Take your training international with IACIS!

Join us in Budapest for our BCFE course and train alongside professionals from around the world!

📅 October 12-23, 2026

📍 Verdi Budapest Aquincum | Budapest, Hungary

🔗 Learn more: iacis.com/events/in-person/b…

2

⎐كُـود⎐كوبِون⎐خـِصم⎐

⎐ايهرب⎐ايهيرب اهرب

⊵GCA5893⊴

⎐نون⎐

⊵S3Q⊴

⎐نمشي⎐

⊵AABN⊴

⎐باث▬اند▬بودي⎐

AB6K⊴

⎐ناتشورال ⊴تاتش⎐

⊵C37⊴

⎐فوغا⎐كلوسـيت⎐

⊵V1⊴

⊴ماكـس ⊴

⊵A9B⊴

___

BCfe

Our team had an incredible time getting to see graduate work from the Animation, Film & Game Design students at this year’s BCFE Grad Showcase. Congratulations to all of the artists on their great work 👏

3

219

Our team checked out the BCFE Graduate Exhibition this month, and had a great time viewing animation, illustration and graphic design work from this year’s grads. Some impressive work on display!

4

233

May 15

الصدمة الحقيقية ان كل دول معملوش breast cancer screening قبل كده؟

يا خسارة حملات التوعية ومؤتمر بهية واكتوبر الوردي وال BCFE

May 14

دكتورة العلاج الطبيعي وهي بتنزل strap التوب/البرا من على كتفي قبل كل جلسة

(This is literally how it feels)

2

1

44

8,052

IACIS Podcast host Farand C. Wasiak speaks with BCFE Row Coach Evangelos Dragonas from Greece during the IACIS 2026 Orlando Training Event.

Take a look at their chat here👉 youtu.be/HZcZHLzYb0s

3

69

🚨 NEW COURSE ALERT🚨

Waz speaks with BCFE Row Coach Bruce Ellis about a new upcoming IACIS course!

Take a look now 👉 youtu.be/201GwVlfxNo?si=SriY…

Don't forget to like and subscribe! ✅

3

81

IACIS Podcast host Farand C. Wasiak follows up with BCFE Student Ashley Florent during the IACIS 2026 Orlando Training Event.

Take a look at what Ashley had to say about her time here 👉 youtu.be/vS3cAeDGZ34

2

79

IACIS Podcast host Farand C. Wasiak speaks with BCFE Row Coach Heidar Gudnason during the IACIS 2026 Orlando Training Event.

