Market loving, 32yr veteran JSE equity analyst covering swathes of small-to-mid cap industrial, agricultural & food stocks. Independent & just giving my opinion

Joined November 2018

- Tweets 38,975

- Following 311

- Followers 25,051

- Likes 20,970

14,332 Photos and videos

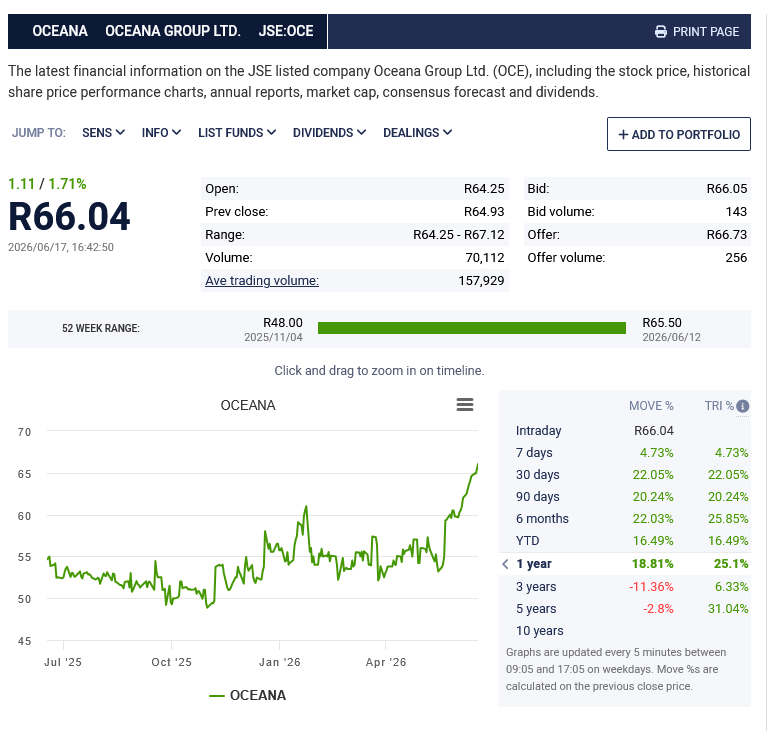

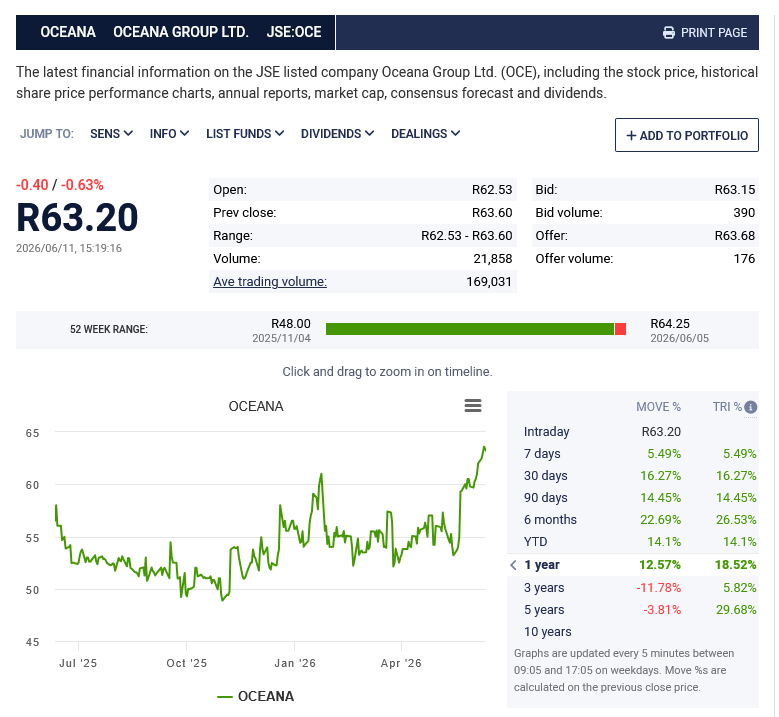

Another new 52-week high fro fishing stock $JSEOCE Oceana Group as it hits R66.04

Is the market at last catching up to the news I have been informing my clients on since early-May ? Its all about Peru

#OCE 24.1% since mid-May as the news started to trickle out about the fishing problems in Peru and the beneficial pricing impact to its US-based Daybrook business

My target remains R70.00

Breaking news

More positive news for Oceana’s Daybrook

Peru has extended its anchovy fishing ban with no date set for its removal, adding further uncertainty to global fishmeal and fish oil supplies. The ban on fishing has been in place since late-April

The suspension, which had been due to expire on June 10th, remains in place across much of Peru’s northern and central coastline

Authorities said the restrictions could be lifted fully or gradually following further scientific assessments by Government Fishing Bodies

The ban remains in force amid ongoing Coastal El Niño conditions and concerns over a high proportion of juvenile fish in the stock

Peru is the world’s largest producer of fishmeal and fish oil, making developments in its anchovy fishery closely watched by aquaculture feed markets

Only 24% of the first season’s TAC of 1.9 million tons was landed before the ban started. The first season fishing traditionally ends in mid-to-late June and the on-going ban on fishing raises concerns that the first season will be cancelled echoing the 2023 El Nino issue that slammed Peruvian fish meal and fish oil production and caused prices to spike

Just in May, when Peru initially had a mini ban, then a mega ban (that was extended to June 10th) fish oil prices have run from $3,500 to $7,000 a ton ( 100%) and fish meal from $2,340 to $2,940 a ton ( 25.6%). I am awaiting my data points for June to update

On this ban extension it is likely prices, where stocks are said to be globally tight, will run further ahead.

