Equable educates employees, retirees, policymakers, and stakeholders about how to achieve retirement plan sustainability, accountability, and income security.

Joined March 2019

- Tweets 261

- Following 66

- Followers 117

- Likes 201

90 Photos and videos

Equable Institute retweeted

16 Dec 2025

So... @LAFPP LA Fire and Police Pension is an investor in Vista Foundation Fund IV, the private equity pool used to buy ESO, the company that's been accused of creating financial stress for rural and small public safety departments.

x.com/anthonyrandazzo/status…

15 Dec 2025

This story from @ByMikeBaker about a venture-backed company potentially financially squeezing rural fire departments is interesting. The PE fund used to back ESO — Vista Foundation Fund IV — is heavily financed with public pension dollars. At least 20 LPs are state ret. systems.

1

1

147

Equable Institute retweeted

15 Dec 2025

This story from @ByMikeBaker about a venture-backed company potentially financially squeezing rural fire departments is interesting. The PE fund used to back ESO — Vista Foundation Fund IV — is heavily financed with public pension dollars. At least 20 LPs are state ret. systems.

1

1

239

Equable Institute retweeted

18 Nov 2025

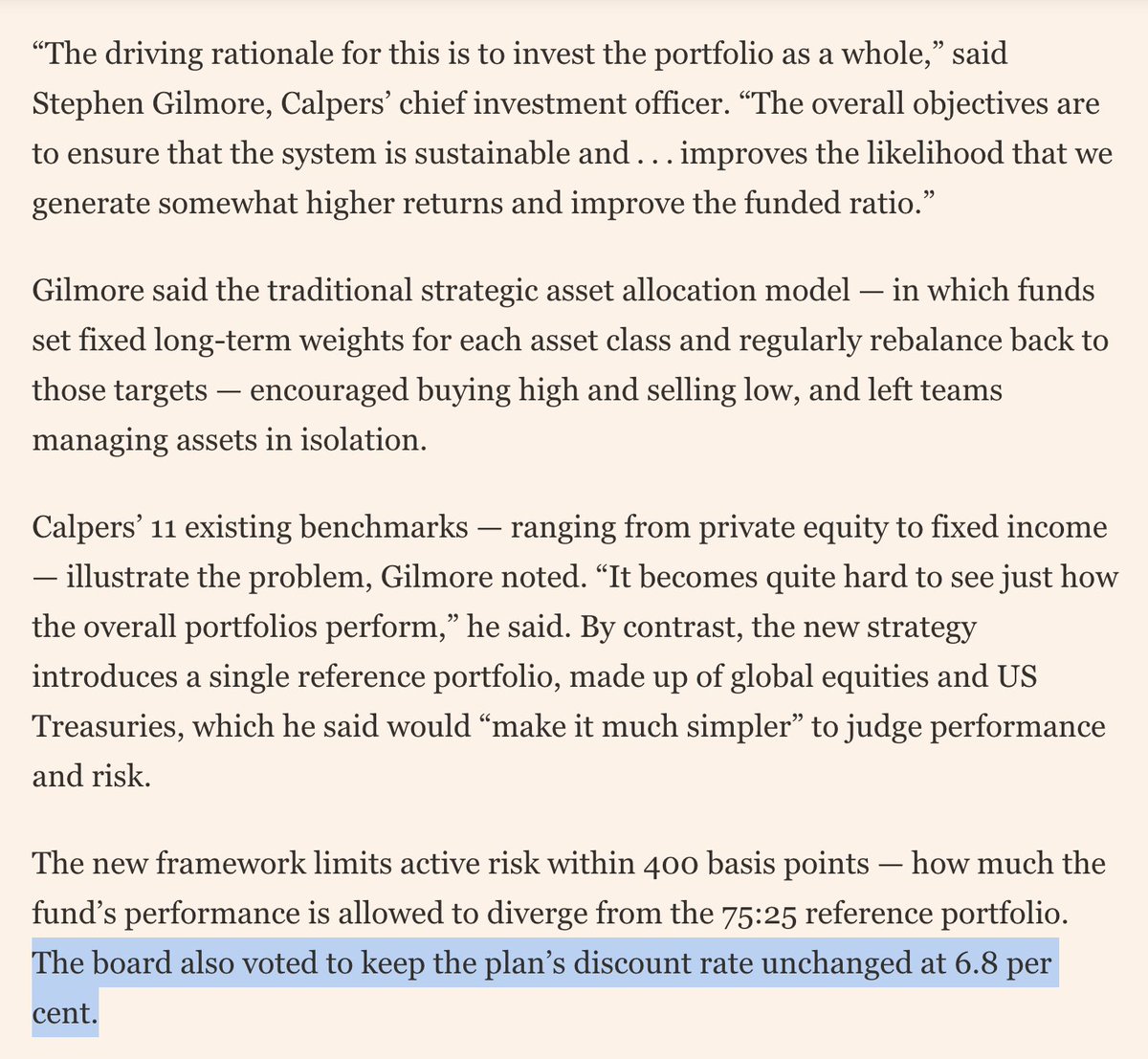

CalPERS is shifting its internal approach to measuring investment success by adopting a "total portfolio benchmark." This approach has pros/cons, but what shouldn't be lost is that CalPERS has always had a single benchmark it should hit—the assumed rate of return.

There is value in having a benchmark for investment performance relative to peers, or relative to what was possible in the market. In practice, though, many public plan investment benchmarks are soft targets that can be gamed by investment managers. Plus the heavy media attention on portfolio benchmarks often obscures the most important target— what actuaries assumed returns would be when calculating contribution rates.

Public plans aren't the same as other institutional investors when it comes to how we should think about their success. Beating the market, or beating other investment managers doesn't always mean a pension fund is appropriately funded. And when investments underperform the assumed return, the price is paid for by taxpayers (higher govt employer contributions) and public employees (higher member contributions, lower pay, or both).

