Founder @ Vision Capital Fund. Investor, author, angel. Invest in companies that reflect our best vision for our future. Musings on investing, business & life.

Joined October 2017

- Tweets 25,782

- Following 1,732

- Followers 27,554

- Likes 41,604

8,255 Photos and videos

I am thrilled to announce the launch of Vision Capital Fund, which has been in the making for over seven years.

We are focused on growing wealth for generations by delivering outstanding long-term investment returns from investing in exceptional companies that best reflect our vision for our future.

Website: visioncapitalfund.co/

Press Release: tinyurl.com/VCFpressrelease

Day One Investor Letter: tinyurl.com/VCFDayOne

37

20

213

62,202

World Models vs Language Models.

Language Models (LLMs) have given us an extraordinary command of concepts, vocabulary, and reasoning.

But our world is not made of words. Our physical world, virtual or real, runs on a different substrate.

Where language models learn the statistical structure of text, world models learn the statistical structure of space and time.

I resonate deeply with this and see the flaws with our current Gen AI technology, particularly LLMs. Excited to see how world models evolve.

drfeifei.substack.com/p/a-fu…

1

9

1,482

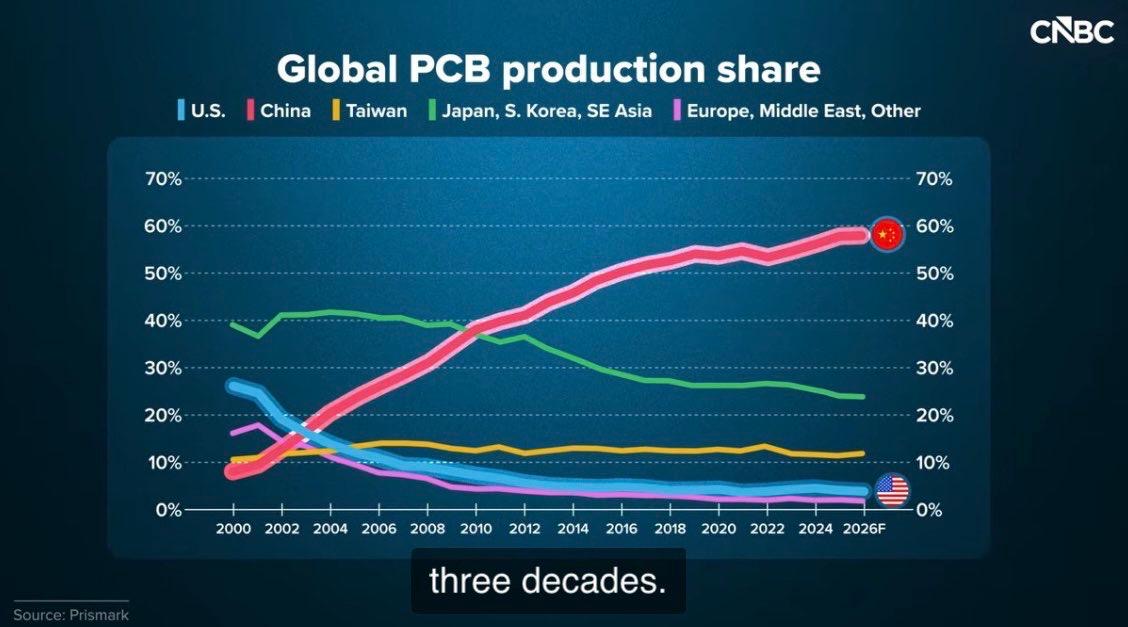

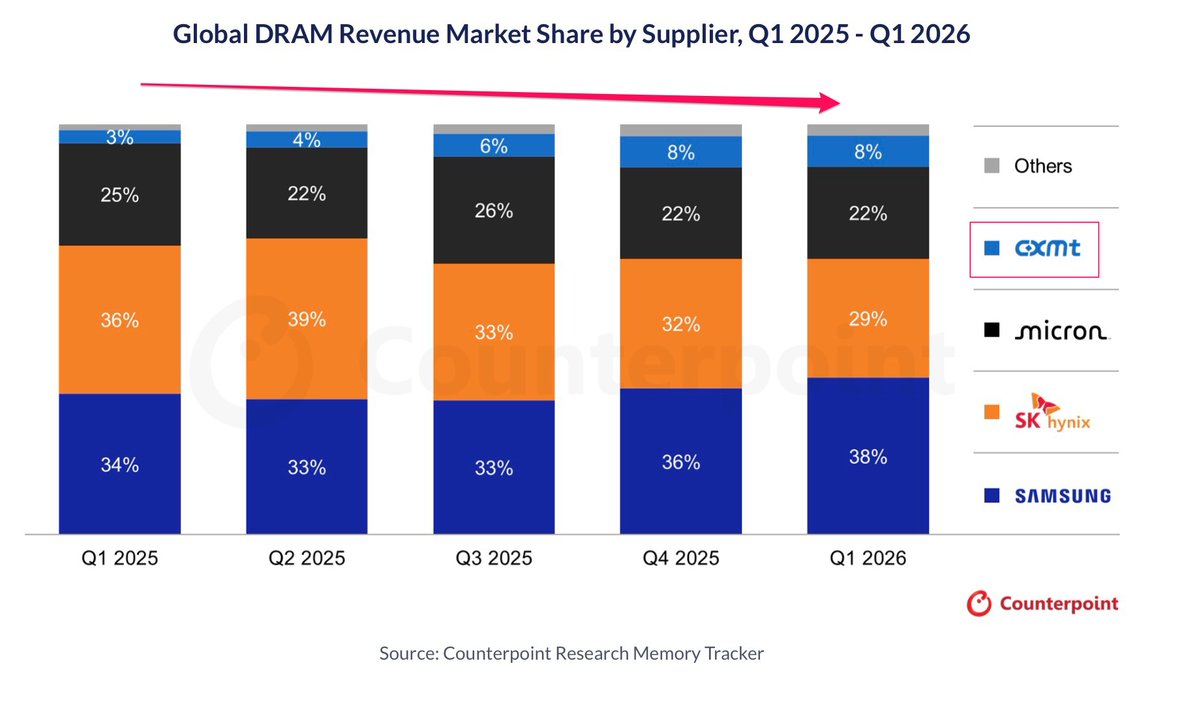

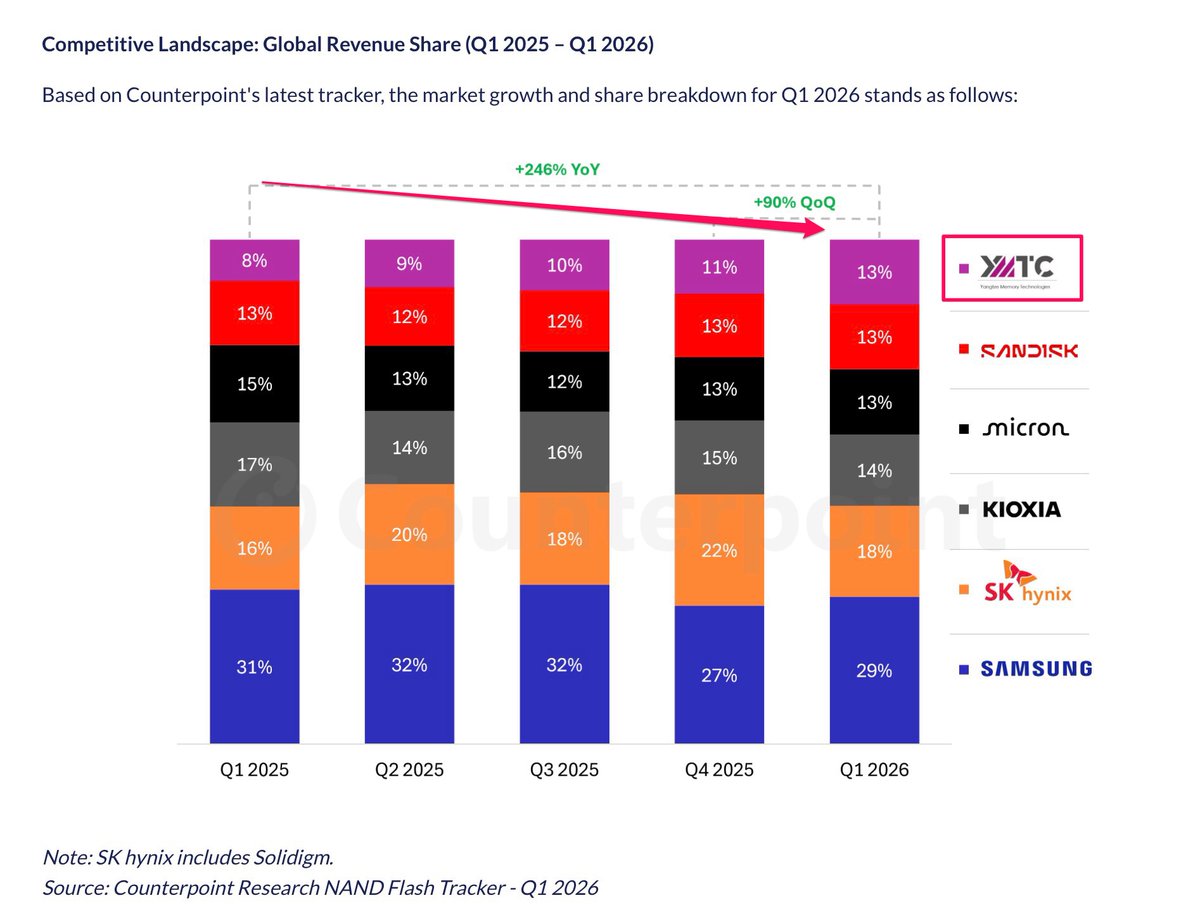

China grew to dominate the PCB market, not by out-innovating, but by out-supplying and undercutting, until most of the competition retreated.

Could the Chinese players repeat that in memory, with CXMT for DRAM and YMTC for NAND?

It is not about winning the frontier first, but winning enough of the base to make the frontier uneconomical for everyone else eventually, and dominance follows.

