Abdul Hadi Adeyinka retweeted

Product & Growth Lead

Location: Hybrid/Remote (Lagos)

About CoreCard:

CoreCard is a product of CoreLink, a technology company focused on building innovative digital solutions for businesses and organizations.

CoreCard is a modern business identity and sales enablement platform that combines Smart ID, Lead Capture, CRM, Reporting, and Customer Management into one ecosystem.

As we prepare for our MVP launch, we are looking for a Product & Growth Lead who can help drive product adoption, customer acquisition, onboarding optimization, and long-term growth.

This role will work closely with the Founder, Product Team, Engineering Team, Design Team, and external marketing partners to help shape the future of CoreCard.

Role Summary:

We are seeking a strategic and execution-focused Product & Growth Lead who will own product growth from acquisition to activation, retention, and expansion. You will be responsible for helping CoreCard find product-market fit, develop go-to-market strategies, improve onboarding, gather customer insights, and drive sustainable growth. This role sits at the intersection of Product, Customer Success, Marketing, and Growth.

Requirements:

• 2–5 years experience in Product Marketing, Growth Marketing, Product Operations, Go-To- Market, or related roles.

• Experience working with SaaS, B2B technology products, CRM platforms, marketplaces, or digital products.

• Strong understanding of customer acquisition, onboarding, activation, and retention.

• Experience working across Product, Engineering, Design, and Marketing teams.

• Excellent communication, storytelling, and presentation skills.

• Strong analytical and problem-solving abilities

Why Join CoreCard?

• Be part of an early-stage product with significant growth potential.

• Work directly with the founder and core product team.

• Influence product strategy, growth, and market positioning.

• Help shape a product from MVP launch to market adoption.

• Opportunity to grow into a Head of Growth or Growth Leadership role as the company scales.

To apply, send your CV, portfolio, LinkedIn profile, or relevant work experience to: tunde.o@corelinkng.com

1

66

The Jesus lover retweeted

Jun 12

Product & Growth Lead

Location: Hybrid/Remote (Lagos)

About CoreCard:

CoreCard is a product of CoreLink, a technology company focused on building innovative digital solutions for businesses and organizations.

CoreCard is a modern business identity and sales enablement platform that combines Smart ID, Lead Capture, CRM, Reporting, and Customer Management into one ecosystem.

As we prepare for our MVP launch, we are looking for a Product & Growth Lead who can help drive product adoption, customer acquisition, onboarding optimization, and long-term growth.

This role will work closely with the Founder, Product Team, Engineering Team, Design Team, and external marketing partners to help shape the future of CoreCard.

Role Summary:

We are seeking a strategic and execution-focused Product & Growth Lead who will own product growth from acquisition to activation, retention, and expansion. You will be responsible for helping CoreCard find product-market fit, develop go-to-market strategies, improve onboarding, gather customer insights, and drive sustainable growth. This role sits at the intersection of Product, Customer Success, Marketing, and Growth.

Requirements:

• 2–5 years experience in Product Marketing, Growth Marketing, Product Operations, Go-To- Market, or related roles.

• Experience working with SaaS, B2B technology products, CRM platforms, marketplaces, or digital products.

• Strong understanding of customer acquisition, onboarding, activation, and retention.

• Experience working across Product, Engineering, Design, and Marketing teams.

• Excellent communication, storytelling, and presentation skills.

• Strong analytical and problem-solving abilities

Why Join CoreCard?

• Be part of an early-stage product with significant growth potential.

• Work directly with the founder and core product team.

• Influence product strategy, growth, and market positioning.

• Help shape a product from MVP launch to market adoption.

• Opportunity to grow into a Head of Growth or Growth Leadership role as the company scales.

To apply, send your CV, portfolio, LinkedIn profile, or relevant work experience to: tunde.o@corelinkng.com

5

21

2,275

Apr 13

$EEFT

Perceived as a foundering EU / emerging markets biz, in reality they have cutting edge technology growing like a weed. Founded in 1994 by current CEO Mike Brown, $EEFT is buying back stock given very low FCF multiple

Two material product lines are reaching their inflection points which are being largely ignored today. These products share highly attractive characteristics: (1) significant addressable market with blue chip customers, 2) high initial fixed cost base with incremental margins potentially 90% as revenue scales, and 3) very sticky and growing revenue base.

REN / CoreCard: Within the EFT Processing segment, REN is a modern cloud architecture for payment switching that focuses on real time payments (think Zelle or Venmo) and is sold to banks as white label software. This is one of the only modern architecture platforms that seamlessly operate ATMs, management POS terminals, issue debit cards, and operate real-time payment systems. In addition, REN just won Bank of America (the largest ATM and POS terminal contract Euronet has ever signed). We estimate, REN products generated roughly $55 million revenue in 2025 with 40% revenue growth year-over-year.

Euronet also recently purchased CoreCard to be integrated into the REN product and provide a full card issuing product offering. Since acquiring CoreCard, Euronet has 15 customer indications of interest and we expect customer wins over the coming months. All in, we estimate REN / CoreCard to generate $125 million revenue during 2026 with revenue growth potential of 20% to 30% for the foreseeable future at highly attractive margins.

Dandelion: Within the Money Transfer segment, Dandelion is a leading real-time cross-border payment platform that offers a modern-day rival to the legacy SWIFT system used globally. Euronet has signed major customers including Citi Bank, HSBC, and Commercial Bank of Australia (40% share in Australia), among others. The SWIFT system came out in the late 1970s and is an antiquated system with fees and slow processing that can take 4 days.

Dandelion is a modern point to point system where 85% of transactions are completed within five minutes with access to billions of bank accounts and wallets globally. Management has noted that each customer they have won sets a new record with transaction volume each month yet still is a very small percentage of the available revenue within those customers.

