Exclusive: Sen. Tom Cotton is urging the Treasury to investigate Airwallex, pushing for potential divestitures by Tencent and Hongshan (formerly sequoia capital China) axios.com/pro/all-deals/2026…

260

What type of accounting/finance project do you want to work on next?

📈 IPO readiness

🚀 AI adoption & readiness

🤝 Mergers & acquisitions

🧩 Carve-outs / divestitures

💡 System implementations

At Siegfried, we care about the work that interests you: hubs.ly/Q04jbjRh0

1

8

Most first-time buyers look for the perfect acquisition.

The best acquirers don't.

They build a system.

Research shows "serial acquirers"—companies that make acquisitions repeatedly—outperform one-time buyers over the long run.

Why?

They don't swing for the fences.

They buy smaller targets.

They preserve cash.

They stay disciplined.

They learn from each deal.

Danaher made more than 60 acquisitions and divestitures over a decade.

Not because they were smarter.

Because they treated M&A like a process, not an event.

That's a lesson every SMB buyer should remember:

Your first deal shouldn't be your last deal.

Build a machine, not a trophy.

15

16h

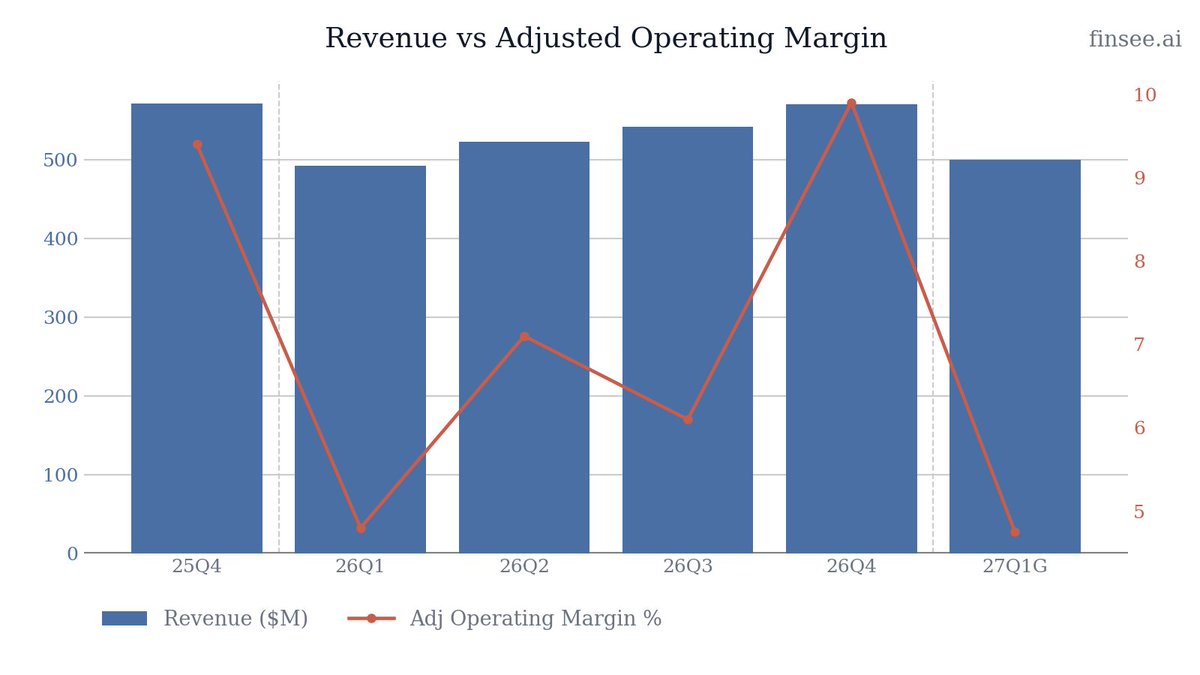

$LZB Q4 2026 earnings: A Strong Headline Built on Two Things That Won't Repeat

*** Updated after the call:

La-Z-Boy posted flat Q4 sales but the headline looked great: adjusted operating margin up 50 bps to 9.9% and adjusted EPS of $1.26, up 37%. Look closer. A full 100 bps of that margin came from a one-time inventory and pricing benefit in the casegoods business it just sold, and EPS included $0.16 from favorable discrete tax items. Strip both out and core margin actually fell roughly 60 bps. The real story is a Retail engine that keeps gaining share through acquisitions while same-store demand stays negative, and a Q1 guide that resets margin back to ~4.75%.

Full article with charts - link in bio

🐂 𝗕𝘂𝗹𝗹 𝗖𝗮𝘀𝗲

𝗥𝗲𝘁𝗮𝗶𝗹 𝗦𝗵𝗮𝗿𝗲 𝗚𝗮𝗶𝗻𝘀 𝗔𝗿𝗲 𝗥𝗲𝗮𝗹: Retail delivered sales rose 9% and written sales 11%, lifting company-owned stores to 230 of 378 (61% of the network, an all-time high). Management opened 15 new and acquired 15 stores in FY26, both company records, with another 3-store deal closing in June.

𝗦𝗲𝗹𝗳-𝗙𝘂𝗻𝗱𝗲𝗱 𝗧𝗵𝗿𝗼𝘂𝗴𝗵 𝘁𝗵𝗲 𝗗𝗼𝘄𝗻𝘁𝘂𝗿𝗻: Operating cash flow hit $204M ( 9%), with $303M cash and zero debt. The board authorized a new $300M buyback, ~20% of shares, alongside a fifth straight year of 10% dividend hikes.

🐻 𝗕𝗲𝗮𝗿 𝗖𝗮𝘀𝗲

𝗨𝗻𝗱𝗲𝗿𝗹𝘆𝗶𝗻𝗴 𝗗𝗲𝗺𝗮𝗻𝗱 𝗜𝘀 𝗦𝘁𝗶𝗹𝗹 𝗡𝗲𝗴𝗮𝘁𝗶𝘃𝗲: Retail written same-store sales fell 2% in Q4 and 3% for the year. All segment growth is coming from acquired and new stores, not organic consumer demand, which management itself calls 'choppy.'

𝗧𝗵𝗲 𝗠𝗮𝗿𝗴𝗶𝗻 𝗕𝗲𝗮𝘁 𝗜𝘀𝗻'𝘁 𝗥𝗲𝗽𝗲𝗮𝘁𝗮𝗯𝗹𝗲: Management explicitly flagged the casegoods margin benefit as non-repeatable after the May divestiture, and Q4 EPS leaned on a low 21.5% tax rate. Q1 FY27 adjusted margin is guided back down to 4.0-5.5%.

⚖️ 𝗩𝗲𝗿𝗱𝗶𝗰𝘁

⚪ Neutral. The Retail expansion strategy is executing well and the balance sheet is a genuine strength, but the flattering Q4 headline masks a core margin that declined and demand that remains negative once acquisitions are excluded. Quality of the beat, not the strategy, caps the grade.

— • — • —

𝗧𝗵𝗲𝗺𝗲𝘀

New: 🔴 𝗧𝗵𝗲 𝗤𝟰 𝗠𝗮𝗿𝗴𝗶𝗻 𝗕𝗲𝗮𝘁 𝗖𝗮𝗺𝗲 𝗙𝗿𝗼𝗺 𝗜𝘁𝗲𝗺𝘀 𝗧𝗵𝗮𝘁 𝗦𝘁𝗼𝗽

Management was unusually direct: the casegoods business delivered ~100 bps of consolidated adjusted margin from favorable inventory adjustments and pricing ahead of its sale, and the CFO called this 'non-repeatable.' When pressed by an analyst, the CFO effectively confirmed core EBIT margin would have been near 8.8% versus 9.4% a year earlier, i.e. down. The over-delivery versus the 7.5-9.0% guide was a one-timer, not a step-change in profitability.

