Jun 11

THETA TOKEN $THETA RETAIL INVESTORS / HOLDERS TOOK THE RISK. WHO CAPTURED THE REWARD?

THE ORIGINAL INVESTMENT THESIS APPEARS TO HAVE SHIFTED AWAY FROM THE PEOPLE WHO FUNDED THE ECOSYSTEM

Many long-term Theta Network investors are asking a question that should have been answered years ago:

What exactly did #ThetaToken holders receive in exchange for funding the growth of this ecosystem?

The original investment thesis was straightforward. Theta Token holders funded the network, secured the blockchain, absorbed the early risk, and provided the capital that helped transform Theta Network from a concept into a functioning project.

Investors accepted that risk because they expected that the people who financed #ThetaNetwork 's growth would ultimately be rewarded if the project ever achieved meaningful adoption and commercial success.

Instead, the story appears to have changed.

Over time, the focus increasingly shifted toward TFUEL. The economic narrative evolved from Theta Token being the centerpiece of the network to TFUEL becoming the asset supposedly positioned to benefit from future usage, computing demand, storage demand, AI demand, and network activity.

Theta Token holders were effectively told to wait. (You know, the ones who FUNDED the project to begin with, with their retail Theta Token investments)

Then wait longer.

Then wait again.

Years later, investors are still waiting.

The fundamental problem is not simply price performance.

The fundamental problem is the apparent disconnect between promises of future adoption and observable economic results.

After years of announcements, roadmaps, product launches, whitepapers, ecosystem expansions, Edge Network initiatives, Metachain initiatives, NFT initiatives, EdgeCloud initiatives, and AI initiatives, investors can reasonably ask a simple question:

Where are the customers?

A technology platform can launch products indefinitely. What ultimately matters is whether meaningful paying demand exists.

Without substantial customer adoption, every new initiative becomes another layer of infrastructure searching for a business model.

That creates a troubling perception among many early investors.

Theta Token holders supplied the capital.

Theta Token holders supplied the market valuation.

Theta Token holders supplied the liquidity.

Theta Token holders supplied the enthusiasm that allowed Theta Network to grow into a multi-billion-dollar project during previous market cycles.

Yet today many investors struggle to identify any clear path by which the capital they contributed was ever expected to produce a meaningful return for them.

If enterprise customers are paying Theta Labs directly, via USD cash, for services, investors naturally want to understand how those revenues benefit the ecosystem that funded the company's development.

If the answer is unclear, frustration becomes inevitable.

The reason many investors compare the experience to a crowdfunding campaign is not because they expected guaranteed profits.

It is because they increasingly feel they provided the funding while the promised economic flywheel never materialized.

The concern is not merely that adoption has been slower than expected.

The concern is that the value proposition itself appears to have shifted.

First the focus was Theta Token.

Then the focus became TFUEL.

Then the focus became future adoption.

Then the focus became future products.

Then the focus became future enterprise demand.

The destination always seems to remain somewhere over the horizon.

At some point investors stop asking when adoption is coming and start asking whether the economic model ever worked as advertised in the first place.

That question sits at the center of the growing dissatisfaction surrounding Theta Network today.

#crypto #digitalassets

7

9

32

1,486

Jun 10

THETA NETWORK'S AI DEMAND CLAIM HIGHLIGHTS A MUCH BIGGER PROBLEM

THETA NETWORK CONTINUES TO PROMOTE GROWTH STORIES WHILE THE THETA TOKEN VALUE CAPTURE QUESTION REMAINS UNANSWERED

Theta Network recently posted:

"GPU demand across the AI industry is at record levels, and Theta EdgeCloud is no exception. Demand on our network is at an all-time high."

The first half of that statement is not news.

Everyone knows AI demand is exploding.

NVIDIA is supply constrained.

Microsoft, Amazon, Google and Oracle are spending billions on AI infrastructure.

GPU demand across the industry is obviously at record levels.

The more interesting part is what Theta Network does next.

It immediately places Theta EdgeCloud beside one of the largest technology trends in the world.

That creates a subtle association.

Readers hear "record AI demand" and "Theta EdgeCloud" in the same sentence and naturally connect the two.

The problem is that industry demand and Theta EdgeCloud demand are completely different things.

Record AI demand globally does not prove meaningful adoption on Theta EdgeCloud.

The obvious questions remain unanswered.

How many paying customers?

How many GPU-hours sold?

What utilization rate?

What monthly revenue?

What customer retention?

What year-over-year growth?

Without those numbers, investors cannot determine whether "all-time high demand" represents significant adoption or simply improvement from a small starting point.

A company can double demand from a very low level and accurately claim an all-time high.

That tells investors almost nothing about commercial scale.

But the larger issue may not be the demand claim itself.

The larger issue is the growing disconnect between Theta Network's business initiatives and Theta Token holders.

Over the years, Theta Network has introduced one narrative after another.

Video delivery.

Streaming infrastructure.

NFTs.

TDROP.

Metachain.

Web3 media.

AI.

EdgeCloud.

Decentralized storage.

Now GPU computing.

Every new initiative is presented as another reason investors should be optimistic.

Yet one question continues to survive every narrative shift:

How does any of this create demand for Theta Token?

>>> Theta Token holders provided the capital. <<<

Theta Token holders took the risk.

Theta Token holders funded the ecosystem.

Yet what little commercial activity happens with Theta Network EdgeCloud appears designed around TFUEL consumption rather than Theta Token demand.

When AI jobs run, where is the mandatory Theta Token purchase?

When GPUs are rented, where is the mandatory Theta Token purchase?

When EdgeCloud grows, where is the mandatory Theta Token purchase?

The answer is usually indirect.

Staking.

Governance.

Network security.

Potential future demand.

Possible future ecosystem growth.

The problem is that indirect value capture is much harder to measure than direct value capture.

Investors are effectively being asked to assume that network growth will eventually benefit Theta Token.

The mechanism often appears more theoretical than observable.

This creates a fundamental risk.

Theta Network could succeed operationally while Theta Token holders receive far less benefit than expected.

Those outcomes are not mutually exclusive.

Another question deserves attention.

If Theta EdgeCloud demand is genuinely becoming significant, why is there no regular public reporting?

Public blockchains often speak about transparency.

Yet investors are frequently expected to evaluate progress without basic business metrics.

Imagine if a public company announced record demand every quarter but refused to disclose revenue, customers, utilization, or growth rates.

Investors would immediately ask questions.

The same standard should apply here.

The deeper concern is not whether Theta EdgeCloud is growing.

The deeper concern is whether Theta Network has spent years building products while never fully solving the value-capture problem for the asset most retail investors actually own.

Retail investors purchased Theta Token because they believed growth of Theta Network would ultimately increase the value of the asset they owned. Theta Labs itself raised substantial capital and built the company around the value created by Theta Token. Years later, investors can reasonably ask whether new products and business initiatives are creating value for the same asset that originally funded the ecosystem.

