Cetera Investment Management LLC, owned by @CeteraFinancial, provides market perspectives, portfolio guidance & other investment advice to its affiliated firms.

Joined November 2013

- Tweets 4,670

- Following 680

- Followers 3,017

- Likes 258

3,827 Photos and videos

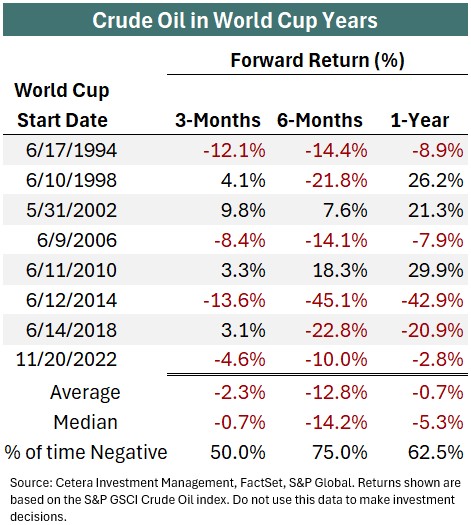

History shows crude oil tends to dip after the FIFA World Cup kicks off, with prices falling 75% of the time within 6 months, averaging a 12.8% decline. While likely coincidental, lower oil could mean relief at the pump for consumers.

1

108

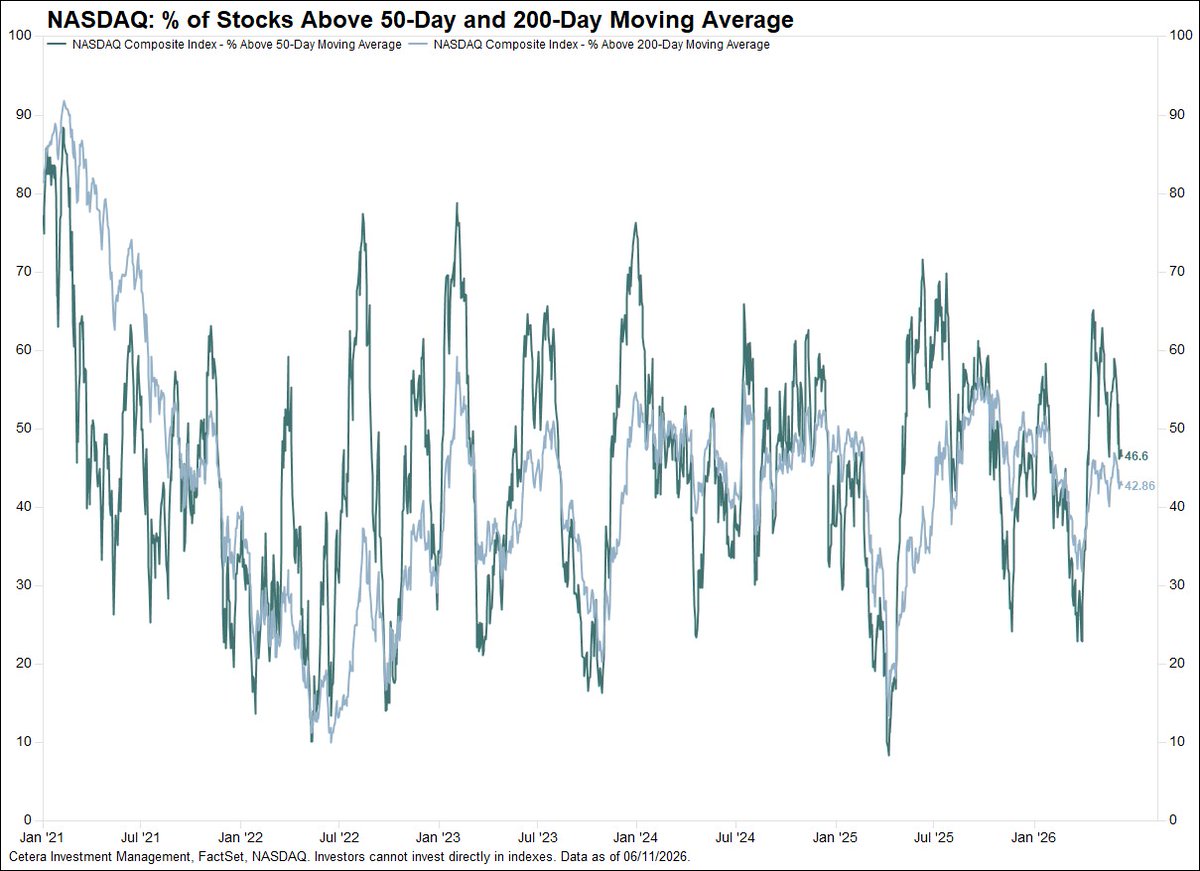

The tech-heavy Nasdaq Composite is up 24% since its late March correction low, but fewer than half of stocks in the index are above their 50-day and 200-day moving averages, signaling weak breadth.

