RT @prettyboynuts: my hb lost a bet wit me but he ain’t have the money to pay up so instead i told him let me get some of his girl pussy, h…

285

Her_SoleS retweeted

Just imagine them wrapped around your 🍆!

Bet it would make you and your 💳 so weak…😈

11

82

881

8,185

AS10 ep 2 is the best, mistress and Lydia are just the bet

But I bet she can tell where you can get the best possum in the state.

世界杯开云体育世界杯买球app平台🧌凯时娱乐 👝2026美加墨世界杯赌球app下注投注世界杯预测比分💀足球即时比分🗃世界杯直播红单推荐💺抢庄牌九💧乐鱼体育🚍bet在线🍅可靠谱世界杯竞猜外围博彩平台网址🏖时时彩🏘世界杯赛程滚球百家乐福利领取☞@kyty888888

Love when I have a best bet that also can be great for account health. Double duty

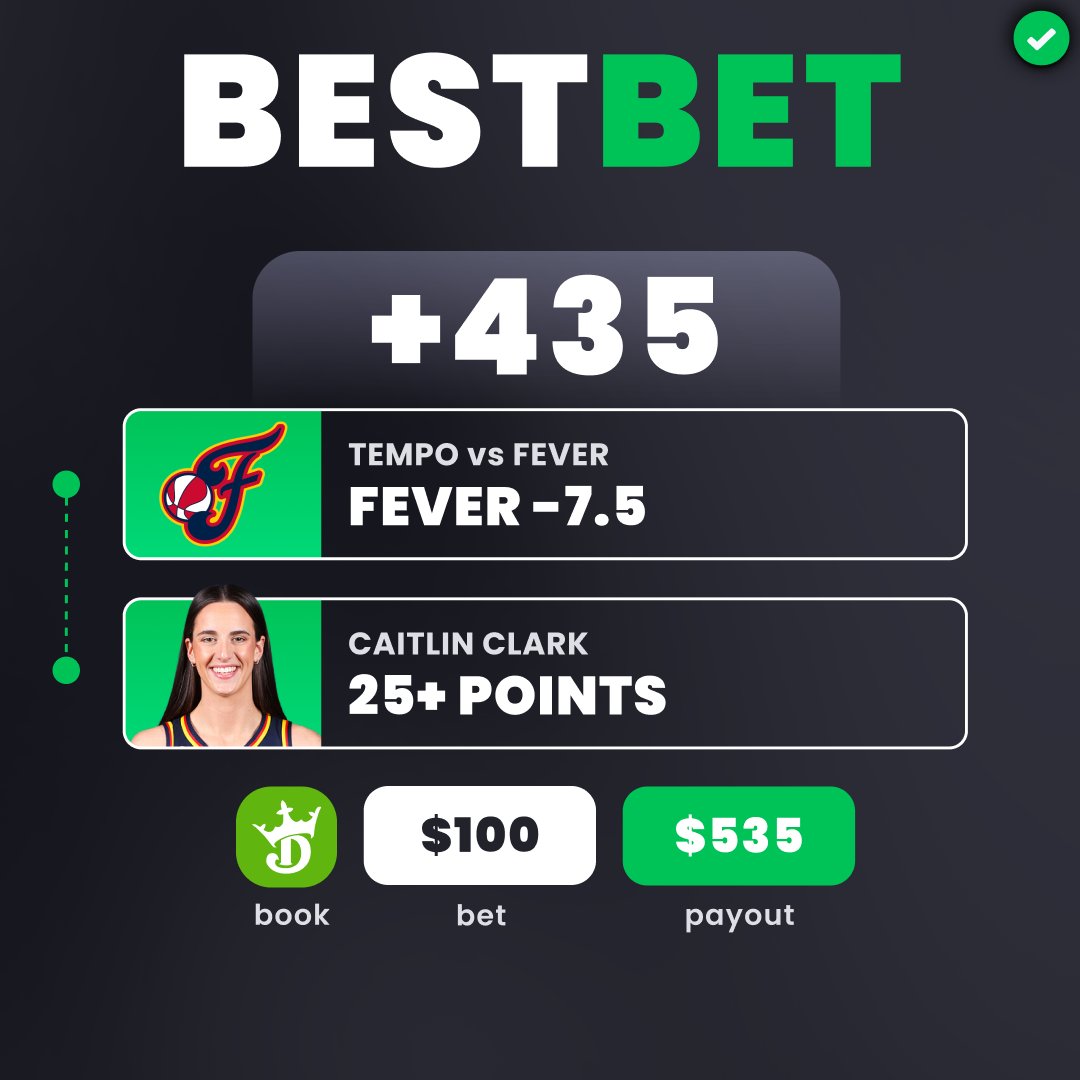

🔥TEMPO vs FEVER SGP

🏀Indiana Fever -7.5

🏀Caitlin Clark 25 Points

👇Add directly to your betslip

bit.ly/WNBA061626

🗣️"This shapes up as a really good game for Caitlin, and the Fever are inherently good when Caitlin is playing well. It's pretty simple: the Fever are 5-1 this season when she scores more than 20 points." -@TurveyBets

Rosário Beirão 🇵🇹🇪🇺🇺🇦🇪🇺🇬🇪 retweeted

What future do you envision for Medvedev, Rogozin, Zakharova, and the rest of Putin’s posse after the war?

