(2/3) $LUXE's TEV is $400mm (50% of mkt cap is cash). MyTheresa (~40% of biz) did ~$70mm of LTM EBITDA, growing double digits w/ expanding margins. Is that worth more than 5.7x LTM EBITDA? How likely is it that investing to turnaround YNAP will yield >$0 value? W/ this team?

1

8

978

(1/3) Great summary. A classic investment opp can be when a valuation capitalizes the losses of a segment in transition (in this case YNAP, which LUXE acquired). So $0 YNAP out completely. Nix it. Now what's it worth?Recall they got $500mm to fix it but they don't have to right?

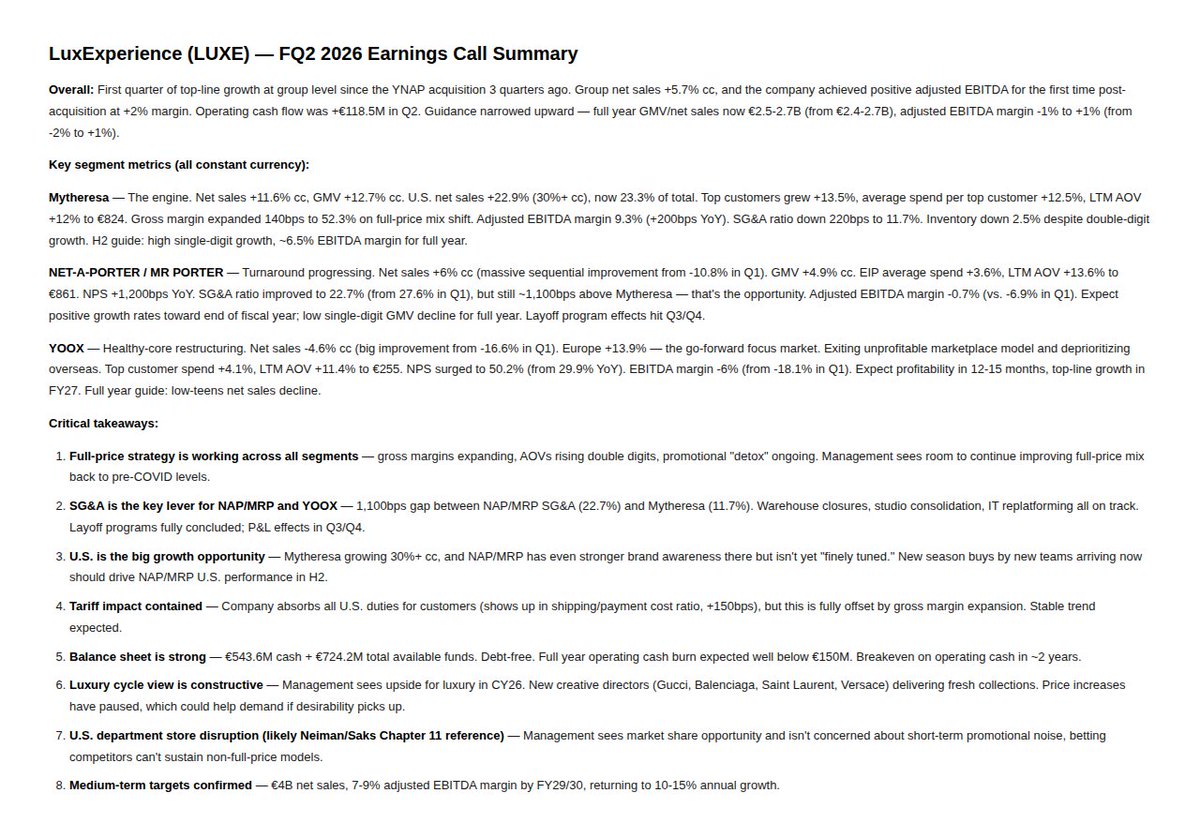

Following up on this, LUXE reported this morning:

OK quarter overall, with some messiness in NAP/MRP that makes it look worse than reality. The good: strong margin expansion across all three segments and another beat at Mytheresa. The bad: NAP/MRP top line -5% cc as the company prioritized full-price sales and lapped a heavily promotional quarter under Richemont. Net-net, LUXE is making good progress on the integration and should be on a path to MSD-HSD EBITDA margins. Stock is extraordinarily cheap — 0.2x EV/sales, 0.4x EV/GP, and ~2x EBITDA on the 7-9% margin target in 2-3 years.

Key highlights:

Net sales flat cc

Group SG&A ratio 18% (vs 19% Q2, 22% Q1)

Adj. EBITDA margin ~1%

Mytheresa: sales 10% cc, GMV 11%, GM 240bps, adj. EBITDA 50% to 5.5% margin ( 160bps)

NAP/MRP: sales -5% cc, GM 700bps, adj. EBITDA margin -0.5%

Off-price: sales -7% cc, GM 620bps, adj. EBITDA margin -5.5%

Standout was Mytheresa: 10% growth (US 34%) with healthy margin expansion. Group SG&A progress sets up real operating leverage from here. Disappointment was NAP/MRP top line, but the 700bps gross margin print shows the focus on higher-quality sales is working. Middle East conflict was a headwind, not quantified.

Somewhat of a reset on top-line expectations, but continued progress on the NAP/MRP/Off-price integration — which we knew would be lumpy. Valuation continues to get sillier: on the 8% margin target, ~2x EBITDA and ~3x EPS a couple years out.

1

1

16

7,604

May 19

Our summary has these points in the bull case:

🐂 𝐁𝐮𝐥𝐥 𝐂𝐚𝐬𝐞

• 𝐂𝐨𝐬𝐭 𝐒𝐲𝐧𝐞𝐫𝐠𝐢𝐞𝐬 𝐌𝐚𝐭𝐞𝐫𝐢𝐚𝐥𝐢𝐳𝐢𝐧𝐠 𝐅𝐚𝐬𝐭 — The group SG&A cost ratio plummeted from 21.9% in Q1 to 18.3% in Q3. The ability to extract costs from the bloated YNAP infrastructure is tracking ahead of schedule.

• 𝐆𝐫𝐨𝐬𝐬 𝐌𝐚𝐫𝐠𝐢𝐧𝐬 𝐄𝐱𝐩𝐚𝐧𝐝𝐢𝐧𝐠 — A strict discipline of full-price selling is working. NAP/MRP gross profit margin surged 700bps YoY to 48.5%, proving the brand equity remains strong when discounts are removed.

1

3

143

Growing instant AI narratives will hand great opps for investors. This AI summary is great, but misses a key punchline. $LUXE is purposely detoxing YNAP from old heavy promos, which impacts NT headline revs, but gross profit $ 7% YoY, and ex-FX probably closer to 13% YoY.