1

2

1,143

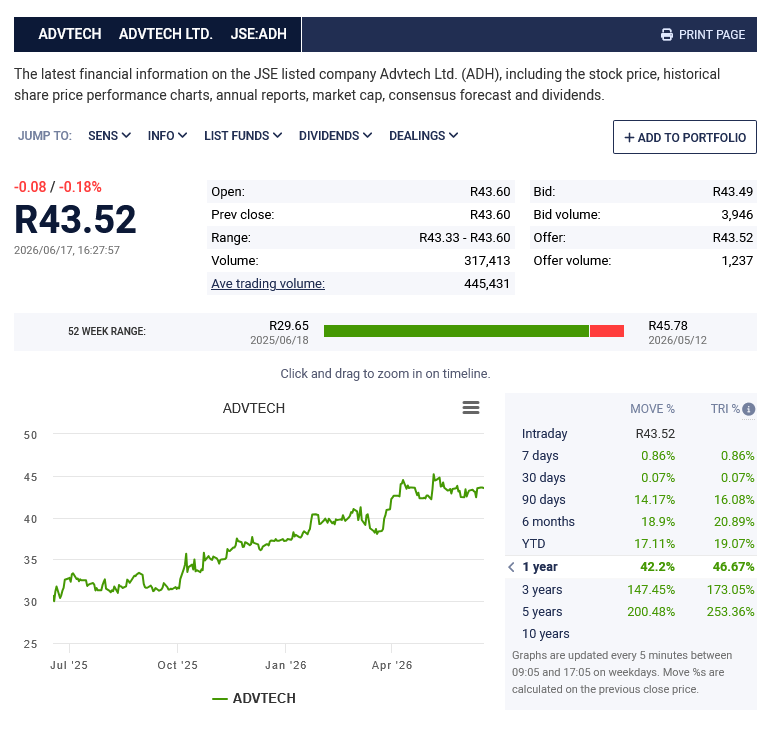

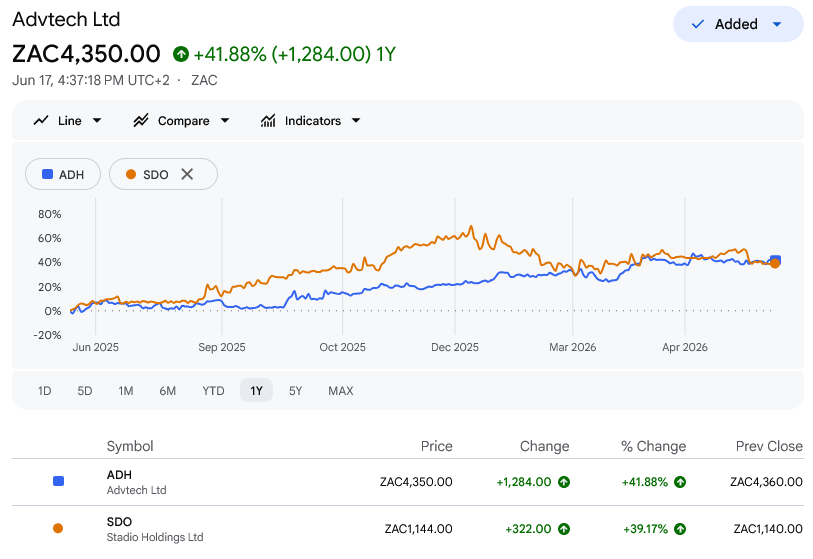

Private education group $JSEADH @AdvtechGroup spends R250 million to buy-back 1.04% (5,740 million shares) and plans to cancel them

They paid between R40.47 and R44.90 indicating the boards confidence that buying back shares at current levels was a judicious use of excess capital

#ADH is in my top stocks of 2026 and year-to-date is 18.86%

My stated target price on selection was R45.00) it achieved this on May 9th 2026) and I maintain that target and raise it to R48.00 ( 10.3% from current ruling price)

