At One Capital Management we have one clear mission: assist our clients in achieving their investment objectives at the least risk possible.

Joined January 2016

- Tweets 461

- Following 33

- Followers 87

- Likes 602

80 Photos and videos

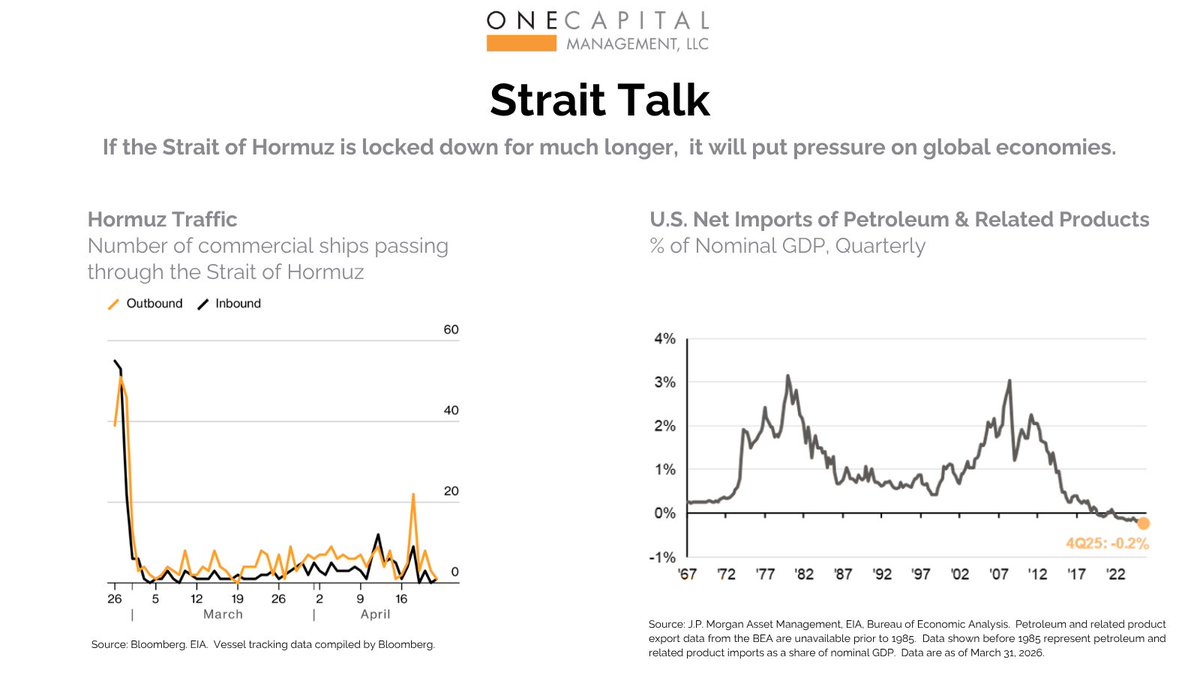

Traffic through the Strait of Hormuz has plunged & oil prices have surged. However, in contrast to oil price spikes of previous decades, the US is now a net exporter of oil. This implies that what domestic consumers lose from higher oil prices, domestic oil producers will gain.

