Jun 13

GARP ETF offers US quality-growth equity with a rules-based, self-healing strategy. Since June 2020, GARP returned 237% vs SPY's 166%. Note for EU investors: PRIIPs/KID regulations make it… More: ravenquant.com/garp-etf-spy-…

#fintwit #fintwitt

12

𝗠𝗶 𝗯𝗿𝗼𝗸𝗲𝗿 𝗻𝗼 𝗺𝗲 𝗱𝗲𝗷𝗮 𝗰𝗼𝗺𝗽𝗿𝗮𝗿 𝗲𝗹 𝗘𝗧𝗙 𝗱𝗲 𝗕𝗶𝘁𝗰𝗼𝗶𝗻 𝗱𝗲 𝗕𝗹𝗮𝗰𝗸𝗥𝗼𝗰𝗸.

Soy europeo. La regulación PRIIPs lo prohíbe.

Y aun así, esta semana he cobrado 520 dólares operando sobre ese mismo ETF. De forma totalmente legal.

¿Cómo?

Las opciones cotizadas sobre el ETF no están bajo PRIIPs. Son derivados, otra categoría regulatoria. Y eso abre una puerta que casi ningún inversor europeo usa.

Vendí 5 puts sobre 𝗜𝗕𝗜𝗧 con strike 35. Si expiran sin asignación, prima al bolsillo. Si me asignan, recibo 500 acciones del ETF que mi broker no me deja comprar de forma directa.

La regulación cierra una puerta y deja otra abierta. Saber cuál es la que separa al inversor que se queda fuera del que sigue operando.

Operación entera y mi estrategia explicada aquí ▶️ youtube.com/watch?v=AFoMipkW…

11

1,207

Actually the luxembourg branch also goes around the issue in T&C "Where possible we will provide you with a UCITS KIID or PRIIPs KID or in your preferred language, but where this is unavailable the KID may only be made available in a different language. /1

1

2

68

$VOO and chill.

❌ Not allowed in Europe 🧵:

"No, a typical European retail investor cannot directly buy VOO (Vanguard S&P 500 ETF) through standard European brokers.

This has been the case since 2018 due to EU PRIIPs (Packaged Retail and Insurance-based Investment Products) regulation (and equivalent UK rules post-Brexit)."

1

1

3

93

May 28

Interessant tema.

Som jeg regner sjøl, så har frivillig (dvs eksludert tegning/innløsning) omløpshastighet siste 12mnd vært 98% i Veritas. Snitt kurtasje har vært 3.93bps (jeg gjør mesteparten sjøl på DMA samt noe blokker som er dyrere). Så transaksjonskostnaden har vært 0.0385%. I eiendomsfondet er tilsvarende tall 33% omløpshastighet og 5.73bps kurtasje (mindre likvide selskaper og større andel blokker) = 0.0189% transaksjonskostnad.

Om jeg ikke ekskluderer tegning/innløsning, ville det i Veritas blitt 39% høyere, dvs 0.0535% transaksjonskostnad. I tillegg kommer såkalt slippage, altså hvor mye beveger du kursene når du handler. I følge AI er det 0.05-0.20%, men fasit der er vel i praksis umulig å finne. I likvide papirer med mye dark-pool handel skulle jeg gjette det er i nedre enden.

Så bruker PRIIPS meg bekjent såkalt arrival price og execution price i sine beregninger og for meg kan det bli litt teoretisk. Ordre kan endres underveis både i størrelse og limit, hva er bid/ask (både intervall og størrelse), hva er i darks, hvilken algoritme blir brukt osv.

Hører gjerne innspill/synspunkter. Bruker mye tid på å gjøre handel så optimalt/billig som mulig

1

10

3,067

May 26

Convexity is my favorite word

Congrats man

Tried to buy $TE warrants a few weeks ago, but access is restricted to US retail and a handful of institutional funds, coz MiFID & PRIIPs blocks European retail without a KID.

1

8

1,352

May 16

People keep asking me how to buy that ETF everyone on Twitter shills - $VOO - because their broker doesn’t offer it.

Bro… that’s not a bug.....

You CAN'T buy the $VOO ETF in EUROPE because it does not comply with European regulatory frameworks known as PRIIPs (Packaged Retail and Insurance based Investment Products) and UCITS (Undertakings for Collective Investment in Transferable Securities).

To track the exact same S&P 500 Index, you must buy UCITS compliant ETFs. These funds hold the same US stocks, are fully legal for EU residents, and are regulated under European law.