ADH Voluntary Announcement: General Repurchase of Shares bit.ly/4ehePuE

1

9

1,856

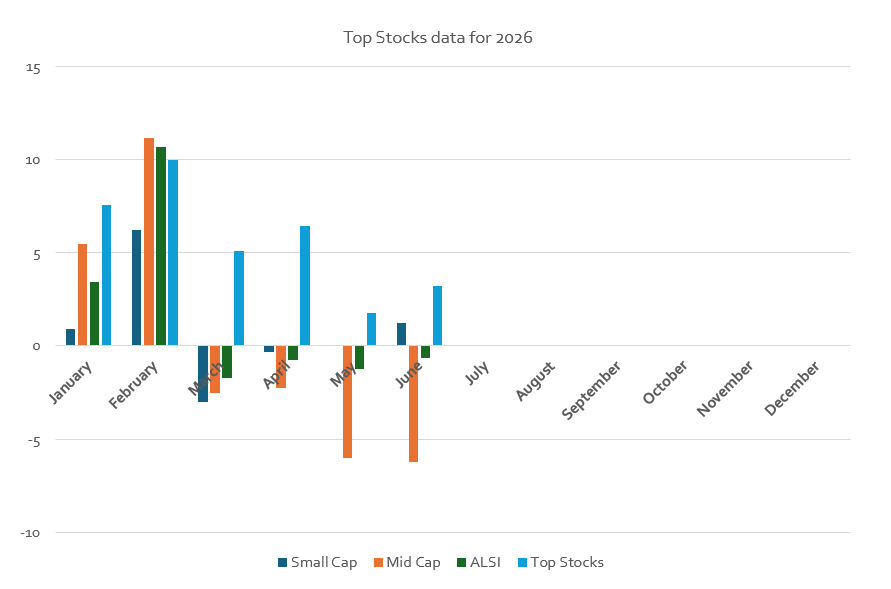

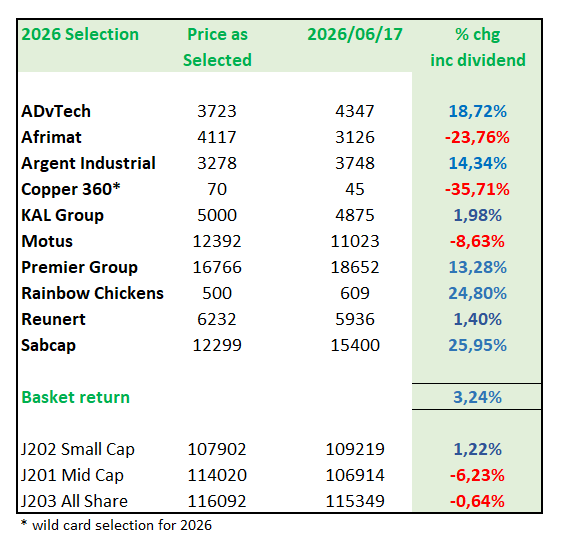

Just a mid-month update on my Top Stocks of 2026 as we came to the six month stage

It's still holding its own and outperforming my J201 & J202 benchmarks

3.24% year-to-date

$JSEAFT Afrimat and $JSECPR Copper 360 my two weakest plays to date

$JSERBO Rainbow Chickens and $JSESBP Sabcap my top stocks

Overall, fairly happy seven of the ten are ahead of benchmark with a good six month yet to go some solid gains in much of the selection aside from the two dogs. Those two stocks shave -6.0% off my total gains

3

14

1,807

~: Fisheries Department to get a New Minister feikemanagement.blogspot.com…

742

Yet MORE delays in getting an opinion & ruling on the fishing “once empowered always empowered (or not) ruling …. sector been waiting for this clarification since 2020 and with yet another new minister the can keeps being kicked down the road

$JSEBRN Brimstone management must be tearing their hair out in despair as it impacts their Oceana & Sea Harvest investments & the long delayed wind up on the BEE investment company

17h

The fisheries dept is to get it's third new minister in 2 yrs! Minister Aucamp moves to Agriculture and @DavidMaynier will be appointed the new minister of @environmentza. @DavidMaynier knows how important fisheries is to WC economy and how it can be grown. @geordinhl