12

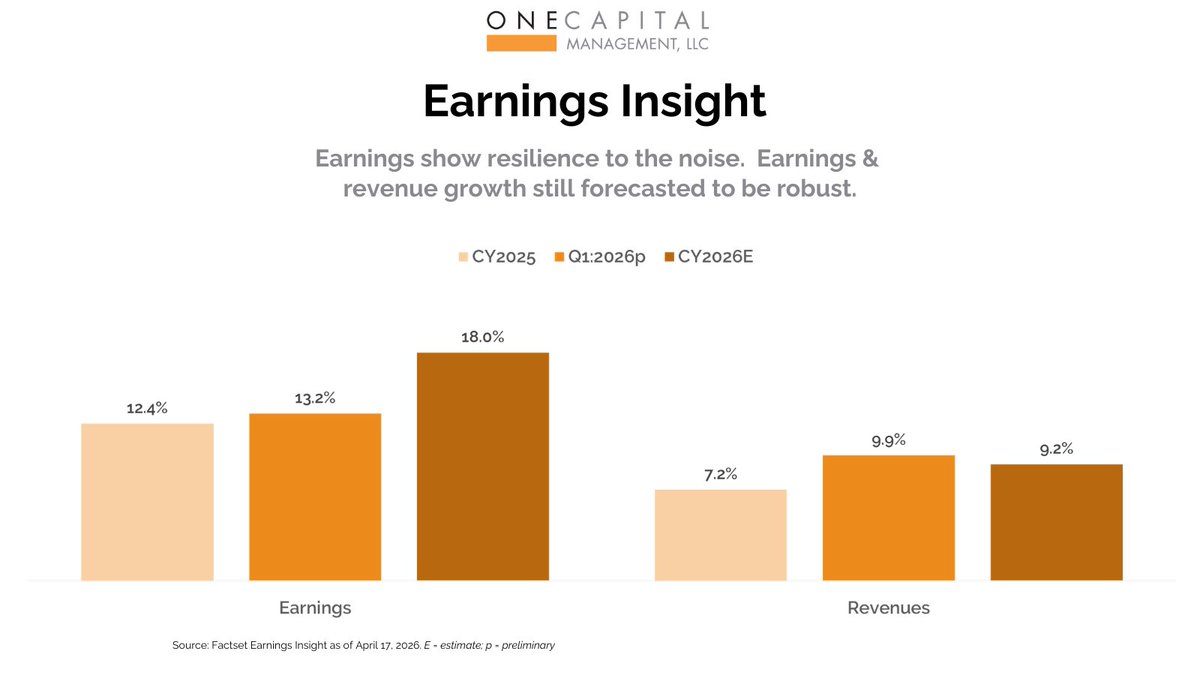

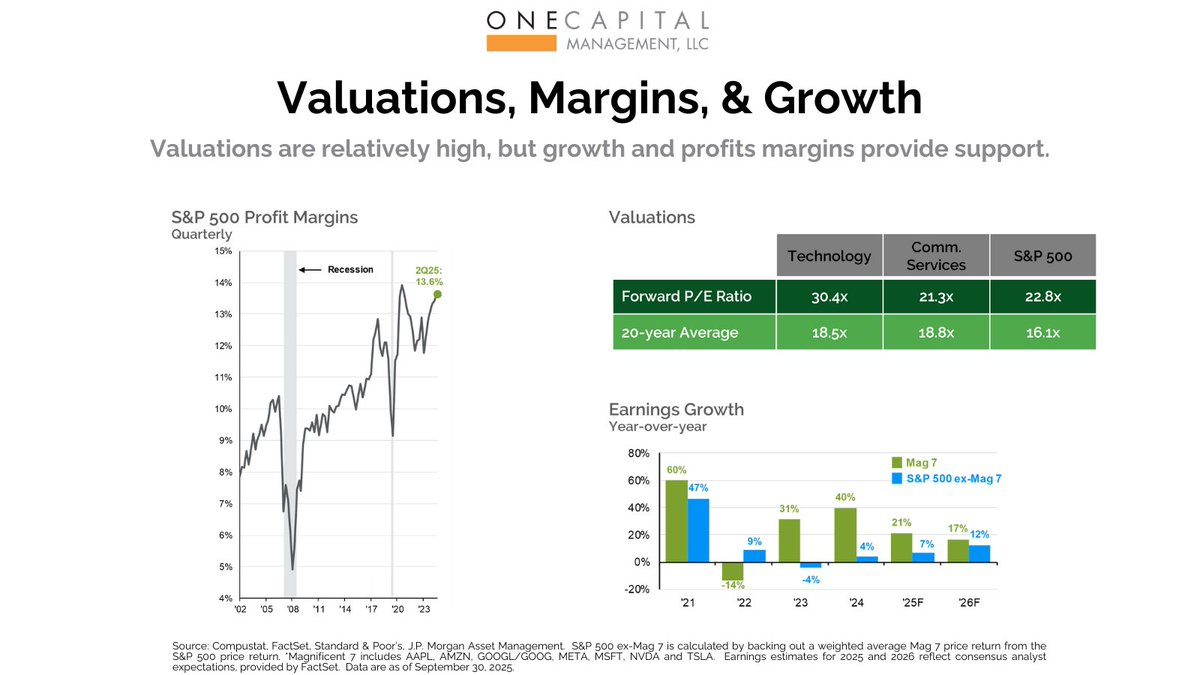

Profit growth should remain solid in 2026 as companies benefit from strong productivity gains, subdued wage increases & recent tax cuts. Earnings of large US companies rose over 12% in 2025, led by tech stocks again, & are expected to rise 13.2% in Q1 2026.