May 19

$LUXE Q3 2026 earnings: Cost Execution Drives Margin Gains, But Top-Line Recovery Stalls

LuxExperience reported its second consecutive quarter of positive Adjusted EBITDA ( €5.7M), validating that its aggressive SG&A reduction plan for the acquired YNAP assets is working. However, the volume recovery is stalling. Group Net Sales fell 5.2% to €618.4M (stable at 0.0% ex-FX). The core Mytheresa segment remains a stable growth engine ( 5.6%), but the turnaround segments—NAP/MRP and YOOX—reversed their Q2 momentum, posting double-digit reported revenue declines. While management confirmed FY26 guidance and the balance sheet is now debt-free, the heavy reliance on adjustments to claim 'profitability' while GAAP net losses expand remains a significant caveat for investors.

Full article with charts - link in bio

🐂 𝐁𝐮𝐥𝐥 𝐂𝐚𝐬𝐞

• 𝐂𝐨𝐬𝐭 𝐒𝐲𝐧𝐞𝐫𝐠𝐢𝐞𝐬 𝐌𝐚𝐭𝐞𝐫𝐢𝐚𝐥𝐢𝐳𝐢𝐧𝐠 𝐅𝐚𝐬𝐭 — The group SG&A cost ratio plummeted from 21.9% in Q1 to 18.3% in Q3. The ability to extract costs from the bloated YNAP infrastructure is tracking ahead of schedule.

• 𝐆𝐫𝐨𝐬𝐬 𝐌𝐚𝐫𝐠𝐢𝐧𝐬 𝐄𝐱𝐩𝐚𝐧𝐝𝐢𝐧𝐠 — A strict discipline of full-price selling is working. NAP/MRP gross profit margin surged 700bps YoY to 48.5%, proving the brand equity remains strong when discounts are removed.

🐻 𝐁𝐞𝐚𝐫 𝐂𝐚𝐬𝐞

• 𝐓𝐮𝐫𝐧𝐚𝐫𝐨𝐮𝐧𝐝 𝐓𝐨𝐩-𝐋𝐢𝐧𝐞 𝐢𝐬 𝐑𝐞𝐯𝐞𝐫𝐬𝐢𝐧𝐠 — After narrowing its sales decline to just -1.0% in Q2, NAP/MRP reversed course in Q3, plunging 11.7%. YOOX also worsened to an 11.4% decline. The turnaround is currently entirely margin-led, not volume-led.

• 𝐃𝐞𝐞𝐩 𝐆𝐀𝐀𝐏 𝐍𝐞𝐭 𝐋𝐨𝐬𝐬𝐞𝐬 — Despite celebrating 'Adjusted EBITDA profitability', the company posted a net loss of €35.4M for the quarter, driven by heavy depreciation, amortization, and transaction costs.

⚖️ 𝐕𝐞𝐫𝐝𝐢𝐜𝐭: ⚪

Neutral. Management is executing brilliantly on the elements they can control—costs and gross margin discipline. However, the top-line deterioration at the YNAP brands and emerging macroeconomic headwinds indicate that the commercial turnaround is far from complete.

𝐊𝐞𝐲 𝐓𝐡𝐞𝐦𝐞𝐬

🟢 𝐀𝐠𝐠𝐫𝐞𝐬𝐬𝐢𝐯𝐞 𝐒𝐆&𝐀 𝐄𝐟𝐟𝐢𝐜𝐢𝐞𝐧𝐜𝐲

Cost reduction is the primary driver of LuxExperience's profitability. The Group Adjusted SG&A ratio has been steadily decelerating, dropping 360 basis points from 21.9% in Q1 FY26, to 19.1% in Q2, down to 18.3% in Q3. This rapid cost extraction from the legacy YNAP businesses is critical to reaching the 7-9% medium-term margin target.

🟢 𝐅𝐮𝐥𝐥-𝐏𝐫𝐢𝐜𝐞 𝐃𝐢𝐬𝐜𝐢𝐩𝐥𝐢𝐧𝐞 𝐑𝐞𝐬𝐭𝐨𝐫𝐞𝐬 𝐆𝐫𝐨𝐬𝐬 𝐌𝐚𝐫𝐠𝐢𝐧𝐬

The mandate to detox from promotions is yielding spectacular results on the gross profit line. NAP & MRP saw its gross margin expand by 700bps to 48.5% YoY, while YOOX expanded by 620bps to 37.5%. Management's willingness to sacrifice unprofitable volume for margin integrity is accelerating the path to break-even.

🟢 𝐌𝐲𝐭𝐡𝐞𝐫𝐞𝐬𝐚 𝐑𝐞𝐦𝐚𝐢𝐧𝐬 𝐭𝐡𝐞 𝐆𝐫𝐨𝐰𝐭𝐡 𝐄𝐧𝐠𝐢𝐧𝐞

The legacy Mytheresa business continues to anchor the group, posting 5.6% reported growth (9.9% ex-FX) and generating €14.1M in Adjusted EBITDA. Growth was driven by a 12.5% LTM increase in Average Order Value (AOV) to €847, fueled by exclusive capsule collections from Balenciaga, Bottega Veneta, and Gucci.

🔴 𝐓𝐮𝐫𝐧𝐚𝐫𝐨𝐮𝐧𝐝 𝐒𝐞𝐠𝐦𝐞𝐧𝐭𝐬 𝐑𝐞𝐯𝐞𝐫𝐬𝐢𝐧𝐠 𝐓𝐨𝐩-𝐋𝐢𝐧𝐞 𝐌𝐨𝐦𝐞𝐧𝐭𝐮𝐦 [NEW]

A major concern is the reversing momentum in the acquired segments. In Q2, management touted that NAP/MRP had narrowed its sales decline to just -1.0%. In Q3, that decline widened dramatically back to -11.7% (-5.1% ex-FX). YOOX also saw its decline worsen from -7.3% in Q2 to -11.4% in Q3. The commercial turnaround is proving volatile.

🔴🔴 𝐄𝐁𝐈𝐓𝐃𝐀 𝐍𝐚𝐫𝐫𝐚𝐭𝐢𝐯𝐞 𝐂𝐨𝐧𝐭𝐫𝐚𝐝𝐢𝐜𝐭𝐬 𝐄𝐱𝐩𝐚𝐧𝐝𝐢𝐧𝐠 𝐍𝐞𝐭 𝐋𝐨𝐬𝐬𝐞𝐬 [NEW]

Management's narrative heavily emphasizes the 'second consecutive quarter of Adjusted EBITDA profitability' ( €5.7M). However, looking at the actual bottom line contradicts this rosy picture: Net Loss for the quarter was -€35.4M. This massive gap is driven by surging Depreciation & Amortization (€18.7M in Q3 vs €11.6M in Q1) and high transaction/restructuring costs (€6.6M). True profitability remains years away.