1

3

101

Economic data is outpacing expectations at an accelerating pace, with the Economic Surprise Index near its highest level since October 2023. This could support an uptick in GDP growth following consecutive sub-2% readings.

1

3

114

The Producer Price Index (PPI) rose 1.1% in May, exceeding expectations of 0.7%. The annual rate climbed to a 42-month high of 6.5%. Final demand goods increased 2.8% M/M, the sharpest increase on record (since 2009), with energy as the primary driver.

1

6

103

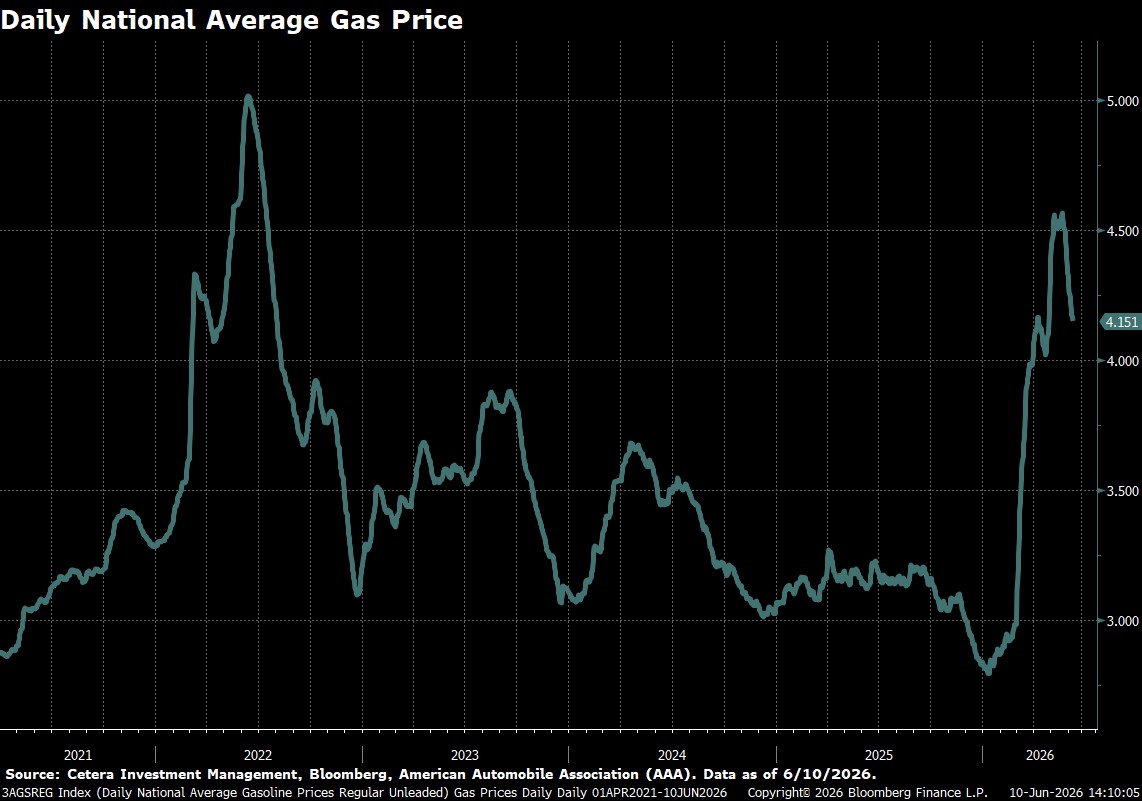

Energy-driven inflation pressures are showing signs of easing. The national average gas price of $4.15/gallon is 9% lower than 3 weeks ago. Fuel prices remain elevated versus pre-Iran war levels but have declined in recent weeks.

