🧲⚙️🇺🇸 "There's no such thing as rare earth. There's rare processing."

The real chokepoint in the rare earth supply chain isn't mining. It's separation. It's the step almost nobody in the West can do — oxide to metal. Metallisation. The missing link. 🧵

▶️ Watch: Anupam Ghildyal, COO of REalloys ($ALOY), on Stocktwits Boardroom Exclusives — breaking down the midstream processing bottleneck and what it actually takes to build a North American supply chain that doesn't run through Beijing.

🏭 What REalloys is actually building

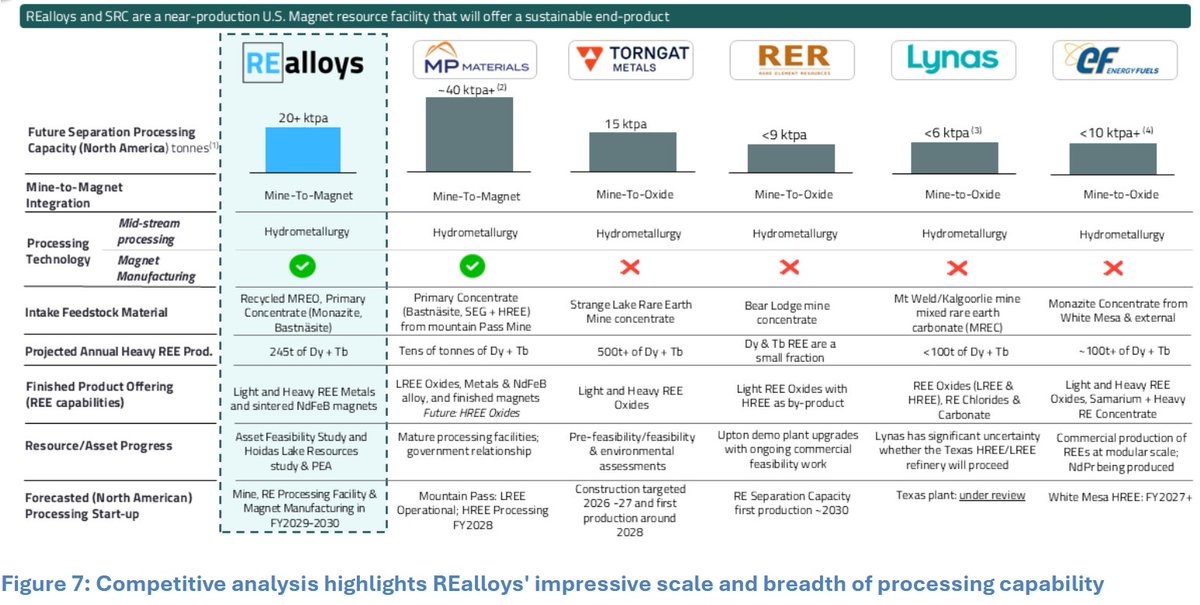

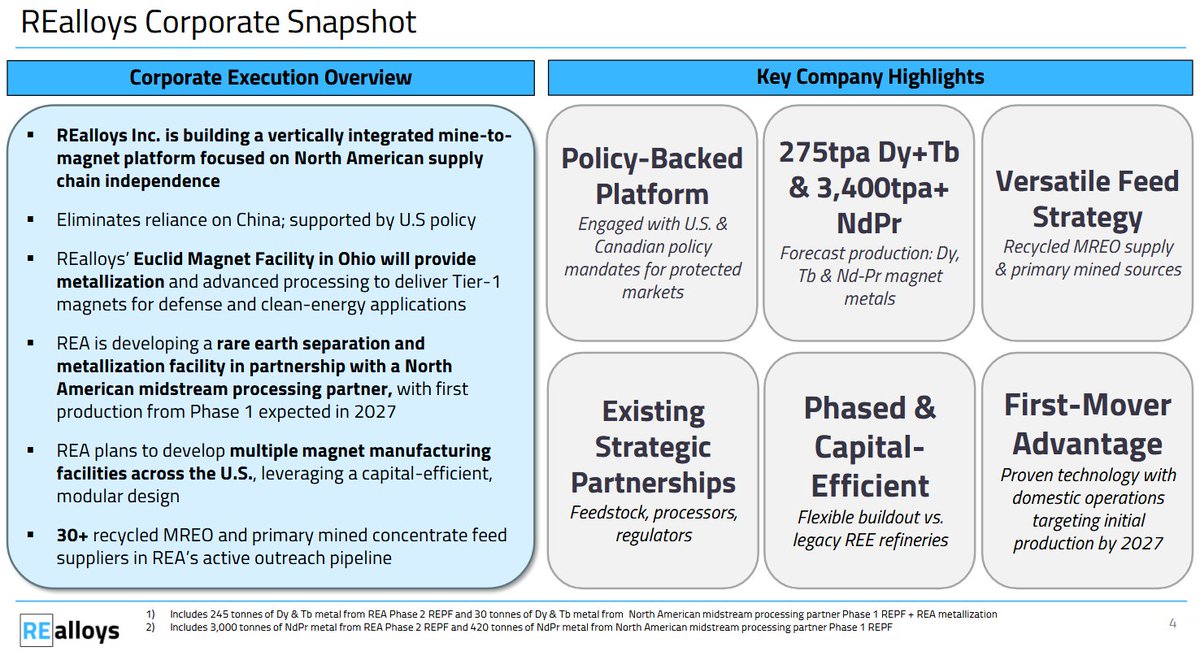

REalloys ($ALOY | NASDAQ) is the only company in North America with an integrated path to producing both heavy rare earth oxides and finished metals in time for the 2027 defense sourcing deadline.

