Jun 12

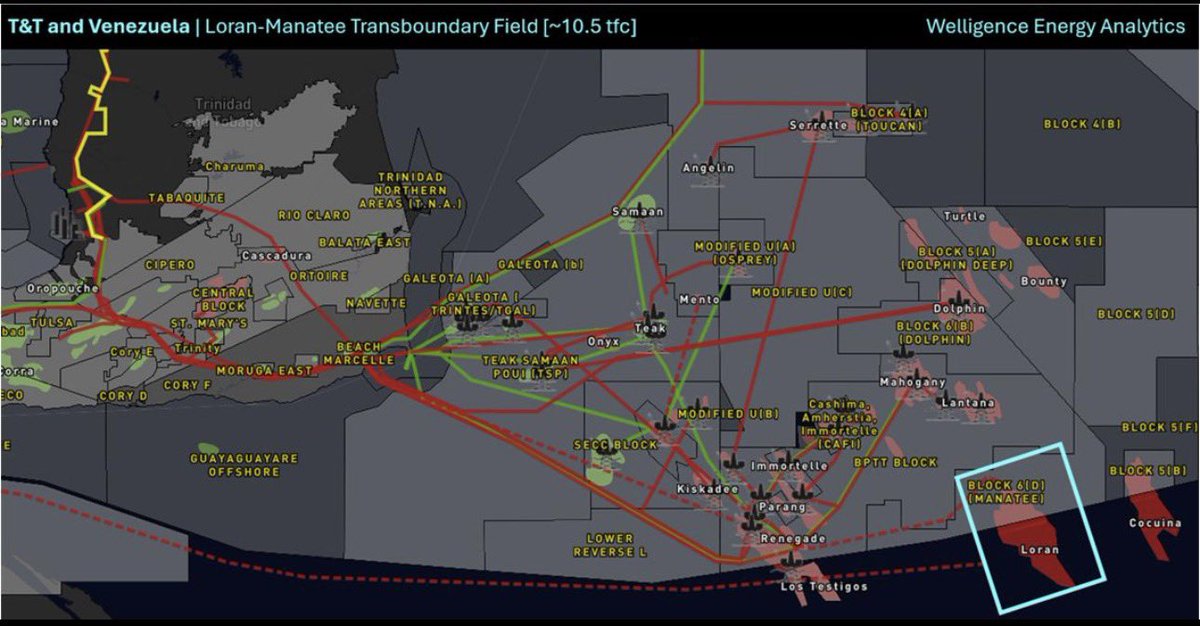

Loran Field -> Venezuela's Ministry of Hydrocarbons has announced that it has awarded Shell and bp a Non-Associated Gas Licence for development of the offshore Loran gas field, marking a significant milestone for the country's offshore gas ambitions.

Loran contains an estimated 7.0–7.5 tcf of gas and forms the Venezuelan portion of the Loran–Manatee accumulation, one of the largest undeveloped cross-border gas resources in the continent. The Manatee field, located in T&T waters, contains a further 2.6–2.7 tcf. Together, the two structures hold close to ~10.5 tcf of gas.

The award follows Chevron's relinquishment of its 60% interest in the Loran licence as part of the asset swap agreement formalised with PDVSA on 13 April 2026. Under the transaction, Chevron secured Ayacucho 8 (Marikitare), an extension to its Petropiar development in the Orinoco Belt, while returning Loran and other offshore exploration acreage to the Venezuelan state.

The development of Manatee is already well advanced. Shell took FID on the T&T side in 2024, with first gas expected in 2027. The project will provide important infrastructure and commercial momentum for the eventual development of Loran.

The Loran–Manatee field was unitised in 2010 but effectively de-unitised in 2019, allowing each country to develop its respective share independently. Nevertheless, given the transboundary nature of the reservoir, a new unitisation agreement is expected to be the next step.

Congratulations to the Shell and bp teams on reaching this important milestone. Loran, together with Dragon and Cocuina-Manakin, has the potential to underpin a new era of offshore gas development in Venezuela while strengthening gas supplies to T&T's LNG and petrochemical sectors.

