Kioxia $285A

As of June 15, 2026, memory stock performance shows Kioxia up approximately 744% YTD, SK Hynix up about 230%, and Samsung Electronics up about 183%, with Kioxia achieving a rise of about 3.2 times that of SK Hynix and about 4.1 times that of Samsung Electronics.

Amid the first wave of AI memory demand centered on HBM/DRAM from 2024–2025 and the second wave centered on NAND/Enterprise SSD from 2025–2026 onward, Samsung and SK Hynix have focused their capital expenditures on HBM, relatively suppressing and postponing the development and ramp-up of leading-edge NAND, whereas Kioxia, as a pure-play NAND company, is positioned to fully capitalize on the second wave. Structural advantages such as cost competitiveness from its joint venture with SanDisk/Western Digital, advancements in BiCS technology, and differentiation through high-performance NAND tailored for AI inference are believed to be the key factors behind the performance gap.

Kioxia has nearly sold out its NAND/SSD supply for the full year of 2026.

In its May fiscal results, it updated to record-high profits, with a bullish forecast for the June quarter of operating income around 1.3 trillion yen.

At the Investor Day on June 2, it upwardly revised its flash demand CAGR from 20% to 22%, reflecting AI inference demand.

32

マルンボーリ retweeted

キオクシアの最新動画ポヨ

3次元フラッシュメモリ「BiCS FLASH™」の大容量化技術

youtube.com/watch?v=0E9kup9u…

8

72

6,548

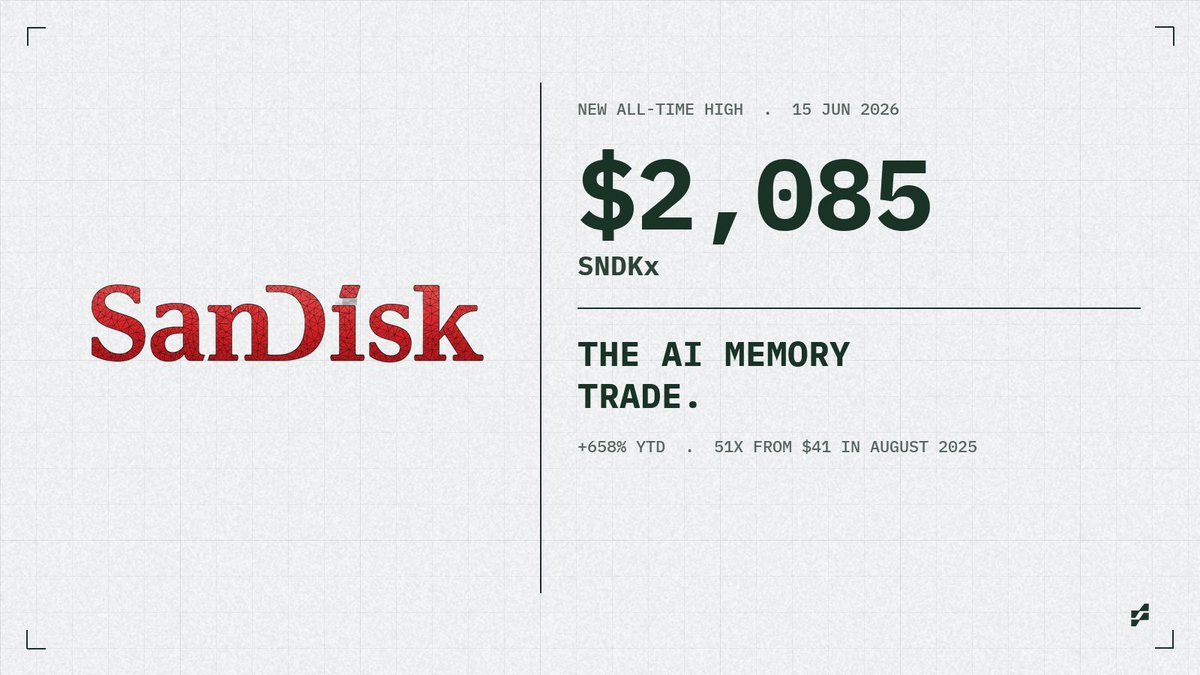

SanDisk just printed a new all time high at $2,085.

YTD: 658%. From $41 last August to $2,085 today.

A 51x in 10 months.

