Gilat to buy Comtech satcoms business six years after failed merger spacenews.com/gilat-to-buy-c…

3

1,373

كوم تكنولوجيز تعلن عن نتائجها للربع الثالث 2026

Comtech announces Q3 2026 earnings

$CMTL

Expected: ⚪

seekingalpha.com/article/491…

#CMTL #الأسهم_الأمريكية #أرباح #تكنولوجيا

75

كومتك تسجل أرباحًا قوية للربع الثالث

Comtech posts strong Q3 earnings

$CMTL

Expected: 🟢

seekingalpha.com/article/491…

#CMTL #الأسهم_الأمريكية #أرباح #استثمار

68

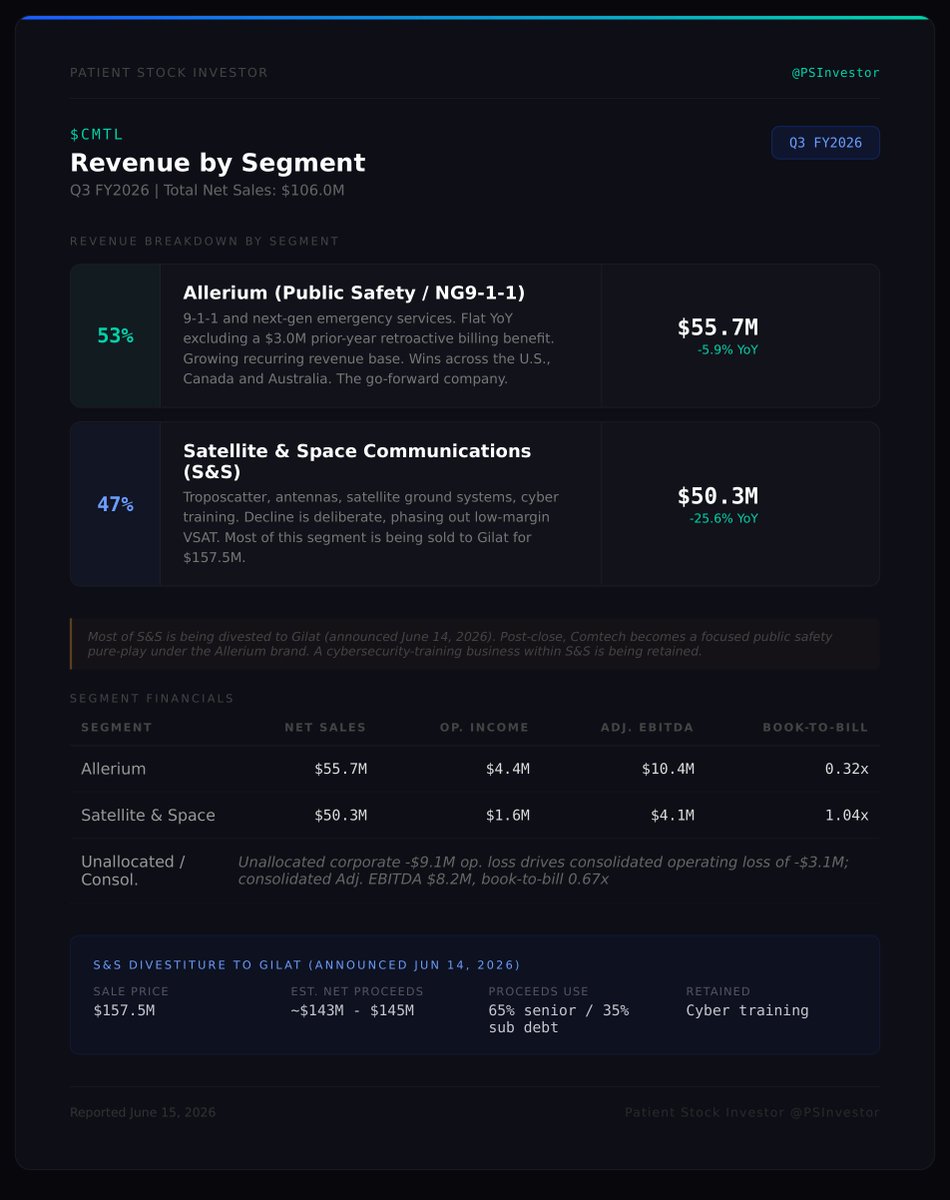

Comtech outlines $143M–$145M in net cash proceeds from Gilat deal as it shifts focus to Allerium ift.tt/Dv6gAuc

14

$CMTL $GILT

• GILT Management stated the acquisition is expected to be funded from existing cash resources.