1

1

115

Equable Institute retweeted

24 Oct 2025

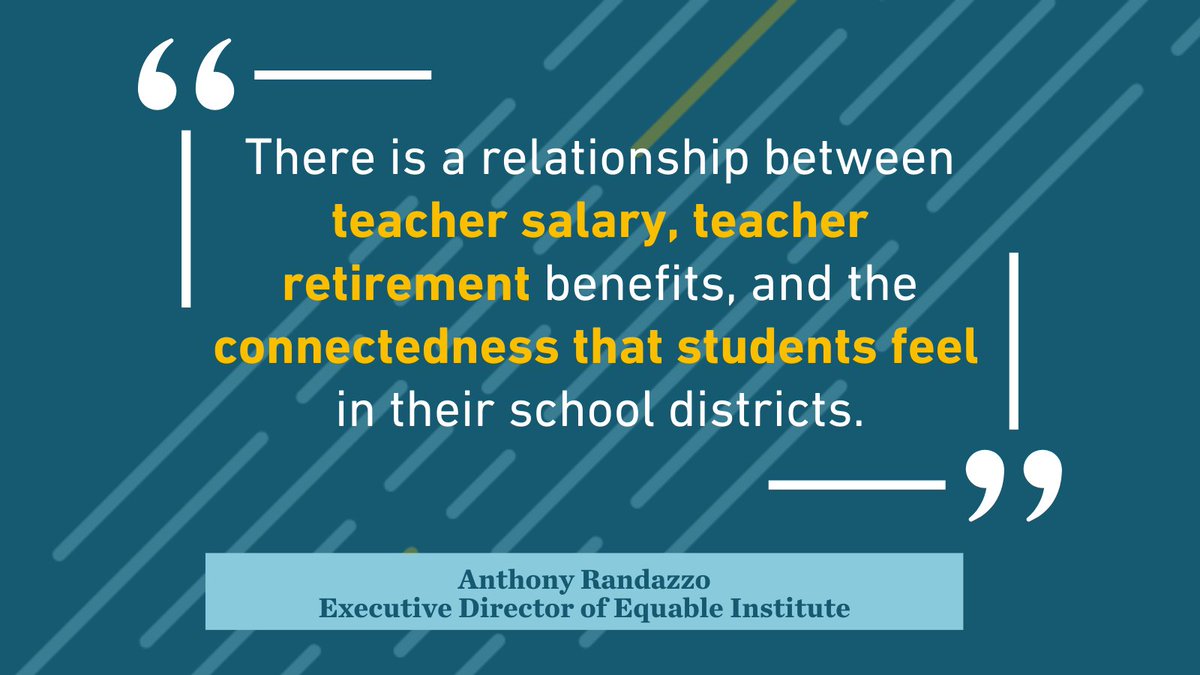

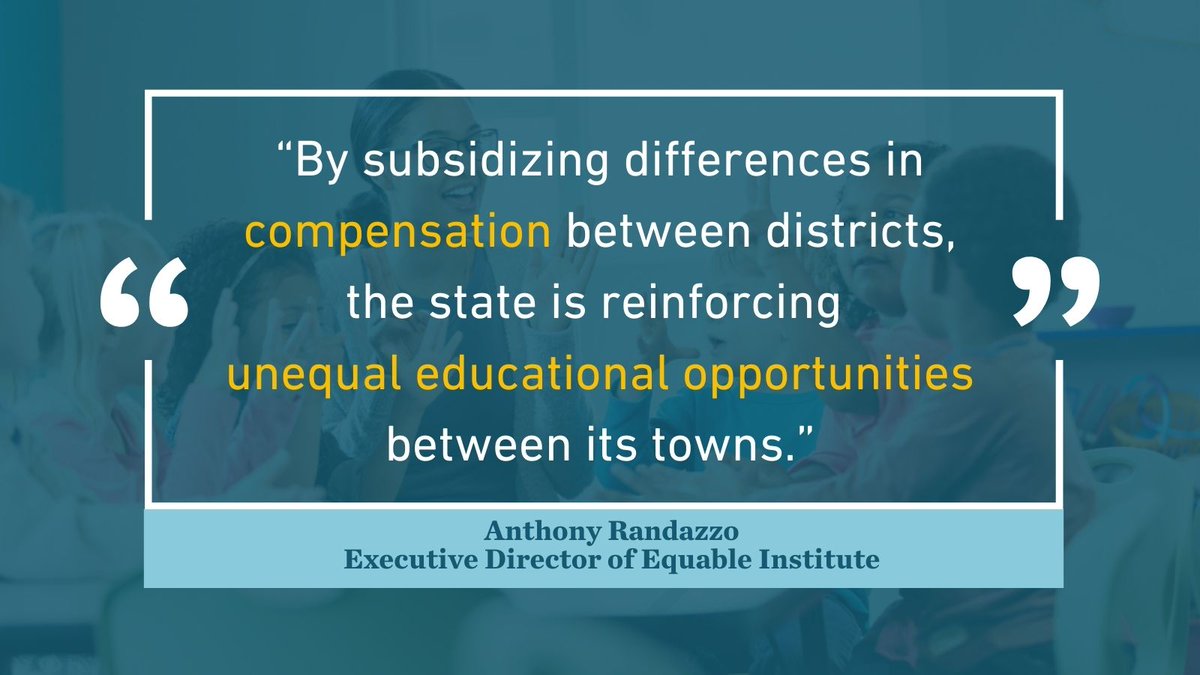

Out TODAY: "Intent of CT's ed finance system is to create a more equitable landscape of resources for educating students," @anthonyrandazzo from @EquableInst. "The way that the state goes about financing (TRB) is running counter to that."