1

6

155

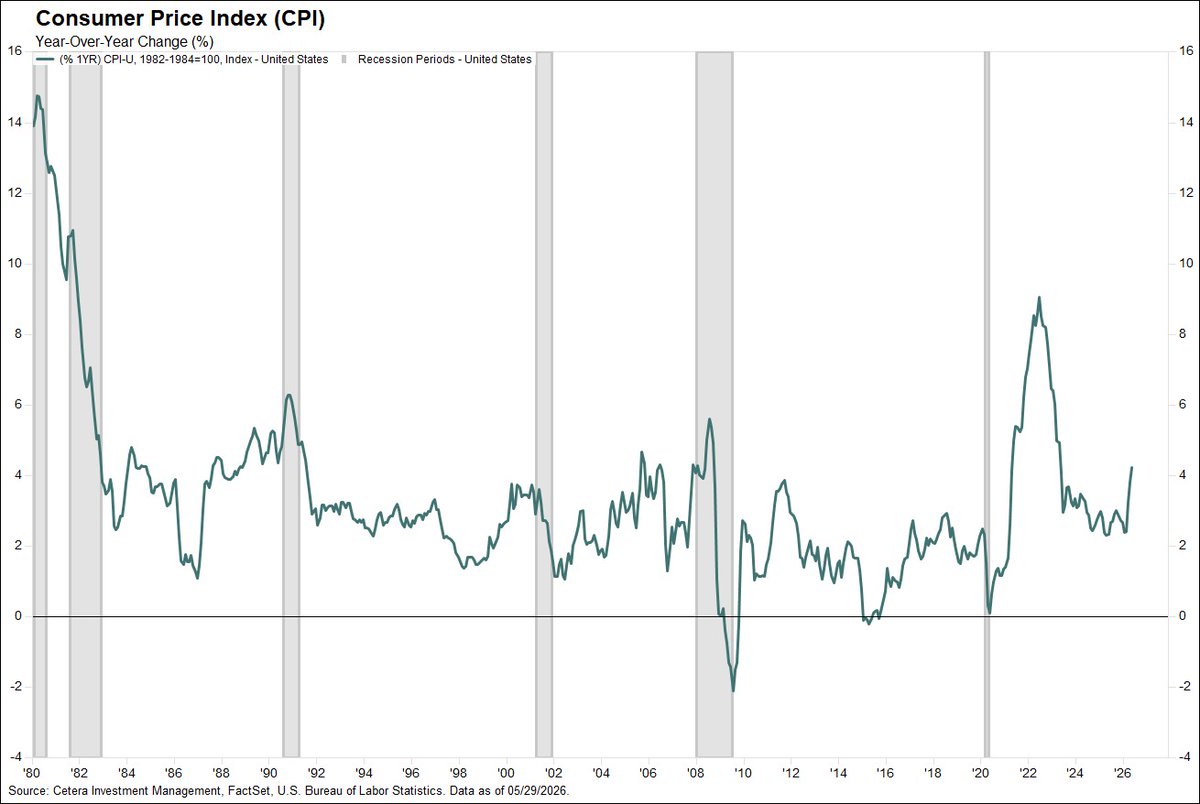

Headline CPI inflation rose 0.5% M/M in May, in line with expectations, while the annual rate of 4.2% was the highest in 3 years. Energy prices accounted for a large share of the overall increase. Core CPI rose 0.2% M/M, below expectations of 0.3%.

