Jun 13

월요일날 정신병원 가기 전에 또 ㅅㅂ Cisco switch 만질생각하니 어질어질하다잉... 어째 이곳에 네트워크 할 줄 아는 가용 인원이 CISCO APJC 딱 한번 5년도 더 전에 수상한 나밖에 없어서 자꾸 ㅅㅂ 기억 더듬으면서 IOS config 만지게 하는거지 책임질 수 있나??

4

85

Jun 12

In this clip from the Culture shift for telco transformation session at DSP Leaders World Forum, co-host Neil McRae, Group CTIO at @CityFibre, who joined remotely, argued that telcos have lost confidence in their engineering capabilities and outsourced critical thinking.

▶️ Watch the full discussion on demand here: telecomtv.com/content/dsp-le…

Also featuring:

⭐ Fahim Sabir, VP, Digital Platform Architecture & Engineering, @Colt_Technology Services

⭐ Jed Pell, MD & Senior Vice President EMEA & APJC, Alianza

⭐ Guarav Sehgal, VP Sales Europe, @tech_mahindra

⭐ Séainín McCoy, Director for Data and AI, @BTGroup

#DSPLeaders #DSPLWF26 #Telecoms #AI #DigitalTransformation #Automation #Networks #GenAI

1

105

Jun 10

Congrats to @peternoszek and SuperAI team on building this influential conference in Singapore.

What they have greatly succeeded in bringing AI experts & companies from west and east together. This conference is quite remarkable in that sense.

After-all, AI is not only a Silicon Valley/Bay Area phenomenon anymore. APJC region contribute greatly in terms of Open Source, Robotics, Semiconductors.

They also got deep thinkers about the impact of AI on society. Also, in addition to model builders, hyper-scalars etc. they also got compute exchanges there too.

Singapore has emerged as, the "Switzerland of AI", and this is a perfect conference format.

Jun 10

SuperAI Day 1 – 10,000 people across 3 floors.

In 2024 convincing people to fly to Singapore for a new AI conference took heavy lifting. 2 years later, the industry is coming in from SF, NY, Boston, Shanghai, Beijing, Shenzhen.

Singapore is cooking.

1

1

8

1,037

Jun 10

APJC Webinar I From Mythos to Reality: Breaking down Must do’s in a Post Glasswing World bit.ly/3SvuH3U

7

Jun 5

In this DSP Leaders World Forum session, Séainín McCoy, Director for Data and AI at @BTgroup, discusses whether the focus should be on techco transformation or rediscovering core telecommunications strengths, with an emphasis on outcome-focused leadership and cross-functional collaboration.

▶️ Watch the full panel discussion, ‘Culture shift for telco transformation’: telecomtv.com/content/dsp-le…

Also featuring:

⭐ Co-host Neil McRae, Group CTIO, @CityFibre

⭐ Fahim Sabir, VP, Digital Platform Architecture & Engineering, @Colt_Technology Services

⭐ Jed Pell, MD & Senior Vice President EMEA & APJC, Alianza

⭐ Guarav Sehgal, VP Sales Europe, @Tech_Mahindra

#DSPLeaders #DSPLWF26 #Telecoms #Engineering #CultureShift #NetworkStrategies #Techco

2

2

97

May 26

【速報】APJC NetAcad Riders 2026

日本国内大会1位~3位独占受賞!世界大会では2位・3位をネットワークセキュリティ科の学生が受賞しました!

👏!おめでとうございます!👏

linkedin.com/posts/cisco-net…

2

10

676

May 20

Our second panel discussion, Culture shift for telco transformation, live from day two of DSP Leaders World Forum 2026 in Windsor, explores how operators can evolve from legacy telecom businesses into agile, customer-centric and AI-driven digital service providers.

Featuring:

⭑ Co-hosted by Neil McRae, Group CTIO, @CityFibre

⭑ Fahim Sabir, VP, Digital Platform Architecture & Engineering, @Colt_Technology Services

⭑ Jed Pell, MD & Senior, Vice President EMEA & APJC, Alianza

⭑ Ranjan Band, Global Telco Portfolio Solutions, @tech_mahindra

⭑ Séainín McCoy, Director for Data and AI, @BTGroup

☞ Watch live here: telecomtv.com/content/dsp-le…

☞ Take part in the live viewer poll and submit your questions: telecomtv.com/content/dsp-le…

#DSPLWF26 #Business #DigitalServices #Telecoms #DSPLeaders

2

49

May 20

Désolé on dit AVJC APJC

d'ailleurs t'es un rebeu c'est pas censé te choquer que l'on parle de Isa/Jésus comme d'une référence de date

1

25

1,207

May 14

🚨 How do telcos reinvent themselves as digital service providers?

Join the panel discussion on the culture shift behind telco transformations, taking place on Wednesday 20 May, day two of DSP Leaders World Forum, to explore how operators can evolve from product-oriented legacy businesses into agile, customer-centric, AI-driven technology companies.

An expert lineup of industry leaders will share their perspectives:

⭐ Neil McRae, Group CTIO, @CityFibre (Co-host)

⭐ Amol Phadke, Chief Transformation Officer, @tech_mahindra

⭐ Fahim Sabir, VP, Digital Platform Architecture & Engineering, @Colt_Technology Services

⭐ Jed Pell, MD & Senior Vice President EMEA & APJC, Alianza

⭐ Séainín McCoy, Director for Data and AI, @BTGroup

👉 Register to watch live on TelecomTV: telecomtv.com/content/dsp-le…

👉 View the full agenda: telecomtv.com/content/dsp-le…

#DSPLWF26 #DSPLeaders #TelcoTransformation #DigitalTransformation #AI #Leadership #Telco #Telecoms

1

2

2

69

May 14

IATA APJC (Agency Programme Joint Council) Türkiye Toplantısı, 12 Mayıs 2026 tarihinde Birliğimizin ev sahipliğinde TÜRSAB Genel Merkezi’nde gerçekleştirildi.

Konsey üyesi Havayolu temsilcileri ve seyahat acentaları temsilcilerinin katılımıyla düzenlenen toplantıda; havayolu taşımacılığı ile seyahat acentacılığı sektörü arasındaki iş birliği süreçleri, sektörel gelişmeler ve güncel uygulamalar değerlendirildi. Toplantıda ayrıca sektör paydaşlarının karşı karşıya bulunduğu güncel sorunlar ele alınarak çözüm önerileri üzerine görüş alışverişinde bulunuldu; karşılıklı koordinasyonun ve iş birliğinin güçlendirilmesine yönelik değerlendirmeler yapıldı.

Katılım sağlayan tüm sektör temsilcilerine katkıları ve değerli görüşleri için teşekkür ederiz.

19

28

331

May 14

WI-FI 7 AND ENTERPRISE ACCESS SEMICONDUCTOR CONTENT (READ-THROUGH 8)

Affected companies: Qualcomm (QCOM: United States); Broadcom (AVGO: United States); MediaTek (2454: Taiwan); Skyworks Solutions (SWKS: United States).

Directional impact and magnitude: Positive, low to medium magnitude. The read-through is high conviction for Wi-Fi 7 adoption but more diffuse for individual suppliers because Cisco did not disclose chipset suppliers or bill-of-material allocations.

Supporting Cisco commentary and data points: Cisco reported its highest-ever wireless orders, up more than 40% YoY. Wi-Fi 7 made up half of the wireless mix in Q3, and the presentation stated that Wi-Fi 7 orders continue to grow high double digits sequentially while generating demand for bundled multi-gig switches.