The top UCITS alternatives to $VOO include:

$VUSA / $VUAA (Vanguard S&P 500 UCITS ETF): This is Vanguard's direct European equivalent to $VOO. $VUSA distributes dividends quarterly, while $VUAA automatically reinvests them.

SXR8 (iShares Core S&P 500 UCITS ETF): A massive, highly liquid alternative managed by BlackRock that automatically reinvests dividends.

$SPYL (SPDR S&P 500 UCITS ETF): State Street's European alternative, notable for having a very low total expense ratio (TER) of just 0.03%.

13

5

27

666

May 11

Con muchos productos bancarios ya de mano tienes que hacer un test de idoneidad que se pasan por el forro y tener la información 24horas antes para repasarla antes de firmar , reglamento PRIIPS.

3

160

May 10

De même, je n’ai jamais été un grand fan des ETF thématiques.

Et malheureusement, celui-ci n’est pas disponible en France pour les investisseurs particuliers européens à cause de la réglementation PRIIPs (absence de KID).

Mais ce qui est particulièrement intéressant ici, ce sont surtout les entreprises qui le composent.

Certaines sont extrêmement bien positionnées sur cette thématique avec de très bons fondamentaux, je pense notamment à SK Hynix, Micron SanDisk ou Samsung

1

1

1,084

May 9

Je t’invite à lire ce passage 👇🏻

⚠️ ETF US → non accessibles aux investisseurs particuliers européens (réglementation PRIIPs / absence de KID)

Mais ce qui est intéressant ici, ce sont surtout les actions qui le composent.

En revanche, tu peux tout à fait te positionner directement sur celles-ci.

3

438

May 8

Et voici probablement l’un des ETF les plus intéressants pour jouer un pilier ESSENTIEL de l’IA 👇