1

143

May 9

your grand opinion & favouring & particularising hinduism *

and trail to unitising hindus *

hatsoff to your program towards hindu unitisation *

I can myself surrender & sacrifice my whole life to support any kind of your future program *jai srimannarayana** -(my friend shankar )

2

1

5

650

Apr 13

Asset Swap Incoming in Venezuela -> Chevron (CVX) secures Ayacucho 8 (an extension of its Petropiar ~180k b/d project in the Orinoco Oil Belt) while relinquishing its 60% stake in the Loran offshore licence (~7.5 tcf) to Venezuela. The government is expected to re-award Loran to Shell (…another company might be involved).

Loran constitutes the Venezuelan portion of the Loran–Manatee field, while Manatee (~2.6–2.7 tcf) lies in Trinidad & Tobago waters; together they form a major transboundary gas field.

The field was unitised in 2010 but “de-unitised” in 2019, allowing each country to develop its respective share independently.

A re-unitisation will need to happen now.

Chevron, Shell to sign agreements for oil, gas areas in Venezuela, sources say

CARACAS/HOUSTON, April 13 (Reuters) - Chevron is expected to sign agreements on Monday to return an offshore gas field to Venezuela and participate i

3

46

110

19,414

Apr 13

للتوضيح... نيوميد مش بس مستثمر سلبي... او silent partner... هي شريك كامل في الكونسورتيوم... اللي بيطور الحقل... يعني هتشارك في اتخاذ القرارات الاستراتيجية ودا مش قليل وهتساهم في تمويل التطوير يعني هتساهم بالمنصة العائمة خط الأنابيب كل البنية التحتية... والتكلفة المتوقعة مليارات...

الحقل في بلوك ١٢ اللي ٩٠٪ منة قبرصي و١٠٪ من اسرائيلي المعروف ب آيشي Ishai ودا جوا المياه الإسرائيلية.

ده جزء من الخزان الغازي المشترك

الحكومتين (قبرص وإسرائيل) في مفاوضات نهائية علشان يوصلوا لاتفاق unitisation علشان يطوره Chevron Shell NewMed مقابل تعويض مالي لمرة واحدة للجانب الإسرائيلي يحدده خبير دولي...

ونيوميد هي اللي أعلنت الاتفاق مع مصر على البورصة الإسرائيلية

نيوميد عندها علاقات خاصة ومتشعبه مع موبل انيرجي قبل ما تستحوز عليها شيفرون

وليس دفاعا عن اي طرف... بس احنا اللي دايما بنحول اي اتفاق بين شركات خاصة لاهلي وزمالك... يعني صفقة الغاز المصري الاسرائيلي هي رسميا صفقة غاز تجارية بين شركات... الناس عندنا اللي حولتها لمصر اسرائيل... ولما اللي بالصفقات دي بيقعدوا مع الاطراف التانيه بيتخونوا وهما قاعدين مع شركات وليس دوله... بمعني تاني اللي بنعمله بيحاولوا يعملوه فينا ويكايدوا وهما اساتذه كيد..

3

2

11

2,194

Apr 3

A delight to sit down with @therollupco to talk through how we are thinking about the institutional side of Crypto at @BaillieGifford.

Key points I have been conveying at conferences:

1/ Tokenisation = unitisation on steroids. This is about taking finance into a world of programmable unitisation.

Baillie Gifford’s approach is long-term, as ever! It’s not just slicing up funds into smaller pieces. It’s the same high-quality fund structure you already trust, but now fully programmable, composable, and 24/7.

Same rights. Same standards. Better outcomes for clients through programmability (automation), cost savings (onchain books and records, self-custody, less intermediaries) and composability (more flexibility to make portfolios without having to use the unsatisfactory fixes we have today).

2/ Tokenised funds are the gateway for TradFi.

Once you build the stack (digital custodians, transfer agents, compliance rails), you’re suddenly positioned to go fully onchain for everything else.