Management is currently talking to 75 of the top banks in the world and believes these initial high quality customer wins could lead to a strong cadence of additional announcements in 2026 and beyond. Estimates for this addressable market are ~$15 trillion of annual transaction volume (charging a fee or some percent) for Euronet or nearly 20x the $800 billion in the money remittance market where the market has placed so much scrutiny.

With the potential for the Dandelion product to be 5% to 10% of total revenue looking out 5 to 7 years (and much larger over time) at highly accretive margins (in excess of 50% operating margins), this growth driver is being completely missed by the market entering an inflection year.

1

2

1,409

Jan 8

On the news of Apple Card moving from GS to JPM Chase, some notes from $CCRD & $EEFT mgmt:

- They will get another $35m in 2026 and in 2027 from GS (based on Apple/JPM Chase news it will take 24 months to coonvert

- A termination fee still applies when GS ends the contract before 2030 (the earlier it terminates, the higher so could assume this is another multi million $)

- GS gap can be filled within 2-3Y

- Non-GS revenue was said to grow 30% CAGR through 2027 by CCRD (EEFT said they can get that higher ; cross-sell with REN)

- Euronet mgmt was fully aware they weren't going to get GS revenue beyond 2027

- Adding some Leland comments from end of 2024 about the CoreCard platform

1

13

3,180

BREAKING: Major expansion for $EEFT.

Euronet announces agreement to acquire CrediaBank’s merchant acquiring business in Greece.

The Deal Stats:

• Adds >$22B in annualized volume

• Adds >240k merchants

• Secures #1 market position in Greece

• Exclusive long-term bank distribution partnership

My Take:

The market ignores the structural pivot here. This isn't just "buying volume." It's a deployment vehicle for their full tech stack (CoreCard IRIS real-time payments).

They are actively replacing capital-intensive ATM revenue with capital-light, recurring fintech fees.

This transformation is exactly why $EEFT remains a 9% weight in my book.

1

3

314

22 Dec 2025

Ask Claude to change it according to your project

-------

You are an expert Python/FastAPI code reviewer performing a thorough review. Your goal is to find bugs, security issues, and improvements.

## Step 1: Get the Diff

Run the following command to get the changes:

- If `$ARGUMENTS` is empty: `git diff master...HEAD`

- If `$ARGUMENTS` is `--staged`: `git diff --staged`

- Otherwise: `git diff $ARGUMENTS`

Also run `git diff master...HEAD --stat` to see which files changed.

## Step 2: Review Each Changed File

For each file in the diff, analyze:

### A. Bugs & Logic Errors

- Off-by-one errors, incorrect conditions

- Null/None handling issues (especially list/array index access like `[0]`)

- Index out of bounds (ensure list is not empty before accessing indices)

- Race conditions, async issues

- Incorrect return values

- Missing error handling

- Edge cases not handled (empty lists, None values, empty strings)

- Type mismatches (string/number conversions)

- State mutations on mutable objects

### B. Security Issues (OWASP Top 10)

- SQL injection (raw queries without parameterization)

- Command injection (subprocess without proper escaping)

- XSS vulnerabilities

- Hardcoded secrets/credentials (API keys, passwords, tokens)

- Insecure deserialization

- Missing authentication/authorization checks

- Sensitive data exposure in logs, error messages, or responses

- Input validation (missing or insufficient validation)

- Resource exhaustion (unbounded loops, recursion)

- CORS/CSRF missing protections

### C. Imports & Dependencies

- Missing imports that will cause runtime errors

- Unused imports

- Circular import risks

- Import order (stdlib, third-party, local)

### D. Naming & Style (PEP8)

- Variable/function naming conventions (snake_case)

- Class naming (PascalCase)

- Constants (UPPER_SNAKE_CASE)

- Descriptive names vs single letters

- Line length (max 120 chars)

- Consistent formatting

### E. Project-Specific Rules (from DEVELOPMENT.md)

**Exception Handling:**

- MUST use `CodedHttpException` instead of `HTTPException`

- MUST chain exceptions with `from` when catching root cause

- MUST use `exc_info=True` when logging exceptions

- MUST check `exceptions/error_definitions/` for existing error codes before creating new ones

- Use `error=` parameter (not `error_code=`)

- Verify error code matches the error context (e.g., `ACCT_*` for account errors, `AUTH_*` for auth errors)

**Error Code Verification Checklist:**

- Is an existing error code from `exceptions/error_definitions/` being reused appropriately?

- Does the error code prefix match the domain? (`AUTH_`, `SNUP_`, `USR_`, `ACCT_`, `SYS_`)

- Is the HTTP status code in the error definition correct for the error type?

- If parameterized, are `message_params` being passed correctly?

- Are sensitive details being exposed in error messages? (should NOT be)

**Audit Logging:**

- `init_audit_log()` should be called BEFORE database operations

- Objects must be loaded into session before modification for tracking

- Use descriptive action types (CREATE_, UPDATE_, DELETE_, APPROVE_, REJECT_)

**Audit Logging Checklist:**

- Is `init_audit_log()` called for routes that modify data?

- Is `http_request: Request` parameter included for audit logging?

- Are objects loaded into session BEFORE modification? (bulk `.delete()` bypasses audit!)

- Is action type descriptive? (e.g., `CREATE_CASHBACK_APPROVAL_BATCH`, not just `CREATE`)

- Is `request_reason` provided when appropriate (for admin actions)?

- For DELETE: are objects loaded with `.all()` before `db.delete()` in a loop?