• Gilat reported approximately $170 million net cash at the end of Q1 2026.

• Gilat is paying cash. No stock. No announced equity raise.

• Key details:

Purchase price: $157.5 million cash

$10 million deposit already paid

Remaining $147.5 million due at closing

———————————-

Post-closing cushion:

$22.5 million remaining net cash per reports.

• the acquisition of Comtech’s (CMTL) Satellite & Space Communications segment by Gilat (GILT) does not include any debt

• Gilat Satellite Networks (GILT) operates an exceptionally clean balance sheet with virtually zero net debt burden.

• Over the last 18 months Gilat has:

• Acquired Stellar Blu

• Grown revenue significantly

• Improved EBITDA

• Returned to profitability

• Built a sizable cash position

————————————

🔸 Gilat is treating this as a transformational acquisition,

• Management’s message was that Comtech’s satellite assets accelerate Gilat’s move into a much larger defense and space communications company.

———————————-

🔸 Gilat’s Key Reasons for Buying

1. Defense gets much bigger

Gilat said the deal will more than double its defense revenue.

Comtech brings established U.S. military SATCOM, modem, troposcatter, and defense communications programs.

———————————-

🔸 2. Scale

Combined company expected to exceed $700M annual revenue. ⭐️

Creates a larger satellite ground infrastructure player able to compete for bigger programs.

———————————

🔸 3. Higher-growth markets

Space communications

Defense communications

Resilient communications

Multi-orbit satellite networks (LEO/MEO/GEO)

———————————

🔸 4. Product synergy

Gilat already has:

Wavestream amplifiers

DataPath military terminals

SkyEdge IV platform

• Comtech adds:

Modems

Defense SATCOM systems

Troposcatter communications

Satellite networking products

⭐️ Together they become a much broader end-to-end satellite communications supplier.

$CMTL $GILT

Back in 2020, Comtech tried to acquire Gilat for about $532M

• The deal collapsed during COVID and Comtech ultimately paid Gilat a $70M termination settlement.

• Now, six years later, the roles have reversed: Gilat is buying a major piece of Comtech.

1

1

316

$CMTL $GILT

Back in 2020, Comtech tried to acquire Gilat for about $532M

• The deal collapsed during COVID and Comtech ultimately paid Gilat a $70M termination settlement.

• Now, six years later, the roles have reversed: Gilat is buying a major piece of Comtech.