9

10

82

11,239

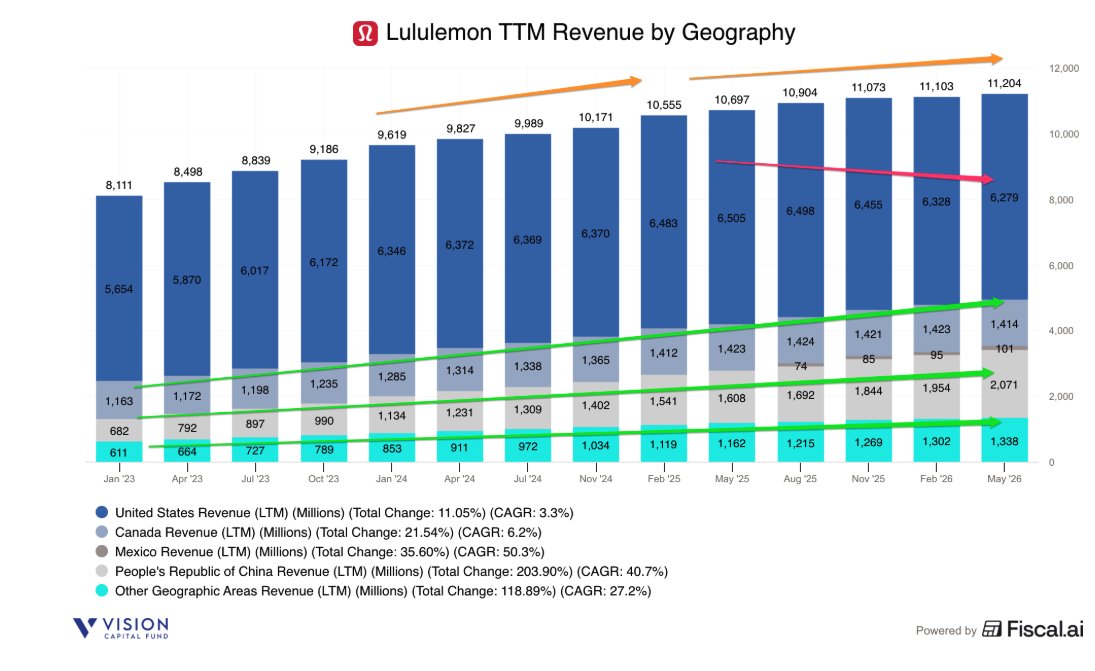

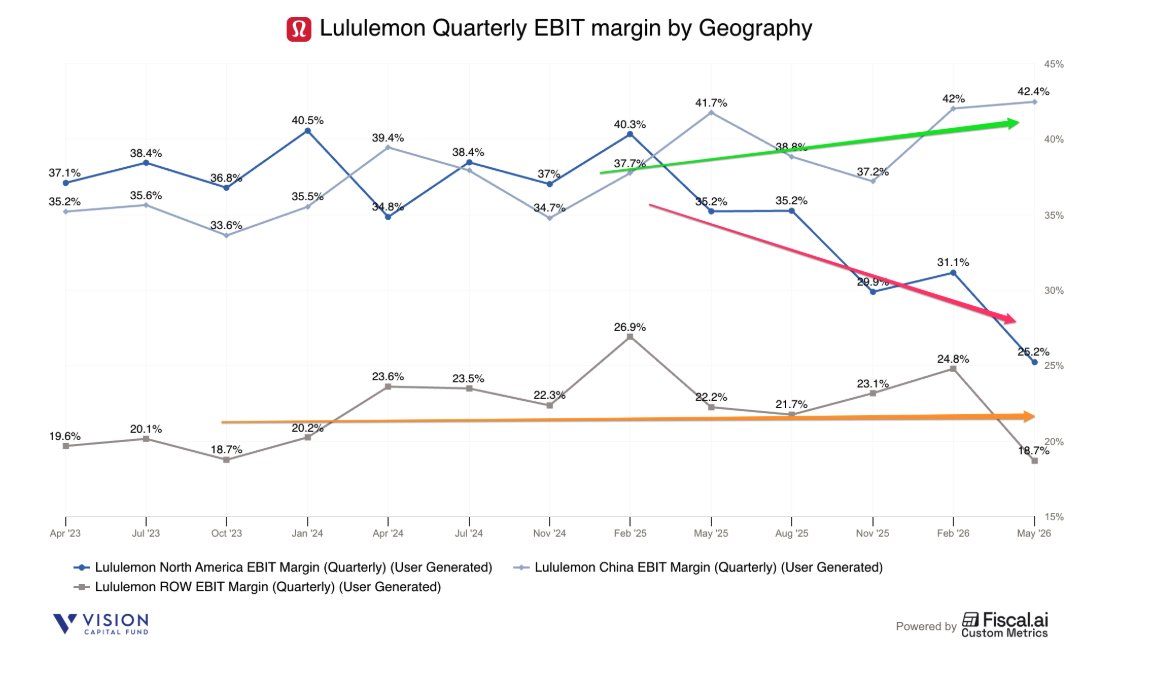

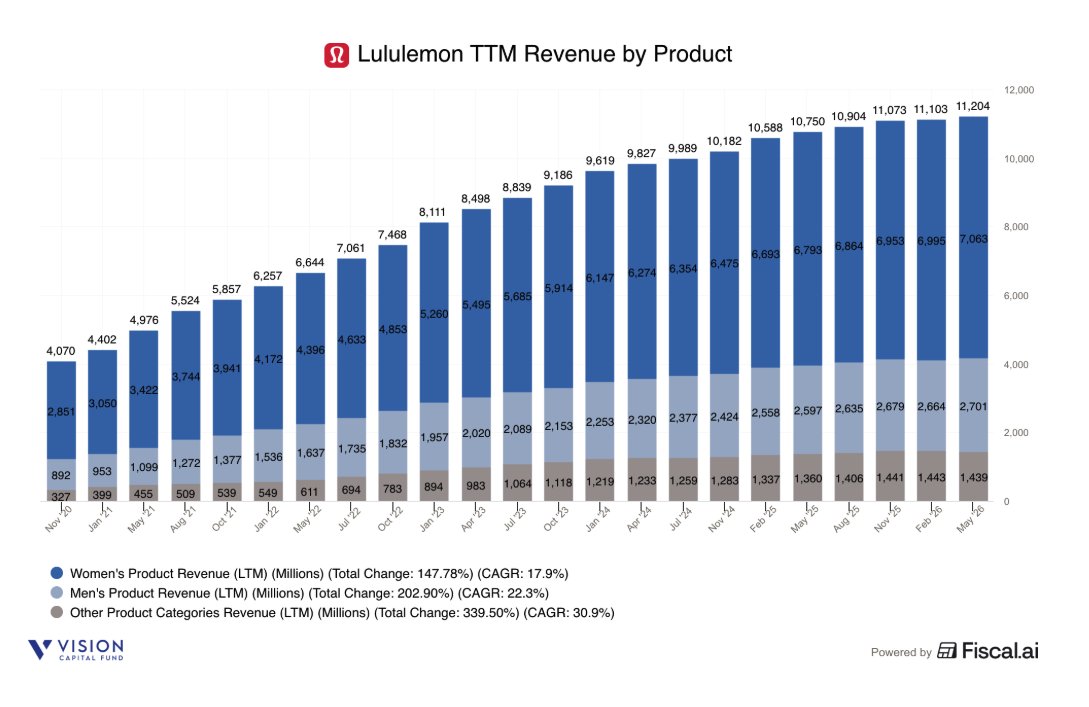

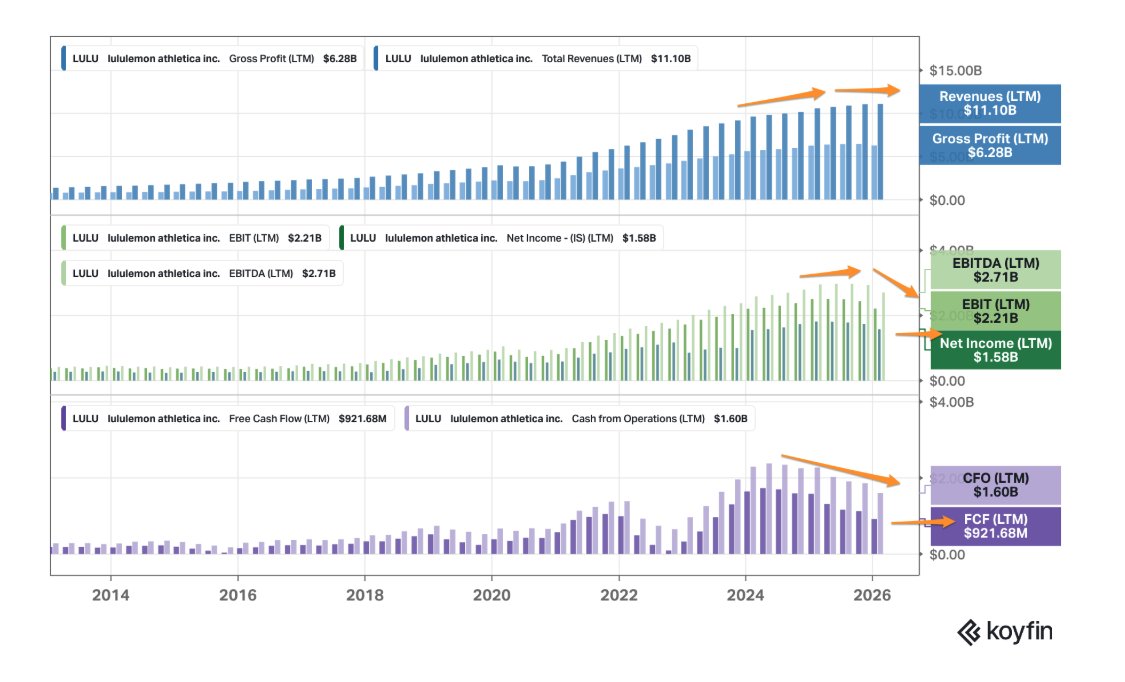

Lululemon $LULU 1Q26 Earnings

- Rev $2.5b 4% ↗️🟡

- GP $1.4b -3% ↘️🔴 margin 54.2% -418 bps ↘️🔴

- EBIT $277m -37% ↘️🔴 margin 11.2% -730 bps ↘️🔴

- Net Inc $195m -38% ↘️🔴 margin 7.9% -538 bps ↘️🔴

- OCF $214m ⤴️🟢 margin 8.7% 1369 bps ✅

- FCF $87m ⤴️🟢 margin 3.5% 1496 bps ✅

Biz Metrics

- Stores 816 6% ↗️🟡

- Gross Sqft 3,788mil 11% ↗️🟡

Comparable Sales

- Total 1% ↗️🟡

- Americas -5% ↘️🔴

- International 13% ↗️🟡

Revenue by Geography

- Americas $1.6b -3% ↘️🔴

- US $1.3b -4% ↘️🔴

- Canada $283m -3% ↘️🔴

- Mexico $25m 28% ↗️🟢

- PBOC $530m 29% ↗️🟢

- China $478m 30% ↗️🟢

- HK, TW, MC $51m 17% ↗️🟢

- Other International $321m 13% ↗️🟡

Revenue by Segment

- Women's apparel $1.6b 4% ↗️🟡

- Men's apparel $582m 7% ↗️🟡

- Accessories $287m -1% ↘️🔴

Revenue by Channel

- Company-operated stores $1.2b 3% ↗️🟡

- E-commerce $997m 4% ↗️🟡

- Other channels $281m 10% ↗️🟡

Revenue and EBIT by Geography

Americas

- Rev $1.6b -3% ↘️🔴

- GP $892m -14% ↘️🔴 margin 55% -693 bps ↘️🔴

- EBIT $408m -31% ↘️🔴 margin 25% -1000 bps ↘️🔴

China (⅓ smaller, growing faster, ~2X as profitable)

- Rev $478m 30% ↗️🟢

- GP $314m 33% ↗️🟢 margin 66% 158 bps ✅

- EBIT $203m 32% ↗️🟢 margin 42% 71 bps ✅

ROW (growing slower, less profitable)

- Rev $372m 13% ↗️🟡

- GP $200m 11% ↗️🟡 margin 54% -98 bps ✅

- EBIT $69m -5% ↘️🔴 margin 19% -355 bps ↘️🔴

Mgmt Guide

- 2Q26 Net Rev $2.475b -2% ↘️🔴

- 2Q26 North America -12% ↘️🔴

- 2Q26 China Rev 18% ↗️🟢

- FY26 Rev $11.5b 0% ➡️🟠

- FY26 US -9% ↘️🔴

- FY26 China 20% ↗️🟢

1 | Continued to struggle and saw moderating sales with spikes of negative commentary with respect to PFAS and weaker than expected product launches.