Here's the architecture — all North American, zero China nexus:

Upstream → Hoidas Lake (Saskatchewan) — one of the only North American deposits with both LREEs and meaningful HREEs (Dy Tb). Allanite-apatite mineralogy = low radioactivity = simplified, HF-free processing. 2.2Mt M&I resource at 1.9% TREO.

Diversified feedstock → CRML Tanbreez (Greenland, 15% Phase 1 offtake — signed May 2026), St George Araxá Brazil (40% MOU), SRC monazite (3,000 tpy feed), Ramaco coal-hosted MREC (Wyoming), acid mine drainage (Mission Critical Materials), recycled end-of-life magnets.

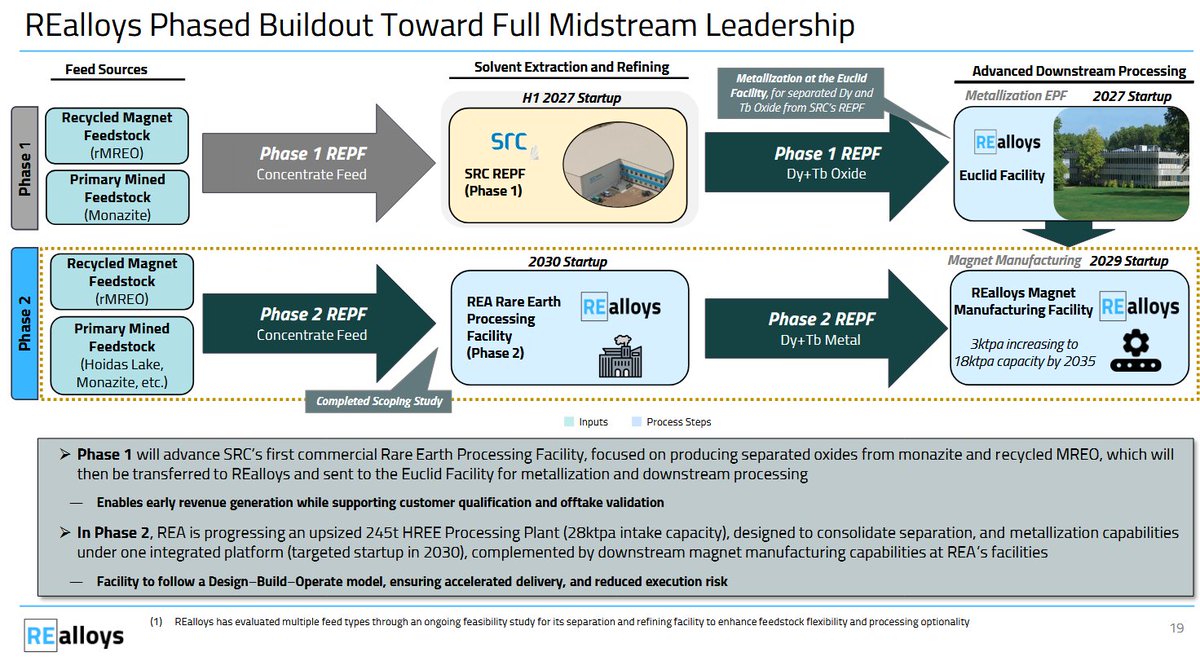

Midstream → Saskatchewan Research Council (SRC) — North America's only fully licensed facility capable of processing radioactive monazite under CNSC nuclear compliance — producing clean, separated REO without burdening US facilities with radioactive liability. Phase 1 targets 525 tpa NdPr metal 40t Dy/Tb oxide pa by H1 2027. Phase 2 scales to 3,000 tpa NdPr 245t Dy/Tb metals pa.

Metallisation → Euclid, Ohio — the PMT Critical Metals facility. 40 years of accumulated rare earth metallothermal processing experience. Proven production of Dy, Tb, Nd, Sm, Gd, Sc metals. Proprietary HF-free oxide-to-fluoride conversion — cleaner product, lower capex, lower opex, no toxic waste streams, faster US permitting. Already operating under multiple DoD and DLA contracts.

Magnets → Giga-scale NdFeB sintering facility — 3,000 tpa Phase 1 → 10,000 tpa at full run rate. Enough for 1.5–2M EV traction motors annually.