It’s the low-friction on-ramp that lets institutions test, learn, and then scale into native tokenised securities.

3/ This unlocks a merging TAMs phenomenon at scale.

Traditional verticals (banks, asset managers, exchanges, custody, wallets, distributors, market makers etc) are suddenly merging into the same market. The onchain rails (particularly combined with the power of AI) means that the hurdle rate to enter other markets has demonstrably dropped. That means that for everyone this is simultaneously an offence and defence matter. That’s what is driving the institutional onchain evolution. But it also means that there is a real reason to collaborate to get the best solutions for end clients. The existing hierarchy and stack is melting.

Bottom line is that institutions aren’t dabbling for hype.

We’re building the future of finance together.

Mar 31

6

464

Mar 17

I'm going to assume your PhD is not in geology!

A handful of fields are trans-boundary (they straddle the maritime border). In those cases we have a 'Unitisation Agreement' with Norway, which determines how much each country can extract. It's not an extraction race!

2

161

Mar 17

I saw a post on CEO.ca about Eco Atlantic $EOG.V $ECO and thought I’d share the 10 things that could get that person in a spot of bother:

1. Orinduik (Guyana) license extension

2. Announcement of exploration drilling in Orinduik

3. Navitas confirmation of farm in to Orinduik

4. Agreement with Exxon & Chevron on the unitisation of Hammerhead (already FIDed)

5. Extension of Canje license

6. Announcement of drilling on Canje

7. Environmental approval to drill 3B/4B triggering USD 11.5m payment to Eco

8. Inevitable run up in price while 3B/4B is drilled by Total as the target is huge

9. Farm out partnership announcement for Namibia blocks

10. Farm out partnership announcement for Block 1 CBK

1

5

351

Mar 4

No. Cross border fields are subject to “unitisation” in order that each country gets their fair share of oil and gas and the overall development is done in the most efficient way.

1

3

77

Feb 5

Press review for Thursday, February 5, 2026

Politics & Governance

The Guardian Post describes Cameroon as being on life support, citing a government on unending borrowing spree and aging leadership fatigue while noting that collaborators are increasingly disputing Paul Biya’s High Instructions.

Cameroon Tribune reports on the launch of a virtual information agency as Minister René Emmanuel Sadi kicks off the experimental phase to provide quality information across 10 regions.

The Horizon highlights a scandal where Gov’t’s tracking of alleged ‘fleeing’ workers via immigration backfires claiming figures like Viviane Biwole Ondoua and Owona Nguini have been victimized.

La Nouvelle Expression reports that at the Port of Douala Les directives du Pm respectées after the Director General bowed to the Prime Minister’s decision regarding contract signatures.

Economy & Finance

L’Economie focuses on private sector competitiveness and Ce que préconise le FMI as the IMF mission stays in Cameroon until mid-February while noting that 160 billion francs CFA is to be raised this month on the public securities market.

Cameroon Insider seeks to explain the Gov’t’s Borrowing Spree following a decree to borrow 1,650 billion francs CFA for infrastructure and settling treasury arrears.

Municipal Updates reports that CEMAC Leaders Advocate Debt Discipline and import substitution to escape a potential FCFA Devaluation.

The Horizon mentions that the Council for the Sovereignty of Cameroon denounces China’s complicity in granting unproductive loans.

International Relations & Diplomacy

Municipal Updates and L’Economie both highlight the Yoyo-Yolanda Cross-border Gas Field noting that Cameroon and Equatorial Guinea Ink Unitisation Agreement for joint exploitation.

Cameroon Tribune and Cameroon Insider report that the WTO Team Lauds Progress on preparations for the 14th Ministerial Conference stating that preparations are Rated Satisfactory.

Municipal Updates covers the Second Türkiye-Cameroon Business Forum opening in Douala to strengthen trade ties.

Security & Humanitarian Crisis

L’Oeil du Sahel reports a major seizure in Touboro where Customs Seizes Nearly 2000 Bladed Weapons in Bogdibo

Echos Santé and L’Oeil du Sahel report on the worsening situation in Logone-et-Chari where At least 366 displaced households are facing a humanitarian crisis.