🟢 𝗥𝗲𝘁𝗮𝗶𝗹 𝗘𝘅𝗽𝗮𝗻𝘀𝗶𝗼𝗻 𝗜𝘀 𝘁𝗵𝗲 𝗪𝗵𝗼𝗹𝗲 𝗚𝗿𝗼𝘄𝘁𝗵 𝗦𝘁𝗼𝗿𝘆

Retail is doing the heavy lifting: FY26 added the most new stores (15) and the most acquisitions (15) in company history, taking company-owned ownership from 45% to 61% of the network over five years. Management sees runway to 450 total stores (from 378) at ~10 openings a year. These deals are immediately sales- and profit-accretive, which is how the company grows while the industry shrinks low-to-mid single digits.

🔴 𝗢𝗿𝗴𝗮𝗻𝗶𝗰 𝗗𝗲𝗺𝗮𝗻𝗱 𝗛𝗮𝘀𝗻'𝘁 𝗧𝘂𝗿𝗻𝗲𝗱

The gap between total written sales ( 11%) and same-store written sales (-2%) is the core tension: take away M&A and the consumer base is still shrinking. Management points to late-quarter positives, with April and May comps turning positive and a solid Memorial Day, but full-year same-store written sales were -3% and the CFO concedes deleverage from negative comps is still pressuring core profitability. A genuine inflection requires same-store sales to turn positive, which has not yet happened on a full-quarter basis.

🔴 𝗝𝗼𝘆𝗯𝗶𝗿𝗱 𝗞𝗲𝗲𝗽𝘀 𝗦𝗶𝗻𝗸𝗶𝗻𝗴, 𝗡𝗼𝘄 𝗧𝗿𝗶𝗴𝗴𝗲𝗿𝘀 𝗮𝗻 𝗜𝗺𝗽𝗮𝗶𝗿𝗺𝗲𝗻𝘁

Joybird delivered sales fell 10% in Q4 and 10% for the year to $130.8M, and the segment took a $20.0M non-cash goodwill impairment, writing the reporting unit down from $55.4M to $35.5M. The digitally native, younger consumer remains 'particularly volatile.' Management is responding by folding Joybird manufacturing into existing La-Z-Boy plants in FY27 to right-size the cost base, an admission the current structure is too heavy for the demand it is seeing.

New: ⚪ 𝗜𝗻𝗽𝘂𝘁 𝗖𝗼𝘀𝘁 𝗜𝗻𝗳𝗹𝗮𝘁𝗶𝗼𝗻 𝗥𝗲𝘁𝘂𝗿𝗻𝘀, 𝗣𝗿𝗶𝗰𝗶𝗻𝗴 𝗟𝗮𝗴𝘀

After several quarters of benign costs, the CFO flagged renewed inflation tied to petroleum and poly (foam) suppliers. Management deliberately chose to absorb it in Q1 FY27 to maximize summer selling-season demand rather than price ahead of it, taking only 'very nominal' pricing effective Q2 onward. There is no supply risk, but the decision to eat costs near-term is part of why Q1 margin guidance is soft.

⚪ 𝗣𝗼𝗿𝘁𝗳𝗼𝗹𝗶𝗼 𝗖𝗹𝗲𝗮𝗻𝘂𝗽 𝗟𝗮𝗿𝗴𝗲𝗹𝘆 𝗙𝗶𝗻𝗶𝘀𝗵𝗲𝗱

The multi-year simplification is now essentially complete: the U.K. manufacturing restructuring finalized in April, and the American Drew and Kincaid wholesale casegoods businesses (~$60M annual sales) were sold in May. Next up is consolidating the two smallest upholstery plants, including all Joybird manufacturing, into the larger U.S. network during FY27. These add modest friction costs but are intended to support the long-term double-digit wholesale margin goal.

⚪ 𝗗𝗶𝘀𝘁𝗿𝗶𝗯𝘂𝘁𝗶𝗼𝗻 𝗧𝗿𝗮𝗻𝘀𝗳𝗼𝗿𝗺𝗮𝘁𝗶𝗼𝗻 𝗡𝗼𝘄 𝗶𝗻 𝗬𝗲𝗮𝗿 𝗧𝘄𝗼 𝗼𝗳 𝗙𝗼𝘂𝗿

The project consolidating 15 distribution centers into 3 centralized hubs completed its western phase (Arizona) and is mid-way through the Midwest and East. Management frames years one and two as roughly equivalent in friction cost, turning break-even-to-positive in year three, with the full 50-75 bps wholesale margin benefit landing in year four. It targets 30% less square footage and 20% less heavy-furniture mileage. This is a real but back-loaded margin lever.

New: ⚪ 𝗣𝗿𝗼𝗱𝘂𝗰𝘁 𝗜𝗻𝗻𝗼𝘃𝗮𝘁𝗶𝗼𝗻 𝗔𝗶𝗺𝗲𝗱 𝗮𝘁 𝗬𝗼𝘂𝗻𝗴𝗲𝗿 𝗮𝗻𝗱 𝗣𝗿𝗲𝗺𝗶𝘂𝗺 𝗕𝘂𝘆𝗲𝗿𝘀

At High Point Market the company launched AudioLuxe, a premium audio-furniture line built with Klipsch, arriving in stores this fall, and Comfort Essentials, an opening-price-point stationary line targeting value-focused and younger first-time buyers. Both directly address the bifurcated consumer: capturing high-ticket design buyers while giving aspirational shoppers an accessible entry point to the brand.

⚪ 𝗧𝗮𝗿𝗶𝗳𝗳 𝗥𝗲𝗳𝘂𝗻𝗱 𝗣𝗿𝗼𝗰𝗲𝘀𝘀 𝗨𝗻𝗱𝗲𝗿𝘄𝗮𝘆

With ~90% of upholstery produced in the U.S., La-Z-Boy is relatively insulated from tariffs, a structural advantage versus importers. Management noted it is applying for refunds of IEEPA tariffs through the standard CBP system and will assess next steps, a small potential upside rather than a headwind for this business.

— • — • —

𝗢𝘁𝗵𝗲𝗿 𝗞𝗣𝗜𝘀

𝗪𝗵𝗼𝗹𝗲𝘀𝗮𝗹𝗲 𝗔𝗱𝗷𝘂𝘀𝘁𝗲𝗱 𝗢𝗽𝗲𝗿𝗮𝘁𝗶𝗻𝗴 𝗠𝗮𝗿𝗴𝗶𝗻 (𝗙𝗬𝟮𝟲 𝗤𝟰): 𝟭𝟬.𝟭%

Up from 8.5% a year ago, but 150 bps of that came from the casegoods inventory and pricing benefit before the divestiture, which the CFO labeled non-repeatable. Underlying wholesale was pressured by distribution-transformation friction costs and softer industry volume (delivered sales -2%). The clean run-rate is closer to the high-8% range seen earlier in the year, not 10%.