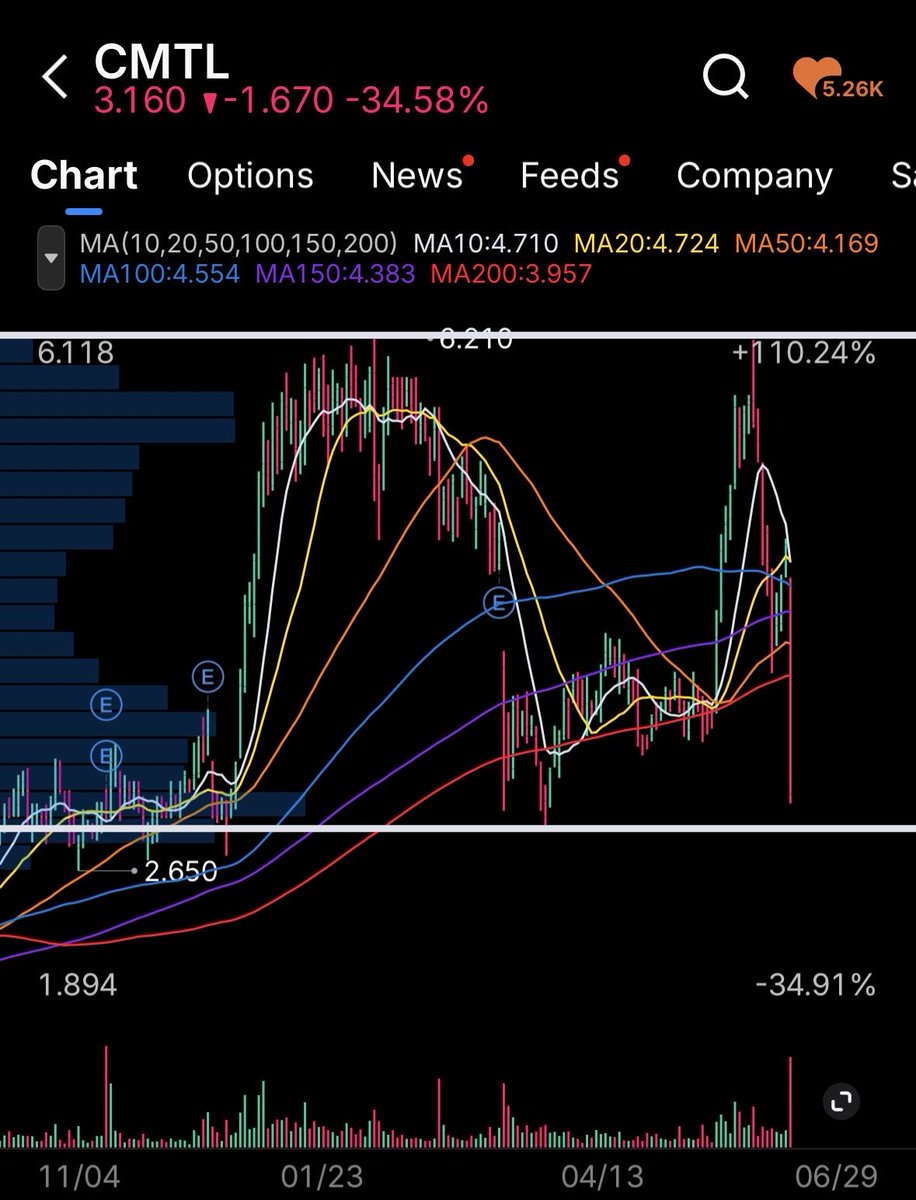

$CMTL BIG NEWS SENDING THE STOCK -35% 🔴

🔸 Comtech announced it is selling most of its Satellite & Space Communications business to Gilat Satellite Networks for $157.5 million.

• Expected net proceeds are approximately $143–145 million, primarily to pay down debt and strengthen the balance sheet.

• 100% of proceeds are earmarked for debt reduction.

————————————

🔸 Management is essentially abandoning the previous “satellite and space” centered turnaround and becoming a focused NG-911 / public safety software company through its Allerium division.

————————————

🔸 For investors who owned CMTL for:

• AWS gateway exposure

• Kuiper opportunity

• Satellite modems

• Troposcatter

• Military SATCOM

• Those assets are largely going to Gilat. $GILT

• thesis is now moving to Gilat Satellite Networks

1

588

$CMTL BIG NEWS SENDING THE STOCK -35% 🔴

🔸 Comtech announced it is selling most of its Satellite & Space Communications business to Gilat Satellite Networks for $157.5 million.

• Expected net proceeds are approximately $143–145 million, primarily to pay down debt and strengthen the balance sheet.

• 100% of proceeds are earmarked for debt reduction.

————————————

🔸 Management is essentially abandoning the previous “satellite and space” centered turnaround and becoming a focused NG-911 / public safety software company through its Allerium division.

————————————

🔸 For investors who owned CMTL for:

• AWS gateway exposure

• Kuiper opportunity

• Satellite modems

• Troposcatter

• Military SATCOM

• Those assets are largely going to Gilat. $GILT

• thesis is now moving to Gilat Satellite Networks

$CMTL & $AMZN Project Kuiper thesis. 🛰️📡🛰️📡

🔸 Everyone thinks Comtech is a legacy hardware play. It’s not. They’ve built the "on-ramp" for next-gen space networks.

• Here is the thesis on why #AMZN (Project Kuiper) needs this tech RIGHT NOW:

——————————-

🔸 The #L3Harris Connection

• #Amazon’s Project Kuiper recently partnered with L3Harris to design satellite payloads for military/government users.

• Guess who builds the underlying software-defined, anti-jam modem hardware for #L3Harris? Comtech via their sole-source A3M program.

—————————-

🔸 The Multi-Orbit Cloud Reality ☁️

• #Amazon’s goal isn’t just selling consumer broadband; it’s feeding data directly into the AWS cloud.

• Enterprise and defense clients don't use isolated networks.

• They require hybrid environments moving between terrestrial fiber, local wireless, and dynamic LEO/GEO/MEO/HEO orbits.