La Nouvelle Expression highlights the Anglophone crisis with the shocking headline babies aged two and three months are in detention in Bamenda.

Health & Society

Echos Santé covers the WHO Summit in Geneva where Cameroon advocates for global health resilience, focusing on the fight against polio and antimicrobial resistance.

L’Oeil du Sahel notes that the North and Far-North regions have the best HIV prevalence rates.

The Horizon reports on social deviance in Douala schools prompting a ministerial crisis meeting led by Nalova Lyonga.

#MMINews

1

1

7

667

Jan 23

He blocked me coupla years ago when I provided his thread's readers with details of his multiple frauds in his landmark Hockeystick, including the remarkable PCA unitisation (scope-"error") trick.

Seems he doesn't appreciate knowledge-sharing.

Odd, for a "scientist"...

1

2

27

Jan 19

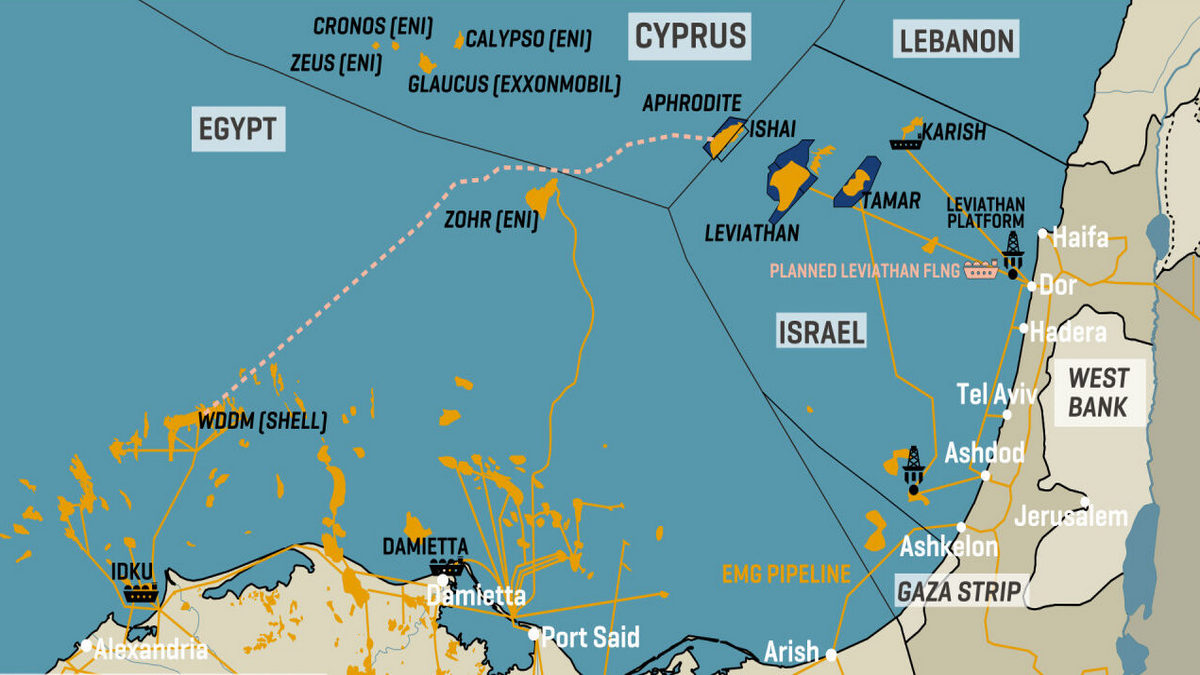

Israel and Cyprus are nearing a bilateral agreement on the Aphrodite–Ishai gas field, as talks reach a final stage on unitisation and joint development terms for the shared gas field.