That question sits underneath every announcement.

Video delivery.

NFTs.

Metachain.

AI.

EdgeCloud.

Storage.

The technology may change.

The narratives may change.

The unanswered question remains exactly the same:

If Theta Network succeeds, where does the value flow?

And how much of it actually reaches Theta Token holders? #ThetaNetwork #Crypto #AI

1

19

834

Jun 7

THETA NETWORK'S BIGGEST UNANSWERED QUESTION

WHEN DOES THE TOKEN ECONOMY START REFLECTING THE ROADMAP?

For years, Theta Labs has introduced new narratives for Theta Network.

First it was decentralized video delivery.

Then Edge Nodes.

Then Elite Edge Nodes.

Then TFUEL staking.

Then ThetaDrop.

Then TDROP.

Then Theta Metachain.

Then EdgeStore.

Then Theta Video API.

Then EdgeCloud.

Then AI.

Every year the roadmap becomes larger.

Every year the list of products becomes longer.

Every year the vision expands.

What has not expanded at the same rate is the visible economic impact on the THETA and TFUEL ecosystems.

This creates an uncomfortable question that investors should examine carefully.

At what point does a growing list of products become evidence of adoption rather than evidence of strategic drift?

The whitepapers repeatedly describe future opportunities.

Theta Network's original vision focused on solving video delivery problems through decentralized infrastructure. Later whitepapers expanded into NFTs, decentralized storage, Web3 business infrastructure, Metachain architecture, and now AI and cloud computing.

The scope of the project has continuously widened.

The challenge is that each new initiative creates a higher burden of proof.

Investors are no longer evaluating a single business thesis.

They are evaluating multiple business theses simultaneously.

Video delivery.

NFT infrastructure.

Web3 business infrastructure.

Storage.

AI compute.

Hybrid cloud services.

The critical question is simple:

Which of these businesses is currently generating MEANINGFUL demand that requires sustained acquisition and consumption of THETA or TFUEL?

Technology announcements are not the same thing as economic demand.

Partnership announcements are not the same thing as economic demand.

Roadmaps are not economic demand.

Whitepapers are not economic demand.

Eventually a network must demonstrate that users, customers, developers, or enterprises are creating enough activity to produce measurable pressure on the token economy.

Investors should ask for evidence rather than narratives.

How much recurring revenue is generated?

How much compute is being purchased?

How much TFUEL is being consumed by real customers?

How much of the EdgeCloud infrastructure is being utilized by PAYING enterprises? And If the platform is generating meaningful revenue from paying customers, (DOUBTFUL) what tangible benefit do retail Theta token holders receive, and through what mechanism is that value passed on to them?

How many customers would leave tomorrow if Theta Network disappeared?

Those questions matter more than any future roadmap.

The greatest risk to Theta Network may not be technical failure.

It may be the possibility that the roadmap continues expanding faster than the adoption base.

A project can survive technical challenges.

It is much harder to survive an indefinite gap between vision and measurable demand.

That gap is where investors should focus their attention.

#ThetaNetwork #CryptoInvesting #Blockchain

1

10

499

Jun 4

ALL ROADS LEAD BACK TO THE SAME QUESTION WITH THETA NETWORK $THETA

THE PROBLEM MAY NOT BE THE TECHNOLOGY. THE PROBLEM MAY BE THE MARKET.

When I evaluate Theta Network today, I no longer start with the technology. I start with a much simpler question:

WHO IS ACTUALLY GOING TO PAY MEANINGFUL MONEY TO USE IT?

For years, Theta Labs has introduced new technical narratives. First decentralized video delivery. Then edge computing. Then NFTs. Then Metachain. Now EdgeCloud and AI computing.

The problem is not the lack of technology.

The problem is that after years of development, there is still no clear evidence that a major industry participant has decided Theta Network solves a problem they are willing to spend significant money to solve.

That distinction matters.

Technology only creates value when customers buy it.

The current flagship narrative is Theta EdgeCloud. According to Theta Labs' own white paper, the vision is a hybrid cloud-edge computing platform that could provide AI, video processing, GPU compute and other services at lower cost than traditional cloud providers.

That immediately raises the most important business question:

Why would a large enterprise choose Theta EdgeCloud instead of AWS, Microsoft Azure, Google Cloud, CoreWeave, Lambda Labs, Crusoe, or the dozens of established AI infrastructure providers already operating at massive scale?

Cost?

Reliability?

Performance?

Unique capabilities?

Distribution?

What exactly is the competitive advantage that would convince a major enterprise to move mission-critical workloads away from proven infrastructure providers?

The challenge becomes obvious when viewed through the lens of incentives.

Large enterprises do not buy infrastructure because it sounds innovative.

They buy infrastructure because it lowers risk, lowers costs, increases performance, or provides capabilities they cannot obtain elsewhere.

Theta Labs has spent years explaining what Theta Network is.

What remains unclear is why major customers would choose it.

This may explain why so many narratives have appeared over time.

The original Theta Network vision centered around decentralized video delivery and reducing CDN costs for streaming platforms. (solving "the last mile problem", etc) The 2018 white paper explicitly positioned Theta Network as a solution to video delivery inefficiencies and CDN expenses.

Years later, decentralized video delivery has not become a major commercial success story.

Then came NFTs.

Then Metachain.

Then AI.

Each narrative arrived before the previous narrative demonstrated substantial market penetration.

At some point investors must ask whether the issue is technological execution or market fit.

Those are very different problems.

A technology problem can be solved with engineering.

A market-fit problem is much harder because it requires discovering a customer need that is large enough to generate meaningful demand.

The token market appears to be recognizing this distinction.

Many investors continue hoping for a future bull market to rescue Theta Token price performance.

That assumption may be outdated.

Crypto markets are becoming increasingly focused on utility, revenue generation, adoption, and actual customer demand.

The question is no longer whether a blockchain has impressive technical architecture.

THE QUESTION IS WHETHER ANYONE NEEDS IT BADLY ENOUGH TO PAY FOR IT.

From my perspective, this is where the concern becomes most serious.

Theta Labs appears capable of creating technical concepts. (and generating patents)

What remains far less visible is the ability to convert those concepts into large-scale COMMERCIAL ADOPTION.

The history of Theta Network is filled with discussions of future possibilities. Hopeful ideas. Wishful thinking.

It is far less populated with examples of major paying customers generating meaningful network demand.

RETAIL THETA TOKEN $THETA INVESTORS HAVE SPENT YEARS WAITING FOR THE TRANSFORMATIONAL CUSTOMER.

The large enterprise.

The major platform.

The client whose usage creates undeniable economic value for the network.

THAT CUSTOMER STILL APPEARS ABSENT.

Meanwhile, team token sales have transferred significant value from retail investors to Theta Labs and its insiders over time. Investors are left evaluating whether those funds produced proportional commercial adoption or whether the majority of the value extraction has already occurred.

This leads to the uncomfortable conclusion.