————————————

🔸 Enter Comtech’s Digital Gateways:

• Instead of static satellite hubs, Comtech’s Digital Common Ground (DCG) line acts as a data translator.

• It ingests messy ground-level data (analog radios, radar, fiber), digitizes it immediately at the antenna via the DIFI standard, and converts it into pure, cloud-native packets.

———————————-

🔸 Why Kuiper Needs It 🛰️

• For Amazon to monetize Kuiper for the Pentagon or Tier-1 telcos, they must bypass proprietary, legacy ground hardware.

• By utilizing DIFI-compliant Digital Gateways (CMTL), Amazon can plug Kuiper's space network straight into virtualized AWS data centers globally.

———————————

🔸 The Orchestration Layer (ELEVATE 2.0)

• While DCG digitizes the data, Comtech’s ELEVATE 2.0 software acts as the sky highway.

• It allows 500,000 terminals to dynamically roam between different satellite orbits seamlessly.

• It provides the multi-provider routing Amazon needs to bridge Kuiper with existing GEO/MEO/LEO/HEO networks.

1

508

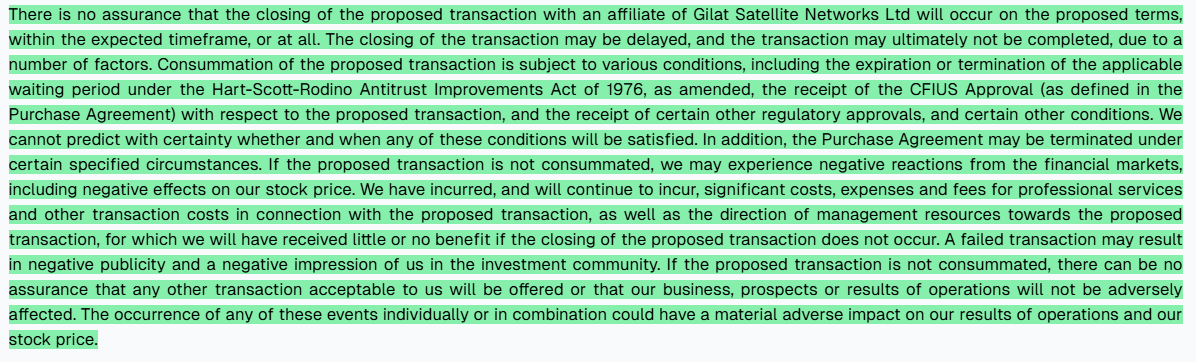

Comtech Telecommunications Corp. has entered into a definitive agreement to sell most of its Satellite and Space Communications segment to Gilat Satellite Networks Ltd. for $157.5 million.

The transaction is subject to customary closing conditions, including regulatory approvals, with the Company currently expecting the transaction to close in calendar Q4 2026.

Upon closing, the Company will use the net cash proceeds to reduce debt and recapitalize the business to provide a stronger and healthier financial position for the remaining Allerium business.

23

كومتك تعلن عن بيع جزء من أعمالها

Comtech sells part of its business

$CMTL

Expected: 🟢

finance.yahoo.com/markets/st…

#CMTL #الأسهم_الأمريكية #استثمار #صفقات

58

$CMTL - Comtech Telecommunications Corp - 10Q - Updated Risk Factors

CMTL flags new risks from its $157.5M sale of satellite/space units to a Gilat affiliate: deal uncertainty may disrupt customers, partners, employees, operations and invite litigation, while failure to close after heavy costs and regulatory hurdles could hit results, reputation and stock price. #SatelliteCommunications #SpaceIndustry #RegulatoryRisk #DealUncertainty #LitigationRisk