Here’s their interview now 👉 youtu.be/UXm4Z-ly--I

4

64

May 5

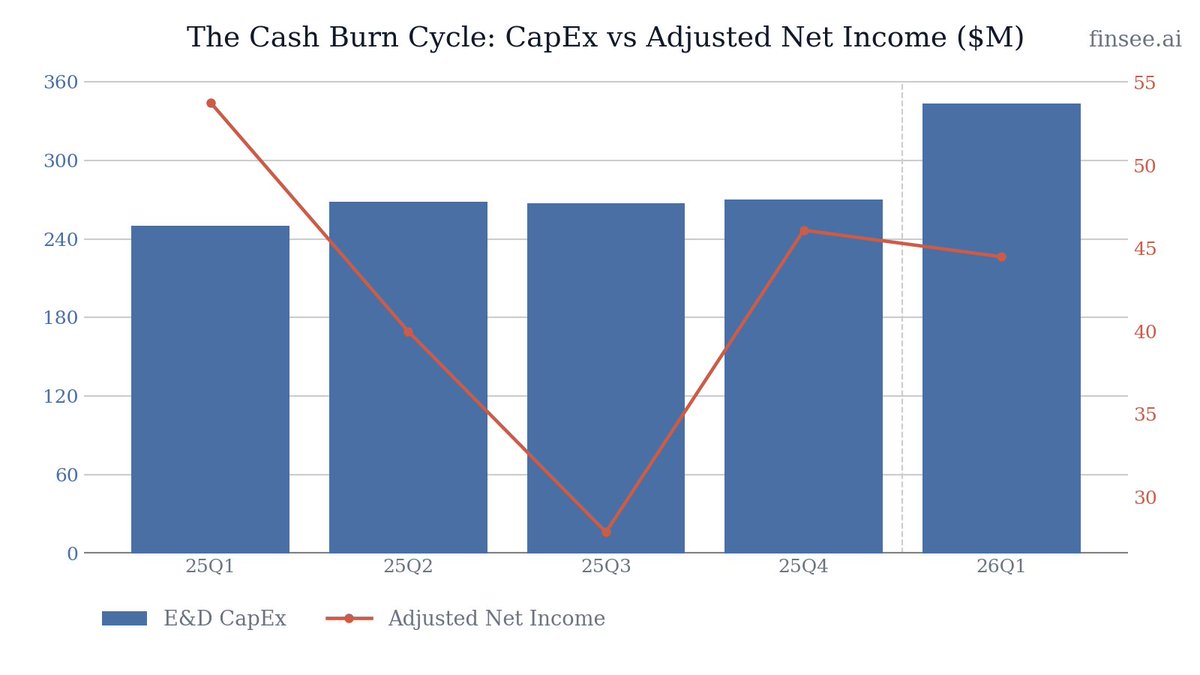

$CRK Q1 2026 earnings: Massive Cash Burn to Fund the Future

Comstock's Q1 results reveal a company caught between two realities: a bold future vision and a painful present. Management is betting the farm on the Western Haynesville, hyping its potential to feed AI data centers and LNG exports. But the cost of this pivot is staggering. Exploration and Development (E&D) CapEx accelerated 37% YoY to $343 million, driving Free Cash Flow into a severe $206 million deficit. Worse, while spending surged, total production is decelerating sharply, down 15% YoY. The company is bleeding cash to prove out its 'company-making' asset, testing the patience of investors waiting for volume growth.

Full article with charts - link in bio

🐂 𝐁𝐮𝐥𝐥 𝐂𝐚𝐬𝐞

• 𝐖𝐞𝐬𝐭𝐞𝐫𝐧 𝐇𝐚𝐲𝐧𝐞𝐬𝐯𝐢𝐥𝐥𝐞 𝐏𝐫𝐨𝐯𝐢𝐧𝐠 𝐎𝐮𝐭 — The company turned six Western Haynesville wells to sales with an impressive average initial production (IP) rate of 29 MMcf per day. The geology works, and the resource is massive.

• 𝐔𝐧𝐡𝐞𝐝𝐠𝐞𝐝 𝐏𝐫𝐢𝐜𝐞 𝐑𝐞𝐚𝐥𝐢𝐳𝐚𝐭𝐢𝐨𝐧𝐬 — Unhedged natural gas prices improved significantly, reaching $4.27 per Mcf in Q1 vs $3.58 a year ago, supporting unhedged operating margins of 78%.

🐻 𝐁𝐞𝐚𝐫 𝐂𝐚𝐬𝐞

• 𝐏𝐫𝐨𝐝𝐮𝐜𝐭𝐢𝐨𝐧 𝐢𝐬 𝐒𝐡𝐫𝐢𝐧𝐤𝐢𝐧𝐠 — Despite a massive capital injection, total production dropped 15% YoY to 97.9 Bcfe. The shift from Legacy Haynesville to Western Haynesville is creating a near-term volume vacuum.

• 𝐒𝐞𝐯𝐞𝐫𝐞 𝐂𝐚𝐬𝐡 𝐃𝐞𝐟𝐢𝐜𝐢𝐭𝐬 — A Free Cash Flow deficit of over $206 million in a single quarter is unsustainable long-term. Elevated drilling costs in the deep, high-pressure Western Haynesville are crushing near-term returns.

⚖️ 𝐕𝐞𝐫𝐝𝐢𝐜𝐭: 🔴

Bearish. The long-term macro story for natural gas is compelling, but Comstock's execution relies on burning massive amounts of cash today to secure production tomorrow. Until the Western Haynesville capital efficiency improves, this is a 'show me' story.

