Mother | I analyze macro, markets & companies to find investments | There's always a story behind the numbers | macrovisor.substack.com/ 🪐🧩

Joined June 2009

- Tweets 33,298

- Following 946

- Followers 57,176

- Likes 67,712

4,255 Photos and videos

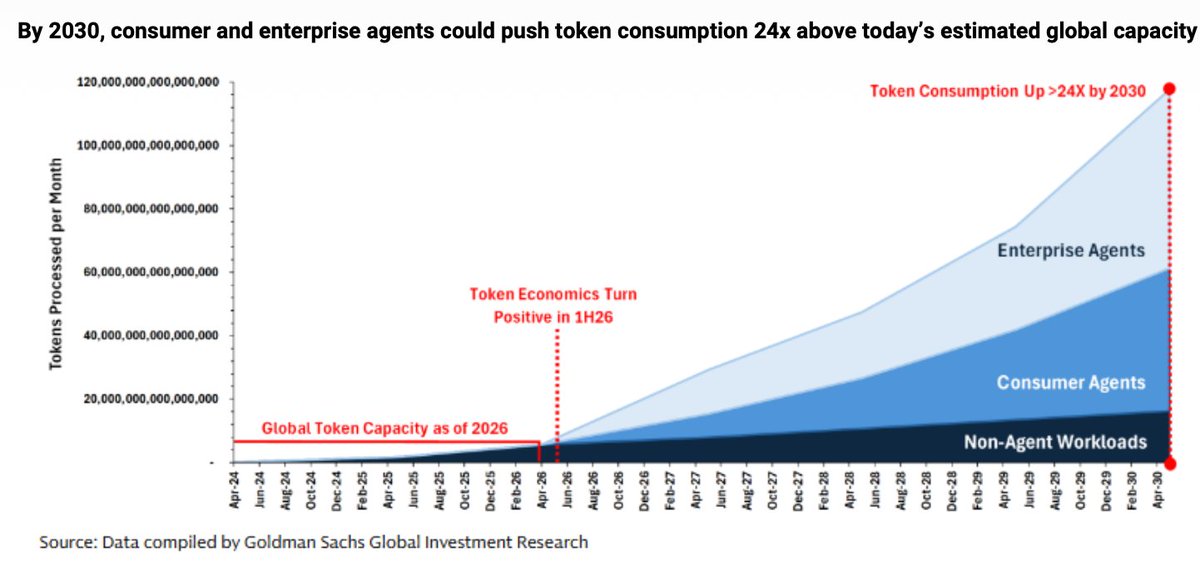

We've now started talking about token economics

GS predicts that token consumption could increase 24x today's estimated global capacity

As the use of agents become more widespread, the demand will be driver by enterprise and consumer agents, compared to non-agent workloads