4

On March 11, 2011, Japan experienced one of the largest earthquakes in recorded history. Yet, the Tokyo Skytree, the tallest tower in Japan, suffered no structural damage. Read more about how skyscrapers & portfolios can be designed to mitigate quakes ow.ly/2i2e50YOcP1

13

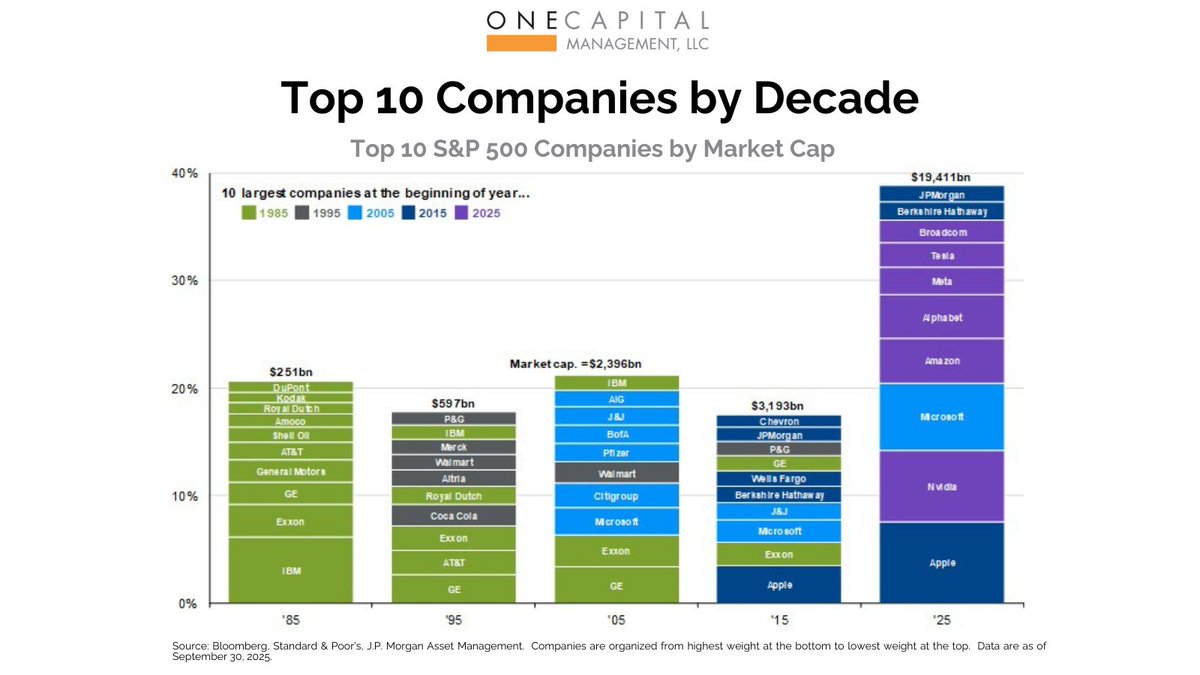

Nothing great lasts forever. Not one of the top 10 S&P 500 companies since 1985 is still in the top 10 today. Only GE & Exxon lasted 30 years in the top 10. By 2025, only Microsoft had spent 20 years in the top 10 & just 4 of the top 10 had been there for 10 years or more.

17

Affordability isn't just a political buzzword. The strength of an economy is rooted in affordability, in households being able to meet their expenses & have a little left over for savings. Here's how we look at affordability & what economic data tells us: ow.ly/tMzP50Y1i1F