The future of Theta Network may not depend on another technical release.

It may depend on whether Theta Labs can finally answer a question that has remained unresolved for years:

Who is going to pay substantial money to use Theta Network, and why would they choose it over everyone else?

Without a convincing answer, every new narrative risks looking like a SEARCH for a market rather than a solution to an existing one.

Can Theta Network recover?

Anything is possible.

But recovery would require more than optimism.

It would require multiple major commercial breakthroughs occurring after years of limited adoption.

That is not impossible.

It is simply a very high hurdle.

#Crypto #Blockchain #ThetaNetwork

4

2

26

2,046

May 30

THE THETA NETWORK–XYO ANNOUNCEMENT RAISES ONE QUESTION: "WHERE ARE THETA NETWORK'S CUSTOMERS?"

ANOTHER PARTNERSHIP. ANOTHER NARRATIVE. STILL NO CLEAR EVIDENCE OF DEMAND.

Theta Labs recently announced a partnership with XYO Network to build a blockchain-based verification layer for AI infrastructure. The stated vision is straightforward: combine Theta Network's EdgeCloud compute platform with XYO's data verification technology to create verifiable AI operations.

The announcement sounds ambitious.

THE PROBLEM IS THAT PARTNERSHIPS ARE NOT CUSTOMERS.

For years, Theta Labs has introduced new initiatives, new products, new roadmaps, new partnerships, new patents, new whitepapers, and new narratives. Video delivery. Edge computing. NFTs. TDROP. Metachain. Decentralized storage. EdgeCloud. AI infrastructure. Now verifiable AI infrastructure.

The pattern is familiar.

A new initiative is announced. The community celebrates. Expectations rise. Attention shifts to the next future opportunity.

Yet the most important question remains unanswered.

WHERE ARE THE CUSTOMERS?

Not pilot programs.

Not proof-of-concept demonstrations.

Not partnership announcements.

Not technical integrations.

Customers.

Who is paying meaningful recurring revenue to use Theta Network infrastructure?

Which enterprises are generating substantial demand for EdgeCloud compute?

How much AI workload is actually being executed on Theta Network infrastructure today?

How much TFUEL demand is being created from real commercial activity rather than speculation?

These are the metrics that ultimately determine whether a business succeeds.

The XYO partnership itself highlights the issue.

The partnership focuses on verifying infrastructure performance, uptime, throughput, and operational data. IF THERE IS NO MEANINGFUL CUSTOMER ACTIVITY, WHAT EXACTLY IS BEING VERIFIED?

VERIFICATION ONLY BECOMES VALUABLE WHEN THERE IS MEANINGFUL ACTIVITY TO VERIFY.

If large numbers of customers were already consuming substantial AI compute resources through Theta Network, the business case for independent verification would be obvious.

That naturally leads to another question.

How much demand currently exists that requires this verification layer?

Investors should pay close attention to the difference between infrastructure capability and infrastructure UTILIZATION.

A network can have patents.

A network can have enterprise validators.

A network can have technical partnerships.

A network can have thousands of edge nodes.

A network can have ambitious roadmaps.

None of those automatically create paying customers.

The technology question and the adoption question are completely different questions.

Theta Labs continues to attempt to expand the technology story. Is this smoke & mirrors? Gaslighting?

The missing piece remains the commercial story.

How many enterprise customers are purchasing compute?

How much recurring revenue is being generated?

How much organic demand exists without relying on future expectations?

The Theta Network–XYO announcement does not answer those questions.

It raises them.

And until clear evidence of significant customer adoption emerges, investors may want to focus less on partnership headlines and more on the metric that ultimately matters:

WHERE ARE THE CUSTOMERS?

#Theta #Network #token #crypto #cryptocurrency #digitalassets $THETA

3

5

28

1,687

May 30

The team is working really hard to revive web3. We got sick and tired of failed promises by fake devs projects farming their community with ads......Incase you don't know, metafoot is a layer1 blockchain.

Metachain is the Ecosystem

$foot is the coin

Metafoot is the company

2

1

2

347

May 24

The Jerry Kowal Lawsuit: Inside the Allegations Surrounding Theta Network's Most Controversial Years

A former executive's lawsuit raises questions about token launches, insider incentives, NFT activity, AI marketing claims, employee investments, and the business practices behind Theta Network's "evolution". The allegations remain unproven, but the scope of the complaint is difficult to ignore.

For years, supporters of Theta Network have been told that the next major breakthrough was "just around the corner." Retail investors of Theta Token $THETA WAITED AND WAITED for anything substantial to occur, or any way for their tokens to increase in value.

First came decentralized video streaming.

Then premium entertainment partnerships.

Then NFTs.

Then Metachains. "SUBCHAINS"

Then artificial intelligence.

Each new initiative was PRESENTED as "evidence" that Theta Network was positioning itself at the forefront of the next major technological trend.

Now a lawsuit filed by former executive Jerry Kowal challenges that narrative and attempts to present a very different account of what was happening behind the scenes.

The complaint names Theta Labs, parent company Sliver VR Technologies, and CEO Mitch Liu as defendants. Across dozens of pages, Kowal alleges misconduct involving token launches, employee compensation, NFT marketplace activity, private investments, internal governance, retaliation, and the company's evolution from media platform to NFT marketplace to AI infrastructure provider.

The complaint may represent one of the most comprehensive insider critiques ever directed at Theta Network from a former senior executive.

Who Is Jerry Kowal?

One reason this lawsuit immediately attracts attention is the identity of the plaintiff.

According to the complaint, Kowal is not an outside critic, anonymous social media account, or former community member.

The lawsuit describes him as a veteran entertainment and technology executive who previously held positions at Netflix, Amazon, and CBS before joining the Theta organization in 2020. The complaint further states that he reported directly to CEO Mitch Liu and played a central role in securing major partnerships for the company.

According to the filing, Kowal helped negotiate relationships involving MGM Studios, Lionsgate, World Poker Tour, Katy Perry, Resorts World Las Vegas, and numerous other organizations that became prominent components of Theta's public-facing business strategy.

That background matters.

Many lawsuits rely heavily on assumptions or secondhand information.

Kowal's complaint is presented as coming from someone who claims to have spent years inside the organization while participating directly in major initiatives and interacting regularly with senior leadership.

His position inside the company is one reason investors may pay attention.

Why This Lawsuit Matters

The complaint is not primarily about salary disputes.

It is not centered on a disagreement over office politics.

It is not simply a termination case.

Instead, the lawsuit attempts to describe an entire operating philosophy.

The central theme running through the complaint is the allegation that publicity, token economics, strategic pivots, and insider incentives became intertwined in ways that allegedly BENEFITED INSIDERS while exposing employees and investors to significant risks. @SECGov @FBI

Repeatedly, the complaint alleges that major initiatives were valued for their public-relations impact and their ability to generate market attention.

According to Kowal, partnerships, token launches, NFT campaigns, Metachain projects, and AI initiatives often generated excitement and headlines, but the underlying business value allegedly DID NOT always match the public narrative.