Transmission mechanism: Enterprise Wi-Fi 7 adoption increases demand for higher-performance Wi-Fi chipsets, RF front-end content, Ethernet switching silicon, and multi-gig access infrastructure. The most direct supplier impact is higher chipset and RF content per access point as enterprises migrate from older Wi-Fi standards to Wi-Fi 7. Broadcom is mixed because it benefits from Wi-Fi silicon demand but faces the separate negative read-through from Cisco Silicon One in AI networking.

Near-term catalyst versus longer-duration shift: The near-term catalyst is Cisco’s disclosure that Wi-Fi 7 already represents half of wireless mix. The longer-duration shift is enterprise access networks becoming higher-bandwidth, AI-ready, and more tightly bundled with multi-gig switching.

FIREWALL AND NETWORK SECURITY COMPETITIVE RESET (READ-THROUGH 9)

Affected companies: Fortinet (FTNT: United States); Palo Alto Networks (PANW: United States); Check Point Software (CHKP: Israel).

Directional impact and magnitude: Negative for firewall competitive sentiment, medium magnitude. Positive for the broader cybersecurity demand environment, but the company-specific read-through for firewall incumbents is negative because Cisco’s product refresh appears to be gaining traction.

Supporting Cisco commentary and data points: Cisco said core security excluding Splunk saw double-digit order growth across new and refreshed products, with strong double-digit firewall order growth. Robbins said the legacy drag was less severe than in the first half and added: “We got a several-quarter run of big win rates, and we’re feeling good about that.” Cisco also stated that more than 1,000 new customers purchased new security products in Q3, bringing total net new customers to approximately 5,000 since launch.

Transmission mechanism: Cisco’s firewall and security momentum creates competitive pressure through bundling secure networking, firewalls, XDR, Secure Access, Hypershield, AI Defense, and network fabric security. If Cisco is improving win rates while customers modernize networks for AI and security, Fortinet, Palo Alto, and Check Point may face tougher refresh competition, pricing pressure, or slower share gains in enterprise accounts where Cisco is the incumbent networking vendor.

Near-term catalyst versus longer-duration shift: The near-term catalyst is Cisco’s strong double-digit firewall order commentary. The longer-duration shift is network security becoming more embedded into the switching, routing, and campus fabric, potentially favoring vendors with deep network installed bases.

AGENTIC AI SECURITY, IDENTITY, AND VULNERABILITY MANAGEMENT (READ-THROUGH 10)

Affected companies: CrowdStrike (CRWD: United States); Zscaler (ZS: United States); CyberArk Software (CYBR: Israel); Okta (OKTA: United States); Qualys (QLYS: United States); Rapid7 (RPD: United States); Palo Alto Networks (PANW: United States).

Directional impact and magnitude: Positive long-term, medium to high magnitude. Near-term impact is low to medium because Cisco explicitly said Q3 had no meaningful Mythos-driven orders. The secular read-through is stronger than the immediate revenue read-through.

Supporting Cisco commentary and data points: Cisco discussed Project Glasswing, private testing of Anthropic’s Claude Mythos Preview model for proactive cybersecurity defense testing, OpenAI’s Trusted Access for Cyber program, DefenseClaw for protecting AI agents, zero-trust access for AI agents, and the intent to acquire Galileo and Astrix for agentic identity, access management, and behavior monitoring. Robbins said customers are concerned about “unpatched technology” and especially equipment past “last day of support” that cannot be patched. He also said there were effectively no meaningful Q3 orders driven by Mythos, but “that could change in the future.”

Transmission mechanism: Agentic AI creates new identities, access paths, behavioral risks, and machine-speed attack surfaces. This supports demand for identity security, zero trust, cloud security, vulnerability management, exposure management, endpoint protection, SOC automation, and AI application security. CyberArk and Okta benefit from machine and agent identity demand; Zscaler benefits from zero-trust access and traffic inspection; CrowdStrike and Palo Alto benefit from platform security and SOC automation; Qualys and Rapid7 benefit from vulnerability and exposure remediation tied to unpatched infrastructure.

Near-term catalyst versus longer-duration shift: The near-term catalyst is limited because Cisco said Mythos did not materially affect Q3 orders. The longer-duration shift is potentially significant: AI agents expand the identity and attack surface beyond human users and traditional workloads, creating a new security budget category.

SPLUNK CLOUD TRANSITION AND OBSERVABILITY MODEL SHIFT (READ-THROUGH 11)

Affected companies: Datadog (DDOG: United States); Elastic (ESTC: United States); Dynatrace (DT: United States); Cisco Systems (CSCO: United States).

Directional impact and magnitude: Positive for cloud-native observability and security analytics vendors, medium magnitude. Negative near-term for Cisco/Splunk reported revenue growth, medium magnitude. The read-through is less about customer demand weakness and more about revenue-model transition risk for legacy on-premise or license-heavy observability/SIEM businesses.

Supporting Cisco commentary and data points: Cisco said Splunk continued to see an acceleration in the shift to cloud subscriptions and away from on-premise deals, creating a near-term drag on revenue growth. Robbins said Splunk’s FY27 trajectory depends on whether the cloud versus on-prem mix stabilizes, noting that the cloud mix shifted another 2 to 3 points in Q3 from Q2. Cisco reported Observability revenue growth of only 3% and Security revenue flat.

Transmission mechanism: Cloud-native observability vendors benefit when customers prefer cloud subscriptions, faster deployment, and usage-based models. Splunk’s transition may improve long-term quality but depress near-term recognized revenue. Datadog, Elastic, and Dynatrace can use the transition period to compete for cloud-native observability, security analytics, and AI monitoring workloads, particularly where buyers want to avoid legacy on-premise migration complexity.

Near-term catalyst versus longer-duration shift: The near-term catalyst is Cisco’s explicit warning that Splunk’s cloud shift is a revenue drag. The longer-duration shift is the observability/SIEM market migrating toward cloud-native, AI-assisted, subscription-based platforms.

IT DISTRIBUTION, VARS, AND PUBLIC SECTOR INTEGRATORS (READ-THROUGH 12)

Affected companies: CDW (CDW: United States); TD SYNNEX (SNX: United States); Insight Enterprises (NSIT: United States); Arrow Electronics (ARW: United States); Leidos Holdings (LDOS: United States); Booz Allen Hamilton (BAH: United States); CACI International (CACI: United States); Science Applications International Corp (SAIC: United States).

Directional impact and magnitude: Positive, medium magnitude for IT channel and integration demand. The strongest read-through is to revenue activity and backlog conversion rather than gross margin, because Cisco price increases may lift revenue but also create pricing and working capital complexity for channels.

Supporting Cisco commentary and data points: Cisco disclosed total product orders up 35% YoY and up 19% excluding hyperscalers. Enterprise product orders grew 18%, Public Sector grew 27%, and all geographies delivered double-digit product order growth, with Americas up 35%, EMEA up 39%, and APJC up 25%. Cisco also described broad-based demand for campus networking, data center switching, wireless, security, and industrial IoT.

Transmission mechanism: Cisco’s broad order strength implies higher enterprise and public sector network modernization activity flowing through resellers, distributors, and integrators. CDW, TD SYNNEX, Insight, and Arrow can benefit from higher Cisco-related product flow, attached services, and refresh programs. Public sector integrators such as Leidos, Booz Allen, CACI, and SAIC benefit if government customers accelerate secure networking, AI readiness, and cyber modernization programs. Cisco did not disclose specific channel partner beneficiaries, so the read-through is sector-level rather than relationship-specific.