𝐊𝐞𝐲 𝐓𝐡𝐞𝐦𝐞𝐬

🔴 𝐏𝐫𝐨𝐝𝐮𝐜𝐭𝐢𝐨𝐧 𝐃𝐞𝐜𝐥𝐢𝐧𝐞 𝐀𝐜𝐜𝐞𝐥𝐞𝐫𝐚𝐭𝐢𝐧𝐠 [NEW]

Total production fell for the fifth consecutive quarter, dropping to 97.9 Bcfe (down 15% YoY). This validates concerns that pivoting capital away from the predictable, high-return Legacy Haynesville to derisk the Western Haynesville is suffocating near-term volume. Management claims they can reverse this with an aggressive 9-rig program, but current data shows an accelerating decline.

🔴 𝐔𝐧𝐢𝐭 𝐂𝐨𝐬𝐭𝐬 𝐂𝐫𝐞𝐞𝐩𝐢𝐧𝐠 𝐇𝐢𝐠𝐡𝐞𝐫

As production volumes drop, unit costs are naturally inflating. Total production costs per Mcfe increased from $0.83 in 25Q1 to $0.93 in 26Q1. This includes a notable jump in Gathering & Transportation (up to $0.43 from $0.37) and Cash G&A. If natural gas prices soften, this elevated cost structure will compress margins significantly.

🟢 𝐖𝐞𝐬𝐭𝐞𝐫𝐧 𝐇𝐚𝐲𝐧𝐞𝐬𝐯𝐢𝐥𝐥𝐞 𝐃𝐫𝐢𝐥𝐥𝐢𝐧𝐠 𝐄𝐱𝐞𝐜𝐮𝐭𝐢𝐨𝐧

Comstock continues to technically de-risk its 535,000 net acre Western Haynesville position. The company successfully turned 6 new wells to sales in Q1 with lateral lengths averaging 10,874 feet and IP rates of 29 MMcf/d. Key highlights include the Kiker BK #1 (35 MMcf/d) and Bumpurs NMH #1 (32 MMcf/d), proving the rock can deliver high-rate wells.

🟢 𝐀𝐈 𝐃𝐚𝐭𝐚 𝐂𝐞𝐧𝐭𝐞𝐫𝐬 & 𝐌𝐚𝐜𝐫𝐨 𝐓𝐚𝐢𝐥𝐰𝐢𝐧𝐝𝐬

Management continues to position the company as a prime beneficiary of structural demand shifts. The joint venture with NextEra Energy aims to develop 'behind-the-meter' gas-fired power generation for data centers. Comstock's acreage sits 100 miles from Dallas and Houston, offering a geographic advantage for power-hungry hyperscalers and Gulf Coast LNG export terminals.

𝐎𝐭𝐡𝐞𝐫 𝐊𝐏𝐈𝐬

𝐅𝐫𝐞𝐞 𝐂𝐚𝐬𝐡 𝐅𝐥𝐨𝐰 𝐃𝐞𝐟𝐢𝐜𝐢𝐭 (𝟐𝟔𝐐𝟏): -$206.1 million

Decelerating violently. This is a massive expansion of the cash burn from practically breakeven (-$22K) in 25Q1. It reveals the heavy toll of ramping up rig counts in the deeper, more expensive Western Haynesville while current production drops.

𝐍𝐚𝐭𝐮𝐫𝐚𝐥 𝐆𝐚𝐬 𝐏𝐫𝐢𝐜𝐞 𝐑𝐞𝐚𝐥𝐢𝐳𝐚𝐭𝐢𝐨𝐧 (𝐔𝐧𝐡𝐞𝐝𝐠𝐞𝐝): $4.27 per Mcf

Accelerating. Unhedged gas prices surged compared to $3.58 in 25Q1. However, heavy hedging limited the actual realized price to $3.45 per Mcf, causing the company to recognize $80.4 million in realized hedging losses for the quarter.