**When Audit Logging is Required:**

- All admin endpoints that modify data

- User-facing endpoints that modify sensitive data (accounts, payments, cards)

- Any endpoint that creates/updates/deletes database records

- External API calls via `HTTPClient` (automatically tracked)

**General:**

- Use type hints consistently

- Use `logger` from `common.logger` not print statements

- Use async/await properly in FastAPI routes

**API Parameter Conventions:**

- Path params: UUID with `Annotated[uuid.UUID, Path()]`, integers with `Path(gt=0)`

- Query params for pagination: `offset: int = Query(0, ge=0)`, `limit: int = Query(20, gt=0, le=100)`

- Optional query params: `filter_value: Optional[str] = Query(None)`

- Enum query params: `status: str = Query(None, enum=["ACTIVE", "INACTIVE"])`

- Headers: `x_did: Optional[str] = Header(None, alias="X-DID")`

- All responses MUST use `BaseResponse` wrapper from `rest_schemas/common_schemas.py`

**Pydantic Model Conventions:**

- Naming: `*Request` (input), `*Response` (output), `*Create`, `*Update`

- String constraints: `Field(min_length=X, max_length=Y)`

- Custom validation: `@field_validator("field_name")`

- Cross-field validation: use `info.data.get("other_field")` in validator

- ORM models: `model_config = ConfigDict(from_attributes=True)`

- Currency: use `Decimal`, not `float`

- IDs: use `uuid.UUID`

- Emails: use `EmailStr`

- Schemas location: `rest_schemas/` directory

**HTTP Status Codes:**

- `200 OK`: GET, PUT success

- `201 CREATED`: POST success (resource created)

- `202 ACCEPTED`: Async operation accepted

- `204 NO_CONTENT`: DELETE success

### F. Test Coverage

- Are there tests for new functionality?

- Do tests cover edge cases (boundary conditions, None values, empty collections)?

- Are test assertions checking the right values?

- Did any test values change that might indicate broken behavior?

- Are mocks set up correctly?

- Missing test cases for error paths

- Test isolation (tests don't depend on each other)

- Clear, descriptive test names

- Missing test cases for:

- Null/None input values

- Empty lists/dicts

- Boundary conditions (0, negative, max values)

- Invalid input types

- Concurrent/race condition scenarios

- All branches of conditional logic

**Project Test Organization:**

- Tests in `Core/tests/` directory

- Feature-specific tests in subdirectories: `auth/`, `digital_wallet/`, `gift_card/`, `rewards/`

- Shared fixtures in `conftest.py` files

- Test naming: `test_<scenario>` (e.g., `test_successful_update`, `test_account_not_found`)

- Class naming: `class Test<FeatureName>:` (e.g., `class TestUpdateMortgageAccount:`)

**Required Test Patterns:**

- Test `CodedHttpException` is raised with correct error code:

```python

with pytest.raises(CodedHttpException) as exc_info:

await function_under_test()

assert exc_info.value.definition.code == EXPECTED_ERROR.code

```

- Test rollback on external service failure (HubSpot, CoreCard, etc.)

- Use TestContainers for database isolation (`testcontainers_db` fixture)

- Mock external services: S3, Firebase, HubSpot, CoreCard, Plaid

**Mock Patterns:**

- Database: `Mock(spec=Session)`

- External services: `@patch('integrations.hubspot.service….HubSpotService.forward_user_info')`

- S3: `@patch('common.utils.upload_file')`

- Firebase: `@patch('common.firebase_client.FirebaseClient')`

**Fixture Scopes:**

- `scope="session"` - Shared across test run (e.g., TestContainers DB)

- `scope="function"` - Fresh per test (default, use for test data)

- `autouse=True` - Auto-applied to all tests in scope

### G. API/Response Changes

- Breaking changes to existing API contracts

- Response format matches expected schema

- Field naming consistency across responses

- Backward compatibility for existing clients

- Pydantic models match actual response structure

**Project Response Patterns:**

- All endpoints MUST return `BaseResponse` wrapper:

```python

return BaseResponse(error=None, message="Success", data=result)

```

- Pagination: use `offset/skip` and `limit` query params consistently

- File uploads: use `UploadFile` with `File()` for files, `Form()` for metadata

**Dependency Injection:**

- Database: `db: Session = Depends(get_db)`

- HTTP client: `http_client: HTTPClient = Depends(_get_http_client)`

- Redis: `redis_client: RedisClient = Depends(get_redis_client)`

- Firebase: `firebase_client: FirebaseClient = Depends(get_firebase_client)`

- Request (for audit): `http_request: Request`

### H. Database & Performance

- Database migrations needed?

- N 1 queries, missing indexes

- Proper transaction handling (commit/rollback)

- Unnecessary loops, redundant calculations

- Blocking operations in async context

### I. Better Practices

- Use context managers (`with`) for resource handling

- Prefer list comprehensions over manual loops where readable

- Use `enumerate()` instead of manual index tracking

- Use `pathlib` over `os.path` for file operations

- Prefer `f-strings` over `.format()` or `%` formatting

- Use `dataclasses` or Pydantic models instead of plain dicts for structured data

- Avoid mutable default arguments (e.g., `def foo(items=[])`)

- Use early returns to reduce nesting

- Prefer specific exceptions over generic `Exception`

### J. Nitpicks

- Typos in comments/strings

- Unnecessary comments

- Dead code

- Inconsistent spacing

- Missing docstrings for public functions

- Magic numbers without constants

- Copy-paste code that could be refactored

- Trailing whitespace

- Missing newline at end of file

- Unnecessary parentheses in conditionals

### K. Router/Endpoint Structure

**Router Definition:**

```python

router = APIRouter(

responses={status.HTTP_404_NOT_FOUND: {"description": "Not found"}},

tags=["FeatureName"],

)

```

**Standard Endpoint Pattern:**

```python

@router.post(

"/resource/{resource_id}/action",

response_model=BaseResponse,

status_code=status.HTTP_201_CREATED,

)

async def action_name(

resource_id: Annotated[uuid.UUID, Path()],

request_body: RequestSchema,

db: Session = Depends(get_db),

http_request: Request,

):

init_audit_log(db=db, action_type="ACTION_TYPE", request=http_request)

# implementation

return BaseResponse(error=None, message="Success", data=result)

```

**Checklist:**

- Path follows RESTful convention: `/resource/{id}/sub-resource`

- `response_model=BaseResponse` is specified

- `status_code` matches operation type (201 for POST, 200 for GET, etc.)

