🚨 California's July 1 crypto licensing deadline is 15 days out, and most founders don't realize their existing licenses won't cover them.

Here's what trips up most founders: your money transmitter license, your BitLicense, your federal MSB registration. None of them automatically cover you under California's new Digital Financial Assets Law (DFAL).

It's a brand-new, standalone licensing regime.

Quick breakdown of what actually matters:

What it covers. If you exchange, transfer, store, issue, or administer digital assets for California residents, you're likely in scope. The transfer and issuance prongs catch more companies than people expect. Move tokens between user wallets? Issue a tokenized fiat balance? You're probably in the net.

It's not a registration. It's a substantive license. DFPI reviews your business model, your finances, your governance, and the people running it before they grant anything. Closer to a state money transmitter or trust company review than a form you file.

The money. Published starting points are $100k in tangible net worth and a $500k surety bond. Read "starting points" literally. Bigger California activity, reserve-backed instruments, or custody obligations push those numbers up during review. And tangible net worth strips out goodwill, intangibles, and affiliate receivables, so the figure on your balance sheet is rarely the figure the regulator uses.

Where applications actually stall. Almost never the legal framing. It's the financial package: pro forma projections with no documented assumptions, reserve methodology that isn't supported, capital composition that doesn't survive adjustment. A deficiency left unanswered for 60 days can get your whole application treated as abandoned.

Here's the structural problem nobody assigns an owner to: counsel handles applicability. Compliance handles AML. Engineering handles custody. But the financial submissions, the projections, the reserve math, the regulator responses on license items, those don't have a default owner at most early-stage companies. Your bookkeeper can produce statements but won't defend a projection assumption to DFPI. The founder knows the business but doesn't have time to build and defend the full package.

That gap is exactly where applications sit in the queue for months.

If you're issuing a stablecoin, it gets heavier. AB 1934 adds a monthly reserve compliance report. Not quarterly. Monthly. If your close process runs on a quarterly rhythm, that's a real upgrade to your reporting capacity, not a minor add-on.

So the real question for the next two weeks isn't "do we qualify." It's "who owns the numbers when DFPI starts asking."

If you're staring at July 1 without a clear answer to that, who's carrying your financial package right now: counsel, your bookkeeper, or nobody yet?

2

1

43

Let me help:

Galaxy Digital does not directly hold a standalone European MiCA license; however, its joint venture, AllUnity (with DWS and Flow Traders), secured a German BaFin e-money license to issue a fully MiCA-compliant euro stablecoin, EURAU. In separate regulatory news, Galaxy secured a New York BitLicense in May 2026 to offer institutional crypto trading and custody services

13

🚨 ICYMI: MoonPay, one of the world's largest crypto on-ramp providers, will be supporting the Injective Summit taking place on July 16th in Washington, D.C.

@moonpay has helped bring millions of users into crypto through its seamless fiat-to-crypto infrastructure and works with some of the biggest names across Web3, payments, and fintech.

The company also holds a New York Trust Charter and BitLicense, making it one of the more heavily regulated players in the industry.

This is particularly relevant when you consider the theme of the summit.

3

1

41

266

Bitlicense获批Mastercard背后的战略布局。

🔗himalayaustralia.com.au

#NFSCHAS7澳喜特戰七中隊

#幣圈風雲

#CRYPTONewsTalk

#TDCCP

32

24

242

Jun 15

But scale is not the only reason this announcement matters.

Injective specifically highlighted MoonPay’s New York Trust Charter and BitLicense two of the most recognized regulatory approvals in the U.S. digital asset industry.

These are not easy licenses to obtain.

1

18

191

Jun 15

🟣 Why MoonPay is quietly powering the entire crypto revolution

Tired of complicated on-ramps, high fees, and sketchy exchanges?

MoonPay makes buying Bitcoin, $Ethereum, $Solana, and 170 more ridiculously easy with your credit card, Apple Pay, Google Pay, bank transfer, PayPal, or even Venmo.

✅ Instant

✅ Secure (NY BitLicense, MiCA licensed, Chainalysis award winner)

✅ Trusted by millions worldwide

Whether you're a newbie dipping your toes in or a degen scaling up, MoonPay is your passport to crypto.

Recent wins:

_Mastercard stablecoin debit card (spend crypto like cash at 150M merchants)

_Partnerships with Hyperliquid, World Series of Poker, and more

MoonAgents app for autonomous workflows

_Powering seamless TradFi → DeFi bridges

No more waiting days for transfers. Just buy → hold → spend.