ctinsider.com/news/education… via @insider_ct

2

90

Equable Institute retweeted

16 Jul 2025

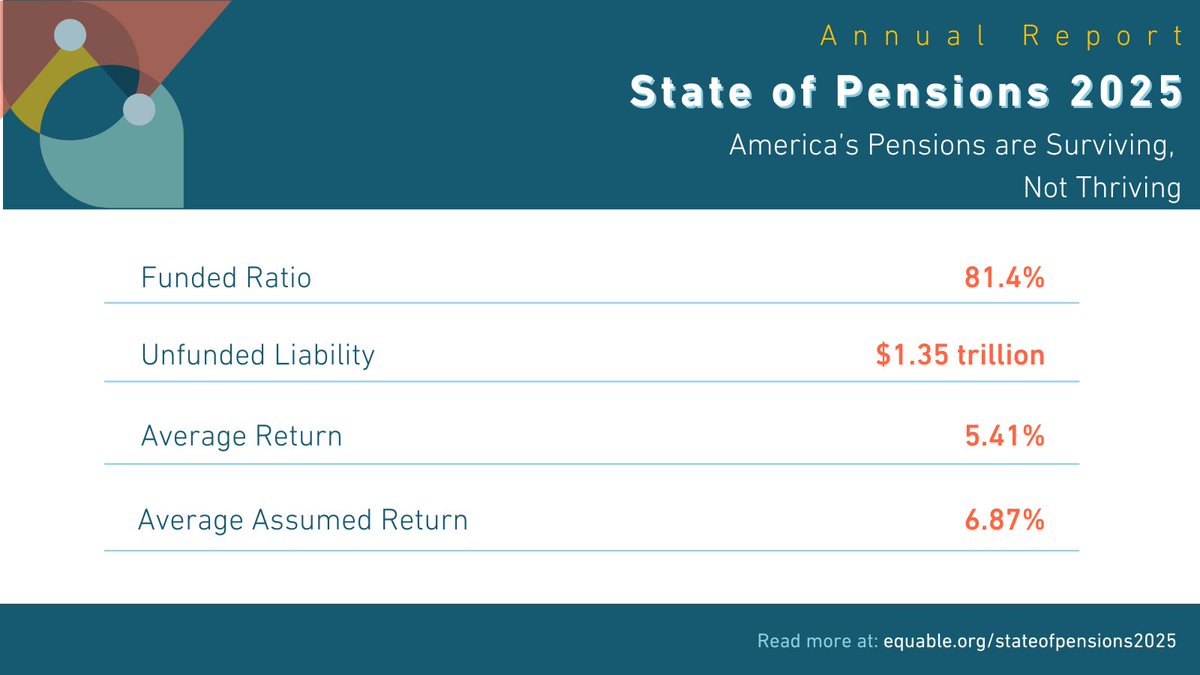

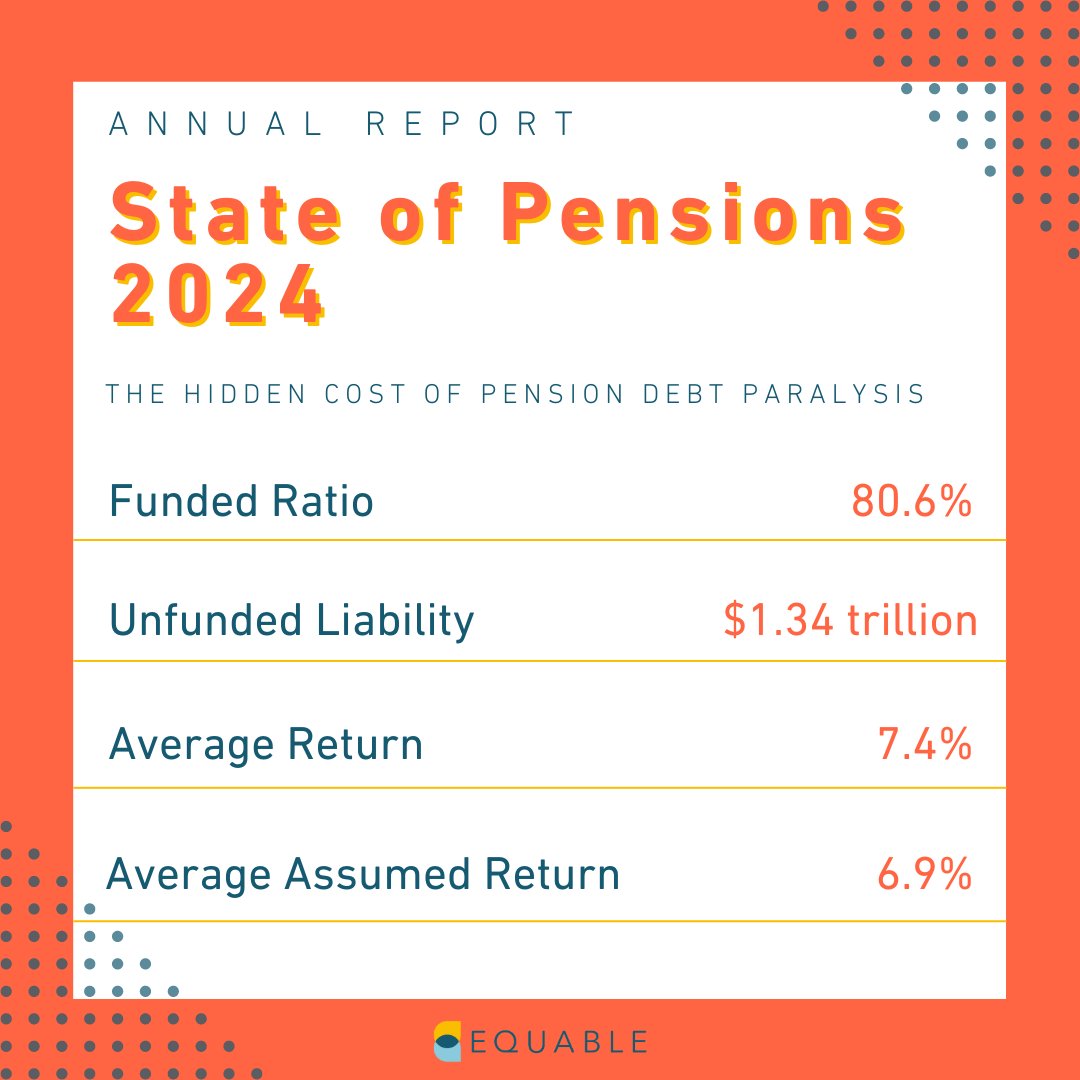

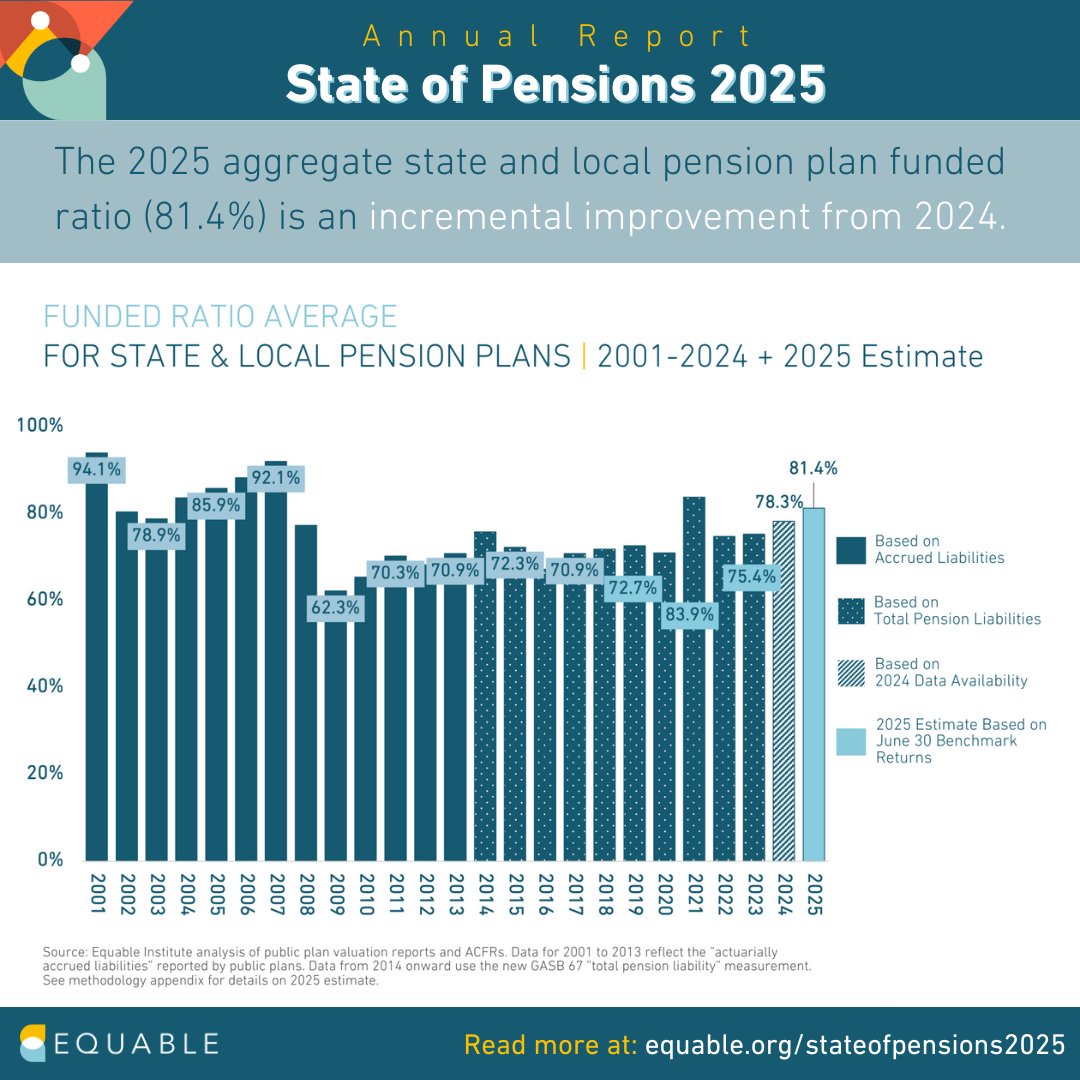

📈New: We published State of Pensions 2025 today, an 80 page financial analysis of state and local plans. Toplines:

- national funded ratio is ⬆️ to 81.4%, this is still very fragile

- investments returned 5.4% for FYE 6/30 on ave, below assumptions

Here's a quick summary 🧵

1

1

8

198

16 Jul 2025

Today, Equable released the 2025 edition of our annual report, State of Pensions. Despite underwhelming investment returns, public pension funds will see a funded ratio improvement in 2025. Read more here: bit.ly/4nQYqQ4