We saw encouraging signs in Q1 that reinforce we're moving in the right direction. But as we closed Q1 and entered Q2, we faced a few headwinds and a moderating sales trend. Based on our early analysis, there are 2 key factors impacting our trend. First, we experienced spikes of negative commentary in the media and on social channels with regard to our brand, which had an impact on traffic and overall top line performance.

And second, not all of our product launches have met our expectations. While we've had several successful launches so far this year, we've seen others, as we start Q2, not generate the anticipated guest response. Taken together, these factors impacted performance and are reflected in our updated guidance.

2 | Negative commentary affected Q1 traffic and sales, but has since subsided.

we're seeing relative stability in the trend of the athletic space. And what we really experienced was a drop-off in -- primarily in traffic and, to a lesser degree, conversion over the last 6 to 7 weeks. And as I mentioned, our analysis indicated it came from 2 key areas. So the first being spikes in negative commentary around the brand, from a number of factors, really at the end of Q1 and entering Q2. I mentioned that's now subsided, but we do believe it impacted our traffic and top line to a degree. And then in

3 | Fast & Free, Swiftly and Metal Vent did better but Align and Groove struggled.

Across the assortment in Q1, we saw good guest response to the updates we brought into some of our key run franchises, including Fast & Free, Swiftly and Metal Vent. Other standouts I'd mention include Daydrift and Define, where we offered expanded silhouettes and new and elevated colors. However, more recently, our new look of yoga campaign didn't drive top line results in line with our expectations.

As part of that campaign, we featured away-from-body styles across our Align and Groove franchises. These styles were met with good guest response, but so far, the campaign hasn't had the expected halo effect on other areas of our assortment.

4 | Expect more warm weather styles in Q2 across running, tennis, and golf, and outerwear and lounge.

We're pleased with our overall product pipeline, and in Q2, you will see more warm weather styles across some of our key activities, including run, tennis, golf and our lifestyle offerings. Over the course of the year, we'll continue to bring newness, excitement and new fabrics into the assortment with focus areas including outerwear and lounge.

5 | Will lean and chase into products that are doing better with customers, chasing 20% more volume this year.

To help improve the sales trend, we are leaning into our chase capabilities now and over the balance of the year. As we discussed on prior calls, our faster chase times improve our ability to read and react to guest demand trends and get back into certain strong performing styles more quickly. We are chasing 20% more volume this year relative to last year, and we see this as an important capability going forward. And with inventory units down approximately 4%, when we see strong guest reaction to new styles, we can get back into them more quickly, which we expect can help accelerate our momentum.

6 | New items sit at approximately 30% of mix, but performance has been mixed.

Yes. Yes. As we set out this year, our aim was to increase our penetration of newness to -- from 23% last year to 35% over the course of this year. Right now, we sit at about 30%. It will fluctuate as we move throughout '26. I would say, I mentioned we've seen some of that newness perform to expectation and some be a little short. And I would say our recent performance is impacting all areas of our business from a product perspective.

7 | Have significantly reduced their product development process from 18 to 24 months to 15 to 16 months and are looking to further reduce it to 12 to 14 months. Product quality remains foundational.

We have also reduced our mainline product development process from 18 to 24 months to 15 to 16 months, and we are working to further reduce it down to 12 to 14 months. Our product teams are focused on bringing new innovations to our guests, updating our iconic franchises and leveraging our increased speed-to-market capabilities to better anticipate, meet and fuel demand. I also want to reiterate that product quality is foundational to our brand, and we will continue to lean into this principle and enduring strength of lululemon.

8 | Consuming numerous projects to improve supply chain, from pricing to volume.

To drill down a bit, projects we are continuing to advance include analyzing our current global supply chain network to ensure the structure is fully optimized, reducing indirect spend through our procurement process, including price and terms optimization, volume consolidation and rationalization and implementing new technology, including AI-powered systems and automation to drive efficiencies across the enterprise. We're pleased with how our teams are implementing the initiatives in these areas, and we expect to see benefits over time.

9 | Saw a sequential QoQ improvement in full-price sales. Expecting higher levels of seasonal clearance in Q2, Full price sales continue to remain a primary focus.

In Q1, I'm encouraged that we have experienced a sequential improvement in our full price sales relative to Q4. In Q2, based on recent sales trends, our guidance assumes higher levels of seasonal clearance, but looking forward, driving full price sales remain a primary focus.

10 | Expect Q3 to sequentially improve from Q2, and Q4 should be better.

In terms of the second half, I would say Q3 will be a sequential improvement to Q2, and then we expect markdowns in Q4 to be under last year, given that was our high water level from a markdown perspective. So I'd say sequentially better as we improve throughout the year. And again, for the full year, flat to modest improvement. So Q2 will be our high-water mark this year.

11 | The largest focus continues to fix and reaccelerate North America’s and the US’s declining business.

We now expect FY26 revenue to be in the range of $11 billion to $11.15 billion, flat to down 1% relative to 2025. By region, we now expect revenue in North America to be down in the high single digits, with the U.S. slightly lower and Canada better

I want to emphasize that we are not sitting still, and we are moving with urgency to make the necessary adjustments to reaccelerate momentum, particularly in North America. With that, let's turn to the work already in motion to strengthen our top line trajectory and position ourselves for long-term sustainable growth.

12 | Have enhanced the store fleet in North America with 15% fewer SKUs, improved storytelling, better visual merchandising, and a significant reduction in markdown sales.

When looking at our store fleet in North America, you can already see several enhancements. These include: first, a less dense presentation of products featuring 15% fewer SKUs, which allows us to better highlight new styles and innovation. Second, a sharper focus on merchandising by performance and lifestyle products, which allow for improved storytelling, better visual merchandising and make the store easier to navigate and shop. And third, a significant reduction in markdowns, which allows the guest to focus more on our new and full price offerings and contribute to our premium shopping experience.

In addition to these strategic shifts across all stores in the market, we have a smaller subset of doors where we are testing additional enhancements. These include further SKU reductions, more curated assortment based on local taste and preferences, new fixture packages and updated imagery and mannequins.

13 | China continued to remain strong but saw momentum slow towards the end of Q1, with spikes of negative commentary with respect to PFAS, but it has since subsided. The activation yoga event on the Great Wall of China have reversed the negativity.

Let me now shift to our international business, beginning with China Mainland. In China, we had a strong start of the year, supported by successful product and brand activations during Chinese New Year run and tennis campaigns, but experienced a slowing of momentum towards the end of Q1 as we saw spikes of negative commentary, which has now subsided. The team is focused on building brand awareness and distinction through our mindful performance position and community activation. In yoga, one of the most powerful examples of this took place just a few days ago in Beijing on the Great Wall of China, where more than 2,000 guests and 70 ambassadors practiced yoga at the flagship event that launched a series of global activations.

14 | CNY was in Q1 rather than Q2 and added 800bps to growth. Expect softer Q2 sales of 15-20%, but continue to expect 20% growth for the year for China, with the majority of new store openings planned for China.

The shift of Chinese New Year into Q1 added 8% to the growth rate in the quarter.

For Q2, we expect sales to increase in the mid- to high teens, and we continue to expect approximately 20% growth for the year, demonstrating the ongoing momentum in the business in China Mainland .

Our new store openings in 2026 will include approximately 10 to 15 stores in North America, including 8 in Mexico and 25 to 30 in our international markets, with the majority of these planned for China.

15 | Remain pleased with the other international business in APAC and EMEA, though saw some disruption in the Middle East franchise due to the Iran conflict and softer tourism in Europe and Japan.

We remain pleased with our business in APAC and EMEA. In Q1, revenue increased 13% or 9% in constant currency. We have seen some disruption in our Middle East franchise business due to the conflict in Iran, and we've also seen some softer tourism in Europe and Japan. We view these as temporary, and we remain excited for our brand's potential in both APAC and EMEA. With the help of our franchise partner, we recently opened the first location in Greece and plans are well underway to open in India later this year.

16 | Gross profit margins declined 410bps, largely driven by tariffs with 280bps, 40bps by markdowns, offset by 100bps from efficiency.

Our gross margin decreased 410bps compared to last year and was driven primarily by the following: a 330bps decline in overall product margin driven predominantly by tariff impact and markdowns. Tariffs had a gross negative impact of 280bps in the quarter, offset by 100bps related to our enterprise efficiency initiatives. Markdowns increased 40 basis points. Deleverage on fixed costs was 140bps, driven by ongoing investments in our store fleet and regional mix, and foreign exchange had 60bps of favorable impact.

17 | While tariffs' impact will start to decline due to comps, expect to see higher markdowns of 50 bps due to slower-than-expected top-line trends in Q2.

We expect increased tariffs to have a gross negative impact of approximately 150bps, with offsets of approximately 100bps. We expect markdowns to be up approximately 50bps versus last year. While we continue to expect markdowns to improve modestly YoY in the second half, the slower-than-expected top line trends in Q2 will necessitate additional seasonal clearance.

18 | Increasing marketing spend by 10 to 15% versus 2.25, expecting margins to be around 6 to 6.5% of sales versus 5.6%. Focusing on activation events.

So yes, we've increased our marketing investment. We are now taking it to approximately 10% to 15% above last year. So it's in the range of 6% to 6.5% of sales versus last year at 5.6%.

I would say in terms of where the dollars are going, we're certainly going after activations, building on some exciting recent events, including the Great Wall yoga experience. We've got SeaWheeze coming up, which is our Vancouver half marathon. We'll have a pinnacle yoga event in New York City to kick off our summer series. And then also another example would be the U.S. Open activation. We'll have some collaborations coming up, continue to build on grassroots community activations, including run and yoga events locally. And then we're going to have some new experiences for press and partners, notably a pop-up in New York City showcasing new products. And then you can look for also a new content series on our social channels with some elite athletes, and those are just a few examples of what's to come

➡️ Final Takeaways on Lululemon $LULU:

The US continues to be weak and declining which is what LULU really needs to fix and fast. China is the gem, fast growing and much more profitable, while ROW remains decently strong. Meghan and Andre holding up the fort while the new CEO for Heidi O’Neill joins in September. Like the return to basics, strong innovative products, full-priced premium offering, exciting customers and getting them to come back and buy more. Expect tariff headwinds to ease into H2. While we are waiting for a reversal into H2, near-term negative sentiment on PFAS which seemed to have reversed and weaker performance on selected styles have weighed on the brand, traffic, and sales. LULU really needs to get its customers excited to buy more, if not they will forget and gradually move on. While valuations are cheap, <10x P/E, it does reflect a business that is struggling in its original core market, and it has struggled to fix.