🔴 𝐆𝐞𝐨𝐩𝐨𝐥𝐢𝐭𝐢𝐜𝐚𝐥 𝐇𝐞𝐚𝐝𝐰𝐢𝐧𝐝𝐬 𝐃𝐫𝐚𝐠𝐠𝐢𝐧𝐠 𝐆𝐫𝐨𝐰𝐭𝐡 [NEW]

Management explicitly cited 'geopolitical headwinds in March' as a factor weighing on Q3 results. This macro factor caused a decelerating trend even in the healthy Mytheresa segment, where growth slowed from 8.8% in Q2 to 5.6% in Q3. Continued macro instability could threaten the FY26 guidance.

⚪ 𝐂𝐨𝐦𝐦𝐞𝐫𝐜𝐞 𝐏𝐥𝐚𝐭𝐟𝐨𝐫𝐦 𝐌𝐢𝐠𝐫𝐚𝐭𝐢𝐨𝐧 𝐨𝐧 𝐓𝐫𝐚𝐜𝐤

A critical technological milestone is underway: the migration of NET-A-PORTER and MR PORTER onto LuxExperience's proprietary tech platform. Completing this infrastructure consolidation is the linchpin to permanently lowering the IT and operational costs of the acquired brands.

𝐎𝐭𝐡𝐞𝐫 𝐊𝐏𝐈𝐬

𝐆𝐫𝐨𝐮𝐩 𝐂𝐚𝐬𝐡 𝐏𝐨𝐬𝐢𝐭𝐢𝐨𝐧: €436.1 million

Stable and secure. Cash and cash investments ended Q3 at €436.1M, giving the company ample runway to fund the remaining cash burn required for the YNAP turnaround. Crucially, the company ended the quarter completely debt-free, having paid down previous bank liabilities.

𝐓𝐇𝐄 𝐎𝐔𝐓𝐍𝐄𝐓 𝐃𝐢𝐯𝐞𝐬𝐭𝐢𝐭𝐮𝐫𝐞: Completed

The sale of THE OUTNET assets to The O Group LLC was successfully closed on April 30, 2026. This divestiture immediately simplifies the Off-Price segment, allowing management to focus purely on fixing the core YOOX business.

𝐆𝐮𝐢𝐝𝐚𝐧𝐜𝐞

𝐅𝐘𝟐𝟔 𝐆𝐫𝐨𝐬𝐬 𝐌𝐞𝐫𝐜𝐡𝐚𝐧𝐝𝐢𝐬𝐞 𝐕𝐚𝐥𝐮𝐞 (𝐆𝐌𝐕): €2.5 - €2.7 billion

Stable. Management confirmed this full-year target. Given the €1.82B consolidated Net Sales generated in the first nine months, the company is on track to hit this target, indicating that Q4 volumes are expected to remain consistent despite ongoing business pruning.

𝐅𝐘𝟐𝟔 𝐀𝐝𝐣𝐮𝐬𝐭𝐞𝐝 𝐄𝐁𝐈𝐓𝐃𝐀 𝐌𝐚𝐫𝐠𝐢𝐧: -1% to 1%

Accelerating probability of achievement. Year-to-date Adjusted EBITDA sits at roughly -€2.7M on €1.83B of sales (essentially a 0.0% margin). Given the structural improvements in SG&A demonstrated in Q3, the company is highly likely to finish the year safely within this confirmed guidance range.

𝐊𝐞𝐲 𝐐𝐮𝐞𝐬𝐭𝐢𝐨𝐧𝐬

𝐍𝐀𝐏/𝐌𝐑𝐏 𝐕𝐨𝐥𝐮𝐦𝐞 𝐑𝐞𝐜𝐨𝐯𝐞𝐫𝐲

The revenue decline for NAP/MRP widened back to 11.7% in Q3 after narrowing in Q2. When do you expect the new buying strategies and merchandise deliveries to finally return this segment to top-line growth?

𝐁𝐫𝐢𝐝𝐠𝐞 𝐟𝐫𝐨𝐦 𝐄𝐁𝐈𝐓𝐃𝐀 𝐭𝐨 𝐍𝐞𝐭 𝐈𝐧𝐜𝐨𝐦𝐞

With Depreciation & Amortization accelerating to nearly €19M this quarter, what is the expected normalized run-rate for D&A post-integration, and when do you expect to achieve positive GAAP Net Income?

𝐆𝐞𝐨𝐩𝐨𝐥𝐢𝐭𝐢𝐜𝐚𝐥 𝐈𝐦𝐩𝐚𝐜𝐭

You cited geopolitical headwinds in March affecting sales. Have these headwinds persisted into April and May, and are they concentrated in specific regions like Europe or the Middle East?

2

13

5,218

May 19

$LUXE Q3 2026 earnings: Cost Execution Drives Margin Gains, But Top-Line Recovery Stalls

LuxExperience reported its second consecutive quarter of positive Adjusted EBITDA ( €5.7M), validating that its aggressive SG&A reduction plan for the acquired YNAP assets is working. However, the volume recovery is stalling. Group Net Sales fell 5.2% to €618.4M (stable at 0.0% ex-FX). The core Mytheresa segment remains a stable growth engine ( 5.6%), but the turnaround segments—NAP/MRP and YOOX—reversed their Q2 momentum, posting double-digit reported revenue declines. While management confirmed FY26 guidance and the balance sheet is now debt-free, the heavy reliance on adjustments to claim 'profitability' while GAAP net losses expand remains a significant caveat for investors.

Full article with charts - link in bio

🐂 𝐁𝐮𝐥𝐥 𝐂𝐚𝐬𝐞

• 𝐂𝐨𝐬𝐭 𝐒𝐲𝐧𝐞𝐫𝐠𝐢𝐞𝐬 𝐌𝐚𝐭𝐞𝐫𝐢𝐚𝐥𝐢𝐳𝐢𝐧𝐠 𝐅𝐚𝐬𝐭 — The group SG&A cost ratio plummeted from 21.9% in Q1 to 18.3% in Q3. The ability to extract costs from the bloated YNAP infrastructure is tracking ahead of schedule.

• 𝐆𝐫𝐨𝐬𝐬 𝐌𝐚𝐫𝐠𝐢𝐧𝐬 𝐄𝐱𝐩𝐚𝐧𝐝𝐢𝐧𝐠 — A strict discipline of full-price selling is working. NAP/MRP gross profit margin surged 700bps YoY to 48.5%, proving the brand equity remains strong when discounts are removed.

🐻 𝐁𝐞𝐚𝐫 𝐂𝐚𝐬𝐞

• 𝐓𝐮𝐫𝐧𝐚𝐫𝐨𝐮𝐧𝐝 𝐓𝐨𝐩-𝐋𝐢𝐧𝐞 𝐢𝐬 𝐑𝐞𝐯𝐞𝐫𝐬𝐢𝐧𝐠 — After narrowing its sales decline to just -1.0% in Q2, NAP/MRP reversed course in Q3, plunging 11.7%. YOOX also worsened to an 11.4% decline. The turnaround is currently entirely margin-led, not volume-led.