1

4

527

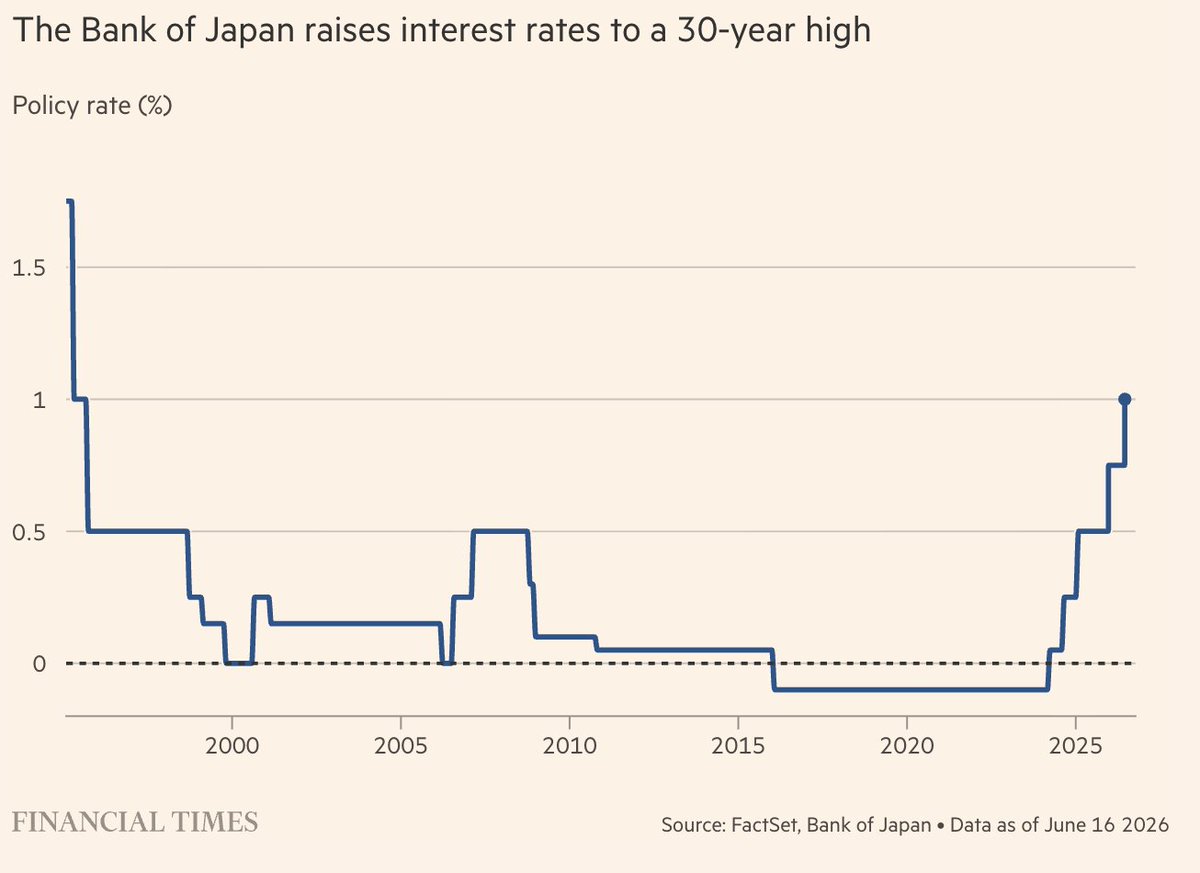

The BOJ delivered the widely expected 25 basis point hike to 1%, the highest policy rate Japan has seen since 1995.

The bank confirmed it will halt the tapering of its government bond purchases in April 2027, letting monthly flows settle at ¥2 trillion. We flagged this QT freeze as a signaling mistake, and the market's initial reaction looked like a reprieve. Equities briefly crossed 70,000 and the Yen traded flat. But the underlying message is dovish, and I think markets will eventually price that in.

The BOJ has explicitly left the door open to step back in with asset purchases if yields rise too quickly. That's not a hawkish hike. That's a hike with a safety net attached, and the safety net changes the signal entirely.

The whole issue was defending the Yen, so none of this helps that cause.

Compounding this is a leadership problem we can't ignore. Governor Ueda is hospitalized. Deputy Governor Himino chaired the vote. Deputy Governor Uchida handled the press conference alone. That's a broken chain of command at exactly the moment when clear, unambiguous guidance is most needed to put a floor under the Yen.

For global investors, the synchronized central bank era is over. The Fed is holding with a hawkish tilt. The BOJ is hiking while keeping the balance sheet on pause.

The risk-reward on Japanese equities is iffy here. Monetary transmission is slow, which means the friction between a nominal rate hike and a frozen normalization path will show up in markets before policymakers acknowledge it. Watch for volatility compression to unwind across global macro desks as this divergence becomes impossible to ignore.

2

5

17

1,459

Ayesha Tariq, CFA retweeted

3

10

18

18,235

Ayesha Tariq, CFA retweeted

Jun 14

4

6

11

22,418

Ayesha Tariq, CFA retweeted

Jun 10

5

12

31

33,634

Ayesha Tariq, CFA retweeted

Jun 10

More signs of the K-shaped distribution of socioeconomic outcomes intensifying

4

15

35

6,527

Ayesha Tariq, CFA retweeted

Hey friends!

Curious what's going on in these markets?

Want to learn more about order flow and how it can help you define risk intraday?

We're going live with this week's episode of Back to the Futures!

Tune in.

x.com/i/broadcasts/1jGXggXaZ…

1

8

11

10,732

Ayesha Tariq, CFA retweeted

Hey friends,

Join me today at 1:30 pm ET as I analyze what's going on with these increasingly volatile markets.

We'll talk about what's going on with sentiment, flows and positioning.

Then we'll shift over to opportunities and risks.

Back to the Futures returns . . . 🦾

4

4

9

5,425

In a surprise move ahead of its scheduled June 17-18 policy review, Bank Indonesia raised its benchmark BI-Rate by 25 basis points to 5.5% on Tuesday.

This follows a larger-than-expected 50 basis point hike in May.