Your move: Download the app or head to moonpay.com and get your first crypto in under 60 seconds.

#MoonPay #Crypto #Bitcoin #Solana #Web3

1

66

Jun 13

Why MoonPay matters?

They aren't just any payment gateway. They hold a highly coveted New York Trust Charter and BitLicense.

They handle fully compliant fiat on-ramps, digital asset settlement and even integrate smoothly across the Mastercard network.(2/3)

1

20

万事达卡获得纽约Bitlicense以支持稳定币和数字支付基础设施。

🔗himalayaustralia.com.au

#NFSCHAS7澳喜特戰七中隊

#幣圈風雲

#CRYPTONewsTalk

#TDCCP

28

22

316

Jun 13

People don't realize how incredibly rare it is for an entity holding a New York Trust Charter and a BitLicense to explicitly back a protocol event.

24

ubitan retweeted

Jun 12

MoonPay just officially joined the @injective Summit.

> MoonPay holds a New York Trust Charter and a BitLicense two of the hardest regulatory approvals to get in crypto.

> They process payments on the Mastercard network. They serve millions of users worldwide.

And they chose Injective.

> New York Trust Charter

> BitLicense

> Mastercard network integration

> Regulated stablecoin settlement

> Regulated companies do their homework before attaching their name to anything.

MoonPay did theirs. And they picked injective.

Pakistan is watching. And we should be paying very close attention. 🇵🇰🥷

دنیا کے سب سے مشہور آن ریمپ پلیٹ فارمز میں سے ایک، مون پے، اب باضابطہ طور پر انجیکٹو سمٹ کی حمایت کر رہا ہے۔

نیویارک ٹرسٹ چارٹر اور بِٹ لائسنس کے حامل مون پے، ڈیجیٹل اثاثوں کی ادائیگیوں اور اسٹیبل کوائنز کے تصفیے کے لیے ایک منظم اور قانونی انفراسٹرکچر فراہم کرتا ہے، حتیٰ کہ ماسٹر کارڈ نیٹ ورک پر بھی۔

یہ انجیکٹو ماحولیاتی نظام میں ادارہ جاتی سطح پر بڑھتی ہوئی شمولیت اور اعتماد کا ایک اور مضبوط اشارہ ہے۔

9

2

32

1,431

Jun 12

Artículo de mi autoría, para Ámbito Financiero aún en papel, de mayo de 2014 sobre BTC. O sea digamos, de los tiempos en que Adorni inventó que tenía un pendrive con Bitcoins. Entonces yo era el jefe de Tesorería de Xapo y todas las transacciones pasaban bajos mis sistemas operativos directos, las online y las OTC contra dólar, euro y libras. Negociábamos cientos de miles de BTC por mes, en compra y en venta, custodiábamos casi 1 millón de BTC (de 13 millones que existían, hoy 20) de clientes de todo el mundo adentro de un bunker militar en una montaña en Suiza. El 15% del Blockchain a nivel global eran cuentas nuestras. Más aún, entonces la mayor cantidad de clientes individuales los teníamos en Alemania Federal, Wences Casares no lo podía creer pero yo le mostré los números y vió que así era, Inglaterra era nuestro segundo y Francia el tercero. Y nuestro grupo laboral era 80% argentino. Un día recibí wire de Camboya, el pibe había gastado un dineral para transferir pero en compensación le dí más BTC de los comprados pagándole el costo de esa manera. El mayor volumen en BTC transados en tanto venía de Estados Unidos donde habíamos obtenido la BitLicense en Nueva York y nuestra mesa era líder mundial de negocios OTC. A las 3 de la mañana de cada día hábil yo me levantaba para loguearme a las cuentas que manteníamos en bancos de Eslovenia, Liechtenstein y Gibraltar para ver cómo caían los miles de depósitos diarios de clientes que fondeaban, con fiat, sus wallets en Xapo. Podemos reconstruir, al detalle, qué era y cómo funcionaba Bitcoin en 2013-2015 que es la época que invocó Adorni para justificar lo injustificable. Cualquier militante de Bitcoin Argentina de esos años puede también describir cosas parecidas sobre sus propios ámbitos. No estaban ni Binance ni Bybit aún, los exchanges puros eran Bitstamp, Kraken, Bitfinex y Coinbase.

77

99

747

91,744

En popüler fiat giriş (on-ramp) çözümlerinden biri olan MoonPay, resmi olarak Injective Summit'i destekliyor.

