Joined September 2020

- Tweets 118

- Following 34

- Followers 3,220

- Likes 73

22 Photos and videos

Experian just launched a personal loan shopping experience inside ChatGPT. Alex Johnson thinks it's the right move…but not for the reasons you'd expect.

The real question isn't whether Experian's ChatGPT app works. It's what happens to the entire B2C financial services lead gen business when AI chatbots become the primary interface for shopping loans, credit cards, and insurance.

Companies like Credit Karma, NerdWallet, and LendingTree are betting on two paths: GEO (becoming the source AI models cite) or embedded apps (building first-party experiences that surface inside the chatbot). Both strategies are defensible.

Neither is fully in their control. That's the problem. OpenAI decides who wins. And no partnership agreement changes that.

Experian happens to be the best-positioned to absorb the risk; its core credit bureau business is a floor that its competitors don't have. But the broader industry has a much harder version of this problem to solve.

1

94

Jun 11

Bankruptcies up 14% YoY. New credit card vintages already underperforming. Subprime auto delinquencies at 20-year highs.

No single data point is a crisis. But Alex Johnson and Dave Wasik of 2nd Order Solutions see all three converging into the same uncomfortable conclusion: the consumer credit system has a lot less room for error than it did a year ago.

On the latest Facing Credit, they get into the research behind those yellow flags, the politicization of consumer sentiment data, and what the rollback of disparate impact enforcement actually means for lenders navigating an increasingly complex patchwork of state and federal requirements.

One of the best Facing Credit episodes yet. Go give it a listen: podcasts.apple.com/us/podcas…

1

73

Jun 8

Cash flow intelligence sounds like a no-brainer…until you try to actually deploy it.

Last month Alex, Collin Galster (Nova Credit), and Michael Krzysko (Imprint) broke down what actually happens when lenders deploy cash flow intelligence at scale. The opt-in findings alone are worth the watch.

1

2

6

10,094

Fintech Takes retweeted

Jun 4

Ramp just raised $750M at a $44B valuation, which is roughly 44x their current revenue.

I'm impressed by the level of conviction Ramp has been able to instill in the investors that have poured roughly $3B into the company since 2019, including, most recently, the Ontario Teachers' Pension Plan.

Personally, I'm not sure I get it.

I admire Ramp. It's a super smart company that has a genuinely strong handle on AI and is growing and shipping product extremely fast, but $44B?

That's more than PayPal, which currently has a market cap of $38B on $32B in revenue.

"Fine," you might say. "PayPal is an absolute mess. Ramp should be worth more than it."

OK, what about Fifth Third? It has almost $300B in assets and generated $9B in revenue last year (good for $2.5B in profit). Its market cap is currently the same as Ramp's valuation.

"Yes," you acknowledge. "Fifth Third is a better-run company than PayPal, but it's a bank. It's slow. Looking forward, its growth trajectory is very modest. Ramp's growth potential makes it a much better bet."

So, what about Affirm? Affirm is just as smart as Ramp. It has just as strong a handle on AI as Ramp. It's profitable and on track to generate more than $4B in revenue this year, which would be a 33% increase year-over-year. Affirm's market cap is currently $22B, half of what Ramp was just valued at.

That just doesn't seem correct.

Something is being mispriced and my hunch is that it's Ramp.

But we won't know that until it goes public, if it ever does.

35

4

188

102,698

Fintech Takes retweeted

May 28

"It's not just a step change — it's a slope change."

Chime Co-founder Ryan King on why AI is different from every technology wave before it, and how Chime is building for this moment.

Full conversation with @AlexH_Johnson on @FintechTakes → fintechtakes.com/podcast/202…

6

9

12,292

May 28

So, who pays for what?

Alex Johnson, joined by Rafe Mazer, researcher and author of the report "Who Pays for What? Pricing and Monetization Options in Open Finance” cover the four distinct cost stages of open finance (most countries only plan for one), plus the five pricing archetypes that exist globally, from Brazil's threshold pricing that was never actually collected to South Korea's voluntary, self-governing open banking exchange that works without a single regulatory mandate requiring it.