Near-term catalyst versus longer-duration shift: The near-term catalyst is product order acceleration across Enterprise and Public Sector. The longer-duration shift is network modernization becoming a prerequisite for AI, zero trust, and cyber resilience across government and enterprise environments.

TELCO AND SERVICE PROVIDER ROUTING RECOVERY (READ-THROUGH 13)

Affected companies: Nokia (NOKIA: Finland); Ciena (CIEN: United States); Adtran Holdings (ADTN: United States); AT&T (T: United States); Verizon Communications (VZ: United States); T-Mobile US (TMUS: United States).

Directional impact and magnitude: Positive for routing and optical equipment demand, low to medium magnitude. Mixed to slightly negative for telco operators near term because AI readiness implies incremental capex without a clearly disclosed monetization mechanism. Competitive impact for Nokia, Ciena, and Adtran is mixed because Cisco’s own routing strength may indicate Cisco share gains, but the demand signal is constructive for the broader network equipment cycle.

Supporting Cisco commentary and data points: Cisco disclosed Service Provider & Cloud orders up 105% YoY, telco orders up 9%, and triple-digit growth in service provider routing and compute. Robbins said telcos are investing in Cisco technology “as they prepare their networks to handle the scale, speed, and complexity of AI.”

Transmission mechanism: AI traffic, distributed inference, and cloud connectivity require higher-capacity routing, optical transport, and network automation. Equipment vendors benefit from routing and transport upgrade budgets. Telco operators face higher capex intensity as they modernize networks for AI traffic, although the call did not provide evidence that operators are receiving incremental AI monetization sufficient to offset that spend.

Near-term catalyst versus longer-duration shift: The near-term catalyst is Cisco’s telco and service provider order acceleration. The longer-duration shift is AI traffic potentially becoming a new driver of IP routing and transport capex after a multi-year period of uneven telco spending.

INDUSTRIAL IOT, ONSHORING, AND PHYSICAL AI (READ-THROUGH 14)

Affected companies: Rockwell Automation (ROK: United States); Siemens (SIE: Germany); Schneider Electric (SU: France); Emerson Electric (EMR: United States); Fortinet (FTNT: United States); Cisco Systems (CSCO: United States).

Directional impact and magnitude: Positive, low to medium magnitude today, with medium longer-duration potential. The signal is high quality because Cisco reported its strongest-ever Industrial IoT quarter and linked demand to manufacturing, utilities, onshoring, agentic AI, and physical AI, but the absolute size relative to large industrial automation vendors was not disclosed.

Supporting Cisco commentary and data points: Cisco stated that its Industrial IoT portfolio reported its strongest quarter ever in Q3 and has grown double digits for 8 consecutive quarters. The presentation said growth was driven by manufacturing and utilities. Robbins said Cisco expects demand to continue “with the onshoring of manufacturing to the United States and as agentic and physical AI are expected to drive massive increases in network traffic.”

Transmission mechanism: Industrial AI, robotics, factory automation, grid modernization, and onshoring require hardened networking, secure OT connectivity, edge compute, and integration with automation systems. Rockwell, Siemens, Schneider, and Emerson benefit from broader industrial automation modernization. Fortinet benefits from OT security demand, although Cisco is also a competitor through secure networking. Cisco benefits directly through Industrial IoT networking and edge connectivity.

Near-term catalyst versus longer-duration shift: The near-term catalyst is Cisco’s strongest-ever Industrial IoT quarter. The longer-duration shift is the convergence of industrial automation, secure networking, edge compute, and physical AI as factories and utilities modernize infrastructure.

HARDWARE PRICE INCREASES AND ENTERPRISE IT INFLATION (READ-THROUGH 15)

Affected companies: Dell Technologies (DELL: United States); Hewlett Packard Enterprise (HPE: United States); Arista Networks (ANET: United States); Extreme Networks (EXTR: United States); Fortinet (FTNT: United States); Palo Alto Networks (PANW: United States); CDW (CDW: United States); TD SYNNEX (SNX: United States).

Directional impact and magnitude: Mixed. Positive for hardware vendors’ revenue and margin defense if price increases stick, medium magnitude. Negative for customers and potentially for unit demand elasticity, low to medium magnitude. Positive for distributors’ reported revenue but mixed for reseller margins and working capital.

Supporting Cisco commentary and data points: Cisco disclosed that hardware price increases contributed 4 to 5 points of acceleration to ex-webscale order growth in Q3, with no software price increases. Management also said pricing impact should be higher in Q4 as increases are fully absorbed, and that Q4 revenue will begin to reflect pricing benefits. Cisco tightened price-increase terms from a multi-month exposure window to roughly 30 days.

Transmission mechanism: Cisco’s ability to pass through memory and component inflation creates a pricing umbrella for other networking and hardware vendors. This can support revenue and protect gross margins across hardware vendors, but it also raises the risk that order growth overstates unit demand. For the channel, higher list prices can lift revenue dollars but may compress margins if customers resist or if vendors alter discounting and quote windows. The fact that Cisco explicitly separated unit growth from price growth is important because it reduces the pure-volume interpretation of enterprise IT demand.

Near-term catalyst versus longer-duration shift: The near-term catalyst is higher Q4 hardware pricing flowing into orders and revenue. The longer-duration shift is a more inflationary enterprise hardware environment where vendors with supply security and installed-base leverage can preserve margin, while smaller or less differentiated vendors may struggle.

BOTTOM-LINE MARKET IMPLICATION

Cisco’s call is broadly positive for AI infrastructure, coherent optics, memory suppliers, enterprise private AI infrastructure, data center physical infrastructure, Wi-Fi 7, industrial IoT, and agentic cybersecurity. The highest-conviction positive read-throughs are to coherent optics, memory, enterprise AI infrastructure, power/cooling infrastructure, and security categories tied to AI agents and unpatched infrastructure. The highest-conviction negative read-throughs are competitive: Cisco’s Silicon One momentum pressures AI networking peers and merchant silicon narratives; Cisco’s campus and wireless refresh pressures enterprise networking challengers; Cisco’s firewall order momentum pressures firewall incumbents; and hyperscaler AI network orders reinforce capex/free-cash-flow pressure on cloud platforms. The most important non-consensus conclusion is that AI infrastructure demand is becoming more network-, optics-, memory-, and security-intensive, not merely GPU-intensive.

SOURCE MATERIALS

Cisco Q3 FY26 earnings call transcript.

Cisco Q3 FY26 conference call presentation.