- Audit logging initialized before DB operations

- Dependencies injected via `Depends()`

### L. Function Length & Complexity

**Guidelines:**

- Functions should ideally be under 30-40 lines

- Flag functions over 50 lines as candidates for refactoring

- Each function should do ONE thing well (Single Responsibility)

**Signs a function is too long:**

- Multiple levels of nesting (3 levels of indentation)

- Multiple distinct logical blocks separated by blank lines

- Comments explaining "sections" of the function

- Repeated patterns that could be extracted

- Multiple try/except blocks handling different concerns

**Refactoring suggestions:**

- Extract helper functions for distinct logical operations

- Use early returns to reduce nesting

- Extract validation logic into separate functions

- Extract data transformation into dedicated functions

- Consider using strategy pattern for conditional branches

**Review checklist:**

- Does the function have a clear single purpose?

- Could any block of code be named and extracted?

- Are there repeated patterns that could be a helper?

- Is the nesting depth reasonable (≤3 levels)?

- Would breaking it up improve testability?

## Step 3: Output Format

Provide your review in this markdown format:

```

## Code Review: [branch-name]

**Files Changed:** [count]

**Lines Added/Removed:** X / -Y

---

### Summary

[2-3 sentences describing what this PR does]

---

### Bugs & Logic Errors

| Severity | File | Line | Issue |

|----------|------|------|-------|

| HIGH | `path/to/file.py` | 42 | Description of the bug |

| MEDIUM | `path/to/file.py` | 100 | Description |

**Details:**

- **file.py:42** - Detailed explanation of why this is a bug and how to fix it

---

### Security Issues

| Severity | File | Line | Issue |

|----------|------|------|-------|

| HIGH | `path/to/file.py` | 50 | SQL injection vulnerability |

**Details:**

- **file.py:50** - Explanation and remediation

---

### Import Issues

- `file.py:1` - Missing import for `SomeClass` used on line 45

- `file.py:3` - Unused import `os`

---

### Naming & Style

- `file.py:20` - Variable `x` should be more descriptive

- `file.py:35` - Function `doThing` should be `do_thing` (snake_case)

---

### Project Guideline Violations

- `file.py:60` - Using `HTTPException` instead of `CodedHttpException`

- `file.py:75` - Missing `exc_info=True` in logger.error()

- `file.py:80` - Exception not chained with `from`

---

### Error Code Issues

- `file.py:45` - Using wrong error code prefix (using `AUTH_` for account error, should be `ACCT_`)

- `file.py:52` - Creating new error code when existing `ACCT_ACCOUNT_NOT_FOUND` could be reused

- `file.py:68` - Missing `message_params` for parameterized error `{user_id}`

---

### Audit Logging Issues

- `file.py:30` - Missing `init_audit_log()` call for data-modifying endpoint

- `file.py:42` - `init_audit_log()` called AFTER database operation (should be before)

- `file.py:55` - Missing `http_request: Request` parameter needed for audit logging

- `file.py:78` - Bulk `.delete()` bypasses audit logging - load objects first with `.all()`

---

### Test Coverage Issues

- Missing test for error case when X fails

- `test_file.py:100` - Assertion value changed from X to Y - verify this is intentional

- No tests for new function `process_data()`

---

### Nitpicks

- `file.py:10` - Typo: "recieve" → "receive"

- `file.py:25` - Magic number 86400, consider `SECONDS_PER_DAY = 86400`

- `file.py:45` - This comment is outdated

---

### Summary Table

| Category | Issues Found |

|----------|--------------|

| Bugs | X |

| Security | X |

| Imports | X |

| Style | X |

| Project Guidelines | X |

| Error Codes | X |

| Audit Logging | X |

| Tests | X |

| API/Response | X |

| Database/Performance | X |

| Better Practices | X |

| Nitpicks | X |

| Router/Endpoint Structure | X |

| Function Length/Complexity | X |

| **Total** | **X** |

```

## Important Notes

1. **Be thorough** - Check every changed line, even small changes

2. **Be specific** - Always include **full file path** with line number (e.g., `Core/services/gift_card_services.py:42`)

3. **Be actionable** - Explain how to fix each issue

4. **Prioritize** - HIGH severity for bugs/security, MEDIUM for style, LOW for nitpicks

5. **Don't over-report** - If code follows best practices, say "No issues found" for that category

6. **Check tests carefully** - Changes in test assertions or missing tests are critical

7. **Report everything** - Even minor issues like formatting, imports, naming conventions