13

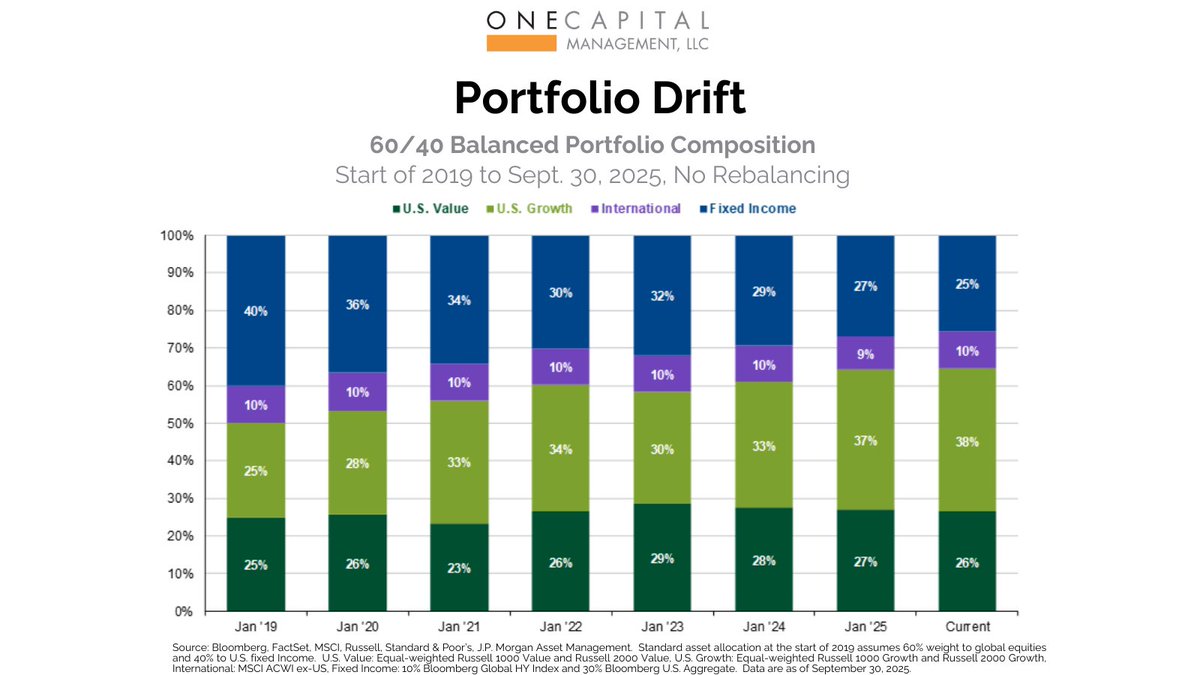

Strong stock market returns may have led to portfolio drift & a higher risk portfolio. Consider that a portfolio of 60% stocks & 40% bonds at the start of 2019 would have grown to over 70% in stocks & just 25% in bonds by Sept. 30, 2025, assuming dividends were reinvested.

