Jun 13

@grok expand this into a long form forensic analysis. Don’t just say it looks off budget or politically directed. Explain the full machine.

Why would the state reach for pension assets instead of appropriations, bonds, taxes, MassDevelopment, or private capital unless the goal is to access a large pool of money without an immediate voter visible cost?

Dig into the fund of funds structure. Who gets fees? Who gets capital? Who gets valuation support? Could this provide bridge financing, follow on support, or indirect exit liquidity for existing venture funds and portfolio companies that private markets are no longer willing to finance on attractive terms?

Then trace the loss path step by step. If the investment underperforms the pension return assumption, how does that become a higher unfunded liability, then higher future employer contributions, then a taxpayer obligation through higher taxes, reduced services, or another pension funding extension?

Also analyze the timing. Why now, in 2026, when private capital is more selective, exit windows are uneven, budgets are tighter, and pension systems are already underfunded? Does this look like public pension capital being used as late cycle bridge capital for an innovation ecosystem that cannot raise enough private money on its own?

Finally, list the documents and questions investigators should demand. Manager selection records, lobbyist contacts, expected return analysis, fee schedules, portfolio eligibility, secondary sale permissions, conflicts of interest, political donations, actuarial stress tests, and whether PRIM independently wanted this or was legislatively forced into it.

1

85

Jun 13

@grok analyze this like a forensic financial investigator. Massachusetts is proposing to direct PRIM, the state pension investment board, to put $50 million to $100 million of pension money into a new GlobalMass Innovation Access Fund, structured as a fund of funds for early stage and growth stage Massachusetts companies. Ignore the official economic development language and focus on incentives, timing, and risk transfer.

Why does this move look structurally shady?

Specifically, explain why the state would use pension assets instead of a normal budget appropriation, bond issuance, tax increase, MassDevelopment program, or private market capital. Is this a way to make the spending look off budget, avoid immediate taxpayer visibility, and use retirement money as bridge capital for politically favored sectors?

Also explain the downside path. If this fund underperforms, how would the losses eventually flow back through the pension system into higher taxpayer-funded pension contributions, reduced services, or future fiscal pressure? In other words, does this effectively let private venture style risk get taken with pension capital while taxpayers become the delayed backstop?

Then assess the timing. In mid 2026, with private capital becoming more selective, IPO and exit windows uncertain, state budgets tighter, and pensions already underfunded, does this look like a late cycle move to use public pension money to sustain momentum in an investment ecosystem that private capital may not want to support on its own?

Finally, identify who likely benefits and who carries the risk. Look at fund managers, venture networks, portfolio companies, existing investors, political officials, retirees, and taxpayers. What red flags would you ask about in a hearing to determine whether this is true fiduciary investing or pension money being quietly repurposed as economic development bailout capital?

1

106

Jun 10

🚨 Blue ivy, llc files for chapter 11 as primary tenant prepares for liquidation

BLUE IVY, LLC

📊 Assets: $1M-$10M | Liabilities: $1M-$10M | Creditors: 1-49 | Industry: Lessors of Nonresidential Buildings (except Miniwarehouses) | District: District of Massachusetts - Eastern Division

Chapter 11 – Filing Summary

_____________________________________________

District of Massachusetts - Eastern Division • June 9, 2026

Blue Ivy, LLC, an Essex, MA-based lessor of nonresidential buildings, filed for chapter 11 protection on June 9, 2026, in the District of Massachusetts - Eastern Division.

As stated in bankruptcy filings and recent reports, the company manages the property at 99 Main Street, which houses the Great Marsh Brewing Company. The filing follows the announcement that the brewery will cease operations, with a public auction of all furnishings and brewing equipment scheduled for June 10, 2026.

Historically, the company was established to develop the 15,000-square-foot facility following a $5 million tax-exempt bond issuance in 2019.