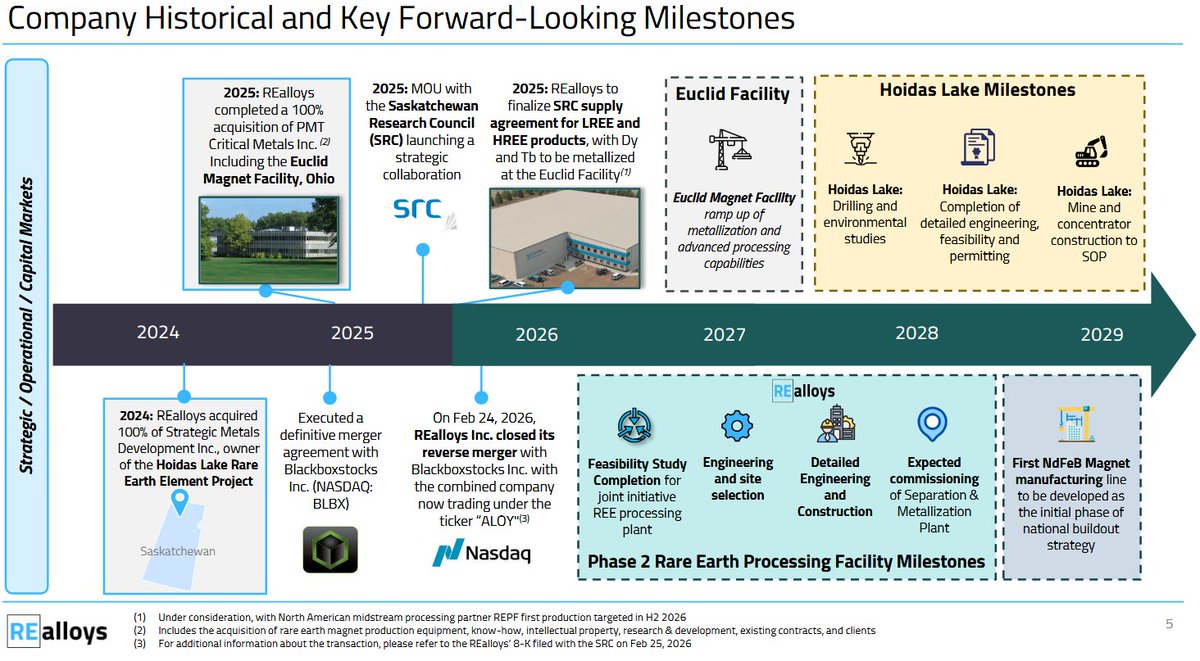

REalloys is genuinely first-mover in North American HREE metallization — that is real and important . The Euclid, Ohio facility is operating today, the SRC partnership is the most credible near-term feedstock path, and the $50M raise in March 2026 does fund the $40M HREMF build .

The DoD DLA contract (March 2026) for Terves LLC (REalloys' subsidiary) to scale domestic rare earth metal production adds further validation .

The two headline offtake agreements — St. George/Araxá and Tanbreez — are essentially options on future production from projects that don't yet have feasibility studies, permitting, or financing.

The company's 2027 targets rest almost entirely on SRC's REPF performing as planned, with recycled MREO as a supplement. If SRC hits delays, or if recycled feed volumes are lower than projected, REalloys faces a feedstock gap at exactly the moment its new metallization facility is supposed to ramp up.

ReAlloys, Heading in the right direction

$ALOY 🇺🇸🇨🇦🇦🇺🧲⚙️

@realloys #REalloys #ALOY #AnupamGhildyal #RareEarths #Metallisation #MidstreamBottleneck #NorthAmericaSupplyChain #CriticalMinerals #DFARS #DefenseSupplyChain #2027Deadline #NdFeB #Dysprosium #Terbium #NdPr #HREE #LREE #HFfree #PMTCriticalMetals #SRC #SaskatchewanResearchCouncil #HoidasLake #Tanbreez #CriticalMetalsCorp #CRML #MineToMagnet #PermanentMagnets #EVMagnets #DefenceMagnets #StrategicMaterials #CriticalMinerals2027 🔬🇺🇸🇨🇦🌏⚙️🧲

1

4

16

1,763

🇺🇸🧲 REalloys (NASDAQ: ALOY) — The Company Building What the U.S. Actually Needs

While most of the sector is still revising timelines and rewriting press releases, REalloys is executing something genuinely different: a fully integrated, zero-China, mine-to-magnet supply chain that covers every step from ore in the ground to finished NdFeB magnets in U.S. defence systems — with the legal framework, patented IP, and government-backed capital to back it up. Here's the full picture. 🧵👇

🔗 THE CHAIN — Start to Finish

The rare earth supply chain has six critical links. Almost every Western competitor is missing at least three of them. REalloys is building all six simultaneously:

1️⃣ Diversified feedstock — Hoidas Lake

(Saskatchewan, LREE HREE), Tanbreez Greenland (HREE-rich eudialyte, 15% Phase 1 offtake), Araxá Brazil (40% offtake, 40.6Mt carbonatite), Brook Mine Wyoming (coal-hosted MREC), acid mine drainage, recycled end-of-life magnets

2️⃣ Nuclear-licensed cracking & Th/U removal

— SRC Saskatoon, the only Canadian Nuclear Safety Commission licensed minerals-to-metals facility in North America. Chinese separation plants don't need to handle this problem — they simply don't. Western competitors either can't crack monazite legally or ship it back to China. REalloys doesn't.

3️⃣ AI-driven SX separation

— Proprietary next-generation solvent extraction at SRC. Custom phase geometries, real-time AI process control, >99% individual REO purity. Phase 1: 525 tpa NdPr 15 tpa Tb oxide. Phase 2: 3,000 tpa NdPr 200 tpa Dy 45 tpa Tb metal.

4️⃣ Patented HF-free metallization

— The "missing link" of the entire Western sector. Most projects mine ore, separate oxide, then ship it to China for metal conversion. REalloys' patented HF-free process does it domestically — lower oxygen contamination, higher coercivity output, no toxic HF waste streams, faster U.S. permitting. Euclid, Ohio. 3,000 tpa metals capacity.