New York Trust Charter ve BitLicense lisanslarına sahip olan MoonPay, stablecoin ödemeleri için düzenlemelere uygun altyapı sunuyor; hatta Mastercard ağı üzerinden bile.

MoonPay'in konuşmacı duyurusu için takipte kalın!

13

Jun 12

MoonPay, a leading crypto onramp, is officially supporting Injective's Summit.

@MoonPay brings regulated infrastructure via New York Trust Charter and BitLicense, enabling seamless stablecoin settlements (including via Mastercard). A MoonPay speaker will be revealed soon.

2

14

193

Jun 12

Moonpay joining injective summit with a bitlicense is a big deal for compliance

13

Jun 12

Injective Summit 2026 - thật đáng chờ đợi👀👀👀

Một cái tên cực kỳ đáng chú ý vừa xác nhận đồng hành cùng Injective Summit 2026

@moonpay là một trong những nền tảng On-ramp lớn nhất thị trường crypto hiện đã chính thức trở thành đối tác hỗ trợ cho sự kiện lần này.

Điều đáng chú ý là #Moonpay không đơn thuần chỉ là cổng thanh toán crypto thông thường. Với việc sở hữu New York Trust Charter cùng BitLicense, Moonpay đang nắm trong tay hạ tầng pháp lý cực mạnh để kết nối thanh toán stablecoin với hệ thống tài chính truyền thống, thậm chí hỗ trợ cả thanh toán qua Mastercard

Đây tiếp tục là một tín hiệu cho thấy @injective đang ngày càng tiến gần hơn tới mục tiêu kết nối giữa TradFi x DeFi – điều mà hệ sinh thái này đã theo đuổi suốt thời gian qua.

Team cho biết speaker đại diện Moonpay tại sự kiện sẽ sớm được công bố 👀 - CỰC CỰC KÌ ĐÁNG CHỜ ĐỢI

Có cảm giác Injective Summit năm nay sẽ không chỉ là một event cộng đồng đơn thuần… mà sẽ còn mang tới khá nhiều BIG NEWS phía trước.

Anh em theo dõi hệ $INJ chắc nên bắt đầu chú ý nhiều hơn rồi đó 👀🔥

#Injective #INJ #Moonpay

Jun 11

The most popular on-ramp solution, @moonpay, is officially supporting the Injective Summit.

With a New York Trust Charter and a BitLicense. Moonpay has the regulated rails for stablecoin settlement, even across the @Mastercard network.

Stay tuned for Moonpay's speaker reveal!