2

1,928

May 14

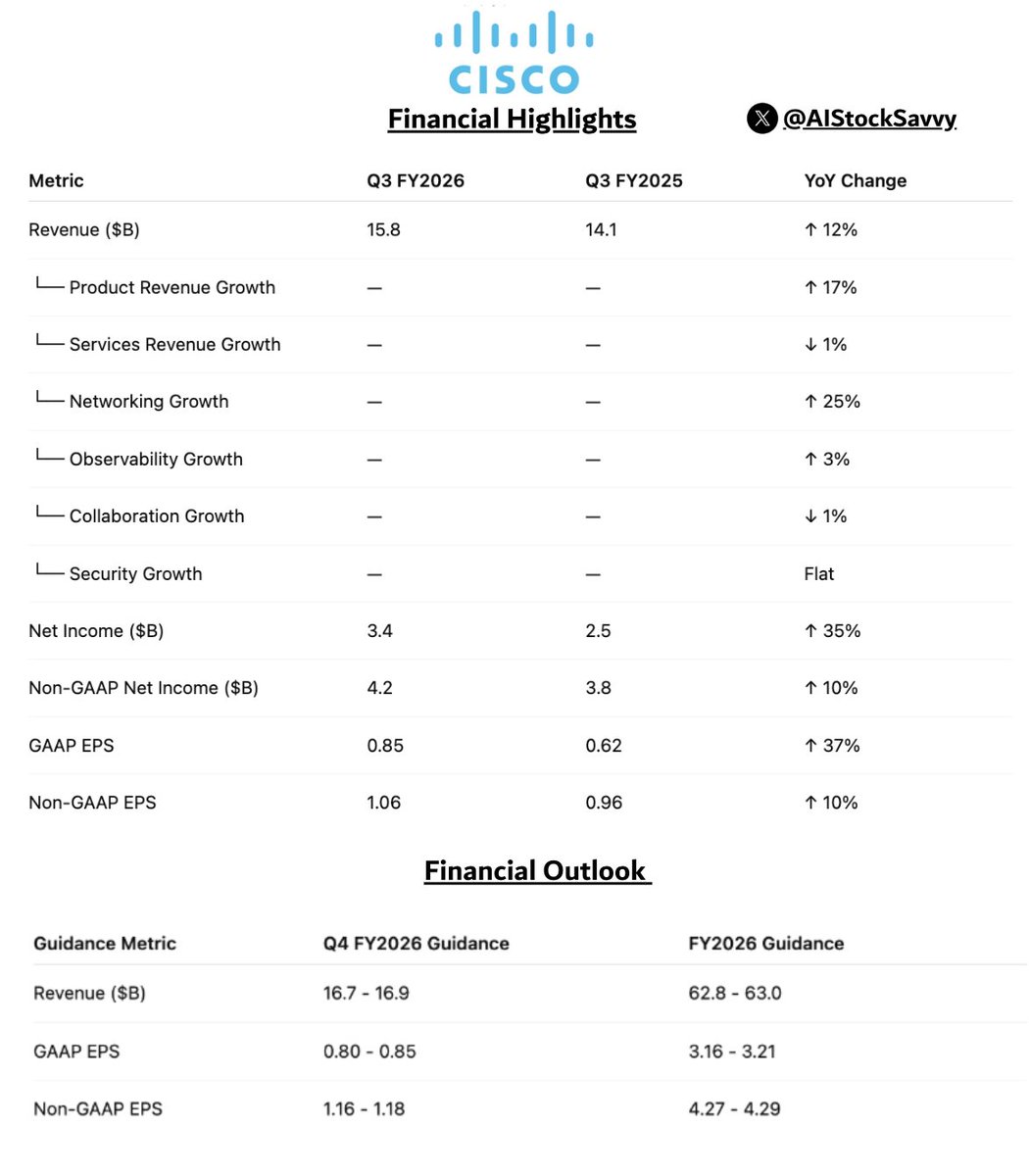

$CSCO EXECUTIVE CALL SUMMARY: Cisco Systems Inc (05/13/26)

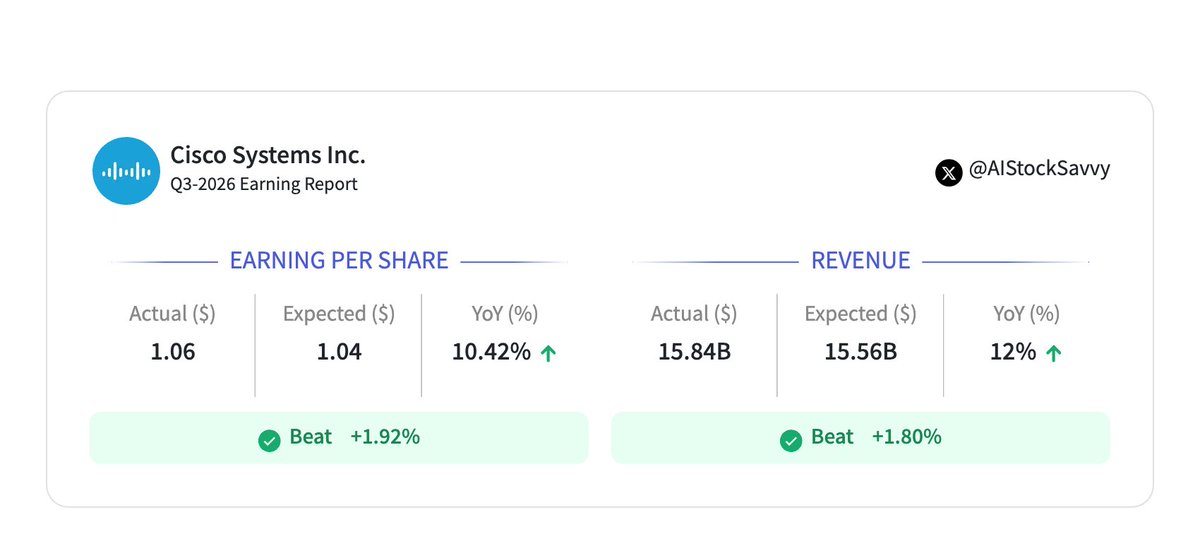

Cisco delivered a materially positive Q3 FY26 call, with the investment debate shifting further from “legacy networking recovery” toward “AI infrastructure scale, campus refresh durability, and margin absorption under hardware mix pressure.” The quarter was strong on reported results and stronger on orders. Revenue reached a record $15.8B, up 12% YoY, above the high end of guidance. Non-GAAP EPS was $1.06, up 10% YoY, also above the high end of guidance. Product revenue grew 17%, led by Networking revenue up 25%, while product orders grew 35% and remained broad-based even after excluding hyperscaler demand, with ex-hyperscaler product orders up 19%. The quality of demand was better than a simple AI-driven hyperscaler spike: Enterprise product orders grew 18%, Public Sector grew 27%, and all geographies posted double-digit product order growth. The key caveat is that order growth was not purely unit-driven; management disclosed that price increases accounted for 4 to 5 points of the acceleration in ex-webscale order growth, and acknowledged some pull-ahead, though characterized it as modest.

The most important incremental message was the step-up in AI infrastructure expectations. Cisco raised expected FY26 hyperscaler AI infrastructure orders to approximately $9B from the prior $5B target and raised expected FY26 hyperscaler AI infrastructure revenue to approximately $4B from $3B. Hyperscaler AI orders reached $1.9B in Q3 and $5.3B YTD, already exceeding the prior full-year target with 1 quarter remaining. The new FY26 target implies approximately $3.7B of Q4 hyperscaler AI orders, a large sequential acceleration, which management framed as non-linear but supported by design wins, optics strength, and Silicon One adoption. Management also said it is “reasonable to expect” at least $6B of hyperscaler AI revenue in FY27, which creates a tangible bridge from order strength into next-year revenue growth, though it is not formal FY27 guidance.

The quarter also strengthened the campus refresh narrative. Campus networking orders grew more than 25% YoY, wireless orders grew more than 40% YoY, Wi-Fi 7 represented half of the wireless mix, and data center switching orders grew more than 40% YoY. Management linked enterprise demand to AI inference, agentic workloads, network modernization, and security hardening rather than only cyclical replacement. The company presentation also highlighted a pre-Catalyst 9K installed base in the tens of billions of dollars nearing end of support, which supports a multi-year refresh thesis. This is important because the stock can work better if investors conclude that Cisco’s growth is not solely hyperscaler concentration risk but also includes a large enterprise and campus modernization cycle.