• 𝐃𝐞𝐞𝐩 𝐆𝐀𝐀𝐏 𝐍𝐞𝐭 𝐋𝐨𝐬𝐬𝐞𝐬 — Despite celebrating 'Adjusted EBITDA profitability', the company posted a net loss of €35.4M for the quarter, driven by heavy depreciation, amortization, and transaction costs.

⚖️ 𝐕𝐞𝐫𝐝𝐢𝐜𝐭: ⚪

Neutral. Management is executing brilliantly on the elements they can control—costs and gross margin discipline. However, the top-line deterioration at the YNAP brands and emerging macroeconomic headwinds indicate that the commercial turnaround is far from complete.

𝐊𝐞𝐲 𝐓𝐡𝐞𝐦𝐞𝐬

🟢 𝐀𝐠𝐠𝐫𝐞𝐬𝐬𝐢𝐯𝐞 𝐒𝐆&𝐀 𝐄𝐟𝐟𝐢𝐜𝐢𝐞𝐧𝐜𝐲

Cost reduction is the primary driver of LuxExperience's profitability. The Group Adjusted SG&A ratio has been steadily decelerating, dropping 360 basis points from 21.9% in Q1 FY26, to 19.1% in Q2, down to 18.3% in Q3. This rapid cost extraction from the legacy YNAP businesses is critical to reaching the 7-9% medium-term margin target.

🟢 𝐅𝐮𝐥𝐥-𝐏𝐫𝐢𝐜𝐞 𝐃𝐢𝐬𝐜𝐢𝐩𝐥𝐢𝐧𝐞 𝐑𝐞𝐬𝐭𝐨𝐫𝐞𝐬 𝐆𝐫𝐨𝐬𝐬 𝐌𝐚𝐫𝐠𝐢𝐧𝐬

The mandate to detox from promotions is yielding spectacular results on the gross profit line. NAP & MRP saw its gross margin expand by 700bps to 48.5% YoY, while YOOX expanded by 620bps to 37.5%. Management's willingness to sacrifice unprofitable volume for margin integrity is accelerating the path to break-even.

🟢 𝐌𝐲𝐭𝐡𝐞𝐫𝐞𝐬𝐚 𝐑𝐞𝐦𝐚𝐢𝐧𝐬 𝐭𝐡𝐞 𝐆𝐫𝐨𝐰𝐭𝐡 𝐄𝐧𝐠𝐢𝐧𝐞

The legacy Mytheresa business continues to anchor the group, posting 5.6% reported growth (9.9% ex-FX) and generating €14.1M in Adjusted EBITDA. Growth was driven by a 12.5% LTM increase in Average Order Value (AOV) to €847, fueled by exclusive capsule collections from Balenciaga, Bottega Veneta, and Gucci.

🔴 𝐓𝐮𝐫𝐧𝐚𝐫𝐨𝐮𝐧𝐝 𝐒𝐞𝐠𝐦𝐞𝐧𝐭𝐬 𝐑𝐞𝐯𝐞𝐫𝐬𝐢𝐧𝐠 𝐓𝐨𝐩-𝐋𝐢𝐧𝐞 𝐌𝐨𝐦𝐞𝐧𝐭𝐮𝐦 [NEW]

A major concern is the reversing momentum in the acquired segments. In Q2, management touted that NAP/MRP had narrowed its sales decline to just -1.0%. In Q3, that decline widened dramatically back to -11.7% (-5.1% ex-FX). YOOX also saw its decline worsen from -7.3% in Q2 to -11.4% in Q3. The commercial turnaround is proving volatile.

🔴🔴 𝐄𝐁𝐈𝐓𝐃𝐀 𝐍𝐚𝐫𝐫𝐚𝐭𝐢𝐯𝐞 𝐂𝐨𝐧𝐭𝐫𝐚𝐝𝐢𝐜𝐭𝐬 𝐄𝐱𝐩𝐚𝐧𝐝𝐢𝐧𝐠 𝐍𝐞𝐭 𝐋𝐨𝐬𝐬𝐞𝐬 [NEW]

Management's narrative heavily emphasizes the 'second consecutive quarter of Adjusted EBITDA profitability' ( €5.7M). However, looking at the actual bottom line contradicts this rosy picture: Net Loss for the quarter was -€35.4M. This massive gap is driven by surging Depreciation & Amortization (€18.7M in Q3 vs €11.6M in Q1) and high transaction/restructuring costs (€6.6M). True profitability remains years away.

🔴 𝐆𝐞𝐨𝐩𝐨𝐥𝐢𝐭𝐢𝐜𝐚𝐥 𝐇𝐞𝐚𝐝𝐰𝐢𝐧𝐝𝐬 𝐃𝐫𝐚𝐠𝐠𝐢𝐧𝐠 𝐆𝐫𝐨𝐰𝐭𝐡 [NEW]

Management explicitly cited 'geopolitical headwinds in March' as a factor weighing on Q3 results. This macro factor caused a decelerating trend even in the healthy Mytheresa segment, where growth slowed from 8.8% in Q2 to 5.6% in Q3. Continued macro instability could threaten the FY26 guidance.

⚪ 𝐂𝐨𝐦𝐦𝐞𝐫𝐜𝐞 𝐏𝐥𝐚𝐭𝐟𝐨𝐫𝐦 𝐌𝐢𝐠𝐫𝐚𝐭𝐢𝐨𝐧 𝐨𝐧 𝐓𝐫𝐚𝐜𝐤

A critical technological milestone is underway: the migration of NET-A-PORTER and MR PORTER onto LuxExperience's proprietary tech platform. Completing this infrastructure consolidation is the linchpin to permanently lowering the IT and operational costs of the acquired brands.

𝐎𝐭𝐡𝐞𝐫 𝐊𝐏𝐈𝐬

𝐆𝐫𝐨𝐮𝐩 𝐂𝐚𝐬𝐡 𝐏𝐨𝐬𝐢𝐭𝐢𝐨𝐧: €436.1 million

Stable and secure. Cash and cash investments ended Q3 at €436.1M, giving the company ample runway to fund the remaining cash burn required for the YNAP turnaround. Crucially, the company ended the quarter completely debt-free, having paid down previous bank liabilities.

𝐓𝐇𝐄 𝐎𝐔𝐓𝐍𝐄𝐓 𝐃𝐢𝐯𝐞𝐬𝐭𝐢𝐭𝐮𝐫𝐞: Completed

The sale of THE OUTNET assets to The O Group LLC was successfully closed on April 30, 2026. This divestiture immediately simplifies the Off-Price segment, allowing management to focus purely on fixing the core YOOX business.

𝐆𝐮𝐢𝐝𝐚𝐧𝐜𝐞

𝐅𝐘𝟐𝟔 𝐆𝐫𝐨𝐬𝐬 𝐌𝐞𝐫𝐜𝐡𝐚𝐧𝐝𝐢𝐬𝐞 𝐕𝐚𝐥𝐮𝐞 (𝐆𝐌𝐕): €2.5 - €2.7 billion

Stable. Management confirmed this full-year target. Given the €1.82B consolidated Net Sales generated in the first nine months, the company is on track to hit this target, indicating that Q4 volumes are expected to remain consistent despite ongoing business pruning.