1

2

3

1,458

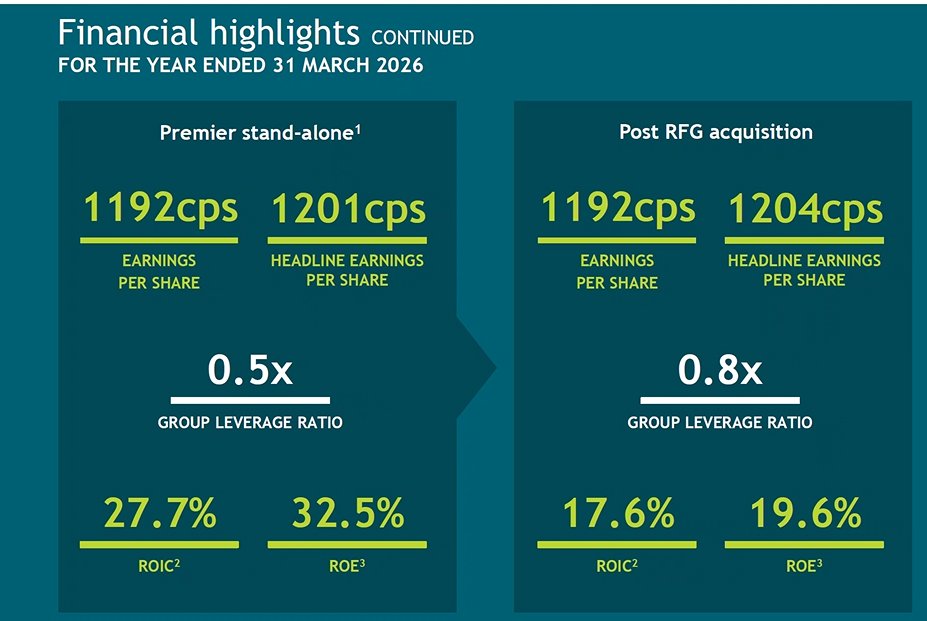

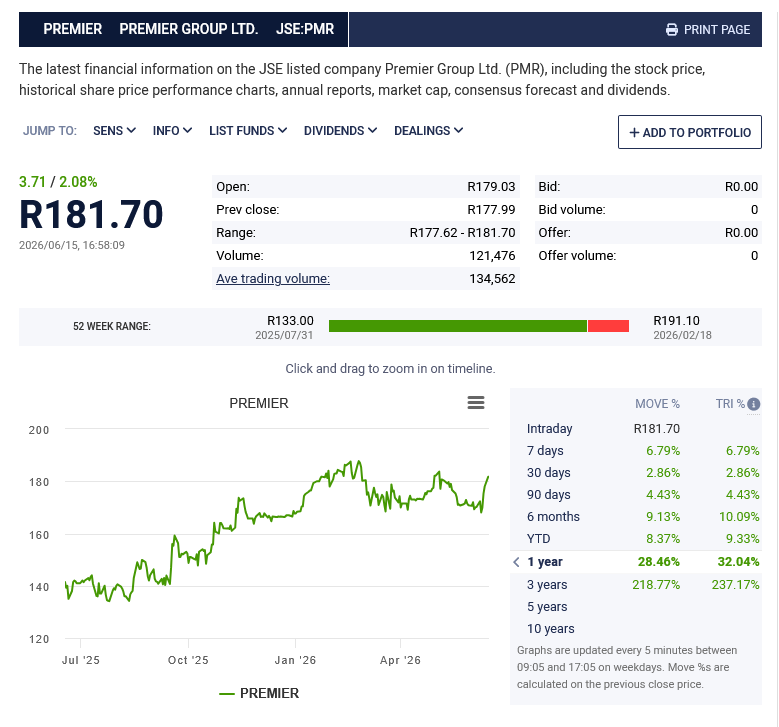

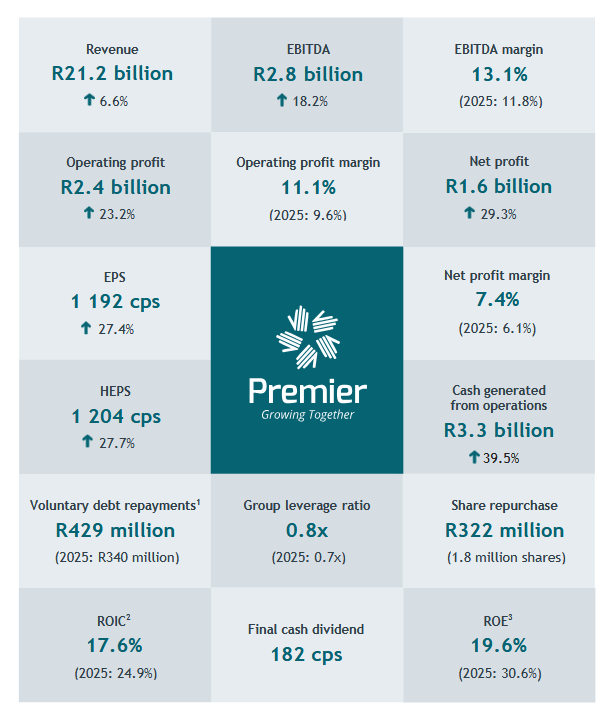

Yet another solid set of results from miller, baker and groceries business $JSEPMR Premier Group

The trading update issued March 20th indicated HEPS 20% to 30% higher and they came in slap in the middle at 27.7% with HEPS of 1204 cents per share and a final dividend of 182 cents for a payout of 341 cents ( 25.8%)

The full benefit of the RFG Group acquisition and associated cost and integration savings are yet to be seen in results and the new mega bakery (again) has only just started to kick-in efficiency and operational savings

Revenue R21.2bn ( 6.6%)

Operating profit R2.4bn ( 23.2%)

Margin 7.4% up 213bps

Millbake revenue 5.1% but operating profit 23.3%. margin rose 180bps (impressive on a basic food item)

Groceries revenue 13.5% but operating profit 14.3%

margin rose by 100bps

Tight cost control (cost of sales 4.2%) finance income / finance cost savings were the main key line items kicking results and operational margin higher alongside bakeries

Prospects statement (due to on-going business, mega bakeries and RFG) is upbeat

Presentation at 9.00am

PMRE Group Financial Results for the year ended 31 March 2026 and Cash Dividend Declaration bit.ly/4vesacR

1

1

7

1,899

Rhodes Foods was only included for 21 days in the Premier FY2026 results and was only effective April 1st

RFG added 3 cents per share to #PMR HEPS highlighting the strong uplift anticipated in the next 12-18 months as the company in integrated, costs cut and investment made in uplifting capacity and efficiencies

3

458

South Africa has a record maize crop with good prior season carry-over & high grade yield

Globally, the world is awash with grain & the strong rand aids SAFEX prices

$JSEARL Astral Foods & $JSERBO Rainbow Chickens will be extending margins as kg realisation prices remain firm, domestic supply vs demand is well-balanced and the QSR sector remain fair

Both stocks remain well placed with solid earnings & dividend prospects into Q1 2027 at least on known knowns within the poultry sector

Jun 16

South African white maize prices, Rands per tonne.