5

114

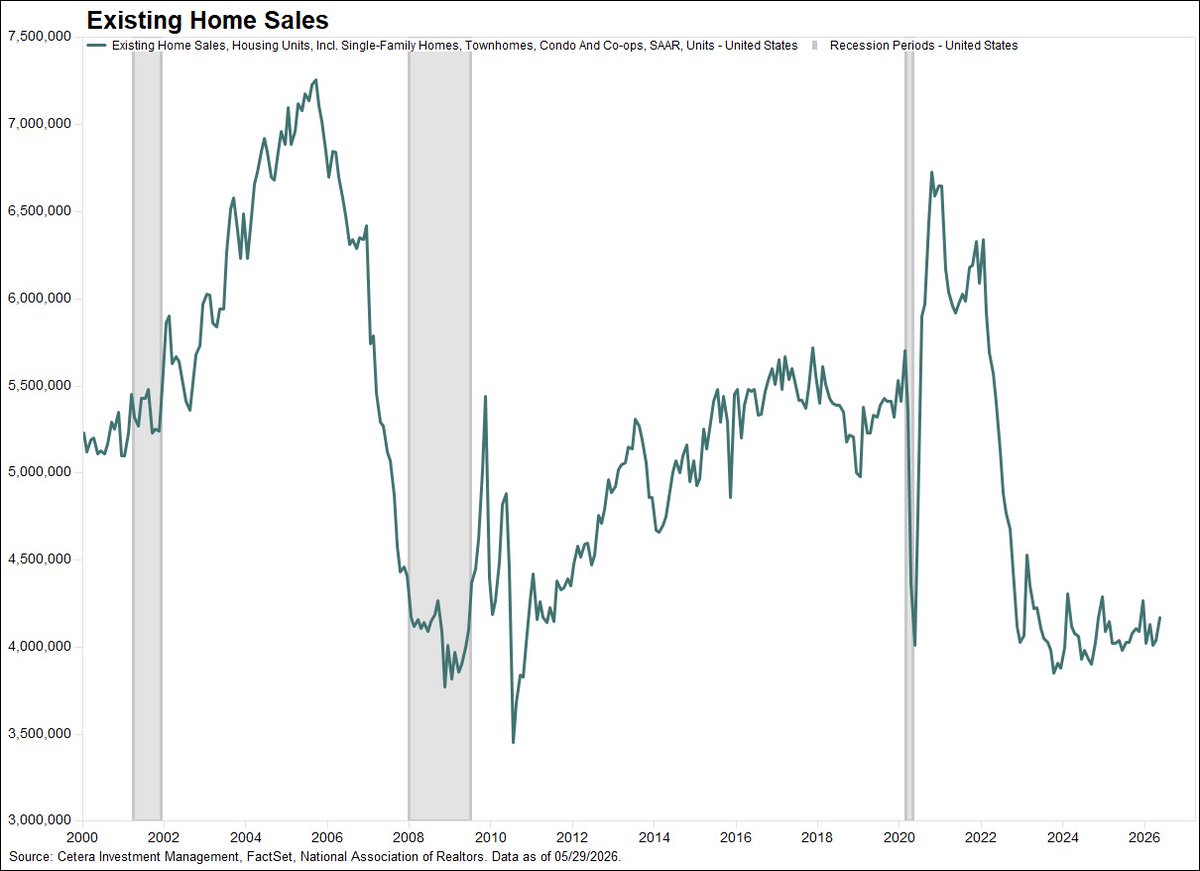

Existing home sales rose 3.2% in May to an annualized pace of 4.17 million, the highest level this year. While overall activity remains low, increasing inventory and improved labor conditions helped boost home purchases.

1

3

142

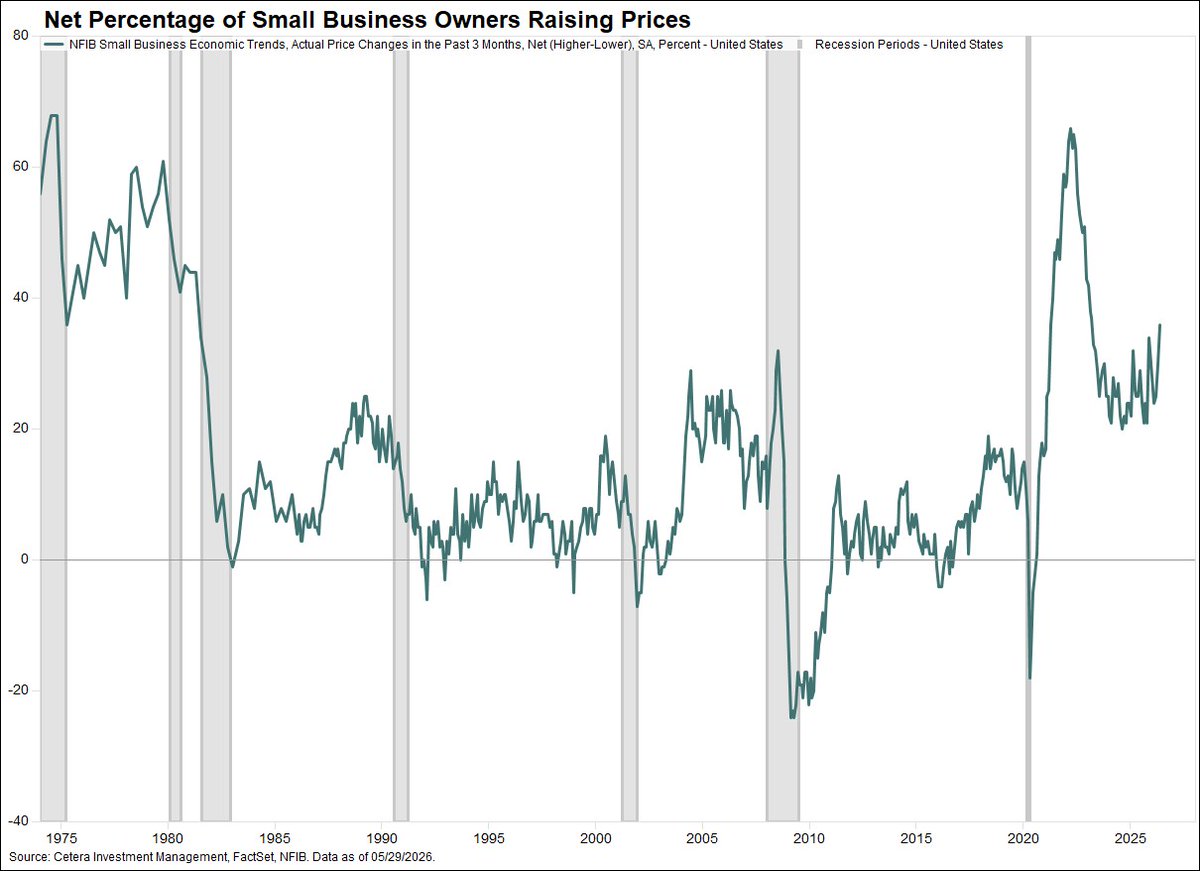

The @NFIB Small Business Optimism Index fell to a 19-month low of 95.3, reflecting increasing uncertainty. Hiring plans declined to their lowest level since May 2020, while the percentage of owners raising prices reached its highest since March 2023.