𝗙𝗿𝗲𝗲 𝗖𝗮𝘀𝗵 𝗙𝗹𝗼𝘄 (𝗙𝗬𝟮𝟲): $𝟭𝟮𝟳.𝟴 𝗺𝗶𝗹𝗹𝗶𝗼𝗻

Up from $113.0M in FY25, with operating cash flow of $204M ( 9%) against $76M of capex. A 14% reduction in inventories ($218M vs $255M) was a meaningful working-capital tailwind. FCF comfortably funded the $86M of acquisitions, $38M of dividends, and $47M of buybacks while cash ended at $303M with no debt. Note capex is guided to rise to $90-110M in FY27.

𝗚𝗔𝗔𝗣 𝗘𝗳𝗳𝗲𝗰𝘁𝗶𝘃𝗲 𝗧𝗮𝘅 𝗥𝗮𝘁𝗲 (𝗙𝗬𝟮𝟲 𝗤𝟰): 𝟮𝟭.𝟱%

Well below the normalized 26-27% the company guides to, and the source of the $0.16 discrete-item benefit baked into both GAAP and adjusted Q4 EPS. For the full year the rate was 25.9% versus 31.4% in FY25, the prior year having been inflated by the non-deductible U.K. goodwill impairment. Investors should normalize Q4 EPS down for this tax tailwind.

— • — • —

𝗚𝘂𝗶𝗱𝗮𝗻𝗰𝗲

𝗙𝗬𝟮𝟳 𝗤𝟭 𝗦𝗮𝗹𝗲𝘀: $𝟰𝟵𝟬 - $𝟱𝟭𝟬 𝗺𝗶𝗹𝗹𝗶𝗼𝗻

Decelerating on a reported basis. The $500M midpoint is 1.6% versus Q1 FY26's $492M, with organic growth guided to 'up to 4%' (excluding acquisitions and divestitures). The reported-versus-organic gap reflects the loss of ~$60M annual casegoods sales now exiting the base. Q1 is seasonally the weakest quarter due to lower industry sales and the annual week-long plant shutdown.

𝗙𝗬𝟮𝟳 𝗤𝟭 𝗔𝗱𝗷𝘂𝘀𝘁𝗲𝗱 𝗢𝗽𝗲𝗿𝗮𝘁𝗶𝗻𝗴 𝗠𝗮𝗿𝗴𝗶𝗻: 𝟰.𝟬% - 𝟱.𝟱%

Reversing sharply lower from Q4's 9.9%, though that comparison is distorted by seasonality and the casegoods one-timer. Against the more relevant prior-year base, the 4.75% midpoint is roughly flat to Q1 FY26's 4.8%. Management cites absorbed input-cost inflation, choppy wholesale demand, and plant-consolidation friction as near-term headwinds it views as short-term.

𝗙𝗬𝟮𝟳 𝗖𝗮𝗽𝗶𝘁𝗮𝗹 𝗘𝘅𝗽𝗲𝗻𝗱𝗶𝘁𝘂𝗿𝗲𝘀: $𝟵𝟬 - $𝟭𝟭𝟬 𝗺𝗶𝗹𝗹𝗶𝗼𝗻

Up from $76M spent in FY26, directed at the distribution and home-delivery transformation, manufacturing investments, and new stores and remodels. At the midpoint of OCF historically near $200M, this still leaves ample room for the company's stated 50/50 split between reinvestment and shareholder returns.

𝗙𝗬𝟮𝟳 𝗡𝗲𝘄 𝗦𝘁𝗼𝗿𝗲 𝗢𝗽𝗲𝗻𝗶𝗻𝗴𝘀: ~𝟭𝟬 𝗟𝗮-𝗭-𝗕𝗼𝘆 𝟯-𝟰 𝗝𝗼𝘆𝗯𝗶𝗿𝗱

Stable pace versus the ~10 going-forward cadence, below FY26's record 15 new plus 15 acquired. Management will continue pursuing independent acquisitions opportunistically, framing them as the best use of cash given they are immediately accretive. A 3-store Florida/Alabama acquisition is expected to close at the end of June.

— • — • —

𝗞𝗲𝘆 𝗤𝘂𝗲𝘀𝘁𝗶𝗼𝗻𝘀

𝗪𝗵𝗮𝘁 𝗜𝘀 𝘁𝗵𝗲 𝗖𝗹𝗲𝗮𝗻 𝗪𝗵𝗼𝗹𝗲𝘀𝗮𝗹𝗲 𝗠𝗮𝗿𝗴𝗶𝗻 𝗥𝘂𝗻-𝗥𝗮𝘁𝗲?

With 150 bps of the Q4 wholesale margin tied to a non-repeatable casegoods benefit and the casegoods business now sold, what should investors model as the underlying wholesale margin entering FY27, before the year-three distribution savings arrive?

𝗪𝗵𝗲𝗻 𝗗𝗼 𝗦𝗮𝗺𝗲-𝗦𝘁𝗼𝗿𝗲 𝗦𝗮𝗹𝗲𝘀 𝗧𝘂𝗿𝗻 𝗣𝗼𝘀𝗶𝘁𝗶𝘃𝗲 𝗳𝗼𝗿 𝗮 𝗙𝘂𝗹𝗹 𝗤𝘂𝗮𝗿𝘁𝗲𝗿?

April and May comps turned positive, but full-quarter same-store written sales have been negative all year. What gives confidence that the recent strength is a trend rather than tentpole-event timing, and what is the organic inflection assumption embedded in the 'up to 4%' Q1 organic guide?

𝗪𝗵𝗮𝘁 𝗜𝘀 𝘁𝗵𝗲 𝗣𝗮𝘁𝗵 𝘁𝗼 𝗝𝗼𝘆𝗯𝗶𝗿𝗱 𝗣𝗿𝗼𝗳𝗶𝘁𝗮𝗯𝗶𝗹𝗶𝘁𝘆?

After a $20M goodwill impairment and a fourth straight year of weakness, what specific revenue and cost milestones must Joybird hit, and by when, before management would consider further strategic action rather than continued investment?

𝗛𝗼𝘄 𝗠𝘂𝗰𝗵 𝗜𝗻𝗽𝘂𝘁-𝗖𝗼𝘀𝘁 𝗜𝗻𝗳𝗹𝗮𝘁𝗶𝗼𝗻 𝗜𝘀 𝗕𝗲𝗶𝗻𝗴 𝗗𝗲𝗳𝗲𝗿𝗿𝗲𝗱?

Management chose to absorb poly and petroleum-linked inflation in Q1 and take only nominal pricing from Q2. How large is the cumulative cost pressure, and is the 'very nominal' pricing sufficient to recover it without denting the demand the strategy is meant to protect?

𝗪𝗵𝗮𝘁 𝗔𝗿𝗲 𝘁𝗵𝗲 𝗤𝘂𝗮𝗻𝘁𝗶𝗳𝗶𝗲𝗱 𝗙𝗬𝟮𝟳 𝗠𝗮𝗿𝗴𝗶𝗻 𝗕𝗿𝗶𝗱𝗴𝗲𝘀?

Management referenced being 'halfway' to the long-term double-digit margin goal through self-help, with the rest requiring industry recovery. Can the plant-consolidation and distribution savings be sized for FY27 specifically, so investors can separate controllable margin gains from macro-dependent ones?

Jun 16

$LZB Q4 2026 earnings: Margin Expansion Driven by Divestitures, Not Just Operations

La-Z-Boy delivered flat YoY sales of $570M for Q4, yet posted a massive 37% jump in adjusted EPS to $1.26. The headline Adjusted Operating Margin of 9.9% looks stellar, but it was artificially boosted by a 150-basis-point benefit from favorable inventory adjustments in the soon-to-be-divested casegoods business. The core growth narrative relies almost entirely on inorganic store acquisitions, which are masking a persistent decline in organic same-store sales. Meanwhile, a $20M goodwill impairment on the digitally native Joybird segment highlights the limits of the company's tech-forward DTC strategy. A new $300M buyback authorization signals management's confidence, but Q1 FY27 guidance warns of steep seasonal deceleration.

