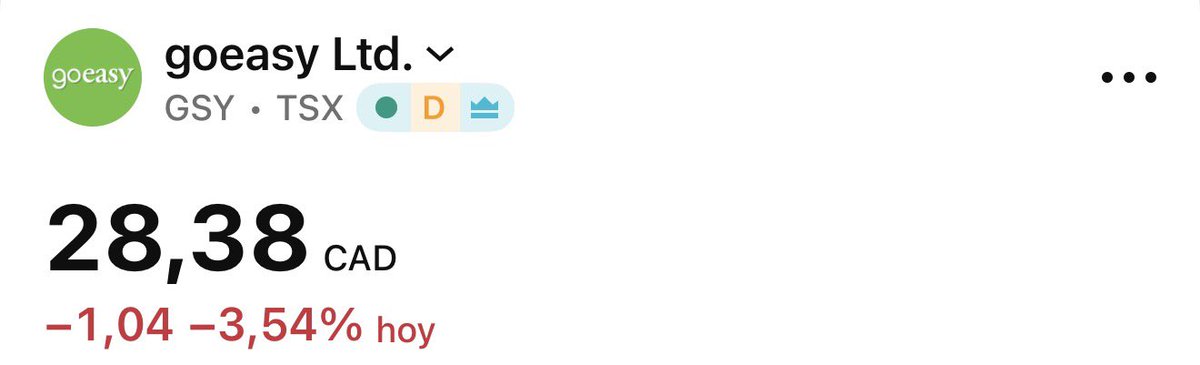

Why goeasy Ltd stock is tanking today

A significant drop in goeasy Ltd's stock raises questions for investors.

wealthawesome.com/why-goeasy…

5

Jun 15

Why goeasy Ltd stock is skyrocketing today

Shares of goeasy Ltd surged by nearly 6% in the latest trading session, reflecting strong investor confidence and strategic financial maneuvers.

wealthawesome.com/why-goeasy…

13

Jun 14

2

57

Jun 13

Yo solo deseo k recompren a muerte y k las cuentas no sean falsas k ya me he comido TISG y GOEASY k no me toquen más los coj xD

1

86

Jun 12

Sus nagarros, teleperformance, goeasy entre otras no dicen eso

1

60

Por mencionar algunas, porque la lista de truños no te la acabas: Nagarro, Teleperformance, Newprinces, caída, telus, dnd, sbb, dole, gdi, mty, data group, goeasy...