South Africa has a record maize harvest of 17.1 million tonnes.

Our annual consumption is about 12.0 million tonnes.

This decline in prices mirrors the ample supplies we have, and bodes well for consumer food price inflation.

South Africa’s consumer food price inflation data for May 2026 is out tomorrow.

2

6

2,025

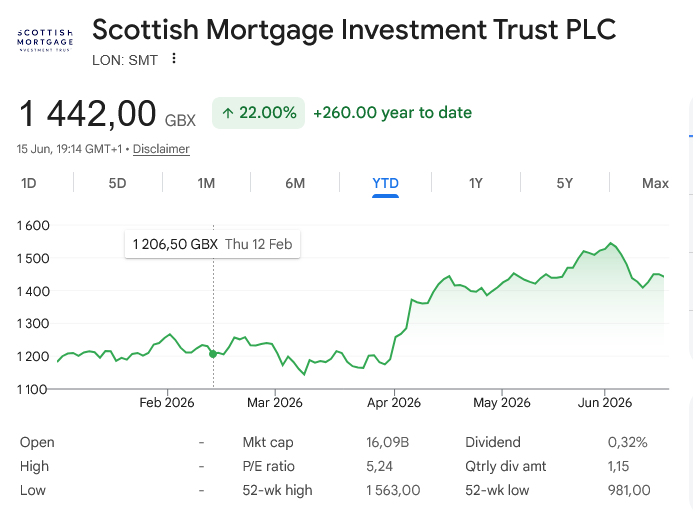

I'm sure this won't end well but (hey) its just an opinion

42.6% higher than last Friday's US$135 IPO price

I'm indirectly invested as UK investment trust Scottish Mortgage has a large percentage of its assets in Space X ... best I watch that carefully as its now trading at a premium to NAV too

4

4

24

5,804

Smalltalkdaily Research retweeted

Jun 15

Plenty of really interesting corporate news in this edition of Ghost Bites.

Be sure to vote in the poll on KAP!

ghostmail.co.za/ghost-bites-…

1

7

1,864

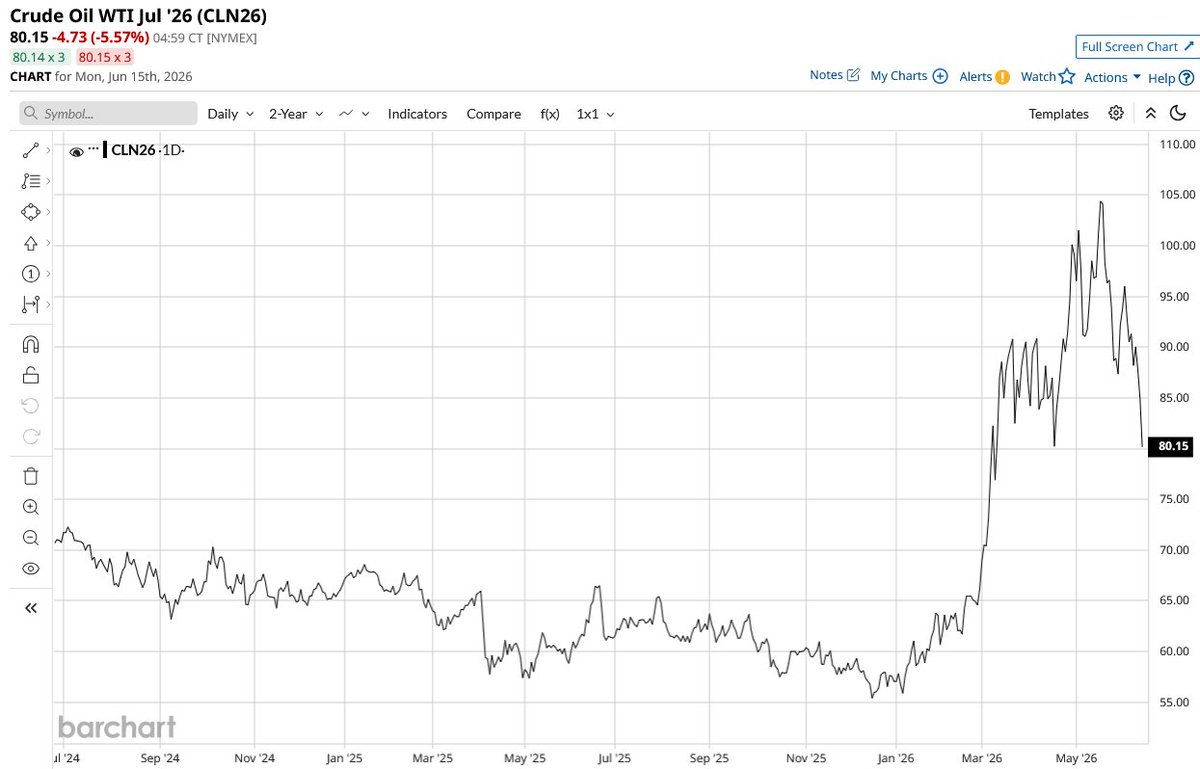

WTI US$80.16 -5.56% on the latest Trump / Iranian news....who's telling the truth or their version of truth ...who knows