𝐆𝐮𝐢𝐝𝐚𝐧𝐜𝐞

𝐅𝐘𝟐𝟔 𝐄&𝐃 𝐂𝐚𝐩𝐢𝐭𝐚𝐥 𝐄𝐱𝐩𝐞𝐧𝐝𝐢𝐭𝐮𝐫𝐞𝐬: $1.4 - $1.5 billion

Accelerating. Set during the 25Q4 call, this implies an average quarterly spend of $350-$375M. Q1 came in at $343M, meaning capital intensity will remain extremely high throughout the year as the company operates 9 rigs.

𝐅𝐘𝟐𝟔 𝐌𝐢𝐝𝐬𝐭𝐫𝐞𝐚𝐦 𝐂𝐚𝐩𝐢𝐭𝐚𝐥 𝐄𝐱𝐩𝐞𝐧𝐝𝐢𝐭𝐮𝐫𝐞𝐬: $100 - $150 million

Stable. The Western Haynesville buildout requires heavy infrastructure investment. Comstock plans to spend aggressively here, though management has previously discussed recapitalizing the Pinnacle midstream unit to make it self-funding.

𝐊𝐞𝐲 𝐐𝐮𝐞𝐬𝐭𝐢𝐨𝐧𝐬

𝐅𝐮𝐧𝐝𝐢𝐧𝐠 𝐭𝐡𝐞 𝐂𝐚𝐬𝐡 𝐃𝐞𝐟𝐢𝐜𝐢𝐭

With a Q1 Free Cash Flow deficit of over $200 million and E&D guidance implying similarly heavy spending for the rest of the year, how much more will you draw on the credit facility, and at what leverage ratio do you hit the brakes?

𝐏𝐫𝐨𝐝𝐮𝐜𝐭𝐢𝐨𝐧 𝐁𝐨𝐭𝐭𝐨𝐦

Production dropped 15% YoY this quarter. At what point in 2026 do you expect the turn-in-line cadence of the 9-rig program to finally reverse the production decline and return the company to sequential volume growth?

𝐏𝐢𝐧𝐧𝐚𝐜𝐥𝐞 𝐌𝐢𝐝𝐬𝐭𝐫𝐞𝐚𝐦 𝐑𝐞𝐜𝐚𝐩𝐢𝐭𝐚𝐥𝐢𝐳𝐚𝐭𝐢𝐨𝐧

You previously mentioned plans to recapitalize your midstream subsidiary by selling common equity to redeem preferred equity. What is the status of that transaction, and how critical is it to funding the Western Haynesville buildout?

