Yeah, it's not his fault the management relies on an upstart as their go-to weapon amd thus, their pivotal weakness. Weby isn't the problem, he was put into impossible circumstances and expectations.

3

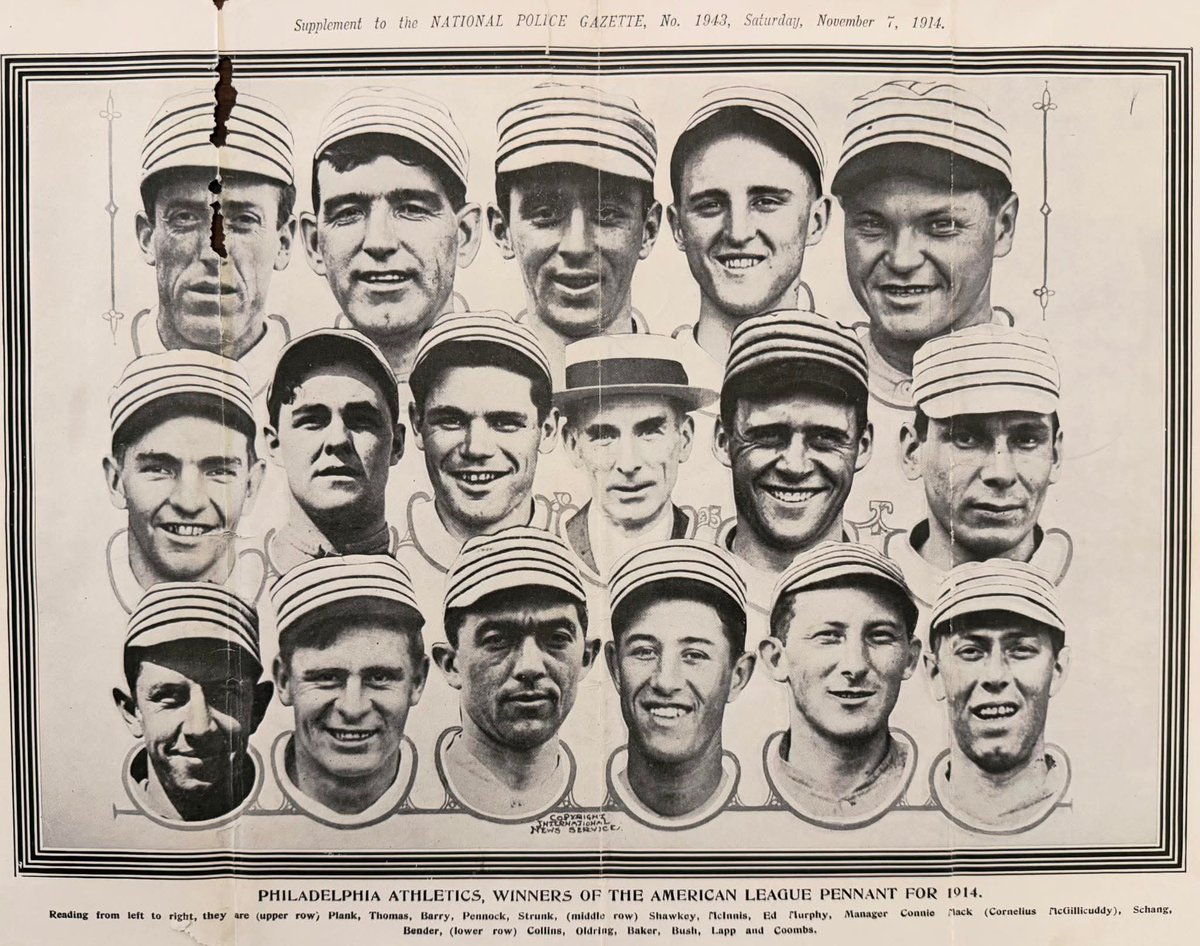

The 1914 American League Pennant winning Philadelphia Athletics are shown on this Police Gazette M128 poster. This squad had already dominated the early 1910’s winning three World Series titles from 1910-1913 and 1914 looked like no exception. However, every dynasty must end. The Boston Braves acquired their own player who knew a thing or two about dynasties in Johnny Evers who helped the Chicago Cubs dominate the NL from 1906-1910. The Braves had already surprised everyone with an unlikely pennant run and were heavy underdogs going up against the Mack Men. The Braves rose to the challenge and not only won the 1914 World Series, but did so with a sweep over the Athletics. The timing marked the end of the Mack dynasty as financial stress and mounting pressure from players jumping to the upstart Federal League, forced Connie Mack to begin dismantling his squad after that season. Shown are future Hall of Fame stars Eddie Plank, Chief Bender, Eddie Collins, Frank Baker, Herb Pennock, and Connie Mack!

