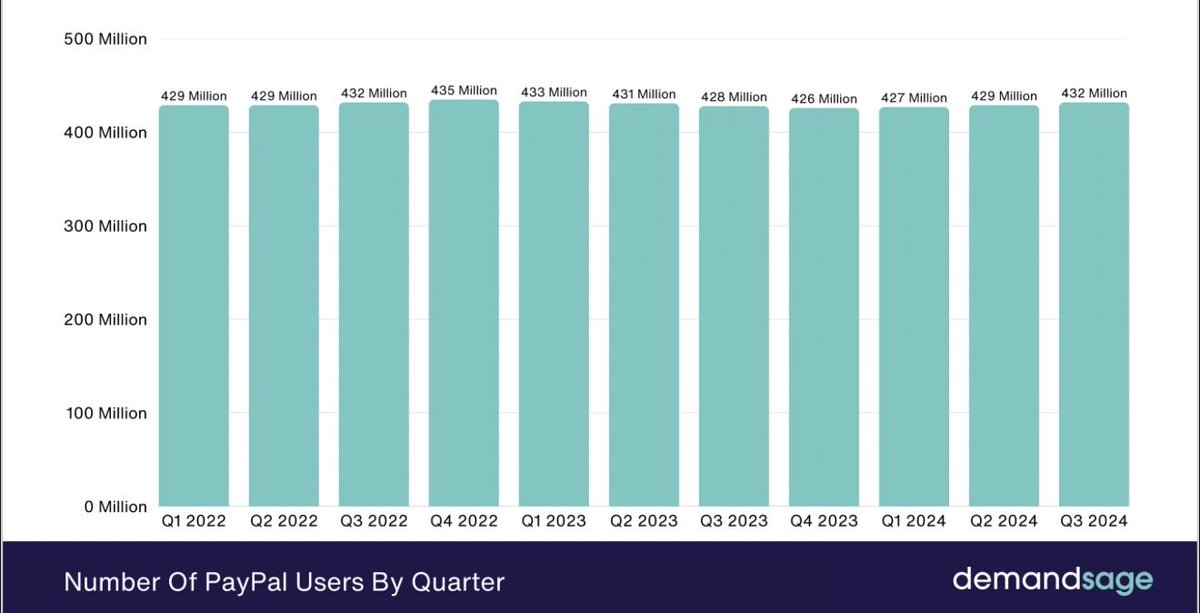

1,206 Photos and videos

great and true words from David Marcus about his frustrated depature from #PayPal 12 years ago. I made similar experience and left for the same reasons a little earlier… #payments

Feb 3

A few thoughts about PayPal, nearly 12 years after I left.

I woke up this morning to dozens of messages from former PayPal colleagues. It pushed me to finally speak up.

I never spoke publicly about the company after I left. Part of that was loyalty to John Donahoe, who gave me an unlikely opportunity, handing the reins of PayPal to a startup guy who, on paper, had no business running a then 15,000-person organization. But part of it was something else: I had left. I chose not to stay and fight for the changes I believed in. Speaking from the sidelines felt like armchair commentary. Easy opinions without the burden of execution. So I stayed quiet.

But twelve years of silence is long enough. And today's news makes it clear the pattern I've watched unfold isn't self-correcting.