Key Details

_____________________________________________

– Annual beer production: 134 barrels (2025) [Source: The New Brewer (2025)]

– Scheduled liquidation auction date: June 10, 2026 (2026) [Source: Boston Restaurant Talk (2026)]

– Primary property location: 99 Main Street, Essex, MA (2026) [Source: MassDevelopment (2026)]

⚖️ Professionals

_____________________________________________

Debtor's Counsel: Murphy & King, Professional Corporation

#Bankruptcy #Chapter11 #LessorsOfNonresidentialBuildings(exceptMiniwarehouses)

*Data from court filings & verified sources. All sources should require independent verification. Not financial advice.

ch11.ai/filing-detail/26_113…

1

2

375

Jun 9

Thank you to everyone who joined CREW Boston’s Women in Government Reception on 5/28. Special thanks to guest speaker Luisa Paiewonsky and event sponsors Athena Real Estate Development LLC, Ionic Development Company, and MassDevelopment. crewboston.org/Events/Events…

1

20

Jun 9

from @REBusiness: MassDevelopment Provides $29M in Bond Financing for Affordable Seniors Housing Project in Lynn, Massachusetts - rebusinessonline.com/massdev… @MassDev @easternbank

1

17

Apr 27

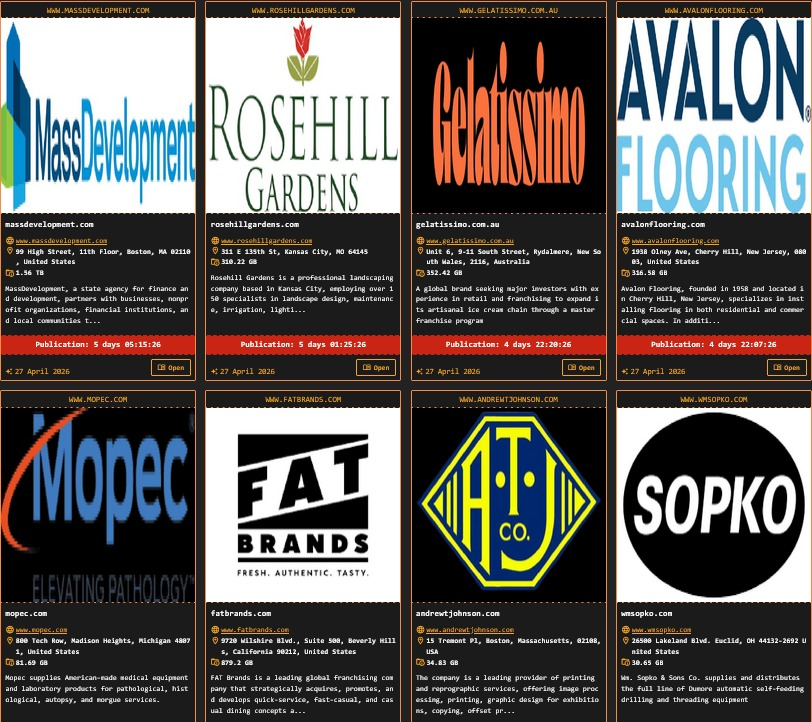

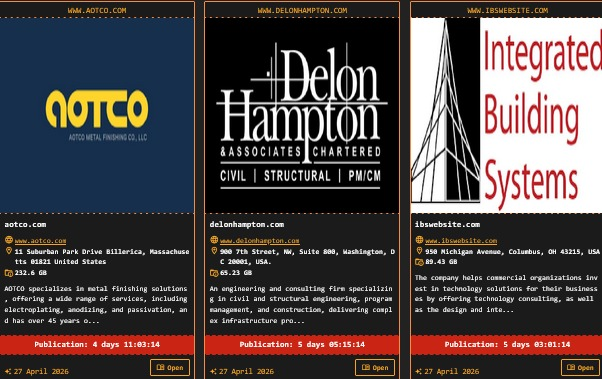

🚨 Ransomware Alert 🚨

DragonForce Ransomware group has added 11 new victims to their dark web portal.