2

2

15

1,772

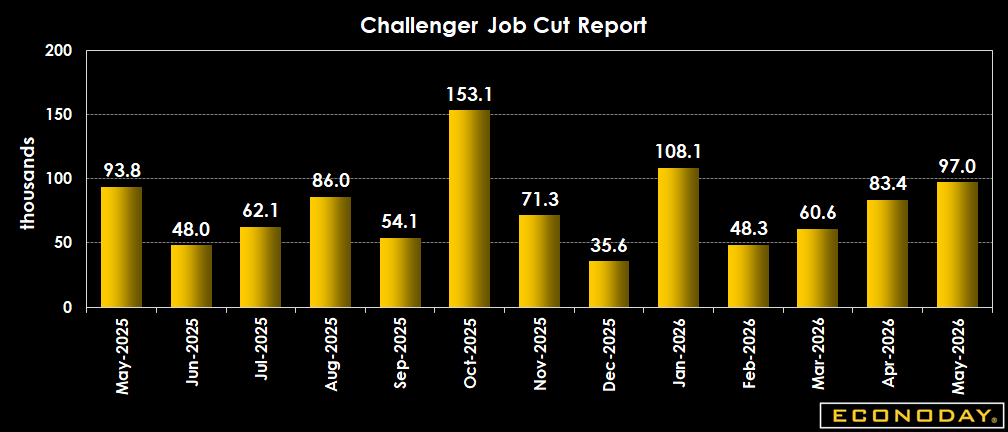

Apparently, AI drove 40% of the job cuts in May 👀

Jun 4

U.S. employers announced 97,006 job cuts in May, the highest May total since 2020. AI drove 38,579 layoffs—40% of all cuts—and has become the leading reason for workforce reductions for three straight months. Tech remains the biggest source of layoffs despite continued hiring plans.

7

14

42

15,061

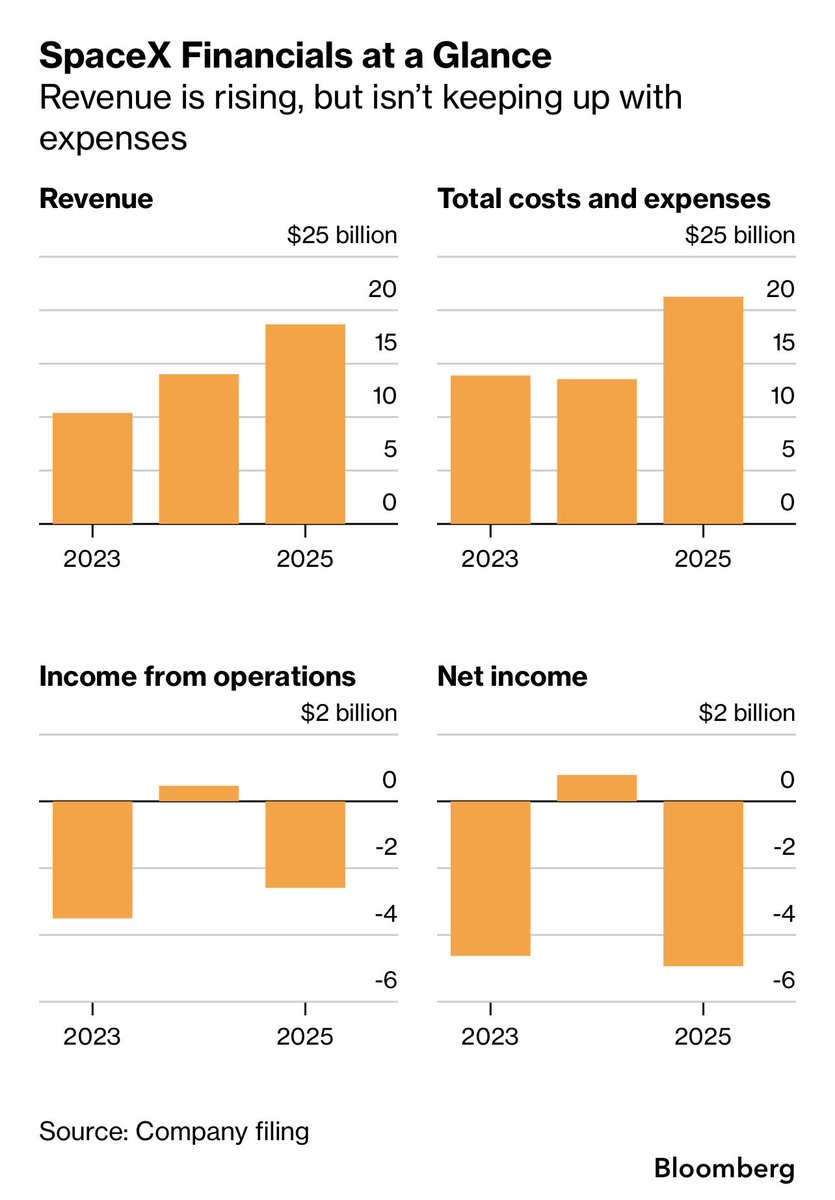

This is so funny. Apparently, Jeffries didn't get invited to the SpaceX IPO party, so now they're facilitating bets against the stock once the company lists.

