How many times as himself urged his xenophobic supporters to leave politics. An aside I don’t see what is happening in South Africa as politics but as laziness to take over someone’s else ppty.

3

@lisanandy Hello! Ms. Nandy, greeting of the day! Myself 8th generation direct descendent of Maharaja Ranjit Singh (Sajra Nasab 1891-92). UK Royal Family is the custodian of my family's wealth, including Kohinoor and no one is to interfere, personal wealth cannot be a state ppty.

6

Jun 14

Can I just say why the limp approach to homesteads being ppty tax free and why is only $250k being exempt (currently proposed); why can’t politicians, especially republicans, go all in for the citizens for once.

51

Jun 13

I’ve got Oceanfront ppty in Atlanta to sell you..You’re so gullible!

23

Jun 12

Yes the Metrocenter area is just as bad and often worse than ScaryVale now...highly comparable but because this area by Metrocenter historically used to be upper middle class so they have more infrastructure from that era whereas Maryvale has been plagued with crime and poverty since I was a child (I'm 49) That area by Metro also benefits from the surrounding tax base whereas Maryvale is surrounded by a mix of homes and heavy industrial areas (holds down ppty values) and the nicer areas with a higher tax base are way too far away to impact them

8

Jun 12

Most properties are geared to 80% or less. Are you saying investors over inflated ppty prices by 20% or more??!!

28

It's stupidity in motion. No wonder he is in consulting

You chose a mate based on who you would absolutely love to live your life with & the ideal you have in your mind.

It should not be based on random salary nos coz if the marriage breaks all of this is in vain plus he stands to lose money & ppty.

Iam not being dreamy but extremely practical. Of what value is a loveless life compared to a few lakhs here or there, especially when he has the financial might to withstand it ?

I have seen this enacted a few times & the results are not always pretty

35

I remarked upon clear racist rioting in Belfast where PoC were targeted & their ppty destroyed. Farage & Yaxley-Lennon, used their platforms to encourage those events in Southampton & Belfast.

Both are too cowardly to be involved in actual protest. They have idiots to do that.

2

1

149

Jun 12

Financially, this last 12 years has been a 'rollercoaster' ride for me and my husband, @Albert_Riopel.

Gladly, our three young adult children (@NYCARE_Wellness) were braved enough to help us along the way.

We noticed, as long as we stick with our 'monthly household budget', both of us will have enough resources to support us for our coming retirement years.

So, Albert and I started the process by considering the following factors:

First, how old we are.

*Our age, Albert (63 yrs old) & myself (59 yrs old).

Thus, Albert still need to work full-time for 2 years and at least 5 years for myself before retiring.

Second, what we need to have a comfortable retirement years.

*So far, we have enough housing for the both of us.

Even for my mom, who lives with us; she has alzheimer, other health issues and constantly requires our support and assistance on her daily activities.

Third, how much cash inflows we need to pay all our monthly expenses and investment capital.

*Our household budget is not easy. Out of $15,000 monthly spendings and investing capital, only $8,350 are fully-funded in cash through employment, and other cash fundings. The remaining $6,650 comes from funds generated through credits, leveraging, and investment withdrawals.