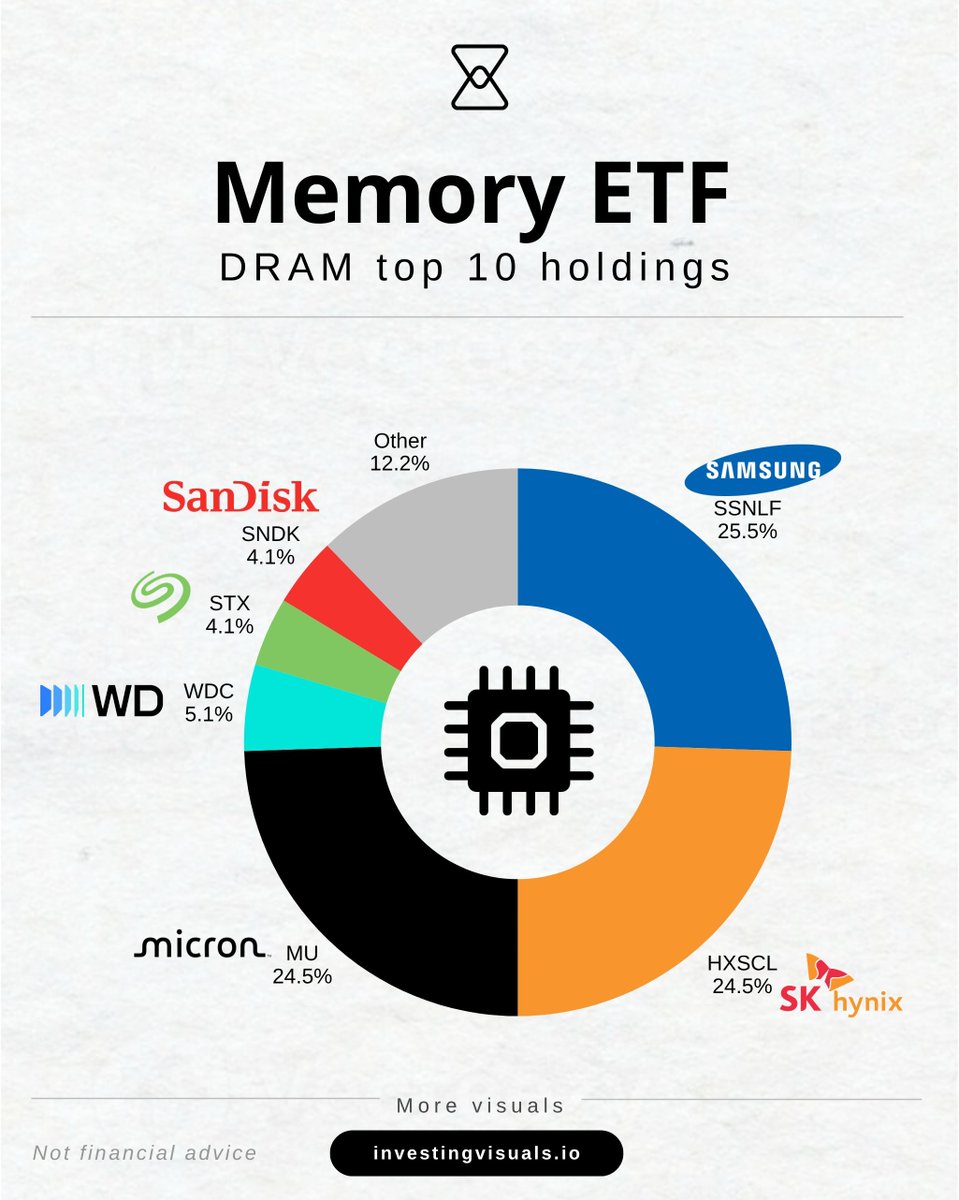

Le DRAM Memory ETF de chez Roundhill Investments

Pourquoi il est intéressant ?

Parce que derrière toute l’euphorie IA :

→ il faut des GPU

→ des data centers

→ du cloud

→ MAIS surtout… énormément de mémoire DRAM & NAND

Sans mémoire : pas d’IA à grande échelle.

Les 3 géants dominent largement l’ETF :

• Micron Technology – 24.5%

• Samsung Electronics – 25.5%

• SK Hynix – 24.5%

À eux seuls : ≈ 75% de l’ETF.

On retrouve aussi :

• Western Digital

• Seagate Technology

• SanDisk

En gros : les leaders mondiaux de la mémoire.

Autres infos :

• ETF récemment lancé

• Frais : 0,65%

• ISIN : US77926X3200

⚠️ ETF US → non accessible aux investisseurs particuliers européens (réglementation PRIIPs / absence de KID)

Mais le plus intéressant n’est pas forcément l’ETF lui-même.

C’est surtout le thème.

La mémoire est selon moi l’un des plus gros “goulots d’étranglement” de l’IA sur les prochaines années.

Personnellement : je suis actionnaire de Samsung.

Et SK Hynix & Sandisk sont également dans ma watchlist 🔎

J’ai détaillé toute la thèse IA les opportunités que je surveille dans cette newsletter 👇