5️⃣ Giga-scale magnet sintering

— U.S. Magnet Manufacturing Facility. 3,000 tpa baseline → 10,000 tpa full capacity NdFeB. At full run-rate: magnets for 1.5–2M EV traction motors, 7,000–10,000 direct-drive wind turbines, and every major U.S. defence platform — Virginia-Class, F-35, PATRIOT, M1A2 Abrams, Tomahawk, DDG-51.

6️⃣ Closed-loop circular economy

— EOL magnets from EVs and wind turbines cycle back into the feed stream as recycled MREO. The supply chain feeds itself over time.

⏱️ THE TIMELINE — Built Around the Deadline

REalloys' entire commercial deployment schedule is explicitly engineered around January 1, 2027 — the date the DFARS ban on Chinese rare earth materials goes into full statutory effect.

📅 H1 2027 — Phase 1: SRC Saskatoon online. 40 tpa Dy Tb oxide. NdPr 525 tpa. Euclid Ohio metallization producing first U.S. defence-grade heavy rare earth metals.

📅 2030 — Phase 2: REA REPF second facility online. 200 tpa Dy metal 45 tpa Tb metal. 3,000 tpa magnet sintering commences.

📅 End of Decade: 10,000 tpa NdFeB giga-scale full capacity.

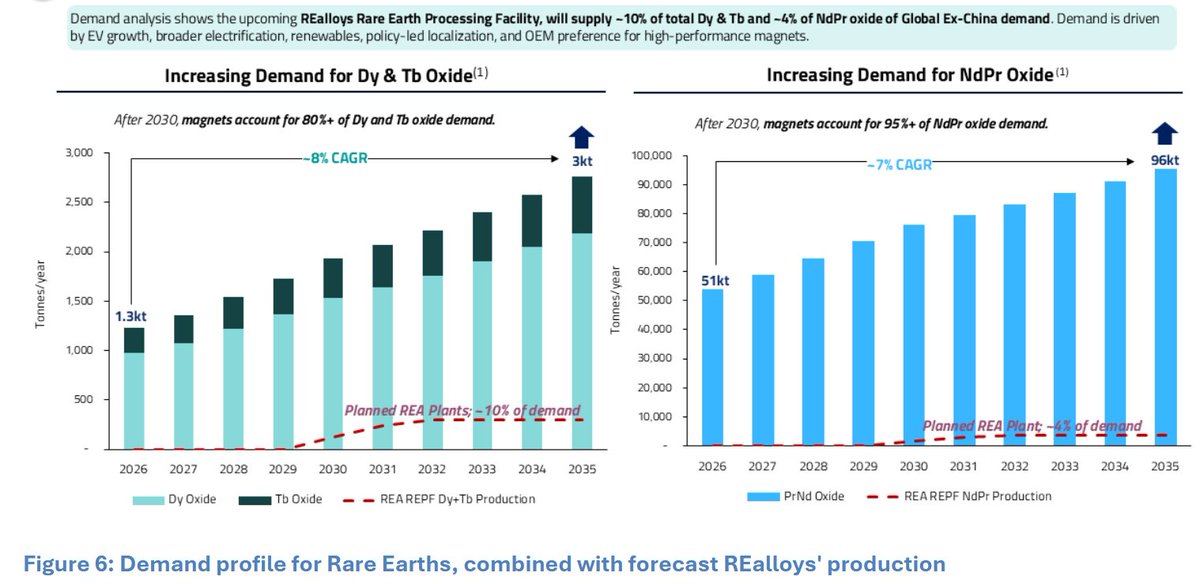

Gold callout: McKinsey MineSpans projects an 82% HREE supply deficit outside China by 2035. REalloys is positioned at exactly that intersection.

💰 THE CAPITAL STACK

$200M EXIM Bank Letter of Interest (15yr term, CTEP programme) — federal sovereign backing

$50M upsized public offering closed March 9, 2026 at $18.50/share

Active DLA (Defence Logistics Agency) contract — Sm and Gd metals, 300 tpa modular facility

NASDAQ: ALOY — listed February 25, 2026 via reverse merger with Blackboxstocks

🎖️ THE BOARD — This Is Not Accidental

Four-star General Jack Keane (Ret.) · Former Saskatchewan Premier Brad Wall · Former U.S. Ambassador to Canada David MacNaughton · Former UBS Vice Chairman Bob Foresman · Former Chief of Staff to the U.S. Secretary of Defense Joe Kasper (Advisory Board Chair).

This board is engineered to access Title III DPA funding, DOE Title 17/48C/45X grants, IRA tax credits, and direct Pentagon procurement. This is a quasi-national strategic infrastructure company wearing a NASDAQ listing.

⚠️ THE HONEST CAVEAT

The feedstock analysis reveals a two-speed reality that strengthens confidence in Phase 1 but is honest about Phase 2 dependency:

Phase 1

(H1 2027) is feedstock-credible. International monazite at SRC is real, licensed, and operational. The $20.6M upgrade is committed and contracted. The 40–45 tpa Dy Tb and 400–600 tpa NdPr target is achievable on existing feedstock — no Hoidas Lake, no Tanbreez required.

Phase 2

(2030) is feedstock-dependent on assets that are 2029 at the earliest. Tanbreez concentrate export Q3 2029 means REalloys' 15% share of HREE-rich eudialyte arrives exactly as Phase 2 is supposed to start — with almost no margin for delay. Hoidas Lake mine development has no confirmed production date. The two largest long-term feedstock assets are not yet producing and won't be until very close to the Phase 2 window opens.