1

4

169

Markets hit pause after a 9-week rally, with a Friday pullback shifting focus to a busy week ahead, including the SpaceX IPO, fresh inflation data, and Middle East developments. Chief Market Strategist @btklimke discusses the Fed’s next move and what is driving the markets and what’s just amplifying the noise in #TheWeekAhead cetera.com/research-and-insi…

1

2

2

11,732

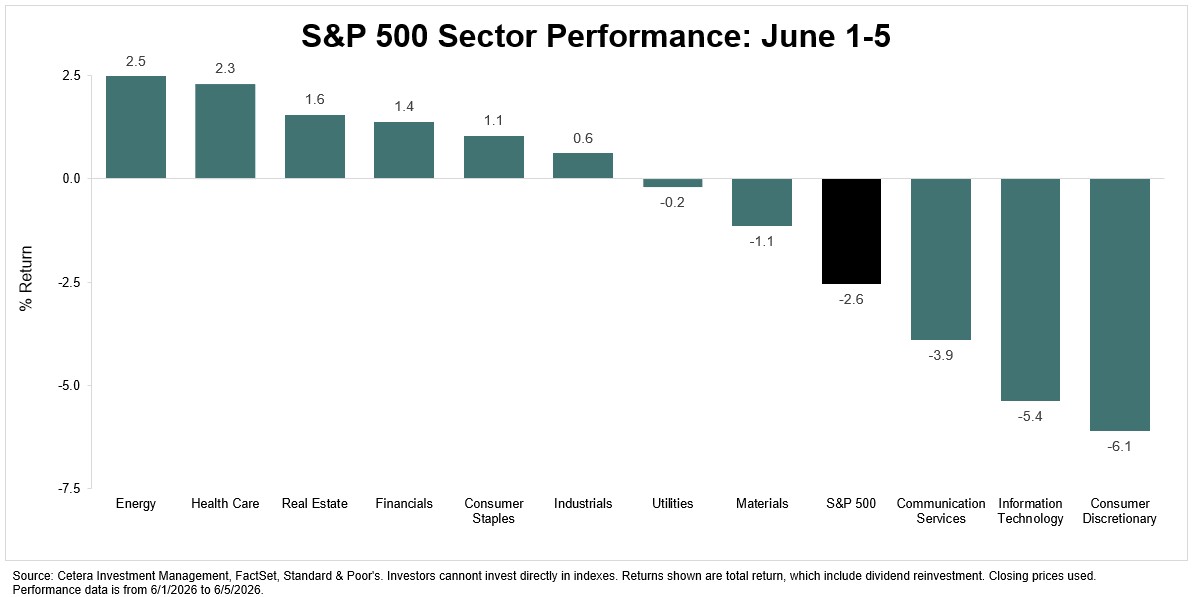

The S&P 500’s 9-week streak of gains ended with a 2.6% decline last week. Despite the pullback, 6 of 11 sectors posted gains, with losses concentrated in Communication Services (-3.9%), Technology (-5.4%), and Consumer Discretionary (-6.1%).