If those allegations are eventually supported by evidence, they would raise fundamental questions about how investors interpreted years of announcements and strategic shifts.

The Alleged Pattern of Narrative Pivots

Perhaps the most striking aspect of the complaint is its attempt to connect multiple seemingly unrelated events into a single pattern.

According to the lawsuit, Theta's strategic focus repeatedly shifted toward whatever segment of the technology market was generating the most attention at a given moment.

The complaint points to a progression that moved through:

streaming and content licensing

entertainment partnerships

NFTs

Metachain ecosystems

artificial intelligence

Each transition was presented publicly as a significant strategic opportunity.

Kowal alleges that many of these initiatives generated substantial publicity while failing to establish durable business fundamentals at the level suggested by the surrounding narrative.

The lawsuit effectively asks a question that investors may find uncomfortable:

Was Theta Network building long-term businesses?

Or was it repeatedly repositioning itself around whichever narrative attracted the most market enthusiasm?

That question sits at the center of the complaint.

The TDROP Allegations

One of the most important sections of the lawsuit concerns TDROP.

The complaint alleges that a large token allocation designated as a marketing reserve existed outside the restrictions imposed on employee allocations. According to Kowal, insiders allegedly controlled unrestricted token supplies while employees were subject to vesting schedules that prevented immediate sales.

The lawsuit further alleges that substantial insider selling occurred while employees remained locked up and unable to access liquidity.

Kowal claims this process severely damaged the value of employee compensation packages that had been tied to token performance.

The significance of these allegations extends beyond TDROP itself.

The complaint portrays TDROP as the beginning of a broader pattern involving token launches and insider incentives.

The POG, Lavita, Replay, and Grove Allegations

According to the complaint, similar issues allegedly appeared across several subsequent projects.

The lawsuit references POG, Lavita, Replay, GroveWars, and other ecosystem initiatives, alleging that insiders received preferential allocations or enjoyed liquidity advantages unavailable to employees and ordinary participants.

Kowal alleges that employees were encouraged to participate financially in some projects while important information regarding token structures and insider incentives was allegedly not fully disclosed.

The complaint repeatedly emphasizes a common theme:

Different participants allegedly operated under different rules.

Whether that allegation can be substantiated remains one of the major questions that future litigation may explore.

The NFT Marketplace Allegations

Another section of the complaint focuses on ThetaDrop and NFT-related activity.

According to the lawsuit, Theta's NFT marketplace became a major strategic priority during the NFT boom.

The complaint alleges that certain marketplace activities created misleading impressions regarding demand and market participation. Specifically, Kowal alleges that false bids were generated on NFT auctions in order to create the appearance of stronger demand. @SECGov @FBI

These allegations remain disputed and unproven.

However, they stand out because they concern market activity rather than internal employment issues.

The complaint specifically references NFT launches connected to major entertainment partnerships and celebrity relationships.

The Employee Investment Allegations

The lawsuit also devotes substantial attention to employee investments.

According to the complaint, employees were encouraged to invest in company-related opportunities through SAFE agreements and token offerings. Kowal alleges that he personally invested significant amounts based on representations concerning future growth and participation in the company's success.

The complaint alleges that important information regarding governance, capitalization, token economics, and insider activities was not adequately disclosed.

These allegations are significant because they involve relationships between company leadership and employees who were simultaneously workers, token holders, and investors.

The AI Allegations

For many current investors, the most relevant portion of the lawsuit may be the allegations concerning artificial intelligence.

Today, Theta Network's public identity is increasingly centered on AI and EdgeCloud infrastructure.

According to the complaint, however, the company's AI pivot followed the broader explosion of enthusiasm surrounding generative AI technologies. Kowal alleges that some publicly promoted AI products were not proprietary breakthroughs but instead relied heavily on third-party technology.

The lawsuit specifically challenges how certain AI offerings were presented to partners and the public.

Whether those allegations withstand scrutiny remains uncertain.

But they strike directly at Theta Network's current strategic narrative.

The Retaliation Claims

The complaint also alleges that Kowal repeatedly raised concerns regarding company practices.

According to the lawsuit, those concerns included token launches, employee investments, NFT activity, and business conduct.

Kowal alleges that after raising objections internally he experienced retaliation, exclusion, and eventually conditions that led to what the lawsuit characterizes as constructive termination.

These allegations form a major part of the complaint's legal claims and provide the framework through which many of the other allegations are introduced.

WHY INVESTORS SHOULD PAY ATTENTION

Regardless of how the litigation ultimately unfolds, investors should understand what makes this complaint unusual.

The lawsuit is not built around a single disagreement.

It attempts to connect years of events into a unified narrative.

Token launches.

NFT marketplaces.

Employee investments.

Strategic pivots.

Artificial intelligence.

Corporate governance.

Partnership announcements.

Insider incentives.

The complaint argues that these events were not isolated incidents but components of a broader pattern.

The defendants will have opportunities to challenge every allegation.

Courts will evaluate the evidence.

Discovery may reveal additional information—or undermine aspects of the complaint.

That process remains ahead.

But investors should recognize that the lawsuit raises questions that extend far beyond one former employee's departure.

Who benefited from major token launches?

How were reserve allocations managed?

Were insiders subject to the same restrictions as employees?

How much value came from products versus publicity?

How much of Theta Network's evolution reflected genuine execution versus strategic repositioning around emerging narratives?

Those questions sit at the center of Jerry Kowal's lawsuit.

And they are unlikely to disappear simply because the complaint was filed.

#Theta #Network #token #crypto #cryptocurrency #digitalassets

2

1

4

1,111

May 23

Jerry Kowal Lawsuit Alleges Token Dumping, NFT Manipulation, AI Misrepresentation, and Retaliation at Theta Labs

A SECOND VERIFIED LAWSUIT filed by former Theta executive Jerry Kowal accuses Theta Labs, Sliver VR Technologies, and CEO Mitchell Liu of operating a pattern of alleged token manipulation, insider enrichment, deceptive business practices, NFT market manipulation, retaliation, and corporate self-dealing.

@FBI

@SECGov

CURRENT STATUS: These are allegations contained in a civil complaint and have not been proven in court as of this date.Core Allegations

Jerry Kowal alleges that Mitchell Liu and Theta Labs engaged in: Alleged token "pump-and-dump" schemes involving TDROP, POG, Lavita, Replay, GroveWars, and other Theta-affiliated projects.

Allegedly allocating large unrestricted token reserves to insiders while employees and investors faced vesting restrictions.

Allegedly selling insider token allocations before employee and public investors could sell.

Allegedly using major partnership announcements primarily to increase publicity and token prices rather than generate sustainable revenue.

Allegedly trading around partnership announcements while benefiting from resulting increases in token market value.

Alleged NFT auction manipulation through false bids on ThetaDrop NFT launches.

Alleged manipulation involving Katy Perry NFT auctions and marketplace activity.