The bottom line: Phase 1 is more credible than most Western peers because it runs on existing licensed infrastructure with committed capital. Phase 2 is contingent on Tanbreez and Hoidas coming in on schedule — and in the rare earths sector, mine development timelines have a well-documented tendency to slip.

⚠️ St. George Mining — Araxá, Brazil — Years Away The REalloys CIM pitches Araxá as a confirmed feedstock agreement, but the timeline is deeply problematic : The TREO grades are good (4.13%), with a reasonable NdPr fraction (18.4%), but Dy (0.3%) and Tb (0.1%) are very low — meaning Araxá is primarily a light REE source, not a heavy REE feedstock for the HREMF's core Dy/Tb metallization thesis .

Realistically, Araxá is 5–8 years from producing any concentrate REalloys could use.

⚠️ Critical Metals Corp — Tanbreez, Greenland — Political Minefield Critical Metals Corp's (NASDAQ: CRML) Tanbreez project is one of the world's largest known rare earth deposits, but faces compounding risks :

1. Greenland is asserting increasing political autonomy from Denmark, with independence sentiment rising sharply in response to President Trump's repeated statements about acquiring Greenland.

2. Even under an optimistic scenario, Q4 2028 first ore means no Tanbreez feedstock reaches REalloys before 2029 at the absolute earliest — two full years after the HREMF is supposed to be operational

3. The 0.38% TREO grade means enormous volumes of rock must be processed to extract usable rare earth content, requiring major infrastructure investment that hasn't been funded.

realloys.com/media/REalloys_…

REalloys' Phase 1 credibility rests entirely on SRC's REPF commissioning on time with sufficient monazite feed — neither of which has been independently verified with locked-in long-term contracts. Phase 2 depends on Tanbreez and Hoidas, both of which are 2029 in the most optimistic scenarios, with Tanbreez carrying genuine sovereign political risk.

The architecture remains the best-designed in North America. But the feedstock thread makes Phase 1 riskier than the investor materials imply, and Phase 2 dependent on a very tight convergence of mining development timelines in multiple jurisdictions simultaneously.👀

$ALOY 🇺🇸🇨🇦🧲⚡

@realloys

#REalloys #ALOY #RareEarths #CriticalMinerals #NdFeB #PermanentMagnets #DFARS #WesternSupplyChain #NationalSecurity #MineToMagnet #Dysprosium #Terbium #HeavyRareEarths #NdPr #SRC #Saskatchewan #HFfree #Metallization #MagnetManufacturing #VerticalIntegration #DefenceSupplyChain #EXIM #DLA #Pentagon #FEOC #ZeroChina #CircularEconomy #MagnetRecycling #CriticalMineralsPolicy #NorthAmerica #Reindustrialization 🇺🇸🧲⚡🏭

6

11

606

SPONSORED

Full Coverage On (Nasdaq: $ALOY) is Starting Right Now!

Now’s the Time | Pull Up (Nasdaq: ALOY) As Early As Possible—Here’s Why

In the race to electrify transportation, harden defense systems, and modernize power grids, a small component sits at the center of it all: rare earth magnets. (Source: ca.finance.yahoo.com/news/re…)

These compact engines of force convert electrical energy into motion in everything from EV drivetrains and drone rotors to radar systems and industrial robots. (Source: realloys.com/blog/from-ore-t…)

They are the unseen workhorses of the 21st‑century economy, and their performance depends on a handful of critical metals: neodymium (Nd), praseodymium (Pr), dysprosium (Dy), and terbium (Tb). (Source: realloys.com/blog/from-ore-t…)

Without these elements, vast downstream industries in defense, technology, and energy simply cannot function. (Source: realloys.com/about/)

It is at this strategic junction that REalloys Inc. (Nasdaq: ALOY) has positioned itself, building a Rare Earth Mine‑to‑Magnet platform in the Western Hemisphere designed to answer both market demand and national security imperatives. (Source: realloys.com/realloys-press-…)