2

1

5

1,967

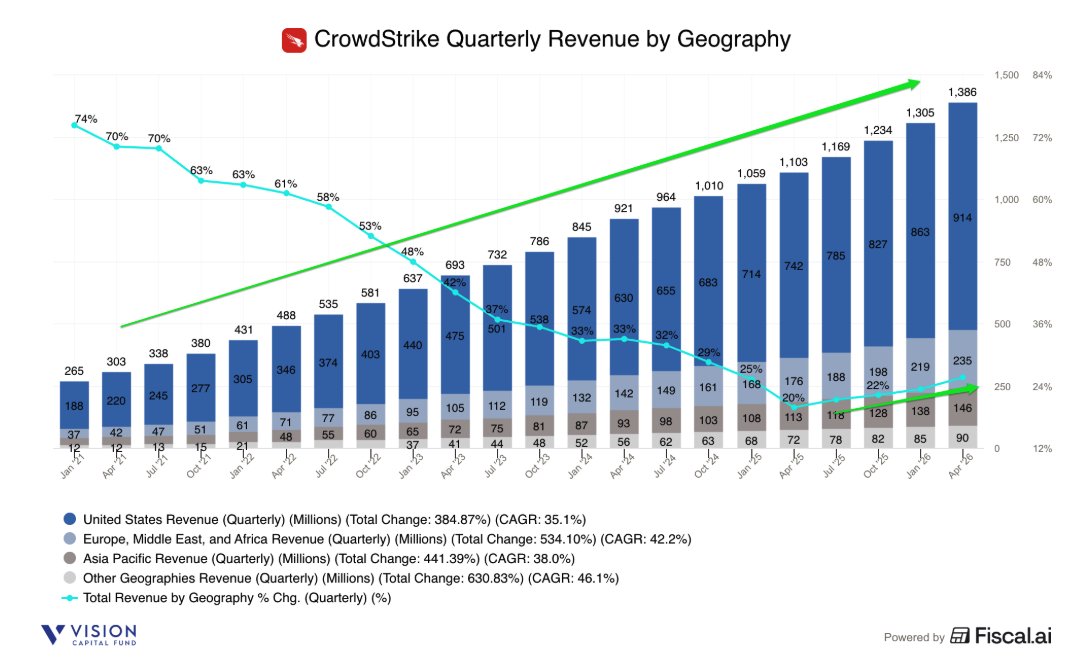

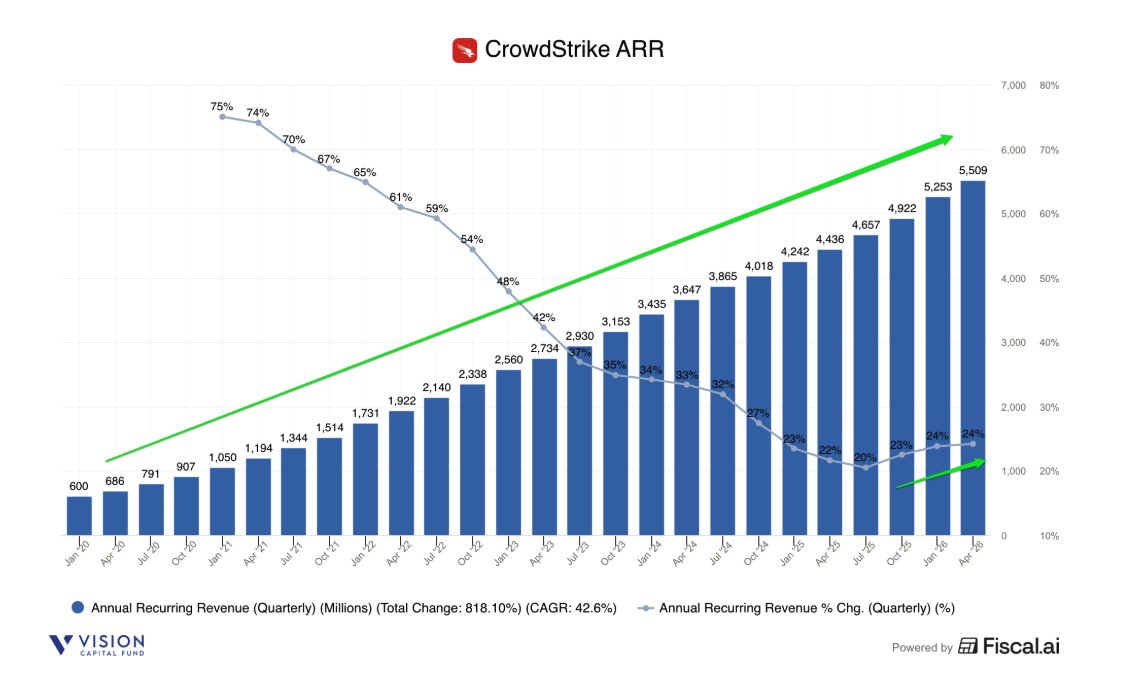

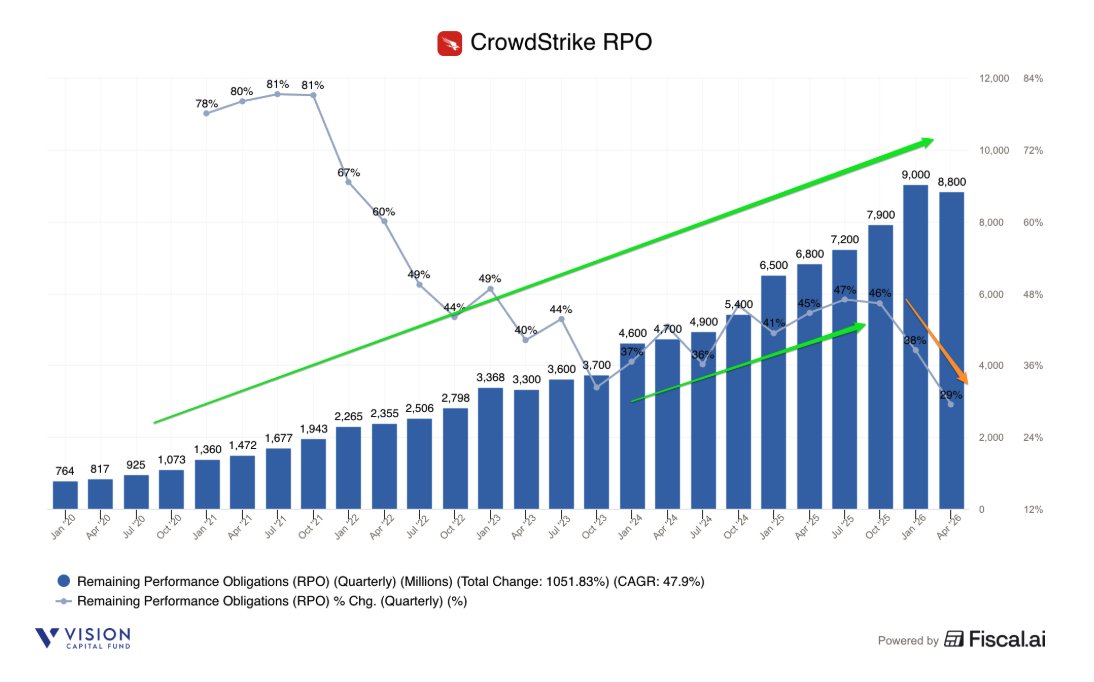

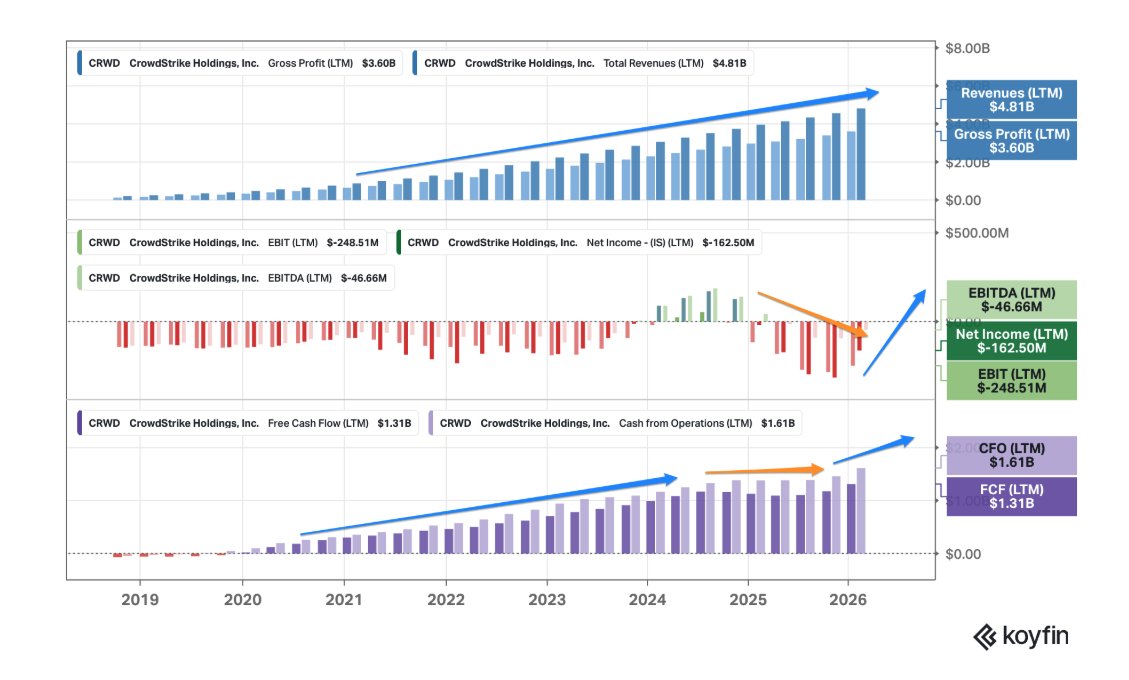

CrowdStrike $CRWD 1Q27 Earnings

- Rev $1.4b 26% ↗️🟢

- GP $1.0b 28% ↗️🟢 margin 75.3% 139 bps ✅

- NG EBIT $326m 62% ↗️🟢 margin 23.5% 528 bps ✅

- EBIT -$31m ⤴️🟢 margin -2.2% 855 bps ✅

- NG Net Inc $283m 53% ↗️🟢 margin 20.5% 372 bps ✅

- Net Inc $46m ⤴️🟢 margin 3.3% 1284 bps ✅

- OCF $591m 54% ↗️🟢 margin 42.6% 784 bps ✅

- FCF $471m 68% ↗️🟢 margin 34.0% 851 bps ✅

Revenue by Geography

- US $914m 23% ↗️🟢

- EMEA $235m 33% ↗️🟢

- APAC $146m 30% ↗️🟢

- Other $90m 25% ↗️🟢

Biz Metrics

- ARR $5.51b 24% ↗️🟢

- Net New ARR $256m 32%

- ARR (Flex) $1.9b 99% ↗️🚀

- RPO $8.8b 29% ↗️🟢

- 6, 7, 8 modules 51%, 35%, 25% 📶✅

- FCF Rule of 40: 59

Mgmt Guide

- 2Q27 ARR $5.795b 24% ↗️🟢

- 2Q27 Net New ARR $286m 29% ↗️🟢

- 2Q27 Rev $1.442b 23% ↗️🟢

- 2Q27 NG EBIT $349m

- 2Q27 NG Net Income $303m

- 2Q27 FCF margin 24.5%

- FY27 ARR $6.55b 25% ↗️🟢

- FY27 Rev $5.96b 24% ↗️🟢 (raise)

- FY27 NG EBIT $1.48b (raise)

- FY27 NG Net Income $1.28b (raise)

- FY27 Capex margin 7-8%

- FY27 FCF margin >30%

- LT GPM 82-85% (vs FY26 74.7%)

- LT NG EBIT margin 28-32% (vs FY26 21.7%)

- LT FCF margin 34-38% (vs. FY26 25.7%)

1 | Strong Q1 results.

We delivered strong first quarter results to begin the new fiscal year, exceeding expectations across all guided metrics…Our Q1 results and FY '27 outlook reflect the very beginnings of this technology wave with broad-based momentum fueled by customers consolidating their security needs, lowering their total cost of ownership and accelerating AI adoption with CrowdStrike as their security foundation. This strength is reflected in our continued strong retention rates, increased module adoption, third consecutive quarter of ending ARR growth acceleration for the endpoint business and Q2 record pipeline

2 | Raising ARR growth expectations by 500bps and expect new ARR growth to accelerate.