27

Equable Institute retweeted

11 Jun 2025

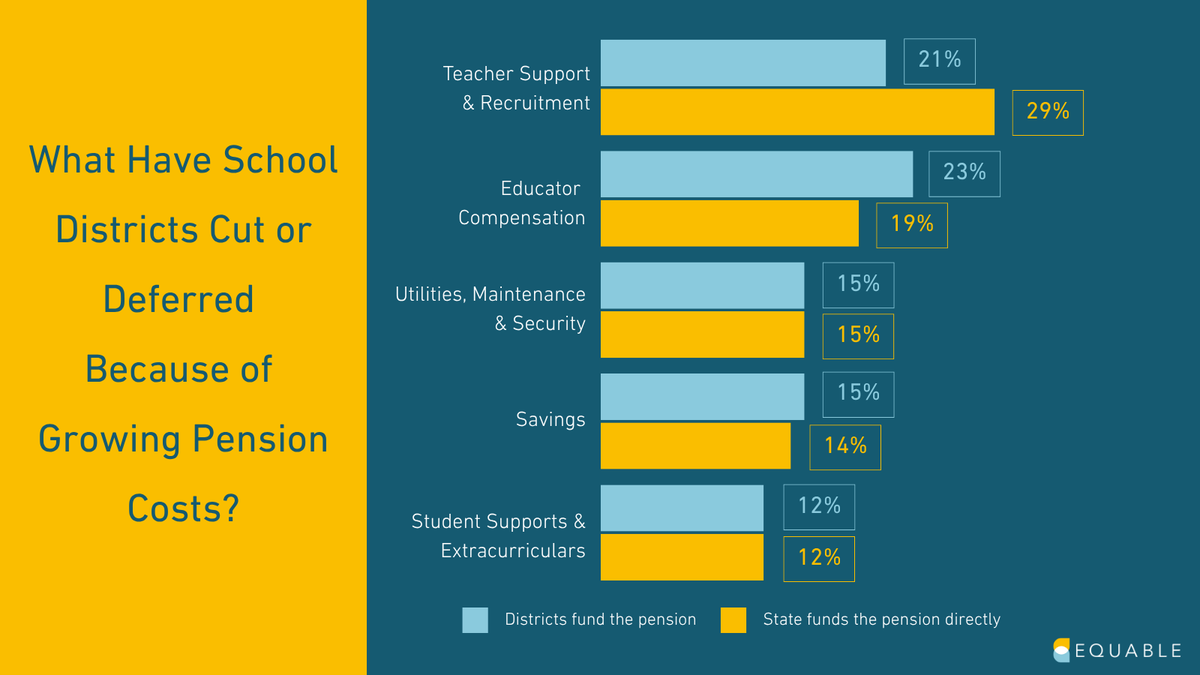

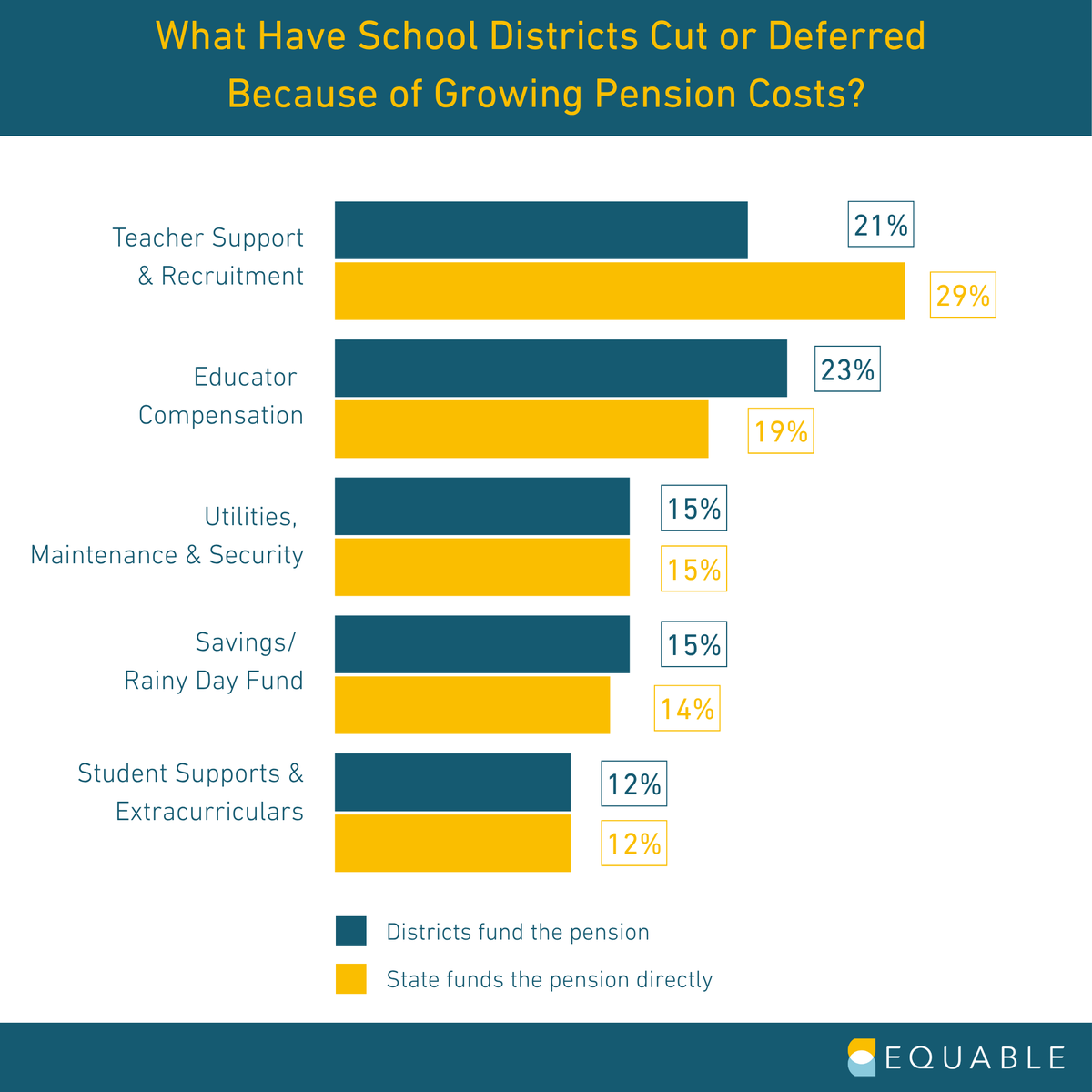

🗞️NEW TODAY: 1 in 3 school districts are cutting classroom priorities because teacher pension costs are devouring K-12 budgets.

Survey data reveals reports from school board members and district admins on what they are cutting explicitly because of growing pension costs. 🧵

1

11

13

2,931

11 Jun 2025

#NewBrief: At least one-third of school districts report funding cuts due to rising pension costs in the last five years and it's impacting teacher pay, support programs, and more.

Read it here: bit.ly/45oF2mZ

32

Equable Institute retweeted

14 Apr 2025

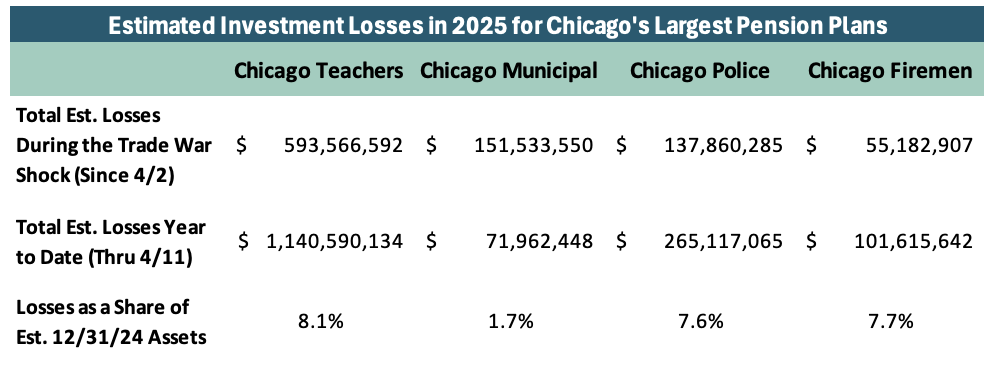

🧵 NEW: Chicago's big four pension funds have lost ~$1.58 billion since the start of 2025.

$938 million of that came in just the past 7 trading days since the "Liberation Day" tariff announcement.

Here's why this is a particularly serious problem.

15

26

112

70,613

Equable Institute retweeted

14 Apr 2025

UPDATE: When markets closed Friday, the top 25 public pension funds had lost an estimated $140.7 billion in 2025, of which $67b was since the 4/2 global tariff policy. This is less than the "pre-pause" market bottom, but still a significant problem. Let's see what today brings.