𝐅𝐘𝟐𝟔 𝐀𝐝𝐣𝐮𝐬𝐭𝐞𝐝 𝐄𝐁𝐈𝐓𝐃𝐀 𝐌𝐚𝐫𝐠𝐢𝐧: -1% to 1%

Accelerating probability of achievement. Year-to-date Adjusted EBITDA sits at roughly -€2.7M on €1.83B of sales (essentially a 0.0% margin). Given the structural improvements in SG&A demonstrated in Q3, the company is highly likely to finish the year safely within this confirmed guidance range.

𝐊𝐞𝐲 𝐐𝐮𝐞𝐬𝐭𝐢𝐨𝐧𝐬

𝐍𝐀𝐏/𝐌𝐑𝐏 𝐕𝐨𝐥𝐮𝐦𝐞 𝐑𝐞𝐜𝐨𝐯𝐞𝐫𝐲

The revenue decline for NAP/MRP widened back to 11.7% in Q3 after narrowing in Q2. When do you expect the new buying strategies and merchandise deliveries to finally return this segment to top-line growth?

𝐁𝐫𝐢𝐝𝐠𝐞 𝐟𝐫𝐨𝐦 𝐄𝐁𝐈𝐓𝐃𝐀 𝐭𝐨 𝐍𝐞𝐭 𝐈𝐧𝐜𝐨𝐦𝐞

With Depreciation & Amortization accelerating to nearly €19M this quarter, what is the expected normalized run-rate for D&A post-integration, and when do you expect to achieve positive GAAP Net Income?

𝐆𝐞𝐨𝐩𝐨𝐥𝐢𝐭𝐢𝐜𝐚𝐥 𝐈𝐦𝐩𝐚𝐜𝐭

You cited geopolitical headwinds in March affecting sales. Have these headwinds persisted into April and May, and are they concentrated in specific regions like Europe or the Middle East?

2

6,903

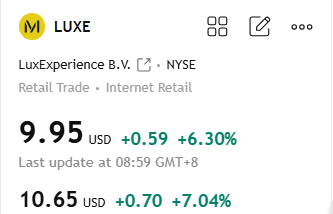

$LUXE

Company: Global luxury group, e-commerce, retail via YNAP.

Strengths: E-com scale, unique experiences, sales growth 5.7%.

Recent News: Q2 sales €647M (tripled), EBITDA positive.

Rise Today: 7.04% to $10.65 on JPM upgrade, Q2 optimism.

170

1

3

229

Feb 10

$LUXE executing

that YNAP deal looking more & more like one of the best M&A trades I’ve seen in recent years

1

5

2,289

Feb 10

$LUXE Q2 2026 earnings: Transformation Takes Hold: Profitability Returns

LuxExperience (formerly Mytheresa) delivered a pivotal quarter, validating its acquisition of YNAP. The Group returned to positive Adjusted EBITDA (€13.2M, 2.0% margin) significantly faster than many expected, driven by aggressive cost discipline and the superior performance of the legacy Mytheresa segment. While the Mytheresa brand continues to outshine with 8.8% sales growth and 9.3% margins, the acquired NAP/MRP and YOOX segments showed dramatic sequential improvements, narrowing losses substantially. The strategic sale of THE OUTNET for $30M further streamlines the portfolio.

Full article with charts finsee.ai/earnings/luxe/2026…

4

5,948

$LUXE 🇩🇪 Luxury online retail sector has been decimated last few years, with plenty of bankruptcies and consolidation.

After the merger of Mytheresa and YNAP = $LUXE is the leading survivor. With Mytheresa leadership in the helm as the last decades best performers in the industry.

Mcap €850m, €460m cash (part of the merger deal), management estimates €440m cash balance end of FY2026, so some cash burning def still ahead.

No debt, 150m leases, €1b inventory. So could very roughly estimate EV around €500-600m.

Consensus estimate FY2026 revenue €2,5B. Gross margins around 45% = €1,1b Gross profit. So EV < 0,5 x gross profit.

Company targeting 10-15% growth, 8% EBITDA margins.

If they can figure out even slight profitability in this historically notoriously difficult and competed industry, $LUXE could be very cheap.

No simple certainties here. But market may be underpricing the opportunity as luxury generally still out of favour and the whole sector, especially online side, is going through major turbulence.

6

28

3,918

Jan 7

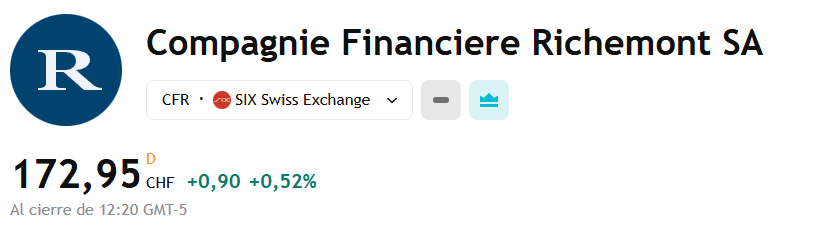

Bernsteinは、2026年のラグジュアリーグッズセクターにおいてRichemontを最優先銘柄として強調。具体的には、他の製品群と比較して宝飾の勢いが継続的に強いこと、CartierやVCAといったブランドにおける主導的な地位、後継者準備が整った組織、そしてYNAPの事業売却後の資本配分規律の改善である。

1

2

18

2,995

💎 Bernstein elige a Richemont $CFR como su principal apuesta en lujo para 2026

📅 Fecha: 5 de enero de 2026

📰 Fuente: Bernstein Research

Bernstein ha señalado a Richemont como su top pick en el sector lujo para 2026, en un contexto de recuperación gradual del sector y mayor selectividad por parte de los inversores.

📈 Perspectiva sectorial 2026

Bernstein proyecta un crecimiento del sector lujo de alrededor del 5% a tipo de cambio constante, con una recuperación en forma de U —especialmente en China— y no un rebote rápido en V. Aunque se observaron señales de mejora en el verano de 2025, la firma espera una normalización progresiva de la demanda.

🔄 Rotación dentro del sector

La casa de análisis anticipa una rotación intrasegmento: salida de valores “self-help” hacia nombres de mayor calidad, a medida que los inversores ganen confianza en las perspectivas de 2026. En este contexto, Bernstein mantiene recomendación Outperform para Hermès, Richemont y LVMH.

💍 Por qué Richemont

Bernstein destaca varios catalizadores clave para Richemont:

Mayor tracción estructural en joyería frente a otras categorías.

Liderazgo de marcas icónicas como Cartier y Van Cleef & Arpels.

Organización preparada para la sucesión directiva.

Mejora en la disciplina de asignación de capital, tras la desinversión de YNAP.