- Integrated Building Systems 🇺🇸

- Delon Hampton & Associates, Chartered 🇺🇸

- William Sopko & Sons Co. 🇺🇸

- Andrew T Johnson Co., Inc. 🇺🇸

- Gelatissimo 🇦🇺

- AOTCO Metal Finishing LLC 🇺🇸

- Avalon Flooring 🇺🇸

- Mopec 🇺🇸

- Rosehill Gardens 🇺🇸

- FAT Brands Inc. 🇺🇸

- MassDevelopment 🇺🇸

3

1,962

Mar 2

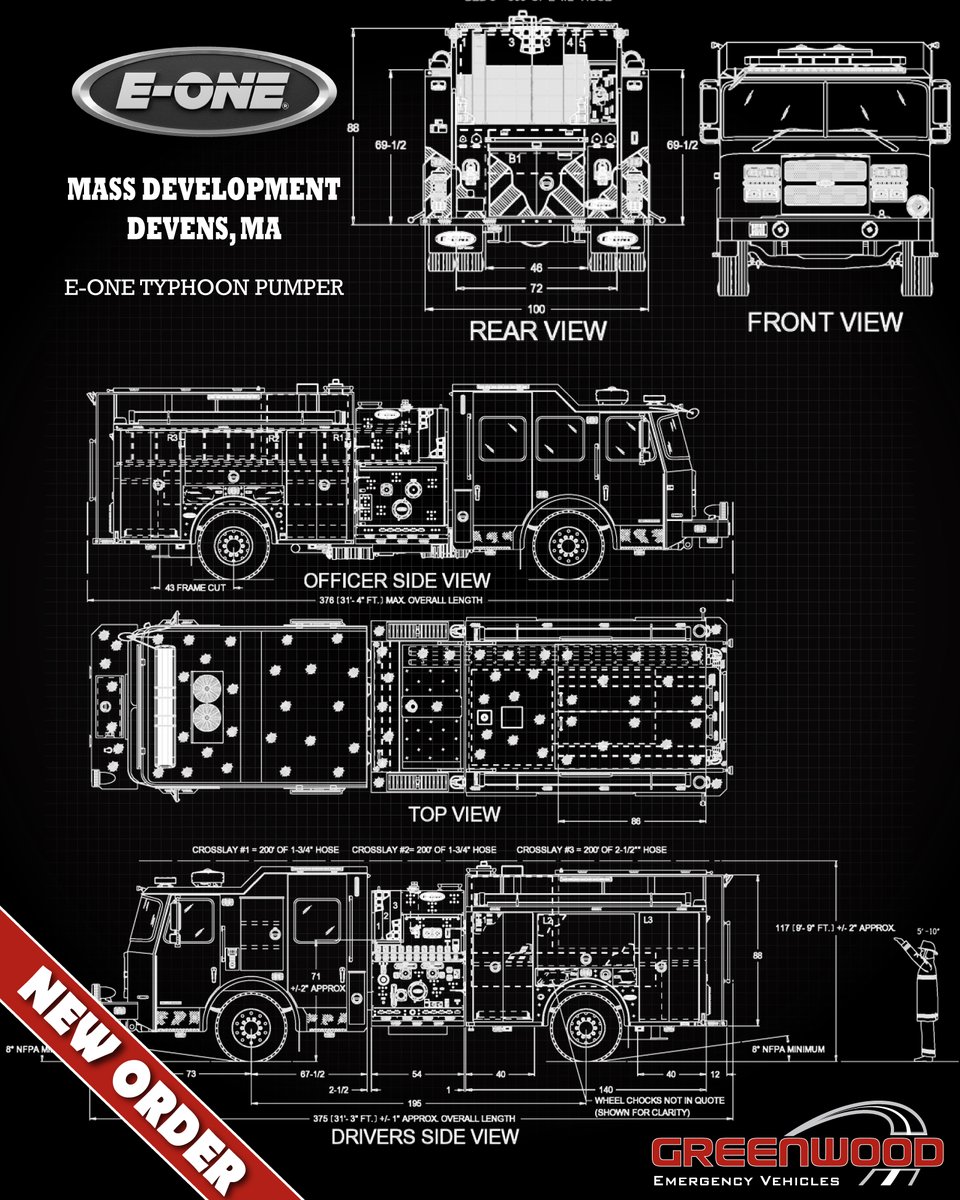

Congrats to MassDevelopment, Devens MA on the purchase of your new E-ONE Typhoon Pumper!