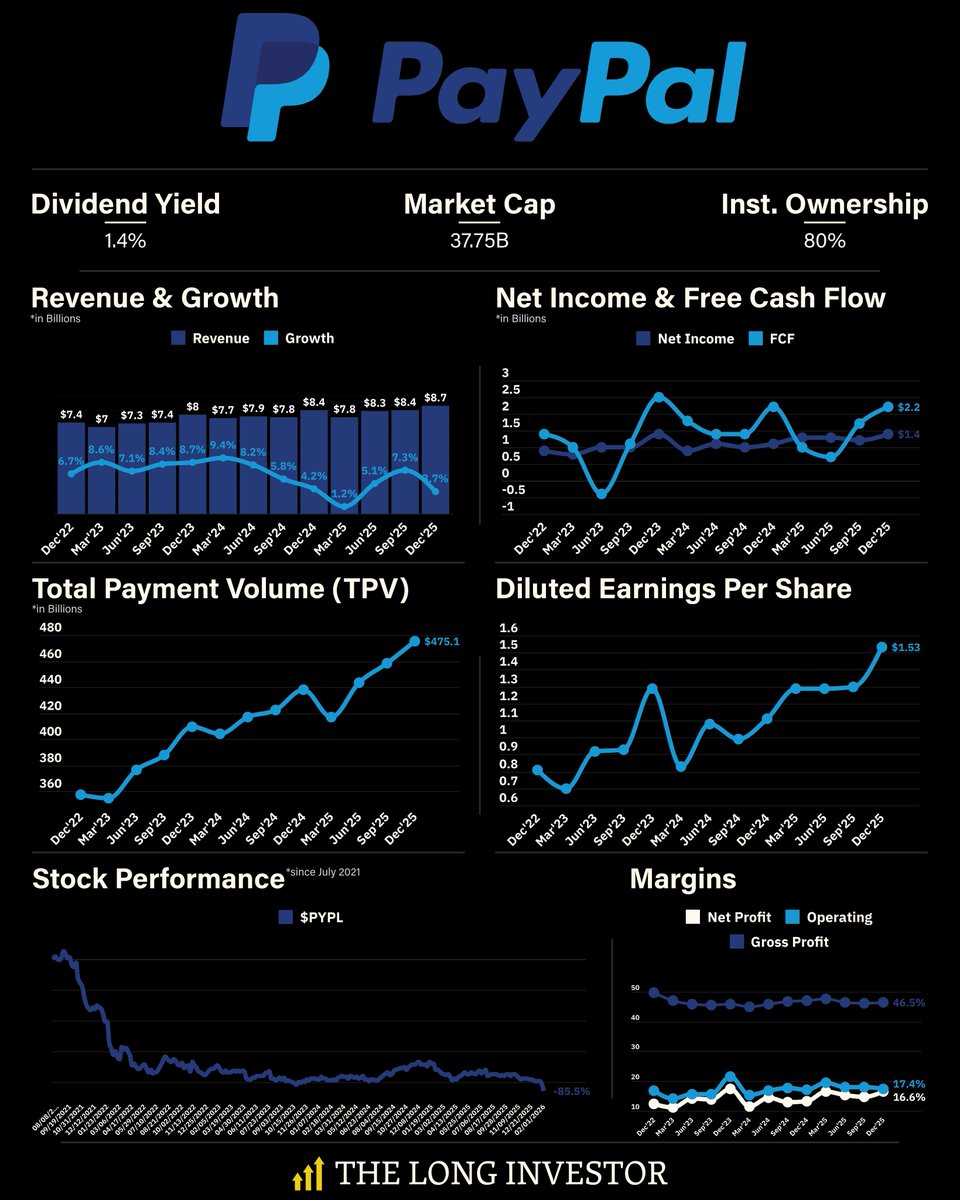

I left PayPal in 2014 because I was deeply frustrated. We had executed a silent turnaround of a company that had lost its soul. We brought back engineering talent, shipped good products quickly, and acquired Braintree and Venmo. The company was on a tear. So much so that Carl Icahn felt compelled to accumulate a position in eBay and push for a PayPal spinoff. At the time, eBay decided to fight Icahn.

It was a difficult period for me, caught between what I felt was right for PayPal and my loyalty to the eBay team.

This is when Mark Zuckerberg approached me to join Facebook. The combination of his conviction that messaging would become foundational, the appeal of going back to building products at scale, and my growing exhaustion with the internal politics at PayPal and eBay eventually convinced me to leave and join one of the best teams in the world, one I had admired for a long time.

In the summer of 2014, I met John in a café in Portola Valley and told him I had decided to leave. During that conversation, he told me that Icahn had effectively won the fight, that PayPal was going to become an independent company, and he tried to convince me to stay on as CEO, but I had already said yes to Mark, and my word is my bond. There was no turning back.

After my departure, the board scrambled to find a replacement, and it took a few months for them to land on Dan Schulman. The leadership style shifted from product-led to financially-led. Over time, product conviction gave way to financial optimization.