↳Bosphorus News

bosphorusnews.com/article/is…

2

77

Jan 6

“…any delays or disruptions in regional cooperation or unitisation agreements, compounded by sanctions and the unclear authority of a transitional Venezuelan administration, leave T&T’s energy planners navigating a precarious landscape…”

Read today’s Guardian Editorial…

guardian.co.tt/article/venez…

166

“…any delays or disruptions in regional cooperation or unitisation agreements, compounded by sanctions and the unclear authority of a transitional Venezuelan administration, leave T&T’s energy planners navigating a precarious landscape…”

Read today’s Guardian Editorial…

guardian.co.tt/article/venez…

2

1

298

10 Dec 2025

Namibia MUST address the extreme historical wealth disparities between blacks and whites but NOT in an exculpatory socialist manner.

We must address the land and business ownership issues or they will continue to manifest as negative externalities on our economy and social fabric.

@NamPresidency could explore:

1. Mass Voucher Privatisation of State-Owned Commercial Assets

The Namibian state already owns or controls ~30–35 % of commercial farmland (resettlement farms parastatal farms) and significant mining/ fisheries/tourism concessions. Issue every adult citizen tradable, non-transferable vouchers worth, say, N$250 000 in shares of a new “Namibia Wealth Fund” that holds these assets. Overnight every black Namibian becomes a shareholder in the country’s productive core. The fund pays dividends (like Alaska’s oil fund). White owners are not touched directly, but the wealth distribution flips immediately.

2. 50-Year Leasehold Conversion with Compulsory Purchase Option

Convert all freehold commercial farmland into 99-year leaseholds. The state has a rolling right to buy any farm at 70 % of 2010 valuation (inflation-adjusted) whenever it comes on the market or changes hands. Farmers keep full use and can sell the lease, but the state gradually acquires the underlying title at a pre-set price. This is essentially what Taiwan and South Korea did, but stretched over decades instead of years.

3. Land-Bond Expropriation (the “Taiwan model” adapted)

Declare that any farm above 5 000 ha can be expropriated at 2.5× its annual land-tax valuation, paid 30 % cash 70 % in 20-year indexed government land bonds. Farmers can keep operating the farm as tenants or sell the bonds on the open market. Used successfully in East Asia; avoids hyperinflation and court battles of Zimbabwe-style seizures.

4. Mandatory Unitisation of Mining & Fishing Quotas

Force every mining license and fishing quota to be re-issued as a joint-venture in which a new state-citizen trust automatically gets 51 % equity (paid for with preferential tax credits over 10 years). The white firms keep management and profits proportional to their 49 %, but majority economic ownership moves to citizens. Namibia’s sovereign wealth fund could be the vehicle.

5. Diaspora Citizen Crowdfunding of Farms

Allow any Namibian citizen or diaspora member to bid for farms using state-backed 50-year zero-interest loans, GDP-linked loans. The state guarantees the loan; if the buyer defaults the farm reverts to the state. This is how Israel settled the Negev and parts of Galilee in the 1950s–60s.

1

3

2

92

28 Nov 2025

IMANI's Brief on Springfield's Latest Dance with Our Government

• In February 2025, the new Minister of Energy announced Ghana’s withdrawal of the forced unitisation directive between ENI’s Sankofa field and Springfield’s Afina discovery.

• IMANI was full of praise for the Minister because the forced unitisation order first issued in April 2020 was plainly absurd. It sought to compel Eni and Vitol to combine the Sankofa field (developed at a cost of almost $7bn) that was a proven, producing, field with Springfield’s Afina, which did not even have confirmed commercial find and hand over 55% of the merged field to Springfield.

• IMANI is aware of the intense lobbying of the current government by powerful people who held sway over the previous one to persist the wrongheaded policies of the past. The government’s and the Minister's decision to stand their ground on the unitisation issue thus impressed us.

• News that the government may want to buy Afina outright worries us because it could open the door for a capitulation to the lobbyists and backroom dealers.

• Afina remains a high-uncertainty asset. It is essentially a one-well discovery with long-delayed appraisal, fragmented testing history, and contested resource estimates. The absence of consistent, transparent, regulator-validated data makes any attempt to fix a reliable commercial value inherently speculative and vulnerable to political influence.