1

5

140

they do indeed. historically, the revolutionaries will make a stern example of tyrants for all to see in order to stop any upstart criminals from attempting to do the same tyranny. usually we chop off their fucking heads or hang them which, tbh, is probably what needs to be done in this abysmally corrupt united states government. i am so ashamed of what america has become. sackless sheeple choking down fake information so they can spit it back out at someone else.

4

There's nothing wrong for him to famz Lyles. Gout is still an upstart who has a lot to learn. That field is very experienced, Dambile is a 200m world junior medallist, while Richardson had been in the South African Junior and Senior teams. It's an experienced field to finish 3rd

1

69

(2/3) $NKE: Nike Must Protect This House!

Know this is a controversial statement but there is a lot that this modern version of Nike could learn from $UAA / $UA. First and foremost is that you do anything possible to protect whatever advantage you have in this industry. Under Armour has first-hand knowledge of how the old version of Nike used to treat competition – their original entry into running shoes (Nike’s heritage business) was annihilated by all resources that Nike could bring to bear at that time. Somewhere along the way Nike forgot that lesson and as a result opened the door to ample competition in the running category going forward. We don’t believe that door will ever be closed again but perhaps Nike can prevent the same thing from happening to its leadership positions in other areas?

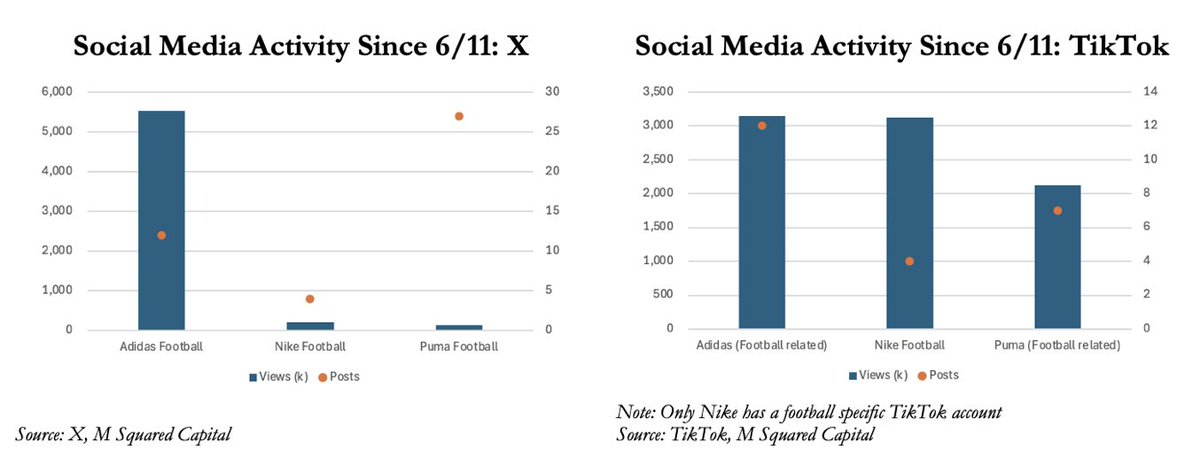

This note focuses specifically on Nike’s football (soccer) business, including the confusing decision to introduce the Jordan brand into the sport. But more importantly, it focuses on Nike’s apparent lack of competitive fire towards defending its home pitch advantage for the World Cup. $ADIDAS dominated the sport of football for most of the past 100 years, beginning with the West Germany win in the 1954 World Cup. Yet 40 years later Adidas took its eye of the ball at the 1994 World Cup and allowed just enough room for Nike to enter the sport in a meaningful way for the first time on their home pitch in the US. Brazil (best team in World Cup history) signed with the upstart Nike in 1996. Ten years later the previously unassailable market share advantage of Adidas became a virtual tie with Nike. That’s how quickly the leadership boards can change and if Nike is not careful, Adidas seems poised to return the favor using the 2026 World Cup as a springboard into a previously unassailable US market for all sports (not just football). Unlike Nike, they already have the product too (particularly in running).