8. **Suggest missing tests** - Explicitly list test cases that should be added

22 Dec 2025

alright, fuck it

i'm going to try every single code review bot to see which one's the best

bugbot, greptile, coderabbit, graphite...?, who else am i missing

1

1,248

18 Dec 2025

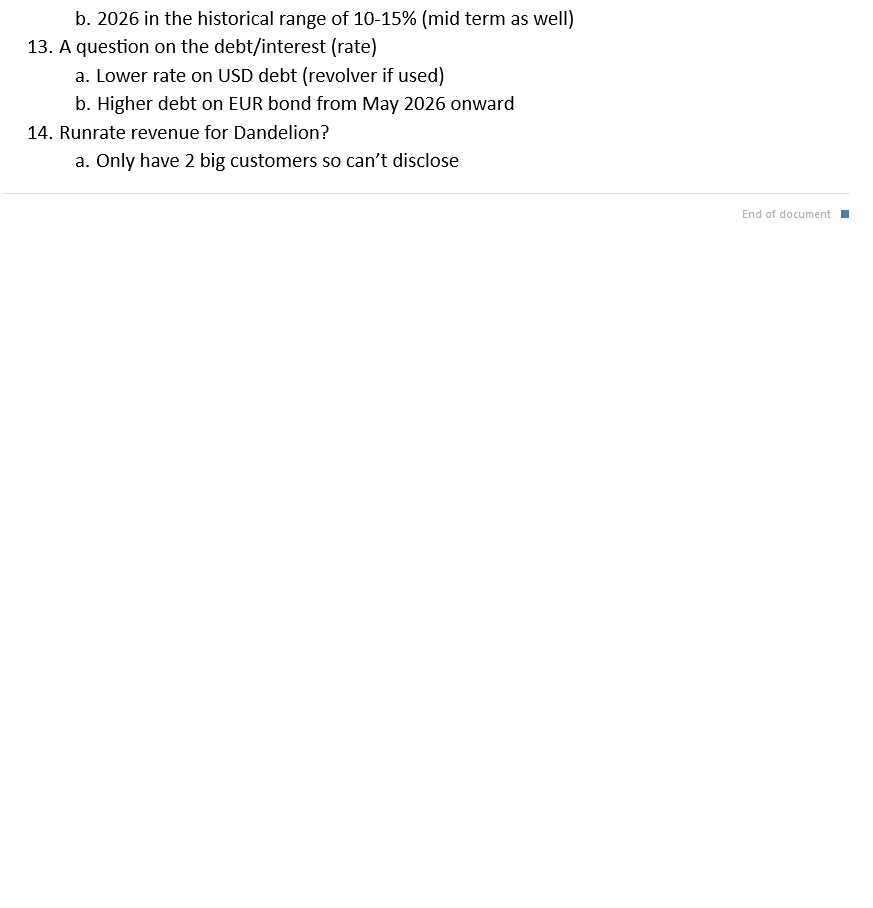

$EEFT value added associated with CoreCard acq, and this doesn't even discuss benefits of taking CoreCard international.

1

6

861

5 Dec 2025

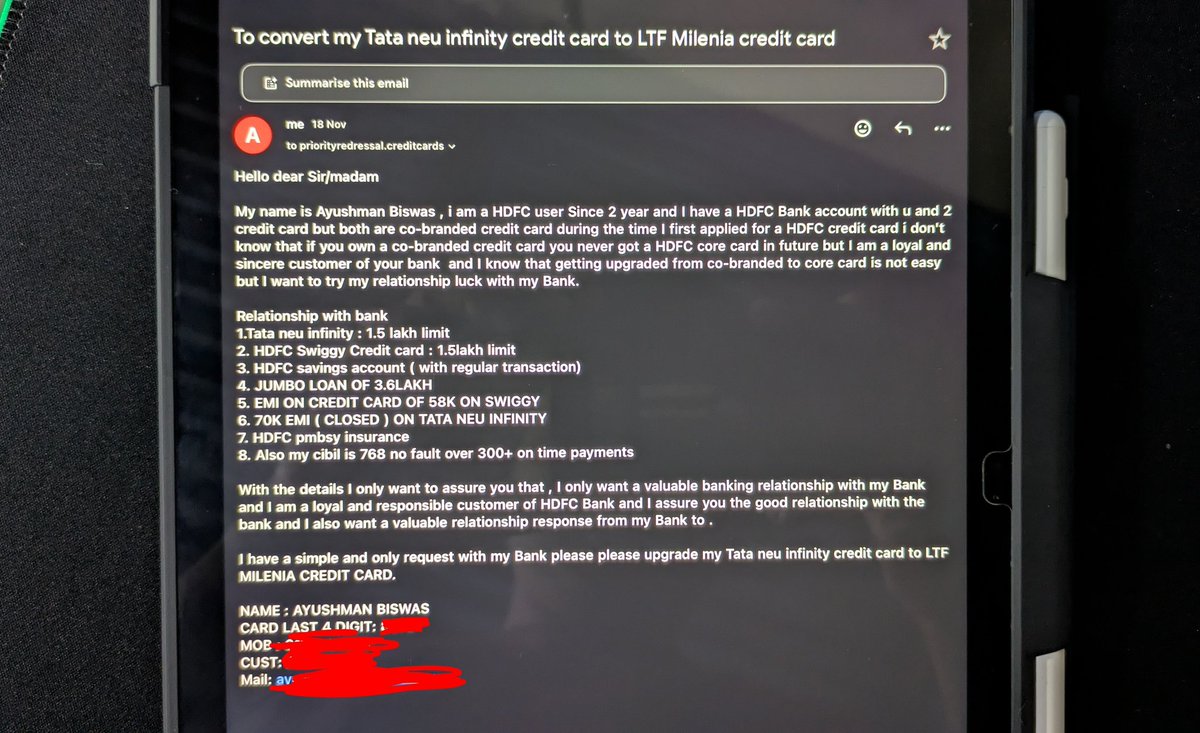

Finally ❤️

Tata neu infinity ——-> Millennia

Core card hits different 😂

Thanks @iSatishAgarwal sir 🙏

Full story 👇🏻

#ccgeeks #hdfcbank #corecard

29 Nov 2025

Full story

I have 2 HDFC co-branded credit card

1.TNI. 2.Swiggy Hdfc

👉I Tried 2-3 times earlier to upgrade to core but rejected then I saw @iSatishAgarwal sir's post and the tips he gave were the best and enough.