• At any rate, Ghana owns stakes already in Afina through Explorco and GNPC. It can choose to lend funds to the implicit joint venture to de-risk the Afina prospect through additional appraisal, including by drilling another well to improve commercial confidence.

• This loan can be structured as a convertible with Ghana owning the exclusive option to convert the loan to additional equity in the block. The option could have step-up provisions towards granting Ghana a controlling stake if necessary.

• The beauty of such an arrangement is that Springfield would then need to bring on board new farm-in partners to avoid being diluted to marginal minority status. At any rate, if Springfield is incapable of bringing onboard additional commercial partners, then it would mean that the block is not commercially viable, a critical assay for any spending by Ghana.

• Springfield’s initial public claim of over one billion barrels of recoverable reserves has not been independently verified through a full appraisal programme overseen by the Petroleum Commission. Contradictory interpretations from ENI, GNPC, and external analysts underscore the depth of technical ambiguity. In simple terms, the block could be worthless.

• Unfortunately, the process of confirming whether the block is commercially valuable for Ghana cannot be limited to a review of data collected by Springfield. The Minister's suggestion that he could base a decision to acquire the block on such a review is untenable. Determining the commercial viability of the block would likely involve significant new investment under an arrangement controlled by the government as a lender.

• GNPC’s exploration of a state-led acquisition based on limited data collected by Springfield risks converting private corporate risk into public fiscal liability. And, no, this cannot be addressed by just hiring a new consultant to vet data collected by Springfield and its contractors in a limited appraisal program designed and controlled by Springfield.

• Springfield’s reported debt exposure and its legal dispute with Swiss trader Petraco raise serious questions about whether GNPC could inadvertently absorb legacy liabilities or financially distressed obligations through the Afina deal. The company that drilled the only well at Afina has already won arbitration proceedings against Springfield because of the latter's refusal to pay its bills. All this raises questions about what actual serious investments Springfield has made in Afina for which reason it should dictate commercial terms through an acquisition process.

• Public denials by GNPC that it endorsed the infamous US$700 million valuation are welcome, yet insufficient. The valuation environment remains compromised if the process continues to rely on data curated or filtered by Springfield, the party with the strongest incentive to inflate asset value.

• Analysts have maintained the consistent position that Afina’s commerciality is unproven and that prior valuation ranges derived from Springfield-supplied data reflect optimism bias and weak regulatory oversight. These concerns remain valid and unaddressed by conclusive, regulator-supervised independent appraisal.

• The government’s evolving position under Minister John Jinapor reflects greater restraint and technical caution, particularly the commitment that any acquisition must be based on independent expert valuation. However, independence must be also be technical sound.

• There has simply not been sufficient appraisal to collect enough serious data for any valuer to work with.

• Once enough robust data is available, the focus can then switch to the appraisal procedure. Who selects the valuer, defines the scope, and controls data access will remain critical. We demand a full seat for civil society at that table to boost public confidence given the murky history of the Afina block.

• GNPC faces a structural conflict of interest: it cannot credibly act as buyer, technical assessor, and quasi-regulator simultaneously. The Petroleum Commission must reassert primacy as the technical arbiter, with full access to raw seismic and well data, and authority insulated from political or commercial pressure.

• Ghana’s current macroeconomic context (debt restructuring, fiscal consolidation, and IMF conditionalities) makes any large-scale upstream acquisition particularly risky and unwise.

• Capital allocated to an outright acquisition of Afina could crowd out more sustainable investments in proven gas infrastructure or other energy-infrastructure priorities.

• International best practice (e.g. Norway, UK, & Canada) shows that unitisation and asset transfers work best when governed by transparent data-sharing, regulator-led reservoir modelling, and strict separation between state ownership and commercial decision-making. Ghana’s process so far falls short of this benchmark.

• Comparative experiences from Brazil and Nigeria illustrate the danger of “national champion” strategies that overburden state oil companies with politically motivated acquisitions, leading to inefficiency, corruption exposure, and value destruction. Afina risks becoming another such cautionary tale if discipline is not enforced.

