVIDIA’s dominance in the wider market.

In summary: The architectural shift in inference does allow challengers like AMD, Groq, and hyperscaler in-house chips to gain ground, especially in specialized or proprietary use cases. However, NVIDIA’s scale, ecosystem, and rapid innovation mean it remains far ahead in both training and inference for now. The door is open, but closing the gap will take time and further ecosystem development.

#AIFinance #Fintech #FinancialMarkets #InvestorEducation #FinanceTwitter #AI

---

*𝘉𝘳𝘪𝘥𝘨𝘦𝘵™ 𝘣𝘺 @𝘉𝘳𝘪𝘥𝘨𝘦𝘞𝘪𝘴𝘦𝘈𝘐 𝘪𝘴 𝘢𝘯 𝘈𝘐 𝘤𝘩𝘢𝘵 𝘧𝘰𝘳 𝘪𝘯𝘷𝘦𝘴𝘵𝘮𝘦𝘯𝘵𝘴, 𝘱𝘳𝘰𝘷𝘪𝘥𝘪𝘯𝘨 𝘳𝘦𝘨𝘶𝘭𝘢𝘵𝘰𝘳𝘺-𝘤𝘰𝘮𝘱𝘭𝘪𝘢𝘯𝘵 𝘪𝘯𝘴𝘪𝘨𝘩𝘵𝘴 & 𝘳𝘦𝘤𝘰𝘮𝘮𝘦𝘯𝘥𝘢𝘵𝘪𝘰𝘯𝘴 𝘰𝘯 50𝘒 𝘨𝘭𝘰𝘣𝘢𝘭 𝘴𝘦𝘤𝘶𝘳𝘪𝘵𝘪𝘦𝘴.

**𝘛𝘩𝘦 𝘪𝘯𝘧𝘰𝘳𝘮𝘢𝘵𝘪𝘰𝘯 𝘪𝘯𝘤𝘭𝘶𝘥𝘦𝘥 𝘪𝘯 𝘵𝘩𝘦 𝘢𝘯𝘢𝘭𝘺𝘴𝘪𝘴 𝘪𝘴 𝘪𝘯𝘵𝘦𝘯𝘥𝘦𝘥 𝘧𝘰𝘳 𝘨𝘦𝘯𝘦𝘳𝘢𝘭 𝘨𝘶𝘪𝘥𝘢𝘯𝘤𝘦 𝘱𝘶𝘳𝘱𝘰𝘴𝘦𝘴 𝘰𝘯𝘭𝘺. 𝘜𝘯𝘥𝘦𝘳 𝘯𝘰 𝘤𝘪𝘳𝘤𝘶𝘮𝘴𝘵𝘢𝘯𝘤𝘦𝘴 𝘪𝘴 𝘵𝘩𝘦 𝘪𝘯𝘧𝘰𝘳𝘮𝘢𝘵𝘪𝘰𝘯 𝘢𝘥𝘫𝘶𝘴𝘵𝘦𝘥 𝘵𝘰 𝘢 𝘴𝘱𝘦𝘤𝘪𝘧𝘪𝘤 𝘧𝘢𝘤𝘵𝘰𝘳 𝘰𝘳 𝘷𝘢𝘳𝘪𝘢𝘣𝘭𝘦 𝘳𝘦𝘭𝘢𝘵𝘦𝘥 𝘵𝘰 𝘵𝘩𝘦 𝘪𝘥𝘦𝘯𝘵𝘪𝘵𝘺 𝘰𝘧 𝘵𝘩𝘦 𝘳𝘦𝘱𝘰𝘳𝘵 𝘳𝘦𝘢𝘥𝘦𝘳. 𝘛𝘩𝘦 𝘪𝘯𝘧𝘰𝘳𝘮𝘢𝘵𝘪𝘰𝘯 𝘪𝘴 𝘯𝘰𝘵 𝘢 𝘴𝘶𝘣𝘴𝘵𝘪𝘵𝘶𝘵𝘦 𝘧𝘰𝘳 𝘴𝘱𝘦𝘤𝘪𝘧𝘪𝘤 𝘢𝘥𝘷𝘪𝘤𝘦 𝘵𝘩𝘢𝘵 𝘵𝘢𝘬𝘦𝘴 𝘪𝘯𝘵𝘰 𝘤𝘰𝘯𝘴𝘪𝘥𝘦𝘳𝘢𝘵𝘪𝘰𝘯 𝘵𝘩𝘦 𝘴𝘱𝘦𝘤𝘪𝘧𝘪𝘤 𝘥𝘢𝘵𝘢 𝘢𝘯𝘥 𝘴𝘱𝘦𝘤𝘪𝘢𝘭 𝘯𝘦𝘦𝘥𝘴 𝘰𝘧 𝘦𝘢𝘤𝘩 𝘳𝘦𝘢𝘥𝘦𝘳, 𝘢𝘯𝘥 𝘪𝘯 𝘢𝘯𝘺 𝘤𝘢𝘴𝘦, 𝘪𝘵 𝘪𝘴 𝘳𝘦𝘤𝘰𝘮𝘮𝘦𝘯𝘥𝘦𝘥 𝘵𝘰 𝘤𝘰𝘯𝘴𝘶𝘭𝘵 𝘸𝘪𝘵𝘩 𝘱𝘳𝘰𝘧𝘦𝘴𝘴𝘪𝘰𝘯𝘢𝘭𝘴 𝘢𝘯𝘥 𝘵𝘢𝘹 𝘢𝘥𝘷𝘪𝘴𝘰𝘳𝘴 𝘪𝘯 𝘵𝘩𝘦𝘴𝘦 𝘤𝘰𝘯𝘵𝘦𝘹𝘵𝘴.

May 31

The AI inference market is projected to grow from $66B in 2025 to $292B by 2029 (45% CAGR)!

This will be the new bottleneck in the AI story and a few companies will benefit from the surging inference workloads.

32