3

13

1,740

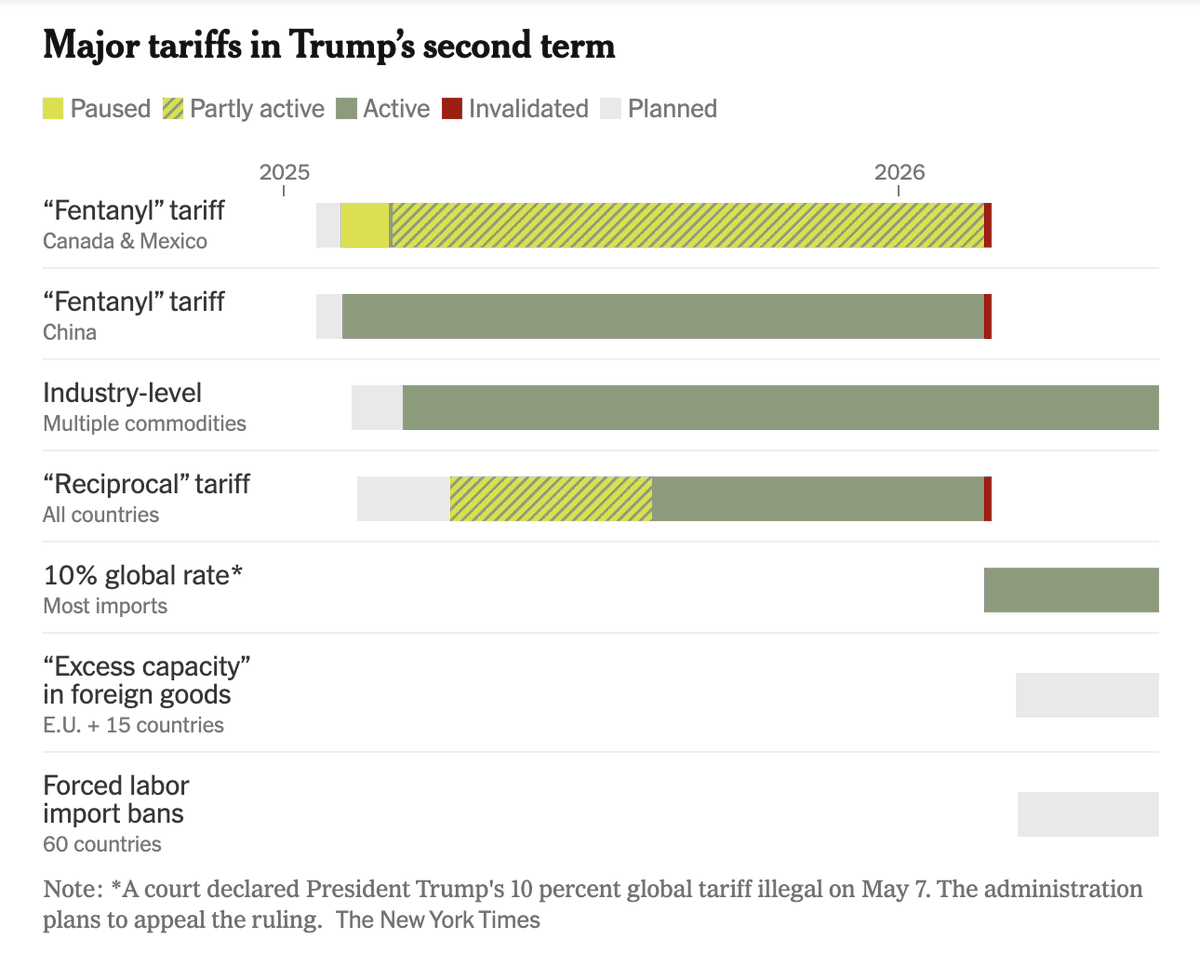

The Trump administration is back at it with the tariffs. After the Supreme Court knocked down their last attempt in February, they just dropped a new Plan B: a 10% to 12.5% tax on 59 countries and the EU.

It's an interesting new spin.