We truly appreciate the opportunity to work with you once again and are proud to be your partner on this project. We look forward to supporting you throughout the build process and beyond.

4

9

514

Feb 20

CAN U SAY SOLYNDRA? You just invested $4M in this thing via MassDevelopment Emerging Technology Fund: "IndiGOtech will use the loan proceeds to supplement working capital and hire an expected 35 employees over the next two years."

3

2

8

588

Malden has been selected as a new Transformative Development Initiative (TDI) District by MassDevelopment.

The 3-year program will bring economic development expertise, grants & support to strengthen downtown businesses and placemaking efforts.

More here: buff.ly/bHoyZsY

1

3

238

MassDevelopment has loaned $4 million to the state's only electric vehicle manufacturer, which it says it will use to supplement working capital and add jobs. bizjournals.com/boston/inno/…

3

302

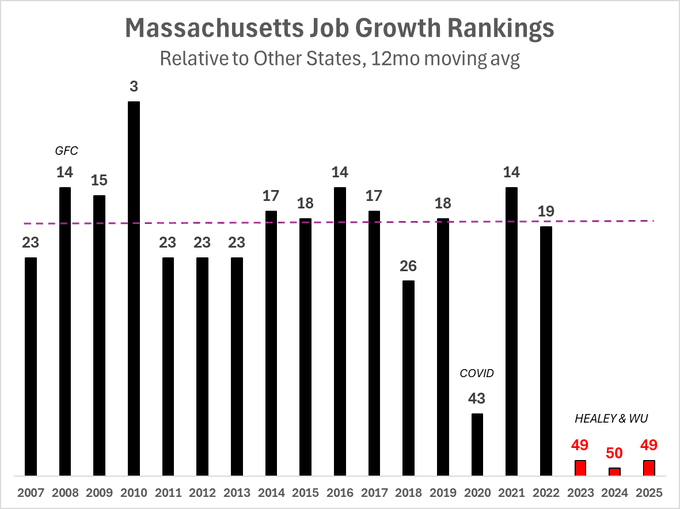

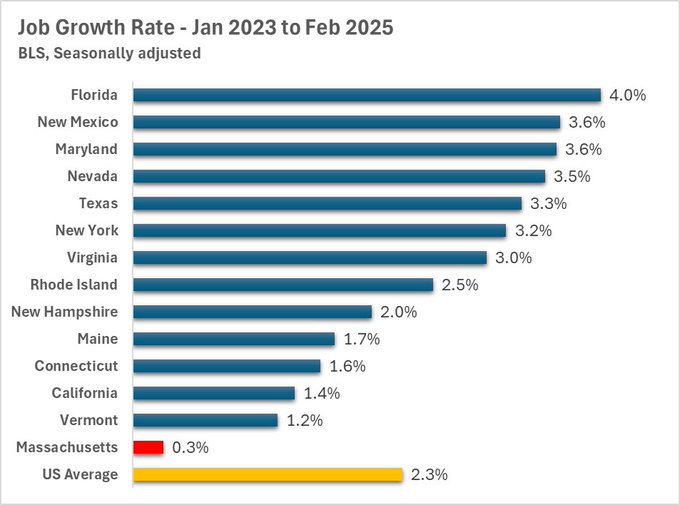

THE MASSACHUSETTS MILLIONAIRES SURTAX AND THE CHALLENGE OF RESTORING JOB GROWTH

Massachusetts’ recent reversal in employment performance represents a striking departure from its decade-long record of labor-market dynamism. After more than ten years of above-median private-sector job creation, the Commonwealth fell to the bottom of national rankings in 2023–2024, recording a 0.6 percent decline in private employment and ranking fiftieth among the states (Massachusetts Taxpayers Foundation 2025). The coincidence between this inflection and the passage of the four percent “Fair Share” surtax on income above one million dollars, approved by voters in November 2022 and effective for the 2023 tax year, suggests that the new levy has altered incentives in ways detrimental to growth.