9

1,204

May 3

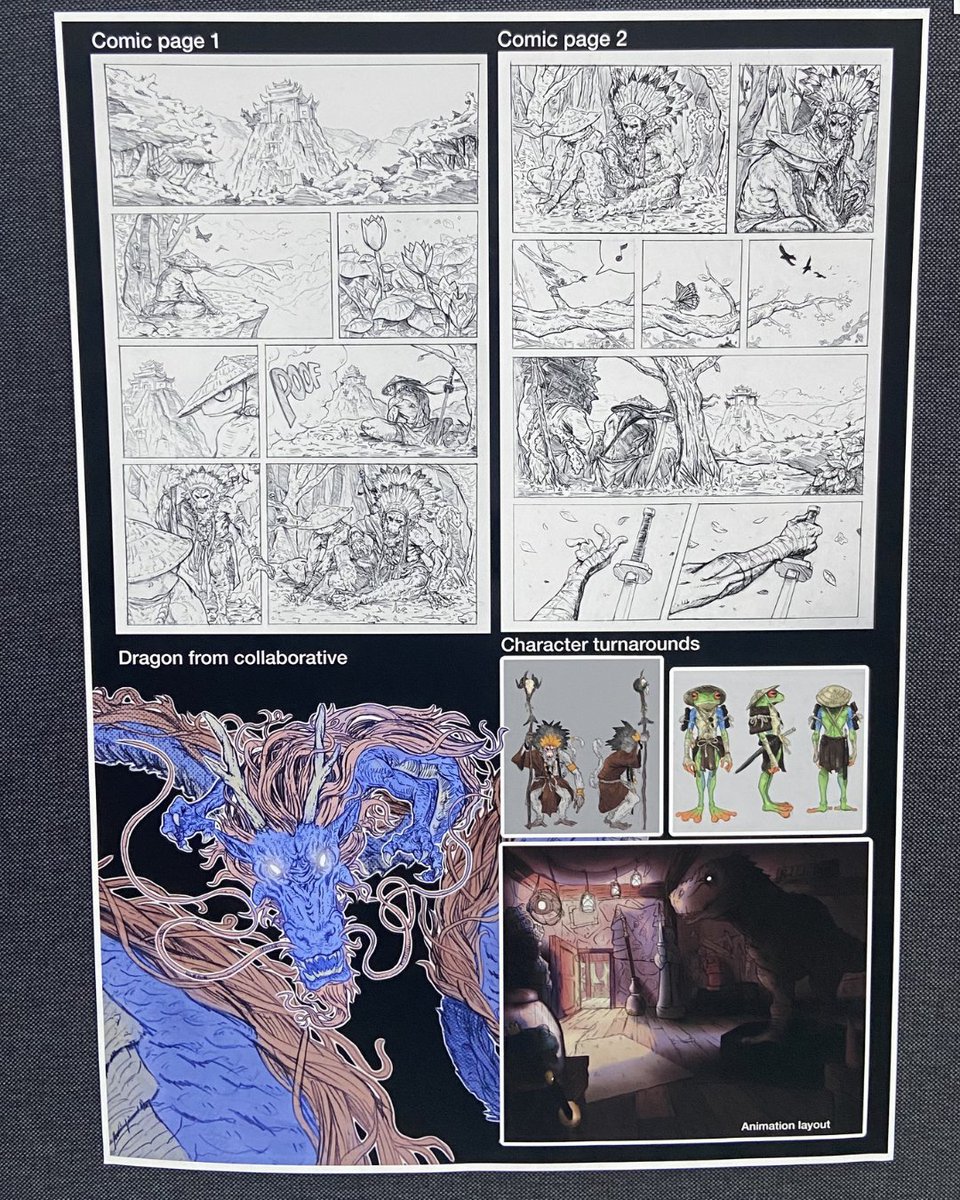

Classical and Computer Animation at BCFE. Good luck with getting into your course anon!

1

10

722

Waz has a great talk with Kazeem Akano from Nigeria!

He is a new BCFE Coach this year and we’re excited to have him!

Take a look at their chat now 👉 youtu.be/BZr--OBoNAY

2

89

Waz took a moment to chat with BCFE Row Coach, Dima Abdejaber to check in on her experience thus far!

Check it out here 👉 youtu.be/fTbRmFJfsZI

2

77

Apr 29

$AR Q1 2026 earnings: Record Production and Massive Cash Flow Mask a Heavily Leveraged Balance Sheet

Antero Resources delivered a blowout quarter driven by the closing of its transformative HG Energy acquisition. Production surged to a record 3.85 Bcfe/d, driving Adjusted Free Cash Flow up 179% YoY to $657 million. The company capitalized on winter weather and strong export markets to achieve a $0.53/Mcf premium on natural gas. However, while top-line results and management's tone are highly optimistic, the HG acquisition came at a steep cost: Net Debt ballooned by $1.5 billion to $2.66 billion. Furthermore, despite overall pricing strength, C3 NGL prices dropped 17% YoY. The investment thesis now hinges on management's ability to seamlessly integrate HG Energy, deliver the promised 15% sequential drop in cash costs, and aggressively pay down debt before commodity tailwinds fade.

Full article with charts - link in bio

🐂 𝗕𝘂𝗹𝗹 𝗖𝗮𝘀𝗲

𝗛𝗚 𝗔𝗰𝗾𝘂𝗶𝘀𝗶𝘁𝗶𝗼𝗻 𝗜𝗻𝘀𝘁𝗮𝗻𝘁𝗹𝘆 𝗔𝗰𝗰𝗿𝗲𝘁𝗶𝘃𝗲: The HG acquisition is projected to drive Q2 production to 4.1 Bcfe/d while structurally lowering cash costs by 15%. This creates a highly profitable, scaled platform.