9 Apr 2025

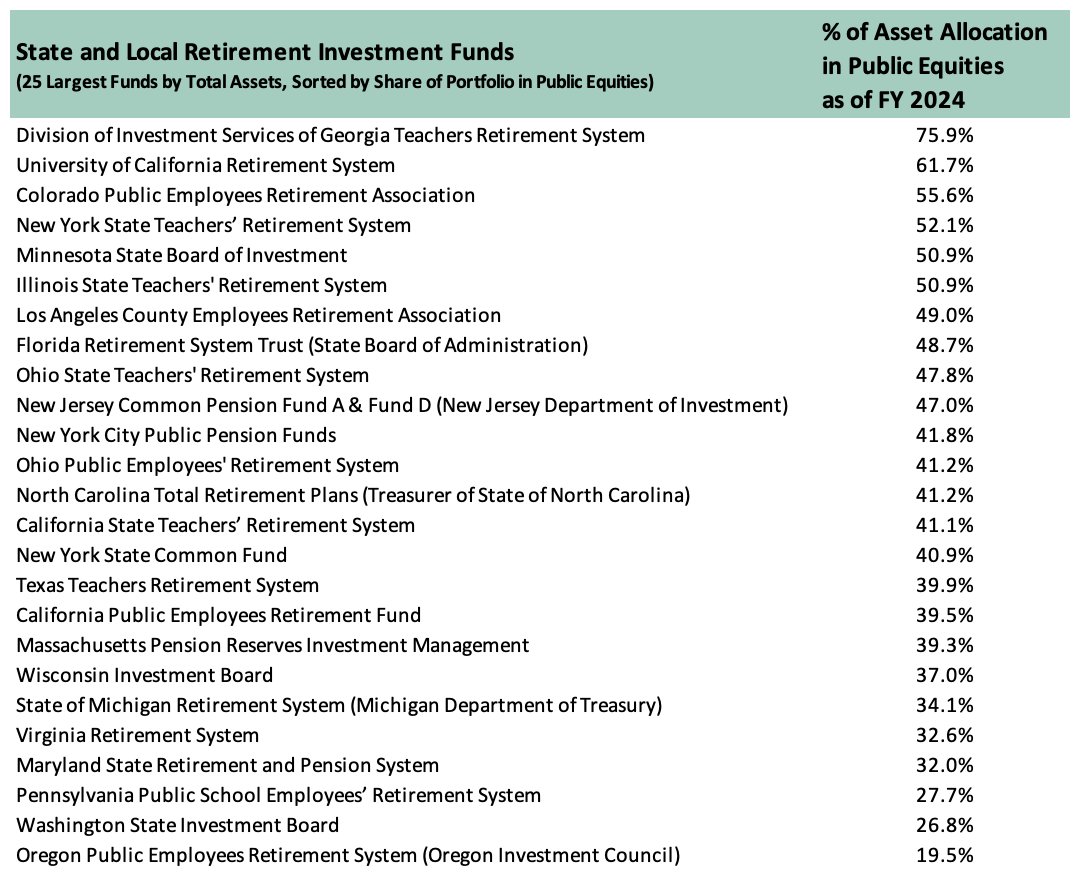

Before the tariff pause and market rally today, the top 25 U.S. pension funds (shown below by % of assets in equities) had lost ~$169 billion in just the last four trading days. Here's an update on what losses have been trimmed and what pension funds should be worried about.

1

1

260

31 Jan 2025

Connecting the Dots: It turns out that by making CT teacher pension financing more fair and equitable, the state can also save hundreds of millions of dollars that could be reinvested into education. @CCMAdvocacy @DalioEducation

Learn more: bit.ly/40H6msG

1

39

30 Jan 2025

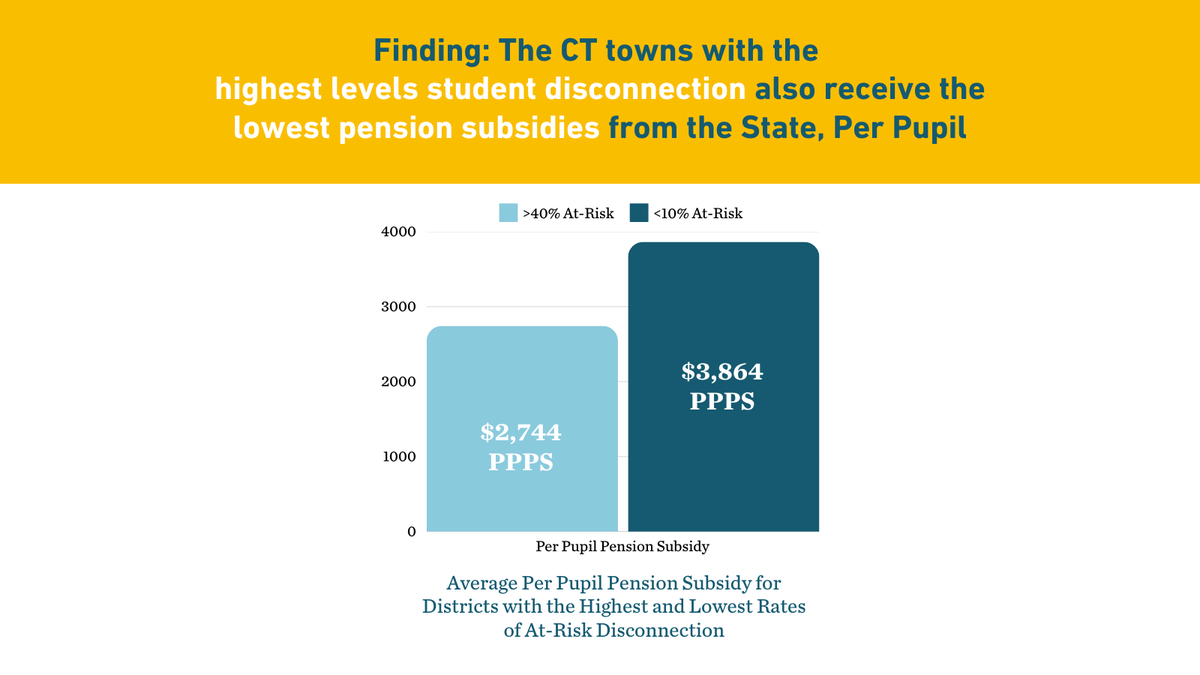

The 119K Commission (@CCMAdvocacy and @DalioEducation) uncovered high rates of youth disconnection across CT schools.

Do high-need districts deserve more or less state funding for teacher compensation?

Should be a no brainer. bit.ly/40P3U4m

26

29 Jan 2025

Don't miss our new brief, which shows a relationship between CT’s investment in teacher retirement and the percentage of disconnected youth in Connecticut public school districts.

@CCMAdvocacy @DalioEducation

bit.ly/40H6msG

2

1

86

28 Jan 2025

#NewBrief: Connecting the Dots on Disconnected Youth: CT Towns with Highest Percentages of Disconnected Youth Receive Lowest Per Pupil Pension Subsidies from the State

#news #CTPensionSubsidy #CTPress @joedelongCCM @CCMAdvocacy

Read all about it here:

bit.ly/40P3U4m

20

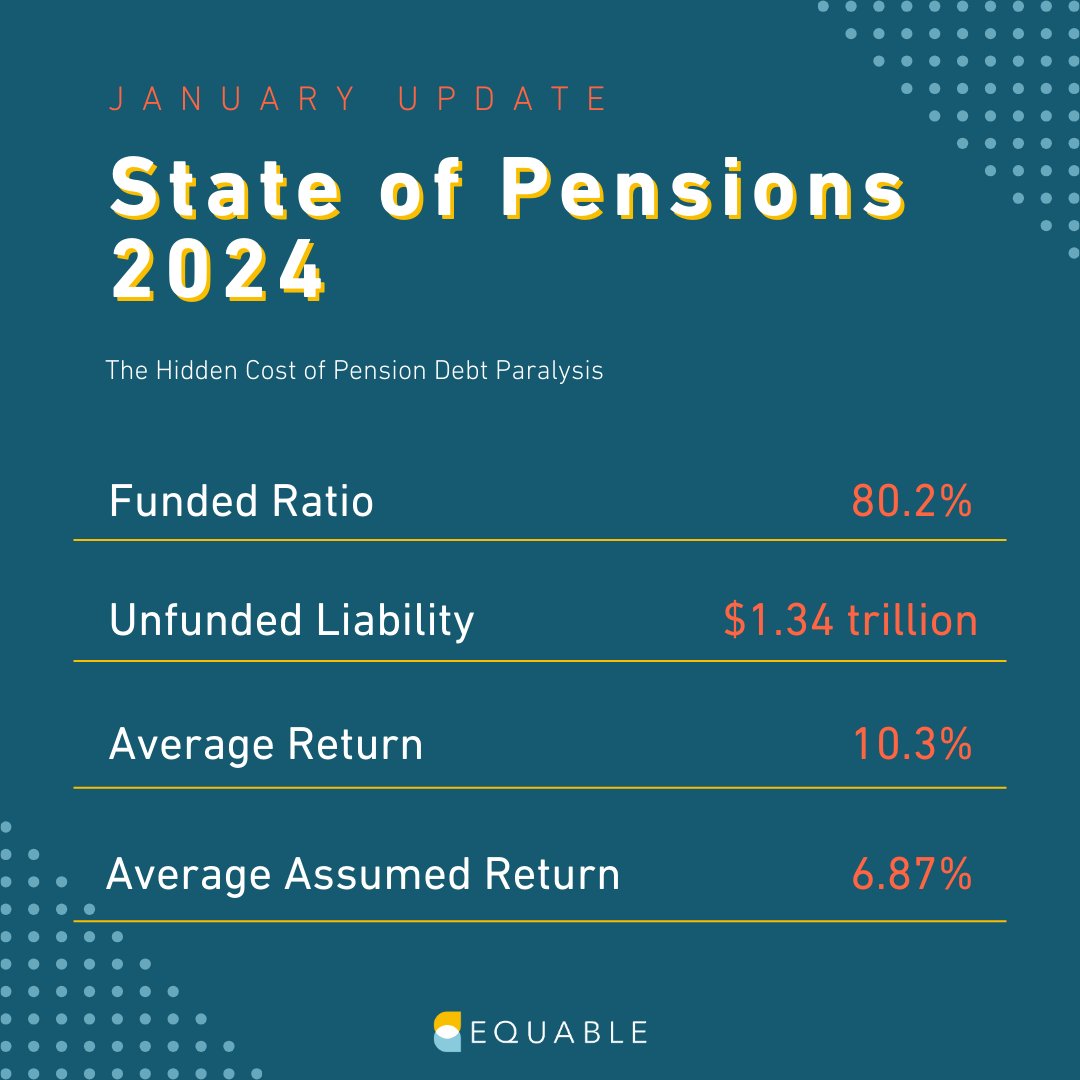

8 Jan 2025

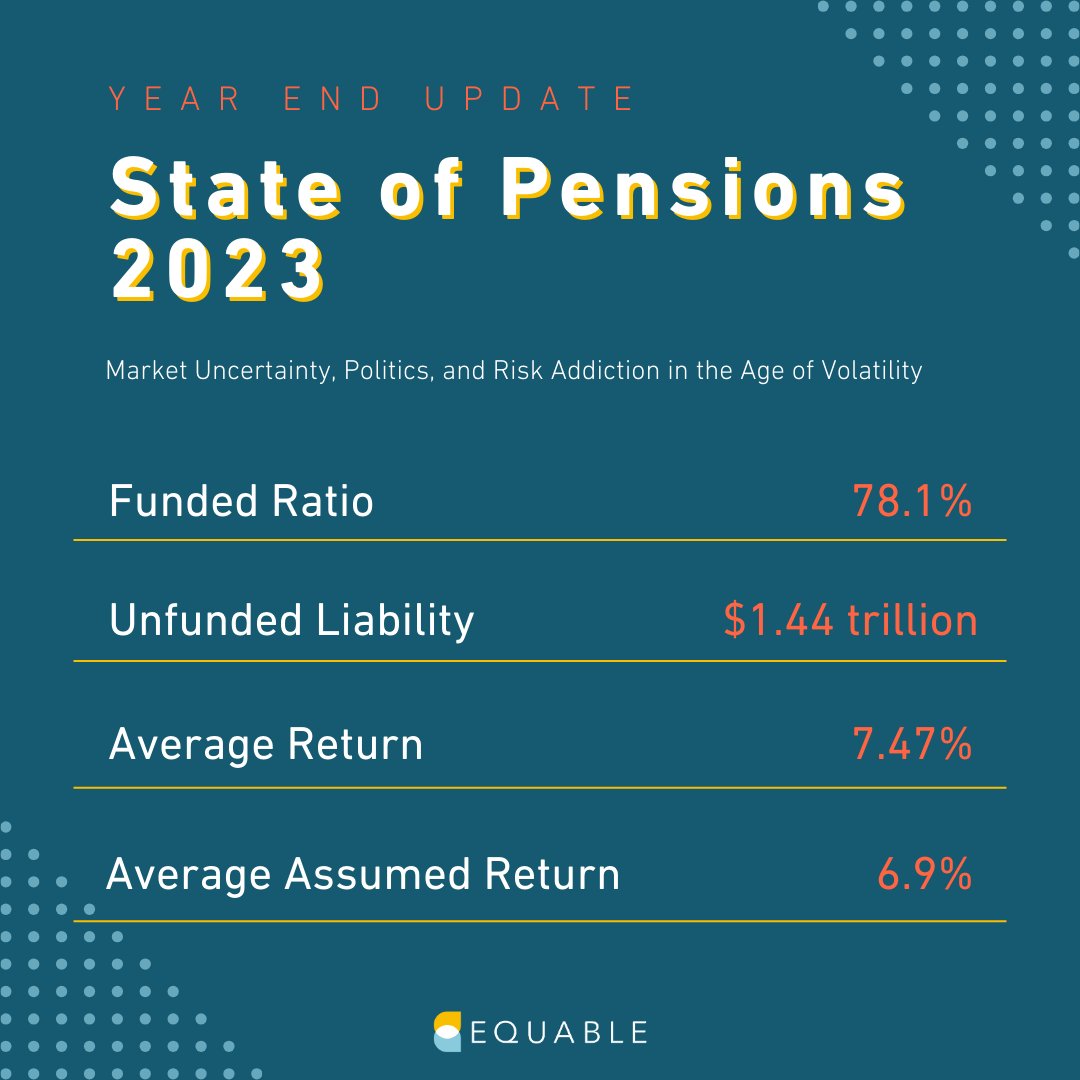

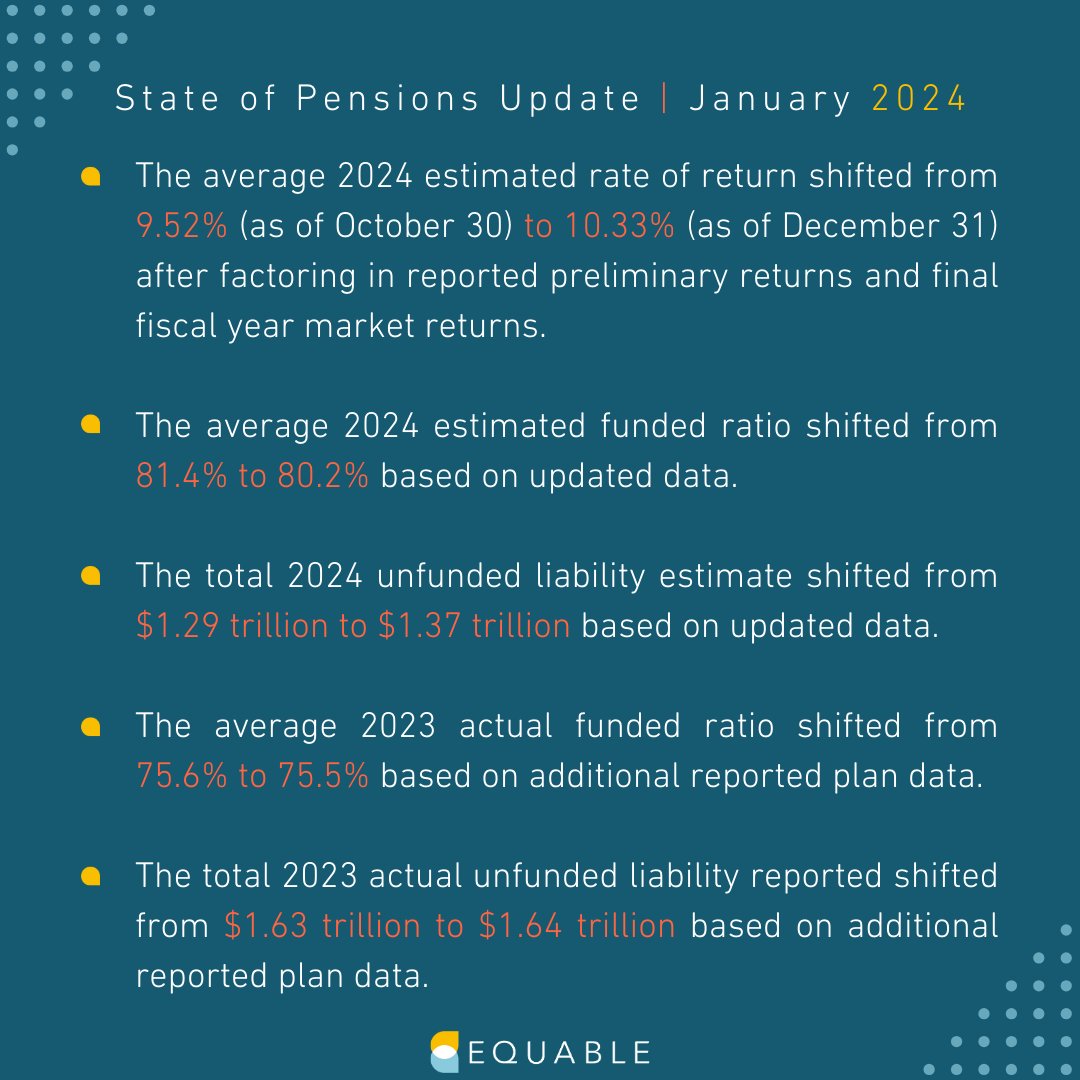

Today, Equable released the Year-End Update to State of Pensions 2024. Public pension funds have fared well this calendar year, thanks to strong market performance. Continued Read the report here: bit.ly/3BO8eHH

1

17

18 Nov 2024

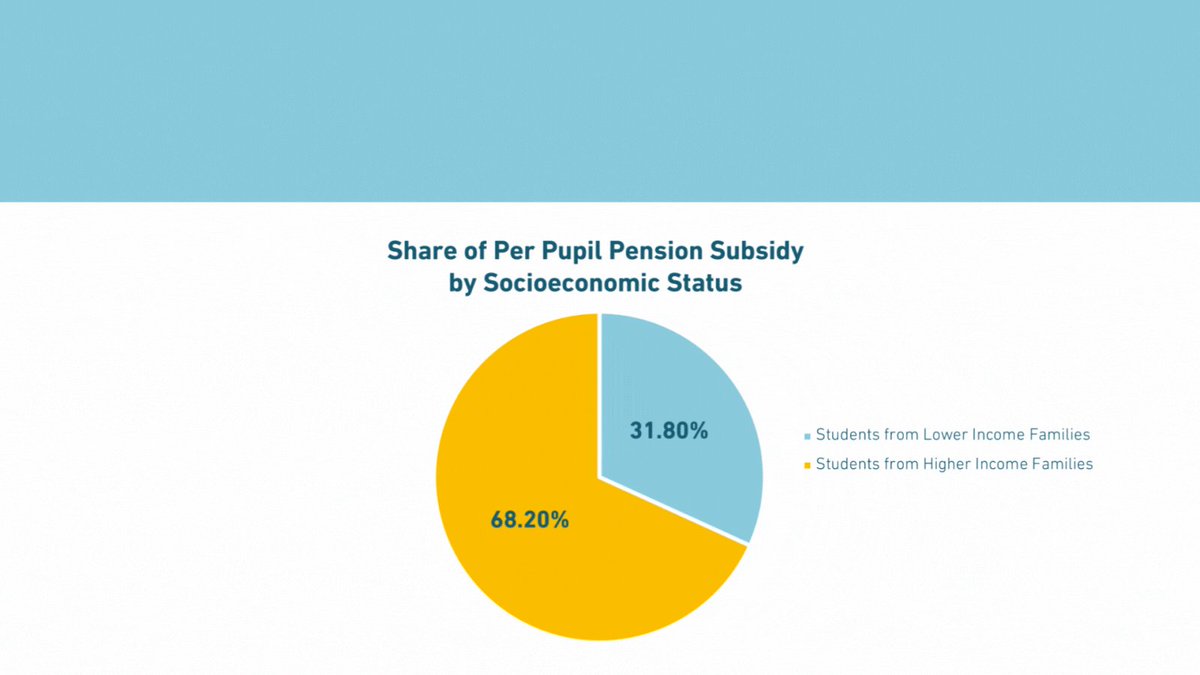

WHO BENEFITS from the state’s inequitable #CTPensionSubsidy?

↪ More affluent school districts.