Full article with charts - link in bio

🐂 𝐁𝐮𝐥𝐥 𝐂𝐚𝐬𝐞

• 𝐀𝐠𝐠𝐫𝐞𝐬𝐬𝐢𝐯𝐞 𝐑𝐞𝐭𝐚𝐢𝐥 𝐅𝐨𝐨𝐭𝐩𝐫𝐢𝐧𝐭 𝐂𝐨𝐧𝐭𝐫𝐨𝐥 — The company successfully integrated 15 acquired stores and opened 15 new locations in FY26, bringing the company-owned share of its network to a record 61%. This structural shift captures retail markup and drives the 13.9% Retail Adjusted Operating Margin.

• 𝐂𝐥𝐞𝐚𝐧𝐞𝐝 𝐔𝐩 𝐏𝐨𝐫𝐭𝐟𝐨𝐥𝐢𝐨 — Exiting the American Drew and Kincaid wholesale casegoods businesses and restructuring the UK supply chain immediately removes structural margin drags, allowing laser focus on the highly profitable North American upholstery core.

🐻 𝐁𝐞𝐚𝐫 𝐂𝐚𝐬𝐞

• 𝐎𝐫𝐠𝐚𝐧𝐢𝐜 𝐃𝐞𝐦𝐚𝐧𝐝 𝐑𝐞𝐦𝐚𝐢𝐧𝐬 𝐍𝐞𝐠𝐚𝐭𝐢𝐯𝐞 — Total Retail segment sales rose 9%, but same-store written sales fell 2%. The company is buying growth to offset a stubbornly weak consumer, which deleverages fixed costs on the legacy store base.

• 𝐉𝐨𝐲𝐛𝐢𝐫𝐝 𝐕𝐚𝐥𝐮𝐞 𝐃𝐞𝐬𝐭𝐫𝐮𝐜𝐭𝐢𝐨𝐧 — The $20M goodwill impairment on Joybird confirms the digitally-native brand is failing to navigate the current macro environment. Delivered sales plummeted another 10% this quarter.

⚖️ 𝐕𝐞𝐫𝐝𝐢𝐜𝐭: ⚪

Neutral. Management is executing a textbook portfolio optimization and capital return strategy, but underlying organic consumer demand remains definitively weak. The Q4 margin pop is heavily influenced by one-time divestiture dynamics.

𝐊𝐞𝐲 𝐓𝐡𝐞𝐦𝐞𝐬

🟢 𝐑𝐞𝐭𝐚𝐢𝐥 𝐀𝐜𝐪𝐮𝐢𝐬𝐢𝐭𝐢𝐨𝐧 𝐒𝐩𝐫𝐞𝐞 𝐑𝐞𝐬𝐜𝐮𝐞𝐬 𝐓𝐨𝐩 𝐋𝐢𝐧𝐞

The Retail segment was the sole engine for revenue stability, growing delivered sales by 9% to $270M. This was entirely engineered via the 'Century Vision' strategy of acquiring independent stores (15 added) and opening new ones (15 added). By shifting to a 61% company-owned model, La-Z-Boy is successfully capturing the retail margin spread.

⚪ 𝐂𝐚𝐬𝐞𝐠𝐨𝐨𝐝𝐬 𝐃𝐢𝐯𝐞𝐬𝐭𝐢𝐭𝐮𝐫𝐞 𝐒𝐩𝐢𝐤𝐞𝐬 𝐖𝐡𝐨𝐥𝐞𝐬𝐚𝐥𝐞 𝐌𝐚𝐫𝐠𝐢𝐧 [NEW]

The Wholesale segment reported a stunning adjusted operating margin of 10.1% (up from 8.5%). However, management explicitly noted that 150 basis points of this improvement came from favorable inventory adjustments and pricing ahead of the American Drew and Kincaid divestitures. Investors should temper expectations for the go-forward run rate of the core upholstery wholesale business.

⚪ 𝐃𝐢𝐬𝐭𝐫𝐢𝐛𝐮𝐭𝐢𝐨𝐧 𝐓𝐫𝐚𝐧𝐬𝐟𝐨𝐫𝐦𝐚𝐭𝐢𝐨𝐧 𝐒𝐪𝐮𝐞𝐞𝐳𝐢𝐧𝐠 𝐂𝐨𝐬𝐭𝐬

The multi-year supply chain transformation is advancing. After launching the Western U. S. centralized hub in Arizona, the company is systematically reducing its footprint from 15 regional centers to 3 major hubs. This is targeted to cut inventory mileage by 20% and eventually deliver 50-75 bps of permanent enterprise margin improvement.

🔴 𝐈𝐧𝐨𝐫𝐠𝐚𝐧𝐢𝐜 𝐆𝐫𝐨𝐰𝐭𝐡 𝐌𝐚𝐬𝐤𝐬 𝐎𝐫𝐠𝐚𝐧𝐢𝐜 𝐂𝐨𝐧𝐭𝐫𝐚𝐜𝐭𝐢𝐨𝐧

Despite management praising 11% written sales growth in the Retail segment, the underlying data contradicts the rosy narrative: same-store written sales were down 2%. This marks the fourth consecutive quarter of negative organic sales (-4% in Q1, -2% in Q2, -4% in Q3, -2% in Q4). The company is masking foot traffic weakness by simply buying more stores.

🔴🔴 𝐉𝐨𝐲𝐛𝐢𝐫𝐝'𝐬 𝐃𝐓𝐂 𝐌𝐨𝐝𝐞𝐥 𝐇𝐢𝐭𝐬 𝐚 𝐖𝐚𝐥𝐥 [NEW]

The digitally-native, tech-forward Joybird segment completely reversed course, resulting in a $20M GAAP goodwill impairment. Delivered sales fell 10% to $32M, and expense deleveraging widened the operating loss. The younger, urban-focused DTC model has proven highly vulnerable to the current macroeconomic cycle, forcing La-Z-Boy to reconsider the segment's carrying value.

🔴 𝐌𝐚𝐜𝐫𝐨 𝐒𝐨𝐟𝐭𝐧𝐞𝐬𝐬 𝐃𝐢𝐜𝐭𝐚𝐭𝐞𝐬 𝐐𝟏 𝐆𝐮𝐢𝐝𝐚𝐧𝐜𝐞

Management continues to cite a 'measured view of the external environment' and an 'industry that remains soft.' Elevated mortgage rates and crushed housing turnover continue to depress organic foot traffic, leaving the company heavily reliant on internal self-help mechanisms to protect earnings.

𝐎𝐭𝐡𝐞𝐫 𝐊𝐏𝐈𝐬

𝐎𝐩𝐞𝐫𝐚𝐭𝐢𝐧𝐠 𝐂𝐚𝐬𝐡 𝐅𝐥𝐨𝐰 (𝐅𝐘𝟐𝟔): $204.1 million

Stable and accelerating. Up 9% from $187.3M in the prior year. Strong working capital management allowed La-Z-Boy to generate robust cash despite flat top-line sales, easily funding $163M in acquisitions and capex.

