18 uczestników

Dwie drużyny

1 zwycięsca

Ciekawe kto zgarnie główną nagrode🔥

#tdm3 #tdm #totalnadramamc #plvtuber #vtpl #minecraft

4

14

363

Jun 3

1

1

12

206

Jun 2

Cute Twitch panels I made for @IkimeVT !!!! Each has a custom outfit (・∀・)

#commission #vtpl #vt #comms

1

2

9

180

HEJKA WSZYSTKIM!

Jesteś minecraftowym twórcą albo po prostu lubisz pograc sobie w MC na streamie z innymi ludźmi? A może jednak interesuje cie gra w pojedynke? To wszystko na #TDM3 !

Zapraszamy was na serwer, który opiera się na twórcach chcacy dać frajde nie tylko sobie ale i swoim widzom dzieki kontentowi który oferujemy!

Rozbudowane mechaniki, role play, 12 klas postacii do wyboru, ekonomia, fabułka, spozniony start serwera, a to wszystko na wyciagniecie reki!

Wejdz w profil i dolacz na discorda jezeli chcesz dolozyc cegielke do naszego wspanialego community!

Do zobaczenia!

#minecraft #totalnadramamc #plvtuber #vtuberpl #plvt #vtpl

2

7

17

625

Biore odpowiedzialnosc za lige Umamusume na #tdm3 Ale za wasze porażki podczas wyścigów już nie.

Trzeba tylko dogadać z bukmacherami obstawianie graczy i będzie wspaniale.

#totalnadramamc #plvtuber #vtuberpl #minecraft #vtpl

3

369

Stockizen Research | SEBI RA: INH000017675

Force Motors (FORCEMOT):

- CMP ~₹20,866 (as of 8 May 2026 close), trading near recent levels; you are stuck at ~8% unrealised loss (implied buy price ~₹22,500).

- 52w range: ₹9,380 low to ₹26,486 high; corrected ~21% from 52w high post Q4 results.

- Q4 FY26: Revenue ₹2,550 Cr ( 8.2% YoY, 19.8% QoQ) — highest ever quarterly revenue; PAT ₹278.5 Cr (-36% YoY, -31% QoQ) due to higher tax, one-offs and margin compression.

- FY26 full year: Revenue ₹9,167 Cr ( 12.8% YoY), PAT ₹1,212 Cr ( 51% YoY); debt-free status achieved (long-term debt minimal).

- Valuation: PE ~26x, PB ~6.6x (BV ~₹3,183); ROE 29%, ROCE 36%.

- Promoter holding stable at 61.63% (zero pledge); board recommended ₹50 dividend.

- Recent update: Launched new Force Traveller N Range (May 2026); acquired VTPL for ₹162 Cr.

- Critical view: Strong annual growth, debt reduction and new product launch are positives in auto ancillary/LCV space, but Q4 profit miss triggered sell-off; premium valuation offers limited margin of safety amid cyclical auto demand risks, raw material costs and execution on volumes. No immediate re-rating catalysts visible unless sustained revenue growth and margin recovery in Q1 FY27. Hold with caution if conviction on long-term auto recovery; consider strict stop-loss to protect capital given 8% loss position.

I/associates do not hold Force Motors as on this date.

Investments in securities market are subject to market risks. Read all related documents carefully before investing.

1

238

Stockizen Research | SEBI RA: INH000017675

Force Motors (FORCEMOT):

- CMP ~₹20,866 (as of 8 May 2026 close), trading near recent levels; you are stuck at ~8% unrealised loss (implied buy price ~₹22,500).

- 52w range: ₹9,380 low to ₹26,486 high; corrected ~21% from 52w high post Q4 results.

- Q4 FY26: Revenue ₹2,550 Cr ( 8.2% YoY, 19.8% QoQ) - highest ever quarterly revenue; PAT ₹278.5 Cr (-36% YoY, -31% QoQ) due to higher tax, one-offs and margin compression.