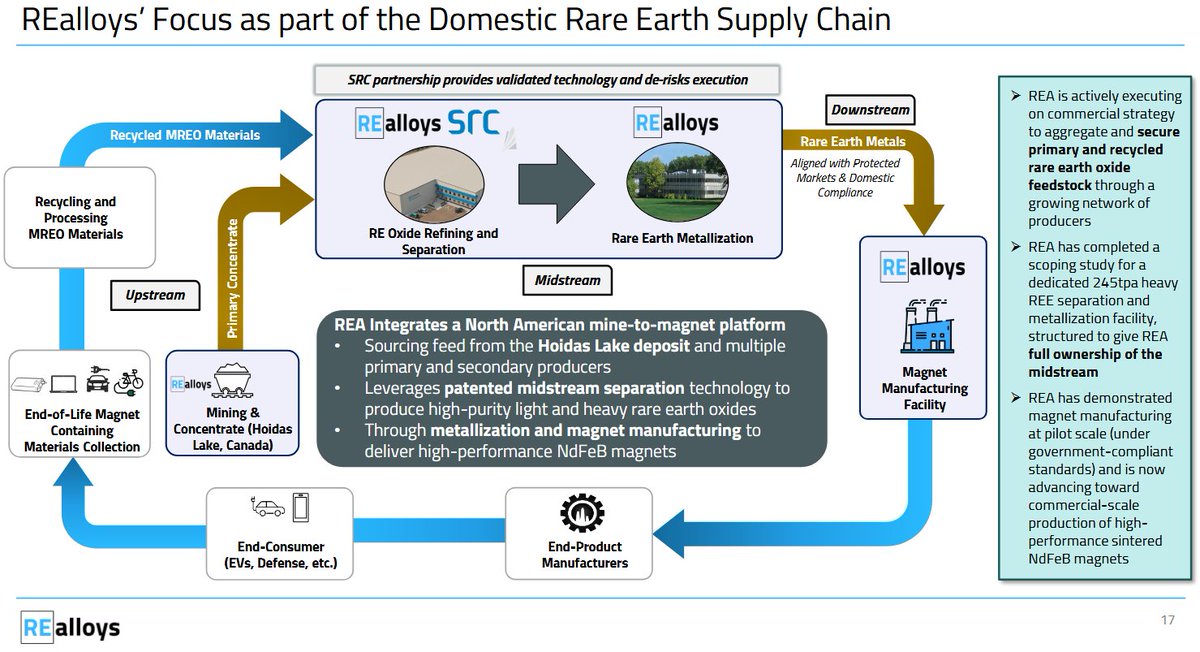

Technology and Midstream Capability In rare earth supply chains, the primary constraint outside China is not mining or separation, but metallization, the oxide‑to‑metal step. (Source: globenewswire.com/news-relea…)

Through its acquisition of PMT Critical Metals, REalloys controls a heavy rare earth metallization platform in North America, built on more than 30 years of specialty metals work and eight years of focused metallothermic and calciothermic processing with U.S. national laboratories and the Defense Logistics Agency. (Source: pmtcriticalmetals.com/post/b…)

The resulting closed‑cycle process converts dysprosium, terbium, samarium, gadolinium, and mixed rare earth streams into high‑purity metals while reclaiming byproducts and eliminating waste streams that typically constrain scale and permitting. (Source: globenewswire.com/news-relea…)

By pairing SRC’s large‑scale separation infrastructure with PMT’s metallization platform and the Euclid magnet facility, REalloys Inc. (Nasdaq: ALOY) secures the most difficult segment of the value chain and establishes a domestic foundation for magnet manufacturing. (Source: globenewswire.com/news-relea…)

Here’s 5 Reasons Why REalloys Inc. (Nasdaq: ALOY) is Topping Our Watchlist This Morning—Tuesday, April 7th 2026

#1. On‑time completion and ramp‑up of SRC’s REPF in early 2027. (Source: globenewswire.com/news-relea…)

#2. Successful commissioning and relocation of the Dy/Tb oxide‑to‑metal conversion unit to Ohio. (Source: globenewswire.com/news-relea…)

#3. Conversion of non‑binding offtake agreements into long‑term, binding contracts. (Source: realloys.com/realloys-press-…)

#4. Positive results from the 2026–2027 Hoidas Lake drilling and permitting program. (Source: realloys.com/media/REalloys_…)

#5. Additional U.S. or allied policy actions that further prioritize non‑Chinese rare earth and magnet supply. (Source: globenewswire.com/news-relea…)

We're officially kicking-off coverage on REalloys Inc. (Nasdaq: ALOY) this morning.

DISCLAIMER: tinyurl.com/yc3jpjsx

6

695

🚨 BREAKING: The most important rare earth company you've never heard of just went fully financed.

Where REalloys Sits — and Why It's the Critical Node

📷

REalloys occupies Step 4 of the mine-to-magnet chain — the oxide-to-metal metallization step — which is the most technologically demanding and strategically sensitive conversion point . CSIS described this step as the one where China has "the most leverage" . REalloys' Euclid, Ohio facility is already operating today, converting separated heavy rare earth oxides into metals and pre-alloyed compositions within the narrow tolerances qualified magnet producers require .

The company's HF-free fluorination process is a proprietary breakthrough: conventional rare earth metallization requires hydrofluoric acid (one of the most dangerous industrial chemicals), generating toxic waste. REalloys' process eliminates this, producing metals at 0.34% oxygen content while cutting processing costs by ~50%

$ALOY @REalloys is building the largest heavy rare earth metallization facility outside China — in OHIO.

This is a US national security story. Thread 🧵👇

1. Why This Matters

⚠️ The US reportedly has ~2 months of rare earth reserves for its military.

But the real crisis isn't ore — it's the midstream: converting rare earth oxides → metals → magnets.

China controls ~95% of that step globally.

2. The Facility

🏭 REalloys' Heavy Rare Earth Metallization Facility (HREMF), Euclid, Ohio:

✅ $40M buildout — fully financed (closed $50M raise @ $18.50/share, March 9 2026)

✅ Phase 1: 45 tpa Dysprosium Terbium metals

✅ 300% capacity expansion underway

✅ Target online: H1 2027

3. The SRC Partnership

🇨🇦 Partner: Saskatchewan Research Council (SRC)

REalloys locked in 80% of SRC's rare earth processing output in exchange for capacity investment.

SRC's REPF in Saskatoon separates Dy, Tb oxides → feeds straight into the Ohio metallization plant.

This is the actual feedstock backbone for 2027. 🧱

Risk: SRC's REPF itself is still scaling up. It processes monazite — a phosphate mineral sourced largely from mineral sand operations globally, with no fully locked-in monazite feed contract disclosed publicly. If SRC's REPF faces commissioning delays, REalloys' 2027 timeline slips entirely.