1

4

231

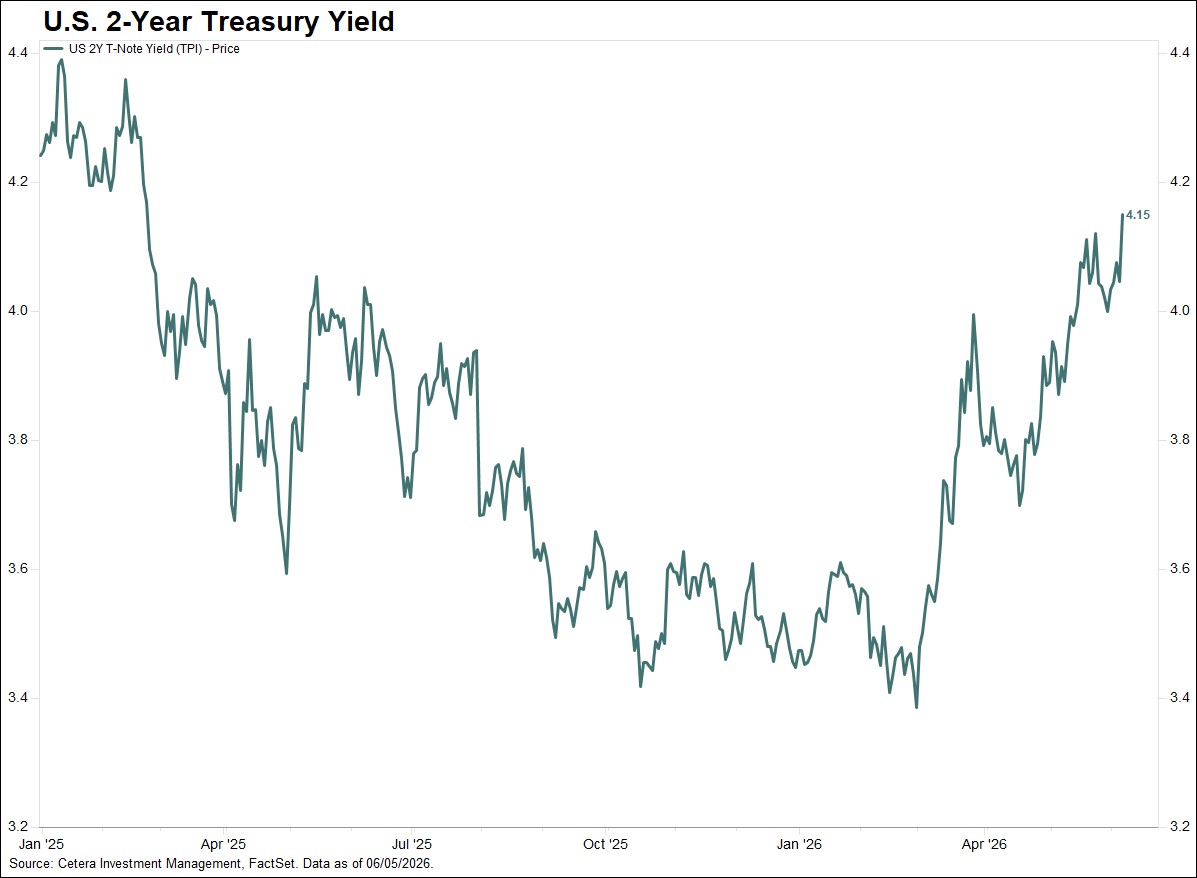

Treasury yields moved higher after this morning’s strong jobs report. The 2-year yield has risen from 3.4% in late February to a 16-month high of 4.15%, suggesting that the bond market is shifting toward a more hawkish Fed policy outlook.

2

4

230

No team wins with just one superstar, and no portfolio should bet on just one market. With the World Cup as a backdrop, we explain why portfolios with global exposure are better equipped to adapt, adjust, and stay competitive no matter how the game changes. cetera.com/playing-on-a-glob…

1

4

153

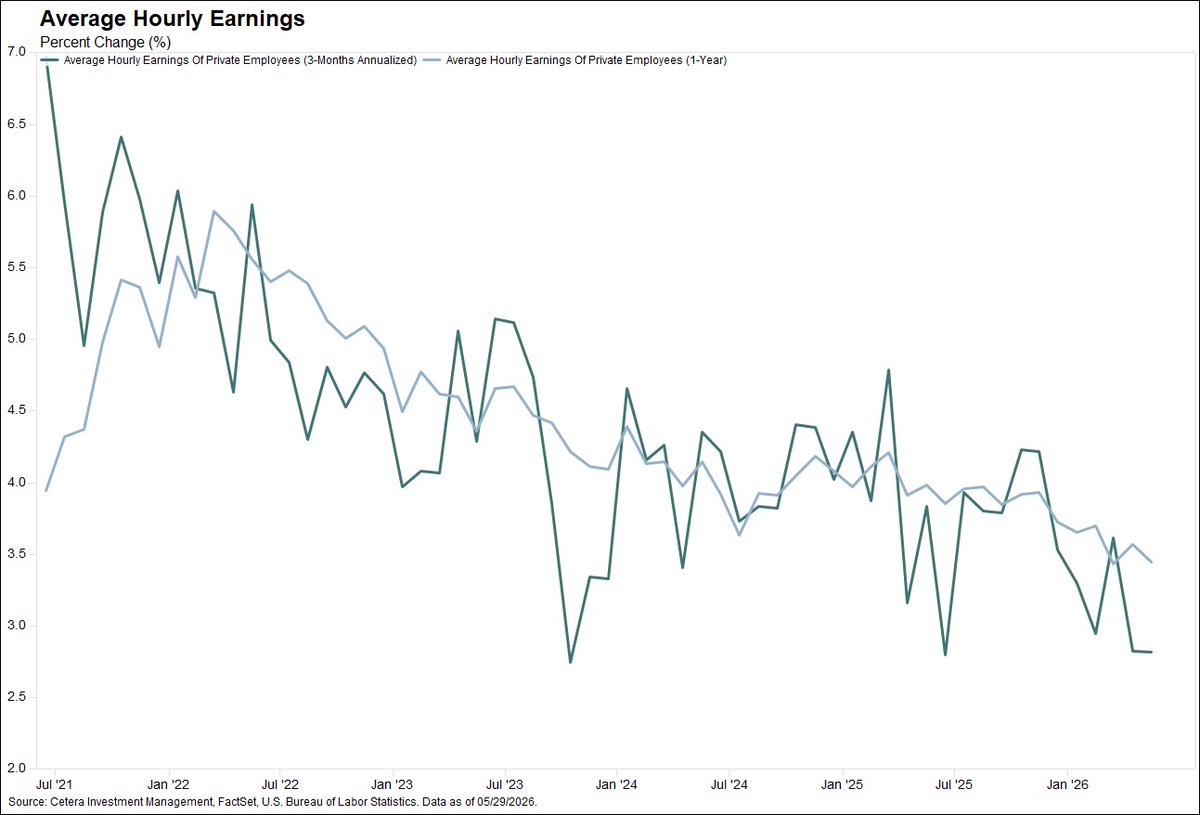

Wage growth has slowed to 3.4% Y/Y, while the 3-month annualized pace is just 2.8%. Despite firmer inflation this year, wage pressures remain contained, which may support a more patient Fed.