Margins were the main offset. Non-GAAP gross margin declined 260 bps YoY to 66.0%, and product gross margin declined 330 bps YoY to 64.3%, driven primarily by negative mix and higher memory costs, partly offset by productivity improvements and pricing. Management said gross margins have stabilized, with Q4 non-GAAP gross margin guided to 65.5% to 66.5%, but the mix shift toward hardware and AI infrastructure is structurally less favorable than a software-led mix. Operating discipline protected earnings quality: non-GAAP operating margin was 34.2%, only down 30 bps YoY, as non-GAAP operating expenses fell to 31.9% of revenue from 34.1% a year ago. The implication is that Cisco can absorb gross margin pressure for now through price, supply-chain productivity, scale, and opex discipline, but the model is becoming more dependent on hardware execution and supply availability.

Security remained mixed. Core security orders excluding Splunk grew double digits, firewalls grew strong double digits, and more than 1,000 new customers purchased new products including Secure Access, XDR, Hypershield, and AI Defense in Q3. However, Security revenue was flat as new and refreshed products continued to be offset by prior-generation declines and the Splunk transition from on-premise deals to cloud subscriptions. Management sounded more constructive on the organic security portfolio than in prior periods, stating that the legacy drag was less severe than in the first half and that the company remains on pace to exit FY26 approaching double-digit revenue growth in organic Cisco security. Splunk remains a revenue headwind near term, and FY27 performance will depend heavily on whether the cloud mix shift stabilizes.

The guidance was strong. Q4 revenue guidance of $16.7B to $16.9B implies a record quarter, approximately 6% sequential revenue growth at the midpoint versus Q3, and management stated that it implies 14.5% top-line growth. Q4 non-GAAP EPS guidance of $1.16 to $1.18 implies approximately 10% sequential growth at the midpoint. FY26 revenue guidance of $62.8B to $63.0B and non-GAAP EPS guidance of $4.27 to $4.29 indicate Cisco is positioned for its strongest year ever and for double-digit top-line and bottom-line growth. Prior full-year revenue and EPS guidance values were not disclosed in the provided material, so the magnitude of the full-year guidance raise cannot be quantified beyond management’s statement that FY26 guidance was raised.

The stock implication is positive but not without quality debate. The call likely supports upward revisions to revenue estimates for Q4, FY26, and FY27, particularly in AI infrastructure and Networking. It also supports a higher strategic narrative multiple if investors increasingly view Cisco as a beneficiary of AI networking, coherent optics, and enterprise inference rather than a mature campus networking incumbent. The principal risk is that the mix of growth is becoming more hardware-heavy, more hyperscaler-influenced, more supply-chain dependent, and more exposed to memory inflation and inventory commitments. The call was therefore positive on demand, positive on revenue visibility, positive on AI relevance, mixed on gross margin quality, and still inconclusive on Security/Splunk.

QUARTERLY PERFORMANCE AND QUALITY OF RESULTS

Q3 FY26 was a high-quality top-line quarter, with record revenue of $15.8B, up 12% YoY, above the high end of guidance. Product revenue was $12.1B, up 17%, and Services revenue was $3.7B, down 1%, primarily due to timing of service contract start dates. The growth engine was clearly product-led and heavily skewed toward Networking, AI infrastructure, campus refresh, and data center switching. Services weakness was not framed as demand deterioration, but the negative growth in Services and the modest growth in software and ARR reduce the “quality” of the quarter from a recurring-revenue perspective.

Networking was the standout contributor. Networking revenue was $8.8B, up 25% YoY, reflecting accelerating growth in AI infrastructure and campus refresh. Security revenue was $2.0B, flat YoY. Collaboration revenue was $1.0B, down 1%, with Webex declines partly offset by devices. Observability revenue was $269M, up 3%. Services revenue was $3.7B, down 1%. This mix indicates Cisco’s growth was not broad across all reported revenue categories; it was highly concentrated in Networking and product-led infrastructure. That concentration is positive if the AI and campus cycles prove durable, but it creates margin and cyclicality questions because the fastest-growing areas are more hardware-intensive.

Product orders were the most important performance metric in the quarter. Total product orders grew 35% YoY, and excluding hyperscaler orders grew 19%. This is materially stronger than reported revenue growth and gives Q4 and FY27 greater visibility. Management emphasized broad-based strength: Americas product orders grew 35%, EMEA grew 39%, and APJC grew 25%. By customer market, Enterprise grew 18%, Public Sector grew 27%, and Service Provider & Cloud grew 105%. The breadth matters because it reduces the risk that the quarter was solely a hyperscaler AI order spike. However, the Service Provider & Cloud growth rate was the largest driver and was clearly lifted by hyperscaler AI demand.

The order quality had several positive attributes. First, growth was broad across geographies and customer segments. Second, Networking product orders grew more than 50%, marking the seventh consecutive quarter of double-digit growth in the portfolio. Third, enterprise data center switching orders grew more than 40%, suggesting enterprise AI and private data center infrastructure are contributing, not only public cloud. Fourth, campus orders grew more than 25%, and wireless orders reached a record level, up more than 40%. These data points support a multi-cycle demand environment: hyperscaler AI, enterprise AI readiness, campus modernization, and security-driven infrastructure refresh.

The order quality also had caveats. Management acknowledged some pull-ahead into Q3 and disclosed that price increases contributed 4 to 5 points of acceleration in ex-webscale product order growth. Ex-webscale order growth accelerated from 10% in Q2 to 19% in Q3, meaning approximately half of the 9-point acceleration was price-related. Management also said pipeline pull-forward from Q4 into Q3 did not differ meaningfully from the prior-year pattern and that the Q4 pipeline did not degrade during Q3. The practical conclusion is that order strength was real, but not purely volume-driven. Price, tariff/memory responses, and customer behavior ahead of supply constraints likely contributed.

Gross margin was the main negative in the results. Non-GAAP gross margin was 66.0%, down 260 bps YoY and 150 bps sequentially. Non-GAAP product gross margin was 64.3%, down 330 bps YoY and 210 bps sequentially. Management attributed product gross margin pressure primarily to negative mix and higher memory costs, partly offset by productivity improvements. Management later clarified that mix was the larger of the 2 factors, with memory also important. This matters because mix pressure is less transitory than spot component inflation if AI infrastructure and hardware remain the growth engines.

Operating leverage was strong. Non-GAAP operating margin was 34.2%, down only 30 bps YoY despite the 260 bps decline in total non-GAAP gross margin. Non-GAAP operating income was a record $5.4B. Non-GAAP operating expenses were $5.0B, flat sequentially and equal to 31.9% of revenue, down from 34.1% in the prior-year quarter. This indicates Cisco used opex discipline and revenue scale to offset hardware mix and memory pressure. The earnings beat therefore appears higher quality than the gross margin decline alone would suggest, because the company preserved operating margin while investing in AI, security, optics, and silicon.

Cash flow quality was mixed. Operating cash flow was $3.8B, down 7% YoY, due to continued investments to meet growing demand, especially in AI infrastructure. Cash, cash equivalents, and investments ended at $16.6B. Inventory increased to $4.7B from $2.8B a year ago and $3.9B in Q2 FY26. Inventory purchase commitments increased to $16.0B from $6.3B a year ago and $10.1B in Q2 FY26. Combined inventory and purchase commitments increased by approximately $6.7B over 90 days and approximately $11.6B YoY, consistent with management’s comments. This is strategically rational if AI orders convert as expected and supply remains tight, but it raises working capital, execution, and obsolescence risk.