24

18 Dec 2025

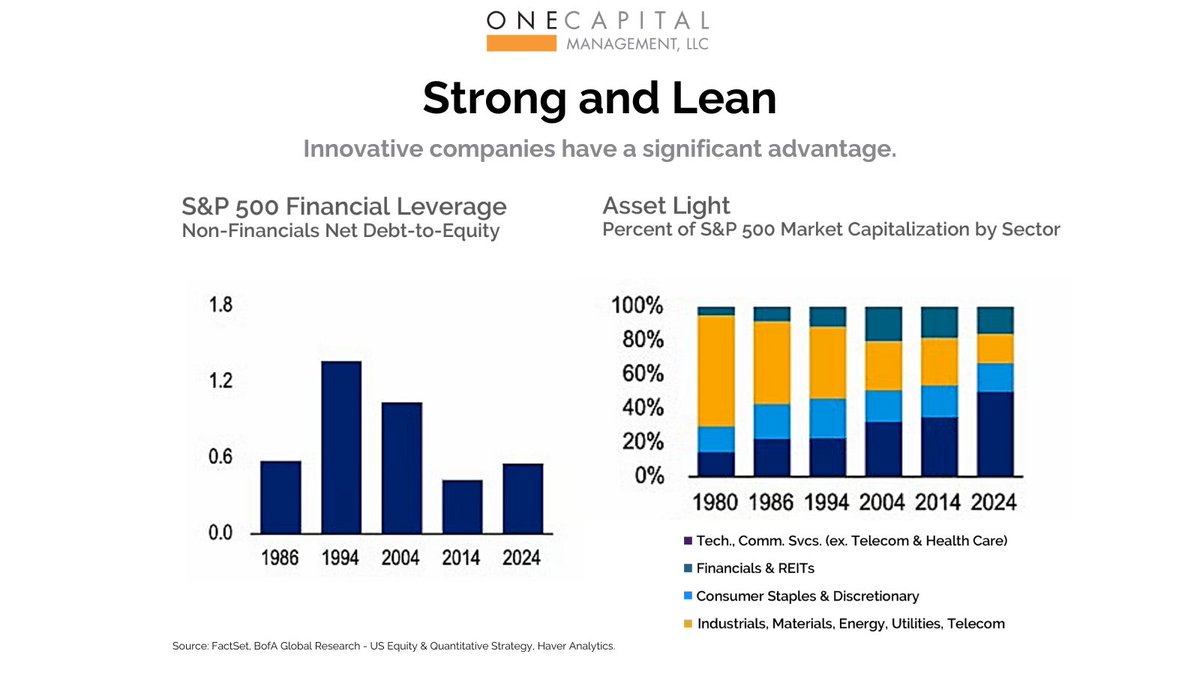

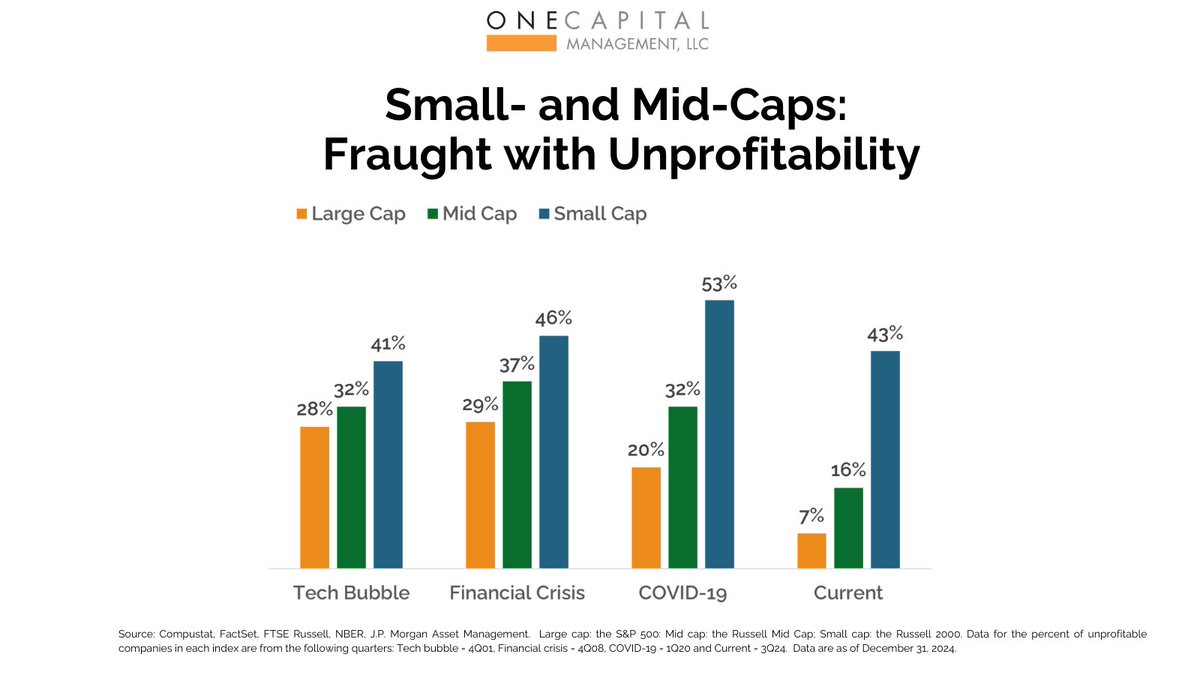

Today's innovative, asset-light companies & industries are not the same businesses, & investors are rightly treating them that way. Net profit margins have expanded through the last 3.5 decades. Technology companies now make up about 45% of publicly traded U.S. companies.

22

11 Dec 2025

Much of the US economy is driven by innovative, asset-light companies w generally stronger balance sheets. Non-financial companies now use less leverage (left chart) & about 45% of the S&P 500 is now tech companies w higher margins & larger moats (right chart).