1

3

141

Nonfarm payrolls increased by 172K in May, outpacing expectations of 85K, while the prior 2 months were revised higher by 93K. Total employment has risen 569K over the first 5 months of 2026 compared to a decline of 110K in the final 5 months of 2025.

5

164

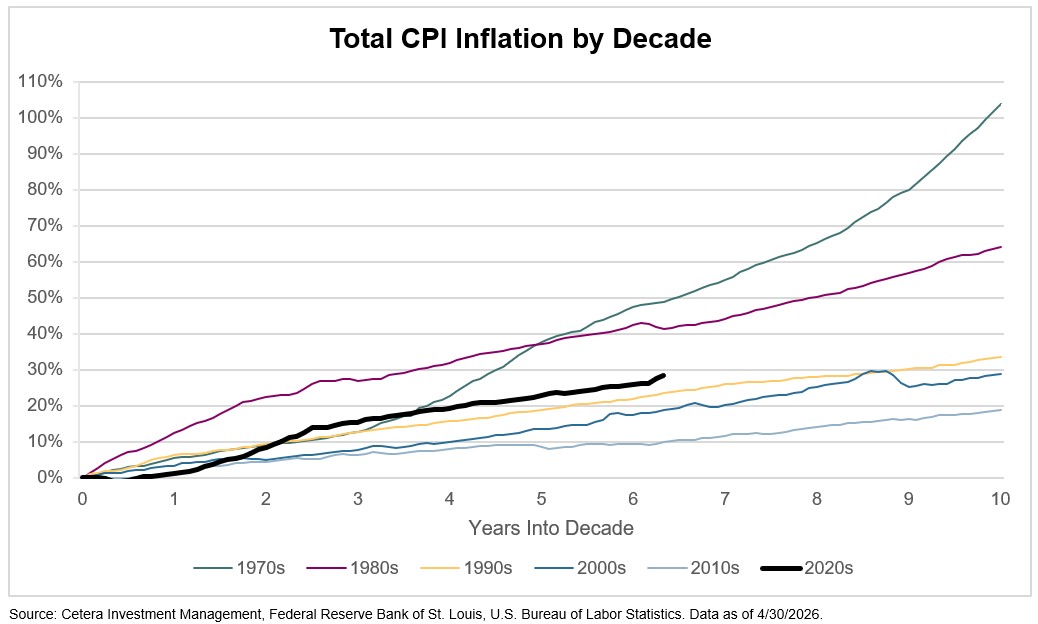

Consumer prices are up 28% this decade, but the pace remains below the 1970s and 1980s when inflation had already exceeded 40% at a similar point. By comparison, the consumer price index was up 104% over the full decade in the 1970s.