42% of Connecticut students come from lower-income families... But they receive only a 32% share of the Per Pupil Pension Subsidy.

bit.ly/48RtIzf

1

199

15 Nov 2024

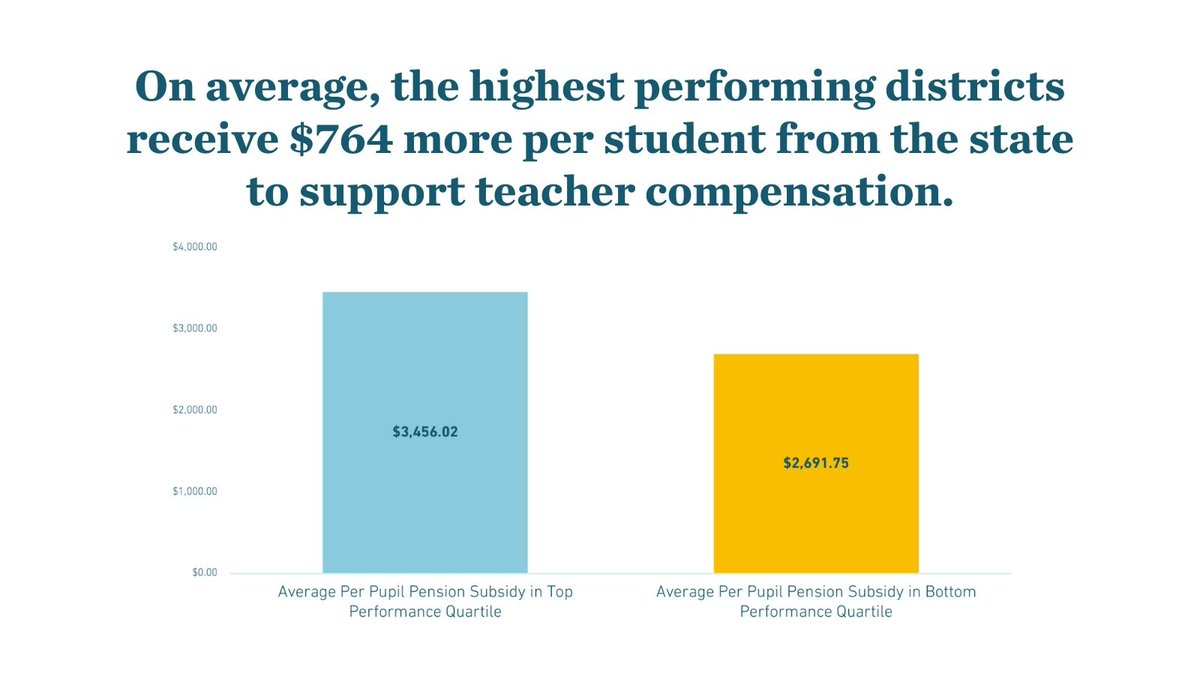

On average, the highest performing districts in CT receive $764 more per student from the state to support teacher compensation. #CTPensionSubsidy

Learn more: bit.ly/48RtIzf

1

22

14 Nov 2024

💡#NotSoFunFact: Connecticut's funding of teacher pension obligations favors wealthier, less diverse, and higher-performing public school districts.💡