Much of the momentum we had created still persisted and carried the company forward, mainly driven by Bill Ready, who came over in the Braintree acquisition and rose to COO. Under his leadership, Venmo grew exponentially, and total payment volume (TPV) accelerated quickly. But the shift under Schulman became more pronounced after Bill's departure at the end of 2019. With him went the product conviction that had defined the post-spinoff momentum. Then, for a period, COVID-fueled online shopping hid a lot of the company's new weaknesses.

During that period, the company made a fundamental miscalculation: it optimized for payment volume instead of margin and differentiation. It leaned into unbranded checkout, where PayPal had the least leverage, instead of branded checkout, where the margin, data, and customer relationship actually lived.

Visa masterfully structured a deal that effectively ended PayPal's ability to steer customers toward bank-funded transactions, which had been a core driver of PayPal's economics. Not long after, PayPal lost a significant portion of eBay's volume. Over time, it saw its share of checkout among its most profitable customers steadily erode as Apple Pay and others continued to execute well.

The same pattern repeated itself across lending, buy-now-pay-later (BNPL), and new rails.

On lending, PayPal missed the opportunity to turn it into a platform weapon. Products like Working Capital were conservative, short-duration, and optimized for loss minimization. Lending never became programmable, never became identity-driven, and never became a reason for merchants or consumers to choose PayPal over something else.

The missed opportunity in BNPL was even more striking. Klarna, Affirm, and Afterpay didn't just offer installment payments, they built consumer finance brands, persistent credit identities, and new shopping behaviors. PayPal saw the BNPL turn, entered the market, and had every advantage: distribution, trust, and merchant relationships. But BNPL was treated as a defensive checkout feature rather than an offensive category. There was no attempt to turn it into a core consumer relationship, no super-app behavior, and no meaningful differentiation for merchants. Others built platforms, PayPal added a feature.

The failure to lean into building and owning new rails followed the same logic. After the spinoff, PayPal had a once-in-a-generation opportunity to build a global, at scale payment network. Instead, the company focused on building on top of existing networks and third-party rails.

More recently, that mindset carried over to PYUSD. Technically, the product was sound. Strategically, it launched without a compelling transactional reason to exist. PYUSD had distribution, but no organic demand. It was not embedded deeply enough into flows to become a true settlement layer, a cross-border merchant rail, or a programmable money primitive. It sat adjacent to the product instead of inside the core of it.

Acquisitions during this period followed a similar pattern. Honey was not a strategic acquisition for PayPal. It added activity, but not leverage. It lived outside the transaction, monetized affiliate economics rather than payment economics, and never meaningfully strengthened PayPal's control of the customer or the checkout moment. Xoom solved a real problem in remittances, but it never compounded PayPal's advantage. It scaled volume without changing the underlying rails, identity graph, or settlement model, and as importantly, it didn’t cater to a high-value, high-margin customer archetype.

None of these were bad companies. They were just a wrong fit for PayPal and became unnecessary distractions.

The board eventually recognized the problem. In 2023, they brought in Alex Chriss, an Intuit veteran with a strong product background, explicitly to restore product conviction. It was the right instinct.

But Alex came from software, not payments. He understood SMB product development. He didn't have the muscle memory for transaction economics, network effects, or settlement infrastructure.

In hindsight, he also made an error: clearing out much of the leadership team that understood payments deeply. Executives with years of institutional knowledge departed within his first year.

This morning, Alex was removed as CEO. Branded checkout grew 1% last quarter. The board tapped another operator, Enrique Lores, the former HP CEO who's been on the PayPal board for five years.

I don’t know Enrique. And he might be a great leader, but on paper at least, he’s a hardware executive. For a payments company.

The common thread through all of this is incentive design. Once PayPal became independent, short/medium-term predictability beat long-term vision and ambition. Stock performance mattered more than platform risk and network opportunity. Financial optimization replaced product conviction.

I'm not claiming I would have made every call differently. Running a public company at scale involves tradeoffs I didn't have to make after I left. But the pattern, choosing predictability over platform risk, again and again, was a choice, not an inevitability.

Over time, the company that had every advantage and could’ve become the most consequential and relevant payments company of our time, lost its mojo, its product edge, and its ability to compete in a market that’s being rewired and reinvented in front of our eyes.