🧵 Otras preferencias y estrategias

Visión positiva también sobre Brunello Cucinelli en el segmento de alta calidad.

Estrategia sugerida: “Short Kering / Long Prada” de cara a 2026.

Burberry aparece como una opción atractiva en Europa para inversores que buscan historias de reestructuración (“self-help”).

⚠️ Nota sobre Hermès

En paralelo, Hermès ha sufrido recientes rebajas de recomendación por parte de Barclays y Morgan Stanley, que citan falta de catalizadores a corto plazo y expectativas de crecimiento más moderadas a medio plazo, además de cambios relevantes en su dirección creativa masculina.

🔍 Conclusión

Bernstein apuesta por un lujo más selectivo en 2026, donde la calidad, el poder de marca y la disciplina financiera serán claves. En ese escenario, Richemont destaca como el mejor posicionamiento riesgo-retorno dentro del sector.

2

620

5 Dec 2025

I'm truly amazed that in less than 2 hours Opus 4.5 completely refactored by YNAP backend dashboard from custom nextjs to laravel, filament, & fly io

This makes perhaps my 10th or 11th project I built this week

1

2

292

4 Dec 2025

🔴🟢🔵 #Yoox #Ynap, positiva conclusione della vertenza sui licenziamenti collettivi!

Filcams Cgil, Fisascat Cisl e Uiltucs accolgono con soddisfazione l’intesa raggiunta oggi al Mimit.

📉 L’accordo riduce gli esuberi salvaguardando 66 posti di lavoro tra Emilia-Romagna e Lombardia.

🤝 Per chi lascerà l’azienda, il criterio sarà solo la volontarietà: previsti un incentivo all’esodo e l’attivazione della cassa integrazione.

📋 Leggi il comunicato unitario

👉 fisascat.it/news/yoox-conclu…

6

10

246

19 Nov 2025

$LUXE Q1 FY26 earnings: Transformation in Progress

— • — • —

𝗧𝗵𝗲 𝗚𝗶𝘀𝘁

LuxExperience (formerly Mytheresa) reported a complex first quarter defined by a sharp divergence in performance. The core Mytheresa business is accelerating and profitable, effectively validating the management's strategy. However, the recently acquired YNAP assets (Net-A-Porter, YOOX) are shrinking rapidly as the company aggressively restructures them, leading to significant consolidated losses and cash burn. The company announced the sale of "The Outnet" to streamline operations.

🐂 𝗧𝗵𝗲 𝗕𝘂𝗹𝗹 𝗖𝗮𝘀𝗲

• 𝗖𝗼𝗿𝗲 𝗦𝘁𝗿𝗲𝗻𝗴𝘁𝗵: The Mytheresa segment is performing exceptionally well, with Net Sales up 𝟭𝟮.𝟮% and Adjusted EBITDA margins expanding to 𝟯.𝟱% (up from 1.4%).

• 𝗤𝘂𝗮𝗹𝗶𝘁𝘆 𝗥𝗲𝘃𝗲𝗻𝘂𝗲: Gross margins expanded across 𝗮𝗹𝗹 three segments (Group 190 bps), proving that the strategy to focus on full-price selling and reduce discounting is working, even if it hurts top-line volume at YNAP.

• 𝗧𝗼𝗽 𝗖𝘂𝘀𝘁𝗼𝗺𝗲𝗿𝘀: Spending by top clients increased significantly (Mytheresa 15%, NAP 4%), indicating high-end demand remains intact despite macro headwinds.

• 𝗚𝘂𝗶𝗱𝗮𝗻𝗰𝗲 𝗨𝗽𝗹𝗶𝗳𝘁: Despite lowering the GMV target due to the Outnet divestiture, the lower end of the Adjusted EBITDA margin guidance was raised (from -4% to -2%).

🐻 𝗧𝗵𝗲 𝗕𝗲𝗮𝗿 𝗖𝗮𝘀𝗲

• 𝗖𝗮𝘀𝗵 𝗕𝘂𝗿𝗻: The company burned through significant liquidity this quarter. Cash and equivalents dropped from €𝟲𝟬𝟯.𝟲𝗠 in June to €𝟰𝟲𝟭.𝟭𝗠 in September (a ~€142M reduction).

• 𝗦𝗵𝗿𝗶𝗻𝗸𝗶𝗻𝗴 𝗔𝗰𝗾𝘂𝗶𝘀𝗶𝘁𝗶𝗼𝗻𝘀: The acquired segments are in deep decline. Net-A-Porter/Mr Porter sales fell 𝟭𝟬.𝟴% and YOOX plunged 𝟭𝟲.𝟲%.

• 𝗗𝗲𝗲𝗽 𝗟𝗼𝘀𝘀𝗲𝘀: On a consolidated basis, the group posted a Net Loss of €𝟵𝟴.𝟱𝗠 and negative Adjusted EBITDA of -€28.1M for the quarter.

• 𝗘𝘅𝗲𝗰𝘂𝘁𝗶𝗼𝗻 𝗥𝗶𝘀𝗸: The turnaround relies on fixing the bloated cost structure of NAP/YOOX before cash runs out. The segment EBITDA for NAP dropped to -€14.6M from a positive €3.9M in the prior year illustrative period.

⚖️ 𝗩𝗲𝗿𝗱𝗶𝗰𝘁

The Bull case is winning on strategy, but the Bear case screams caution on liquidity. Management is successfully applying the Mytheresa "playbook" (high margin, full-price focus) to the acquired assets, evidenced by the gross margin expansion. However, the financial cost of this transition is massive. While the core business is a jewel, the cash burn requires close monitoring. The improved margin guidance suggests management is confident in their cost-cutting measures.

— • — • —

𝗧𝗵𝗲𝗺𝗲𝘀, 𝗗𝗿𝗶𝘃𝗲𝗿𝘀, 𝗮𝗻𝗱 𝗖𝗼𝗻𝗰𝗲𝗿𝗻𝘀

🟢 𝗠𝘆𝘁𝗵𝗲𝗿𝗲𝘀𝗮 𝗮𝘀 𝘁𝗵𝗲 𝗟𝗶𝗳𝗲𝗯𝗼𝗮𝘁

The original Mytheresa business is not just stable; it is accelerating. Sales growth improved to 𝟭𝟮.𝟮% (vs 8.9% in FY25), and profitability more than doubled. This segment provides the cash flow and credibility needed to support the wider group restructuring.

🔴 𝗦𝘁𝗿𝗮𝘁𝗲𝗴𝗶𝗰 𝗦𝗵𝗿𝗶𝗻𝗸𝗮𝗴𝗲 𝗮𝘁 𝗬𝗡𝗔𝗣

Management is intentionally letting revenue fall at Net-A-Porter (NAP) and YOOX to improve health. By cutting unprofitable promotions, they drove Gross Margins up 𝟭𝟮𝟬 𝗯𝗽𝘀 at NAP and 𝟯𝟵𝟬 𝗯𝗽𝘀 at YOOX. While sales are down double-digits, this "shrink to grow" strategy is necessary to fix the unit economics.