They’re using Section 301 of the Trade Act, claiming these countries don't have strong enough laws against forced labor. Officially, it’s a human rights push.

Will it actually go through? Yes, probably as soon as July.

Section 301 is a much tougher legal tool than the emergency powers they tried before. It’s the same mechanism used against China in the first term that survived multiple court challenges. Plus, wrapping it in a bipartisan issue like human rights makes it politically bulletproof to dismantle.

For major allies like the EU, Canada, and Mexico, this means more friction and potentially retaliatory duties.

For developing countries, it proves that recent bilateral trade deals won't save them from Washington's broader goals.

It's a massive curveball for global supply chains, and it's hitting right when inflation is already keeping central banks on edge.

Source: NYT

3

3

24

2,343

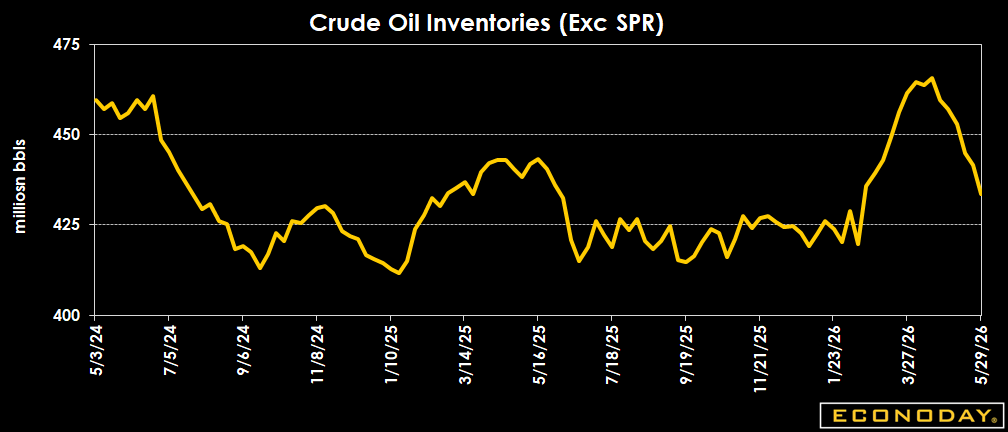

The crude draw intensifies. Gradually, domestic production is falling short of what the market requires, forcing companies to rely on existing stockpiles to fill the gap.

Persistent crude draws often lead to inflationary conditions as it drives up the cost of transportation.

Jun 3

U.S. crude oil inventories fell by 8.0 million barrels last week, pushing stocks 3% below the seasonal five-year average. Petroleum demand remains firm, with total products supplied up 3.0% from a year ago, while refineries continued operating at a strong 94.7% utilization rate.

3

8

24

3,846

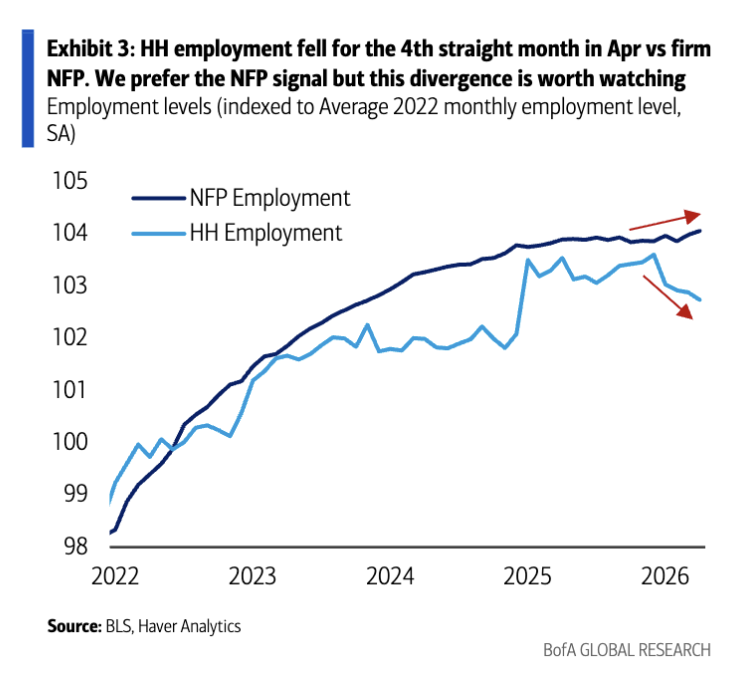

BoFA flags the divergence between NFP Employment and the Household Survey. This is not uncommon and it's happened before as well, as you can see.

The NFP data or Establishment Survey basically provides estimates of jobs.