Apr 26

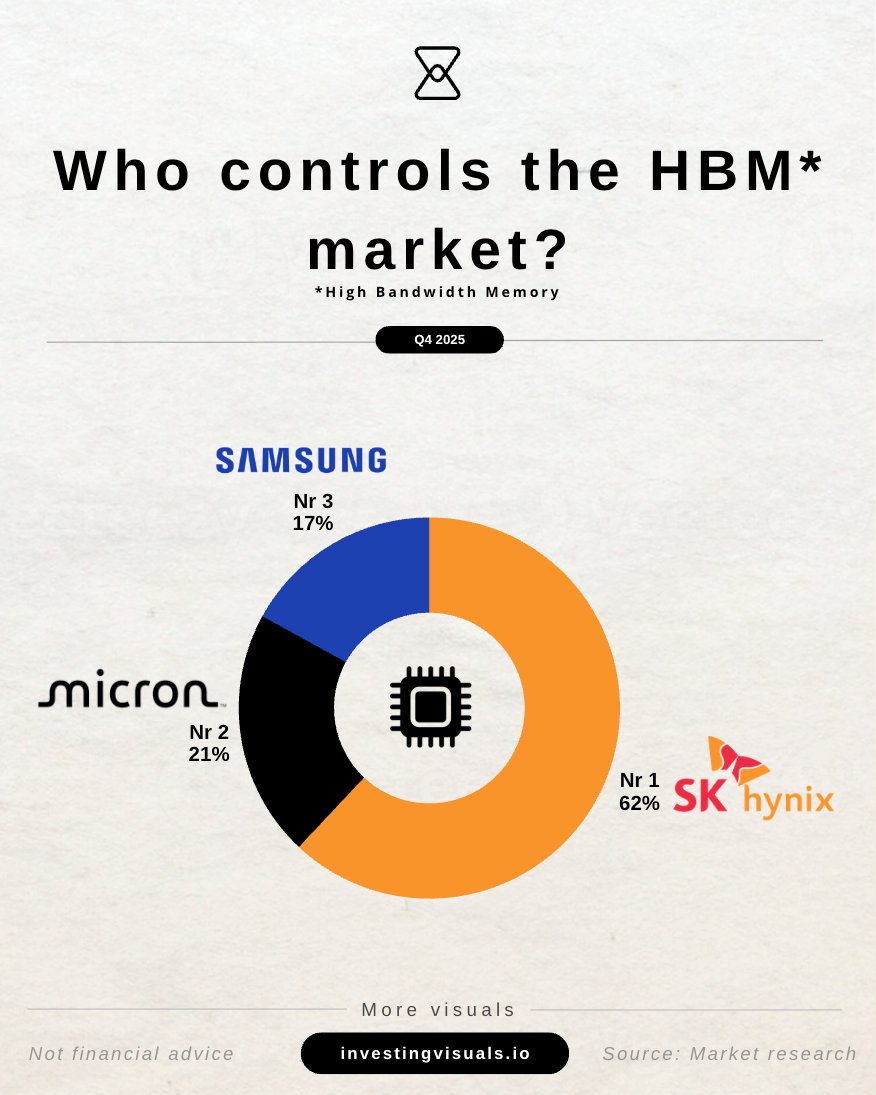

3 entreprises contrôlent le nerf de la guerre de l’IA.

Et presque personne n’en parle.

Le marché du HBM (High Bandwidth Memory) est verrouillé par :

• SK Hynix 61%

• Micron 21%

• Samsung 17%

Pourquoi c’est crucial ?

Le HBM est indispensable aux GPU d’IA.

Sans HBM :

→ pas de modèles avancés

→ pas de data centers performants

→ et donc pas d’IA à grande échelle

Le vrai gagnant aujourd’hui : SK Hynix

• Leader technologique (HBM3 / HBM3E)

• Fournisseur clé de NVIDIA

• Demande > offre → pricing power

📈 Résultat Q1 2026 :

• Revenus 198% YoY

• Profits 400% YoY

• Une des plus fortes dynamiques du secteur semi

Vous êtes positionné sur le HBM en bourse ?

9

5

73

43,406

May 8

OTC market structure quirk, with potentially a second layer depending on your account setup:

The US OTC mechanics piece (applies to all retail): The displayed ask isn’t a public order queue. When you see “OTCN $0.1044 × 6,000,” that’s Susquehanna International Group’s broker-dealer quote institutional market maker flow with their own customer priority.

Same with NITE (Citadel Securities), ETRF (Morgan Stanley), CDEL (Citadel), MAXM (Maxim). Retail orders route through wholesalers (Citadel Securities, Virtu Financial typically) which fill from their internalization pool first not against displayed quotes elsewhere.

Best-execution rules require the NBBO at the moment of execution, not crossing against external displayed quotes. Of yesterday’s 36.4M shares, roughly 23M went through dark pools and ATSs that retail orders never access. That’s institutional crossing flow.

The cross-border piece (depends on your broker): If your account is with a Swiss-domiciled broker (Swissquote, PostFinance, UBS Switzerland, Saxo, Cornèr, or even Interactive Brokers Switzerland AG / Charles Schwab International / Fidelity International these are European entities, not US), additional friction applies. PRIIPs/FIDLEG suitability checks, MiFID II execution rules, and longer routing chains (European order management → US clearing → US wholesaler) all add latency that bumps your order to the back of the queue.

Many EU/Swiss brokers also block OTC buys entirely on sub-$1 names while permitting sells.

If your account is a true US-domiciled broker (US Fidelity, US Schwab, US Interactive Brokers LLC), physical location in Switzerland doesn’t matter for routing then it’s the wholesaler mechanics piece only.

A few practical tests:

•Try a much smaller order (2,000-5,000 shares). If small clips fill but 50K-150K orders don’t, it’s just sizing — wholesalers handle small clips on OTC much more reliably than institutional-size limit orders.

•Check whether your broker is showing a “execution venue” or “fill report” if it routes to NITE or CDEL, you’re on US infrastructure. If you don’t see that detail, you might be on European compliance overlay.

•If you’re on a Swiss broker and trades just sit indefinitely, that’s the cross-border friction, not the company refusing to sell.