11

5

46

7,329

3

2

16

3,084

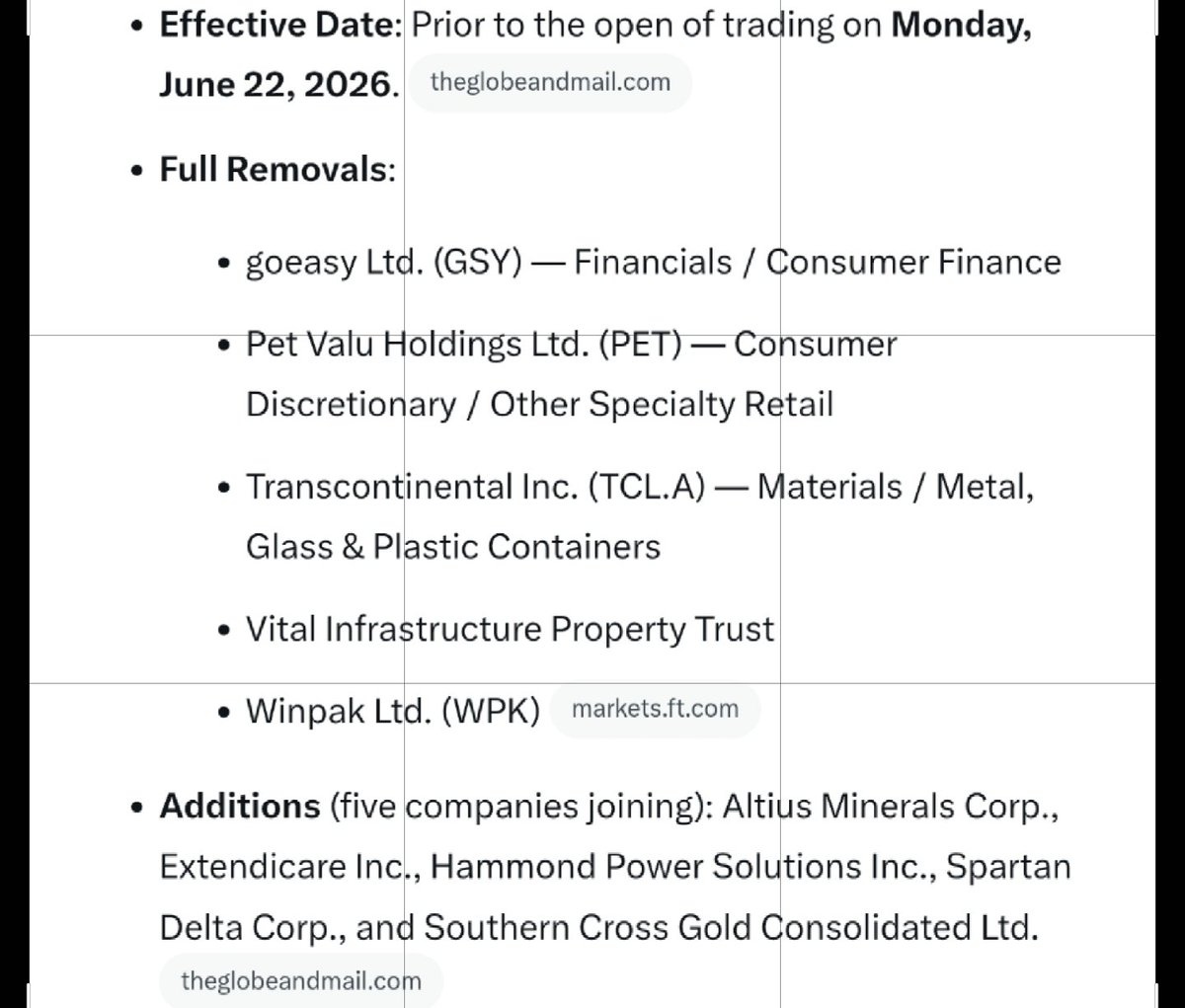

Goeasy, Pet Valu among companies removed from Canada’s main stock index theglobeandmail.com/investin…

2

1

2,825

Jun 5

Just Go Easy 🔥😎

@trroystudios

Special shout out to:

@calvinmayani_

@allanchri

@BassetFame

And the team @trroystudios for helping bring this to life! 🫶🏼

#dance #goeasy

1

2

30

716

May 14

News of the day: Bank of Canada's worries, Agnico Eagle's mining investment, falling rents, Goeasy results, workplace harassment allegations and more financialpost.com/uncategori…

1

514

May 13

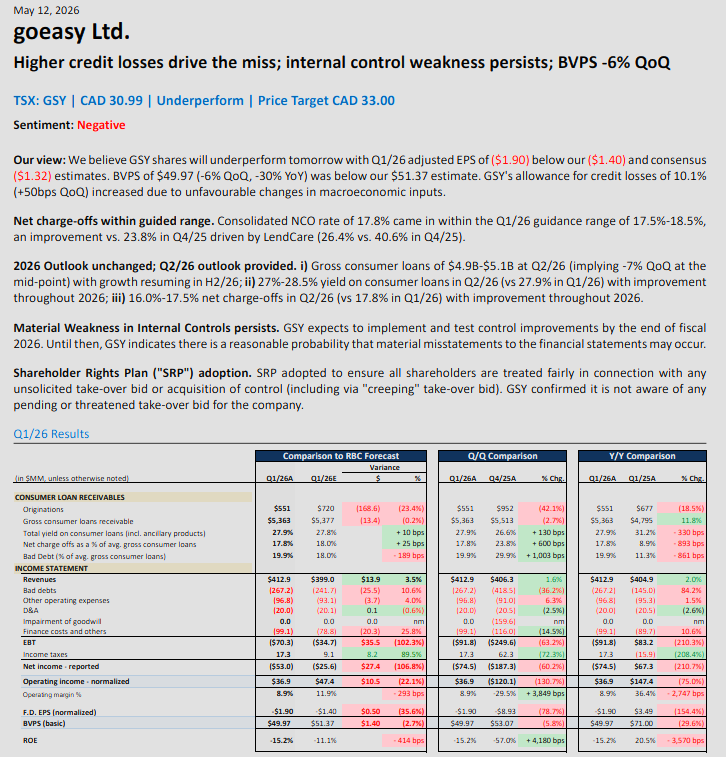

Goeasy reports $53M loss in Q1, compared with net gain of $38.7M last year bnnbloomberg.ca/business/202…

1

1,863

$GSY GoEasy $225 to $29.50 in less than a year.

BNN "They are thwarting take-over bids"

Being acquired with most of the Board and the management team being replaced is probably a very good move.

Seriously, they need to be thwarting going to court.

Several Canadian law firms (e.g., Siskinds LLP/Strosberg, Berger Montague, Rochon Genova, Kalloghlian Myers, SMK Law) have filed or are actively pursuing proposed class actions in Ontario Superior Court.

4

2

11

3,225

May 13

goeasy $GSY

Canadian financial services company offering loans to non-prime borrowers and providing point-of-sale consumer financing....

the (long) share holders crying out to the shorts "goeasy" on us! please...