The memory thesis the market kept underpricing:

Why memory is the AI bottleneck nobody priced in:

• Every AI cluster needs two memory layers: HBM (next to the GPU) and NAND (storage for training data and inference cache)

• NAND is now structurally undersupplied. Hyperscaler buildouts pulled forward years of demand in a quarter

• Memory pricing was deflationary for 30 years. It just turned structurally inflationary

Why SNDK specifically:

• Spun off from Western Digital in early 2025 as the pure play NAND leader

• Largest BiCS architecture player. Highest bit density per wafer in the industry

• Q3 FY26 revenue grew 251% YoY

• Beat guidance by $1.15B in a single quarter

The supply chain:

• NVDA ships the GPUs

• MRVL connects them with silicon photonics

• SNDK and MU feed them memory

• DELL and SMCI rack them

• CEG powers them

Every dollar of AI capex flows through these names.

$1T of hyperscaler AI capex committed through 2027.

Memory was the part of the chain the market underpriced.

SNDK on Spreads. NVDA, MRVL, MU, DELL, SMCI, CEG too.

1

1

136

5h

三星是规模之王,垂直整合最深,从晶圆、控制器到固态盘一手包办,出货量长期第一。三星的优势是体量和全栈,软肋是大公司在路线上的犹疑,以及把注意力分散在内存、HBM、逻辑代工等多条战线。

SK 海力士借收购英特尔闪存业务而来的 Solidigm,在生成式 AI 急需的大容量四比特企业级盘上占住了身位,做出过 122TB 的产品;它与闪迪联手主导下一代HBF。SK 海力士的优势,是在HBM上练就的堆叠与键合功力可以直接迁移到 NAND,软肋则是 Solidigm 的单元技术代际偏老、整合仍需时间。

铠侠是这六家里最被低估、也最值得单独说的一家。它的强大,首先是血统:NAND 这个东西,就是它的前身东芝在 1987 年发明并商业化的,世界第一颗多比特 NAND 也出自它 2001 年之手——这个产业的底层专利和工艺传统,有相当一部分姓“东芝”。但血统只是入场券,铠侠真正的护城河在架构。它主推的 BiCS,是电荷俘获型三维 NAND 的开创性结构之一;而它最新的杀手锏,是被称为 CBA、即“逻辑电路直接键合于阵列”的工艺——把存储单元阵列和外围控制电路分成两片晶圆,各自用最优工艺独立制造,再精密键合在一起。这一招的厉害之处,要害不在层数,而在密度效率:铠侠的 332 层,明显少于三星的 430 层、SK 海力士的 375 层,单位面积比特密度却能做到接近每平方毫米 5GB 的业界最高水平,读写速度还比对手快两到三成。

真正决定竞争力的,是每平方毫米能放下多少比特、每个比特的制造成本是多少。铠侠用更矮的堆叠做出更高的密度,意味着更低的刻蚀难度、更好的良率、更优的成本曲线,是工程上的以巧胜力。把外围电路从阵列下方挪到独立晶圆,既释放了存储面积,又让两片晶圆可以各自优化,是 NAND 摆脱平面思维之后最聪明的一步。铠侠的第二重优势是纯粹:三星、SK 海力士、美光都同时背着内存与高带宽内存的战线,资源和注意力天然分散,而铠侠几乎是唯一一家把全部身家压在 NAND 上的玩家,战略最聚焦。第三重优势是它与闪迪的合资联盟——两家共用四日市和北上两座工厂、共担巨额资本开支,2026 年合资体的投资额同比提高 41% 到 45 亿美元,合并份额逼近 27%,足以与三星正面相望。第四,它绑定了最稀缺的客户:与英伟达合作开发可直接挂在 GPU 旁、比当前型号快近百倍的固态盘,意在为 AI 服务器补充高带宽内存之外的容量,目标 2027 年落地。

其余三家各有定位。闪迪是铠侠合资联盟的另一半,技术与产能共享,一个轻资产却高度依赖合资体的角色。美光是美国唯一的存储独苗,第九代做到 276 层,在数据中心四比特盘上份额稳步上行,软肋是体量偏小、资本开支压力大。长江存储则是被低估的变量:它的 Xtacking 把外围电路晶圆与阵列晶圆键合的思路,在商业化上比许多对手都早、都激进,可以说整个行业向晶圆键合的收敛,长江是早期推手;300 层产品在路上,工艺并不落后,真正的天花板来自出口管制对其先进设备和海外市场的封锁,而非技术本身。