👉Then mailed the bank with some butter within it 😂.

#ccgeeks

5

2

11

26,683

DEEP DIVE: WHY $EEFT IS MY HIGHEST CONVICTION TRADE 💡

Position: 9% of Portfolio

Entry: ~$74

Target: $160 (2Y)

The Thesis: A "Triple-Engine" Compounder disguised as a legacy ATM operator.

The market ignores the data. We exploit the gap.

1. THE GROWTH ENGINE (Fintech Infrastructure) 🚀

Investors see "Cash." Data shows "Tech."

• Digital transactions grew 32% YoY via the Dandelion network.

• With the CoreCard acquisition, they now own the full stack: Issuing Processing Settlement.

• They are building a "SWIFT alternative" for the $320T cross-border market.

2. THE "CANNIBALIZATION" ENGINE (Buybacks) ⚙️

This is the missing number. Management is aggressively retiring the float.

• Q3 2025 Activity: ~$130M bought back in a single quarter.

• Track Record: Over the last 4 years, they returned ~85% of annual profits to shareholders via buybacks.

• Strategy: CEO Mike Brown is explicit—if he can't find accretive M&A, he buys the stock because it is mathematically undervalued.

3. THE CAPITAL ARBITRAGE 🏦

They are playing the game on "Easy Mode."

• In Aug 2025, they raised $1B in convertible debt at just 0.625% interest.

• They use cheap debt for growth and free cash flow to buy back shares at ~7x Forward P/E.

• Result: EPS expansion is mathematically inevitable.

THE VERDICT:

You are buying a high-growth fintech platform at a utility-stock valuation, protected by a management team that supports the price with massive buybacks.

The repricing to $160 isn't hope. It's just math catching up to reality.

---

The Challenge: Name another fintech stock with double-digit growth trading at <8x Forward P/E. I'm listening.

1

1

6

679

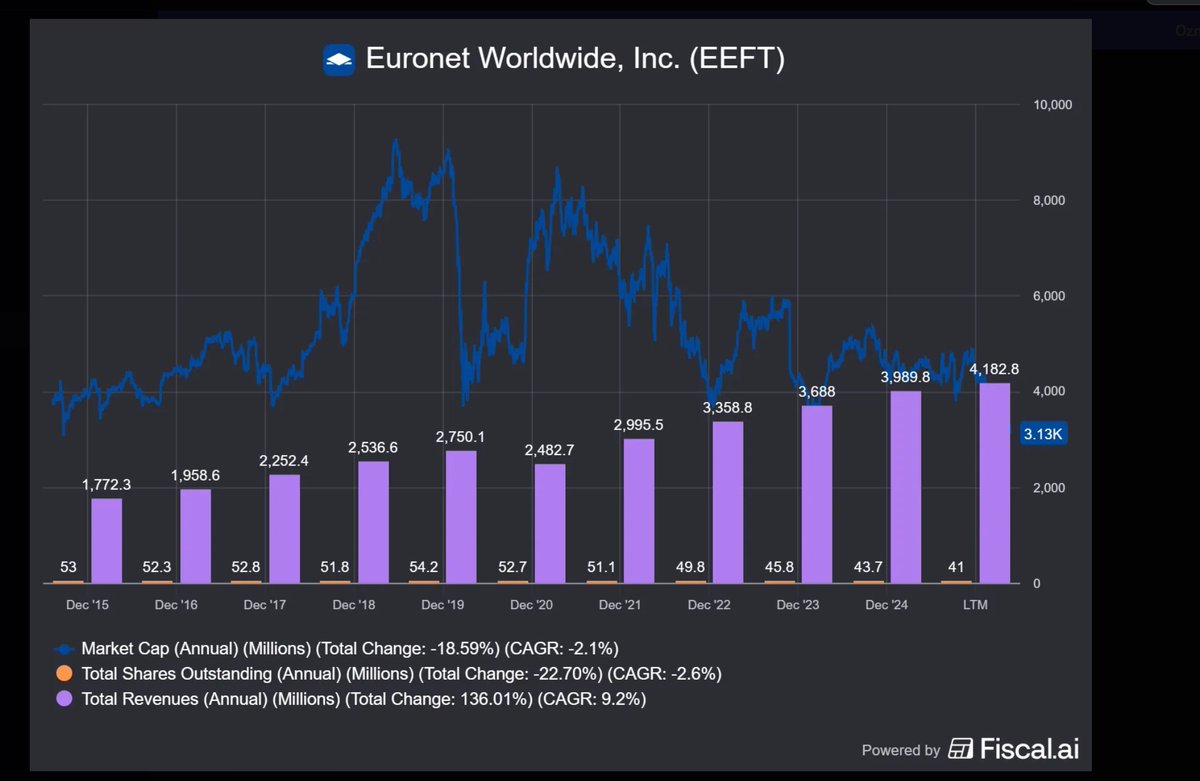

$EEFT: Revenue 136% over decade, stock down 18.6% = divergence begging to close 📊

THE ILLOGICAL SETUP:

Chart shows decade-long disconnect:

- Revenue: 136% total (9.2% CAGR) to $4.18B LTM ✅

- Shares Outstanding: -22.7% (buybacks) ✅

- Market Cap: -18.6% (CAGR -2.1%) ❌

Translation: Fundamentals UP, stock DOWN. This is multi-year multiple compression.