𝐂𝐚𝐩𝐢𝐭𝐚𝐥 𝐑𝐞𝐭𝐮𝐫𝐧𝐬: $85 million

Reversing prior conservative guidance. After stating in Q1 that FY26 capital allocation would prioritize business investment over share repurchases, the company ended up buying back $47M in stock. The Board just authorized a massive new $300M repurchase program, signaling a sharp pivot back to aggressive capital returns.

𝐆𝐮𝐢𝐝𝐚𝐧𝐜𝐞

𝟐𝟕𝐐𝟏 𝐑𝐞𝐯𝐞𝐧𝐮𝐞: $490 - $510 million

Decelerating sequentially but stable YoY. The $500M midpoint implies a 12% drop from Q4's $570M due to normal seasonality (annual plant shutdowns), but represents a modest 1.6% organic growth versus the $492M reported in 26Q1.

𝟐𝟕𝐐𝟏 𝐀𝐝𝐣𝐮𝐬𝐭𝐞𝐝 𝐎𝐩𝐞𝐫𝐚𝐭𝐢𝐧𝐠 𝐌𝐚𝐫𝐠𝐢𝐧: 4.0% - 5.5%

Decelerating. A sharp sequential drop from Q4's 9.9%, driven by the seasonal volume dip that deleverages fixed costs across the newly expanded company-owned store network. The 4.75% midpoint is effectively flat compared to the 4.8% posted in 26Q1.

𝐊𝐞𝐲 𝐐𝐮𝐞𝐬𝐭𝐢𝐨𝐧𝐬

𝐉𝐨𝐲𝐛𝐢𝐫𝐝'𝐬 𝐏𝐚𝐭𝐡 𝐭𝐨 𝐏𝐫𝐨𝐟𝐢𝐭𝐚𝐛𝐢𝐥𝐢𝐭𝐲

Given the $20M goodwill impairment and ongoing double-digit declines in delivered sales, is Joybird still considered a core component of the 'Century Vision', or is management exploring strategic alternatives for this segment?

𝐍𝐨𝐫𝐦𝐚𝐥𝐢𝐳𝐞𝐝 𝐖𝐡𝐨𝐥𝐞𝐬𝐚𝐥𝐞 𝐌𝐚𝐫𝐠𝐢𝐧𝐬

With 150 basis points of Q4 Wholesale margin driven by favorable casegoods inventory adjustments prior to divestiture, what is the normalized baseline operating margin expectation for the core upholstery wholesale business heading into FY27?

𝐏𝐚𝐜𝐞 𝐨𝐟 𝐭𝐡𝐞 𝐍𝐞𝐰 𝐁𝐮𝐲𝐛𝐚𝐜𝐤 𝐏𝐫𝐨𝐠𝐫𝐚𝐦

The Board approved a $300M share repurchase program after management previously telegraphed a shift toward reinvestment. Does this size indicate a lack of attractive independent store acquisition targets, or purely a view that LZB shares are currently undervalued?

2

2

1,041

El Coyotl | 🐺📈 retweeted

Jun 16

$LZB Q4 2026 earnings: Margin Expansion Driven by Divestitures, Not Just Operations

La-Z-Boy delivered flat YoY sales of $570M for Q4, yet posted a massive 37% jump in adjusted EPS to $1.26. The headline Adjusted Operating Margin of 9.9% looks stellar, but it was artificially boosted by a 150-basis-point benefit from favorable inventory adjustments in the soon-to-be-divested casegoods business. The core growth narrative relies almost entirely on inorganic store acquisitions, which are masking a persistent decline in organic same-store sales. Meanwhile, a $20M goodwill impairment on the digitally native Joybird segment highlights the limits of the company's tech-forward DTC strategy. A new $300M buyback authorization signals management's confidence, but Q1 FY27 guidance warns of steep seasonal deceleration.

Full article with charts - link in bio

🐂 𝐁𝐮𝐥𝐥 𝐂𝐚𝐬𝐞

• 𝐀𝐠𝐠𝐫𝐞𝐬𝐬𝐢𝐯𝐞 𝐑𝐞𝐭𝐚𝐢𝐥 𝐅𝐨𝐨𝐭𝐩𝐫𝐢𝐧𝐭 𝐂𝐨𝐧𝐭𝐫𝐨𝐥 — The company successfully integrated 15 acquired stores and opened 15 new locations in FY26, bringing the company-owned share of its network to a record 61%. This structural shift captures retail markup and drives the 13.9% Retail Adjusted Operating Margin.

• 𝐂𝐥𝐞𝐚𝐧𝐞𝐝 𝐔𝐩 𝐏𝐨𝐫𝐭𝐟𝐨𝐥𝐢𝐨 — Exiting the American Drew and Kincaid wholesale casegoods businesses and restructuring the UK supply chain immediately removes structural margin drags, allowing laser focus on the highly profitable North American upholstery core.

🐻 𝐁𝐞𝐚𝐫 𝐂𝐚𝐬𝐞

• 𝐎𝐫𝐠𝐚𝐧𝐢𝐜 𝐃𝐞𝐦𝐚𝐧𝐝 𝐑𝐞𝐦𝐚𝐢𝐧𝐬 𝐍𝐞𝐠𝐚𝐭𝐢𝐯𝐞 — Total Retail segment sales rose 9%, but same-store written sales fell 2%. The company is buying growth to offset a stubbornly weak consumer, which deleverages fixed costs on the legacy store base.

• 𝐉𝐨𝐲𝐛𝐢𝐫𝐝 𝐕𝐚𝐥𝐮𝐞 𝐃𝐞𝐬𝐭𝐫𝐮𝐜𝐭𝐢𝐨𝐧 — The $20M goodwill impairment on Joybird confirms the digitally-native brand is failing to navigate the current macro environment. Delivered sales plummeted another 10% this quarter.

⚖️ 𝐕𝐞𝐫𝐝𝐢𝐜𝐭: ⚪

Neutral. Management is executing a textbook portfolio optimization and capital return strategy, but underlying organic consumer demand remains definitively weak. The Q4 margin pop is heavily influenced by one-time divestiture dynamics.

𝐊𝐞𝐲 𝐓𝐡𝐞𝐦𝐞𝐬

🟢 𝐑𝐞𝐭𝐚𝐢𝐥 𝐀𝐜𝐪𝐮𝐢𝐬𝐢𝐭𝐢𝐨𝐧 𝐒𝐩𝐫𝐞𝐞 𝐑𝐞𝐬𝐜𝐮𝐞𝐬 𝐓𝐨𝐩 𝐋𝐢𝐧𝐞

The Retail segment was the sole engine for revenue stability, growing delivered sales by 9% to $270M. This was entirely engineered via the 'Century Vision' strategy of acquiring independent stores (15 added) and opening new ones (15 added). By shifting to a 61% company-owned model, La-Z-Boy is successfully capturing the retail margin spread.

⚪ 𝐂𝐚𝐬𝐞𝐠𝐨𝐨𝐝𝐬 𝐃𝐢𝐯𝐞𝐬𝐭𝐢𝐭𝐮𝐫𝐞 𝐒𝐩𝐢𝐤𝐞𝐬 𝐖𝐡𝐨𝐥𝐞𝐬𝐚𝐥𝐞 𝐌𝐚𝐫𝐠𝐢𝐧 [NEW]

The Wholesale segment reported a stunning adjusted operating margin of 10.1% (up from 8.5%). However, management explicitly noted that 150 basis points of this improvement came from favorable inventory adjustments and pricing ahead of the American Drew and Kincaid divestitures. Investors should temper expectations for the go-forward run rate of the core upholstery wholesale business.