- FY26 full year: Revenue ₹9,167 Cr ( 12.8% YoY), PAT ₹1,212 Cr ( 51% YoY); debt-free status achieved (long-term debt minimal).

- Valuation: PE ~26x, PB ~6.6x (BV ~₹3,183); ROE 29%, ROCE 36%.

- Promoter holding stable at 61.63% (zero pledge); board recommended ₹50 dividend.

- Recent update: Launched new Force Traveller N Range (May 2026); acquired VTPL for ₹162 Cr.

- Critical view: Strong annual growth, debt reduction and new product launch are positives in auto ancillary/LCV space, but Q4 profit miss triggered sell-off; premium valuation offers limited margin of safety amid cyclical auto demand risks, raw material costs and execution on volumes. No immediate re-rating catalysts visible unless sustained revenue growth and margin recovery in Q1 FY27. Hold with caution if conviction on long-term auto recovery; consider strict stop-loss to protect capital given 8% loss position.

I/associates do not hold Force Motors as on this date.

Investments in securities market are subject to market risks. Read all related documents carefully before investing.

2

290

Właśnie na discordzie TDM wleciał jeden z najważniejszych newsów dla graczy! Jeżeli jesteś graczem to sprawdź ogłoszenia, a jeżeli się nie zapisałeś to na co czekasz??

#totalnadramamc #tdm3 #vtpl #plvtuber

3

11

940

Hejo wszystkim!

Nasz pre sezon powoli zbliża się wielkimi krokami! Niedługo bedziecie mogli ogladac swoich faworytów na TDM pre sezonowym.

A dla twórcyw którzy chcieliby po popykać oficjalnie zapraszamy na discorda. Serwer startuje już w lipcu (aczkolwiek znając moderacje to gdzieś we wrześniu 🤭)

Do zobaczenia!

#TDM3 #minecraft #vtpl #plvtuber

1

6

24

879

Apr 24

8

19

718

Apr 23

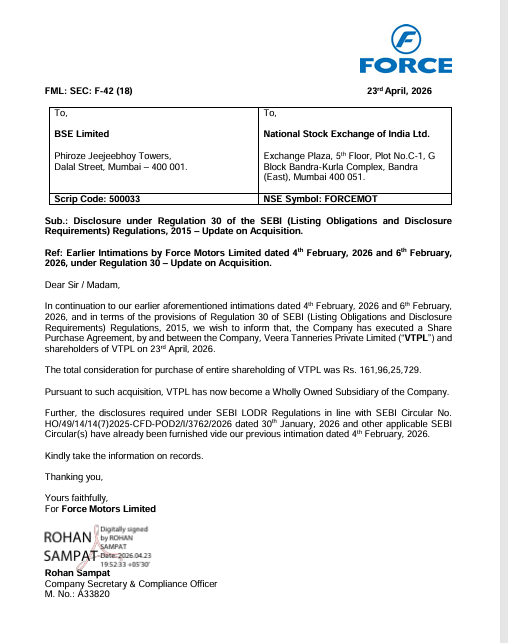

FORCE Motors Update 👇

FORCE Motors has acquired 100% stake in Veera Tanneries Pvt Ltd (VTPL)

Total deal value is around ₹161.96 crore

The acquisition was completed on 23rd April 2026.

3

1

30

10,009

Company: Force Motors

Update Type: Acquisition 🛒

📦Acquired Company: Veera Tanneries Private Limited (VTPL)

💼Business Overview: Refer Filing

📊Percentage Acquired: 100% (Entire shareholding)

💰Total Consideration Paid: Rs. 161,96,25,729

9

968

Apr 21

12

22

1,337

Też dostaje pytania na temat #TDM3 jak niby ma wyglądać gameplay i czym on ma się różnić od zeszłego sezonu. Tyle co powiedziałem na DC musi każdemu starczyć. Niespodzianka dla twórców to najlepsza rzecz kiedy startuje taki server!

#totalnadramamc #plvtuber #vtpl #minecraft

1

11

482

Apr 18

18

23

1,564