20

8 Dec 2025

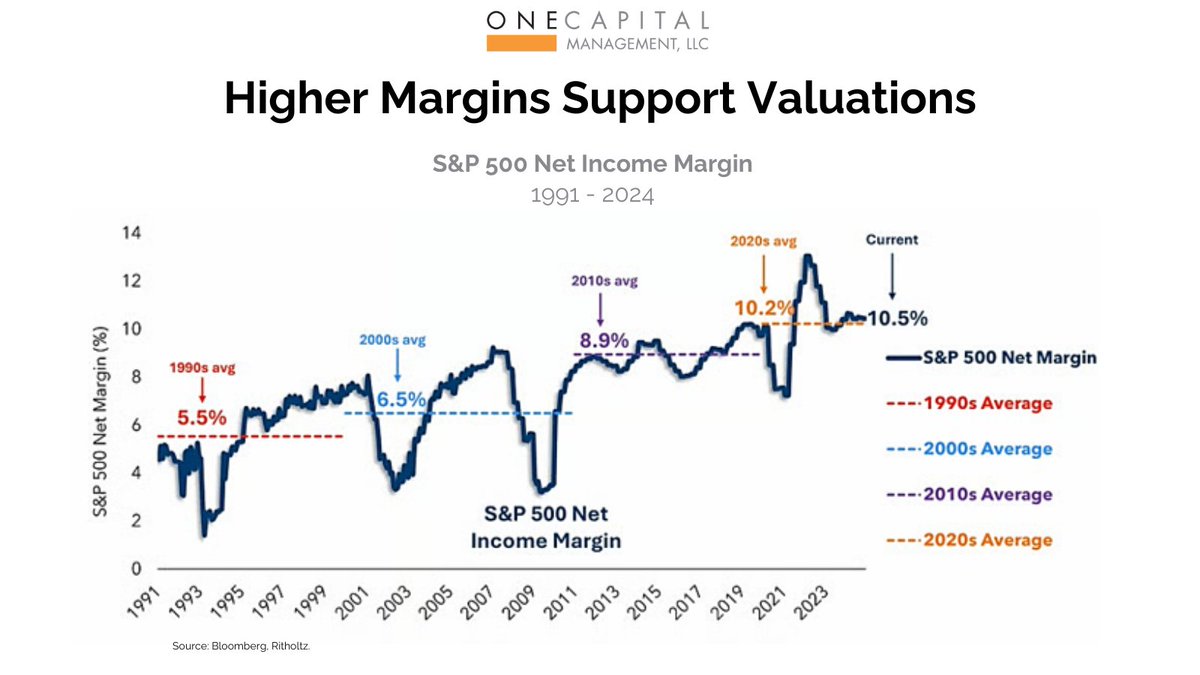

While valuations (chart at upper right) are higher than the long-term average, especially in the technology & communication services sectors, their higher earnings growth rates are driving near record profitability (left hand chart).

16

6 Nov 2025

The effective YTD tariff rate is 6.2%, which is 4% above the 2.3% average of the last 45 years, but lower than you might assume, given the estimates in April 2025. Tariffs on goods have been rising, rather than on services, which currently account for most of overall inflation.

22

27 Oct 2025

The elephant (& the donkey) in the room won’t be ignored. We’ll address the U.S. government shutdown. But first, let’s take a trip back to January 1984 when tensions between the U.S. & the Soviet Union were running high. ow.ly/t3yX50Xgutc

27

20 Oct 2025

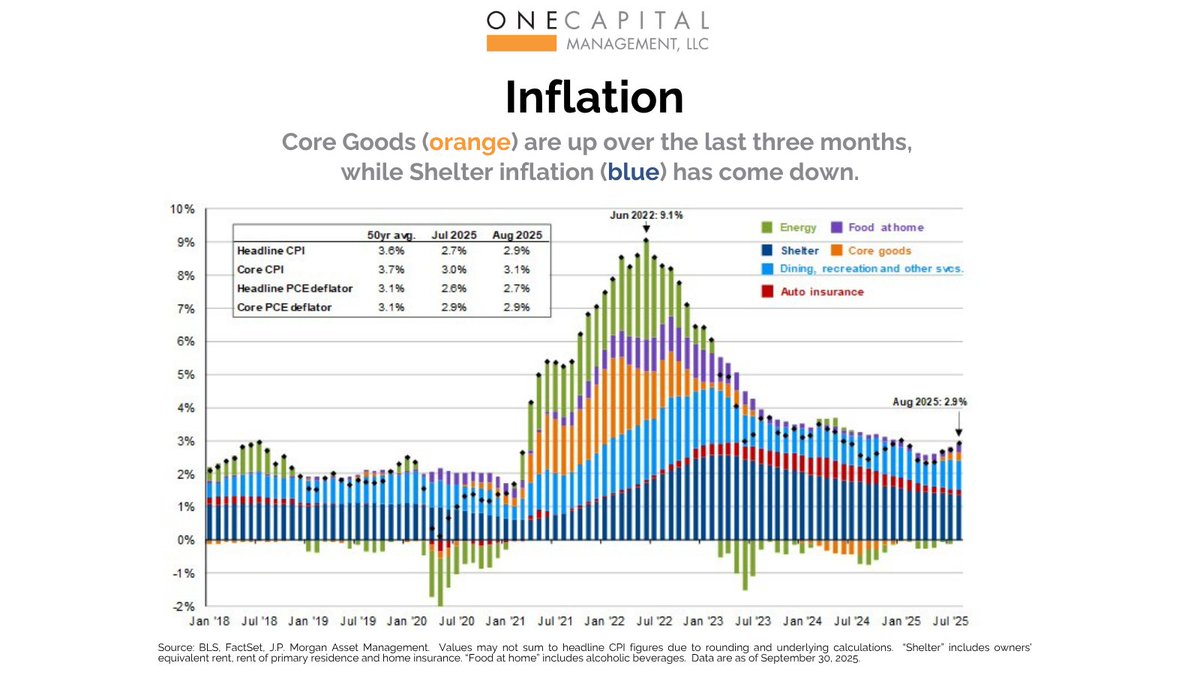

We expect inflation to rise over the next year due to tariffs & fiscal stimulus but fall later in 2026. Tariffs are starting to impact inflation, w/ YoY CPI inflation rising to 2.9% in August. We believe this will increase as retailers apply mark ups to new inventories.