🟡 𝗣𝗼𝗿𝘁𝗳𝗼𝗹𝗶𝗼 𝗖𝗹𝗲𝗮𝗻𝘂𝗽

The company announced the sale of "The Outnet" assets for $30M. This is classified as "discontinued operations." While the cash influx is modest, it simplifies the Off-Price division, allowing resources to focus solely on stabilizing YOOX and the luxury segments.

🔴 𝗖𝗮𝘀𝗵 𝗖𝗼𝗻𝘀𝘂𝗺𝗽𝘁𝗶𝗼𝗻 𝗪𝗮𝘁𝗰𝗵

The liquidity position tightened significantly. The drop of ~€142M in cash balances in a single quarter is steep, though partly due to seasonal inventory builds (Operating Cash Flow was -€147.7M). Management previously guided for €350M-€450M cash consumption for the full turnaround; they have used a large portion of that budget in Q1 alone.

— • — • —

𝗠𝗮𝗶𝗻 𝗙𝗶𝗻𝗮𝗻𝗰𝗶𝗮𝗹𝘀

• 𝗚𝗿𝗼𝘂𝗽 𝗚𝗠𝗩: €589.0M (🔴 -4.3% vs illustrative prior year)

• 𝗚𝗿𝗼𝘂𝗽 𝗡𝗲𝘁 𝗦𝗮𝗹𝗲𝘀: €557.2M (🔴 -4.2% vs illustrative prior year)

• 𝗚𝗿𝗼𝘂𝗽 𝗚𝗿𝗼𝘀𝘀 𝗠𝗮𝗿𝗴𝗶𝗻: 44.1% (🟢 190 bps year-over-year)

• 𝗔𝗱𝗷𝘂𝘀𝘁𝗲𝗱 𝗘𝗕𝗜𝗧𝗗𝗔: -€28.1M (Margin -5.0%)

• 𝗡𝗲𝘁 𝗟𝗼𝘀𝘀: -€98.5M

𝗦𝗲𝗴𝗺𝗲𝗻𝘁 𝗕𝗿𝗲𝗮𝗸𝗱𝗼𝘄𝗻:

• 𝗟𝘂𝘅𝘂𝗿𝘆 | 𝗠𝘆𝘁𝗵𝗲𝗿𝗲𝘀𝗮:

• GMV: €245.9M (🟢 13.5%)

• Adj. EBITDA: €7.9M (Margin 3.5%, up from 1.4%)

• 𝗟𝘂𝘅𝘂𝗿𝘆 | 𝗡𝗔𝗣 & 𝗠𝗥𝗣:

• GMV: €224.5M (🔴 -10.8%)

• Adj. EBITDA: -€14.6M (Margin -6.9%, down from 1.6%)

• 𝗢𝗳𝗳-𝗣𝗿𝗶𝗰𝗲 | 𝗬𝗢𝗢𝗫:

• GMV: €118.6M (🔴 -19.3%)

• Adj. EBITDA: -€21.4M (Margin -18.1%)

— • — • —

𝗚𝘂𝗶𝗱𝗮𝗻𝗰𝗲

Management updated its FY26 outlook, primarily to reflect the divestment of The Outnet.

• 𝗙𝗬𝟮𝟲 𝗚𝗠𝗩: €2.4 billion to €2.7 billion.

• 𝘊𝘰𝘯𝘵𝘦𝘹𝘵: Lowered from the previous range of €2.5B–€2.9B. This adjustment appears largely structural due to removing The Outnet from continuing operations.

• 𝗙𝗬𝟮𝟲 𝗔𝗱𝗷𝘂𝘀𝘁𝗲𝗱 𝗘𝗕𝗜𝗧𝗗𝗔 𝗠𝗮𝗿𝗴𝗶𝗻: -2% to 1%.

• 𝘊𝘰𝘯𝘵𝘦𝘹𝘵: This is an improvement at the lower end compared to the previous guidance of -4% to 1%. It signals that despite lower expected GMV, cost controls and margin improvements are potentially ahead of schedule.

— • — • —

𝗠𝗮𝗶𝗻 𝗤𝘂𝗲𝘀𝘁𝗶𝗼𝗻𝘀 𝗳𝗼𝗿 𝘁𝗵𝗲 𝗘𝗮𝗿𝗻𝗶𝗻𝗴𝘀 𝗖𝗮𝗹𝗹

1. 𝗖𝗮𝘀𝗵 𝗕𝘂𝗿𝗻 𝗖𝗮𝗱𝗲𝗻𝗰𝗲: With ~€142M cash consumed in Q1, how should investors model cash flow for the remainder of FY26? Is the bulk of the "turnaround spend" now behind us, or is this the quarterly run rate?

2. 𝗡𝗔𝗣 𝗦𝘁𝗮𝗯𝗶𝗹𝗶𝘇𝗮𝘁𝗶𝗼𝗻: While gross margins improved, NAP EBITDA collapsed to -€14.6M. When does management expect the cost-cutting measures to cross over with the sales decline to return this segment to breakeven EBITDA?

3. 𝗧𝗵𝗲 𝗢𝘂𝘁𝗻𝗲𝘁 𝗜𝗺𝗽𝗮𝗰𝘁: Can you quantify exactly how much of the GMV guidance reduction is solely due to The Outnet sale versus organic trends in the remaining business?

4. 𝗨𝗦 𝗠𝗮𝗿𝗸𝗲𝘁 𝗧𝗿𝗲𝗻𝗱𝘀: The US now represents 31.6% of sales. Given the discussion of "prudent conservatism" regarding customs in the previous quarter, how did US demand trend intra-quarter, and are you seeing any shifts post-September?

2

787

19 Nov 2025

jajan #CFXXI ynap ──★ ˙🍫 ̟ !!