1

3

180

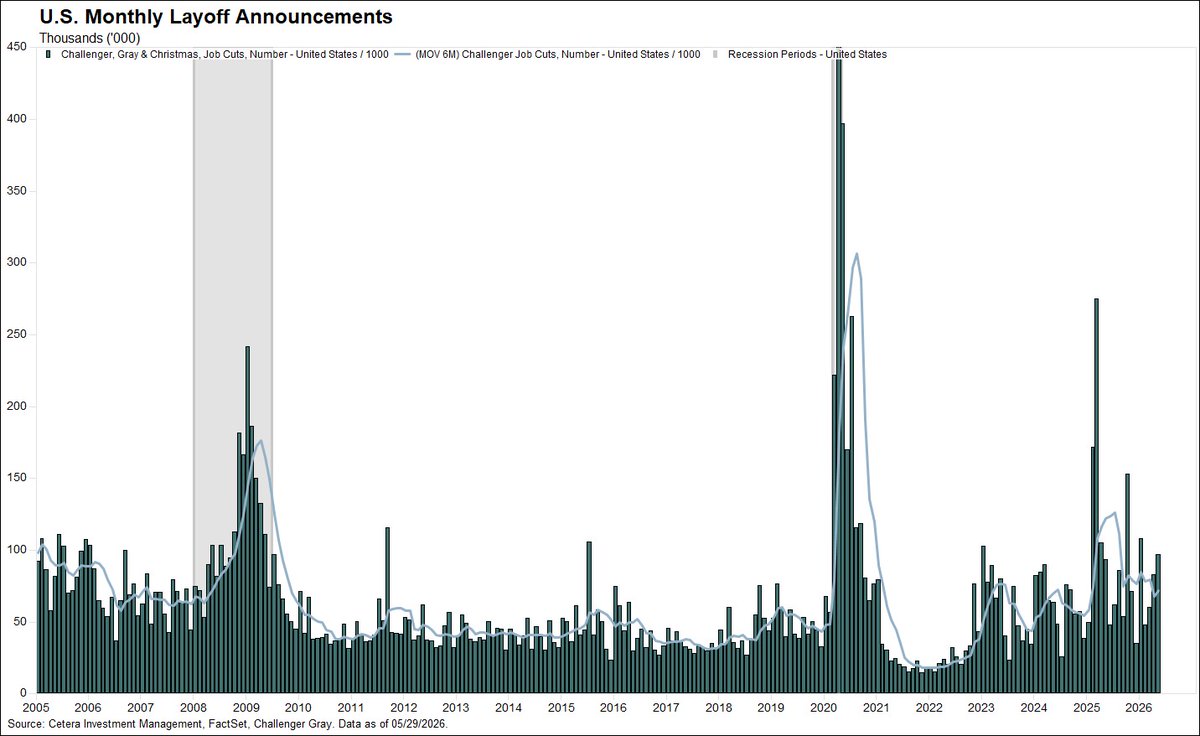

US layoff announcements climbed to 97K in May, marking the 2nd highest May reading since the GFC, surpassed only by May 2020. The increase was driven by the Tech sector, which accounted for 38K job cuts. Positively, hiring plans are higher YTD vs 2025.

2

3

189

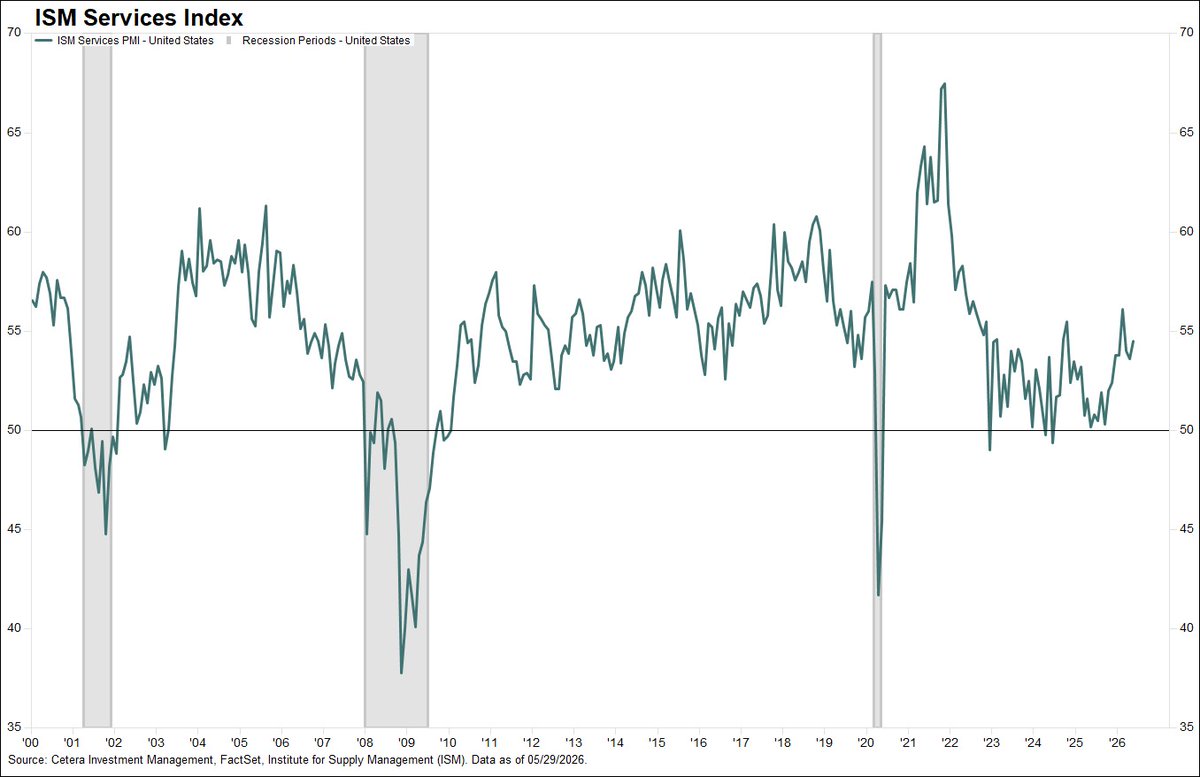

Service activity advanced in May, with the ISM Services Index edging higher to 54.5, near its long-term average. While new orders expanded, price pressures continued to mount. The prices paid index reached its highest level since August 2022.

1

3

165

Private payrolls increased by 122K in May per ADP, slightly ahead of expectations ( 117K). Hiring was the strongest in 16 months and relatively broad-based across firm sizes and industries. Education and health services ( 57K) led overall job gains.

1

3

168

Job openings rose to a 7-month high of 7.62 million in April, well above expectations of 6.8 million. Openings exceeded job seekers, indicating rising labor demand. Overall, labor market data has stabilized in recent months following weaker trends in 2025.

1

4

239

The S&P 500 has notched all-time highs in each of the last 5 trading days and 23 times in 2026, after 96 record closes over the prior two years. Yet sentiment remains cautious, with bears outnumbering bulls in the latest AAII weekly survey.

1

5

233