3

1,066

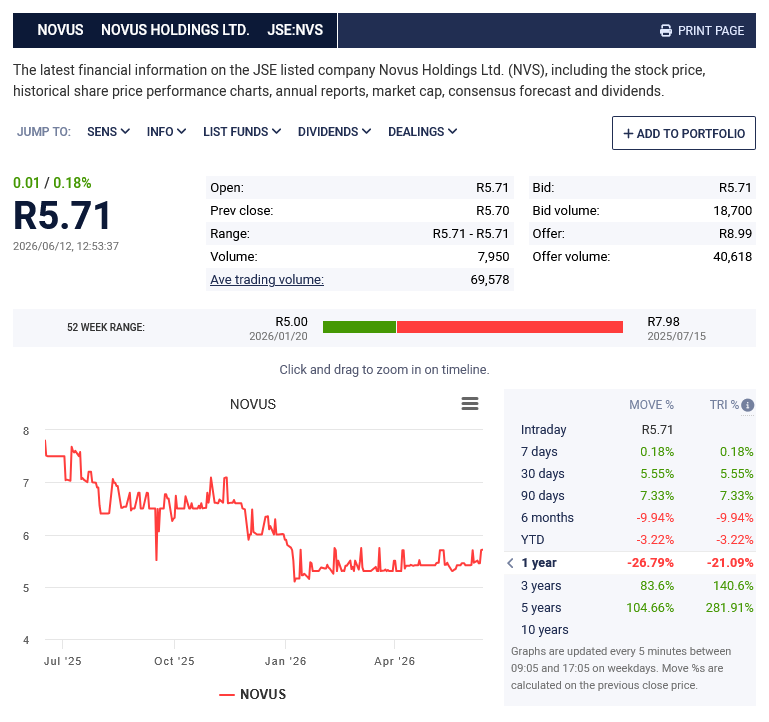

My opinion on Novus Holdings results

Printing, packaging & education small cap $JSENVS Novus Holdings issued its YE2026 trading update to March on June 11th

It indicated HEPS would be 0% and 8% lower to a range 81.26 cents and 88.32 cents. This decline was likely due to weakness in the education division and timing issues regards awarding of departmental book contracts that impacted H1 and swelled into H2

Actual YE2026 HEPS came in at 84.79 cents -4.0% on the comparative 88.33 cents per share

Before I unpack my observations I will detail some facts so as to calm those who will surely bitch & moan like that little twat Trump at me

I've owned #NVS p.a since 140 cents after A2 Investment Partners initially became involved as an activist acquiring from Media24 their initial investment at 100 cents a share to acquire 17.4% in April 2021

I have had nor have any corporate relationship whatsoever with A2 Investment Partners or its listed assets aside from just personally owning shares in Novus & Nampak (I've made great gains on both stocks as have institutional shareholders who also followed A2)

Novus is trading today at 571 cents with a market cap of R1,960 million. It's a tightly held small cap. A2, related Novus entities and institutions own 83.73% of the shares

This (could) create an opportunity should Novus return to earnings growth and with its Mcap hovering around the R2 billion value - many institutions cannot own shares in stocks below <R2bn - any improvement in earnings prospects (could) see a push in #NVS shares due to this illiquidity

Since A2 got involved with Novus in April 2021 (facts that will annoy some)....

Share price 100 cents to 571 cents = 471% (has been as high as 798 cents July 15th 2025)

Total dividends specials paid since A2 involved in Novus = 300 cents (including the 55c declared for YE2026)

= 871 cents of value from a stock you could have bought at 100 cents = 771%

In same period the J202 Small Cap Index has risen (from when A2 bought their initial stake in Novus) = 101%

Complain about business performance, and you can, I will join you and the machinations around $JSEMST Mustek BUT your up 771% in total return since early-April 2021.....that is a stellar return no matter your personal stance on Novus and A2

Ok, looking at year end results to March 2026

Mixed performance. In order to get the current 6.7x PE re-rated, management need to get growth and sustainability returned to Novus

I'm concerned the education business has become a riskier asset given the inconsistent and budgetary constraints within various Departments of Education and Provincial education authorities and the recent DoBE book order scandal (now under review) does not help sector education publishing sentiment

Novus cash at year end of R1,017 billion = 320 cents per share is a solid year-on-year increase but much of this uplift will be used to buy-out Mustek where Novus now holds 50.39% directly (control) and 70.68% via its deemed concert parties