𝗣𝗿𝗲𝗺𝗶𝘂𝗺 𝗣𝗿𝗶𝗰𝗶𝗻𝗴 𝗘𝘅𝗲𝗰𝘂𝘁𝗶𝗼𝗻: Antero continues to sidestep weak local basis pricing. Q1 natural gas realized a $0.53/Mcf premium to NYMEX, aided by firm transportation to LNG fairways.

🐻 𝗕𝗲𝗮𝗿 𝗖𝗮𝘀𝗲

𝗕𝗮𝗹𝗹𝗼𝗼𝗻𝗶𝗻𝗴 𝗡𝗲𝘁 𝗗𝗲𝗯𝘁: Net Debt more than doubled sequentially from $1.19B to $2.66B. While FCF is strong, the balance sheet is suddenly much more vulnerable to a commodity price shock.

𝗖𝟯 𝗡𝗚𝗟 𝗣𝗿𝗶𝗰𝗶𝗻𝗴 𝗪𝗲𝗮𝗸𝗻𝗲𝘀𝘀: Despite a bullish narrative on exports, realized C3 NGL prices fell 17% YoY. If international NGL arbs narrow, cash flow will face significant headwinds.

⚖️ 𝗩𝗲𝗿𝗱𝗶𝗰𝘁

🟢 Bullish. The scale of the free cash flow generation ($657M in a single quarter) provides a clear and rapid path to de-leveraging the HG acquisition debt, while structural cost reductions cement Antero's position as a low-cost leader.

— • — • —

𝗧𝗵𝗲𝗺𝗲𝘀

New: 🟢🟢 𝗛𝗚 𝗘𝗻𝗲𝗿𝗴𝘆 𝗔𝗰𝗾𝘂𝗶𝘀𝗶𝘁𝗶𝗼𝗻 𝗧𝘂𝗿𝗯𝗼𝗰𝗵𝗮𝗿𝗴𝗲𝘀 𝗦𝗰𝗮𝗹𝗲 𝗮𝗻𝗱 𝗘𝗳𝗳𝗶𝗰𝗶𝗲𝗻𝗰𝘆

The integration of the HG assets (closed early February) is the primary engine for the quarter's 13% YoY production growth. Moving forward, management expects this acquisition to add 700 MMcfe/d of annual net production, 385,000 net acres, and 400 drilling locations. More importantly, the integration of these lower-cost assets is guided to slash corporate cash production expenses.

New: 🟢 𝗥𝗲𝘃𝗲𝗿𝘀𝗶𝗻𝗴 𝗖𝗼𝘀𝘁 𝗧𝗿𝗮𝗷𝗲𝗰𝘁𝗼𝗿𝘆

In 26Q1, all-in cash expense temporarily rose to $2.64/Mcfe (up from $2.56/Mcfe a year ago), driven by higher fuel costs tied to higher natural gas prices. However, management expects this trend to aggressively reverse. Full integration of HG Energy in Q2 is guided to drive cash production expenses down 15% sequentially to $2.25-$2.35/Mcfe.

🟢 𝗚𝗹𝗼𝗯𝗮𝗹 𝗘𝘅𝗽𝗼𝗿𝘁 𝗘𝘅𝗽𝗼𝘀𝘂𝗿𝗲 𝗦𝗲𝗰𝘂𝗿𝗲𝘀 𝗣𝗿𝗲𝗺𝗶𝘂𝗺 𝗣𝗿𝗶𝗰𝗶𝗻𝗴

Antero's firm transportation to Gulf Coast LNG corridors continues to pay dividends. Natural gas pre-hedge realized price was $5.57/Mcf—a massive $0.53/Mcf premium to NYMEX. Additionally, ethane realized a $3.64/Bbl premium to index, prompting management to raise full-year ethane premium guidance by $1.00/Bbl at the midpoint.