That's the part that's hardest to watch for a company I care so deeply about.

1

2

792

Jochen Siegert retweeted

Feb 2

Erst wenn der letzte Industriearbeitsplatz verlagert, das letzte Unternehmen liquidiert, der letzte Selbständige aufgegeben hat, werdet ihr merken, dass man vom öffentlichen Dienst nicht leben kann.

237

947

4,314

63,638

Jan 19

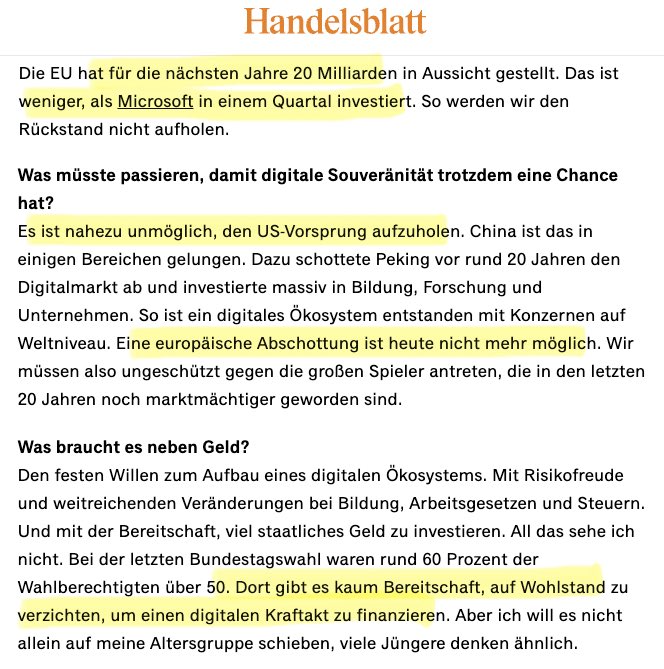

gilt 1:1 im #payment: Mikro-Budgets der hiesigen Banken für Souveränitäts-Versüchelchen vs US Incuments (Paypal/MasterCard/Visa) - PP gab im Okt & Dez jeweils €20/Monat cashback für NFC vs Banken einmalig €5 für ne Registriertung von Wero 🤣 Aber dafür schriller im Lobbying 🤦♂️

Jan 19

#UnitedInternet-Gründer Ralph Dommermuth mit einem klaren Verdikt über das europäische Streben nach digitaler Souveränität: „Das ist feinstes Souveränitäts-Washing“

2

274

13 Aug 2025

Wie kann #worldline wieder in die Spur kommen? 5 Thesen von mir bei @paymentbanking

#payment

paymentandbanking.com/5-thes…

3

1

4

931

8 Jul 2025

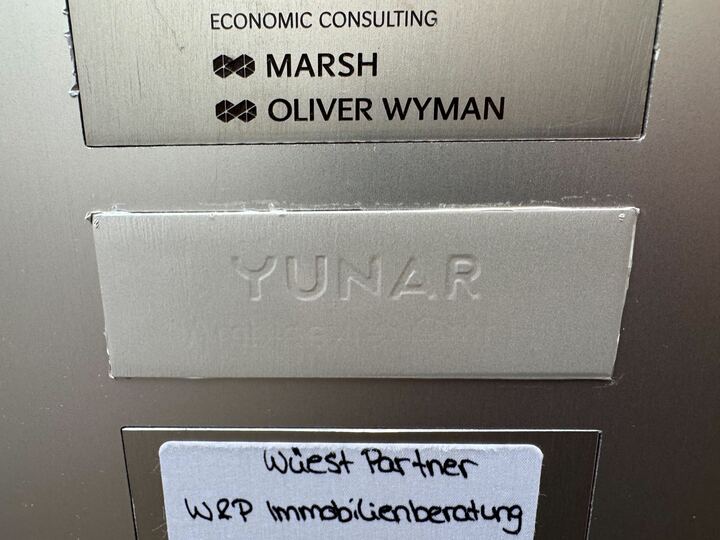

Überklebtes Aufzugsschild des "Fintechs" #yunar in Berlin. Etage des 2020 (!) abgewickelten Corporate Ventures der Dt. Bank leer oder dank langfr. Vertrag post-mortem gar weiter bezahlt? Alleine die Wahl des Officegebäudes zeigt das komplett fehlende StartUp-Mindset.🤦♂️#keinwunder