⚪ 𝐃𝐢𝐬𝐭𝐫𝐢𝐛𝐮𝐭𝐢𝐨𝐧 𝐓𝐫𝐚𝐧𝐬𝐟𝐨𝐫𝐦𝐚𝐭𝐢𝐨𝐧 𝐒𝐪𝐮𝐞𝐞𝐳𝐢𝐧𝐠 𝐂𝐨𝐬𝐭𝐬

The multi-year supply chain transformation is advancing. After launching the Western U. S. centralized hub in Arizona, the company is systematically reducing its footprint from 15 regional centers to 3 major hubs. This is targeted to cut inventory mileage by 20% and eventually deliver 50-75 bps of permanent enterprise margin improvement.

🔴 𝐈𝐧𝐨𝐫𝐠𝐚𝐧𝐢𝐜 𝐆𝐫𝐨𝐰𝐭𝐡 𝐌𝐚𝐬𝐤𝐬 𝐎𝐫𝐠𝐚𝐧𝐢𝐜 𝐂𝐨𝐧𝐭𝐫𝐚𝐜𝐭𝐢𝐨𝐧

Despite management praising 11% written sales growth in the Retail segment, the underlying data contradicts the rosy narrative: same-store written sales were down 2%. This marks the fourth consecutive quarter of negative organic sales (-4% in Q1, -2% in Q2, -4% in Q3, -2% in Q4). The company is masking foot traffic weakness by simply buying more stores.

🔴🔴 𝐉𝐨𝐲𝐛𝐢𝐫𝐝'𝐬 𝐃𝐓𝐂 𝐌𝐨𝐝𝐞𝐥 𝐇𝐢𝐭𝐬 𝐚 𝐖𝐚𝐥𝐥 [NEW]

The digitally-native, tech-forward Joybird segment completely reversed course, resulting in a $20M GAAP goodwill impairment. Delivered sales fell 10% to $32M, and expense deleveraging widened the operating loss. The younger, urban-focused DTC model has proven highly vulnerable to the current macroeconomic cycle, forcing La-Z-Boy to reconsider the segment's carrying value.

🔴 𝐌𝐚𝐜𝐫𝐨 𝐒𝐨𝐟𝐭𝐧𝐞𝐬𝐬 𝐃𝐢𝐜𝐭𝐚𝐭𝐞𝐬 𝐐𝟏 𝐆𝐮𝐢𝐝𝐚𝐧𝐜𝐞

Management continues to cite a 'measured view of the external environment' and an 'industry that remains soft.' Elevated mortgage rates and crushed housing turnover continue to depress organic foot traffic, leaving the company heavily reliant on internal self-help mechanisms to protect earnings.

𝐎𝐭𝐡𝐞𝐫 𝐊𝐏𝐈𝐬

𝐎𝐩𝐞𝐫𝐚𝐭𝐢𝐧𝐠 𝐂𝐚𝐬𝐡 𝐅𝐥𝐨𝐰 (𝐅𝐘𝟐𝟔): $204.1 million

Stable and accelerating. Up 9% from $187.3M in the prior year. Strong working capital management allowed La-Z-Boy to generate robust cash despite flat top-line sales, easily funding $163M in acquisitions and capex.

𝐂𝐚𝐩𝐢𝐭𝐚𝐥 𝐑𝐞𝐭𝐮𝐫𝐧𝐬: $85 million

Reversing prior conservative guidance. After stating in Q1 that FY26 capital allocation would prioritize business investment over share repurchases, the company ended up buying back $47M in stock. The Board just authorized a massive new $300M repurchase program, signaling a sharp pivot back to aggressive capital returns.

𝐆𝐮𝐢𝐝𝐚𝐧𝐜𝐞

𝟐𝟕𝐐𝟏 𝐑𝐞𝐯𝐞𝐧𝐮𝐞: $490 - $510 million

Decelerating sequentially but stable YoY. The $500M midpoint implies a 12% drop from Q4's $570M due to normal seasonality (annual plant shutdowns), but represents a modest 1.6% organic growth versus the $492M reported in 26Q1.

𝟐𝟕𝐐𝟏 𝐀𝐝𝐣𝐮𝐬𝐭𝐞𝐝 𝐎𝐩𝐞𝐫𝐚𝐭𝐢𝐧𝐠 𝐌𝐚𝐫𝐠𝐢𝐧: 4.0% - 5.5%

Decelerating. A sharp sequential drop from Q4's 9.9%, driven by the seasonal volume dip that deleverages fixed costs across the newly expanded company-owned store network. The 4.75% midpoint is effectively flat compared to the 4.8% posted in 26Q1.

𝐊𝐞𝐲 𝐐𝐮𝐞𝐬𝐭𝐢𝐨𝐧𝐬

𝐉𝐨𝐲𝐛𝐢𝐫𝐝'𝐬 𝐏𝐚𝐭𝐡 𝐭𝐨 𝐏𝐫𝐨𝐟𝐢𝐭𝐚𝐛𝐢𝐥𝐢𝐭𝐲

Given the $20M goodwill impairment and ongoing double-digit declines in delivered sales, is Joybird still considered a core component of the 'Century Vision', or is management exploring strategic alternatives for this segment?

𝐍𝐨𝐫𝐦𝐚𝐥𝐢𝐳𝐞𝐝 𝐖𝐡𝐨𝐥𝐞𝐬𝐚𝐥𝐞 𝐌𝐚𝐫𝐠𝐢𝐧𝐬

With 150 basis points of Q4 Wholesale margin driven by favorable casegoods inventory adjustments prior to divestiture, what is the normalized baseline operating margin expectation for the core upholstery wholesale business heading into FY27?

𝐏𝐚𝐜𝐞 𝐨𝐟 𝐭𝐡𝐞 𝐍𝐞𝐰 𝐁𝐮𝐲𝐛𝐚𝐜𝐤 𝐏𝐫𝐨𝐠𝐫𝐚𝐦

The Board approved a $300M share repurchase program after management previously telegraphed a shift toward reinvestment. Does this size indicate a lack of attractive independent store acquisition targets, or purely a view that LZB shares are currently undervalued?