Spoiler: The U.S., despite having one of the most competitive financial markets in the world, may be poorly positioned to get this right.

Press play: podcasts.apple.com/us/podcas…

1

1

1

126

Fintech Takes retweeted

May 26

One unelected government official who is filling multiple high-level positions and using them to sabotage a government program that has strong bipartisan support from elected government officials seems like a good example of the "deep state" doesn't it?

news.bloomberglaw.com/bankin…

1

10

20

2,312

May 20

The most important insight in AI-powered collections isn't about the technology. It's about why people avoid collections in the first place.

Pedro Maya, Head of Collections and Credit Risk at Tangerine, makes the case clearly: consumers avoid collections calls for the same reason they avoid the doctor. Dread. Discomfort. Shame. The interaction feels threatening before it even starts.

Pedro and Alex dig into what it really takes to train teams to work with AI across the credit lifecycle: podcasts.apple.com/ke/podcas…

2

9

6,758

May 19

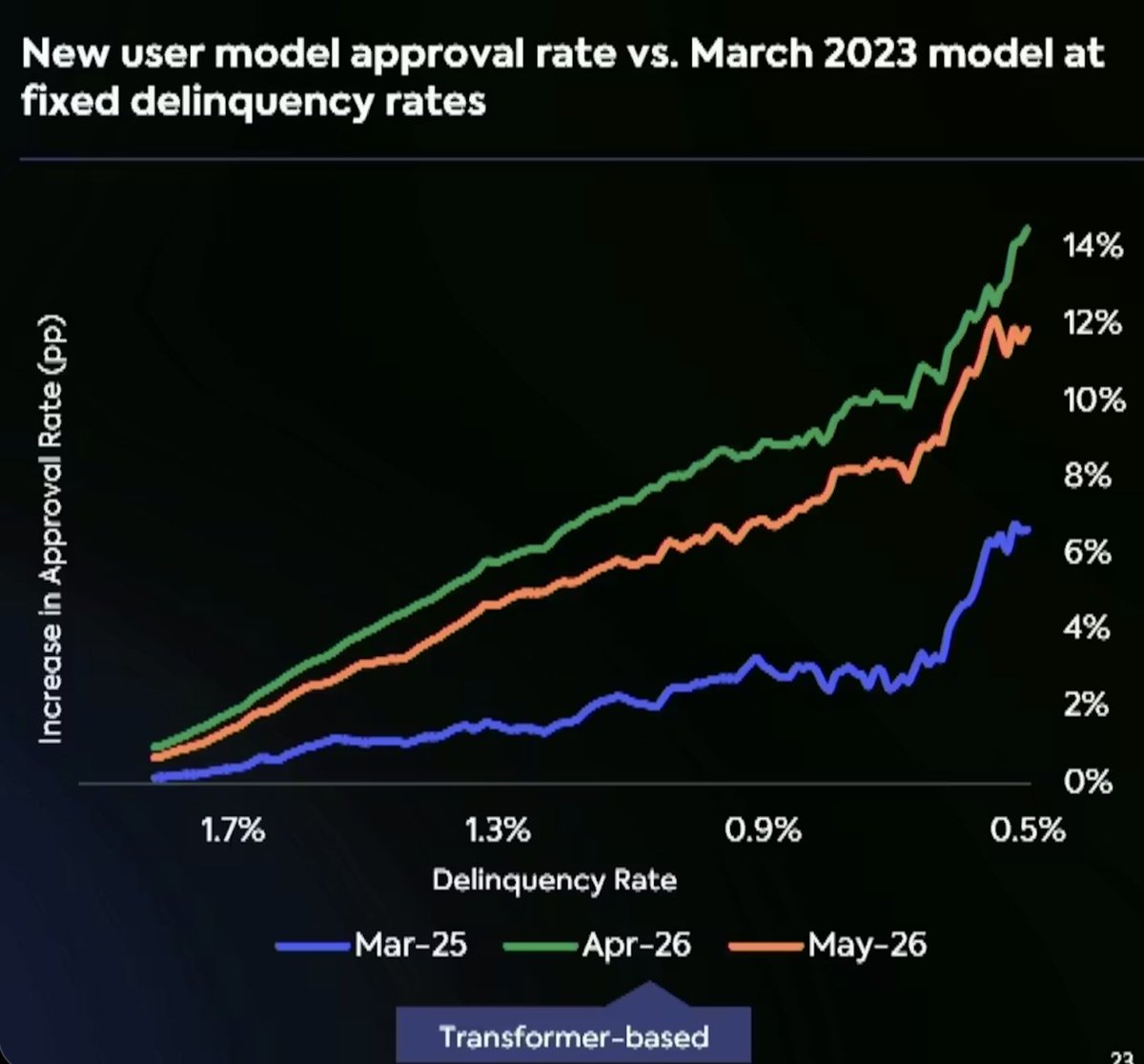

Affirm buried the most interesting part of its investor forum inside 90 seconds of a 3-hour presentation.

At its New York investor day, Affirm's President Libor Michalek disclosed that the company is now testing transformer-based AI models for underwriting -- and they're outperforming its current gradient-boosted models in experiments.

The chart Michalek showed tells the story clearly. The transformer model, despite being older, sits above Affirm's current production model across the full risk-approval frontier. More approvals at the same loss tolerance. On the same data. Same problem. Same methodology.

Why does this matter?

Gradient-boosted models require engineers to hand-pick time windows in a consumer's financial history and flatten them into single numbers. Transformer models can read the full sequence of a consumer's financial behavior -- every purchase, repayment, and balance change, in order -- and find patterns that humans didn't know to look for. Affirm says the model is "discovering more pockets of opportunity more deeply" in its existing data.

Michalek confirmed this is no longer just an experiment. Transformer architecture will become the new baseline across all of Affirm's models.