🟢 Added 🟠 Removed

d-risk.ai/CMTL/10-Q/2026-06-…

410

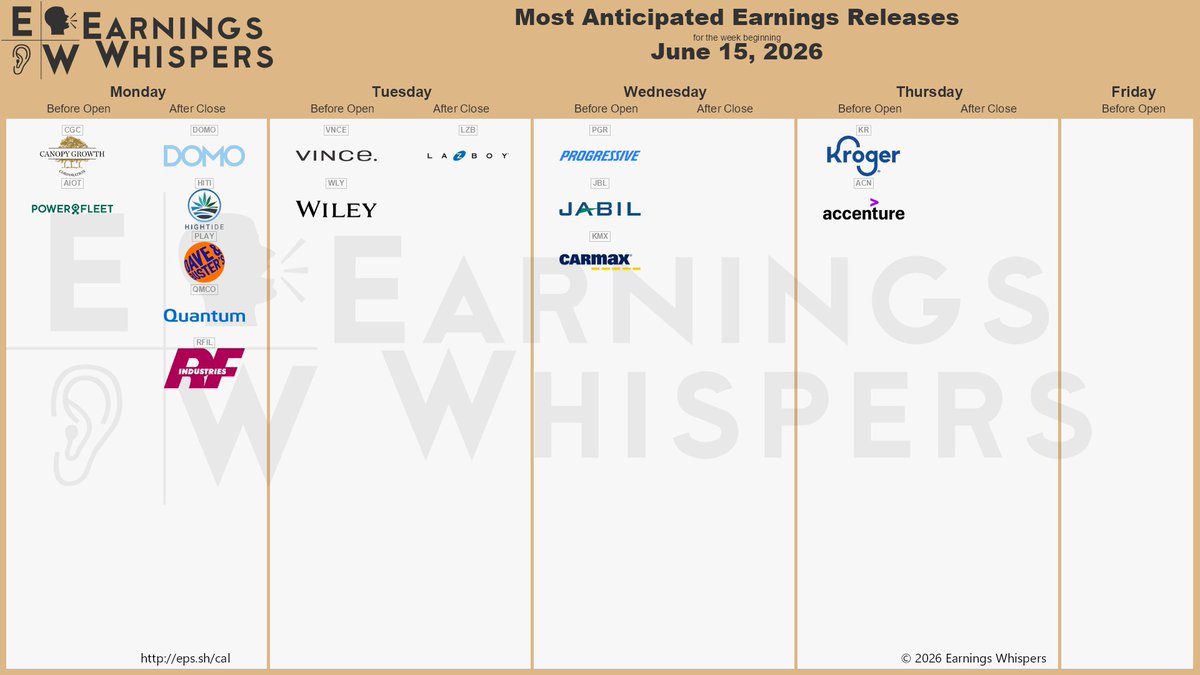

The most anticipated earnings releases for the week of June 15, 2026, are @kroger $KR, @progressive $PGR, Accenture $ACN, @Jabil $JBL, @Domotalk $DOMO, @HighTide_HITI $HITI, @CanopyGrowth $CGC, @lazboy $LZB, @CarMax $KMX, and @vince $VNCE.

earningswhispers.com/calenda…

#mostanticipated #earningswhispers #kroger #progressive #accenture #jabil #hightide #canopy #LaZBoy #carmax #vince #smithandwesson #Comtech #earningswhisper #earnings #earningscalendar

Jun 12

#earnings for the week of June 15, 2026

earningswhispers.com/calenda…

$KR $PGR $ACN $JBL $DOMO $HITI $CGC $LZB $KMX $VNCE $AIOT $PLAY $RFIL $QMCO $WLY

ALT The most anticipated earnings releases for the week of June 15, 2026, are Kroger #KR, Progressive #PGR, Accenture #ACN, Jabil #JBL, Domo #DOMO, High Tide #HITI, Canopy Growth #CGC, La-Z-Boy #LZB, CarMax #KMX, and Vince #VNCE.

2

30

52,390

$Comtech Telecommunications Non-GAAP EPS of -$0.22 beats by $0.05, revenue of $106M misses by $4.2M

9

Wall Street apre al rialzo: riflettori su Dave & Buster’s dopo i conti attesi in serata. SpaceX continua a far parlare di sé dopo il debutto record, mentre analizziamo i risultati di Comtech e Domo.

#WallStreet #Borsa #SpaceX #Azioni

it.benzinga.com/news/usa/tra…

35

10h

What's Happening in US Markets Now (2/3):

1) J&J to invest $1 bn to expand vision operations

2) Parsons wins $184 mn Navy contract

3) Gilat to buy Comtech unit for $157.5 mn

4) TripAdvisor sells TheFork to AXP for $700 mn

5) JP Morgan upgrades Kratos on growth outlook

1

477

$CMTL ( 12.6% pre) Comtech: Fiscal Q3 Earnings Snapshot

ooc.bz/l/105109

1,489

Comtech Announces Definitive Agreement to Sell Most of Its Satellite and Space Communications Business to Gilat

satcom.digital/news/comtech-…

19

$CMTL Q3 FY26 earnings are out, and the headline is not the print, it is the pivot.