The Household Survey provides estimates of employment status. The scope is wider and includes paid and unpaid employment, self-employment, farm workers, and those on unpaid leave.

10

11

67

25,843

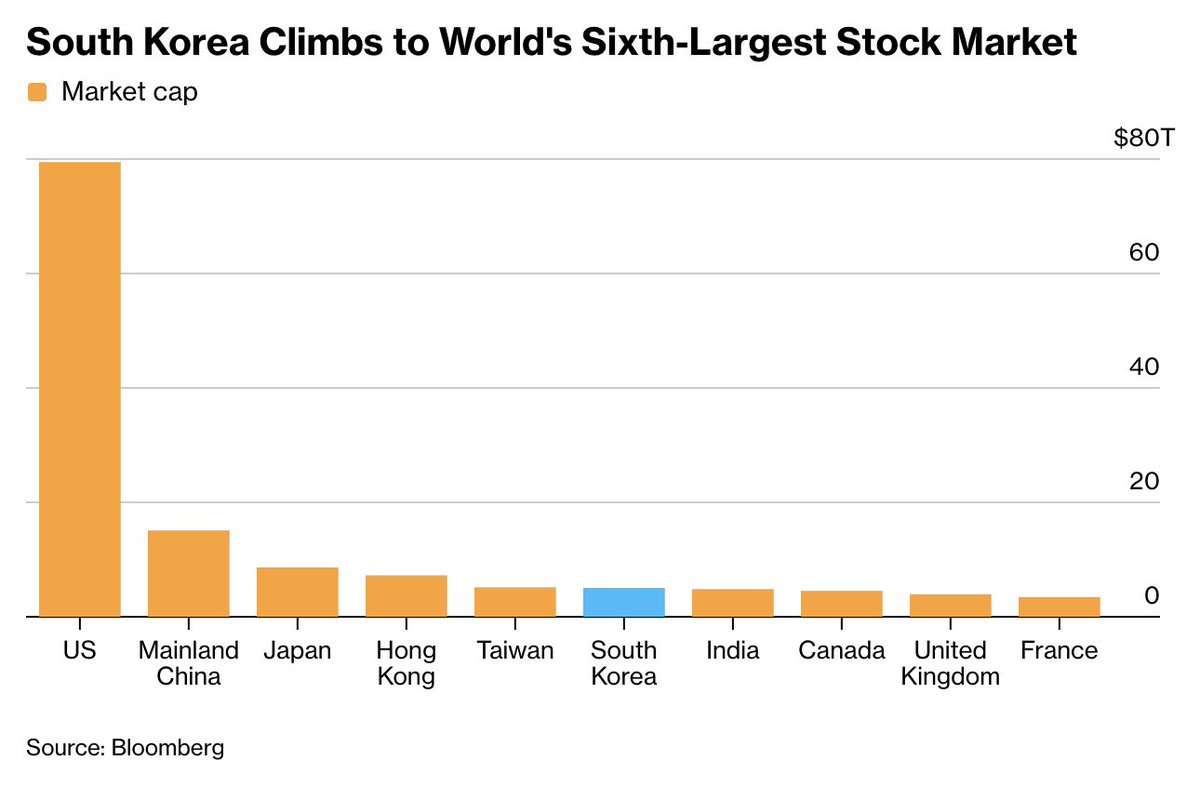

South Korea has claimed the spot of the world's sixth-largest stock market.

We all know this is largely driven by tech, specifically Samsung and SK Hynix.