讲完物理来泼冷水。计算机的内存层级,是一条以延迟排序的金字塔。DRAM 坐在 CPU 和 GPU 的关键路径上:处理器每一次缓存未命中,都得停下来等 DRAM 把数据送来,DRAM 快一纳秒,整台机器就快一分。正因为 DRAM 的速度直接决定算力,它的性能就是可以标价的——带宽、延迟、容量都能卖出溢价。HBM就是 DRAM 这条逻辑走到极致的产物:把多片 DRAM 用硅通孔垂直堆叠、与加速器深度集成,做成定制化、性能差异化、按近乎市盈率逻辑定价的产品,跳出了商品的命。

NAND 则坐在关键路径之外。数据在被计算之前,总要先从 NAND 搬进 DRAM;NAND 本身的读延迟以微秒计、写延迟以毫秒计,比 DRAM 慢上千倍。这“慢”,恰恰是那道非易失势垒的必然代价——你不可能既要电子十年不逃逸、又要电子瞬间进出。既然 NAND 注定慢、又不在算力的关键路径上,那么把它做得更快,对系统的边际收益就迅速递减。应用真正在乎的,只剩两件事:每比特多便宜、单盘多大容量。当性能不再是可标价的差异,竞争就只能坍缩到成本一个维度——这就是同质化商品的定义。NAND 的商品属性,不是哪家公司经营不善,而是它在内存层级里的位置决定的,而这个位置,又是它的物理决定的。

那么 NAND 有没有可能像 DRAM 靠高带宽内存翻身那样,找到自己的差异化出口?HBF就是这个尝试,也是理解 NAND 能否摆脱商品命的关键样本。它由闪迪提出、联合 SK 海力士推动标准化,三星也在跟进,做法是把 16 颗 NAND 裸片加一颗基底裸片堆成一摞,外形、功耗、堆高都对齐高带宽内存第四代,单摞容量做到 512GB,是同等高带宽内存的 8 到 16 倍,读带宽高达每秒 1.6TB,比顶级 PCIe 5.0 固态盘快约 50 倍,目标 2026 下半年出样、2027 年初进入 AI 推理设备。

285

11h

キオクシア

2026年6月15日時点のメモリ株パフォーマンスは、キオクシアがYTDで約 744%、SKハイニックスが約 230%、サムスン電子が約 183%となっており、キオクシアはSKハイニックスの約3.2倍、サムスン電子の約4.1倍の上昇率となっている。

AIメモリ需要の第1波は2024〜2025年中心のHBM/DRAM、第2波は2025〜2026年以降のNAND/Enterprise SSDが中心となる中で、サムスンとSKハイニックスはHBMへの設備投資に集中し、先端NANDの開発・増産を相対的に抑制・先送りした一方、キオクシアはNAND専業であるため第2波をフルに享受でき、SanDisk/Western Digitalとの合弁によるコスト競争力、BiCS技術の進化、AI推論向け高性能NANDでの差別化といった構造的優位性がパフォーマンス差の要因となっていると思われる。