1

5

622

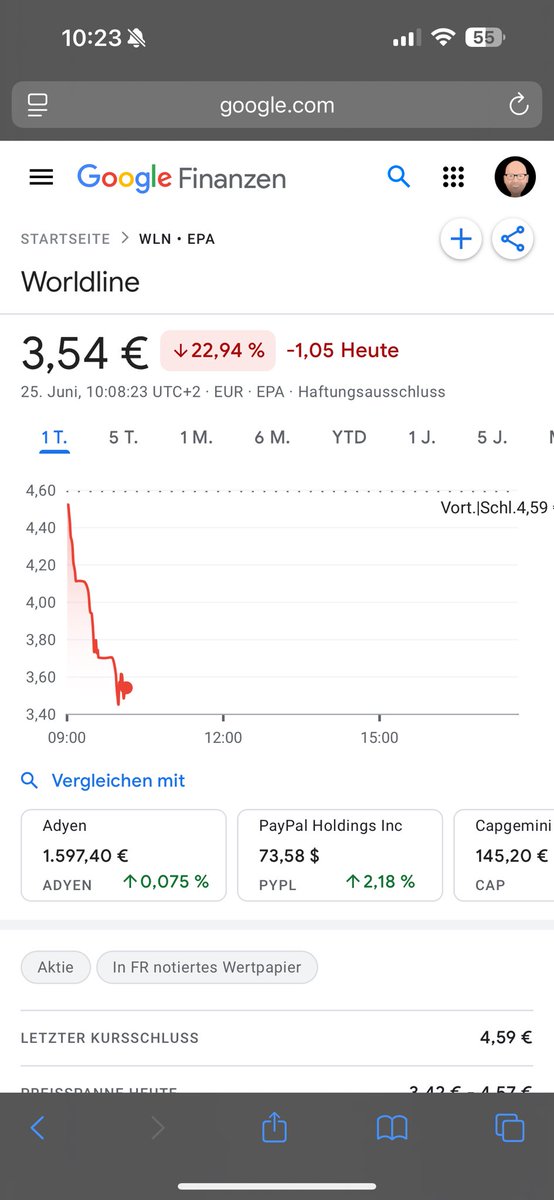

25 Jun 2025

Meine Kurzanalyse bei @paymentbanking zu Auswirkungen der heutigen pan-europäischen Berichterstattung verschiedener Medien zu #dirtypayments bei #worldline und #payone

paymentandbanking.com/worldl…

#payments #konsolidierung

5

1

11

1,973

25 Jun 2025

impact of pan-eu press articles on „#dirtypayments“ from German #worldline & #savingsbanks #payments JV #payone…

Worldline market cap below 1bn€ 😳

2

2

8

1,755

25 Jun 2025

🤣🤦♂️ … und was haben sich v.a. die Sparkässler über das „Schmuddelgeschäft“ von #wirecard früher immer das Maul zerrissen.

Aber wenn hohe Marge 🤑 winkt, gilt Doppelmoral…

Dumm nur, wenn dann nicht die Risk/Infrastruktur angepasst wird 🤦♂️ #payment

spiegel.de/wirtschaft/untern…

3

7

1,116

Jochen Siegert retweeted

12 Jun 2025

12 Jun 2025

Shopify will enable USDC (Stablecoins on @Base) in Checkout via Shopify Payments and Shop Pay. Early access starts today, roll out throughout the year.

We think that stablecoins are a natural way to transact on the Internet and worked with coinbase to develop the commerce payment protocol smart contract that powers this work

3

3

14

6,259

Jochen Siegert retweeted

6 Jun 2025

After watching social media for a long time, I met a "guy" who explained to me what is important and what is not.