Novus has agreed to acquire outstanding shares at 1541 cents but has greedily been hoovering up shares at 1500 cents as institutions bail out of this long-too-long dragged out M&A issue with Mustek. R311m of the cash is reserved for Mustek

Novus agreed to pay a flat year-on-year dividend of 55 cents which gives a current yield of 9.6%, not too shabby at all

On underlying performance

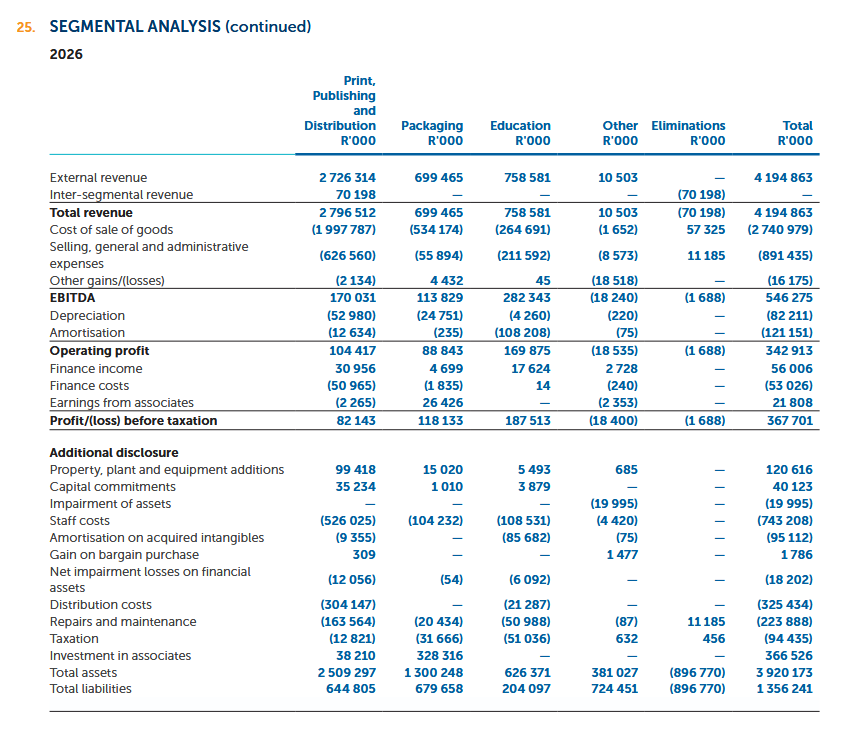

Mixed is the best term. Group revenue R4,195m (-0.7%) with declines in print (-9.9%), education (-18.1% to R758.6m and packaging (-5.1%) to R699.5m

Operating profit fell -18.7% to R342.9m but looking into this, there are lots to unpack;

Education saw operating profits 4.4% to R169.8m but that was down to accounting wizardry rather than underlying performance

Packaging operating profit 2.7% to R88.8m mainly due to cost controls as revenue was down due to general market pressures

Print & distribution saw revenue rise 6.8% to R2,726m but operating profit slumped -37.3% to R104.4m with some benefits year-on-year from lower paper prices, costs savings and the full 12-month inclusion of an asset previously only accounted for 5 month but strip out OnTheDot and print was -9.9% hitting overall profitability

Novus needs to return to its growth tack which was why investors piled in way back in the day. Since November 2024, Novus has been bogged down with Mustek and the overall business has flatlined

Yes, cash generation and dividends are solid but I own a R2 billion small cap mainly for growth not for dividends ... CEO Andre v.d Veen will assuredly get back to wheeling & dealing when Mustek is done.... at the last AGM they indicated (given their balance sheet) they could buy businesses >R2 billion

At 571 cents and a current PE of 6.7x and a dividend yield of 9.6x I want to like Novus. The rating is fair but the company needs growth and earnings uplift to get the stock moving and the market wanting to own and buy the stock

Until the Mustek issue is done & dusted and integrated and some update is given regards the uncertainty around education and Government ineptitude...I see the share just treading water

Just my opinion as a long-standing (reasonably happy) shareholder given the total returns made to date since purchase

11

1,430

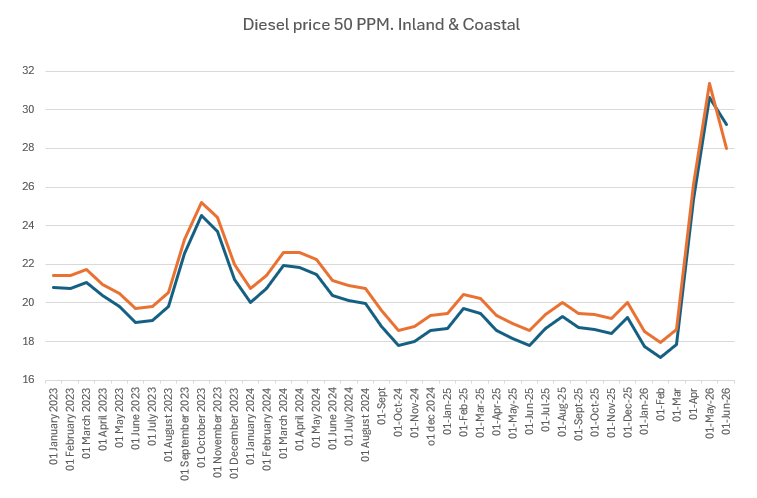

Update on the diesel price. I use 50ppm as its the main commercial / agricultural / transport fuel

lowest recent price was R17.19 a litre in February. Price 72.4% since pushing inflationary costs onto food production and industry