キオクシアは2026年通年のNAND/SSDがほぼ完売状態。

5月決算で過去最高益更新、6月期も営業利益1.3兆円規模の強気予想。

6月2日のInvestor Dayでフラッシュ需要CAGRを20%→22%に上方修正とAI推論需要を反映している。

Jun 2

キオクシア IRデイ資料

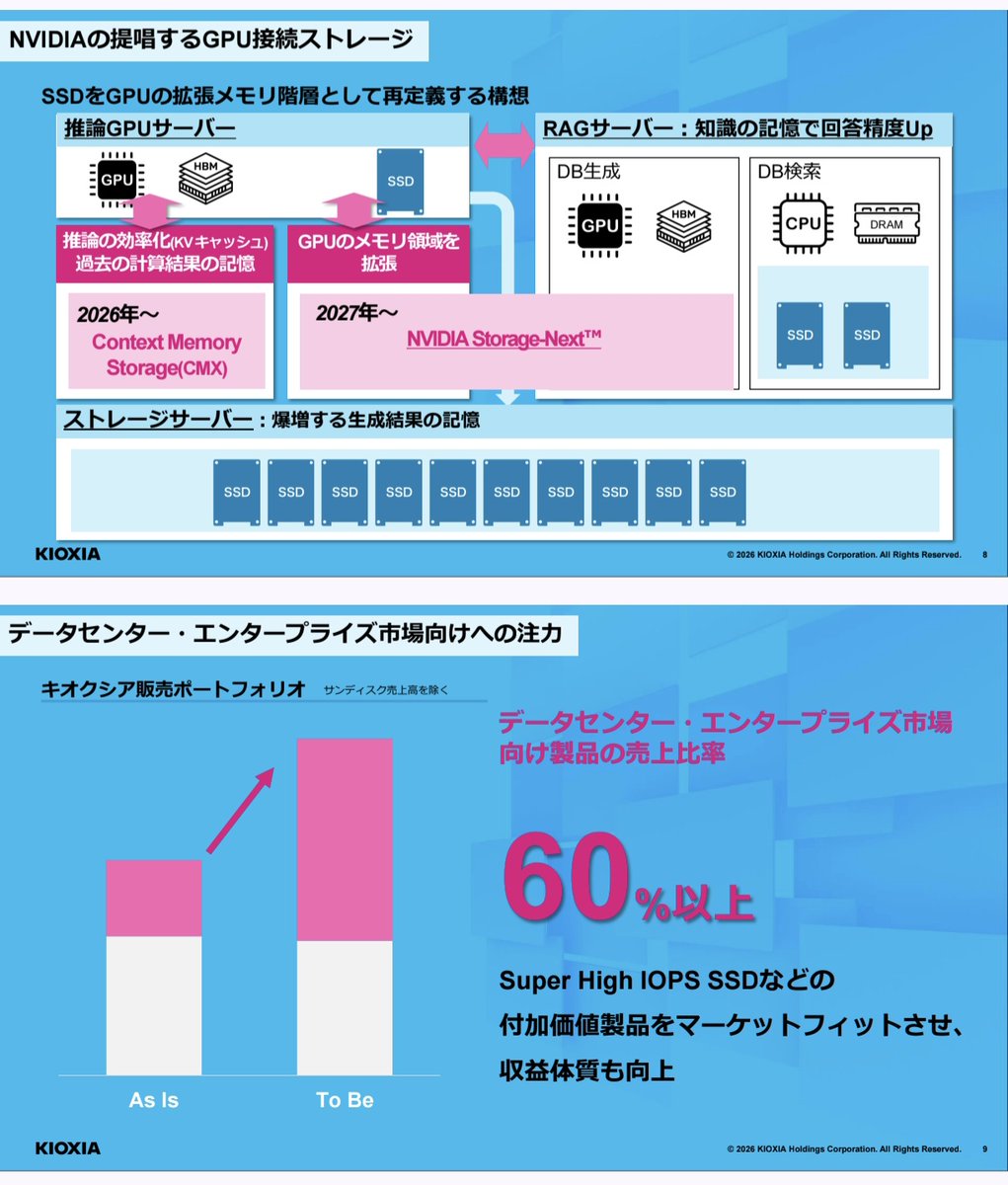

一番良い点は、AI推論でSSDの役割をかなり具体化しているところです。資料では、RAGサーバー、大規模ベクタDB、KVキャッシュ、Context Memory Storage、NVIDIA Storage-Nextまで出しており、SSDを単なる保存装置ではなく、GPUメモリ不足を補うメモリ階層として説明しています。ここはかなり重要でSSD側でRAG、DB生成・検索、CMX、Storage-Nextを正面から取りにいく説明をしています。