The thing that’s NOT happening: SGMO refusing to sell. Listed companies don’t sell their own stock against retail buy orders on the open market. The “they’re not even trying to sell anything” framing isn’t how this works there’s no “they” choosing whether your order fills. It’s market maker queues, wholesaler internalization, and (potentially) cross-border routing friction.

2

7

284

May 8

OTC market structure plus European broker access creates the issue you’re seeing. Two layers:

First, the displayed ask on OTC isn’t a public order queue. When you see “OTCN $0.1044 × 6,000,” that’s Susquehanna International Group’s broker-dealer quote, a US market maker offering to fill US institutional flow. Same with NITE (Citadel Securities), ETRF (Morgan Stanley/E*Trade), CDEL (Citadel), MAXM (Maxim Group). These aren’t retail sellers in a queue , they’re institutional market makers with their own customer flow that gets priority.

Second, & more important for you specifically: European retail orders for US OTC stocks face structural barriers. Your order routes from your Swiss broker (Swissquote, IB Switzerland, Saxo, PostFinance, etc.) through a longer chain European order management → US clearing → US wholesaler (Citadel Securities or Virtu Financial typically) → maybe an OTC venue. Each hop reduces priority.

PRIIPs/FIDLEG regulations mean many Swiss and EU brokers either block OTC buys entirely or place them in a slower compliance pathway that doesn’t get filled when there’s any friction.

Of yesterday’s 36.4M shares, roughly 23M went through dark pools and ATSs that European retail orders cannot access, that’s US institutional crossing flow.

Different brokers handle US OTC very differently:

•Most Swiss/EU brokers (Swissquote, PostFinance, UBS Switzerland, Cornèr): block OTC buys, sometimes allow sells of existing positions

•Interactive Brokers Switzerland: usually allows OTC buys but routes through US infrastructure with European compliance overlay; can be slow to fill

•Saxo Bank: variable, often requires phone confirmation for OTC under specific tiers

•DEGIRO: blocks most US OTC entirely

•US-based brokers (if you have access): Fidelity, Schwab, IBKR US all allow OTC with fewer restrictions

•JPMorgan Self-Directed (US): blocks OTC buys on sub-$1 names entirely; you can only sell existing positions

Two possible reasons your orders aren’t filling:

1.OTC market makers fill their own customer flow first retail orders don’t have priority access to displayed asks even when the asks are below your limit. Of yesterday’s 36M shares, ~23M went through dark pools that retail orders never touch.

2.If you’re using a Swiss/European broker (even ones with US branding like IB Switzerland, Schwab International, Fidelity International), your order routes through European compliance overlay that adds latency. If you’re on a true US broker (US Fidelity, US Schwab, US IBKR LLC), then it’s just the OTC wholesaler mechanics.

Try a smaller order (2-5K shares). Small clips fill on OTC much more reliably than 50K-150K. If small clips also sit unfilled, your broker is the bottleneck not the market.