These data points illustrate momentum, traction and achievement. It's on the backs of our strong Q1 results and the unprecedented market dynamics I see that we are raising our growth expectations for the full year net new ARR by more than 500 bps. For the full year, we now expect net new ARR growth to accelerate over FY '26. What I see is AI driving structural demand for cybersecurity that compounds not decelerate. The AI enterprise unfolding in real time and CrowdStrike is a necessity to secure it.

3 | Next-Gen SIEM, Cloud and Identity continue to do well now $2bn in ending ARR.

Moving to Next-Gen SIEM, Cloud and Identity. We saw a record Q1 net new ARR from the combination of these businesses. Combined, these businesses have now exceeded $2 billion in ending ARR. Our Next-Gen SIEM business exceeded $600 million in ending ARR and has transformed CrowdStrike into the operating system of the AI SOC. Charlotte AI, where ending ARR accelerated sequentially over Q4 is now the reasoning engine across Falcon.

4 | CrowdStrike was the only cybersecurity company selected by both Anthropic and OpenAI from the very start to secure these new models, their adoption and the new risk they create.

In April of Q1, more happened in a matter of weeks in cybersecurity than in the whole year prior, the Mythos inflection moment. In collaboration with Anthropic from the start, we saw a new model emerge that had relevance for the cybersecurity market, relevance for defenders in identifying vulnerabilities much faster than before, including the chaining of multiple vulnerabilities to create lethal cyber attacks. Project Glasswing brought together CrowdStrike and a focused group of consequential companies to ensure market readiness for Anthropics new model. Shortly thereafter, OpenAI announced GPT 5.5 cyber later known as Daybreak, where we were selected as a founding member of their trusted access for cyber program.

CrowdStrike is the only cybersecurity company to secure both Anthoropic and OpenAI's introduction programs from the very start. What the Mythos moment proved is that the world, starting from the Frontier AI labs themselves realize that AI needs a cybersecurity ecosystem. This was a Mythos inflection point. The discussion evolved from is AI going to disrupt cybersecurity to organizations and even the Frontier AI labs relying on Falcon as their AI-powered Defender for the post Mythos era.

5 | Cybersecurity is now foundational AI infrastructure with the explosion in greenfield attack surfaces.

Cybersecurity is now foundational AI infrastructure; and two, an explosion in greenfield attack surfaces each of which needs cybersecurity. The AI revolution has led to a boom in one, hardware, GPUs, MPUs, GPUs and training chips; two, data centers and hyperscalers, training and housing AI models; three, neo-cloud, a whole new class of cloud focusing on inference; four, token factories, we're seeing unprecedented eye-watering demand for Anthropic and OpenAI; and five, agentic applications a whole new class of identic tools such as Cursor, Sierra, [ 11 Labs, Exa, Lagora ] and more.

6 | Saw continued acceleration for the third consecutive quarter in the endpoint business

First, endpoint, our endpoint business again accelerated for the third consecutive quarter, the endpoint has become the epicenter of where AI happens and our best-in-class efficacy sets us apart. The rapid adoption of AI tools like [ Quad Cowork ] and codecs have dramatically expanded the endpoint attack surface. Our endpoint leadership continues to widen with Gartner naming as a leader for the seventh consecutive year and storing us the very highest both axis of the Magic Quadrant, ahead of all other participants for the fourth year in a row.

7 | While Crowdstrike pioneered EDR, AIDR is becoming a new growth pillar.

We pioneered EDR. We have the endpoint real estate, and that gives us the structural advantage to own what we're bringing to the market, AIDR, AI detection and response. AIDR is quickly becoming a new growth pillar in our business with ending ARR growing more than 250% sequentially and Q2 pipeline already exceeding $50 million. We went from 0 to this in under 2 quarters. In my career, I've never seen adoption happen this fast.

8 | See AIDR as a larger opportunity than EDR, Because Crowdstrike can detect, block, and respond where AI actually runs, which is similar to EDR, and AIDR market is significantly larger.

But when you look at AIDR, I mean, it's 250% QoQ up with a $50 million-plus pipeline and that's only growing by the day.

As I look forward, I see AIDR as a larger opportunity than EDR. Here's why. First, our structural advantage. We built EDR because the endpoint is where attacks execute, and you need a sensor there to see them. The same is true for AI. Agents run on the end point. They make tool calls, access files in both APIs and move data at the process level to detect and respond to AI threats in real time, you need a runtime sensor where AI executes. That's Falcon. While competitors may provide AI visibility, only CrowdStrike can detect, block and respond where AI actually runs, the pattern that made EDRs repeats.

Second, the AIDR market opportunity is structurally larger. EDR secured one attack surface, the host. AIDR secures 7 data, models, prompts, agents, identities, infrastructure and the interaction layer where they converge. Worldwide spending on AI is forecasted to total over $2.5 trillion and only a low single-digit percent of organizations have an advanced AI security strategy. The gap between AI adoption and AI protection is the widest asymmetry in security since the cloud transition, and it's moving faster.

9 | Flex continues to do very well as customers are renewing and expanding their spend, coming back multiple times and spending and consolidating more.

The most exciting part is the re-flex dynamic customers renewing and expanding their investment beyond their first Flex contract with highlights including the number of re-Flex customers reached 480, representing nearly 25% of all Flex customers. The average re-Flex uplift was 26% with the average re-Flex happening in 7 months, well ahead of their subscription renewal date and the most compelling over 130 customers have re-Flex multiple times with the average ARR uplift over their original Flex coming in at 51%. Customers are coming back multiple times and they're continuously spending more, consolidating on CrowdStrike.

10 | See opportunity to add token consumption to Flex, still foccused on providing flexibility and certainty.

Well, it is an evolving market. And the great news is that Falcon Flex license already contemplates that. Remember, Flex is a commitment model, but it has the ability to use tokens, use credits, things of that nature. So I think we're in a great spot because we've done the hard work of getting these Falcon Flex licenses in place. We've got customers who already committed massive dollars to it.

And then as it evolves, we can easily add token consumption into the model. And that's certainly something that we may do in the future. But obviously, it's moving pretty quick and we want to make sure that we get it right. We want to make sure we meet customers where they want to be met where they've got a level of flexibility but also a level of certainty around the spend. And I think as a company, we've done a good job to help provide that to our customers, which is why you've seen the adoption around Flex.

11 | Doing a 4-for-1 stock split to lower the prices

we are announcing a [ 4:1 ] forward stock split to make ownership of CrowdStrike stock more accessible to investors. Stockholders of record after the close of market on June 25, 2026 we'll receive an additional 3 shares of common stock for every 1 share held after the close of market on July 1, 2026, with trading on a split-adjusted basis expected to commence at market open on July 2, 2026.

12 | CrowdStrike is well positioned to be the best defender in cyber security for frontier AI.

The world of cybersecurity and Frontier AI collided. The result is that Frontier AI needs the very best defender and that's CrowdStrike. The inflection is now the need for cybersecurity to defend AI is nonnegotiable. CrowdStrike is not only in the right place at the right time, we're the right technology to stop the breach. Think of CrowdStrike as the picks and shovels for the world's largest technology gold rush of all time.

CrowdStrike is in the prime position to be the world's AI security layer with nearly 100,000 businesses, including hundreds of the Fortune 500 already trusting us to secure their organizations. Our ecosystem of thousands of partners are looking to us the answers on how to secure AI at global scale. This is even bigger than customers and partners.

➡️ Final Takeaways CrowdStrike $CRWD:

Crowdstrike’s growth continues to hold up strongly with strong continued growth reacceleration and is showing no signs of being disrupted by AI. Instead, it should be viewed as an AI beneficiary with the growing surface area of AI agents that needs to be protected. CrowdStrike is becoming one of the key companies to secure AI. CrowdStrike continues to displace legacy AV, supported by numerous opportunities to add cloud, Next-Gen Identity and Next-Gen SIEM and in endpoint as it increasingly consolidates cybersecurity under one single platform. Flex is doing especially well, with the higher flexibility, driving for higher module adoption, usage, larger and longer deals, and more customer stickiness. All of which point to sustained continued growth.

8

1,812

Interesting thoughts on TSMC from Sachin Katti, OpenAI, with Apoorv Agrawal:

- TSMC is a single choke point in the compute supply chain (advanced semiconductors).

- TSMC wants diversification and not to be overly reliant on a single large customer (i.e., NVIDIA).

- TSMC diversifies by allocating wafers to multiple customers, and it is in their business interest to try to make sure their customers are successful.

- The multiple wafer allocations mean that there will be multiple varieties of chips, which means the flexibility to use all the different chips is key.