On the same day it reported results, Comtech $CMTL announced it is selling most of its Satellite and Space business to Gilat and reset terms with its lenders and preferred holders. In one move a debt-heavy conglomerate becomes a focused public safety pure-play.

Key catalysts from the report:

- Sale of most of the Satellite and Space business to Gilat, with proceeds going straight to senior and subordinated debt paydown

- Renegotiated credit facilities and a replaced preferred stock series, with covenant relief extended into 2027

- Operating cash flow positive again, extending the streak built through the turnaround

- Allerium NG9-1-1 momentum, including statewide Kentucky go-lives and a new Canadian facility in Gatineau

Ken Traub $CMTL, Chairman, President and Chief Executive Officer:

'𝘛𝘰𝘨𝘦𝘵𝘩𝘦𝘳, 𝘵𝘩𝘦𝘴𝘦 𝘢𝘤𝘵𝘪𝘰𝘯𝘴 𝘪𝘮𝘮𝘦𝘥𝘪𝘢𝘵𝘦𝘭𝘺 𝘧𝘶𝘳𝘵𝘩𝘦𝘳 𝘴𝘵𝘳𝘦𝘯𝘨𝘵𝘩𝘦𝘯 𝘰𝘶𝘳 𝘧𝘪𝘯𝘢𝘯𝘤𝘪𝘢𝘭 𝘱𝘰𝘴𝘪𝘵𝘪𝘰𝘯 𝘢𝘯𝘥 𝘦𝘯𝘢𝘣𝘭𝘦 𝘶𝘴 𝘵𝘰 𝘵𝘳𝘢𝘯𝘴𝘪𝘵𝘪𝘰𝘯 𝘵𝘰 𝘢 𝘴𝘵𝘳𝘦𝘢𝘮𝘭𝘪𝘯𝘦𝘥 𝘣𝘶𝘴𝘪𝘯𝘦𝘴𝘴 𝘸𝘪𝘵𝘩 𝘢 𝘤𝘭𝘦𝘢𝘳 𝘴𝘵𝘳𝘢𝘵𝘦𝘨𝘪𝘤 𝘧𝘰𝘤𝘶𝘴 𝘢𝘴 𝘢 𝘭𝘦𝘢𝘥𝘦𝘳 𝘪𝘯 𝘯𝘦𝘹𝘵-𝘨𝘦𝘯𝘦𝘳𝘢𝘵𝘪𝘰𝘯 𝘱𝘶𝘣𝘭𝘪𝘤 𝘴𝘢𝘧𝘦𝘵𝘺 𝘢𝘯𝘥 𝘮𝘪𝘴𝘴𝘪𝘰𝘯-𝘤𝘳𝘪𝘵𝘪𝘤𝘢𝘭 𝘵𝘦𝘤𝘩𝘯𝘰𝘭𝘰𝘨𝘪𝘦𝘴 𝘢𝘯𝘥 𝘴𝘦𝘳𝘷𝘪𝘤𝘦𝘴.'

The two segments tell opposite stories. Allerium, the public safety and NG9-1-1 business, is the engine Comtech $CMTL is keeping, with a growing recurring base and wins across the U.S., Canada and Australia. Satellite and Space is shrinking on purpose as low-margin VSAT work gets cut, and it is the piece being sold.

Inflection point: this is the quarter Comtech $CMTL stops being a satellite-plus-public-safety hybrid and commits to a single mission as a public safety company under the Allerium name.

323

10h

$CMTL — Comtech just executed a dramatic strategic pivot. The company is shedding most of its Satellite business for $157.5M. This move fundamentally reshapes CMTL's financial profile, with the sale value noted to exceed its current market capitalization at the $5.41 filing price. The substantial proceeds are earmarked for significant debt reduction, a critical step for a company that has faced "going concern" disclosures.

We’ve peeled the details. This isn't just an asset sale; it's a complete capital structure re-engineering. The associated extension of credit covenant relief provides crucial financial breathing room, allowing Comtech to focus entirely on its remaining, higher-margin Allerium public safety business. This dual action de-risks the balance sheet while sharpening strategic focus, aiming for long-term stability and growth in a concentrated market segment.

The implications are clear: a leaner, more focused CMTL emerging from a period of financial strain. Traders should watch for execution in this new, streamlined operational framework.

Headlines are late. Filings aren't.

Source & full breakdown: Wiseek (link in bio)

192