17

16 Oct 2025

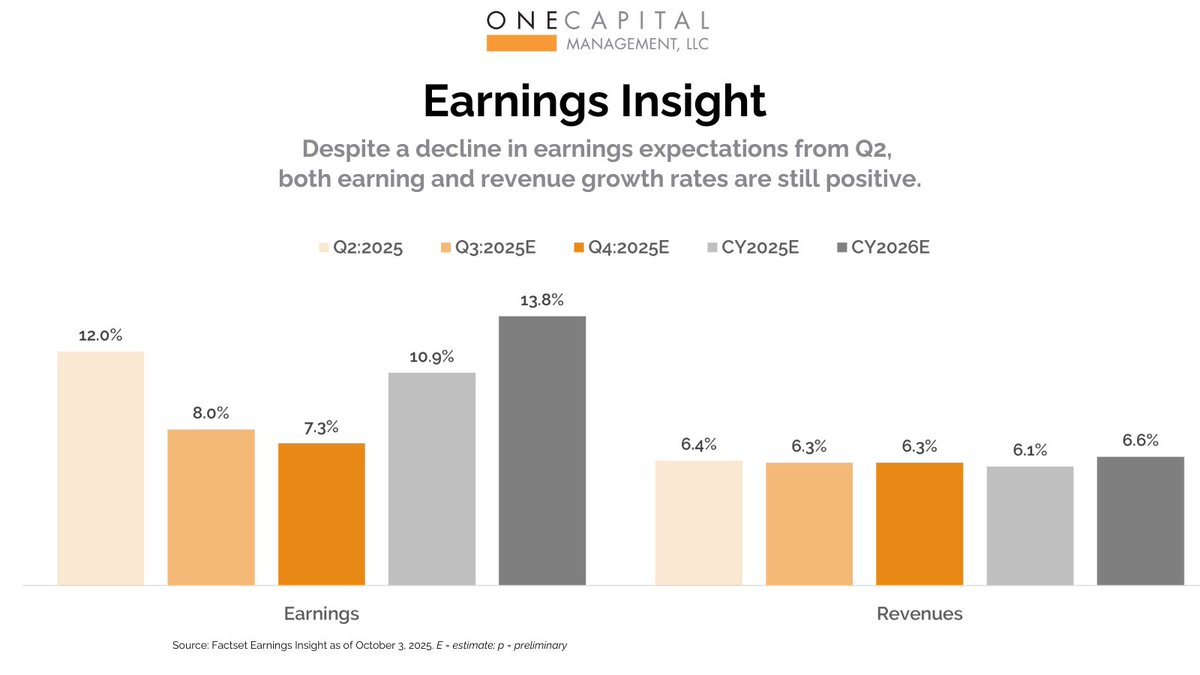

Earnings have continued to be strong, driving markets upward, while revenue has been steady. Net profit margins remain healthy at 12.8%.

18

22 Jul 2025

Labor markets are currently an under-the-radar but crucial piece of the global economy, especially when it comes to the U.S. & Canada. Labor markets can be understood by thinking about...the bathtub. Find out more in the Summer folio: ow.ly/j0CF50WrAz8

