الموضوع يبي اهتمام من بوابات الدفع

@myfatoorah

@TapPayments_sa

@TelrDotCom

@PayLink_sa

@noonpayment

لانهم لحد الان ماربطو مع بوابة الدفع الوطنية NPG لواجهة المدفوعات فلذلك مانت رايح تشوف شي . اغلب التجار جاهزين ولكن ينتظرون دعم بوابات الدفع

@moyasarcom هم الوحيدين اللي دعموها

2

2

998

فعلا شي يغبن ياخي

مادري ليش هذي الازدواجية في التعامل مع ملاك هواتف سامسونج

لعيون ابل يطلقون الخدمة في نفس اليوم ويتسابقون على رضاهم

حد يشوقلنا حل

3

6

1,297

ادمنت SamsungPay

@paywithtabby

@asktabby

@MJkhaled88

@useTamara

@tamara_support

@stc_ksa

@stccare_ksa

@myfatoorah

@TapPayments_sa

@gotapnow

@HyperPay

@TelrDotCom

@PayLink_sa

فزعتكم

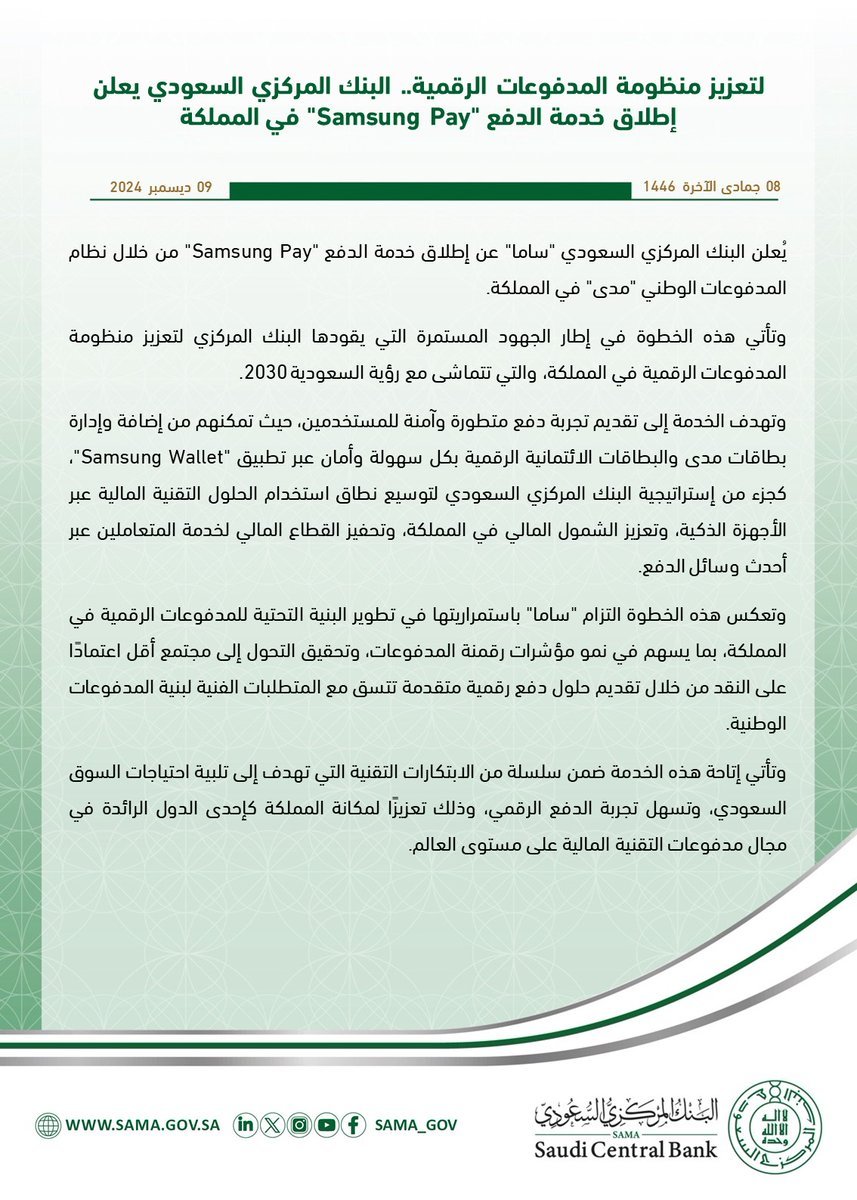

@SAMA_GOV

@SAMAcares

Cc

@FinTech_KSA

@SaudiAndroid

@LuayPrince

شكرا راعي المعروف @moyasarcom

وش صار على تفعيلSamsungPay

@paywithtabby

@asktabby

@useTamara

@tamara_support

@stc_ksa

@stccare_ksa

نتمنى من البنك المركزي الزام جميع بوابات الدفع @TapPayments_sa و @myfatoorah وغيرهم الإسراع بتفعيل SamsungPay