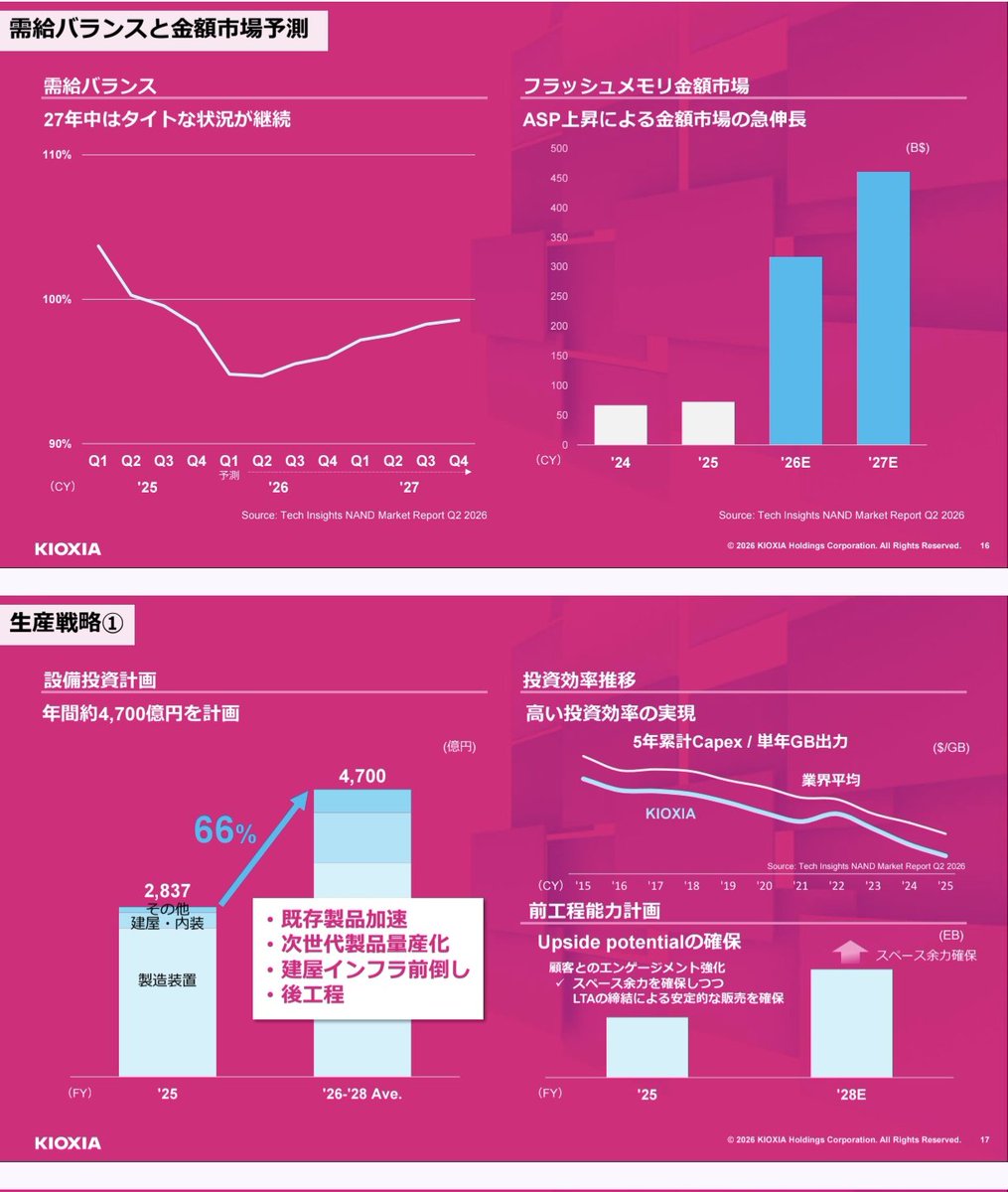

2つ目によい点は、データセンターSSD向けNANDの成長数字が強いことです。資料では、データセンター向けフラッシュメモリ市場について、2025年295EB、2026年909EB、2028年1,807EBという見通しを出し、推論向けはCAGR86%としています。PC・スマホ向けは横ばいまたは微減という扱いなので、成長の主役は完全にデータセンターと推論AIです。