• A state acquisition of Afina can only be justified if strictly ring-fenced to the asset itself, excluding all non-Afina liabilities, backed by independent double-blind technical reviews, and publicly scrutinised by Parliament with civil society input prior to any commitment.

• But even these safeguards are not the first step. The first step is to design, fund, and execute a robust appraisal program to gather rigorous data. This first step to de-risk the prospect would naturally involve far less money than being bandied about.

• That money should be provided in the form of a convertible loan after the governance of Afina has been retooled to ensure that the current joint management committee has multistakeholder state and society dominance and assumes substantive control of the appraisal.

• Otherwise, the Afina acquisition would represent a classic moral hazard scenario: rewarding weak corporate governance, offsetting speculative risk at public expense, and institutionalising a precedent where distressed private oil firms can lobby the state for financial rescue via “strategic” resource narratives.

• The Afina saga is therefore not merely about petroleum. It is a powerful test of this government’s commitment to good governance and the prudent use of the public purse.

4

19

68

6,511

21 Nov 2025

This morning, I listened to Ghana’s Minister of Energy and Green Transition on Joy FM. A few comments:

1. To be fair, the Minister shared the same position when I asked him before my earlier post. We have had open and honest engagement with him since he assumed office. ACEP’s policy engagement and influence have strengthened under his tenure more than under any other minister. We agree and disagree frankly, and he has never tried to gag our policy views.

2. He and the Minister of Finance entrusted us with leading negotiations with the IPPs, saving the country about $250m in exiting debt and more than $7 billion across the life of the agreements.

3. We also acknowledge the significant reforms he has driven in the energy sector over the past ten months, which are genuinely commendable.

4. Our position is not about his support for local companies. The law already provides incentives for Ghanaian participation in the oil sector. ACEP supports the local content regulations, even though their implementation leaves much to be desired.

5. The real issue is that no law allows the state to absorb private sector losses, whether local or foreign, especially when the evidence shows the venture is risky and likely to cost the country.

6. On the “independent evaluation” of the Springfield’s field: the Petroleum Commission is the legally mandated independent regulator with more than a decade of institutional history. If the government doubts its independence, or the Commission itself cannot assert it, then we have a much bigger governance problem.

7. The Commission has repeatedly stated that Springfield has not provided the complete raw data. If the regulator is not satisfied, its evaluation remains inconclusive. Full stop. The state must allow the Commission to deliver a judgment that the industry can also assess and trust or critique.

8. There’s no need to sidestep an incomplete regulatory process simply because a private company dislikes the outcome. Doing so undermines the entire regulatory ecosystem and weakens the authority of the Commission over all sector players.

9. We insist that having GNPC and Explorco lead a new “independent valuation” is problematic. Their past actions and poor judgement have cost the country money, both directly and through project delays. The Minister himself reversed some of their decisions which anchored the unitisation claim until Ghana lost at arbitration. It is the same technical people leading the corporation today.

10..These same entities carried out a valuation less than six months ago that endorsed Springfield’s data, ignoring the Commission’s technical concerns and established international processes for reservoir audits.

11. If the Commission is no longer independent, that should be stated openly. Otherwise, it must be allowed to complete its work with full access to the data before any external intervention. Companies may challenge the Commission’s decisions in law only after complying fully with regulatory requirements.

12. Bringing in a new consultant, paid with state funds before the regulator completes its job, weakens institutional control and undermines the state’s ability to manage the petroleum sector.

13. Thus far, every analysis, except that of Springfield and GNPC, contradicts the claims of commerciality of the field.

14. The solution is simple: give the regulator full access to the raw data and allow it to finish its work. If any party disagrees, the remedies lie in law, not political shortcuts.

20

78

175

51,455

19 Nov 2025

The government’s intention to reassign the block to a more financially robust operator sends a very clear signal. From the protracted unitisation deadlock with ENI, to the recent $100 million fraud allegations by Petraco, and

1

1

3

107

19 Nov 2025

This is refreshing to see. Mind you, this is the same company that almost secured the benefit of a forced/arbitrary unitisation directive under the previous government.