👉 important

- do selfie🤳

🚫 not important

- content

🤯 impossible

- fact based talks

i said: hey then i am totally wrong here!?!

his answer: take my posts

🙈🙉🙊

1

1

3

971

3 Jun 2025

#Paypal with 1M #NFC installs since launch 2 weeks ago in Germany. Also introduces high street retailer cashbacks to the NFC-feature (up to 10%). Now they really challenge ApplePay. #payment

newsroom.paypal-corp.com/202…

13 May 2025

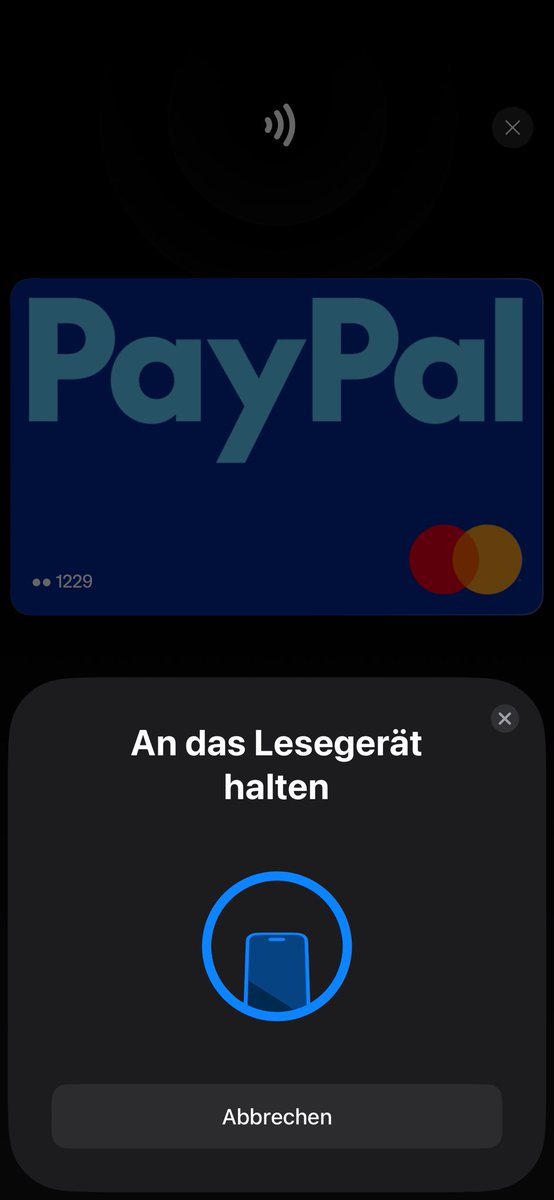

Today #Paypal launched in Germany #NFC-#payments at point of sale on iphone competing with #applepay. Based on PP issued Mastercard. Surprisingly pretty good onboarding and less complex vs many banks on applepay. Option to become „standard“ / leading NFC wallet. Very well done!

1

491

13 May 2025

Today #Paypal launched in Germany #NFC-#payments at point of sale on iphone competing with #applepay. Based on PP issued Mastercard. Surprisingly pretty good onboarding and less complex vs many banks on applepay. Option to become „standard“ / leading NFC wallet. Very well done!

4

9

2,404

Jochen Siegert retweeted

13 May 2025

🚀 Die DigiFin geht in eine neue Runde – und das stärker denn je!

@Bitkom und @paymentbanking bündeln 2025 erstmals ihre Kräfte und veranstalten am 18. November im Kosmos Berlin gemeinsam die DigiFin25.