New: 🔴 𝗡𝗲𝘁 𝗗𝗲𝗯𝘁 𝗕𝗮𝗹𝗹𝗼𝗼𝗻𝘀 𝗣𝗼𝘀𝘁-𝗔𝗰𝗾𝘂𝗶𝘀𝗶𝘁𝗶𝗼𝗻

The acquisition fundamentally altered the balance sheet risk profile. Net Debt surged from $1.19 billion at year-end 2025 to $2.66 billion at the end of 26Q1. While the rapid generation of $657M in Adjusted FCF suggests the company can quickly de-lever, Antero is currently carrying significantly more financial risk than in the prior year.

🔴 𝗖𝟯 𝗡𝗚𝗟 𝗣𝗿𝗶𝗰𝗶𝗻𝗴 𝗗𝗶𝘀𝗰𝗼𝗻𝗻𝗲𝗰𝘁

Despite management's positive macro comments on U.S. NGL exports and global supply constraints, realized C3 NGL prices actually fell 17% YoY to $37.83/Bbl (from $45.65/Bbl in 25Q1). This underperformance in a key liquids segment warrants close monitoring, as it contradicts the broader pricing strength seen in natural gas and ethane.

🟢 𝗢𝗽𝗲𝗿𝗮𝘁𝗶𝗼𝗻𝗮𝗹 𝗘𝘅𝗰𝗲𝗹𝗹𝗲𝗻𝗰𝗲 𝗶𝗻 𝗘𝘅𝘁𝗿𝗲𝗺𝗲 𝗖𝗼𝗻𝗱𝗶𝘁𝗶𝗼𝗻𝘀

Operations navigated Winter Storm Fern without shutting in any volumes, a rare feat that allowed Antero to capture premium pricing during peak demand. The company also set a record for drilling days per well (under 9 days, a 9% improvement vs 2025) and increased completion stages to 13.8 per day.

— • — • —

𝗢𝘁𝗵𝗲𝗿 𝗞𝗣𝗜𝘀

𝗔𝗱𝗷𝘂𝘀𝘁𝗲𝗱 𝗘𝗕𝗜𝗧𝗗𝗔𝗫 (𝟮𝟲𝗤𝟭): $𝟳𝟮𝟯 𝗺𝗶𝗹𝗹𝗶𝗼𝗻

Accelerating. Up 32% YoY from $549 million in 25Q1, driven by a 13% increase in production and a 39% increase in realized natural gas prices, easily offsetting the decline in NGL and oil prices.

𝗡𝗲𝘁 𝗖𝗮𝘀𝗵 𝗣𝗿𝗼𝘃𝗶𝗱𝗲𝗱 𝗯𝘆 𝗢𝗽𝗲𝗿𝗮𝘁𝗶𝗻𝗴 𝗔𝗰𝘁𝗶𝘃𝗶𝘁𝗶𝗲𝘀 (𝟮𝟲𝗤𝟭): $𝟴𝟱𝟵 𝗺𝗶𝗹𝗹𝗶𝗼𝗻

Accelerating. Surged 88% YoY from $458 million. The massive cash generation outpaced EBITDAX growth due to highly favorable working capital changes ($180 million tailwind in Q1).

𝗗𝗿𝗶𝗹𝗹𝗶𝗻𝗴 𝗮𝗻𝗱 𝗖𝗼𝗺𝗽𝗹𝗲𝘁𝗶𝗼𝗻 𝗖𝗮𝗽𝗘𝘅 (𝟮𝟲𝗤𝟭): $𝟮𝟮𝟯 𝗺𝗶𝗹𝗹𝗶𝗼𝗻

Stable. Only slightly up from 25Q1 levels, demonstrating strict capital discipline. Antero successfully onboarded a massive acquisition without letting base capital expenditures spiral out of control.