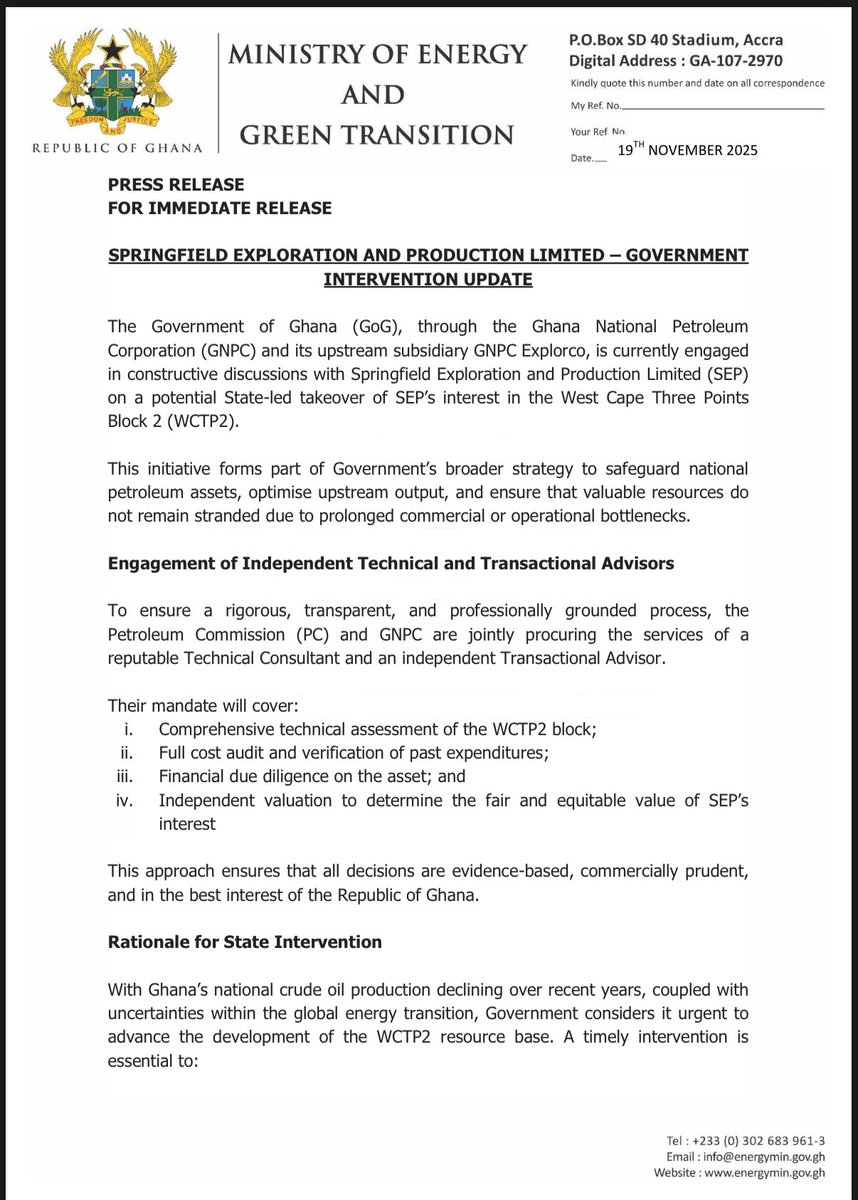

19 Nov 2025

The Government of Ghana (GoG) currently engaged in constructive discussions with Springfield Exploration and Production Limited (SEP) on a potential State-led takeover of SEP's interest in the West Cape Three Points Block 2 (WCTP2).

3

15

2,822

18 Nov 2025

What kind of warped logic is this??? How is that fraud??? His oil block and ENI’s oil block were supposed to be unitised. He’s fulfilled all requirements however the new government cancelled the unitisation and the investors are crying foul. How is that fraud???

41