RECENT PANIC (-5% on Q3):

Everyone saw: Revenue growth 6% → 1% (immigration headwinds)

Nobody saw:

- Market share GAINED 12pp in US-Mexico corridor while overall market collapsed -12%

- EBITDA margin 21.3% ( 100bps YoY) despite weak revenue

- Digital mix shift (epay 70%, Money Transfer digital 32%) printing higher margins

THE BULL THESIS: 💡

Stock at $88 (down from $114 June high) pricing in permanent impairment. But:

1) **Market share gains** = when immigration normalizes, $EEFT owns MORE of BIGGER pie

2) **Margin expansion continuing** = digital mix 22-25% margins vs physical 12-15%

3) **THREE catalysts loading NOW**:

- CoreCard vote THIS WEEK ($22/share value, accretive year 1)

- Stablecoins Q1 2026 via Fireblocks (nobody has this modeled)

- Dandelion B2B scaling (Citibank Commonwealth partnerships)

VALUATION SCREAMING:

- $EEFT: 12.1x P/E

- Fiserv: 19.5x | FIS: 15.2x

- 38-46% discount despite SUPERIOR margin expansion MORE catalysts

Market thinks "dying ATM company." Reality: ATMs = 31% of revenue. This is fintech platform executing digital transformation.

PATH TO $165: 🎯

From $88 current → $165 target = 87% upside

- Baseline EPS growth margin expansion

- CoreCard accretion

- Stablecoin catalyst

- Multiple re-rating from 12x to peer 16-18x

Chart proves it: Revenue 136%, stock flat. When that gap closes = violent snapback.

Quality company temporary headwind stupid valuation catalysts = 3-bagger setup 💎

$EEFT

2

494

🚨 EURONET ($EEFT): When Everyone Panics, Smart Money Acts

Market crushed $EEFT -5% on Q3 earnings. Revenue growth crashed from 6% to 1%. "Immigration headwinds!" "Macro weakness!" Everyone's running.

But here's what they missed:

MARKET SHARE GAINS:

• $EEFT's US-Mexico corridor: FLAT

• Overall market: COLLAPSED -12% (Reuters)

• That's a 12pp MARKET SHARE GAIN in the world's biggest remittance corridor

• When immigration normalizes → they own MORE of a BIGGER pie

MARGIN EXPANSION (Despite Weak Revenue):

• Q3 EBITDA margin: 21.3% ( 100bps YoY)

• epay: 70% digital (vs. 40% in 2020)

• Money Transfer digital: 32% YoY

• Digital margins: 22-25% vs. physical 12-15%

• The mix shift is printing money

THREE CATALYSTS LOADING RIGHT NOW:

1️⃣ CoreCard vote THIS WEEK

• $248M all-stock deal (no cash outflow)

• Credit issuing platform: Goldman, Amex, Gemini as clients

• TAM: $9-10B (CoreCard <1% penetration)

• Accretive year 1

• Value: $22/share

2️⃣ Stablecoins Q1 2026

• Fireblocks partnership announced Q3 call

• "4 billion bank accounts, 638K locations = unmatched crypto on/off-ramp"

• Nobody has this modeled

• Potential: $6-18/share

3️⃣ Dandelion B2B scaling

• New partnerships: Citibank Commonwealth Bank

• Banks want cross-border pipes, $EEFT provides wholesale infrastructure

• High-margin recurring revenue

THE VALUATION IS INSANE:

• $EEFT: 12.1x P/E

• Fiserv: 19.5x | FIS: 15.2x | Global Payments: 12.8x

• That's a 38-46% discount despite:

- SUPERIOR margin expansion ( 100bps vs. peers flat)

- MORE catalysts (CoreCard, stablecoins, digital)

- Comparable revenue growth

• Market thinks "dying ATM company" (ATMs = only 31% of revenue)

• Reality: fintech platform executing digital transformation

THE MATH: $82 → $165 = 101% UPSIDE

• $33 baseline EPS growth to $12.56 @ 13x P/E

• $22 CoreCard (vote imminent)

• $24 Money Transfer digital stablecoins

• $16 epay margin expansion

• $6 new stablecoin catalyst

• -$18 risk discount

WHY NOW:

• Management maintained 12-16% EPS guidance (Q3 = temporary, not structural)

• Everyone's panicking → valuation 5% CHEAPER

• THREE near-term catalysts about to hit (CoreCard vote this week!)

MY POSITION:

• BUY: $78-85

• Target: $165 ( 101%)

• Stop: $70 (-15%)

• Horizon: 24-30 months

• Risk/reward: 3.2:1

This is how you find 3-baggers: when they're hated at the bottom, not loved at the top.

Quality company temporary headwind stupid valuation catalysts loading = opportunity.