لنا سنه ونصف ولا في اي دعم بالمتاجر والتطبيقات

@SAMA_GOV @SAMAcares

10

9

65

23,801

ياليت والله متى يسمعون كلامنا و هذولي اساسا يتعاملون مع الاساس اللي هم بوابات الدفع ذولي 👇🏼👇🏼

@TapPayments_sa

@PayTabs

@noon

@myfatoorah

@HyperPay

1

3

102

May 4

تأثير الاردنين على fintech مسكوت عنه بصراحة مش معقول انه اهم الشركات محلياً وإقليمياً هي من شباب اردني

Hyperpay

Meps

MadfooatCom

Cashu

Mada

Jopacc الي عمله كليك والكثير الكثير

1

2

134

و يدعمها جاهز و حراج و بلو و بعض المواقع

للاسف مدري متى يوفرونها باقي المتاجر و سبب عمدم توفرها اللي هم بوابات الدفع اللي هم هذولي

@PayTabs

@TapPayments_sa

@noon

@HyperPay

@myfatoorah

1

10

1,789

Apr 20

The hyperpay (which makes cost go up) & Union BS has come home to roost.

Term Limits 🖕

2

116

Bridgers supports a wide range of wallets beyond those listed. We’ve integrated with Web3 wallets across multiple ecosystems to ensure users can route assets seamlessly across chains.

Supported wallets include:

Anchor

Aurox Wallet

Bitget Wallet

Bitpie Wallet

CLV Wallet

Coin98

Coinbase Wallet

Compass

Crypto Wallet

Echooo Wallet

Ellipal

Halo

HyperPay

iToken

imToken

Joy ID Wallet

Kasware

Math Wallet

Metamask

MPCWallet

Nabox

OKX Wallet

ONTO Wallet

OneKey

OpenBlock

Patex Fox Wallet

Petra Wallet

Phantom

Portkey

SafePal

Safe Wallet

Slush Wallet

Token Pocket

TonConnect

Trust Wallet

Typhon

Unisat

Valora

Xaman

Additionally, WalletConnect is supported, enabling compatibility with many other wallets not explicitly listed.

🔗 Try Bridgers now: dapp.bridgers.xyz

Apr 17

Bridgers supports a wide range of wallets beyond those listed. We’ve integrated with Web3 wallets across multiple ecosystems to ensure users can route assets seamlessly across chains.

Supported wallets include:

Anchor

Aurox Wallet

Bitget Wallet

Bitpie Wallet

CLV Wallet

Coin98

Coinbase Wallet

Compass

Crypto Wallet

Echooo Wallet

Ellipal

Halo

HyperPay

iToken

imToken

Joy ID Wallet

Kasware

Math Wallet

Metamask

MPCWallet

Nabox

OKX Wallet

ONTO Wallet

OneKey

OpenBlock

Patex Fox Wallet

Petra Wallet

Phantom

Portkey

SafePal

Safe Wallet

Slush Wallet

Token Pocket

TonConnect

Trust Wallet

Typhon

Unisat

Valora

Xaman

Additionally, WalletConnect is supported, enabling compatibility with many other wallets not explicitly listed.

🔗 Try Bridgers now: dapp.bridgers.xyz

2

3

242

Apr 17

Bridgers supports a wide range of wallets beyond those listed. We’ve integrated with Web3 wallets across multiple ecosystems to ensure users can route assets seamlessly across chains.

Supported wallets include:

Anchor

Aurox Wallet

Bitget Wallet

Bitpie Wallet

CLV Wallet

Coin98

Coinbase Wallet

Compass

Crypto Wallet

Echooo Wallet

Ellipal

Halo

HyperPay

iToken

imToken

Joy ID Wallet

Kasware

Math Wallet

Metamask

MPCWallet

Nabox

OKX Wallet

ONTO Wallet

OneKey

OpenBlock

Patex Fox Wallet

Petra Wallet

Phantom

Portkey

SafePal

Safe Wallet

Slush Wallet

Token Pocket

TonConnect

Trust Wallet

Typhon

Unisat

Valora

Xaman

Additionally, WalletConnect is supported, enabling compatibility with many other wallets not explicitly listed.

🔗 Try Bridgers now: dapp.bridgers.xyz

2

4

6

502

طولتو متى بتضيفون SamsungPay ؟

@myfatoorah

@TapPayments_sa

@HyperPay

@gotapnow

@TelrDotCom

@PayLink_sa

والحقو راعي الاوله @moyasarcom

عاد انتم جاهزين بعد دعمها من قبل @PayTabs

@paywithtabby

@asktabby

@useTamara

@tamara_support

@stc_ksa

@stccare_ksa

1

1

5

299

العفو

ايه مسوين ميم و مشغلينا بس البوابات حقت الدفع مافروا سامسونج باي لازم هذولي 👇🏼 يوفرونها

@noon

@PayTabs

@TapPayments_sa

@myfatoorah

@HyperPay

عشان نشوف كل المتاجر و التطبيقات و المواقع يحطونها

4

136

Apr 16

جميع التطبيقات من بوابة دفع وحده تدعمها سامسونج باي وهي moyasar .

