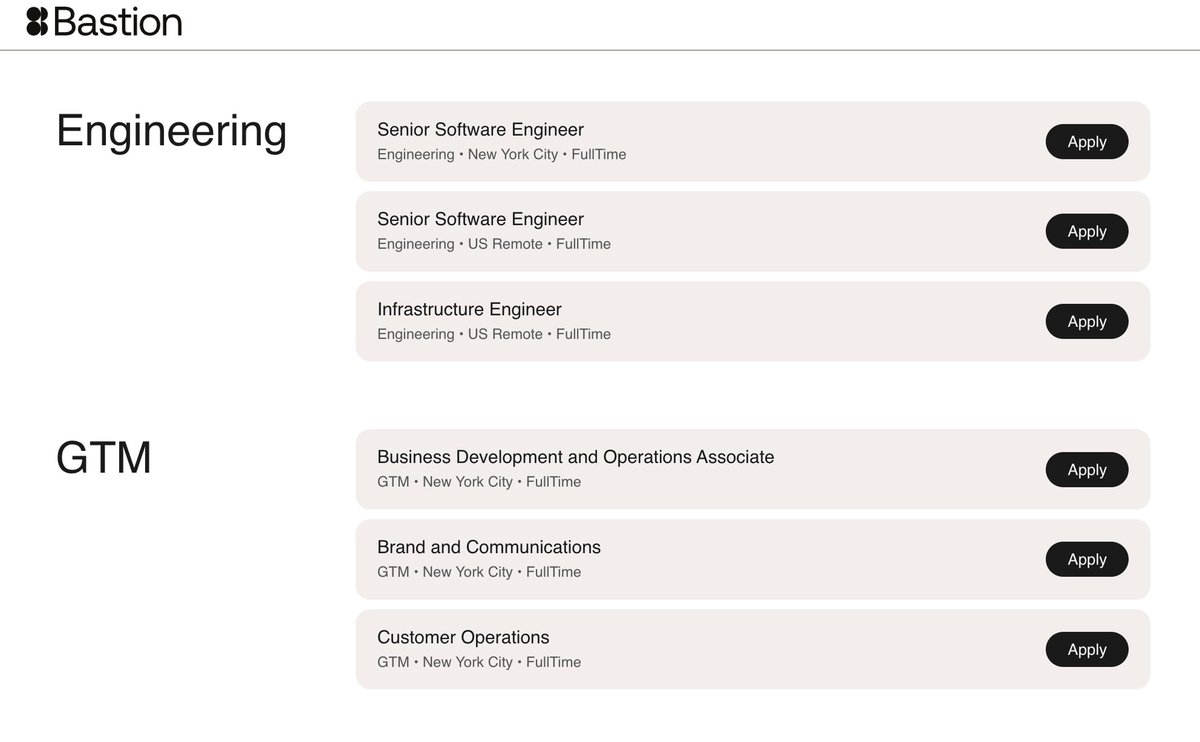

Bastion is the trusted stablecoin infrastructure for enterprises with wallets, custody, orchestration, and issuance. More details at: bastion.com

Joined May 2023

- Tweets 178

- Following 14

- Followers 6,194

- Likes 218

28 Photos and videos

Today, Bastion enters a new era, so we are launching our new brand and logo.

For the past three years we’ve been building quietly with banks, fintechs, and enterprises to create the next generation of compliant stablecoin infrastructure.

We’re moving into a future where compliance, custody, and orchestration are no longer separate pieces, they’re seamlessly integrated into one continuous, responsive platform.

Bastion handles KYC, stablecoin wallets, custody, orchestration, and issuance with compliance and security built in.

All under our licenses, or your own.

Ready to move beyond fragmented tools and deploy a unified stablecoin stack?

Visit bastion.com/ to get started.

7

15

3,177

1/ Trapped liquidity and reconciliation are two of the biggest operational pain points in B2B payments, and stablecoins solve them effectively.