— • — • —

𝗚𝘂𝗶𝗱𝗮𝗻𝗰𝗲

𝗤𝟮 𝟮𝟬𝟮𝟲 𝗣𝗿𝗼𝗱𝘂𝗰𝘁𝗶𝗼𝗻: 𝟰.𝟭 𝗕𝗰𝗳𝗲/𝗱

Accelerating. Represents a 6% sequential increase from 26Q1, driven entirely by the first full quarter of integration of the newly acquired HG Energy assets.

𝗙𝗬𝟮𝟲 𝗖𝗮𝘀𝗵 𝗣𝗿𝗼𝗱𝘂𝗰𝘁𝗶𝗼𝗻 𝗘𝘅𝗽𝗲𝗻𝘀𝗲: $𝟮.𝟮𝟱 - $𝟮.𝟯𝟱 𝗽𝗲𝗿 𝗠𝗰𝗳𝗲

Reversing. Reduced from prior guidance of $2.35 - $2.45 per Mcfe. This implies a steep drop from the $2.64 per Mcfe incurred in 26Q1, resting heavily on realizing operational synergies from the HG assets.

𝗙𝗬𝟮𝟲 𝗘𝘁𝗵𝗮𝗻𝗲 𝗥𝗲𝗮𝗹𝗶𝘇𝗲𝗱 𝗣𝗿𝗶𝗰𝗲 𝗣𝗿𝗲𝗺𝗶𝘂𝗺 𝘃𝘀 𝗠𝗼𝗻𝘁 𝗕𝗲𝗹𝘃𝗶𝗲𝘂: $𝟮.𝟬𝟬 - $𝟯.𝟬𝟬 𝗽𝗲𝗿 𝗕𝗯𝗹

Accelerating. Increased by $1.00 at the midpoint from previous guidance, reflecting higher structural demand and successful marketing execution in the ethane segment.

— • — • —

𝗞𝗲𝘆 𝗤𝘂𝗲𝘀𝘁𝗶𝗼𝗻𝘀

𝗗𝗲𝗯𝘁 𝗥𝗲𝗱𝘂𝗰𝘁𝗶𝗼𝗻 𝘃𝘀. 𝗕𝘂𝘆𝗯𝗮𝗰𝗸𝘀

With Net Debt jumping to $2.66 billion post-HG acquisition, what is the precise cadence for debt paydown over the next 12 months, and at what leverage threshold will share repurchases be reintroduced to the capital allocation mix?

𝗖𝟯 𝗡𝗚𝗟 𝗣𝗿𝗶𝗰𝗶𝗻𝗴 𝗪𝗲𝗮𝗸𝗻𝗲𝘀𝘀

Realized C3 NGL prices dropped 17% YoY despite management's previous commentary on expanding export capacity and slowing domestic supply. What specific international or domestic headwinds drove this decline, and when do you expect the trend to reverse?

𝗛𝗚 𝗜𝗻𝘁𝗲𝗴𝗿𝗮𝘁𝗶𝗼𝗻 𝗘𝘅𝗲𝗰𝘂𝘁𝗶𝗼𝗻

Guidance implies a rapid 15% sequential drop in cash production expenses in Q2. Given the complexities of integrating 385,000 net acres, what are the primary operational risks that could delay or dilute these forecasted cost synergies?

1

2

507

IACIS Podcast host Farand C. Wasiak chats with BCFE Student Chris Scherr, a Special Agent with the Colorado Bureau of Investigation, during the IACIS 2026 Orlando Training Event.

Check out the interview here 👉 youtu.be/fg3pPU3giUI?si=m2D7…

2

94

Apr 28

$EXE | Expand Energy Q1 Earnings Highlights

Q1 Results (Beat on EPS, Revenue):

🔹 Earnings per Share (EPS): $3.83, $0.22 better than the Consensus of $3.61

🔹 Revenue: $4.40B ( 100.2% YoY), beating the $3.53B Consensus

2026 Capital and Operating Outlook:

🔹 Rigs: Operating 11 to 12 rigs

🔹 CapEx Investment: Estimated at $2.85B for 2026

🔹 Daily Production Target: Approx. 7.5 Bcfe/d

1

1

969