6

7

43

7,840

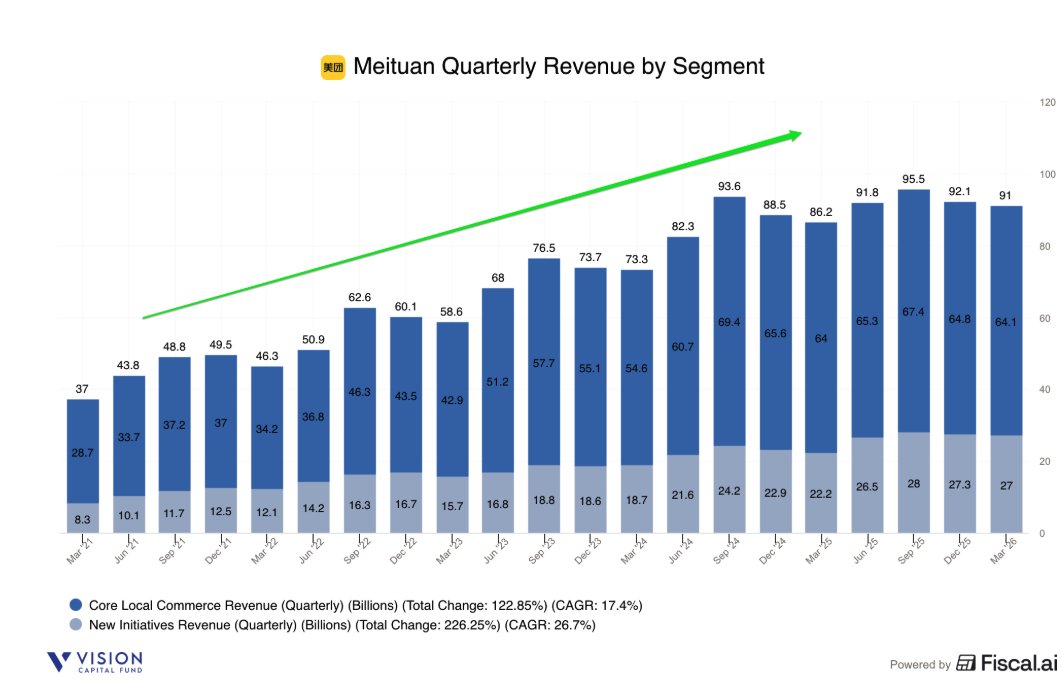

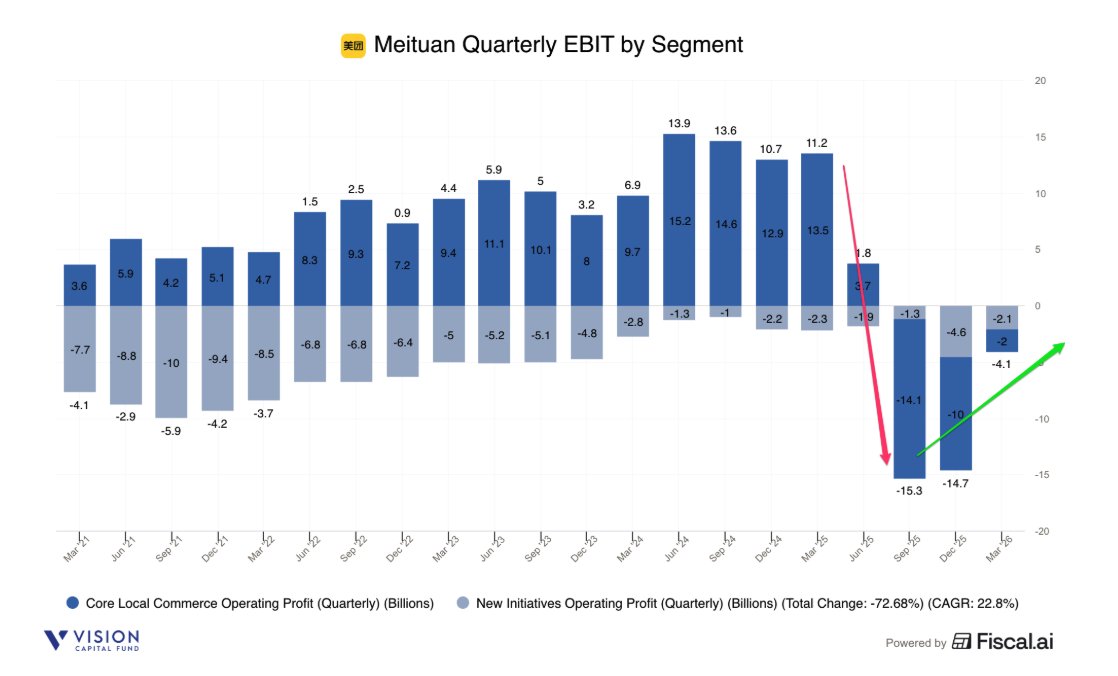

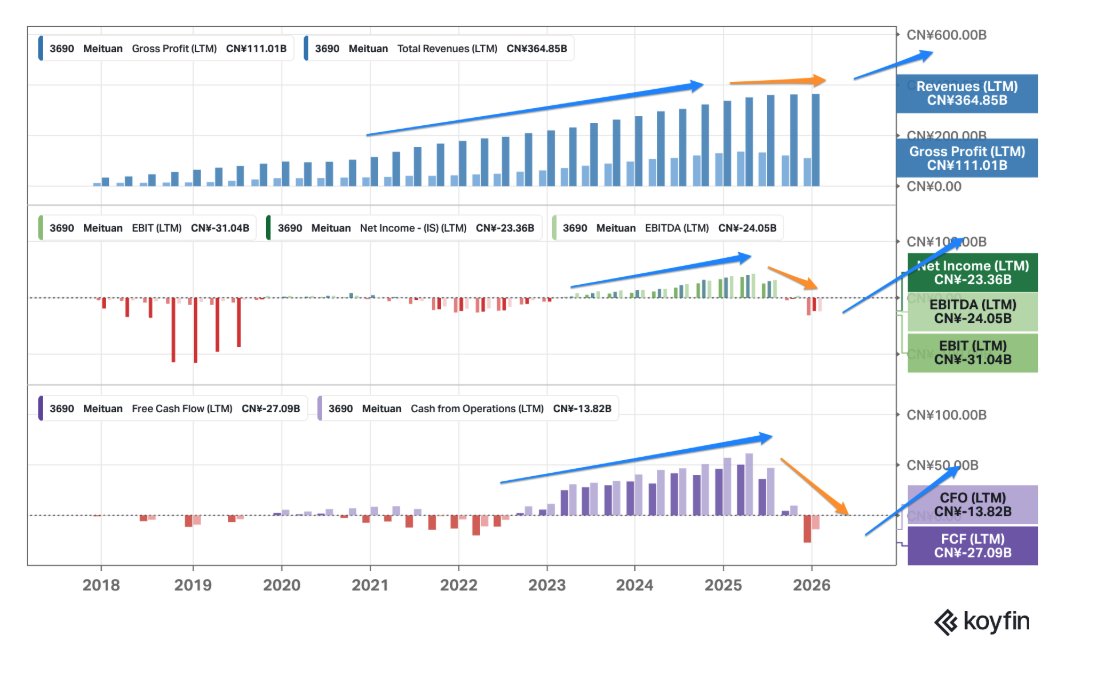

Meituan $3690 1Q26 Earnings

- Rev $91b 6% ↗️🟡

- GP $26b -19% ↘️🔴 margin 28.5% -867 bps ↘️🔴 (↗️🟢 QoQ)

- Adj EBITDA -$3b ↘️🔴 margin -3.3% -1762 bps ↘️🔴 (↗️🟢 QoQ)

- EBIT -$6.5b ↘️🔴 margin -7.1% -1936 bps ↘️🔴 (↗️🟢 QoQ)

- NG Net Inc -$5b ↘️🔴 margin -5.5% -1816 bps ↘️🔴 (↗️🟢 QoQ)

- Net Inc -$6.8b ↘️🔴 margin -7.5% -1917 bps ↘️🔴 (↗️🟢 QoQ)

- OCF -$7b ↘️🔴 margin -7.7% -1946 bps ↘️🔴

Core Local Commerce

- Rev $64.1b 0% ➡️🟠

- GP $20.8b -27% ↘️🔴 margin 32.4% -1208 bps ↘️🔴

- EBIT -$2b ↘️🔴 margin -3.2% -2426 bps ↘️🔴 (↗️🟢 QoQ)

New Initiatives

- Rev $27b 21% ↗️🟢

- GP $5.3b 42% ↗️🟢 margin 19.5% 286 bps ✅

- EBIT -$2.1b ⤴️🟢 margin -7.8% 238 bps ✅ (↗️🟢 QoQ)

Revenue by Type

- Delivery services $25b -3% ↘️🔴

- Merchant services $38.1b 3% ↗️🟡

- Product sales $21b 47% ↗️🟢

- Others $7b -25% ↘️🔴

Core Local Commerce Revenue by Type

- Delivery services $24.1b -6% ↘️🔴

- Merchant services $35.6b 0% ➡️🟠

- Product sales $3b 96% ⤴️🟢

- Other $1.4b 19% ↗️🟢

New Initiatives Revenue by Type

- Delivery services $924m ⤴️🟢

- Merchant services $2.5b 98% ⤴️🟢

- Product sales $18b 41% ↗️🟢

- Other $5.6b -32% ↘️🔴

1 | Delivered solid results that improve and profitability continue to improve QoQ despite the ongoing competitive market environment.

Looking back at the first quarter, I would say we delivered solid results and ongoing industry changes. All our businesses showed strong resilience amid a competitive market environment. For the full year of 2026, we aim to further deepen our competitive moat for core local commerce while further improving overall operational efficiency.

In this quarter, we have achieved substantial financial improvement while maintaining resilient growth, and we are the go-to platform for local service merchants to run their business and for consumers to discover and transact.

2 | Higher gross profit margins were due to more consumer incentives and higher rider incentives, and higher promotion, advertising and user incentives.

Total revenue was RMB 91 billion, up 5.6%. Cost of revenue ratio increased by 8.7 percentage points to 71.5%. This was primarily driven by 2 factors: more consumer incentives deducted from revenue, higher rider incentives to maintain leading service quality amid intensified competition.

Selling and marketing expenses ratio rose by 7.6 percentage points to 25.2%, largely due to our increased investments in promotion, advertising and user incentive to enhance our brand awareness and core user engagement to address the competition. R&D expenses ratio increased to 7.7%, reflecting our increased investment in AI, while the G&

3 | Core Local Commerce Segment returned to positive YoY revenue growth, supported by higher annual purchase frequency and cross-selling

Our revenues from the Core Local Commerce segment were RMB64.1 billion for the first quarter of 2026, returning to positive year-over-year growth. The resilient growth of GTV was driven by the growth in annual purchase frequency and cross-selling among our different services, while the number of annual active advertising merchants also recorded growth. However, our revenue recorded a modest growth on a year-over-year basis, primarily driven by the elevated incentives deducted from revenues to address the intensified competition.

4 | New initiatives continue to grow rapidly while profitability continuecontinuesd to improve.

Our revenues from the New Initiatives segment increased by 21.3% to RMB27.0 billion for the first quarter of 2026 from RMB22.2 billion for the same period of 2025. Despite the impact of discontinuation for Meituan Select (“美团優選”), our revenue continued to grow steadily, driven by the expansion of our grocery retail businesses and overseas businesses.

5 | Operating losses continued to narrow for the 2nd consecutive quarter as irrational subsidies moderated, seeing a sequential improvement in EBIT and net income.

Their operating losses narrowed significantly compared with the prior quarter. In the first quarter, in on-demand delivery industry, the irrational subsidy moderated compared with the last quarter.

Our bottom line showed a strong improvement this quarter. Sequentially, we achieved more than RMB 10 billion loss reduction with total segment operating loss and adjusted net loss narrowing to RMB 4.1 billion and RMB 5 billion, respectively. This meaningful improvement reflected a moderation of competition, our effective execution on high-quality growth and operational efficiency improvement.

6 | Segment operating losses continued to narrow meaningfully for the second consecutive quarter as on-demand delivery industry right subsidies continued to decline, remaining focused on high AOV order segment.

Segment operating loss narrowed meaningfully from last quarter to RMB 2 billion. On-demand delivery industry-wide subsidy started to go down in Q1. We further improved our subsidy efficiency and stayed focused on high AOV order segment and our core user base. Both the order volume and GTV of our on-demand business maintained resilient year-over-year growth during this quarter. We further solidified our leadership in both food and nonfood sectors. Our on-demand deliveries unit economics improved significantly QoQ.

So for your question on our food delivery subsidy and on the UE. So I think with industry-wide subsidy finally getting more rational, so we are seeing competition shifting back to the fundamentals. That's operational efficiency and user experience. So this transition plays to our strength. But even as we see -- we gradually pull back subsidies, we still continue to see healthy user growth and stronger engagement from our core users. We also solidified our leadership in mid- to high AOV order segment.

7 | Meituan's superior order mix and user structure support a faster recovery in AOV. It will take some time to go back to more reasonable levels, and will weigh in the near-term.

This is mainly driven by 2 factors. First, our superior order mix and user structure supports a faster recovery in AOV. And second, our overall better operational capability allow us to adapt more quickly to market shifts and drive further efficiency. However, both the AOV and subsidy for our on-demand business still need more time to go back to a reasonable level. So they continue to weigh on the revenue growth and operating profit of on-demand delivery business during this quarter.

8 | If competition remains more rational, Meituan expects a meaningful unit economic improvement in Q2 for the third consecutive quarter, which will be supported by seasonal tailwinds.

If competition stays more rational, we expect a meaningful UE improvement in Q2 compared to Q1, supported by seasonal tailwind, and we have sustained our market leadership in recent months, while also widening our UE gap advantage. We will continue to monitor the market closely and adapt thoughtfully.

Our focus stays on sustaining our leading position while driving operational efficiency improvement, both for ourselves and our merchants. However, our UE improved in the second half, we'll still depend on how the competition environment evolves. Also, keep in mind that delivery cost per order is seasonally higher in Q3 and Q4 compared with Q2.

9 | Despite the near-term higher subsidized competition, Meituan’s food delivery continues to remain intact, high and mid frequency users became more active, and saw higher ARPU and user loyalty.

our food delivery business continued to attract a large number of new users. This shows that consumers chooses Meituan for our comprehensive and reliable services rather than price incentive alone. In addition, our stable, reliable delivery services during holidays and extreme weather, together with our growing high-quality supply have further strengthened our users' stickiness.