93

1

81

9,570

Jun 12

Crypto One Liners - Crypto Equities

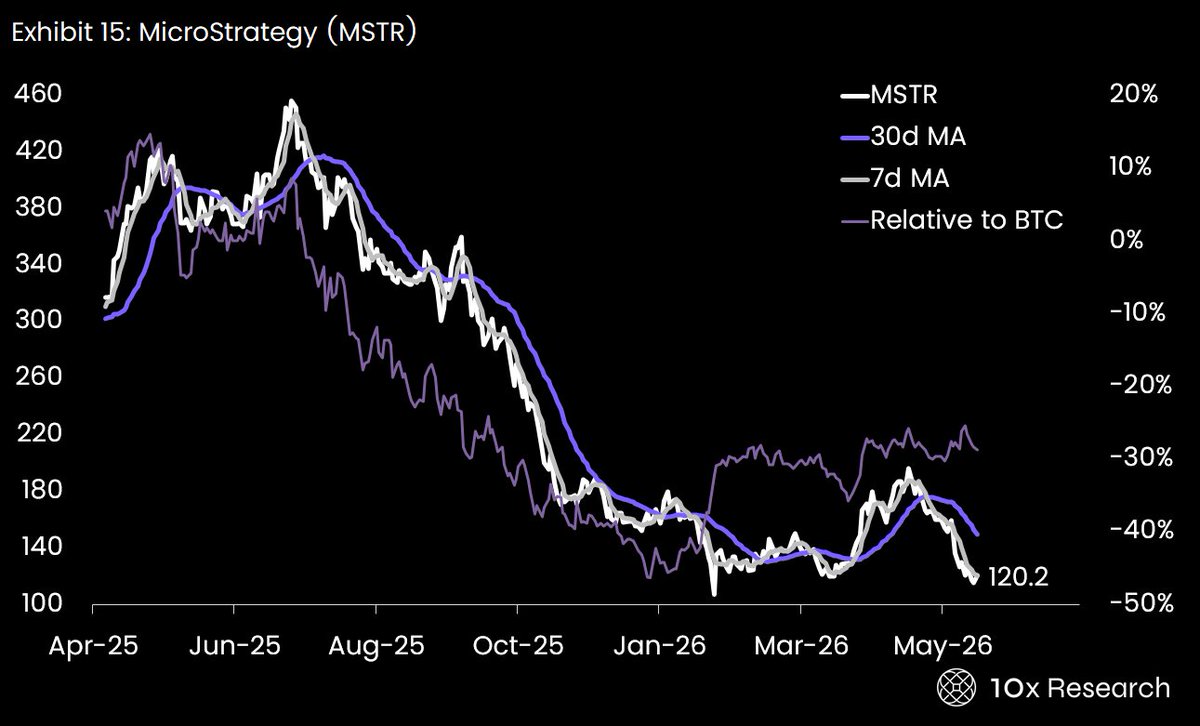

MSTR (-8.9%) — CEO share sale spooked the market at $60K BTC, but a 1,550 BTC buyback restored confidence; STRC trading below par signals preferred-equity stress.

3350.T (-9.8%) — Metaplanet cut its warrant floor from ¥298 to ¥187 as mNAV fell below 1.0x, BTC yield turned negative, and unrealized losses hit $1.64 billion.

BMNR (-7.5%) — Largest weekly ETH buy of 2026 ($214M) lifted shares 5% premarket before a $274M preferred offering sent common stock down 5–10% on dilution fears.

BNC (-22.6%) — Lawsuit against asset manager 10X Capital plus a Nasdaq delisting warning for missing its AGM created a dual governance crisis driving shares to historic lows.

GLXY ( 5.8%) — America's largest planned AI data center (1.6 GW, West Texas, half-leased), a NYDFS BitLicense, and a Morgan Stanley ETP partnership drove the week's standout gain.

COIN (-5.7%) — Baird's "Bearish Fresh Pick" downgrade flagged a Q2 revenue miss and CLARITY Act delays, while Bybit's tokenized SpaceX IPO product took direct aim at Coinbase's pre-IPO business.

HOOD ( 4.2%) — IPO underwriting approval, record $377B platform assets ( 48% YoY), a $20.2M insider buy, and a Goldman price target raise to $105 made Robinhood the week's clearest crypto-equity winner.

BLSH (-7.1%) — Solid May volume metrics ($32.9B) were overwhelmed by a Wall Street Sell downgrade and executive insider selling; shares down 38% over the past month.

CRCL (-12.4%) — Stripe/Visa/Mastercard rival stablecoin platform reports hit USDC's moat thesis hard; Mizuho cut its target to $85 from $135, and CEO Allaire's $5M stock sale added fuel to the fire.

BTGO (-8.7%) — Dubai VARA launch was a genuine positive, but a Goldman price target cut to $9 from $10.50 kept a lid on any recovery.

BTDR (-18.3%) — COO, CBO, and CFO all departed within weeks of each other; management's "controlled restructuring" framing did little to calm investors.

HUT (-19.5%) — No company-specific news beyond the AGM; pure sector selling, down nearly 20% on the week.

IREN (-21.3%) — Bernstein's Street-high $100 target and "Nvidia blessing" endorsement, plus an 800 MW South Australia campus announcement, couldn't prevent IREN from falling with the broader mining complex.

More one liners, including crypto currencies, see previous posts or link in bio.

1

1

9

917

The most popular on-ramp, MoonPay, is backing the @injective Summit

With a NY Trust Charter and BitLicense, it’s pushing regulated stablecoin rails even across Mastercard’s network.

Speaker reveal coming soon 👀

Jun 11

The most popular on-ramp solution, @moonpay, is officially supporting the Injective Summit.

With a New York Trust Charter and a BitLicense. Moonpay has the regulated rails for stablecoin settlement, even across the @Mastercard network.

Stay tuned for Moonpay's speaker reveal!

69

13

246

7,687

yuki.k.inj🥷 retweeted

Jun 12

🏛️ 業界最大級のオンランプソリューションである @moonpay が、Injective Summitの公式パートナーとして参加します。

ニューヨーク州信託ライセンス(New York Trust Charter)とBitLicenseを取得するMoonPayは、@Mastercard ネットワークを含むステーブルコイン決済のための規制対応インフラを提供しています。

そして、MoonPayからの登壇者発表もまもなく!

続報をお楽しみに🇺🇸🥷

1

1

75