At REDeFiNE TOMORROW 2026 with @SCB10X_OFFICIAL, Bastion Co-Founder & CEO @nassyweazy discussed how global enterprises regularly manage high-volume payment flows across multiple entities, currencies, and suppliers.

These payment flows create trapped liquidity, FX friction, slow settlement cycles, and complex reconciliation.

Stablecoins address many of these challenges with 24/7 near-instant settlement, lower FX costs, reduced trapped liquidity, on-chain ledgering, and stronger auditability.

1

4

4

942

2/ Watch the full interview: youtube.com/watch?v=L5bTSXRF…

863

1/ Today, Bastion On/Offramps APIs are live.

Most on/offramps operate like a disconnected add-on because they don’t integrate with the rest of your infrastructure.

That’s why we built a unified orchestration layer that fuses fiat ↔ stablecoin and stablecoin ↔ stablecoin conversions with virtual accounts, onboarding, custody, compliance, liquidity, and reporting.

With Bastion, businesses get more control over their stack, end-to-end workflow coverage, and lower operating costs than fragmented multi-vendor ramp architectures.

2

2

15

2,103

4/ Bastion is modular and agnostic.

That means your business can:

• Use Bastion wallets, or bring your own.

• Support the stablecoins and networks that fit your use case.

• Integrate with the providers and partners that best fit your workflows.

The goal is flexibility without fragmentation: your business can configure the stack around its needs while managing conversions through one connected orchestration layer.

1

2

196

5/ If you’re already operating at scale and tired of high ramp fees, vendor fragmentation, and constant integration friction, Bastion delivers what most platforms don’t:

End-to-end orchestration designed to support cost-efficient conversions with virtual accounts and minimize operational complexity as payment operations grow.

Learn more: bastion.com/

3

155

1/ Stablecoin adoption is accelerating fast: $6.25T in transaction volume so far this year, with Chainalysis projecting $719T by 2035

The opportunity is massive, but growth often comes with fragmented infrastructure

That’s the problem Bastion is built to solve ⬇️

3

4

15

1,277

3/ Bastion is built for companies ready to move beyond fragmentation

We deliver trusted stablecoin infrastructure without lock-in to a single chain, stablecoin, or vendor

This gives you a neutral full-stack solution to issue, custody, move, and convert stablecoins at scale:

• Access to all products through a single API

• Built-in compliance checks, monitoring, and screening

• Direct connections to banking and liquidity partners

• Flexible architecture designed to scale with your business

1

308

4/ Growth should expand your business, not your infrastructure problems

Build with Bastion: bastion.com/

200

Spot on

We are the full stack solution to securely issue, custody, move, and convert stablecoins, under our licenses or your own

May 15

The $400B Map: Who's Actually Moving Stablecoins Outside the US?

If you only know Bridge, you're seeing a fraction of the market.

Real-world stablecoin payment volume hit $400B in 2025, with 60% being B2B. Bridge covers 35 countries. The math doesn't work and yet most fintechs I talk to still default to "we'll just use Bridge."

Here's the uncomfortable truth: stablecoin infrastructure has gone regional, and the strongest players in each corridor aren't household names in San Francisco.

Three years ago, "stablecoin orchestration" meant a handful of US-based APIs. Today, every major payment corridor has its own pure-play, built by people who actually understand local rails, mobile money, central bank relationships, and FX realities on the ground.

That's why a B2B treasury team paying suppliers across Lagos, São Paulo, Jakarta and Dubai doesn't need one provider. They need a regional stack.