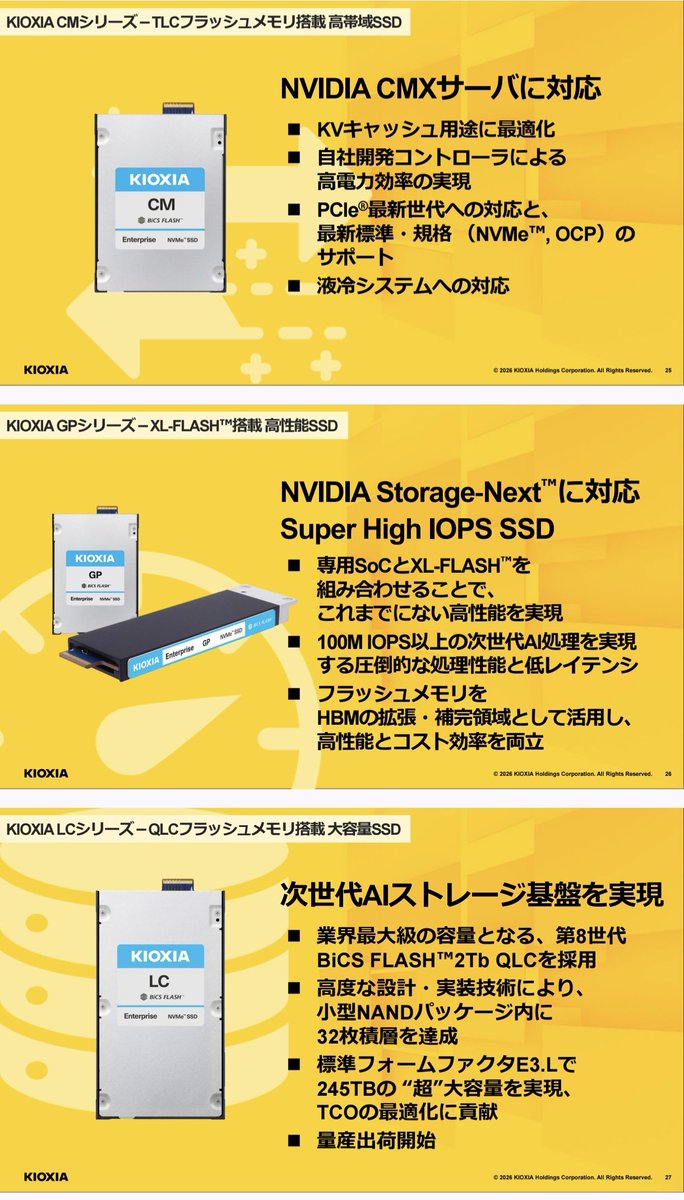

3つ目は、製品ラインナップがかなり分かりやすいことです。CMシリーズはNVIDIA CMXサーバー対応、KVキャッシュ用途、高電力効率、PCIe最新世代、NVMe・OCP、液冷対応。GPシリーズはXL-FLASH搭載で100M IOPS以上、HBMの拡張・補完領域として使う説明。LCシリーズはQLC大容量で、E3.Lフォームファクタ245TB、量産出荷開始。ここまで用途別に整理されているなら、AIサーバーが増えたらSSDも増えることがわかります。