Capital allocation remained shareholder-friendly. Cisco returned $2.9B to shareholders in Q3, including $1.7B in dividends and $1.3B in repurchases. The company repurchased 16M shares at an average price of $80.28 and had $9.6B remaining under the repurchase authorization. The dividend per share was $0.42. Capital return remains a core part of the equity story, but the incremental investment debate is now less about buybacks and more about whether AI infrastructure can re-rate Cisco’s growth profile without structurally diluting margins.

Recurring metrics were not as strong as headline revenue and orders. Total RPO was $43.5B, up 4%, decelerating from 5% growth in Q2 FY26 and 7% growth in Q3 FY25. Product RPO was $22.1B, up 6%, and Services RPO was $21.4B, up 2%. ARR was $31.2B, up 2%; Product ARR was $17.5B, up 4%; Services ARR was $13.8B, down 1%. Total subscription revenue was $7.8B, representing 49% of revenue, but was down modestly YoY and sequentially. Software revenue was $5.7B, up only 1%. These metrics show that the strongest growth is not coming from recurring software expansion. That is a valuation consideration because the market may reward the AI growth narrative but apply a lower multiple if growth is viewed as hardware-heavy and less recurring.

SEGMENT AND PRODUCT ANALYSIS

Networking is the core of the current investment case. Networking revenue of $8.8B grew 25% YoY, and networking product orders grew more than 50%. Management cited triple-digit growth in service provider routing and compute, double-digit growth in data center switching, campus switching, wireless, enterprise routing, and industrial IoT. This performance suggests Cisco is participating in multiple infrastructure cycles at once: hyperscaler AI networking, data center switching, campus modernization, wireless refresh, routing, and industrial edge. The strongest evidence of acceleration is that the networking portfolio has now posted 7 consecutive quarters of double-digit order growth.

Hyperscaler AI infrastructure was the most important product theme. Q3 hyperscaler AI infrastructure orders were $1.9B, compared with $600M in the prior-year period. YTD hyperscaler AI orders were $5.3B, already above the prior FY26 expectation of $5B. Management raised expected FY26 hyperscaler AI infrastructure orders to approximately $9B, implying a 4.5x increase versus FY25’s $2B total. Management also raised expected FY26 hyperscaler AI revenue to approximately $4B from $3B. The magnitude of this raise is the single most important change in the call because it provides an order-backed basis for revenue revisions and for a more durable AI networking narrative.

Silicon One is central to the hyperscaler thesis. Cisco disclosed 3 systems design wins in Q3: 2 Silicon One P200-powered systems for major scale-across use cases and 1 Silicon One G200-powered system for a scale-out use case. Management also disclosed that a third hyperscaler P200 scale-across design win occurred in early Q4. The Silicon One portfolio spans integrated access, services router, enterprise switch, scale-across data center, and scale-within data center use cases, with the presentation highlighting P200 at 51.2T and G300 at 102.4T. Management’s message was that differentiated silicon is now a prerequisite for relevance with hyperscalers. This is strategically important because it positions Cisco as more than a system integrator and gives the company more control over product roadmap, supply chain, and differentiation.

Acacia was the other major AI product driver. Acacia generated more than $1B in orders in Q3, up triple digits YoY, and management said the business is on track to grow more than 200% YoY in FY26. The presentation highlighted more than 750,000 coherent 400G port shipments and more than 40,000 coherent 800G port shipments. Acacia’s role is particularly important in scale-across AI data center architectures, where coherent optics are required to connect GPUs across multiple data centers. The presentation described scale-across as a 14x bandwidth multiplier relative to conventional WAN/DCI connectivity. This creates a credible mechanism for sustained optics demand as AI workloads become distributed across campuses and regions rather than confined to single clusters.

Enterprise data center switching was also strong. Orders grew more than 40% YoY and have grown double digits in 7 of the past 9 quarters. Nexus switch orders tagged for AI deployments were up almost 50% sequentially in Q3. This is an important detail because it supports the view that enterprise AI infrastructure is beginning to move from concept to procurement. It also helps address the risk that Cisco’s AI story is entirely hyperscaler-driven. The enterprise AI ramp remains earlier-stage than hyperscaler orders, but the order trajectory and pipeline suggest a potentially meaningful second leg.

Campus networking is in a major refresh cycle. Campus networking orders grew more than 25% YoY, with the next-generation portfolio ramping faster than prior product launches. Management cited modern Wi-Fi, multi-gig switching, AI-driven traffic growth, and end-of-support dynamics as demand drivers. The presentation highlighted recently launched Smart Switch orders growing triple digits sequentially in Q3, Wi-Fi 7 orders continuing to grow high double digits sequentially, and Wi-Fi 7 demand generating bundled demand for multi-gig switches. The presentation also disclosed that the pre-Catalyst 9K installed base is in the tens of billions of dollars and nearing end of support. This provides a concrete installed-base replacement mechanism, not merely a high-level AI traffic story.

Wireless was particularly strong. Cisco reported its highest-ever wireless orders, up more than 40% YoY. Wi-Fi 7 represented half of the wireless mix in Q3 and grew strong double digits sequentially. This supports a campus upgrade cycle driven by device density, AI-enabled applications, and higher throughput requirements. Wireless strength also matters because it can pull through switching, security, and management software. The durability of wireless demand will depend on whether Wi-Fi 7 adoption remains early and whether enterprise budgets continue prioritizing edge modernization.

Industrial IoT posted its strongest quarter ever and has now grown double digits for 8 consecutive quarters. Management cited manufacturing and utilities in the presentation and also linked future demand to onshoring of manufacturing, agentic AI, and physical AI. This is a smaller part of Cisco’s total revenue than core Networking, but it is strategically relevant because industrial networks are likely to require secure connectivity, edge compute, and deterministic performance as automation and physical AI adoption increase.

Security remains in transition. Security revenue was flat at $2.0B. Core security excluding Splunk posted double-digit order growth, and the new/refreshed portfolio grew double digits, including strong double-digit firewall order growth. More than 1,000 new customers purchased new security products in Q3, bringing total net new customers to approximately 5,000 since launch. However, prior-generation declines continued to offset growth, and Splunk’s shift from on-premise deals to cloud subscriptions created a near-term revenue drag. The business is improving but has not yet translated order momentum and product refresh into reported revenue acceleration.

Splunk is a key swing factor for FY27. Management said the expected acceleration in the shift to cloud subscriptions and away from on-premise deals continued in Q3 and is expected to continue in Q4. Cisco remains on track to exceed 1,000 new Splunk customer logos in FY26. Management said the cloud mix shifted another 2 to 3 points in Q3 versus Q2 and that FY27 depends on whether the mix shift stabilizes. If it stabilizes, revenue comparisons should improve as Cisco laps the transition. If it continues to accelerate, revenue growth could remain suppressed even if customer adoption is healthy.

Collaboration remains a drag. Collaboration revenue declined 1%, with Webex declines partially offset by device growth. The call did not present Collaboration as a strategic growth driver. The segment appears stable to slightly declining and is not central to the investment debate. Any upside from devices is likely insufficient to change the overall Cisco thesis without a broader Webex reacceleration that was not evident in the provided material.

Observability grew 3% to $269M, but the call focused far more on Splunk’s cloud transition than on standalone observability revenue. Observability remains strategically important because it intersects with security operations, AI monitoring, and Splunk, but the reported segment growth was modest. The current issue is not product relevance; it is the revenue recognition and mix transition from on-premise to cloud subscription.