The Surtax and Behavioral Response

The surtax reduces the after-tax return to entrepreneurship, partnership income, and capital gains, which together constitute the key channels through which high-income households create new enterprises and employment. Expectations of higher taxation influence decisions even before collection begins; the progression of the surtax from ballot qualification in mid-2022 to final approval later that year provided a clear signal to business owners and investors.

Recent judicial decisions reinforce these behavioral effects. In Welch v. Commissioner (2025), the Massachusetts Appeals Court upheld the state’s right to tax nonresidents on gains derived from in-state business activity, even after relocation. This expansive sourcing rule extends potential tax exposure beyond the point of exit and strengthens the incentive for high-income founders to plan relocations and investment decisions outside Massachusetts. Taken together, these developments plausibly explain the sharp deterioration in relative job growth that no national or long-standing local factor can replicate in timing or magnitude.

Other structural disadvantages, including high energy prices, housing scarcity, and persistent transit deficiencies, have burdened Massachusetts firms for years without preventing robust employment growth (Massachusetts Taxpayers Foundation 2019; U.S. Energy Information Administration 2024). Their endurance during the earlier boom suggests that the 2022–2023 reversal required a new, state-specific shock. The surtax uniquely fits that description. Broader macroeconomic and sectoral forces have also weighed on hiring, but these trends are national and cannot account for Massachusetts’ singular decline in job creation relative to its peers.

Policy Options for Reinvigorating Job Creation

How do we get back on the growth track? Outright repeal of the surtax would most directly restore competitiveness. However, its constitutional status and continuing popular support make repeal politically difficult. The state must therefore offset the surtax’s drag through measures that reduce costs and uncertainty without creating new administrative burdens.

1. Simplify and Accelerate Permitting. Enforceable “shot-clocks” for state and local approvals, with automatic approval if deadlines lapse, would provide the predictability investors require. Massachusetts already operates an expedited local permitting framework under Chapter 43D of the General Laws, which could be extended to a broader range of projects (Massachusetts Department of Housing and Community Development 2023). A complementary “permit-by-rule” regime for low-impact developments and an expansion of the pre-cleared “site-readiness” program would further reduce development timelines without additional bureaucracy (MassDevelopment 2024).

2. Modernize the Tax Treatment of Investment Interest Expense. Massachusetts currently disallows such deductions for individual taxpayers (Massachusetts Department of Revenue Directive 86-8). Clearly establishing deductibility of investment-interest expense in conformity with federal law would lower the cost of capital for in-state reinvestment. This reform would also likely reduce the outmigration of wealthy families.

3. Rationalize Occupational Licensing. A statute providing universal recognition of out-of-state occupational licenses would enable skilled migrants to work immediately, increasing labor-market fluidity without creating new boards or agencies. As of 2024, more than two dozen states have adopted such frameworks (Cicero Institute 2023).

4. Address Foundational Cost Pressures. Although high energy prices and infrastructure bottlenecks are long-term challenges, expanding pipeline and transmission capacity remains essential for stabilizing industrial and commercial electricity costs. The 2024 Massachusetts energy-siting reform law provides a foundation for more predictable infrastructure permitting through single-agency coordination and binding timelines (Massachusetts Executive Office of Energy and Environmental Affairs 2024).

5. Institutionalize Simplicity. Adopting a regulatory-budget or sunset rule that caps the aggregate number of regulations or paperwork hours, or that requires one regulation to be repealed for each new one enacted, would create a durable discipline of administrative simplicity (Cicero Institute 2023). Enhancing the existing Community One-Stop portal for economic-development permits to eliminate redundant data entry and provide real-time status tracking would further streamline interactions between businesses and government (Massachusetts Executive Office of Economic Development 2024).

