#IZMO: The Indian Company getting into Silicon Photonics packaging:

A GPU cluster is only as fast as the wires connecting it. And copper — the material every data center has been wired with for decades — is hitting a physical wall. Moving data between chips at the speeds AI demands causes heat, signal loss, and energy bleed that no engineering tweak can fully fix. It's a physics problem, not a software one.

The solution the entire semiconductor industry is converging on is silicon photonics — transmitting data using pulses of light instead of electrons. Wells Fargo estimates the total addressable market for photonics hits $10–12B by 2030. The CPO packaging market alone is expected to approach $5B by 2031

Now here's where IZMO comes in:

izmoMicro — IZMO's semiconductor subsidiary — is doing something extremely specific in this supply chain: advanced photonic IC packaging. A silicon photonics chip is incredibly delicate. You can't just solder it onto a board. It needs to be precisely aligned with optical fibers at sub-micron tolerances — we're talking accuracy smaller than 1/70th of the width of a human hair — bonded, thermally managed, and assembled into a module that can survive real-world operating conditions. This is called photonic packaging, and it is one of the hardest unsolved manufacturing challenges in the entire silicon photonics supply chain.

izmoMicro has built a facility in Bengaluru that does exactly this. Their specific achievement: a high-density silicon photonics packaging platform handling 32 fiber connections simultaneously with signal loss under 2 decibels. That's a very precise engineering benchmark, not a marketing claim. They are the official Photonic IC Packaging Partner for IIT Madras' CPPICS program — India's national silicon photonics mission funded by MeitY. Their R&D unit is DSIR-recognized by the Government of India. And crucially, the MD confirmed in the Q4 FY26 earnings call that in India, no other company has demonstrated capability across stack die, flip chip, and silicon photonics packaging at the same time.

They have also quietly entered defence electronics — high-frequency RF packaging, radar modules, airborne electronics — which is a second large addressable market running parallel to data centers.

The numbers behind the recent upper circuits:

Q4 FY26 consolidated revenue: ₹109 Cr — 82% YoY growth, highest quarterly revenue in company history. Net profit: ₹17.3 Cr, up 151% YoY. Management guided ₹50 Cr from izmoMicro alone in FY27, up from ₹18–19 Cr in FY26. Order book: ₹40 Cr. Visible pipeline: ₹100 Cr over the next 12–18 months. A Bengaluru semiconductor company with IIT Madras backing and real order flow posting its biggest quarter ever — the market noticed.

What about the rest of the business?

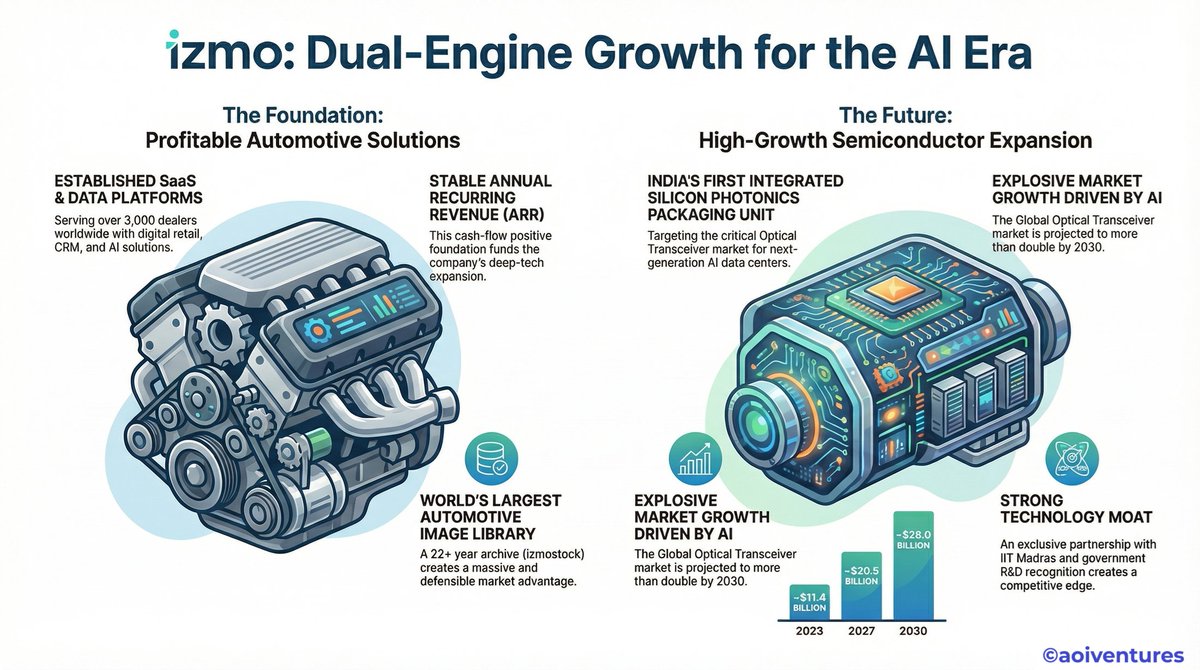

IZMO has been around since 1995 as an automotive software company — car dealer websites, CRM tools, and the world's largest library of automotive CGI images. These legacy divisions are in structural decline. AI is commoditizing website and CRM tooling, and AI image generation is an existential long-term threat to a business built around producing thousands of car images manually. The standalone India parent entity actually posted a loss in Q4. All the growth is in subsidiaries.