3

2

2,935

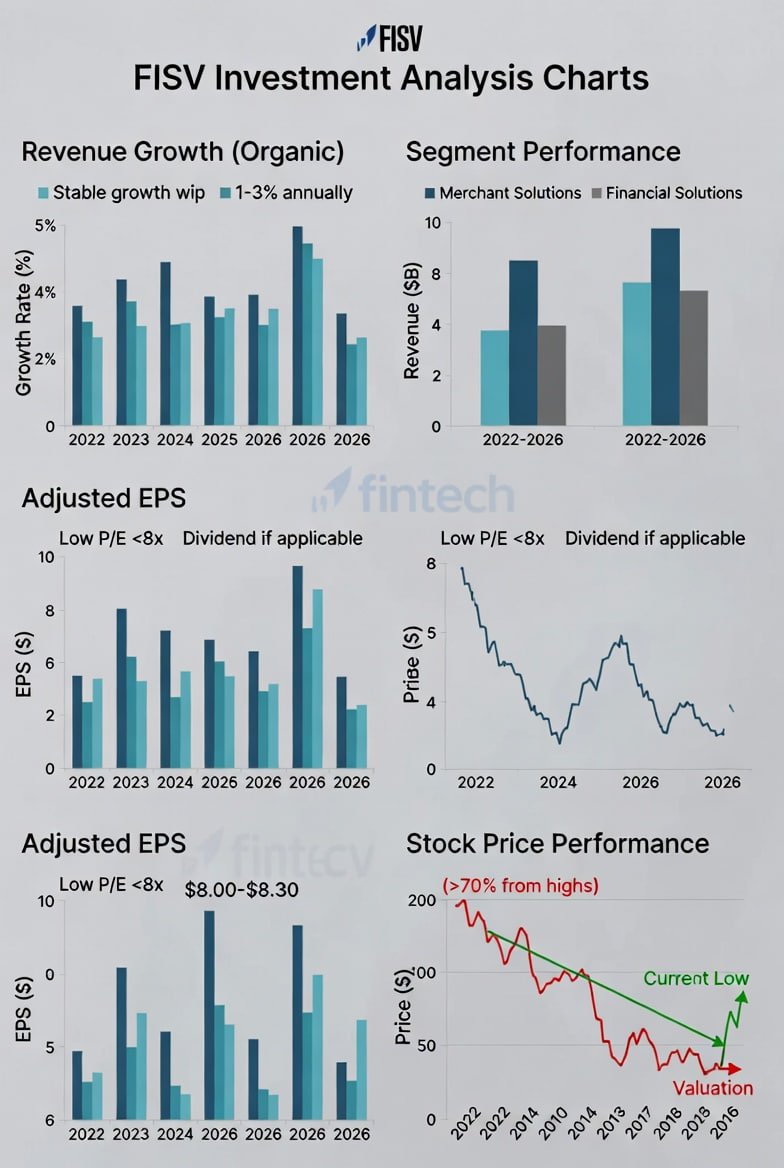

Is FISV's current valuation too low? What are its growth prospects?

What impact will the sudden departure of the CEO (Mike Lyons joining Truist, with Takis Georgakopoulos promoted internally to succeed him) have on the company?

Is the 2026 guidance reliable? How are the Merchant Solutions and Financial Solutions segments performing?

Can competitive pressure, the possibility of asset divestitures, and AI/digital transformation drive a rebound?

Attractive valuation but with risks: The stock price has fallen significantly from its all-time high (over 70%), the current P/E ratio is low (approximately 8x), and the average analyst target price is around $70 (potential upside of 40% ), with some forecasts as high as $80 . The company maintains its 2026 organic revenue growth guidance of 1-3% and adjusted EPS guidance of $8.00-$8.30.

CEO change: The market views this as short-term uncertainty (the stock price has fallen), but the internal successor has experience in merchant platform modernization and AI; the company reiterates its full-year guidance. Some insiders and investors (such as Michael Burry mentioned) see the low point as a buying opportunity.

Business Fundamentals: Q1 2026 revenue declined slightly, but EPS exceeded expectations. Merchant solutions remained relatively stable, while financial solutions faced pressure. Small business sales data was mixed (slight sales growth but slower customer traffic).

Long-Term Positioning: Leading Fintech company with strong competitive advantages in payments, banking solutions, and the Clover platform.

Short-Term Target Price: $60-65

#FISV

#SOFI

#NFLX

#NVDA

#AIStocks

#FinTech

#StockMarket

1

1

119

@stocktwits $LZB Results deceiving. Here's why:

La-Z-Boy's Q4 results appear stronger on the surface than they are underneath. While adjusted operating margin expanded to 9.9% and adjusted EPS jumped 37% year-over-year, the improvement was driven largely by divestiture-related benefits rather than stronger consumer demand or accelerating product sales.

Revenue was essentially flat at $570 million, highlighting the lack of meaningful top-line growth. More concerning, same-store written sales declined 2%, marking another quarter of negative organic demand. The company's reported retail growth was fueled primarily by acquisitions and new store openings rather than increased customer traffic or higher sales productivity.

The margin story is even less impressive after adjusting for one-time factors. Management disclosed that approximately 150 basis points of Wholesale segment margin expansion came from favorable inventory adjustments and pricing actions tied to the divestiture of the American Drew and Kincaid casegoods businesses. Without these benefits, underlying margin performance would have been substantially weaker.

Meanwhile, the $20 million goodwill impairment at Joybird underscores ongoing challenges within the company's direct-to-consumer strategy. Delivered sales at Joybird fell another 10%, suggesting demand pressures remain broad-based across the portfolio.

Looking ahead, management's Q1 FY27 guidance points to a sharp sequential decline in profitability, with adjusted operating margin expected between 4.0% and 5.5% versus 9.9% in Q4. This suggests the quarter's elevated profitability was not sustainable and benefited from temporary factors surrounding portfolio restructuring.

Ultimately, La-Z-Boy's earnings beat was driven more by divestitures, accounting adjustments, and financial engineering than by stronger furniture demand. Until same-store sales return to consistent growth, investors should question whether recent margin expansion reflects a fundamentally stronger business or simply the temporary benefits of portfolio cleanup activities.

29

$CRL Charles River Laboratories — Morgan Stanley upgrades to Overweight, raises PT 📈

PT ↑ $220 (from $185) | Current $188 (Upside ~17%)

⠀

• Morgan Stanley sees improving biopharma funding translating into stronger RFP activity and bookings, benefiting CRL's preclinical business

• Recent acquisitions and divestitures could provide upside to consensus estimates from 2027 onward

• Firm believes AI-driven drug development may increase demand for safety testing despite potential pressure on discovery work

1

270

$CRL Morgan Stanley Upgrades Charles River Laboratories to Overweight, Raises PT to $220 from $185Key Highlights:Morgan Stanley upgrades CRL from Equal Weight to Overweight

Price target increased to $220 from $185

Analyst Kallum Titchmarsh highlights improving biopharma funding environment translating into stronger RFPs and bookings

Expects CRL’s leading preclinical capabilities to drive meaningful upside

Recent acquisitions and divestitures should reduce earnings volatility (especially NHP supply) and provide upside to 2027 estimates

Sees potential tailwinds from WuXi’s inclusion on the U.S. DoD 1260H list and Inotiv’s Chapter 11 filing

On AI: While discovery work may moderate, safety testing demand is expected to rise as pipelines become more efficient

Raises 2027 EPS estimates by low-single digits

New $220 PT implies 14x 2026E EV/EBITDA

#CRL #CharlesRiver #MorganStanley #Upgrade #Biopharma #Preclinical #LifeSciences

43

Morgan Stanley Upgrades $CRL to Overweight from Equalweight, Raises PT to $220 from $185

Analyst comments: "With a strong uptick in biopharma funding beginning to transition into RFPs and bookings, we think CRL is well positioned to benefit given its leading preclinical capabilities. We also believe recent acquisitions and divestitures offer clear upside risk to Street numbers from 2027 onward and help to reduce areas of historical volatility through the P&L, such as building out a more reliable NHP, or non-human primates, supply network. While small, additional upside could present itself from WuXi’s recent inclusion on the U.S. DoD’s 1260H list as well as Inotiv’s Chapter 11 filing. On AI, though we acknowledge a potential reduction in discovery work for CRL, we believe the company could see a notable uptick in safety testing as pharma/biopharma pipelines become smarter with lower barriers for taking shots on goal. Our recent New Approach Methodologies deep dive provided us comfort in the size of potential headwinds facing the business, even under aggressive NAM penetration scenarios, with the profit pool remaining intact. Despite growth lagging clinical-stage peers today, we see a clearer path for acceleration here and believe that’s what investors will assign value to versus concerns of stagnation. Taking these factors into consideration, we’ve moved our 2027 EPS estimates up low-single digits and upgrade CRL to Overweight with a $220 PT, implying a 14x 2026E EV/EBITDA multiple, from 12x prior."