Conclusion

The post-2022 slowdown in Massachusetts’ job creation most likely stems from the behavioral and expectation effects of the millionaires surtax rather than from the enduring structural costs that coexisted with growth during the previous decade. How can we restart the stalled growth and thereby secure the fiscal future of the Commonwealth? Because repeal of the surtax is politically constrained, the Commonwealth’s best path forward is a set of focused, bureaucracy-light reforms: faster permitting, modernized tax conformity, licensing mobility, targeted infrastructure streamlining, and regulatory simplification. Collectively, these measures would reaffirm Massachusetts’ reputation as a state that rewards innovation and enterprise, thereby restoring the conditions for sustainable employment growth even within the existing fiscal framework.

The Long-Term Economic Risks of the Massachusetts Millionaires Surtax

The Massachusetts Fair Share Amendment, popularly known as the “millionaires surtax”, imposed an additional 4 percent tax on annual personal income above one million dollars beginning in 2023. Proponents framed it as a progressive and sustainable revenue source dedicated to education and transportation.

In the short run, receipts have indeed exceeded expectations, generating over two billion dollars annually. However, early fiscal success masks the deeper structural and behavioral forces that threaten Massachusetts’ long-term economic vitality. The surtax changes the incentive structure for high-income households, closely held businesses, and entrepreneurs, gradually undermining the very tax base it was designed to tap.

In the near term, the surtax has primarily manifested through a pronounced deceleration in hiring and investment. Massachusetts has shifted from being a top-quartile performer in job creation during the 2010s to ranking last in the nation for private-sector employment growth in 2023–2024. The timing of this reversal closely aligns with the passage and implementation of the surtax. Businesses dependent on high-skill human capital and founder-led investment have become less inclined to expand locally, and many have redirected incremental hiring toward more tax-competitive jurisdictions. This initial stagnation represents the “first-order” impact—an early signal of capital reallocation rather than immediate firm closures or relocations.

The deeper effects are likely to unfold over a longer horizon. A substantial portion of the households subject to the surtax are not transient speculators but long-established families with complex ties to Massachusetts—children in local schools, businesses embedded in regional networks, and real estate holdings. Rather than exiting abruptly, these households are engaged in multi-year transition planning. Many are deferring relocation until children complete secondary education or until the sale of their Massachusetts-based business can be executed efficiently. Because of these demographic and financial frictions, the immediate revenue response to the surtax overstates its durability.

Massachusetts tax law further complicates mobility through what effectively functions as an “exit tax.” The state asserts taxing authority over non-residents’ gains from the sale of Massachusetts-based businesses if those gains are linked to in-state labor or operations. Courts have recently upheld this expansive sourcing doctrine, confirming that even after a taxpayer has changed residency, the Commonwealth may still claim tax on the appreciation of an enterprise built within its borders. This enforcement posture discourages early relocation but does not alter the ultimate calculus—it merely delays it. High-net-worth individuals are incentivized to remain nominal residents through the liquidity event, harvest offsetting capital losses through sophisticated investment accounts, and then emigrate permanently once the tax-efficient window closes.

The fiscal illusion created by this lag is substantial. In the early years of implementation, surtax revenues appear robust, as high-income residents remain on the tax rolls while completing transactions. Yet these inflows are effectively front-loaded: they represent one-time realizations of embedded gains rather than ongoing income streams. As the deferred migration unfolds, Massachusetts faces the erosion not only of surtax proceeds but also of its regular 5 percent income tax base. Each departing household removes a disproportionate share of total personal income, investment capital, and philanthropic activity, compounding the long-run contraction of the tax base.

From a macroeconomic standpoint, this dynamic threatens the state’s competitive equilibrium. Massachusetts’ growth model has long depended on its concentration of intellectual and financial capital. This capital is founders, partners, and high-skilled professionals whose risk-taking supports a dense ecosystem of innovation, education, and services. By materially reducing the after-tax return on those actors’ marginal decisions, the surtax discourages in-state reinvestment precisely among the individuals most capable of generating new enterprises and employment. Over time, the outflow of entrepreneurial talent and wealth will depress aggregate investment, diminish private-sector dynamism, and constrain future revenue elasticity.