I bet you’ll absolutely LOVE what “Caesar” (Maximilian Andronnikov), spokesperson for the Freedom of Russia Legion, has in mind for them.

😁😁😁

15

58

193

4,217

It's a musty tether. I bet he was harassing a Foundational Black American. He got blindsided because he beat him to HR with a complaint.

Lewis Valentine retweeted

15h

POV: you bet on the world cup thinking "no more draws.. this next game, someones gotta win for sure"

102

47

330

12,298

ʜᴀʀᴜʜɪ ᴏғ 🏚️ ᴛᴡᴛ retweeted

Bet Jeff the killer can't even be stealthy because everyone can smell him kilometers away

2

12

33

527

𝗦𝗧𝗥𝟴 𝗚𝗔𝗬 𝗕𝗢𝗬𝗭 | 333𝙆 retweeted

Name something better than gay sex, Bet you can't!!!

@DimitrySimonit took every drop I had to offer

20

373

942

46,331

Vicky McGonigle retweeted

What a racket. Bet there are hundreds of them !like the French guy in trois riviera who controls rare mineral rights with no band but an heritary chief

1

1

44

22s

Price is the king of kings in the market, and there is absolutely no room for doubt about that. If one refuses to accept this, then there is no reason to trade at all. I think that is self-evident. Risk management is the trader’s responsibility, and becoming attached to a position is, in my view, an incredibly foolish thing for a trader to do.

I always aim for very large profits, but the thing I am even more obsessed with is my win rate. Rather than taking countless trades over the course of a year, I place top priority on maintaining a high win rate through a smaller number of trades.

Recently, quite a lot of people have asked me, “Why are you still holding your long-dated call option position in crude oil?”

I will answer honestly. In addition to crude oil, I have already generated quite substantial profits through some positions I disclosed transparently here, which have all since been closed out, as well as through other trades I did not disclose. After all, my main profession is in FICC.

I have gone long and short bonds several times over already, and I am currently long. I have also generated fairly satisfying profits in FX. The yen has been sluggish, but I still believe it will move close to my target. On top of that, before and after the war, I alternated between long and short positions in crude oil and earned satisfying profits there as well. On a year-to-date basis, my profits have exceeded those of 2025.

I am not saying this to boast. I am saying it because I want to be honest.

One trading method I use frequently is to exploit asymmetry. People call this a contrarian strategy, but in truth I am not attached to that term itself. What I focus on instead is how far price has deviated from the fair value I have personally set, and when I see that asymmetry normalizing, I add fairly large size to the position. If you look back at my past writings, you will probably find similar trading ideas. This strategy is a way of driving up the win rate dramatically in a short period by putting on very large lots. Has this strategy always worked? Absolutely not. My goal is to get 8 out of 10 attempts right. An 80% win rate. That is why my loss cuts are extremely tight. I only use this strategy when asymmetry is at its peak, with the intention of realizing it within one to two weeks at most.

The second method is to put on more long-term positions. Paradoxically, this means placing the largest risk factor into the portfolio. As I kept emphasizing in my posts on X right before the war in February, I have consistently held the view that hedges are best put on when they are cheapest. At the time, I placed an 80–85 bull call spread. This is less a strategy than a kind of insurance payout against things that the market is overlooking or pricing far too cheaply, but which, if realized, could become a critical market threshold. From a business perspective, it serves as a hedge. Personally, this is my biggest bet.

So where is crude oil positioned right now? It is in the second category. And with this second type of positioning, I place considerable constraints on myself. First, I do not scale up the initial position too aggressively. Second, my research must be airtight. Third, unless the points I believe the market is overlooking are not merely partially damaged but completely invalidated, I do not close the position.

At the moment, I have violated the first principle. My conviction was too strong. That is my mistake. I will not attempt to make up for this mistake through further trading. I can simply trim the position. Today, I am closing one-third of my Z26 position. But I plan to maintain the remaining lots.

Quite a lot of people have given me advice. I am always grateful to them.

Let me share one personal piece of research. It may be an incredibly foolish thing, but in my view, the market right now is pricing too many things at once in only the “right” direction. Math and physics have not completely broken down, yet it seems as though people are thinking and acting as if they are releasing all the stress that had built up until now. Personally, I believe this is extremely dangerous pricing. The one thing I remain fixated on is this: even if wars begin because of the personal motives of actors or the security motives of groups, the way they are ultimately resolved must move toward an institutional and binding process.

I am highly skeptical that the United States will simply hand out money unilaterally, while placing no meaningful restrictions on Iran’s proxy forces or ballistic missiles, and that Iran will then adopt a constructive attitude and comply with the United States on the nuclear issue.

Also, after spending several days researching this, I feel I have at least been able to understand, in a very rough framework, what the term “management mechanism” is supposed to mean, on what layers it is meant to operate, and in what manner. And I do not believe this process will be smooth at all. This is not merely a U.S.-Iran problem. I believe there is no ideal point at which the commitments of the various actors, and even their asymmetrical domestic interests, can all be unified in a single moment.

Of course. This entire piece of work was done entirely through Claude. I first conducted the research in Korean and then translated it into English, so there may well be some expressions that are awkward or inappropriate. LLMs still cannot replace every function in the world, after all.

shy-bird-07f5.alexanderparis…