Full report here: bit.ly/48RtIzf

1

2

106

14 Nov 2024

#PressRelease: CT’s Teacher #Pension Financing is Reinforcing #Inequity

Read all about it here: bit.ly/3Z6QZKg

#news #CTPensionSubsidy #CTPress

1

3

32

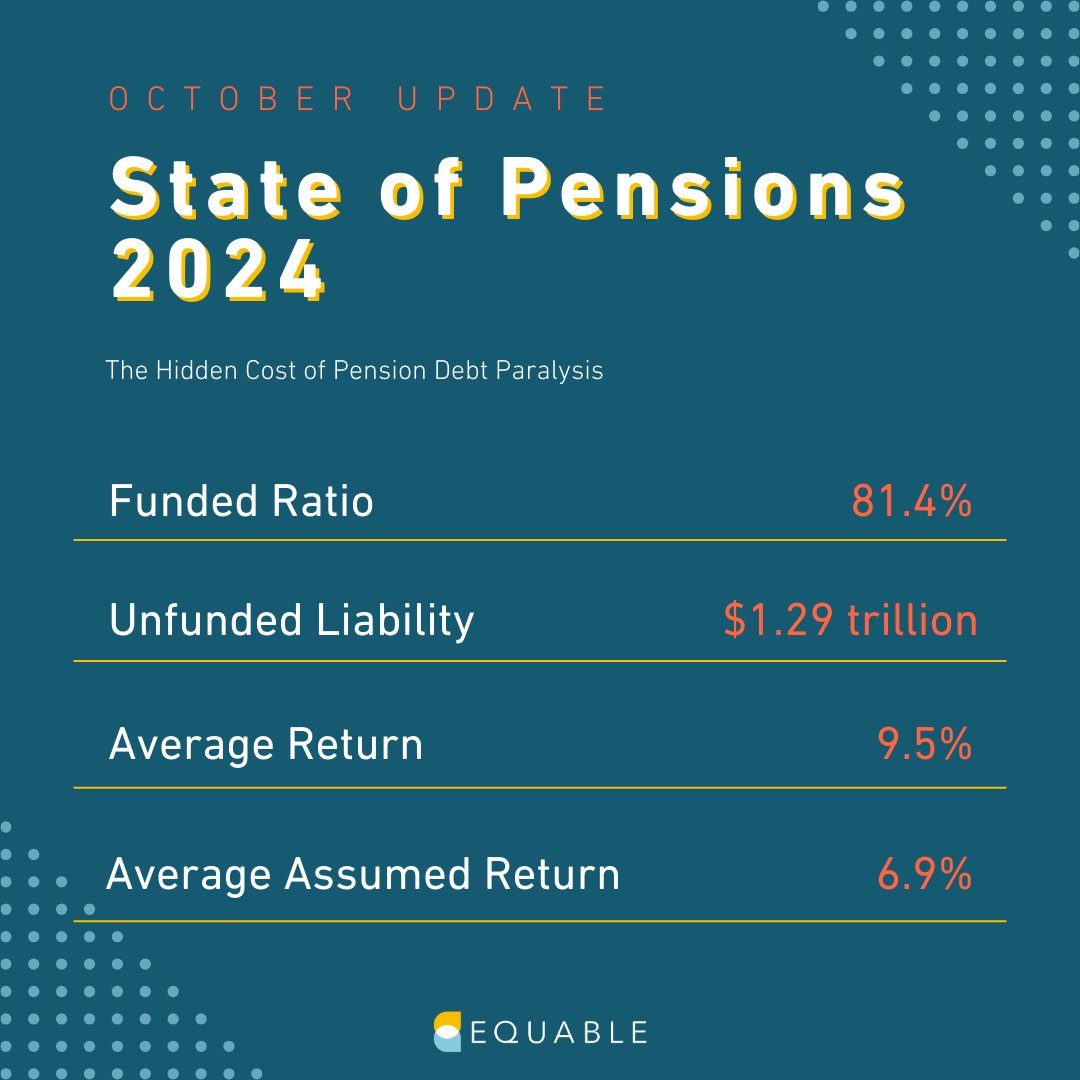

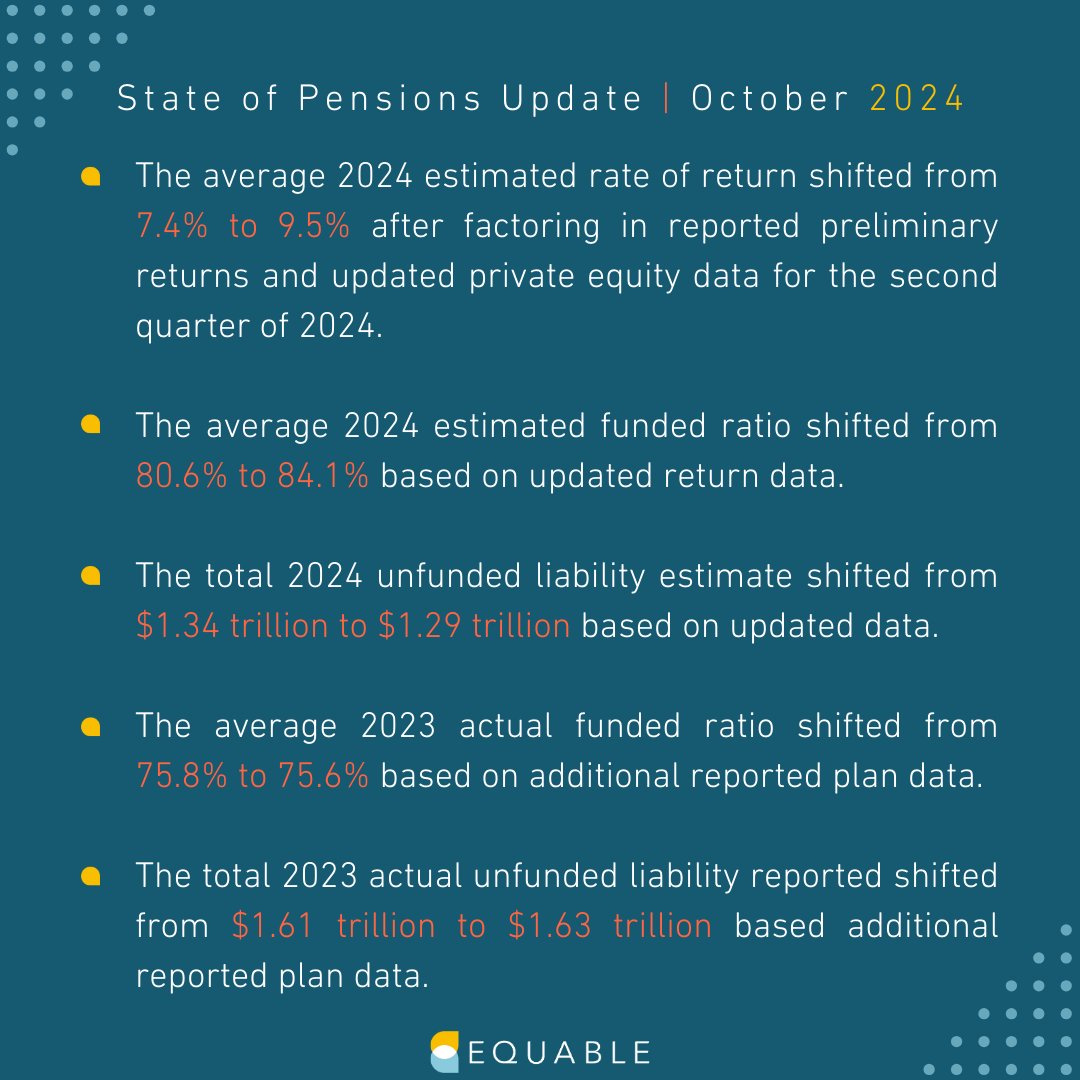

9 Oct 2024

Today, we released the October Update to State of Pensions 2024. We estimate unfunded liabilities will total $1.29 trillion for the 2024 fiscal year, compared to $1.63 trillion in 2023, as a result of strong market performance. Read the full update here: bit.ly/3U5Hl7Y

1

208