The one bright spot in the older business is FrogData — an AI analytics platform for US dealerships, growing at 50% annually. But even that is a sideshow to the photonics story now.

The honest framing: this is a profitable 30-year-old SaaS company whose original business is slowly dying, and it has been using that cash flow for nearly two decades to quietly fund a deep-tech semiconductor capability that India has never really had. The photonics timing — with the entire AI industry screaming for optical interconnect capacity — couldn't be better.

Why it's a watchlist, not a buy right no

⚠️ The valuation has run ahead of reality. Market cap is ₹1,500 Cr. izmoMicro's order book is ₹40 Cr. The stock is pricing in a future that hasn't been proven at scale yet.

⚠️ The ₹150–200 Cr capex raise to build the advanced packaging plant is still pending. Without it, they cannot fulfil the ₹100 Cr pipeline they're talking about. This raise also carries dilution risk.

⚠️ Large-scale CPO adoption is targeted industry-wide for 2028–2030. The big revenue wave may still be 2–3 years away.

⚠️ Zero mutual fund ownership. No institutional floor if sentiment turns.

⚠️ Micro-cap with thin float. Upper circuits happen fast. So do lower circuits.

The photonics packaging opportunity is real. The technology is real. The IIT Madras partnership and DSIR recognition are real. But the stock has already moved and is priced for a future that still needs to be executed.

The story is genuinely interesting. The entry point, right now, is not.

2

238

Jun 12

First- the business structure nobody explains properly!!

👉Izmo runs TWO completely different engines:

1. Digital (SaaS): izmocars izmostock FrogData AI

🔹3,000 auto dealers across 22 countries

🔹<3% annual churn on izmostock

🔹1,000 FrogData deployments in the US

2. Semiconductor: izmo Microsystems

🔹Advanced packaging, Silicon Photonics, Optical Transceivers

🔹Defence Space Export

👉The SaaS business is the cashflow engine that funds the semiconductor build. Capital discipline built into the DNA.

@nsinghal211 @OvindSingh_01 @sarang_contra @RamTeluguTrader @AmitWorldPeace

1

6

285

Jun 12

IZMO Ltd is getting a lot of traction recently, so I decided to share some thoughts.

The company operates across 4 divisions - 3 of which are basically SaaS while the 4th one is Izmo Microsystems

--> izmostock, izmoauto and frogdata are their legacy SaaS divisions selling stock images of cars, digital marketing for automotive clients and data analytics for automotive industry respectively.

While stock imagery and digital media divisions have historically anchored the business, they are facing long-term headwinds and are practically sunset businesses now in the generative AI era.

--> Izmo Microsystems represents the company’s high-margin, scalable, deep tech semiconductor ATMP division which is the primary catalyst for investor optimism

So far, they have demonstrated capabilities in advanced semiconductor packaging and silicon photonics (although the latter is not good enough for data center use case as of now but good for defence/aerospace purposes from where they are getting almost all their orders for now).

The bull case rests on the assumptions that eventually they will be able to tap into the massive $50-100 Billion global TAM but for now this seems like an overblown narrative to pump the stock price (promoters here have a history of overpromising and underdelivering in past as well).

Also, the semiconductor fabs in US/Taiwan/Korea are fairly advanced themselves and there is no logical reason for them to outsource such critical tech to Indian foundries in future. So, stating $100 Billion TAM seems to be an exaggerated guidance for a company whose yearly revenue today is barely ~$30 million with no huge orderbook to back the claims.

--> The reasonable bull case which I can see is them getting orders in coming years from ISRO and Indian defence-aerospace companies for specific components related to optics/lasers/semiconductors etc.

Izmomicro getting hyperscaler data center orders for critical bottleneck components seems very far-fetched as of now.

In future, there is a small possibility that data centres being built in India are told to indigenize the supply chain to some extent which could be a big future tailwind.

--> Regardless, the stock price currently is driven by future narrative rather than financials and the cheap 30x PE valuation also allows people to take some risk here.

I have a small tracking size of this company in my portfolio. Let's see how far they take it based on the narrative alone.

Ofc any new order updates would act as sharp triggers for the stock price going ahead.

1

1

13

1,167

FrogData is the most underrated piece.

Acquired via Geronimo in July 2024, it's an AI analytics platform for US car dealerships. Think: pricing intelligence, warranty boosters, fixed ops decision tools.