❌ St. George Mining — Araxá, Brazil — Years Away

The REalloys CIM pitches Araxá as a confirmed feedstock agreement, but the timeline is deeply problematic :

The TREO grades are good (4.13%), with a reasonable NdPr fraction (18.4%), but Dy (0.3%) and Tb (0.1%) are very low — meaning Araxá is primarily a light REE source, not a heavy REE feedstock for the HREMF's core Dy/Tb metallization thesis . Realistically, Araxá is 7–10 years from producing any concentrate REalloys could use.

❌Critical Metals Corp — Tanbreez, Greenland — Political Minefield

Critical Metals Corp's (NASDAQ: CRML) Tanbreez project is one of the world's largest known rare earth deposits, but faces compounding risks :

1. Greenland is asserting increasing political autonomy from Denmark, with independence sentiment rising sharply in response to President Trump's repeated statements about acquiring Greenland.

2. Even under an optimistic scenario, Q4 2028 first ore means no Tanbreez feedstock reaches REalloys before 2029 at the absolute earliest — two full years after the HREMF is supposed to be operational

3. The 0.38% TREO grade means enormous volumes of rock must be processed to extract usable rare earth content, requiring major infrastructure investment that hasn't been funded.

4. The DoD Contract

🪖 On March 2, 2026, the US Defense Logistics Agency (DLA) awarded REalloys subsidiary Terves LLC a contract to scale domestic production of:

⚙️ Samarium (Sm) — samarium-cobalt magnets, radar

⚙️ Gadolinium (Gd) — precision guidance, advanced optics, nuclear

First time the US has attempted domestic Sm/Gd production at scale.

🔗 globenewswire.com/news-relea…

5. Risk Explainer 🧵

REalloys is genuinely first-mover in North American HREE metallization — that is real and important . The Euclid, Ohio facility is operating today, the SRC partnership is the most credible near-term feedstock path, and the $50M raise in March 2026 does fund the $40M HREMF build . The DoD DLA contract (March 2026) for Terves LLC (REalloys' subsidiary) to scale domestic rare earth metal production adds further validation .

However, your instinct is correct: the feedstock story has a significant gap between the investor narrative and operational reality. The two headline offtake agreements — St. George/Araxá and Tanbreez — are essentially options on future production from projects that don't yet have feasibility studies, permitting, or financing. The company's 2027 targets rest almost entirely on SRC's REPF performing as planned, with recycled MREO as a supplement. If SRC hits delays, or if recycled feed volumes are lower than projected, REalloys faces a feedstock gap at exactly the moment its new metallization facility is supposed to ramp up.

The 30 recycled MREO and primary feed suppliers "in the outreach pipeline" is an important hedge — but as of March 2026, these are not contracted supply, they are a prospecting list.

Let's Look at IXR Belfast HREE Output vs. REalloys HREMF Requirement

The Chemistry First, Metallisation discussed many times with LCM, With real-world metallization efficiency (80–92% of theoretical yield depending on process maturity), the practical conversion is ~80–87%, losing the Oxygen molecule

The correct theoretical yield based on molecular weights is:

Dy₂O₃ → 2Dy: Dy atomic mass 162.50 g/mol, Dy₂O₃ = 373.00 g/mol → 87.1% theoretical yield

Tb₄O₇ → 4Tb: Tb₄O₇ = 747.72 g/mol → 85.0% theoretical yield (IXR's DFS correctly specifies Tb₄O₇)

Bottom line: IXR Belfast at full nameplate production (37 tpa Dy₂O₃ 13 tpa Tb₄O₇) could generate enough oxide to produce approximately 35–40 tpa of Dy Tb metals — covering 77–89% of REalloys' 45 tpa Phase 1 target .

That is a very significant but not complete supply of REalloys' needs, with a shortfall of roughly 5–10 tpa of metals requiring a supplemental source (SRC, MCM, or recycled MREO).

IXR already has a downstream metals partner — and it's not REalloys 🔴

The DFS explicitly names Less Common Metals (LCM) as IXR's existing metals and alloys manufacturing partner, alongside Vacuumschmelze (VAC) . The circular supply chain IXR is building runs: IXR oxide → LCM metals/alloys → VAC magnets.

Two companies. Adjacent steps in the same chain. Near-perfect volume alignment.

Zero commercial relationship today.

⚠️ This is a speculative thought experiment only. Not financial advice. Do your own due diligence. $IXR and $ALOY are both pre-commercial, speculative, high-risk stocks.

🌏 The US-China rare earth standoff isn't just about ore.

It's about who controls the conversion steps — oxide → metal → alloy → magnet.

$ALOY is the only public pure-play attacking the most acute chokepoint: heavy rare earth metallization.

Watch this space. 🇺🇸🧲

⚠️ Note: The stock ran from $2.60 to $26.90 in its 52-week range on thematic rare earth momentum, then pulled back sharply after the equity dilution from the $50M offering. It remains a high-risk, pre-revenue speculative play tied almost entirely to execution of the 2027 HREMF target and SRC feedstock delivery.

#RareEarths #CriticalMinerals #NationalSecurity #Mining #DefenseIndustry #Magnets #Dysprosium #Terbium #SupplyChain #USChina #ALOY #REalloys #DoD #DLA #Geopolitics #CriticalMetals

realloys.com/media/REalloys_…

6

240

REalloys acquired PMT Critical Metals (April 2025), which holds the rare earth assets of Terves LLC and Powdermet Inc.