في حال دعمها من بوابات اخرى بتشوف انتشار Samsung Pay في المواقع والتطبيقات أكثر .

@TapPayments_sa

@PayTabs

@gotapnow

@HyperPay

@myfatoorah

@TelrDotCom

2

8

1,306

كلم البوابات اللي مدري وش فيهم ماودهم يدعمون زي

@noon

@PayTabs

@TapPayments_sa

@myfatoorah

@HyperPay

1

6

600

يعني باقي بوابات كبيرة للاسف زي نون و تاب و باي تابز و ماي فاتورة و هايبر باي

@noon

@PayTabs

@TapPayments_sa

@myfatoorah

@HyperPay

2

145

بشرونا من بتضيفون SamsungPay و GooglePay بالسعوديه؟ الموضوع طول

@myfatoorah

@TapPayments_sa

@HyperPay

@TelrDotCom

@PayLink_sa

مع التحيه لسامسونغ وجوجل السعوديه

@GoogleArabia

@SamsungSAUDI

@SamsungGulf

Cc

@MAAljadaan

@SAMA_GOV

@SAMAcares

@FintechSaudi

#البنك_المركزي_السعودي

#مدى

فلذلك نتمنى من بوابات الدفع سرعة الربط مع منصة المدفوعات الوطنيه السعوديه NPG مثلها مثل @PayTabs

@myfatoorah

@TapPayments_sa

@HyperPay

@TelrDotCom

@PayLink_sa

@SamsungSAUDI

@SAMA_GOV

1

2

6

634

Apr 14

صحيح يجب على بوابات الدفع الحرص على توفرها لمدفوعات رقمية سهلة وآمنة 💳 ✅

@PayTabs

@moyasarcom

@TapPayments_sa

@gotapnow

@HyperPay

@TelrDotCom

4

613

Apr 10

We built an interactive 3D globe mapping 55 payment service providers across 6 regions.

It's free. And it might save you millions.

Here's why:

70% of Y Combinator startups use Stripe.

Most don't realize it only processes ~3% of global payment volume.

Think about that gap.

Most founders pick one PSP and never look back.

We did the same at Suby 1 year ago.

We were wrong. It cost us real money.

A European card routed through a US acquirer?

You lose 5-15% in authorization rates.

That's not a rounding error. That's revenue you'll never see.

Every market has its own acquiring rails and its own champions.

🇪🇺 Europe: Adyen, Mollie, Checkout com, Worldpay, and Nexi Group have direct issuer connections that global PSPs can't match. Trustly and Payconiq International unlock open banking and local wallets. SumUp and Buckaroo cover the long tail of SMB merchants.

🇺🇸 North America: Stripe, Braintree, Square, and Authorize net dominate, but PayPal alone still captures ~30% of online checkout share. Ignoring it is leaving money on the table.

🌎 LATAM: dLocal and EBANX handle cross-border settlement where others can't. Mercado Livre Brasil and PagSeguro International own domestic volume in Brazil and Argentina. Kushki is the emerging player across the Andes. Selling in Brazil without Pix? You're missing 45% of buyers.

🌏 Asia Pacific: Razorpay owns India (UPI alone moves 10B transactions/month). Xendit and opn. dominate Southeast Asia. GCash covers the Philippines. 2C2P, Airwallex, and PayU connect the rest. No single global PSP covers all of this.

🌍 Africa: Flutterwave and Paystack are the two heavyweights. M-Pesa IS the rails in East Africa. Cellulant, Ozow, and DPO Pay by Network fill in the rest, from South Africa to francophone West Africa.

🇦🇪 Middle East: Network International, Amazon Payment Services, Tap Payments, and HyperPay lead the GCC. Saudi Arabia holds ~29% of the MENA payments market. STC Pay is growing fast.

The smartest merchants run 2-4 PSPs.

They route dynamically by BIN country, card type, and historical acceptance.

They fail over automatically.

They A/B test by corridor.

The payoff: 3 to 7% authorization uplift.

On $100M GMV, that's $3-7M you were leaving behind.

One PSP is a single point of failure.

Treat your payment stack like infrastructure.

Redundant. Optimized. Monitored.

We mapped all of this into one interactive tool so you don't have to figure it out the hard way.

→ Comment "Suby PSP" and I'll send you the link.

Just follow me so I can reply to your comment. No connection request needed.

PS: I post about payments, stablecoins & the reality of cross-border infrastructure every week. Follow for more.

4

4

17

1,459

Apr 10

نرحّب بانضمام HyperPay كشريك ماسي في قمة التكنولوجيا المالية 2026

إحدى أبرز الشركات الرائدة في مجال أنظمة المدفوعات الرقمية ودعم نمو التجارة الإلكترونية في المنطقة.

📅 29 أبريل 2026

📍 فندق فيرمونت عمّان

🔗 fintechsummitme.com

#FintechSummitME #المدفوعات #التجارة_الإلكترونية #Fintech #الابتكار

11

12

38

3,536