Notably, high and mid-frequency users become more active. Their ARPU increased and user loyalty strengthened. A large number of mid-frequency users upgraded to high-frequency users. These high-quality users have more diverse consumption needs and value services and supply quality more. Meanwhile, core users of Meituan Instashopping also demonstrated higher order frequency. Notably, the post-2000s generation has emerged as a key growth driver.

10 | Healthier order mix as its customers more increasingly willing to pay for quality.

Also, keep in mind that delivery cost per order is seasonally higher in Q3 and Q4 compared with Q2. And on order volume, given the high basis from last year, we may see negative year-over-year order growth in the second half. But we are seeing a healthier order mix as consumers are increasingly willing to pay for quality. I would say this is a very positive sign for merchants who invest in quality supply.

11 | Introduced one-to-one faster premium express deliveries for more time sensitive shopping needs.

To better meet user demand, especially that of our core users, we continue to improve our delivery services, merchant supply and the whole ecosystem. First, we expanded the coverage of our high-quality delivery service. More food delivery users now choose to use one-to-one express delivery, eDouyin Jisong, and they are willing to pay a premium for faster delivery.

During the holiday shopping season, we further promoted this delivery service for Meituan Instashopping. This service addresses users' time-sensitive shopping needs for categories such as mother and baby products or daily necessities and their needs for high-end gift purchase, including electronics, baiju.

12 | Did numerous initiatives for local restaurants merchants.

In the first quarter, we provided a targeted operational support for more high-quality local restaurant merchants. We launched practical tools and policies to improve merchant experience, including malicious review management, order damage protection and AI-powered operational solutions among others.

On food safety, we launched 10 improvement initiatives in April. We strengthened food safety governance in 3 core areas. The first is merchant onboarding and the second is transparent operations and the third is cross-party supervision. Our goal is to build a safer and more trustworthy food delivery environment for all users.

13 | Improve the supply site with more recommendation lists of merchant restaurants.

First, on the supply side, we built a full-scope value-for-money supply system, spanning all categories and price tiers with a particular emphasis on high-quality supply. We expanded the reach and influence of our authoritative recommendation list, including the Black Pearl List, Hei Zhenzhu, Must-Eat List, Bichi Bang, Must-Visit List and Must-Stay List. This recommendation list help direct targeted traffic to high-quality merchants while providing consumers with clear, reliable guidance to inform their decision making.

14 | Xiaoxiang Supermarket continued to grow rapidly as supply chain capabilities strengthened, and saw faster-growing sales in private label products.

Now let's turn to our new initiatives segment. In the first quarter, we focused on the high-quality development of grocery retail and Keeta. For grocery retail, Xiaoxiang Supermarkets increased its coverage to 55 cities in the first quarter through accelerated expansion. While sustaining robust GTV growth, it further strengthened its supply chain capabilities, offering consumers a broader selection of high-quality and very competitively priced products. For example, in the first quarter, private label products accounted for a higher share of its GTV.

15 | Xiaoxiang supermarket is growing faster than its peers, That on-demand retail will be driven by a hybrid 1P/3P model ocused on high-quality supply with competitively priced products.

yes, we know that all our peers are growing fast. I could say Xiaoxiang is growing even faster. So thank you for paying attention to Xiaoxiang Supermarket. So here Xiaoxiang is competing on a level playing field on the Meituan platform. But it's very important that as everything now becomes the new normal for more and more users, and they are raising their expectations on product variety, quality and value, they know they can get the same very fast delivery from any seller, but they are expecting more from the sellers. And we believe the future growth of on-demand retail markets will be driven by a hybrid model, including the so-called 3P model or like -- or initiatives by Meituan Instashopping and together with a 1P model like a Xiaoxiang Supermarket. And Xiaoxiang provides a very consistently high-quality supply with a very competitively priced product fulfillment.

16 | See grocery retail as a long game, as Xiaoxiang's profit margins continue to improve and is confident that it will become one of the leading China grocery online players, which is aligned with wanting to help people eat better.

So physical store will be a very good channel to strengthen Xiaoxiang's brand awareness over time. And on the other hand, even with this very rapid expansion, we remain very focused on ROI because grocery retail is a long game. And this reflects in our continued year-over-year improvement in margins in Q1. And looking ahead, we are confident that Xiaoxiang will become one of the leading players among online grocery stores. And we are targeting a sustainable low single-digit profit margin in the long run.

But what's most important is that we want to build Xiaoxiang to become one of the most loved grocery brand in future. Because the mission of our company is to help people eat better. Besides food delivery, people who want to cook for themselves need to buy grocery, and we want to build Xiaoxiang to become one of the most loved grocery brands. That's our target.

17 | Keeta continued to achieve meaningful efficiency gains in both Hong Kong and Saudi Arabia faster than expected, saw solid growth in other Middle Eastern countries and Brazil, and losses improved QoQ.

Operationally, Keeta maintained solid growth across all markets in Q1. Following Hong Kong's unit economics breakeven in Q4 last year, we delivered further efficiency gains in both Hong Kong and Saudi Arabia this quarter. This also is encouraging to see that the efficiency in ramp-up in other Middle East markets and Brazil has been even faster, thanks to the operational experience accumulated earlier. We will prioritize operation improvement this year over new market expansion.

18 | Despite near-term challenges in the Middle East due to the war, believe that it is one of the most attractive on-demand delivery markets globally. The market is going fast, penetration remains low, and customers have a strong willingness to pay.

Regarding the Middle East, we have seen some near-term fluctuations in our growth metrics given what's happening in this region. However, the impact has been manageable so far and our long-term conviction for this market is unchanged. We still believe Middle East is one of the most attractive on-demand delivery markets globally. The market is still growing fast, penetration remains low, and consumers there have strong willingness to pay. Notably, even in this challenging environment, we continue to see a clear acceleration in the transition from offline to online. Consumer mind share for on-demand retail continues to strengthen and industry-wide online penetration is accelerating. On-demand delivery has clearly become an essential infrastructure.

19 | Meituan views the local in-store services as much more than a traffic-driven business like Douyin, one-stop local service platform remains strong and expects in-store margin to stay stable in the near term, with room to recover over the longer term

We have always viewed the local in-store services as more than just a traffic-driven business. It is a business built on physical world fulfillment and on consumers' trust. Traffic alone doesn't automatically translate into transactions. In local services, Meituan has built strength that cannot be replicated purely through traffic. While competition has created some near-term noise, we believe market players have to continue to differentiate across category, merchant segment and market scenarios.

Our position as a one-stop local service platform stays strong. Our in-store revenue keeps growing steadily, and we continue to lead in core categories. We have also expanded into new service retail verticals and deepened our reach in lower-tier markets. We expect the in-store margin to stay stable in the near term, with room to recover over the long term. We have the conviction and patience to keep leading the evolution of the local service sector.

20 | With higher oil prices, they expect there will be near-term challenges to the hotel and travel industry. Will focus on their core market leadership in the lower-star hotel segments and continue to expand footprint in the mid- to high-end hotels. Confident of driving healthy, sustainable, and high-quality growth for hotel and travel.

Looking ahead to the full year, we recognize that the recent hike in airline fuel surcharge will bring near-term vulnerability to hotel and travel industry. Long-distance travel and high-star hotels are likely to face headwinds, while short-term distance leisure travel, local accommodations and low-star hotels will remain resilient. Our structural advantage in these resilient domains position us well to navigate the current market cycle.

First, we will further solidify our core market leadership in the low-star hotel sector. Second, we will continue to expand footprint in the mid- to high-end hotels, deepen strategic partnerships with merchants, enrich our offerings and strengthen our ecosystem synergies. We will also continue to leverage the Meituan membership program to deliver targeted services to high-value users and push for further progress in the high-star hotel domain. We are confident in driving healthy, sustainable and high-quality growth for our hotel and travel space.

21 | Positioned their AI assistant, Xiao Tuan in the Meituan app and seeing complex cross-use cases due to its strong foundation backed by authentic consumer reviews and comprehensive information and a proprietary model trained for local service businesses.

We have placed our AI assistant, Xiao Tuan, front and center in the Meituan app. It now sits in the middle of the bottom navigation bar for easier access. But I would say it is still at a very early stage. But anyhow, we are already seeing good initial results. More and more users are coming to Xiao Tuan, not just for very simple and short searches, but for more complex cross-use cases queries, things like please recommend a restaurant between 2 locations for guests who do not eat spicy food or book an on-site repair service.

And what makes Xiao Tuan different is the foundations. It's the authentic consumer reviews and comprehensive POI information and proprietary model trained specifically for local service businesses. Together, this gives Xiao Tuan the ability to understand better the full context and provide users with personalized recommendations. And particularly when users change their mind and adjust criteria like price range, locations or anything else, Xiao Tuan can seamlessly factor that in all prior instructions and update its recommendation accordingly. They are actually using Xiao Tuan to discover services, destinations and ultimately plan and make a purchase on our platform. And beyond the Xiao Tuan, we are also embedding AI deeper into some specific verticals.

See Xiao Tuan as one of Meituan's key AI products on the consumer side and expect to deepen its integration further, will be launching partnership with Tencent's AI chatbot Yuanbao for more agent-to-agent.

And looking ahead, Xiao Tuan will be one of our key AI products on the consumer side. We will continue to deepen its integration into Meituan app. And beyond improving the effectiveness of user agent interactions, we will deploy Xiao Tuan's agentic task execution capabilities progressively across our business verticals. And our partnership between Meituan AI Assistant Xiaomei and the Tencent's AI chatbot Yuanbao will also be launched soon. And when the user submit local services related requests in Yuanbao, it will trigger an agent-to-agent communication with Xiaomei.

22 | Meituan continues to see upside in China's food delivery market as it becomes a high-frequency daily necessity.

And the expected AOV recovery supported by our user structure advantages. And looking long term -- longer term, we continue to see upside in China's food delivery market.

The service is becoming a high-frequency daily necessities for border and broader demographic, a structural shift that provides sustained momentum for deeper market penetration over time. And as we broaden our reach, we also help merchants access a bigger customer base. In fact, we are seeing the industry user base continue to expand.

23 | Food delivery is helping Meituan to penetrate deeper into the lower price segment, increasing the user base, which can position Meituan to capture higher purchase frequency and retention.

On one hand, food delivery is penetrating deeper into the lower price segment. On the other hand, in our better service to consumers seeking premium and diverse options, driving steady expansion in the user base as well. We see high growth potential in purchase frequency and retention for the new users, and we believe our superior services supplies can well position us to capture this upside.

24 | Meituan is of the view that the wave of irrational competition proved that volume acceleration driven solely by subsidy is not sustainable. Ultimately, true long-term growth has to come down from supply-side innovation and better management of demand and supply across diverse use cases.

Looking back, this wave of irrational competition proved one thing. Volume acceleration driven solely by subsidy is not sustainable. True long-term growth comes down to supply-side innovation and better managing of demand supply across diverse use cases. Leveraging AI and other technologies to drive efficiency and experience improvement across the industry is also super important. These are the true foundation for healthy, sustainable growth. And that's exactly where we will continue to invest with conviction.

25 | Meituan continues to have confidence in the industry's long-term growth potential and achieving a sustainable 1 million orders per day and attractive long-term unit economics, As food delivery unit economics improves back to a reasonable level.