Allegedly encouraging employees to invest in token offerings while concealing insider advantages and token allocations.

Allegedly misrepresenting Theta's AI chatbot as proprietary technology when it was allegedly built around OpenAI services.

Allegedly paying sports organizations for chatbot deployments while promoting them as technology milestones.

Allegedly failing to properly address accusations that a Theta executive received more than $800,000 in kickbacks from a partner.

Allegedly retaliating against Kowal after he raised concerns regarding token activity, NFT practices, AI representations, and other conduct.

Major Partnerships Mentioned

The complaint references numerous business relationships and projects, including:

MGM Studios

Lionsgate Films

World Poker Tour

Katy Perry NFT partnership

Resorts World Las Vegas

Las Vegas Golden Knights chatbot deployment

Houston Rockets chatbot deployment

New Jersey Devils chatbot deployment

Lavita Metachain project

Replay Metachain project

POG Digital token project

Secret Pineapple Society NFT project

Former Theta Executive Paints a Damaging Picture of Internal Operations

Jerry Kowal was not an outside critic. According to the lawsuit, he served as Head of Content and helped secure some of Theta's most recognizable entertainment partnerships, including MGM, Lionsgate, World Poker Tour, Katy Perry, and others. The complaint portrays Kowal as one of the executives responsible for bringing major media relationships into the Theta ecosystem.

The lawsuit claims that after Kowal began questioning internal practices, he discovered what he describes as a pattern of token launches, insider allocations, hype-driven marketing, and token sales that allegedly enriched insiders while employees and investors suffered severe LOSSES.

One of the most serious allegations involves TDROP. Kowal claims that a large unrestricted marketing reserve was allegedly allocated to Mitchell Liu before launch. According to the complaint, Liu allegedly sold significant amounts shortly after launch while employee allocations remained locked.

The lawsuit claims the token subsequently lost more than 90% of its value.The complaint then alleges a similar pattern occurred with POG. Kowal says employees were encouraged to participate in a private sale while Liu allegedly retained access to unrestricted allocations.

The lawsuit claims insiders sold while employees were delayed from receiving their distributions, leading to substantial losses after the token's collapse.

The allegations do not stop with TDROP and POG. Kowal describes Lavita, Replay, and GroveWars as additional examples of projects that allegedly followed a similar pattern of launch hype, insider-controlled allocations, rapid declines, and losses for ordinary participants.

NFT Marketplace Allegations

The lawsuit also targets ThetaDrop. Kowal alleges that false bids were allegedly generated during NFT auctions in order to create the appearance of stronger demand and higher prices. The complaint specifically references NFT launches connected to Katy Perry and claims that artificial bidding activity misled buyers regarding market demand. If true, such conduct could raise serious questions about marketplace integrity because auction prices are often interpreted by participants as indicators of genuine demand.

AI Claims Under Fire

The complaint further alleges that Theta's AI chatbot marketing materially overstated the underlying technology. According to Kowal, sports-team deployments were promoted as significant AI breakthroughs, but the lawsuit claims the chatbot was largely a wrapper around OpenAI functionality rather than a proprietary Theta innovation.

The complaint further alleges that Theta paid sponsorship fees associated with certain deployments while publicly highlighting them as major technology achievements.The organizations specifically mentioned include the Las Vegas Golden Knights, Houston Rockets, and New Jersey Devils.

Secret Pineapple Society Allegations

Among the more unusual allegations is a dispute involving the Secret Pineapple Society NFT project. The lawsuit alleges that creator James Simmons reported evidence suggesting that a senior Theta executive demanded more than $800,000 in kickbacks connected to NFT listings. Kowal claims he brought the matter directly to Mitchell Liu and urged remedial action.

According to the complaint, Theta allegedly chose damage control rather than referral to law enforcement authorities. @SECGov @FBI

Retaliation Claims

The complaint ultimately argues that Kowal became a target after repeatedly raising concerns regarding token activity, NFT practices, partnership conduct, AI representations, and legal compliance. Kowal alleges that he was marginalized, excluded from leadership discussions, and eventually forced out after continuing to raise objections. That retaliation claim forms a central pillar of the lawsuit.

Why This Lawsuit Matters

The Kowal complaint goes beyond a simple employment dispute. The allegations strike directly at issues that crypto investors, regulators, and law-enforcement agencies often examine closely: insider token allocations, token sales by insiders, NFT marketplace integrity, representations about technology products, executive self-dealing, whistleblower retaliation, and corporate governance. None of these allegations have been proven in court. However, if even a portion of the allegations were ultimately substantiated, the issues raised would extend far beyond a workplace dispute and directly into questions regarding investor protection, disclosure practices, token markets, and public representations surrounding the Theta ecosystem.

Timeline

March 2020 — Kowal joins Theta/Sliver as Head of Content.

2020–2021 — Major partnerships secured with MGM, Lionsgate, World Poker Tour, and others.2021 — Theta pivots heavily toward NFTs and launches ThetaDrop initiatives.February

2022 — TDROP launches; complaint alleges insider allocation and subsequent sales.Late 2022 — Lavita Metachain project announced.Mid-2023 — Secret Pineapple Society kickback allegations reported internally.Late

2023 — POG token initiative begins.May 2024 — POG token controversy escalates and employee distributions become an issue.

2024–2025 — AI chatbot partnerships promoted with professional sports organizations.

May 2025 — Kowal formally details misconduct allegations and departs the company.

#Theta #Network #token #Crypto #Cryptocurrency #DigitalAssets $THETA

2

2

11

1,104

May 20

Is Theta Network an Intentional Long-Term Rug Pull?

TWO Lawsuits from previous executive level employees accusing Mitch Liu and Theta of fraud and other accusations, insider-sale allegations, and years of investor losses have fueled growing questions about whether Theta Network was designed to enrich insiders while retail investors carried the risk, and SUFFERED THE LOSS.

For years, Theta Network promoted an ambitious vision: decentralized video delivery, blockchain infrastructure, NFTs, edge computing, AI workloads, decentralized storage, and a future where growing network adoption would supposedly support long-term ecosystem value. Multiple whitepapers described shifting narratives, enterprise participation, staking economics, edge-node growth, and future compute services.

Today, many retail investors are asking a much darker question:

Was Theta Network simply an ambitious project that failed to deliver expected value, or was it allegedly structured from the beginning in a way that disproportionately benefited insiders while public investors absorbed the losses?

That question has gained additional attention because of legal disputes and allegations involving former insiders and company leadership. Public lawsuits and accusations have raised issues regarding token sales, internal conduct, business representations, and the handling of company affairs. The existence of litigation does not prove wrongdoing, but it does place claims that were once dismissed as internet speculation into a more serious arena where evidence, testimony, and records can / will be scrutinized.

Critics point to what they view as a troubling pattern.