There is no doubt that Nike still makes impressive marketing that cuts through the clutter and leaves a lasting impression, which we see with their “RIP The Script” short video for the World Cup. But they released that a week before the event began and have done practically nothing since other than posting shorter clips of the same video every few days on social media. Meanwhile peers like Adidas and Puma are constantly engaging with consumers through social media channels to celebrate the accomplishments of sponsored teams and players. Nike didn’t even feel it necessary to say anything on social media when the US team they sponsor won its first game in a shared home country by setting a historical record for goals in a single match.

We now believe the reasonable range of EPS estimate in FY26 is $1.45 to $1.60 and are more positively biased than current consensus of $1.50. The current narrative is stabilization in FY27 and back to growth afterwards but as investors can see with VF Corp, nobody seems willing to get involved until the later growth stage becomes more visible. Our work on the football business indicates that Nike might have more problems than they are letting on at the moment – not necessarily related to revenue generation for the World Cup but more towards operational gaps and strategic failures.

...(Abridged)...

All we have heard from Nike on social media so far is radio silence towards the performance of any of its sponsored teams or players (particularly with the much more specific Nike Football account). The US example is most egregious as the performance was record breaking (most goals ever for US in a single World Cup match) and they are supposed to the be the home team for Nike. We can’t think of a single reason why Nike didn’t feel compelled to celebrate (other than singularly focusing on the NBA Finals) – doesn’t a company the size of Nike at least have an intern somewhere that can post a picture of the final score and say congrats every time one of their sponsored teams wins during the World Cup? Heaven forbid they could have planned for eventualities ahead of time with higher quality marketing ready to go at the push of a button whenever an event happens. There isn’t really anything else that the Nike Football social media account can do for the next month or so anyway, other than endlessly cutting up the same “RIP The Script” commercial. Maybe, just maybe, they can do both?

...(Abridged)...

This is a highly abridged version of this 8 page note. We provide the entire note and financial model for free at our website in post #3 of this thread (link also in profile).

While we always provide our work on Nike and Restoration Hardware for free, subscribers have access to all research for the 20 consumer/retail companies that we currently cover. See our website for more information and feel free to sign up to our distribution list for notification of the research we publish.

2

3

1,330

Let us take a look at what everyone are talking about - SoFi $SOFI

SoFi is trying to build a full financial app for younger, higher-income customers: banking, loans, investing, credit cards, savings, insurance referrals and financial services in one place. The model only really works if members keep adding more products over time.

The latest quarter suggests they are. Q1 2026 adjusted net revenue hit a record $1.1B, up 41% year-on-year. Adjusted EBITDA was $340M, up 62%, and SoFi reported its tenth straight quarter of GAAP profitability. Members reached 14.8M, up 34%, while total products reached 21.6M, up 35%. That is the key metric for me: not just more users, but more products per user. (SEC)

Let’s compare the competition - Robinhood $HOOD is more trading-focused. LendingClub $LC and Upstart $UPST are more lending-focused. Chime is more digital banking-focused. SoFi is trying to sit across all of it. That gives it a bigger opportunity, but only if played right.

What do others think about it you ask.. Well analysts are not fully convinced yet. MarketBeat shows an average target around $22.56, with a high of $35 and a low of $16. With the company hovering aaround $17.78 today, that implies roughly 27% upside to the average target, but the range tells you Wall Street still disagrees on what this business should be worth.

What next? Well, that’s a difficult one, the company fell quite a bit over the past six months, despite strong operating numbers, which tells me the market is wrestling with valuation - the question on the street is whether growth can stay this strong.

So, if SoFi stays mostly a lender, the upside may be limited. If it becomes the default financial platform for millions of people who bank, borrow and invest in one place, then I bet you that bright things await.

Which path will it be?

74

⚡Choose between a 7000 year old regional power with 93 million ppl,globe's highest education rate, scientific prowess, rich oil/gas, & a 48 year old upstart which stole uranium fr you, is high maintenance, spies on you,specializes in agression/assassination,incl towards you.

4