The credit risk case is obvious. The regulatory questions -- around explainability and replicability -- are harder.

1

192

May 18

Rohit Chopra just landed his next role and fintech companies should be paying attention.

Governor Newsom appointed the former CFPB Director to lead California's new Business and Consumer Services Agency, a cabinet-level umbrella organization launching July 1 that oversees the state's Department of Financial Protection and Innovation, Department of Consumer Affairs, Department of Real Estate, and more.

This isn't a California CFPB. Chopra won't have standalone rulemaking authority; his leverage is directional and coordinative across existing departments. But that may not matter much.

A few things worth watching:

California's market size means state-level enforcement routinely becomes de facto national policy. Providers typically implement California-compliant practices everywhere rather than maintain separate systems.

Chopra has every incentive to swing for the fences. Newsom is term-limited in 2027 and widely expected to run for president. The incentive structure here favors marquee cases over incremental supervision.

Disparate impact, SPCPs, algorithmic underwriting - all of it remains viable under California law, even as the federal government walks away from each. Expect Chopra to pursue exactly the fair lending theories Washington is abandoning.

1

196

May 15

The DOJ just settled a fair lending case against PayPal. There's one problem: no loans were ever made.

PayPal's Economic Opportunity Fund, launched in 2020, directed capital to minority depository institutions, CDFIs, and minority-led VC funds. It issued grants to Black-owned small businesses. It funded nonprofit partners. None of it was lending.

And yet the DOJ opened a fair lending investigation under ECOA, a law that governs credit discrimination.

PayPal settled anyway. The terms aren't punitive - the company agreed to launch a small business initiative focused on veteran-owned businesses and those in farming, manufacturing, and technology. The original fund had already been wound down.

Alex's read: PayPal probably made a calculated decision. The company has an ILC charter application pending with the FDIC, and staying in the administration's good graces has real business value. But the legal logic here is paper-thin, and the precedent it sets is worth paying attention to.

1

257