thanks to kak @nekomakucing as jastiper yg mau kurepotkan slalu ttg nitip cf 🫶🏼

1

1

6

269

14 Nov 2025

📈 Richemont $CFR

💰Resultados💰

🚀 Operaciones y estrategia de crecimiento

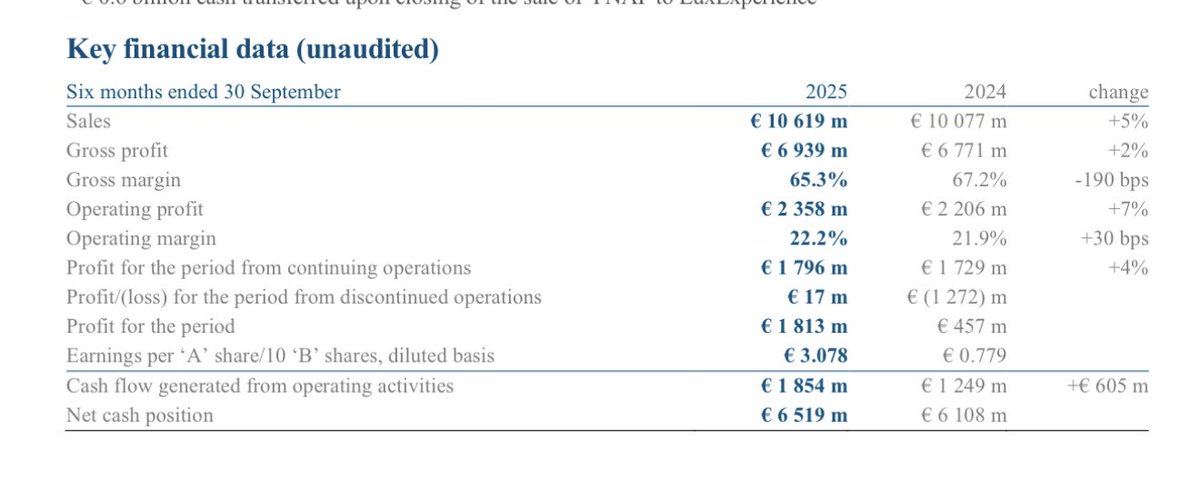

Fuerte aceleración en Q2 ( 14% CER) con doble dígito en todas las regiones; ventas DTC 76% del total y retail 70% (1.398 boutiques). Joyería (Cartier, Van Cleef & Arpels, Buccellati, Vhernier) crece 14% CER en H1 y 17% CER en Q2, apoyada por alta joyería y lanzamientos (p. ej., Flowerlace en VCA; campaña “Love Unlimited” en Cartier). Relojería especializada frena la caída y vuelve a crecer en Q2 ( 3% CER). Se completó la venta de YNAP (abril 2025).

3.💸 Análisis de costos y gastos

La bajada de margen bruto (−190 pb) obedece a FX adverso, oro más caro y, en menor medida, aranceles adicionales en EE. UU.; se mitigó con subidas de precio selectivas y disciplina de costos. Selling & Distribution 3% (25.7% de ventas vs 26.4%), Communication −4% (8.2% vs 9.0%) y Administración −2%: ello explica el apalancamiento que eleva el margen operativo a 22.2%.

4.📈 KPIs sectoriales

•Regiones H1 (reported / CER): Europa 10% / 11%, Américas 11% / 18%, MEA 13% / 19%, Asia Pacífico 0% / 5%, Japón −5% / −4%. En Q2, todas las regiones crecieron doble dígito CER.

•Canales H1 (mix): Retail 70% ( 6% reported / 10% CER), Online 6% ( 3% / 7%), Wholesale 24% ( 5% / 9%). DTC 76%.

5.💧 Liquidez y apalancamiento

Caja neta €6.5bn, caja bruta €12.5bn; CFO €1.85bn ( 48%). Capex neto €350m; inventarios €9.6bn (rotación 18.1 meses, mejor que 19.9m hace un año). Bonos corporativos €5.9bn; equity 54% del activo.

6.🧭 Narrativa estratégica (citas traducidas)

•Presidente, Johann Rupert: “El segundo trimestre fue particularmente fuerte, con doble dígito en todas las regiones, reflejando los múltiples motores de crecimiento del Grupo.”

•“Hemos enfrentado FX, oro y los nuevos aranceles en EE. UU.; con subidas de precio equilibradas y disciplina de costes aumentamos el beneficio operativo y mantenemos un balance sólido.”

7.🔮 Proyecciones y orientación

No hay guía cuantitativa. La compañía estima un impacto FY26 de ~€0.3bn por aranceles adicionales en EE. UU. (asumiendo tarifas actuales) y anticipa entorno incierto (China aún irregular), requiriendo agilidad y disciplina.

8.💰 Dividendo y retorno al accionista

Pago de dividendo ordinario 2025: CHF 3.00/acción (salida de caja €1,888m). Compra de 1.12m acciones ‘A’ para cubrir planes de ejecutivos (outflow neto €177m). Caja neta se mantiene sólida.

9.⚖️ Puntos positivos y negativos del semestre

•Positivos: (i) Q2 fuerte ( 14% CER), (ii) Joyería en máxima forma ( 14% CER H1, margen 32.8%), (iii) apalancamiento operativo (opex/ventas −220 pb), (iv) caja neta €6.5bn y CFO 48%, (v) DTC 76% sostiene control de marca y precios.

•Negativos / riesgos: (i) Margen bruto −190 pb por FX/oro/aranceles; (ii) Relojería con margen 3.2% y Asia Pac. aún débil, (iii) aranceles EE. UU. (~€0.3bn FY), (iv) China/Japón con comparativas exigentes.

10.🎯 Opinión / calificación del desempeño

Semestre sólido: ventas y OP crecen pese a vientos en contra; Joyería compensa la debilidad de Relojes. La calidad del P&L (apalancamiento y caja) es clara; la clave a 2H será gestión de FX, oro y aranceles mientras se normaliza Asia. ¿Cumplió vs consenso? La verdad es que no sé. Puntaje: 8.4/10.

11.📝 Resumen conciso y puntos clave

Richemont reportó ventas €10.6bn ( 5%; 10% CER), margen OP 22.2% ( 30 pb) y beneficio €1.81bn, con Q2 acelerando a 14% CER; Joyería lidera ( 14% CER, margen 32.8%), Relojes mejoran en Q2 pero aún presionados; DTC 76% y CFO €1.85bn refuerzan el balance (caja neta €6.5bn). El entorno (FX, oro, aranceles) pesa en el margen bruto, pero la disciplina de costos y el mix sostienen la rentabilidad.

12.🔔 Cierre

No olvides seguirme en mi cuenta X para mantenerte al tanto de los mercados financieros 👉 x.com/IngJuanPa7

3

4,145

14 Nov 2025

Out on SENS ⌚ | CFR |

• Richemont (CFR) H1 25 group sales rose 10% (constant FX) to €10.6 bn, as all regions recorded double-digit Q2 growth.

• HEPS up 5% in euro terms to €3.01, vs Bloomberg estimates of €2.92.

• Operating profit rose 7% to €2.36 bn ( 24% in constant currency) with margins up 30bps to 22.2%.

• Jewellery Maisons sales gained 14% (constant FX) with a 32.8% operating margin.

• Specialist Watchmakers returned to growth in Q2.

• Profit surged to €1.81 bn from €457m a year ago, aided by the completion of the YNAP sale & discontinued losses.

• Net cash position of €6.5bn, for brand development and selective expansion.

senspdf.jse.co.za/documents/…

1

4

754

13 Nov 2025

👏 Big step for animal-free fashion! LuxExperience B.V, parent company of @mytheresa_com & YNAP, has adopted its first Animal Welfare Policy, banning fur, angora & exotic skins (incl. kangaroo).

Proud of our member @LAV_Italia for driving this change.

bit.ly/4p9vKlm

5

10

237