The project repeatedly introduced new narratives: video delivery, enterprise adoption, NFTs, Metachain expansion, EdgeCloud infrastructure, AI computing, decentralized storage, and future ecosystem growth. None of these shifting narratives ever reach fruition to where it produced a price increase for Theta Token $THETA With YEARS of announcements and roadmap expansions, many investors remain deeply underwater compared with prior market-cycle highs.

Meanwhile, critics allege that founders, executives, and insiders may have had opportunities to realize substantial profits through token holdings and token sales long before ordinary investors had any realistic chance of recovering their investments, to the tune of multiple millions of dollars of profit.

Critics argue that the most overlooked flaw in Theta Network was not whether the technology could work—it was whether the Theta token would meaningfully benefit even if it did. The token's role was largely confined to staking, while the overwhelming majority of economic activity was designed to occur through TFUEL and off-chain business operations controlled by Theta Labs and its partners. This meant that even if decentralized video delivery, EdgeCloud services, AI computing, NFT platforms, and enterprise integrations had achieved widespread commercial success, there was no clear mechanism forcing a proportional increase in demand for the Theta Token $THETA itself. In other words, the technology could have succeeded while Theta Token $THETA holders still suffered severe LOSS. Critics contend that this represented a fundamental value-capture problem at the heart of the project: ecosystem growth did not necessarily translate into token-holder prosperity, making the investment thesis far weaker than many retail investors originally believed when they invested, EXPECTING A PROFIT. @SECgov

The question critics continue to raise is whether any of those developments created sustainable demand capable of meaningfully benefiting Theta Token $THETA holders—or whether the primary economic beneficiaries were the individuals and entities that controlled large token positions from the outset.

Critics respond that market downturns do not explain everything. They argue that if insiders allegedly extracted significant value while retail investors were encouraged to remain optimistic about future adoption, then the economic outcome begins to resemble what many investors describe as a long-duration extraction model rather than a conventional startup failure.

After years of losses, allegations, lawsuits, and ongoing questions regarding insider incentives, many investors are no longer asking whether the project succeeded.

They are asking who benefited most from its existence.

#Theta #Network #token #crypto #cryptocurrency #digitalassets

1

4

26

2,107

May 19

Tips & Tricks 💡

✦ .typed(MyProxy) gives you compile-time argument checking on cross-contract calls. The proxy is auto-generated by sc-meta all proxy from the target's ABI — never edit it by hand, just regenerate.

✦ .transfer_execute() is fire-and-forget — sends value plus a function call, doesn't await a response. Cheaper than .async_call_and_exit() when you don't need a callback.

✦ .sync_call() works for same-shard targets only. Cross-shard calls are async by protocol — you can't return synchronously across the metachain. Use .async_call_and_exit() with a callback when crossing shards.

✦ .payment(payment_obj) lets the same code path handle EGLD and ESDT transparently. Useful when an endpoint accepts either, or when you're forwarding whatever the caller sent.

1

1

13

205

Otherwise: no product launches, no new enterprise validators, no new EdgeCloud models. On-chain metrics holding steady too — Activity Index and Metachain Utilization Index both calm. Fundamentals, not catalysts. Quiet weeks are part of the trajectory.

1

6

191

May 13

Along with this new game which adds to our whitelabel system and opens doors for UE devs they have been seeking for a decade, I will be fully integrating to our existing lineup. This is how worlds become connected. At the base. PARACYT is the only METACHAIN

May 13

After many long uncelebrated hours I have completed the gridiron system and today I will be incorporating this and the PARACYT dashboard and building a game that runs on our network directly, this is the first SDK built by a chain founder and the first Game that will be built by a chain founder native to the chain, you will miss its significance even if I tell you in plain english.

1

4

8

113

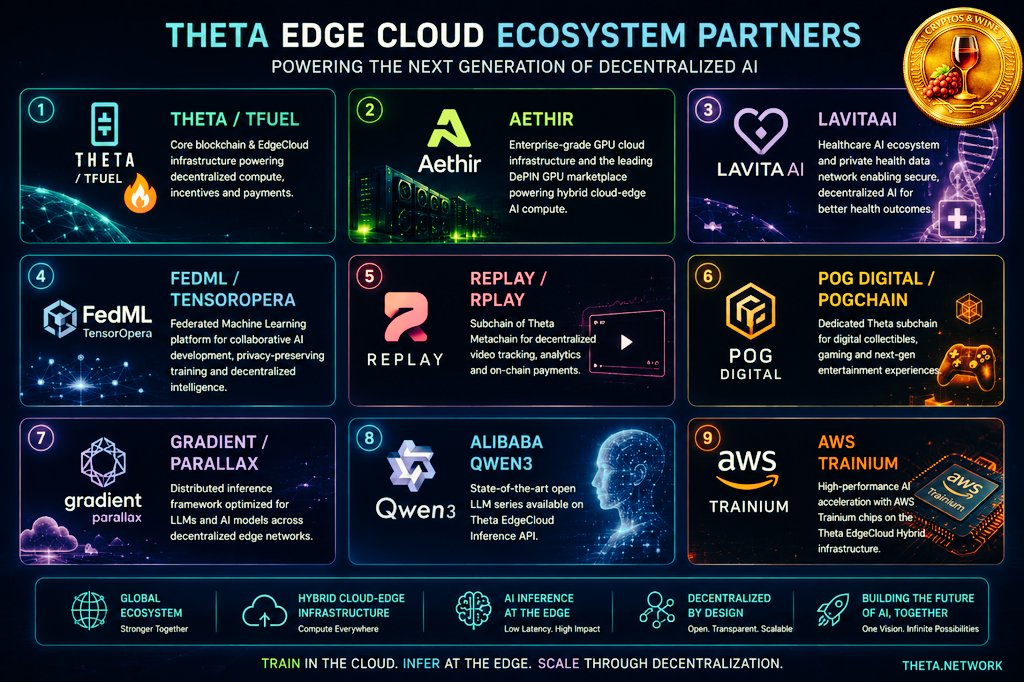

May 13

Category map for Theta ecosystem / crypto adjacent partners, because not every partner is a standalone crypto token. (Big SUMMARY cryptos only) (9 Categories of AI) Several of these partnerships have legs.