Tell me why I'm wrong 👇

1

3

7

967

23 Oct 2025

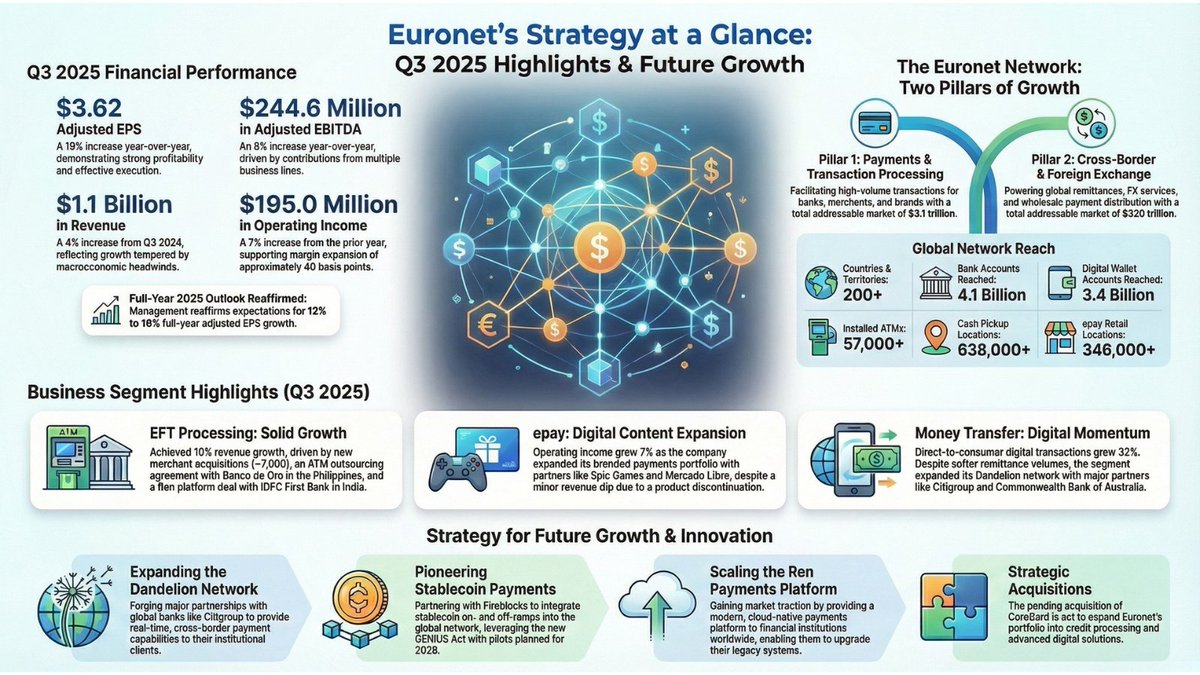

$EEFT earnings:

Euronet: Strong Bottom Line and Reaffirmed Guidance Overshadow Softer Revenue

Euronet delivered a mixed but ultimately positive quarter. The company posted strong 19% adjusted EPS growth, beating internal expectations and leading to a confident reaffirmation of its full-year 12-16% earnings growth guidance.

Bulls will focus on this bottom-line execution and the reaffirmed outlook as proof of management’s ability to navigate a tough environment.

However, bears will point to the significant slowdown in top-line growth, with consolidated revenue up only 1% on a constant currency basis, and a surprising dip in profitability for the key Money Transfer segment.

Overall, the bull case appears stronger as long as management continues to deliver on the bottom line and reaffirms its long-term growth story.

Themes, Drivers, and Concerns

Themes

🟢 Strategic Shift to Digital Continues: Management continues to highlight progress in its digital transformation, emphasizing Ren deployments, Dandelion sales momentum, and the pending CoreCard acquisition. The strong 32% growth in Money Transfer digital transactions underscores that this shift is bearing fruit where it matters most for future growth.

Drivers

🟢 EFT Segment Rebounds: After a flat Q2 that raised concerns, the EFT segment’s growth “restored itself” as management predicted. Operating income grew 9% (4% constant currency), driven by expansion in banking services and merchant acquiring, alleviating a key concern from the previous quarter.

🟢 Strong Bottom-Line Execution: Despite acknowledging that revenues were softer than anticipated due to macro pressures, the company delivered impressive 19% adjusted EPS growth. This suggests disciplined cost management and a focus on profitability, which is a significant positive in the current economic environment.

🟡 epay Focuses on Profitability: The segment’s revenue declined 5% in constant currency due to the discontinuation of a low-margin product in the U.S. However, operating income and adjusted EBITDA grew. This trade-off of unprofitable revenue for better earnings is a positive strategic move.

Concerns

🔴 Consolidated Revenue Slowdown: Top-line growth was muted at just 1% on a constant currency basis. The CEO explicitly stated they “anticipated more robust revenues,” citing “stronger economic and immigration pressure across the globe.” This macro impact is the most significant new concern this quarter.

🔴 Money Transfer Profitability Dips: Following an exceptional Q2 with 33% operating income growth, the Money Transfer segment saw a surprising 2% decline in constant currency operating income in Q3. While revenue grew slightly and digital transactions surged, management attributed the dip to investments in digital and Dandelion products. This sharp deceleration raises questions about the segment’s near-term margin profile.

🟡 Persistent Macro Headwinds: The “economic and immigration pressure” mentioned by the CEO materialised this quarter, impacting revenues. These external factors, which were noted as a risk last quarter, are now having a tangible effect on the top line and remain a key uncertainty.

Main Questions for the Earnings Call

Revenue Headwinds: You mentioned anticipating more robust revenues. Could you quantify the impact of the “economic and immigration pressure” and specify which segments or geographies were most affected?

Money Transfer Margins: The Money Transfer segment’s operating income declined on a constant currency basis. Can you detail the specific investments made this quarter and clarify if this profitability level is a temporary dip or a new baseline?

Guidance Confidence: What gives you the confidence to reaffirm the full-year 12-16% adjusted EPS growth guidance, given the softer top line in Q3? Does this imply significant margin expansion or a very strong Q4 performance?

Balance Sheet & Capital Allocation: With the $1B convertible debt offering completed and 1.3 million shares repurchased, how are you thinking about capital allocation priorities—specifically further buybacks vs. M&A—heading into 2026?

3

763

16 Oct 2025

REN Corecard is a $140m revenue business (at high margin) growing at 40% per year? $EEFT

30 Sep 2025

"REN doing $55M of revenue with 65% operating margins, growing 40% y/y."

1

9

3,889