On March 2, 2026 — the same week as the Iran strikes — the US Defense Logistics Agency (DLA) awarded Terves LLC a historic contract under topic DLA212-004 to scale samarium (Sm) and gadolinium (Gd) metal production using next-generation metallothermal processes.

REalloys targets 10,000 tonnes/year magnet manufacturing at scale — NdFeB for EVs, wind turbines, robotics and SmCo for defence. Production beginning 2027 via PMT Critical Metals' existing magnet manufacturing capabilities.

REalloys is the most comprehensively structured allied mine-to-magnet play in North America right now, uniquely focused on the heavy rare earths (Dy, Tb, Sm, Gd) that are most critical for defence magnets, but The key question is execution — can they build what they've announced by 2027 before DFARS compliance becomes mandatory and before the US weapons stockpile is critically depleted?

And

The full integrated vision — Phase 2 REPF at 3,000t NdPr and 245t Dy Tb — is a 2030 commissioning target. Hoidas Lake production is 2029 at earliest. Magnet manufacturing at scale is 2029–2035. The Iran war and DFARS 2027 deadline will both have played out long before REalloys' Phase 2 is operational.

Once again

What most people don’t seem to get about the rare earths sector is this, Outside China, almost nothing is actually built and running at scale yet. Nearly everything being talked up is 2–3 years away – if it gets funded and if it delivers what’s promised.

Very few companies in the West today have signed, executed, fully funded contracts that take them all the way from ore to separated oxides to magnet alloys and finished magnets. Almost everyone is still stitching pieces together and asking the market to give them full value for a supply chain that doesn’t exist yet.

TOTALLY DISJOINTED FRAGMENTED CHAIN

2

71

Mar 10

Uppsalaprofessorn har rätt.

Med vänlig hälsning,

Ordförande emeritus för @RepF

Hör en Uppsalaprofessor i statskunskap påstå i radions P1 att monarki är en sorts diktatur. I och för sig handlar samtalet om Irans framtid. Men jag undrar ändå om hon känner till Sverige.

3

198

Great time yesterday with our @LehighFootball Awards Banquet, celebrating a perfect season and another @PatriotLeague Championship!

🏈🏈🏈🏈🏈🏈

Top Position Award Winners

RB: Yoder

OL: Repf

WR: Jamiel

DB: Singleton

LB: Edwards

DL: Spatny

ST: Poole

🏈🏈🏈🏈🏈

3

25

1,344

20 Dec 2025

<全日本選手権>◇20日◇東京・代々木第一体育館◇男子フリー

#鍵山優真(オリエンタルバイオ/中京大)

183.68点→287.95点🏆

4S( 4.57)

4T( 4.34)

3Lz( 1.94)

1A 1Eu 3S( 0.31)

FCSSp4( 0.94)

4Tq REPF(-4.75)

3F 3Lo( 1.21)

3A 2T( 1.94)

CCoSp4( 1.10)

ChSq1( 2.07)

StSq4( 1.78)

FCCoSp3( 1.11)

CO=9.14

PR=9.11

SK=9.36

#figure365

61

197

12,110

2 Dec 2025

🎉 Breckland is delighted to support Tollgate Studios Limited with a £25,000 REPF grant!

🎙️ Led by voice artist and presenter Angus Scott, Tollgate Studios has rapidly grown from a small voiceover setup into a professional recording and film facility.

🧵👇

ALT Cllr Sam Chapman-Allen, Leader of the Council, and Maxine O'Mahony, Chief Executive, presenting the certificate to Angus Scott.

ALT Cllr Sam Chapman-Allen, Leader of the Council, and Maxine O'Mahony, Chief Executive, with Angus Scott.

ALT Cllr Sam Chapman-Allen, Leader of the Council with Angus Scott.

ALT Cllr Sam Chapman-Allen, Leader of the Council, and Maxine O'Mahony, Chief Executive, with Angus Scott.

1

2

2

73

16 Nov 2025

<#GPシリーズ スケートアメリカ>◇15日(日本時間16日)◇ 米・レークプラシッド◇男子フリー

#友野一希(第一住建グループ)

149.80点→245.57点🥉

4TqF(-4.75)

4T REPF(-4.75)

4S( 0.14)

3Lo( 0.84)

FCSp3( 0.44)

3A(-1.83)

3F 2A SEQ( 1.14)

3A 1Eu 2S( 1.26)

StSq4( 1.11)

CSSp3( 0.56)

ChSq1( 1.21)

CCoSp4( 0.40)

CO=8.11

PR=7.93

SK=8.32

#figure365

80

298

19,229

8 Nov 2025

<#GPシリーズ NHK杯>◇8日◇ 大阪・東和薬品RACTABドーム◇女子フリー

#樋口新葉(ノエビア)

115.12→168.27

2A 3T( 0.90)

3Lz<(-0.54)

3Lo<(-0.28)

FCSp4( 0.73)

3S( 0.86)

3Lz REPF(-2.36)

2S 2T( 0.02)

3Fq(-0.76)

CCoSp4( 0.45)

StSq4( 1.28)

ChSq1( 1.43)

FCCoSp3( 0.69)

CO=7.82

PR=7.96

SK=8.32

#figure365

36

140

11,249

5 Aug 2025

Avsluta monarkin med det snaraste, detta måste alla ”moderna demokrater” rösta för!

3

17