11

268

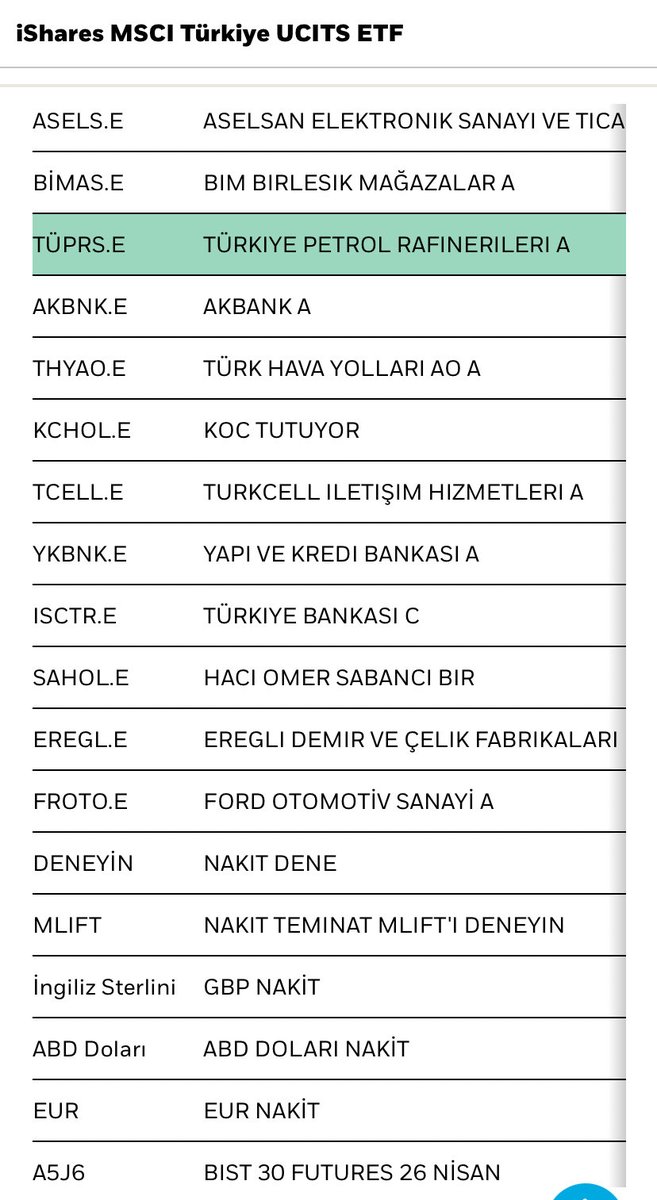

Apr 25

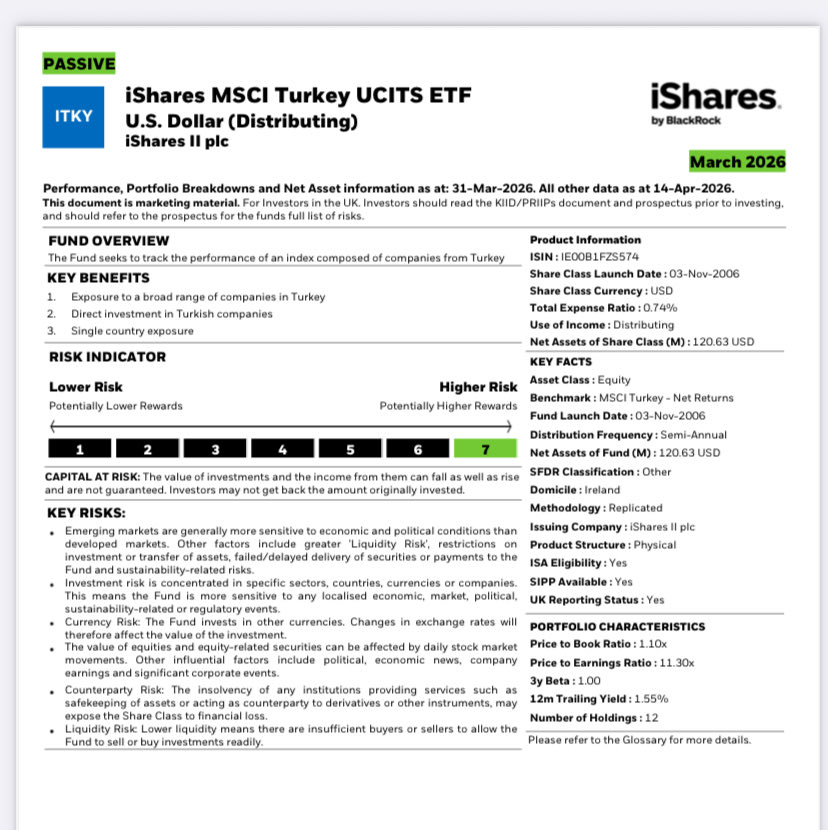

iShares MSCI Türkiye UCITS ETF

Mart 2026 raporu yayınlandı

Performans, Portföy Dağılımları ve Net Varlık bilgileri

Diğer tüm veriler 14 Nisan 2026 tarihi itibarıyladır.

Bu belge pazarlama materyalidir.

Birleşik Krallık’taki yatırımcılar içindir.

Yatırımcılar, yatırım yapmadan önce KIID/PRIIPs belgesini ve izahnameyi okumalıdır ve fonun tüm risklerinin yer aldığı tam liste için izahnameye başvurmalıdır.

blackrock

Fon bir önceki paylaşımda 22 usd iken

Cuma kapanış ile 24 usd seviyesinde işlem görüyor.

iShares MSCI Türkiye UCITS ETF

blackrock

Yatırım yaptığı şirketler aşağıda sıralanmıştır.

Bu fonun dünki getirisi yaklaşık

%1,43 yükselerek 22,03 usd den işlem görüyor.

Yıl başından bu güne fon yaklaşık dolar bazlı ,69 getiri sağladı!!!

9

5

145

8,387