Geographically, the Americas generated $9.6B of revenue, up approximately 14% YoY and 8% sequentially, but gross margin fell to 63.7% from 67.7% a year ago and 65.8% in Q2. EMEA generated $4.1B, up approximately 9% YoY but down sequentially from $4.4B, with gross margin of 71.3%. APJC generated $2.2B, up approximately 9% YoY and 11% sequentially, with gross margin of 66.1%. Product order growth was broad geographically, with EMEA orders up 39%, Americas up 35%, and APJC up 25%. The regional order breadth reduces macro concentration risk, though Americas margin pressure appears most pronounced.

May 13

(Bloomberg) -- Cisco boosted its adjusted earnings per share guidance for the full year; the guidance beat the average analyst estimate.

YEAR FORECAST

Sees adjusted EPS $4.27 to $4.29, saw $4.13 to $4.17, estimate $4.16 (Bloomberg Consensus)

Sees revenue $62.8 billion to $63 billion, saw $61.2 billion to $61.7 billion, estimate $61.64 billion

Still sees Adjusted Effective Tax Rate about 19%, estimate 19%

FOURTH QUARTER FORECAST

Sees revenue $16.7 billion to $16.9 billion, estimate $15.82 billion

Sees adjusted EPS $1.16 to $1.18, estimate $1.07

Sees adjusted gross margin 65.5% to 66.5%, estimate 66.6%

Sees adjusted operating margin 34% to 35%, estimate 34.4%

Sees Adjusted Effective Tax Rate about 19%, estimate 19%

THIRD QUARTER RESULTS

Adjusted EPS $1.06, estimate $1.04

Revenue $15.84 billion, estimate $15.57 billion

Product revenue $12.12 billion, estimate $11.79 billionNetworking revenue $8.82 billion, estimate $8.47 billion

Security revenue $2.01 billion, estimate $2 billion

Collaboration rev. $1.02 billion, estimate $1.06 billion

Observability revenue $269 million, estimate $276.8 million

Service revenue $3.72 billion, estimate $3.78 billion

Remaining performance obligations $43.46 billion, estimate $43.27 billion

Adjusted gross margin 66%, estimate 66.2%

Adjusted operating margin 34.2%, estimate 34%

COMMENTARY AND CONTEXT

Systems Announces Restructuring Plan

Orders From Hyperscalers to Date at $5.3B

Systems to Record Pretax Charges to Gaap Finl up to $1B

Systems Expects to Record ~$450M of Charges in 4Q

Systems: Remaining Charges to Be Recognized in Fy2027

Declares Qtrly Div of 42c/Shr, Meets Bdvd Projections

To Cut Less Than 4,000 Jobs, Fewer Than 5% Workers

Margin and EPS guidance includes the estimated impact of tariffs based on current trade policy

Data center switching orders grew greater than 40% year over year

Campus networking orders grew greater than 25% year over year

Cisco estimates that GAAP EPS will be $0.80 to $0.85 for the fourth quarter of fiscal 2026.

1

1

5

12,016

May 13

シスコシステムズ $CSCO

2026年度Q3決算を発表‼️

売上高・EPS・ガイダンス全て予想を上回る✨

AIインフラ需要が爆発的に拡大🚀

株価は時間外で13%上昇📈

🔸FY26 Q3業績

⭕️EPS: 1.06ドル(予想1.04ドル)

⭕️売上高: 158.4億ドル(予想155.6億ドル)

📈売上高成長率: 12% Y/Y

🔸FY26 Q4ガイダンス

⭕️EPS: 1.16〜1.18ドル(予想1.07ドル)

⭕️売上高: 167〜169億ドル(予想158.2億ドル)

🔸FY26通期ガイダンス

⭕️EPS: 4.27〜4.29ドル(予想4.16ドル)

⭕️売上高: 628〜630億ドル(予想616.0億ドル)

※ガイダンスは現行の関税政策の影響を織り込み済み

🔸製品カテゴリ別売上高(Q3)

📈ネットワーキング: 88.2億ドル( 25% Y/Y)

📊セキュリティ: 20.1億ドル(0% Y/Y)

📉コラボレーション: 10.2億ドル(-1% Y/Y)

📈オブザーバビリティ: 2.7億ドル( 3% Y/Y)

🔸地域別売上高(Q3)

📈アメリカズ: 95.7億ドル( 14% Y/Y)

📈EMEA: 40.5億ドル( 9% Y/Y)

📈APJC: 22.2億ドル( 9% Y/Y)

🔸受注動向(AI・ネットワーク需要が加速)

📈総製品受注: 35% Y/Y(ハイパースケーラー除く 19%)

📈ネットワーキング製品受注: 50%超 Y/Y

📈キャンパスネットワーキング受注: 25%超 Y/Y(次世代ポートフォリオが過去製品より速いペースで立ち上がり中)

📈データセンタースイッチング受注: 40%超 Y/Y

🔸AIインフラ需要(ハイパースケーラー向け)

📈年初来受注額: 53億ドル

📈FY26通期AI受注見通し: 90億ドルに上方修正(従来予想50億ドルから)

📈FY26通期AI売上高見通し: 40億ドルに上方修正(従来予想30億ドルから)

🔸未履行残高・繰延収益

📈残存履行義務(RPO): 434.6億ドル( 4% Y/Y)

📈長期製品RPO: 117億ドル( 6% Y/Y)

📈繰延収益合計: 286億ドル( 2% Y/Y)

🔸株主還元

✔️Q3の株主還元総額: 29.1億ドル(自社株買い+配当)

✔️自社株買い: 約1,600万株を平均80.28ドルで12.5億ドル実施

✔️四半期配当: 1株あたり0.42ドル(支払日: 2026年7月22日)

✔️自社株買い残枠: 96億ドル(期限なし)

🔸リストラクチャリング計画

✔️2026年5月13日、シリコン・光学・セキュリティ・AIへの重点投資に向けた構造改革計画を発表

✔️税引前費用: 最大10億ドル(退職金・一時費用等)

✔️FY26 Q4に約4.5億ドル、残額はFY27に計上予定

🔸会社概要

Cisco(NASDAQ: CSCO)は、組織のネットワーク接続とセキュリティ保護の方法を革新する世界的テクノロジーリーダーです。

40年以上にわたり世界を安全につなぎ続け、AI時代においても業界をリードするAI搭載ソリューションと

サービスを通じて、顧客・パートナー・コミュニティのイノベーション創出・生産性向上・デジタルレジリエンス強化を支援しています。

2

10

86

12,700

May 13

$CSCO | 𝐂𝐢𝐬𝐜𝐨 𝐐𝟑 𝐅𝐘𝟐𝟎𝟐𝟔 𝐄𝐚𝐫𝐧𝐢𝐧𝐠𝐬 𝐑𝐞𝐩𝐨𝐫𝐭: Revenue: $15.8B (↑ 12% YoY) | GAAP EPS: $0.85 | Adjusted EPS: $1.06

👉 𝐁𝐮𝐬𝐢𝐧𝐞𝐬𝐬 𝐇𝐢𝐠𝐡𝐥𝐢𝐠𝐡𝐬:

➤ 𝐓𝐨𝐭𝐚𝐥 𝐩𝐫𝐨𝐝𝐮𝐜𝐭 𝐨𝐫𝐝𝐞𝐫𝐬 increased 𝟑𝟓% year over year.