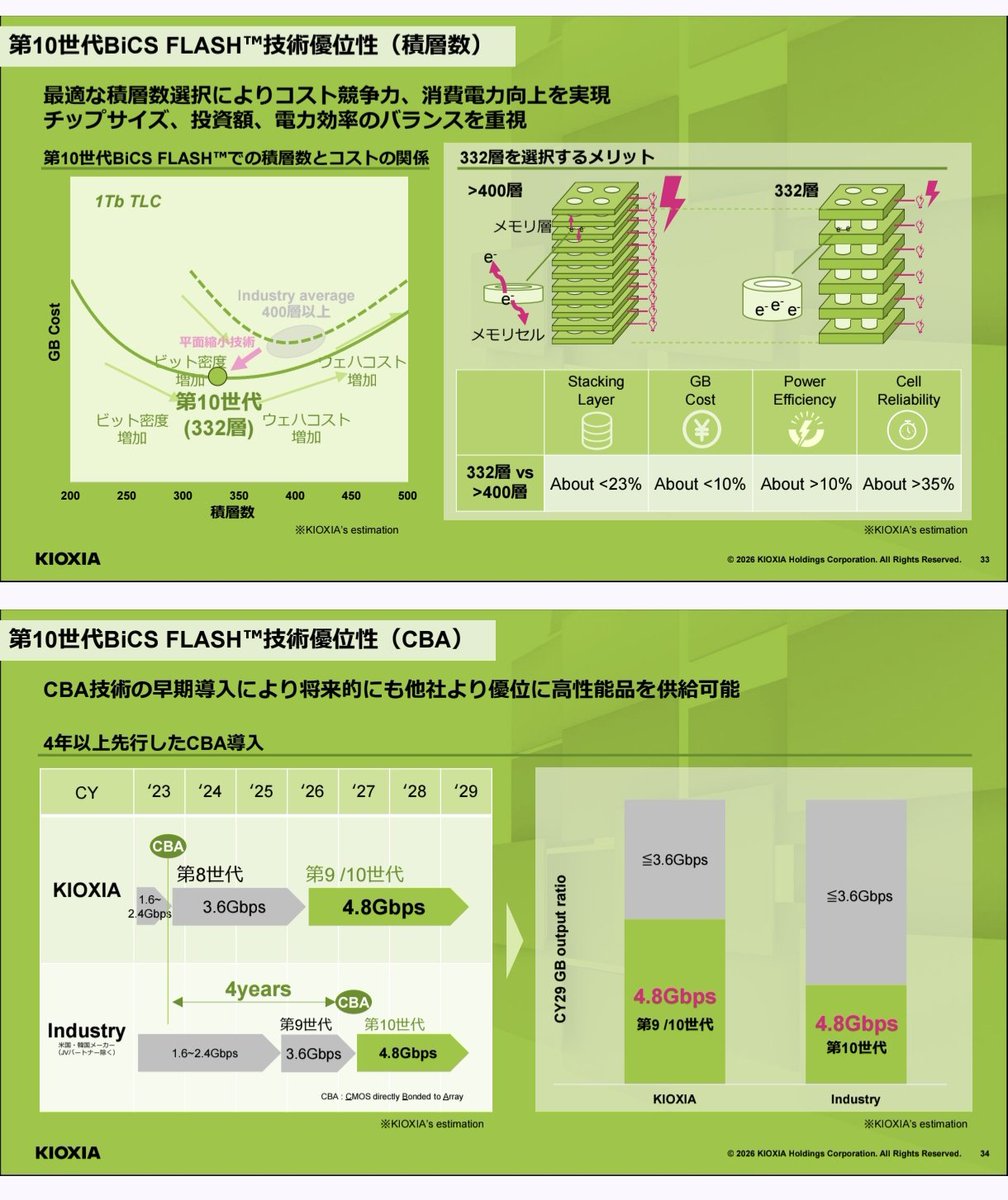

4つ目は、第10世代BiCS FLASHの説明が思ったより強いことです。第10世代1Tb TLCは2026年夏にサンプル提供開始予定で、第8世代比でBit Density 59%、Interface Speed 33%、Read Throughputが15%超改善、Write Throughputが30%超改善、Read Power Efficiencyが40%超改善、Write Power Efficiencyが30%超改善。さらにPCIe Gen.6対応の高帯域TLC-SSDにつなげる説明になっています。これはAI推論SSDの性能・電力効率に直結します。

5つ目は、332層を選んだ理由を400層超より少ないから遅れているではなく、コスト、電力効率、信頼性、投資額のバランスとして説明している点です。資料では、第10世代BiCS FLASHで332層を選ぶメリットとして、最適な積層数選択によりコスト競争力と消費電力向上を実現するとしています。これは、単純な積層数競争ではなく、AI向けSSDで必要な電力効率とコストを取りにいく説明です。

6つ目は、CBA技術の先行を強く出しているところです。資料では、CBAを4年以上先行して導入し、将来的にも他社より優位に高性能品を供給可能としています。米国・韓国メーカーとの差を明示しているので、ここはかなり投資家向けに強めたメッセージです。

7つ目は、売上構成を変える意思がはっきりしていることです。データセンター向け売上比率をFY28までに60%以上にする方針を出しています。さらに、複数年LTAで安定収益を作る、Super High IOPS SSDなど高付加価値品を出す、大容量QLC・高性能4.8Gbps品を拡大する、としています。これはメモリ市況で上下する会社からAIデータセンター向け高付加価値の会社に見せたいという意思を感じる。

まだあるけどとりあえずこれくらいで。

2

7

49

13,213

Check this out, why I own L.A. Conf is because I am correlative with barrel bics. It was a French scientist who setup the lighter, whenever there's one near me I find it but I reproduced them to clear out the timers. I probably hit a fault line and train hopped to the middle of nowhere, found a huge patch of a former growers' crops, a barrel bic which led me there (that's where I found it most likely) that's the only answer to that logic puzzle. Unconscious from nuclear timers. Tagging up the trainline with alien crop circles. That was me. 2021.

1

24

1⃣ weel until #EBN2026 co-organised with @TnSviluppo!

Join us for the first parallel session exploring how EU|BICs can evolve in response to today’s social, environmental, economic and technological challenges.

🔗 Last week to register: ebncongress.eu/

25

Hapo kwwa lighter ..bics zangu ziusonga na hawa wasichana wenyu mbaya 😂

Jun 14

Rules za chain>>>

1. No wetting the blunt

2. Blunt moja 3 people max

3. Weed inaenda left

4. Kama uko msick usijoin chain

5. Blunt sio microphone

6. Weka ash kwa tray before passing

7. Hakuna kuangusha blunt

8. Kohoa na class

9. Hakuna kuiba lighter

10. The roller,the honours.

2

3

5

131