76

3 Jul 2025

1

56

5 Jun 2025

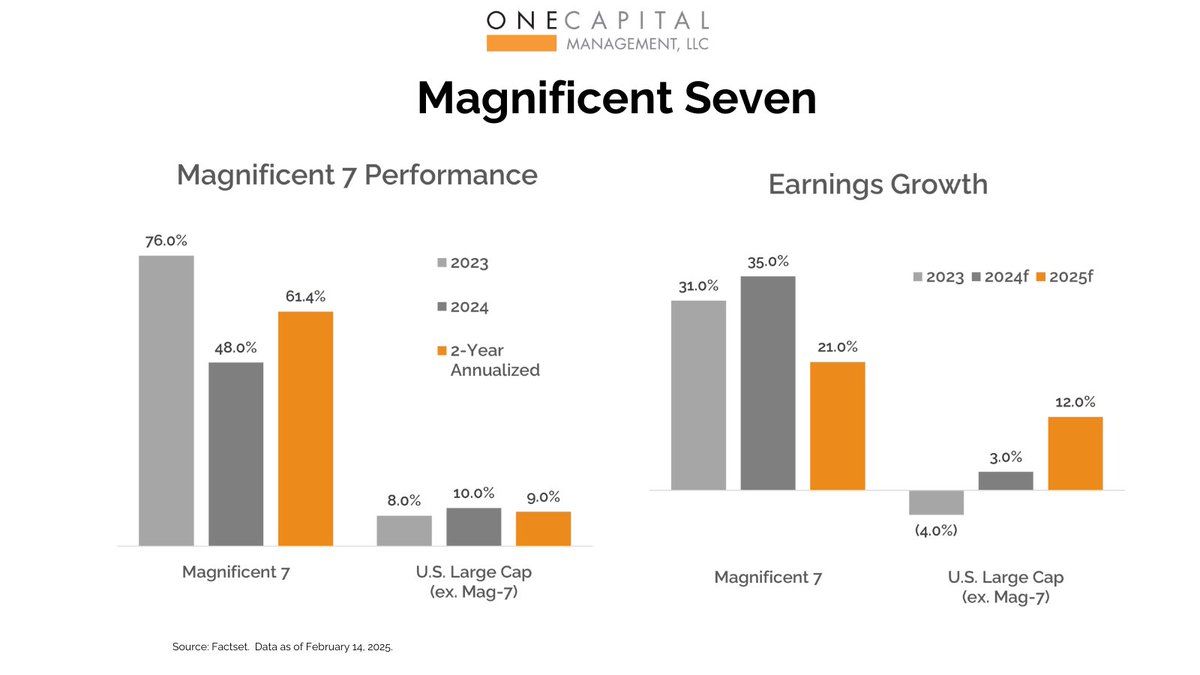

AI enthusiasm significantly drove US large-cap stocks over the last 2 years as the #Magnificent7 stocks generated outstanding returns & earnings growth. Without the #Mag7, the remaining stocks had almost zero earnings growth, but the wealth is likely to expand.

49

14 May 2025

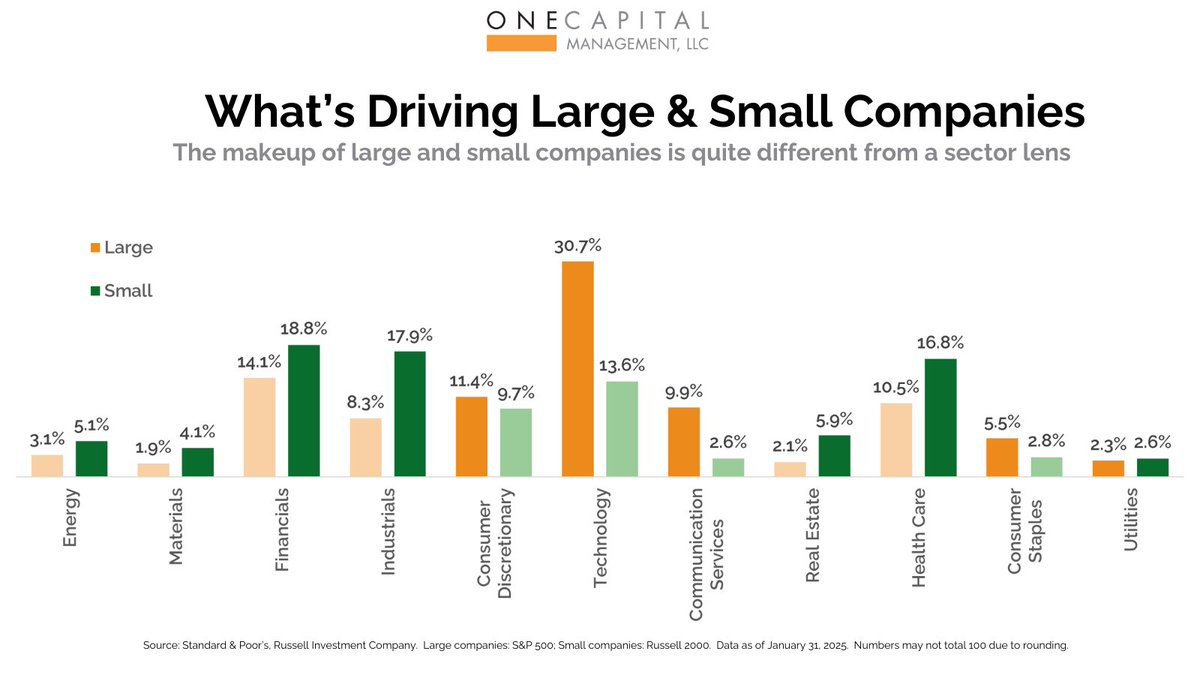

The makeup of large companies and small companies is quite different from a sector lens. Technology & telecom dominate the large-cap space, while financials, industrials, & health care drive the universe of small companies.

43

7 May 2025

Our Spring 2025 folio was inspired by this Warren Buffett advice. We shared what we believe is important and knowable about volatility & tariffs.

Read it here: ow.ly/Cjrv50VN1UA

37

30 Apr 2025

Our perspective on the early April tariff tumult, starting with an assessment of the markets’ immediate reaction and some insights on capital markets and tariffs in general. ow.ly/ONsu50VJXUV

39

23 Apr 2025

Tariffs & the ensuing market volatility have caused anxiety & uncertainty. So, let’s take Warren Buffett's advice: “What you really want to do in investments is figure out what’s important & knowable." Here's what we believe is important & knowable: ow.ly/4BSb50VFREN

47