Analyst: Kallum Titchmarsh

1

3

25

7,976

Report from Global Banking & Finance Review Italy’s engineering sector evolves: unit sales, new leadership moves, and broader M&A activity reshape growth. Explore insights on engineering divestitures, strategic exits, and cross-border deals shaping the m… globalbankingandfinance.com/…

7

Anticipated Changes for Xbox under Asha Sharma’s Leadership

1. Shift Toward Annual Exclusives

Xbox will push to release signature exclusives every year. This could strengthen brand identity but also put heavy pressure on development teams to deliver consistently.

2. Expansion Beyond Gaming

By framing competition as “attention,” Xbox will expand into TV, film, and apps. This diversification could broaden reach but risks diluting focus if execution is weak.

3. Restructuring for Sustainability

Unsustainable operations will be cut. Xbox may transform into a Microsoft-owned but independently managed entity, similar to LinkedIn or GitHub, to gain financial autonomy.

4. New Hardware Partnerships

With console production challenges, Xbox is likely to embrace OEM partnerships. Companies like ASUS, MSI, or Razer could manufacture licensed Xbox hardware, reshaping the console market.

5. Studio Consolidation

Overextended first-party expansion will be corrected. Expect closures or divestitures of weaker studios, with resources concentrated on flagship franchises like Halo, Gears, Forza, COD and Fallout.

6. Third-Party Exclusives Strategy

Xbox will actively pursue third-party exclusives, a notable shift from past policy. This could intensify competition with Sony and alter the balance of power in the industry.

7. Platform Infrastructure Overhaul

The Xbox Store and ecosystem will undergo major redesigns. If successful, this could improve user experience significantly; if not, frustration may deepen.

8. Entertainment Ambitions

Xbox aims to become the #1 gaming and entertainment company. Success will depend on how well it integrates gaming with broader media ventures.

6월 10일 발표된 Xbox 리셋 (Reset) 선언문과 앞으로 나타날 현실 (출처 : XBOX 정보 카페 | 네이버 카페) naver.me/FLER6Rfw

1주일 전, 6월 10일 Xbox는 앞으로 100일 동안 Xbox 사업을 재설정 (Reset) 하겠다는 선언문을 발표했습니다.

이 글에 나온 주요 내용을 다시 보고, 앞으로 어떤 일이 나타날지 생각해보겠습니다.

1. Players can continue to expect signature exclusives from us every year

앞으로 매년 Xbox는 시그니처 독점작을 선보일 것입니다. 올해는 기어스 오브 워: E-Day와 클락워크 레볼루션 2개의 게임을 독점으로 발표했고, 이런 독점작 발표는 앞으로 매년 나오게 됩니다.

2. Going forward, our competition is attention.

Xbox의 경쟁상대는 '대중들의 관심' 그 자체라고 선언했습니다.

앞으로 Xbox는 게임에만 한정되지 않고, TV와 영화 등 다양한 컨텐츠 포맷이나 앱 등으로 확장되게 됩니다.

3. Going forward, this cannot continue.

앞으로 지속불가능한 사업은 하지 않겠다고 합니다.

3%에 불과한 책임 마진, 매년 떨어지는 매출, 본사로부터 계속 지원금을 받아야 하는 상황에서 벗어나야 한다고 합니다.

Xbox가 MS로부터 경영 자체가 독립된 별도 법인으로 바뀔 가능성을 열어두고 있는 부분입니다.

현재 가장 가능성 높은 시나리오는 링크드인이나 깃허브처럼 MS가 완전 100% 소유는 하고 있지만 경영 자체는 독립적으로 하는 법인 형태로 변하는 시나리오입니다.

4. We are currently unable to make as many consoles as players want to buy, and we need a new business model and partnerships for hardware as we remain committed to Helix.

하드웨어 부품 값이 천정부지로 오르고 있는 시점에서 게다가 MS는 타 콘솔회사보다 부품 수급에 더 대처를 하지 못했고, 그 결과 콘솔 생산도 현재 제대로 할 수 없는 상황이라고 인정했습니다.

MS는 헬릭스 (MS의 퍼스트파티 콘솔) 계획은 계속 진행하지만

현재 상황을 극복하기 위해서는 하드웨어 사업에서도 새로운 사업 모델과 파트너십이 필요하다고 인정합니다.

오래 전부터 예상되어온 서드파티 Xbox 콘솔 하드웨어 (OEM Xbox)가 본격적으로 추진될 가능성이 높다고 예상할 수 있습니다.

ASUS, MSI, Razor 등 다양한 PC 제조업체들이 라이센스를 받아 Xbox 콘솔 하드웨어를 만들 게 될 가능성이 높습니다.

5. we have found ourselves over extended as we executed on changing strategies in a landscape of more readily available content.

콘솔, PC, 클라우드, 구독 시스템, 스트리밍 등 다양한 방면으로 게임 컨텐츠를 확장하려다보니

퍼스트파티 스튜디오를 너무 지나치게 확장했다는 사실을 인정했습니다.

앞으로는 핵심 프랜차이즈에만 자원을 집중하고 성과가 약한 스튜디오들은 정리하겠다는 뜻입니다.

그 결과로 어제 오늘 몇몇 퍼스트파티 스튜디오들의 폐쇄나 매각 이야기가 나오고 있습니다.

6. a reliable pipeline of first- and third-party exclusives and new IP are critical to our success.

안정적인 퍼스트/서드 파티 독점작 및 신규 IP가 성공에 중요하다.

독점작이 Xbox 성공에 필수라고 명백히 선언하고 있습니다.

퍼스트 뿐만 아니라 서드 파티에서도 독점작이 필요하다고 한 것이 인상적입니다.

서드파티 독점작이 중요하다는 언급 자체가 필 스펜서 시대에는 전혀 없었던 것입니다.

앞으로 MS는 소니가 그러고 있는 것처럼 유망한 서드파티 게임들에도 독점 계약을 시도할 가능성이 높습니다.

7. Our current platform infrastructure is not built for the battle ahead

현재 Xbox 플랫폼 인프라가 경쟁에 적합하지 않다고 인정하는 글입니다.

외주(벤더)에만 의존해왔던 구습에서 벗어나 Xbox가 직접 플랫폼 인프라를 만들고 관리하여

업무를 더 간소화하고 빠른 움직임을 보여야 한다고 합니다.

올 연말에는 Xbox 스토어가 완전 달라질 것이라는 루머가 Jez 기자를 통해 나온 적도 있습니다.

유저들이 가장 불편함을 느끼는 부분이 Xbox 스토어/앱/웹사이트 등인데 얼마나 개선되어서 나올지 기대해봐야겠습니다.

8. Let’s reset for a stronger XBOX and build the #1 gaming and entertainment company.

Xbox를 세계 1등 게임 및 엔터테인먼트 회사로 만들겠다고 선언합니다.

게임 뿐만 아니라 엔터테인먼트까지 합쳐서 매출액 1위로 만들겠다는 선언입니다.

앞으로 어떻게 확장해나갈지 모르지만, 여러가지 다양한 시도들이 있을 것으로 보입니다.

news.xbox.com/en-us/2026/06/…

3

16

138

9,820

Jun 17

FTC requires Ascension divestitures in $3.9B AmSurg deal monkeylink.co/385f4b via @healthcaredive #healthcare #ftc

15