➤ 𝐍𝐞𝐭𝐰𝐨𝐫𝐤𝐢𝐧𝐠 𝐩𝐫𝐨𝐝𝐮𝐜𝐭 𝐨𝐫𝐝𝐞𝐫𝐬 accelerated more than 𝟓𝟎% year over year.

➤ 𝐀𝐈 𝐢𝐧𝐟𝐫𝐚𝐬𝐭𝐫𝐮𝐜𝐭𝐮𝐫𝐞 orders reached 𝐚𝐛𝐨𝐯𝐞 $𝟓.𝟑𝐁 year-to-date.

➤ Cisco raised expected FY26 𝐀𝐈 𝐨𝐫𝐝𝐞𝐫𝐬 to $𝟗𝐁 from $𝟓𝐁.

➤ Cisco increased expected FY26 𝐀𝐈 𝐫𝐞𝐯𝐞𝐧𝐮𝐞 to $𝟒𝐁 from $𝟑𝐁.

➤ 𝐂𝐚𝐦𝐩𝐮𝐬 𝐧𝐞𝐭𝐰𝐨𝐫𝐤𝐢𝐧𝐠 orders grew more than 𝟐𝟓% year over year.

➤ 𝐃𝐚𝐭𝐚 𝐜𝐞𝐧𝐭𝐞𝐫 𝐬𝐰𝐢𝐭𝐜𝐡𝐢𝐧𝐠 orders increased more than 𝟒𝟎% year over year.

➤ Geographic revenue growth: 𝐀𝐦𝐞𝐫𝐢𝐜𝐚𝐬 ↑𝟏𝟒%, 𝐄𝐌𝐄𝐀 ↑𝟗%, 𝐀𝐏𝐉𝐂 ↑𝟗%.

➤ Cisco declared a quarterly 𝐝𝐢𝐯𝐢𝐝𝐞𝐧𝐝 of $𝟎.𝟒𝟐 per share.

👉 𝐂𝐄𝐎 𝐒𝐭𝐚𝐭𝐞𝐦𝐞𝐧𝐭:

“Cisco delivered record quarterly revenue in Q3 and we saw very strong, broad-based demand for our products, demonstrating the relevance of our technology for connecting and securing AI,” said Chuck Robbins, chair and CEO of Cisco.

👉 𝐂𝐅𝐎 𝐒𝐭𝐚𝐭𝐞𝐦𝐞𝐧𝐭:

“In Q3, we once again delivered double-digit growth on both the top and bottom lines which exceeded the high end of our guidance, coupled with record non-GAAP operating income,” said Mark Patterson, CFO of Cisco.

3

10

2,965

Well, this is London 🇬🇧

Au British museum, enfin voir le célébrissime vase de Portland (15 avJC-25 apJC), camées en verre.

Et autres merveilles.

1

2

15

582

Apr 14

AWS の APJC DevRel の Japan DA(Developer Advocate)のポジションがオープンになりました! 日本のデベロッパーに向けてAWSの認知度・選好度向上のための活動をします。上司はシドニー在住、日本の同僚は私ふくめて2人いますが、ほかはAPJCリージョン内にいる社員です!

amazon.jobs/jp/jobs/10389318…

21

32

3,296

Le bout de tissu on peut remonter jusqu’à 435 apJC, c’est un négatif et l’impression est impossible à refaire même avec notre technologie du 21eme siècle. Le tissus fait 3mm d’épaisseur et si on se présente juste devant on voit rien

1

19

534

Mar 30

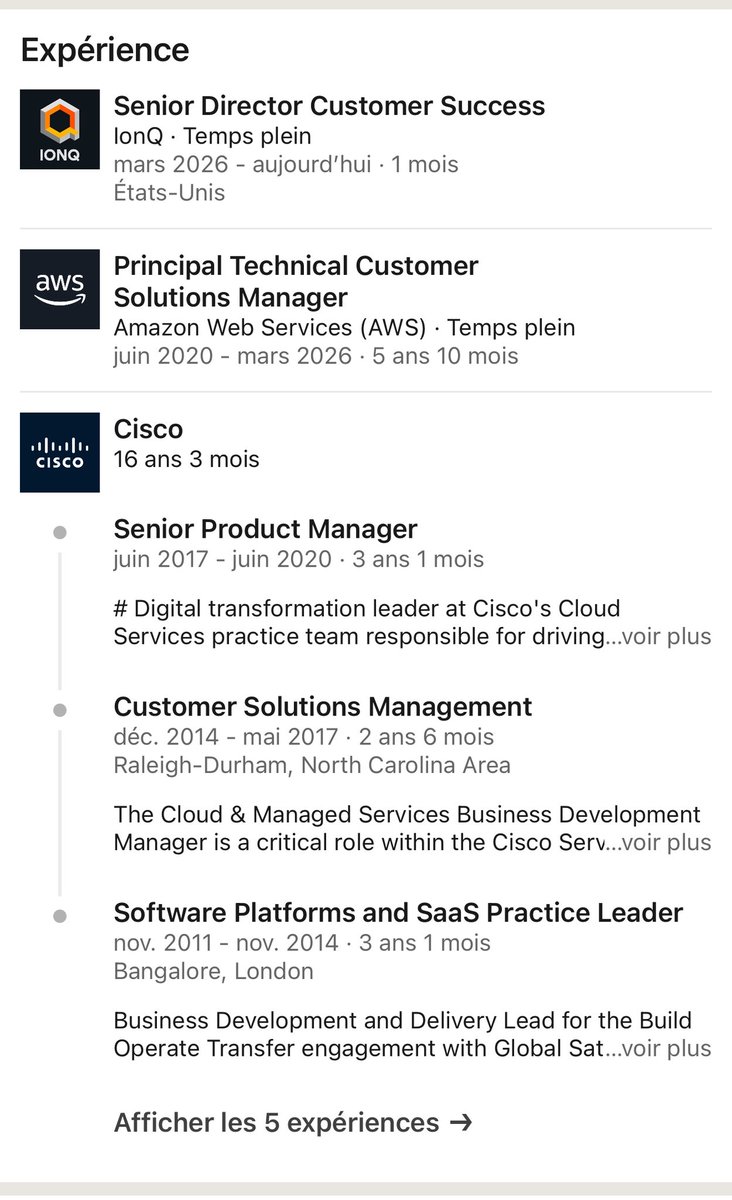

$IonQ Ves Sathya just joined @IonQ_Inc as Senior Director, Customer Success. Based in Cary, North Carolina.

16 years at Cisco. Started as Solutions Engineer in Bangalore, rose to Senior Product Manager running Cloud & Managed Services. Along the way: Global Service

Delivery across APJC (South Korea, Malaysia, Indonesia), SaaS Practice Leader managing $300M multi-year deals in Bangalore and London, $24M in wins FY16, $67M FY17.

Then nearly 6 years at AWS as Principal Technical Customer Solutions Manager.

That’s 22 years of enterprise cloud and managed services delivery before walking into a quantum company.

As we covered with Dr. Daniela Becker (AWS Braket → Director of Product Management), that’s now two senior AWS hires in the same quarter. Becker builds the product. Sathya makes sure customers actually succeed with it.

Those two roles working in parallel is how you go from “we sell quantum access” to “we retain and expand enterprise accounts.”

The title matters too. “Customer Success” is not “Sales.”

It’s the post-sale function onboarding, adoption, renewal, expansion. IonQ is hiring for a stage where customers already exist and need to be managed at scale.

$IONQ #IonQ #QuantumComputing

6

37

2,472