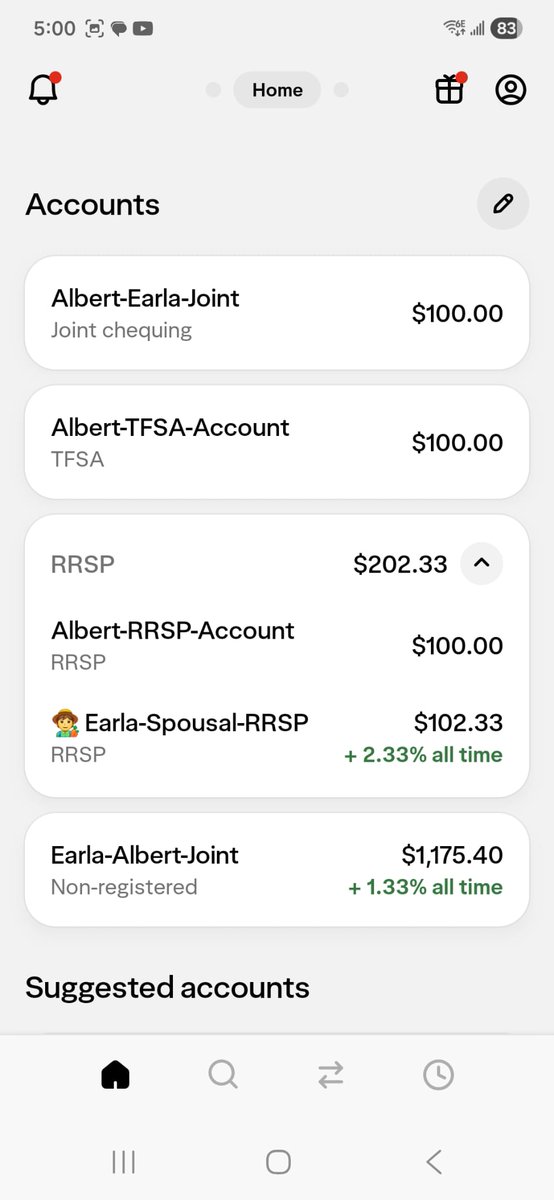

Fourth, how much pension income, RRSPs, TFSAs, and other cash sources we need during retirement years.

*Based on our future CPP and OAS pensions we likely received during retirement, and other possible cash sources, I think we are going to be fine, financially. We don't spend much. Our lifestyle is very simple, if we can do it ourselves, we just do it. Thus, we saves quite a bit.

Fifth, how much assets and debts we can handle before and during retirement years.

*Assets:

Marketable Securities = Cnd$76,000 approx.

Long-term Receivables = Cnd$135,000 approx.

Personal Properties = Cnd$125,000 approx.

*Real Estates:

(1) New Westminster, BC, Canada, Condo Ppty (67% Owned), 718 Sq. Ft., Cnd$506,000, as per BC Assessment. Current Market Value: N/A

(2) Lantzville, BC, Canada, Residential Ppty, .51 acre, Cnd$349,000, as per BC Assessment.

Current Market Value: N/A

(3) Point Roberts, WA, USA, Residential Ppty, 7,498 Sq. Ft., paid, US$38,000; Assessed at US$111,435, as per Whatcom County 2026 Property Assessment.

Current Market Value: N/A

(4) Conway, Mount Vernon, WA, USA, Skagit Valley (near Milltown Boat Launch), Undeveloped Land Ppty, 3.5 acres, paid, US$27, 900 in Sept. 2021.

Current Market Value: N/A

*Debts:

(1) Federal & Prov BC Student Aid (0% Interest): Cnd$35,000 approx.

(2) Vehicle Loan (0% Interest, 6yrs):

Cdn$70,700 approx.

(3) Credit Cards & Credit Lines:

Cdn$278,000 approx.

(4) Lantzville Property Financing:

Cdn$162,500 approx.

(5) New Westmisnter Mortgage:

Cdn$405,000 (67% Owed) approx.

*Net Worth:

Cdn$402,316.70 = ($1,222,985.20-$820,668.50) Approx. (Cost only),

*Note:

Net Worth is possibly higher, if Market Values (MV) of all 4 real estates are 'known'.

If MV is used based relevant factors, Net Worth is likely higher in the range: $402,316.70 to $970,056.70

Cc:

@NYCARE_Wellness,

@albert_riopel,

@blsbc,

@EarlaSportsPics,

@EarlaFoodPics

Nearing retirement can be a scary part of our lives. Just to think, you're getting a full paycheck from your 20s to 60s. But all of a sudden, retirement years hits you, and you're only getting half of that amount when you retire from work.

For Canadian retirees, will CPP and OAS combined enough to retire to?

Maybe. It really depends on related factors and lifestyle we are pursuing during retirement years.

We know that, mortgage(s) has to come down or paid off around retirement years. Housing costs shouldn't be more than $2,000/month.

Also, high interest loans and other debts must be paid off as soon as possible, or within at least 2-3 years. Work part-time if you need to.

It's a must to have a term life insurance that will pay all existing loans and related debts. A minimum of $500K is ideal for each spouse.

Finally, keep investing! There's a reason why in Canada 🇨🇦 we have TFSA and RRSP to help us, with tax savings, but it also helps us before and during our retirement years.

With us, we sort of used some of our RRSP and TFSA investments before retirement years.