The Global Stablecoin Money Movement Map:

🇺🇸 USA & Canada: the API-first layer Sphere Labs, Mural Pay, Brale, Modern Treasury, Bastion, Iron (by MoonPay), Conduit, Routefusion, Crossmint, Cybrid, HopNow

🇪🇺 Europe: MiCA-native, EU passporting BVNK, Due, Currencycloud, Rapyd, Merge Money, Fipto, Depa, OpenPayd

🇧🇷 LATAM: built around PIX, SPEI, local FX volatility Bitso, dLocal, Pomelo, CambioReal, BlindPay, Koywe, Avenia, Mesta

🇦🇪 UAE & Middle East: the fastest-regulated jurisdiction in the world Fasset, TransFi, Hubpay, Fuze Finance, damex io

🌍 Africa: mobile money meets stablecoin sandwich Yellow Card, Flutterwave, Conduit (deepest Africa coverage at 23 countries), Juicyway, NALA/Rafiki, Nestcoin, ivorypay, Quidax, Paychant, VALR, Kotani Pay

🌏 Asia: the fastest-growing region globally FOMO Pay, StraitsX (~$30B cumulative volume), Tazapay, Triple-A, Coins ph, PhotonPay, Reap (just acquired by Kraken for $600M)

The aggregation layer stitching them together: Borderless xyz turns this regional fragmentation into a single API by plugging into local liquidity providers across markets.

Why this matters for anyone building cross-border:

Bridge charges up to 1% FX. Conduit ships ~10 bps. Bridge has zero local rails in APAC. BVNK processes $30B annualized. Fasset just hit $32B annualized across 50 corridors in Asia, Africa and the Middle East after its $51M Series B.

The point isn't that Bridge is worse. It's that "global stablecoin infrastructure" was always a regional game pretending to be global. The market has split into specialists, and the winners in each corridor have already emerged.

If you're picking a stablecoin partner in 2026, the right question isn't "who is the Bridge of X?"

It's: "Which corridors do I actually need, and who owns the rails there?"

PS: And if you need a card acceptance gateway to plug into your stablecoin flows, that's exactly why we built @subyhq

1

1

9

1,546

Last night, we hosted a private dinner in Miami with @AlliumLabs and @awscloud ahead of @consensus2026, bringing together leaders across banking, fintech, and payments sectors

The momentum around stablecoin infrastructure is accelerating. If you're in Miami this week, let's talk

1

13

873

Bastion is your new stack for global finance.

1⃣ Custodial wallets

2⃣ Orchestration in 60 countries

3⃣ Issuance

Better. Global. Money. 🌎💵

8

1,015

At Bastion, we believe that a rising tide lifts all boats, especially when bringing the global money supply onchain.

Just like bridges, DEXs, and CEXs, stablecoin issuers are becoming the target of hacks and minting bugs.

Time to focus on security to bring trillions onchain.

4

11

1,552

Platform operators invest millions building networks that connect people and businesses. Yet substantial value leaks out when transactions move off-platform.

When suppliers use wire transfers instead of platform payment systems, or creators withdraw funds through third-party tools, platforms lose both fee revenue and transaction data that could strengthen their ecosystem.

Our latest blog post explores why transaction leakage happens and how platforms can retain value by keeping transactions in-network.

We examine real-world examples across business models:

→ Disney's closed-loop rewards

→ Fortnite's creator payouts

→ Shopify's merchant banking

We quantify the hidden costs of off-platform transactions, and break down how branded stablecoin infrastructure transforms closed-loop systems into open ecosystems while maintaining platform control.

Link to the blog post below ⬇️

7

1

32

3,847

Here's the link to the blog post: bastion.com/blog/why-platfor…

2

1

6

2,554

We're thrilled to announce that Sony Bank is partnering with Bastion to deliver compliant stablecoin solutions for their digital asset initiatives.

Sony Bank joins a growing ecosystem of major institutions choosing Bastion's regulated rails to unlock new possibilities in digital finance.

This partnership follows Bastion’s backing from @Sony_Innov_Fund

@cbventures, @SamsungNext, @a16zcrypto, and @hashed_official.

Together, we’re laying the groundwork for a more programmable, efficient and cohesive global financial system. Only the beginning 🚀

Read more below ⬇️

16

22

88

51,726