1. Hybrid Cloud-Edge Infrastructure

Aethir | Hybrid GPU marketplace with Theta EdgeCloud

FedML / TensorOpera | Federated ML and edge AI platform

LavitaAI | Healthcare AI workloads running through Theta Edge Nodes

Replay / RPLAY | Theta Metachain subchain for video tracking and payments(Legacy partner, quiet not much movement since 2022)

2. Distributed GPU Compute

Aethir | Most direct fit. Distributed GPU supply plus Theta EdgeCloud marketplace

Theta / TFUEL | Core decentralized edge node compute economy

FedML / TensorOpera | Distributed edge compute for collaborative ML

LavitaAI | Uses Theta Edge Nodes for AI jobs

3. AI Inference

Theta / TFUEL | EdgeCloud inference API and community node inference

LavitaAI | Healthcare AI inference and data workloads

FedML / TensorOpera | Deploying AI models across decentralized nodes

Gradient / Parallax | Distributed inference framework adapted for Qwen3 on Theta EdgeCloud

Alibaba Qwen3 | Open-source LLM now available through Theta EdgeCloud inference API

4. AI Training

LavitaAI | AI training jobs through Theta Edge Nodes

FedML / TensorOpera | Collaborative machine learning and model training

Aethir | GPU compute for model training and fine-tuning

Theta / TFUEL | Infrastructure layer for AI/deep learning jobs

5. LLMs and Multimodal AI

FedML / TensorOpera | Generative AI and collaborative ML

Alibaba Qwen3 | LLM inference on Theta EdgeCloud

Gradient / Parallax | Distributed LLM inference framework

Google Cloud | Video-to-text AI model pipeline collaboration with Theta

Theta / TFUEL | Model templates, AI APIs, and EdgeCloud deployment layer

6. AWS Trainium / AI Acceleration

AWS Trainium | AI acceleration hardware used through Theta EdgeCloud Hybrid

Theta / TFUEL | EdgeCloud Hybrid layer connecting AWS Trainium-style acceleration with distributed compute

Yonsei University / Syracuse University | Academic users tied to AWS Trainium research on Theta EdgeCloud

7. Healthcare AI

LavitaAI | Strongest fit. Healthcare AI, private health data marketplace, medical AI workloads

Theta / TFUEL | Edge node infrastructure supporting Lavita AI jobs

Seoul Women’s University / Emory / SeoulTech / healthcare-focused academic partners | Research-side healthcare AI users

8. Federated and Decentralized Computing

FedML / TensorOpera | Strongest fit. Federated learning, collaborative ML, privacy-preserving AI

Theta / TFUEL | Decentralized edge node network

LavitaAI | Private health data and decentralized AI participation

Aethir | Decentralized GPU infrastructure

Replay / RPLAY | Theta Metachain subchain ecosystem

9. Blockchain-Integrated AI Systems

Theta / TFUEL | Core blockchain and compute reward layer

LavitaAI / LAVITA | AI blockchain health data marketplace

Replay / RPLAY | Blockchain video tracking and payments on Theta Metachain

POG Digital / POGCHAIN | Dedicated Theta subchain for digital collectibles

FedML / TensorOpera | AI collaboration aligned with Web3 and decentralized agents

Aethir | DePIN GPU infrastructure partner

Most Important Highlights:

@Theta_Network Theta/ TFUEL

@AethirCloud

@LavitaAI

@FedML / TensorOpera

Replay / RPLAY

@PogDigital / POGCHAIN

Gradient / Parallax

@Alibaba Qwen3

@AWSAI Trainium

Cheers 🍷

1

14

50

898

elrond-erd-2:native

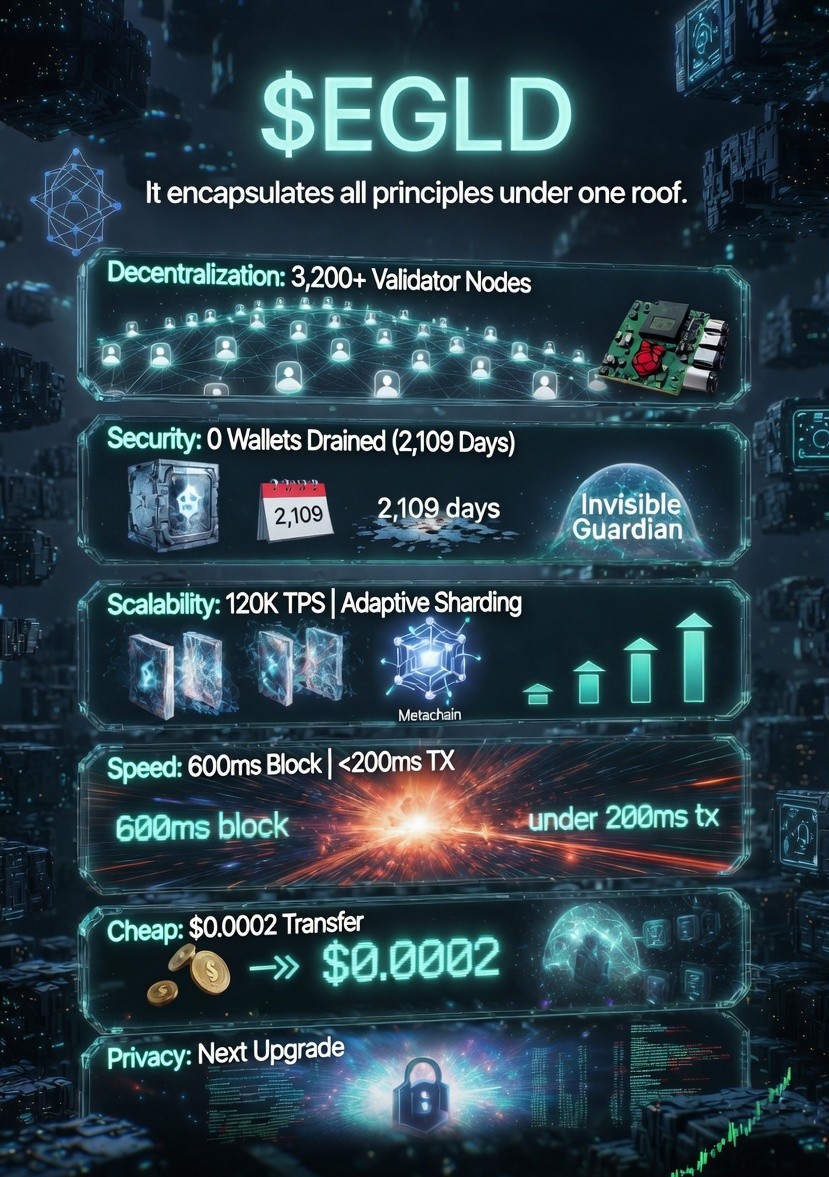

It encapsulates all principles under one roof.

1⃣. Decentralization: 3,200 validator nodes | low barrier entry - you can run a node on a raspberry pi.

2⃣. Security: 0 wallets drained since mainnet - 2,109 days | you can leak your secret phrase with Invisible Guardian or 2FA on-chain ON.

3⃣. Scalability: Full State Adaptive Sharding - 3 shards metachain | Scale with demand - add more shards | 120,000 TPS on Supernova testnet.

4⃣. Speed: 600ms block finality and under 200ms tx finality - with Supernova.

5⃣. Cheap: $0.0002 for a simple EGLD transfer.

6⃣. Privacy: After Supernova, privacy will be the next upgrade.