3

13

86

7,773

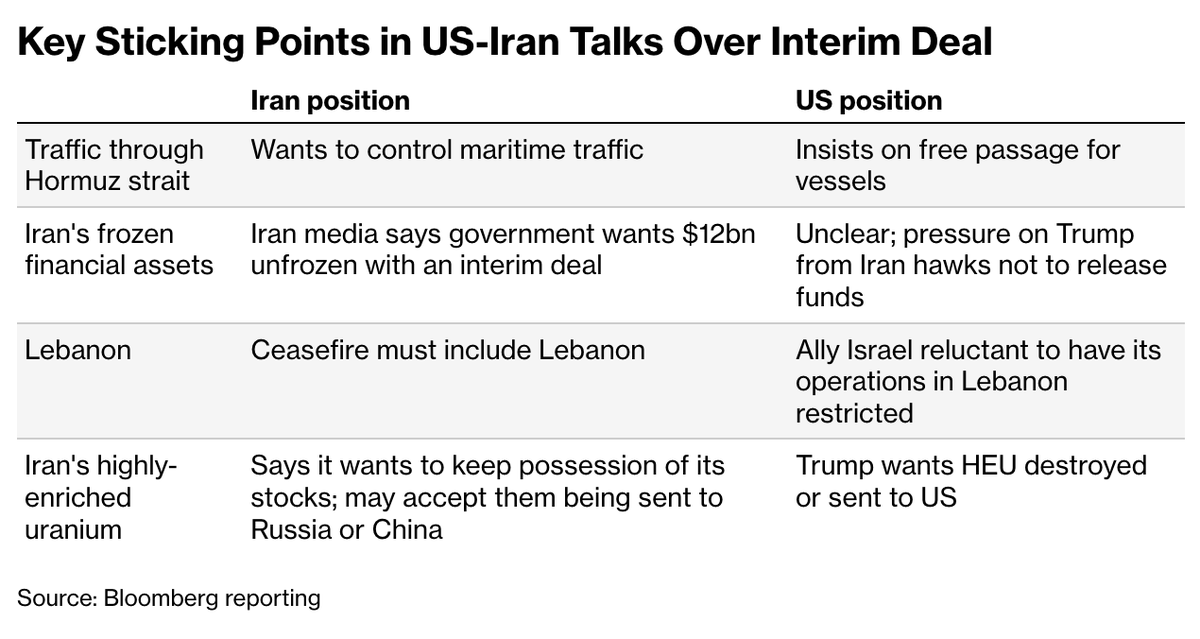

A quick summary on where the US and Iran differ on negotiations from Bloomberg.

While the Uranium enrichment issue is what started this whole fiasco, the deal has now very much turned to maritime trade.

The free passage through the SoH is the most important sticking point, and if this is not resolved, I doubt we will see a real deal.