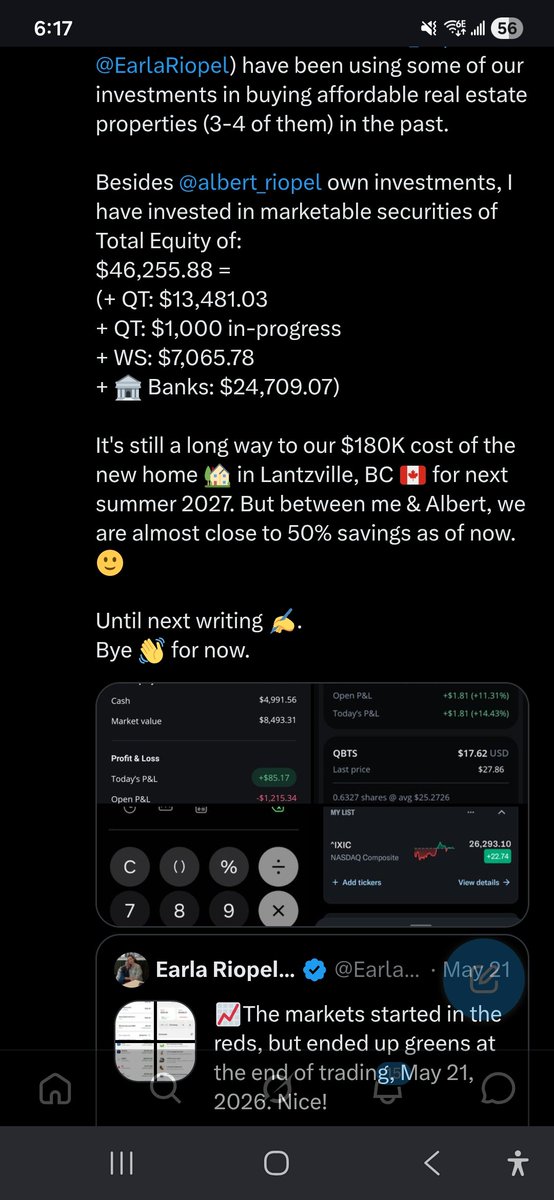

We bought four (4) real estate properties that we'll be using during retirement years. Two of these properties are paid off, and the other two has affordable mortgage payments.

For us, we only need two (2) properties, one in the mainland and one in the Vancouver Island. The other two properties in the mainland are more like investments properties, besides our marketable securities.

We need at least $180K to put a new home in our recent purchase of .51 acre in Lantzville, BC 🇨🇦 (Vancouver Island).

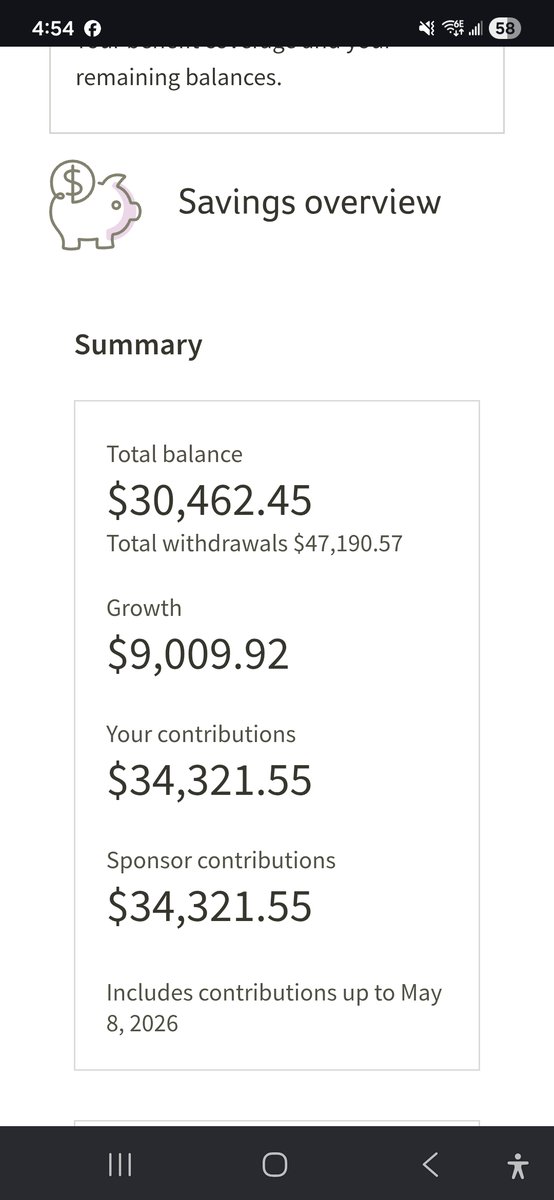

So far, we have at least invested the following marketable securities:

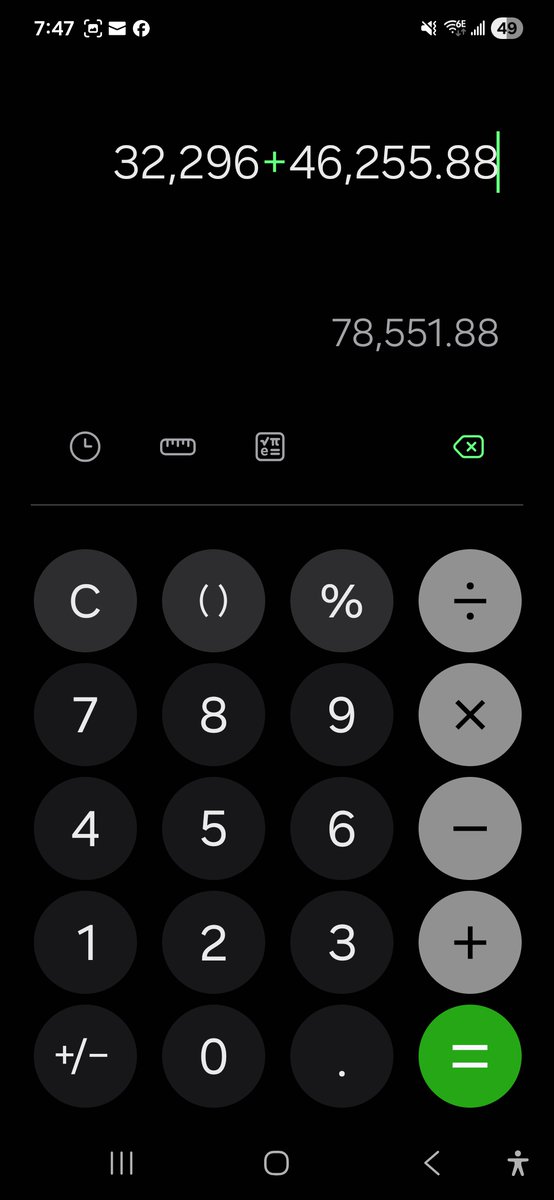

(1) Albert's ICOM RSP, 🏦 Banks RRSP/TFSA & Wealthsimple RRSP/TFSA accounts

= $32,296 Approx.

(2) Earla's Banks RRSP/TFSA, Questrade accounts & Wealthsimple accounts

= $46,255 Approx.

Overall Total of Marketable Securities

= $78,551 Approx.

So, we're at 43.64% of our $180K for our new home 🏡 in Lantzville, BC 🇨🇦.

If you're curious, I'll be attaching a bi-weekly screenshots of our investments, including our recently opened Wealthsimple. ^ER

3

5

386

Jun 12

A fair few are family holiday homes used in peak periods but let occasionally at other times to fund the outgoings including often very large land tax bills. A taxpayer subsidised personal holiday house. Not a genuine investment ppty.

3

169

No it won’t. That’s the theory - but when first home buyers are now CGT taxed to high hell on their ETFs / shares / ppty that they use to save for their first home deposit … it’ll mean nothing. Landlords will just be more picky about who they allow to be tenants.

1

14

Jun 11

why should we stay here? to pay for what the clowncil is doing? over a million to tell them how to work well with others? grade school stuff? billions in fraud? higher ppty taxes?

what is a woman? we don’t even get fair sport or our own spaces now

wth

12

Jun 8

Need major fact checking Premier. Canada isn’t in a recession- AB is losing thousands of jobs every month, we have negative real wage growth, you’ve cranked up expenses for HC, largest ppty tax increase in Calgary, we are losing drs, wait times⬆️, voter list fraud, corrupt care

1

4

25

277

Because they likely were in a high ratio/CMHC mortgage when the mortgage originated and the property value has gone down from what they paid.

Banks will only refinance up to 80% LTV.

It’s also possible they didn’t have a high ratio mortgage, put 20% down but due to ppty value decrease they are currently over 80%LTV.

4

1,194

May 30

mano kkkkkkkkk eu nao aguento mais ppty

5

91