👉 Alle Infos & Tickets: digifin.berlin/de

1

3

4

592

7 May 2025

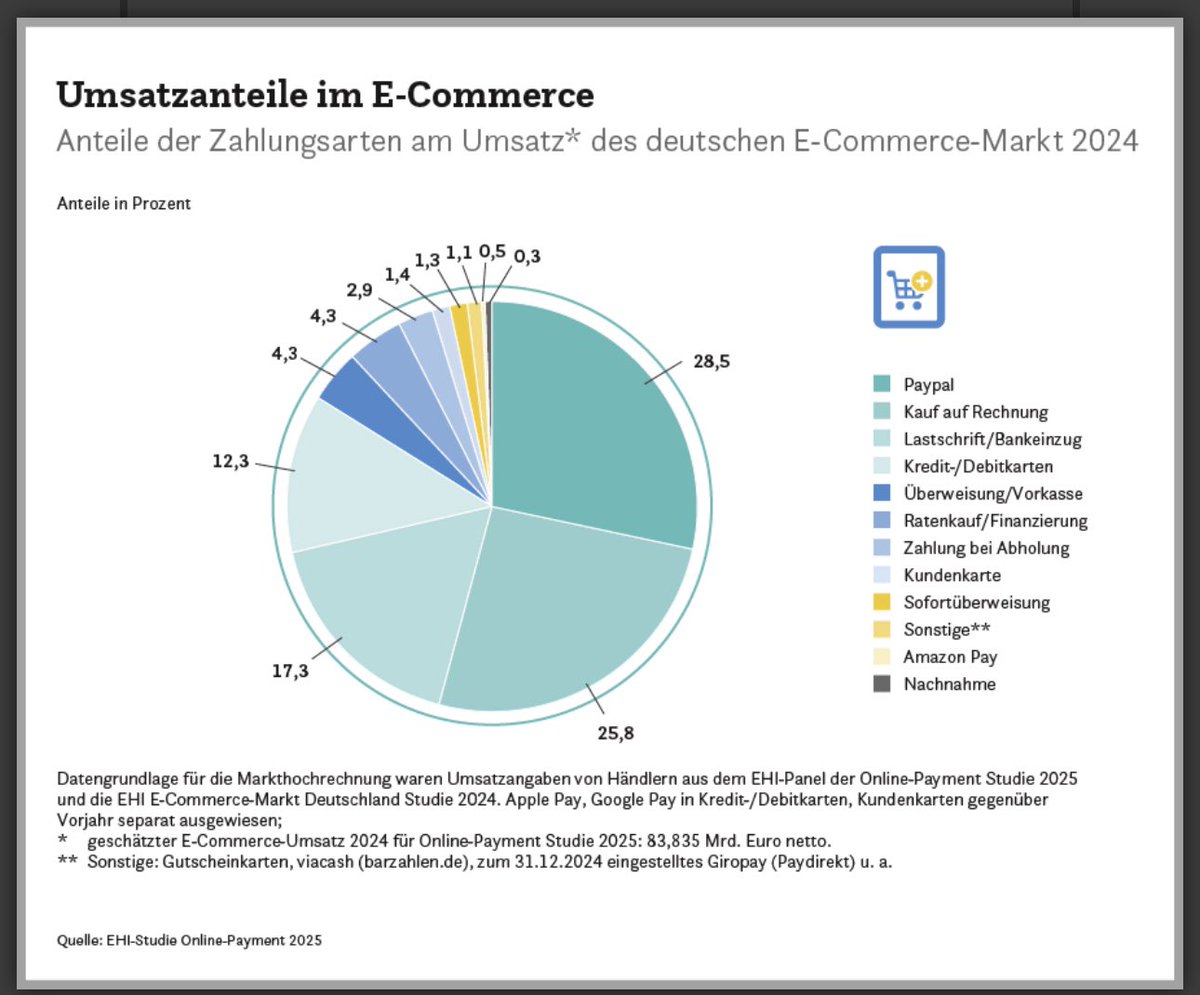

… and today fresh 2024 German #payment stats from top 1k ecom merchants

Paypal continues to dominate 🇩🇪 online payments, followed by open invoice, SEPA direct debit and cards.

Excluding Amazon (no Paypal, primary SEPA DD) PP share is probably north of 40% at merchants.

3

9

1,064

7 May 2025

Meinungsartikel zum #paypal Move und dem War of Wallet 2.0 bei @paymentbanking #payments #payment