5

1

22

2,293

May 28

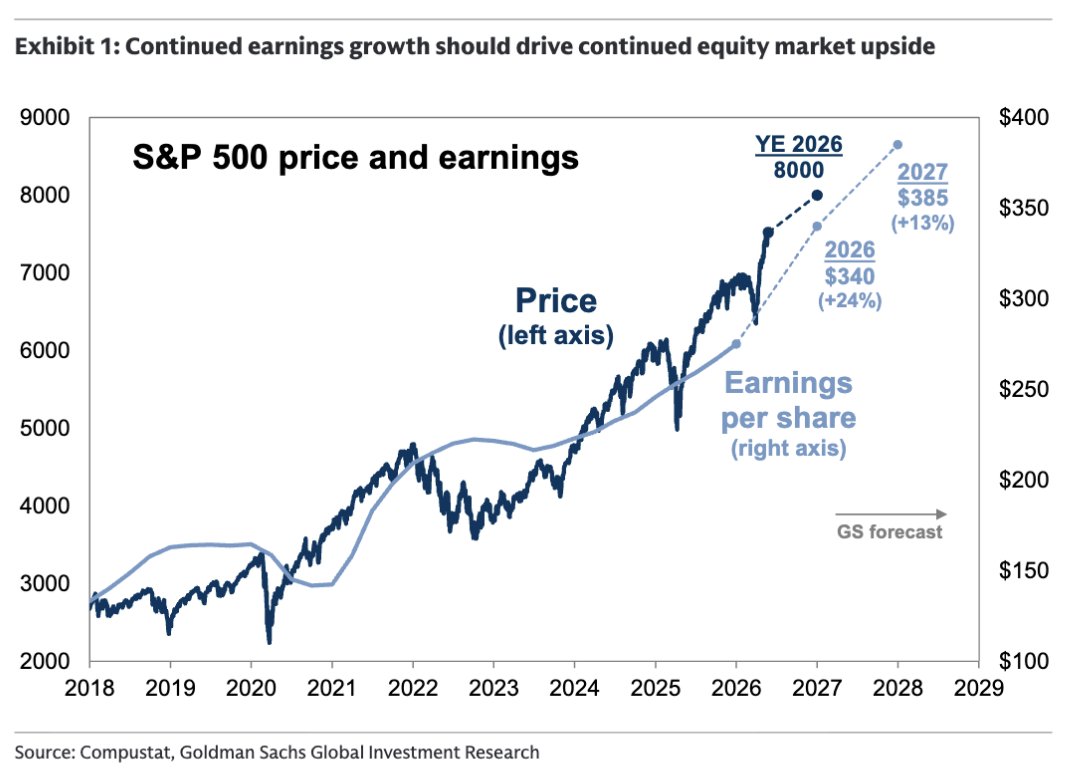

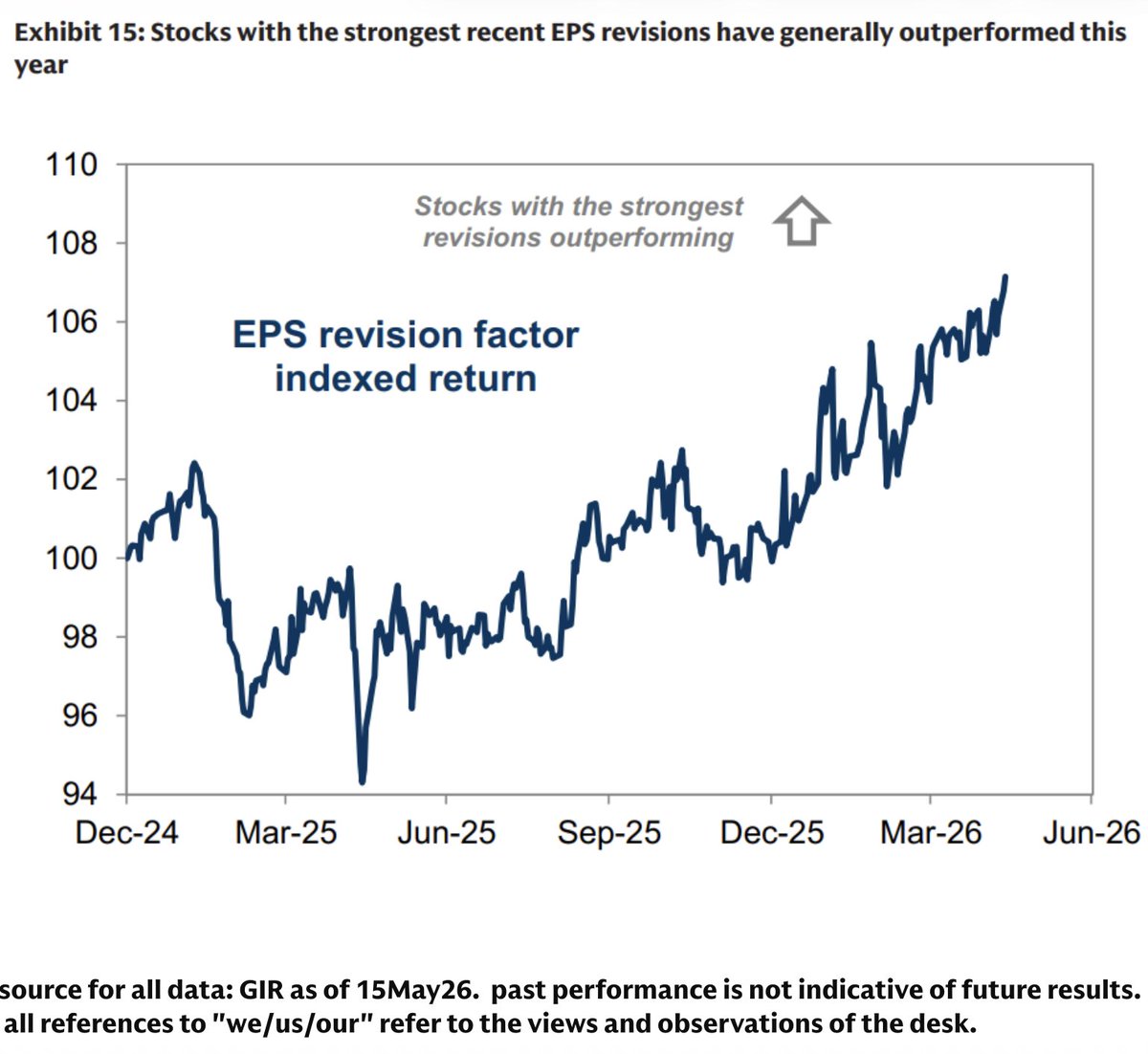

Goldman raised its year-end S&P 500 target to 8,000 from 7,600 on Wednesday, lifting 2026 EPS to $340 ( 24% year-on-year) and 2027 EPS to $385 ( 13%).

The entire target increase is attributed to earnings growth, not multiple expansion. The critical point is that AI infrastructure beneficiaries will account for roughly half of S&P 500 EPS growth this year.

Goldman's conditions for bull market termination, speculative mania and deteriorating macro fundamentals, remain largely absent. The risk is concentration, not valuation.

3

8

34

6,717

Ayesha Tariq, CFA retweeted

May 28

A peace deal is close, they said.

We're going to open up the Strait, they said.

11

9

95

7,890