We have confidence in the industry long-term growth potential and achieving a sustainable high-quality 1 million order per day stays our target. On long-term unit economics, we expect competition to be more rational, particularly under regulatory guidance. And we are confident in sustaining our industry-leading operational efficiency, which will support our long-term competitiveness. We believe our food delivery long-term UE will get back to a reasonable level. And beyond that, significant synergy potential remains untapped across our core local commerce businesses. We will actively drive cross-selling between food delivery and other services. Ultimately, this will generate a long-term compounding value for the entire core local commerce segment.

26 | Meituan's goal is to reduce information asymmetry in local services and to build a standardized trust system.

Our goal is to reduce information asymmetry in local services and build a standardized trust system. We believe this will help lower barriers to transaction conversion and particularly for nonstandard local service categories, thereby supporting the long-term sustainable growth of both our platform and merchants.

➡️ Final Takeaway on Meituan $MPGNY:

Domestic competition in China food delivery from Alibaba and JD will continue to pressure Meituan’s growth rates and profitability in the near-term. Losses driven by higher subsidies, incentives, advertising look to have peaked in Q3, and has improved QoQ for 2 consecutive quarters and should continue further into 2026. Without price/subsidy led competition, Meituan’s superior product offering will become more dominant, allowing it to defend its market leading position. Remain confident of Meituan’s long-term competitive advantage of their strong intra-city fulfilment, resilience and strong execution. Business “weakness” could likely translate into continued near-term price weakness, which could present very opportunistic long-term buying opportunities. Meituan’s long-term thesis remains intact as China’s go-to platform for on-demand services for local commerce. Continue to see strong progress in international expansion with HK now profitable, Keeta in Saudi Arabia, Qatar, UAE and Brazil.

2

3

1,030

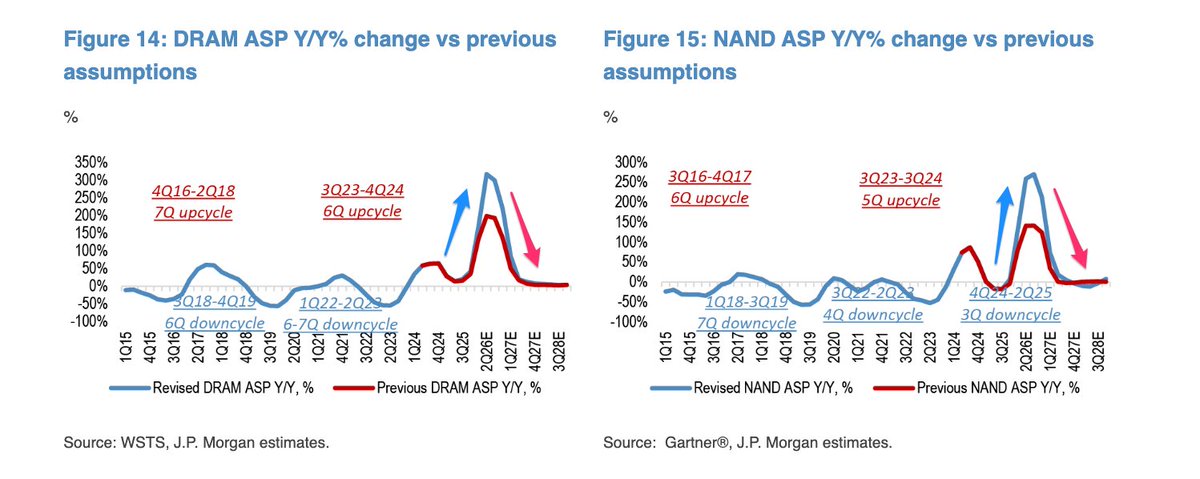

JPM continues to forecast that YoY changes in memory DRAM and NAND ASPs will begin to decelerate rapidly from the end of 2026/early 2027.

While the forecasts (of when and how much) are most likely to be precisely wrong, they should be directionally correct.

Important for those who think memory is not cyclical, and is different this time round.

Interesting to watch how this plays out.

42

40

295

92,504

I am excited about Thomas Chua's @SteadyCompound upcoming book on investing. An excellent book that I highly recommend.

It has been years in the making, and I was fortunate to read an early transcript.

Thomas is extremely intentional in his writing, and the many selected business examples, coupled with his life story, bring investing to life.

"Thomas Chua writes like a friend who has already walked the road and wants to save you from the wrong turns. Every chapter is packed with real experience and real examples. If you want to stop trading and start owning great businesses, this is the book that will show you how."

May 29

Back in 2020, I started this account to post stock breakdowns from my lunch break.

Hardly anyone read them.

Today, something I still can't quite believe: I wrote a book.

📖 The Lunch Break Investor

Out 18 August with Harriman House

For people with real jobs, families & lives who still want to invest properly.

One big shift: Stop renting stocks. Start owning businesses.

One focused lunch break at a time.

What’s your biggest struggle investing while busy? Reply 👇 I’ll share a tip from the book.

1

1

15

6,665

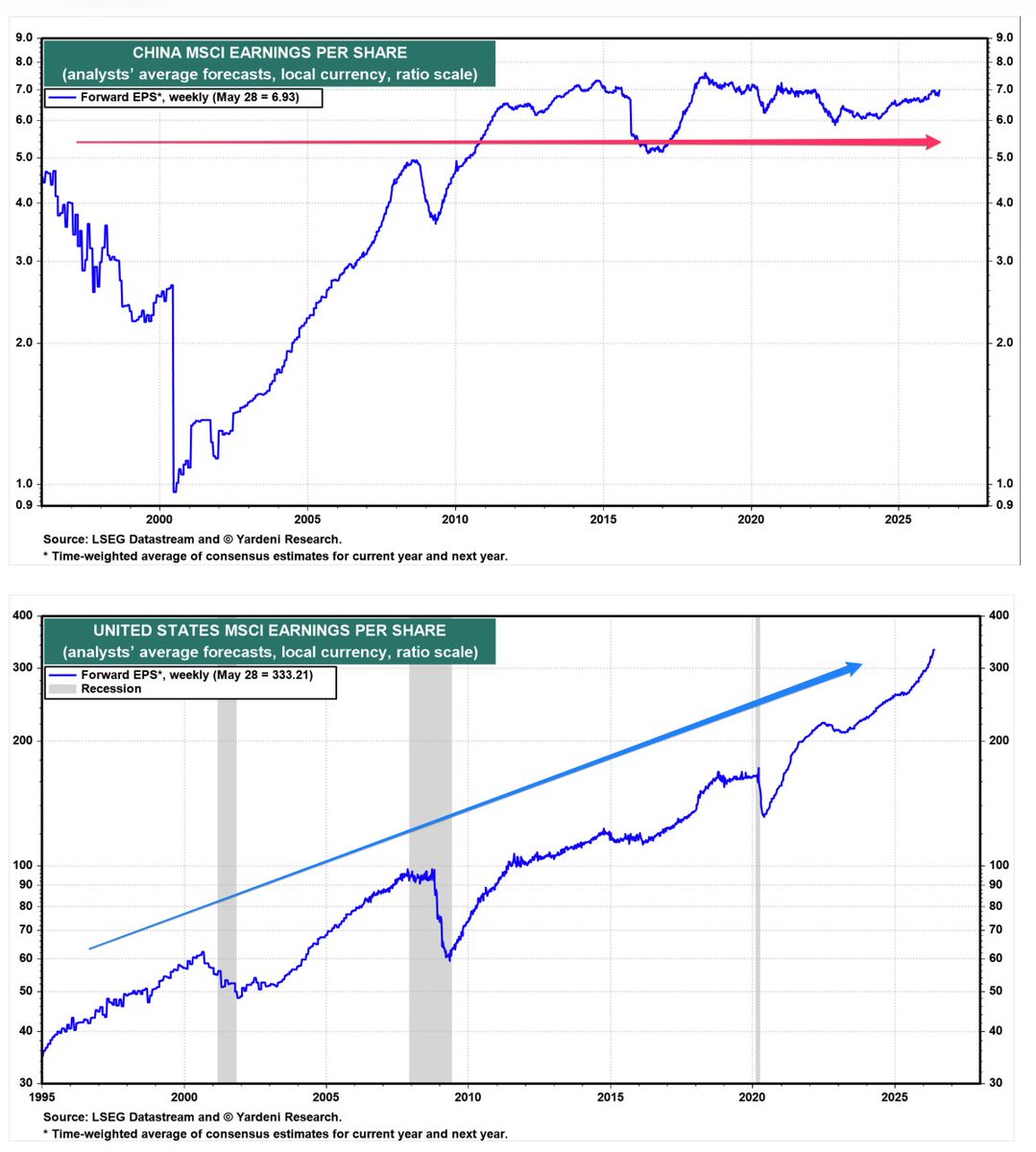

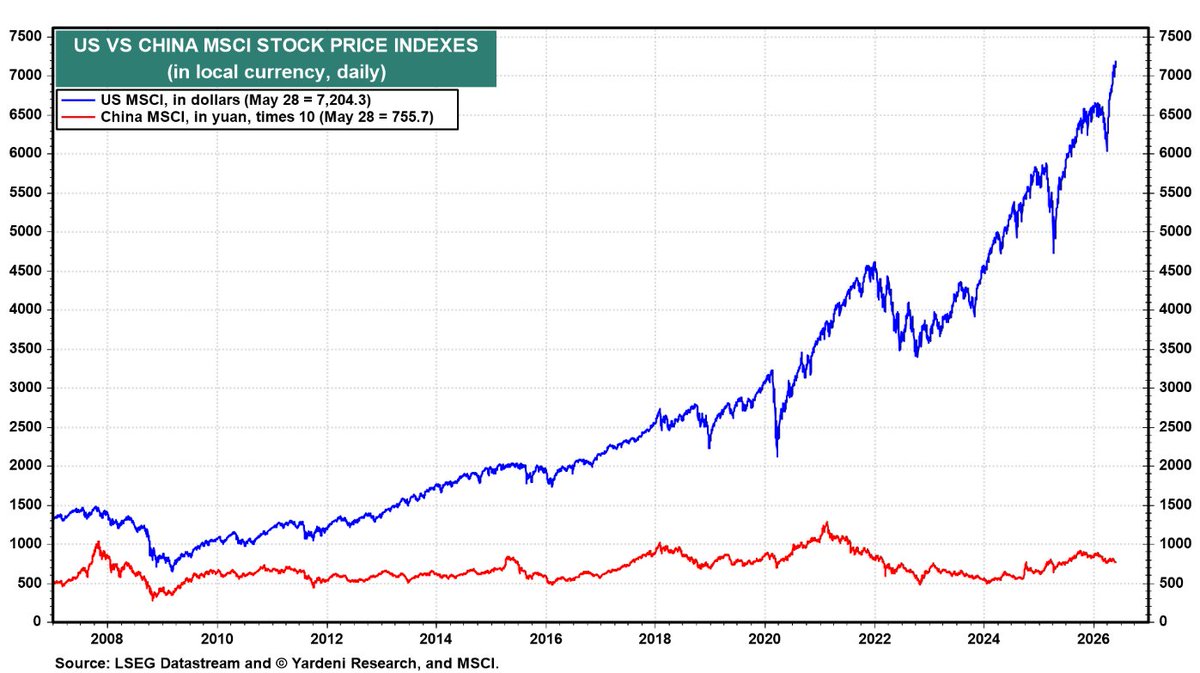

Why did the MSCI US outperform MSCI China over the last 30 years?

Plot out the EPS chart, and the answer becomes clear.

MSCI China's EPS largely went sideways, and its index followed.

MSCI US's EPS continued to rise, and its index followed.

1

6

20

3,284