Current coastal 50ppm R28.00 a litre with expectation (yet to be updated given Trump has ended the war he started - with no real win at all seemingly just global surge in costs) - with July diesel to fall at this stake between R2.96 - R3.51 a litre

2

13

2,338

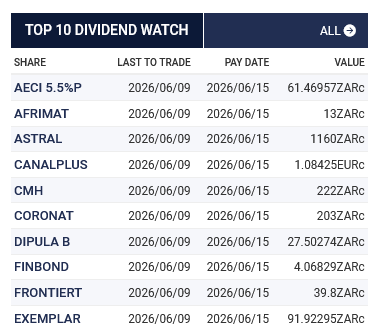

Some juicy dividend payout's coming shareholders way today ahead of tomorrow's Public Holiday

1

1

15

2,783

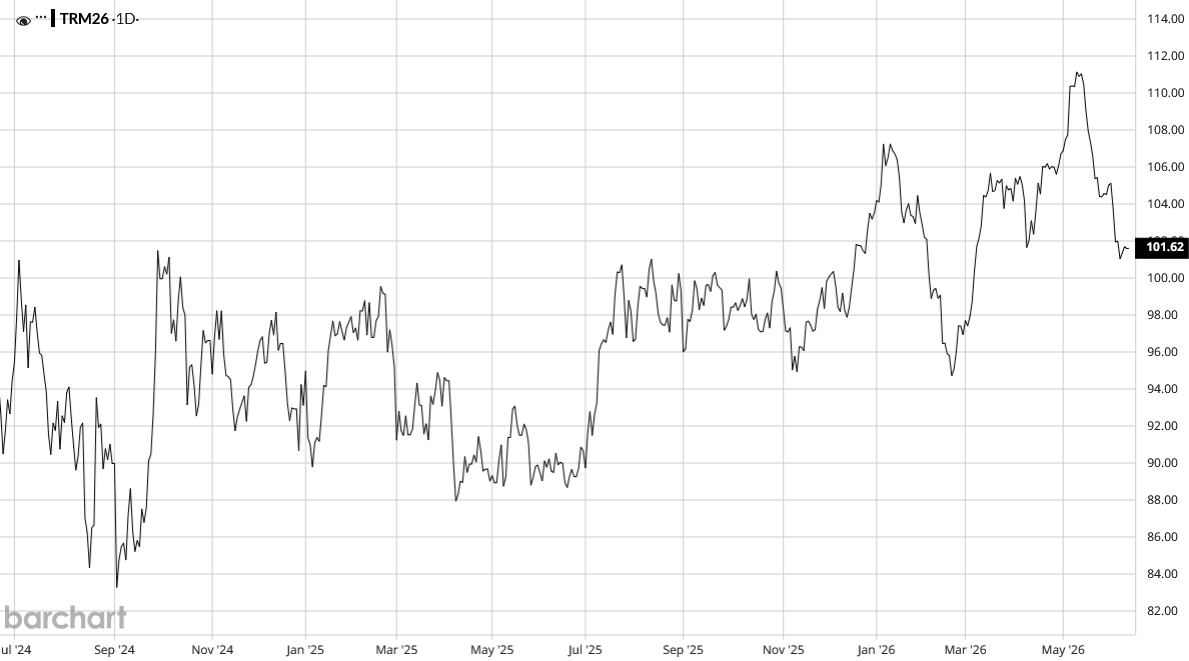

Monday data pointy

Iron e dull on the week at $101.62 = R1,643 at current16.17). Iron ore's slide Rand strength been main hits to local exporters

To date in 2026

Year low US$94.43 price 7.27%

Year high US$111.15 price -8.57%

Year-to-date -1.91% with Rand strength on top

Iron ore has been weak the past month on concerns over Chinese steel margins shrinking and steel consumption weakening amid high input costs

China also goes into its slower steel production in the summer as the Government aims to reduce air pollution

A strike at BHP's main Australia export hub (electricians striking) may he a temporary bump in prices should the strike extend but globally there is plenty of iron ore availability especially from the giant Chinese partly owned Guinea mine which continues ti ramp up production

2

925

Smalltalkdaily Research retweeted

Jun 12

JUST IN: 🇮🇷🇺🇸 Iranian state media confirms deal with the US and says it includes lifting sanctions, withdrawing US military from around Iran, and ending the naval blockade.

875

3,583

23,828

1,883,521

Smalltalkdaily Research retweeted

Jun 12

David Hockney, one of the most popular and influential artists of the past century, has died aged 88. ft.trib.al/YLDTpOW

24

261

789

61,963