paymentandbanking.com/der-ne…

2

195

6 May 2025

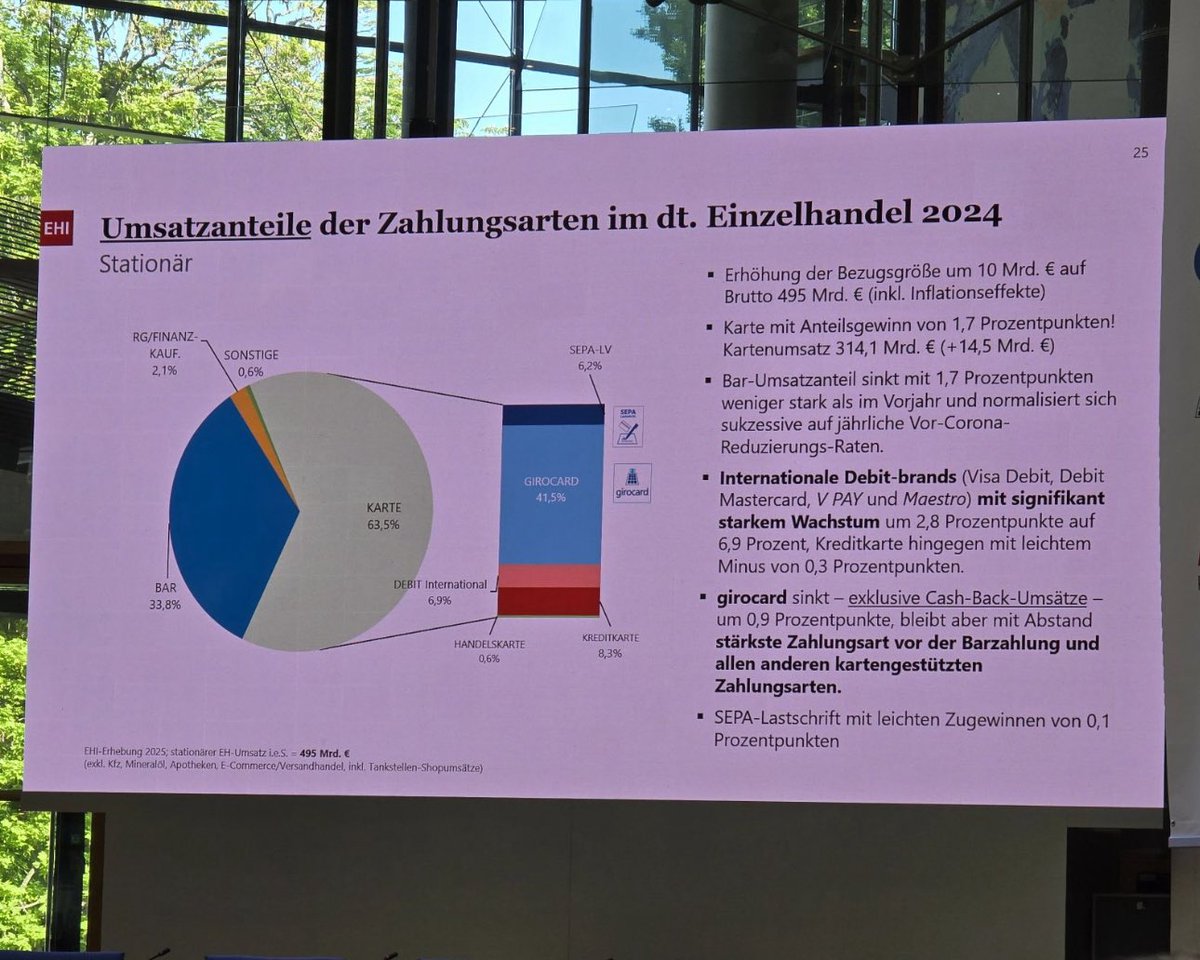

2024 #payment stats at German retail POS:

* Cash usages continues to shrink to just 1/3 of total #payments

* #peakgirocard leading domestic debit @girocard first time loss marketshare -0.9%

* Successful go-to-market of int debit schemes MC/Visa 3% to 7%. Almost 2x increase yoy

1

1

5

883

Jochen Siegert retweeted

5 May 2025

Still hard to believe that Apple lost its monopoly on the use of the NFC chip. “In the coming weeks, PayPal’s first-ever contactless mobile wallet will launch nationwide, available to PayPal consumers in Germany before anywhere else in the world.” $PYPL

18

13

159

20,994

4 May 2025

A2A-#Payments and #PSD2 obviously gaining finally traction - and smart move of Visa to have „bought-in“ into this non-card based payment stream…

4 May 2025

Visa $V FY Q2 2025 earnings call: “Tink has reached a milestone of over 10,000 merchants choosing Tink's Pay by Bank capability via our more than 10 European PSP partnerships.”

1

391