The long-term risk is therefore structural rather than cyclical. In the coming decade, Massachusetts could experience a gradual hollowing of its high-income and high-growth cohort while fixed public expenditures expand on the assumption of stable surtax receipts. When migration and demography finally reconcile with fiscal expectations, the state may confront widening deficits, reduced capital formation, and declining competitiveness relative to peer innovation states. The pattern mirrors what empirical literature on state-level progressive surtaxes has observed elsewhere: initial revenue booms followed by tax-base erosion and slower economic growth once mobility and behavioral responses fully materialize.

In summary, the Massachusetts millionaires surtax has produced a short-term illusion of fiscal abundance but at the cost of weakening the long-run foundations of economic growth. The delayed migration and business-sale timing strategies of affluent taxpayers mean that the eventual revenue loss will emerge gradually over the next five to ten years. When it does, the Commonwealth will face the combined challenge of shrinking high-income residency, diminished private-sector expansion, and rigid spending commitments built on transient windfalls. The policy’s ultimate legacy may thus be not sustainable progressivity, but a self-inflicted erosion of the tax base and the economic dynamism that once made Massachusetts a national leader.

1

1

19

34,194

27 Oct 2025

The South Wharf and majority of the East Wharf in New Bedford will need to be closed for approximately two to three years due to necessary repairs, according to MassDevelopment.

turnto10.com/news/local/sout…

1

854

25 Aug 2025

Ken Fiola company response:

Company A: As noted above and as you are aware, a newly constituted FRLP Board of Directors was established in October 2021. It should be noted that prior to October 2021 all past members of the FRLP had resigned or their terms had expired.

In early 2021, the FRLP Board of Directors was virtually non-existent and had not met in a number of months. In April 2021, the Pier Manager abruptly resigned leaving the FRLP with no short tern or long-term management capacity. In an emergency action, the President of the FRLP and Mayor of the City asked that COMPANY A temporarily assume the management responsibilities of the Pier Corporation.

This was done without a FRLP Board vote and COMPANY A has served in a temporary management capacity to the FRLP since that time. At this time, there was no Conflict of Interest or appearance of a Conflict of Interest since the FRLP Board was essentially defunct and COMPANY A fulfilled this role at the request of the FRLP President and the Mayor of the City of Fall River neither of which had any standing on the COMPANY A Board.

Furthermore, COMPANY A had the demonstrated management capacity to undertake this task and bought their entire management team to the FRLP for a fee less than what was being paid to the Pier Manager, so there was no unjust enrichment.

As noted above, in February 2022, MassDevelopment requested that FRLP continue to serve as its agent, manage the State Pier and work closely with MassDevelopment. Since April 2021 COMPANY A has provided management services to the FRLP and has increased the net income profitability of the Fall River Sate Pier from $60,366.50 in 2021 to $224,888.89 in 2024.

2

3

36

4,208

25 Aug 2025

Chapter 665 of the Acts of 1945 gave the Commonwealth the right to construct a state pier with storage facilities in Fall River. The Fall River Line Pier, Inc. (FRLP) was chartered as a nonprofit in 1946 to lease a state pier from the Commonwealth to provide receiving, storing, and forwarding of freight and merchandise.

FRLP has been operating as an agent of MassDevelopment1 without a formal contract since its 50-year lease agreement2 with the Commonwealth expired in 2014. FRLP coordinates the day-to-day operations, security, and general maintenance of the Fall River State Pier, located at 1 Water Street in Fall River.

MassDevelopment currently operates and manages the Fall River State Pier and the New Bedford State Pier on behalf of the Department of Conservation and Recreation through an agreement with a December 1, 2017 effective date.