1

1

7

979

If you invest in $GSY GoEasy

Your just fine with a financial institution that...

"Expects to implement and test control improvements by the end of fiscal 2026.

Until then, $GSY indicates there is a reasonable probability that material misstatements to the financial statements may occur"

Are you actually kidding me ?

5

20

3,786

May 12

$GSY.TO — goeasy Ltd. | Q1 2026 Results

Canada's largest non-prime consumer lender posts first quarterly loss in years as merchant-originated auto/powersports portfolio hit by elevated charge-offs

📊 Q1 2026 Highlights:

• Revenue: $412.9M ( 2% YoY)

• Net loss: $(53.0)M (vs $38.7M Q1/25 restated)

• Diluted LPS: $(3.22) (vs $2.28 Q1/25)

• Adj. diluted LPS: $(1.90) (vs $3.49 Q1/25)

• Operating income: $28.9M (-80% YoY)

• EBITDA: $36.4M (margin 8.8% vs 38.9%)

• OCF: $122.3M (vs -$180.3M Q1/25)

⚡ Portfolio & Credit:

• Loan book: $5.36B ( 12% YoY, -3% QoQ)

• Originations: $551.3M (-19% YoY)

• Net charge-off rate: 17.8% ( 890 bps YoY, -600 bps QoQ)

• Total yield: 27.9% (-330 bps YoY, 130 bps QoQ)

• Allowance ratio: 10.09% (up from 9.57% at Dec/25)

• Active customers: 466,000 ( 7%)

💰 Capital Actions:

• Dividend suspended (indefinite)

• NCIB buybacks suspended (indefinite)

• Cash on hand: $356M ( 133% from Dec/25)

• Liquidity: $1.10B (only $360M currently drawable)

• Adopted shareholder rights plan May 12

🔮 Q2/26 Guidance:

• Loan book: $4.9-5.1B (declining before resuming growth later in year)

• Total yield: 27.0-28.5%

• Net charge-off: 16.0-17.5% (mid-teens for FY26)

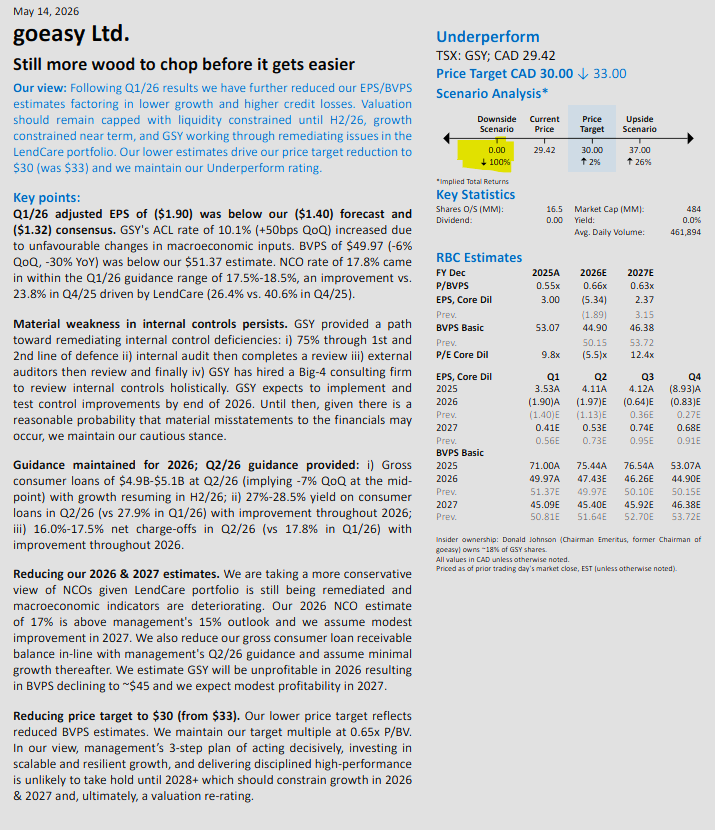

This is the messy quarter the market was bracing for. Merchant-originated auto/powersports loans drove the $267M bad debt charge (up 84% YoY) and pushed GSY to its first loss. Management's six-point action plan is now executing: tighter underwriting, dividend/buyback suspension to preserve capital, and a rights plan to protect against opportunistic bids while the stock is depressed. The direct-to-consumer easyfinancial business remains profitable (op margin 11.5%). The thesis now hinges on charge-offs normalizing to mid-teens by year-end and the loan book troughing before resuming growth — neither is guaranteed.

Full analysis:

investorlens.io/stocks/GSY.T…

#TSX #CanadianStocks #ConsumerFinance #NonPrimeLending #Earnings

8

947