6

127

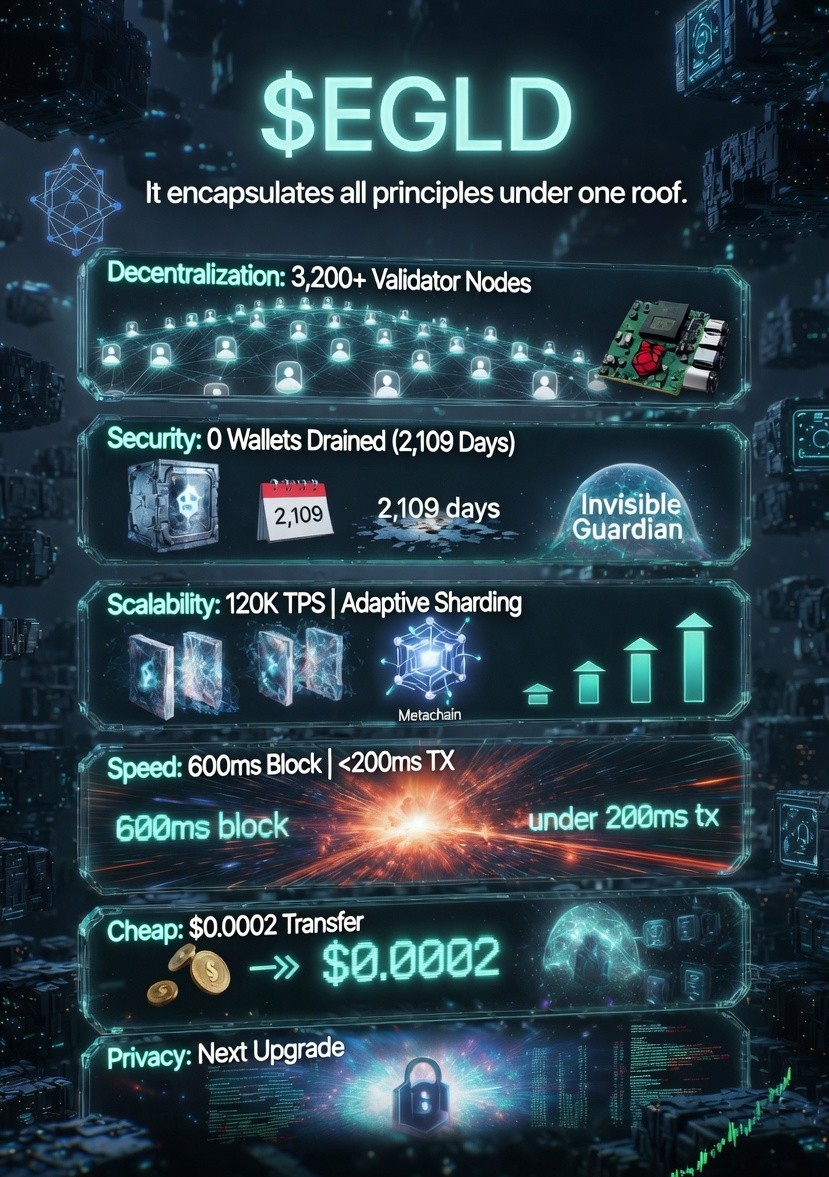

elrond-erd-2:native

IT ENCAPSULATES ALL PRINCIPLES UNDER ONE ROOF.

1⃣. Decentralization: 3,200 validator nodes | low barrier entry - you can run a node on a raspberry pi.

2⃣. Security: 0 wallets drained since mainnet - 2,109 days | you can leak your secret phrase with Invisible Guardian or 2FA on-chain ON.

3⃣. Scalability: Full State Adaptive Sharding - 3 shards metachain | Scale with demand - add more shards | 120,000 TPS on Supernova testnet.

4⃣. Speed: 600ms block finality and under 200ms tx finality - with Supernova.

5⃣. Cheap: $0.0002 for a simple EGLD transfer.

6⃣. Privacy: After Supernova, privacy will be the next upgrade.

1

37

118

7,741

3,600 elrond-erd-2:native IN FEES FOR 72M TXS IMPACT.

On the Supernova tests, we hit 120,000 TPS on the current setup ( 3 shards metachain), with the same hardware but, with 600ms block finality and even under 100ms for tx finality.

Imagine the mainnet hitting 120,000 TPS, not for 1 second, not for 1 minute but for 10 entire minutes.

We’re talking 72 million transactions processed live, no pauses, no excuses, no delays - all under real network load with actual value moving on the same setup at lightning speed.

No chain out there has ever sustained anything close to this kind of performance in a live environment. Not for 1 minute, let alone 10.

At the usual 0.00005 EGLD fee for a basic transfer, that run alone would use 3,600 EGLD in fees collected by the protocol, not paid for marketing campaign.

LET'S SPEND THE MARKETING BUDGET FOR ON-CHAIN ACTIONS THAT WILL TURN INTO FREE MARKETING CAMPAIGNS WORLDWIDE BY ITS OWN.

We need to prove our superiority at a scale nobody else can touch.

Supernova is the reset.

Public wallet is the spark.

This burst is the rocket.

Let's send it to the 🌕.

MULTIVERSX DEAD, THE NETWORK IS USELESS, PROGRESS IS HAPPENING TOOOOO SLOW, MARKETING, WHAT IS MARKETING?

Fair. Here's the fuller story.

Presenting the MULTIVERSX STATE OF THE FOUNDATION REPORT, 2ND Edition.

A few key highlights.

(a) 5 protocol upgrades. 6 governance proposals passed. Footprint down 60%.

(b) A full account for $EGLD holders, what was funded, what was built, what was ratified.

(c) A focused look at 2026, SUPERNOVA, and what comes next.

The picture is simple: the network has been rebuilt from the ground up. Set for a radical reset with the launch of SUPERNOVA. Ahead of this new GENESIS moment, we are documenting the work, clearing the record, and showing what was built.

There's one thing this team has been consistently known for, backed by the data: TECHNOLOGY SUPERIORITY, ENGINEERING EXCELLENCE, PRODUCTIVITY OUTPUT, that benchmarks at the top of the industry. Delivered with a team a fraction the size of our peers.

Some other things, I’ll say plainly, are far from optimal: chain focus, business pipeline, revenue traction.

SUPERNOVA is where we sharpen the first to a razor’s edge, and reforge the second.

The report is the receipt for the last two years, and the HIGH PERFORMANCE NETWORK WE HAVE LIVE TODAY.

Onward. To SUPERNOVA.

------

Read in full, here: files.multiversx.com/Multive…

7

30

104

3,013

🌌 @MULTIVERSX POWER 🌌

Adaptive State Sharding

[METACHAIN]

│

┌─────▼─────┐

│ SHARD ⚡ │10k TPS

│ SHARD ⚡ │ Dynamic

│ SHARD ⚡ │

└─────▲─────┘

Parallel Magic

1

22

265

Built a Theta Network AI assistant powered by live on-chain data. Ask it what Metachain score 47 means. Ask about staking APY. It knows. Runs on Theta's own decentralized GPU network. thetasimplified.com/use-edge… @Theta_Network

2

5

55

1,607