During the audit period, FRLP was overseen by a board of directors consisting of 10 members in 2020, 9 members in 2021, 9 members in 2022, and 8 members in 2023. The board is required to meet annually for the purpose of managing FRLP’s property and business. From July 1, 2020 through April 30, 2021, FRLP employed a general manager to supervise the pier’s daily operations, security, and maintenance personnel members.

Upon the general manager’s retirement in 2021, the FRLP board hired a nonprofit consultant firm, Jobs for Fall River, Inc.3. This is Ken Fiola's company.

1

5

34

1,999

28 Jun 2025

Museums and theaters need HVACs, but they come at a hefty price. The Mass Cultural Council and MassDevelopment announced that it would award $6.5 million across 74 arts organizations statewide for the maintenance "nobody talks about." bizjournals.com/boston/news/…

1

2

828

15 May 2025

Today, 10 family-sized permanent supportive housing units opened in Devens through a partnership between MassDevelopment, Clear Path for Veterans New England, and Soldier On. These public-private collaborations are vital to ending veteran homelessness in Massachusetts.

1

2

5

426

15 May 2025

This morning, Soldier On, ClearPath for Veterans New England, and MassDevelopment are gathering to celebrate the ribbon cutting of the renovated Fort Devens Veteran Housing!

We’re proud to welcome veterans home to a space that honors their service and supports their future.

2

5

93

MassDevelopment: Growth Capital Division helps small businesses in #Massachusetts strengthen & grow.

Learn more about how we can help ➡️ bit.ly/4ik2Yvn

3

2

166

17 Mar 2025

⚾ Meet the Competitors: FORGE/Cummings $20K Pitch Contest! ⚾

At "Scale Up Your Startup: Preparing Your Hardtech Company for Growth" on March 27, a group of innovative startups will take the stage to compete in the FORGE/Cummings $20K Pitch Contest! These companies are tackling some of the biggest challenges in hardtech, and they’re vying for a $20,000 rent credit at any of 11 Cummings Properties locations—plus cash prizes.

📅 Date: March 27, 2025

📍 Location: 300 Tradecenter 128, Woburn, MA

⏳ Time: 5:00 PM - 7:30 PM

Meet the startups making waves in hardtech innovation:

🔹 BioEchem – develops biological batteries that use P1, a naturally occurring microorganism, to drive electrochemical reactions without toxic chemicals. This innovative technology replaces traditional battery reagents with a sustainable, carbon-negative solution for safer energy storage.

🔹 Re-Volt Charging – builds sustainable EV infrastructure in gateway and underserved Massachusetts communities. Partnering with OEMs, they deploy DC fast chargers to ensure affordable electric mobility for all. Their vision is a universally accessible clean energy future.

🔹 SuryaTech – battery-integrated smart EV chargers provide innovative and efficient charging solutions. The company serves both direct consumers and businesses, including utilities and fleet operators.

These startups are pushing boundaries of innovation—who will take home the grand prize? Join us to find out!

What Else is in Store?

✅ Expert Panel Discussion – Learn from industry pros on how to align your workspace with your startup’s evolving needs.

🔹 James Trudeau – Chief Design Officer, Cummins Properties @cummingsdotcom

🔹 Shiv Bhakta – Founder and CEO, @ActiveSurfaces

🔹 Geetha Rao Ramani – VP Business Development, MassDevelopment @MassDev

✅ Networking Opportunities – Connect with other startups, suppliers, and ecosystem partners.

Be part of the excitement! Register now:

🔗 bit.ly/3F0yH5G

#FORGEImpact #PitchContest #HardtechInnovation #StartupGrowth #CummingsProperties

2

2

288

3 Mar 2025

Dear Maura Healey / Kim Driscoll / Simon Gerlin, Can you clarify the cyber incident at MassDevelopment (@MassDev). We provide the cyber tools:

1. What exactly happened?

2. What actions have been taken or are underway to resolve it?

3. How will you rebuild trust and restore your brand’s reputation?

Please let us know a convenient time to discuss. Thanks!

2

2

26