98.5% gross revenue retention. That number should stop you.

In Q4 FY26, they closed a partnership with Ford via FordDirect's The Shop marketplace. That's distribution into Ford's entire US dealer network.

FrogData didn't even exist in IZMO's portfolio 2 years ago.

1

6

1,805

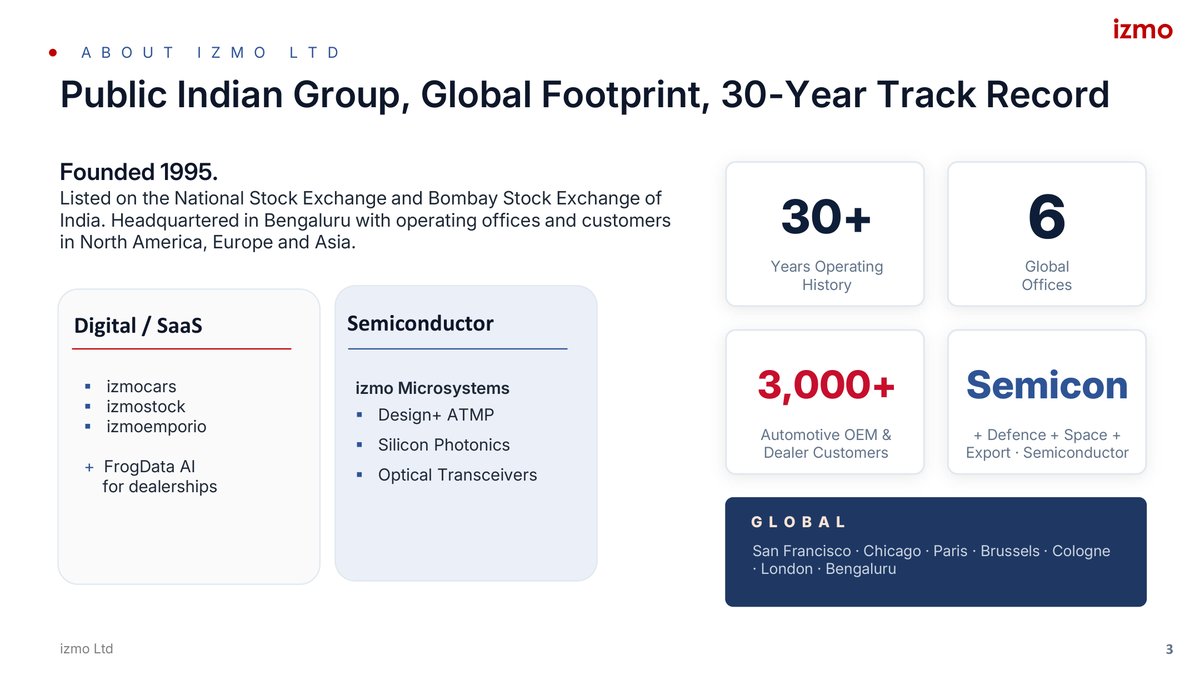

IZMO Ltd (NSE: IZMO | BSE: 532341) started in 1995 as an automotive digital retail platform.

Today it runs 4 completely different businesses:

→ izmoStock: world's largest auto imagery library

→ izmoAuto/izmocars: SaaS for 3,000 car dealers across 22 countries

→ FrogData: AI analytics for US dealerships

→ izmoMicro: semiconductor packaging in Bangalore

Yes, the last one is real. And it's where the story gets interesting.

1

2

15

2,805

Jun 10

🔍 IZMO Ltd: Leading India’s Silicon Photonics & Packaging Innovation | MCap 1,150.62 Cr

- izmo Ltd. operates in two main divisions: Digital/SaaS (cashflow engine) and Semiconductor (growth engine).

- Digital/SaaS includes izmocars, izmostock, izmoemporio, and FrogData AI with 3,000 dealers across 22 countries and 1,000 FrogData deployments.

- Semiconductor division (izmo Microsystems) focuses on Design ATMP, Advanced Packaging, Silicon Photonics, and Optical Transceivers with a 10 year delivery record in defence, space, and export.

- izmo Ltd. has a 30 year operating history and global presence with offices in San Francisco, Chicago, Paris, Brussels, Cologne, London, and Bengaluru.

- The company has strategic partnerships with IMEC, ISRO, Lionix International, and CPPICS/IIT Madras for Silicon Photonics.

- izmo Microsystems hosts India's first integrated Silicon Photonics packaging line, aiming for 50% faster time-to-market and 30-50% improved first-pass yield.

- Optical Transceivers business is positioned to benefit from India's datacenter boom with ~45% YoY growth.

- The AI infrastructure build-out is a key driver, with Advanced Packaging and Silicon Photonics markets estimated at $50B → $80B and $23B → $10B respectively by 2030.

- izmo's unique advantages include decade-long specialty packaging experience, ±0.1 µm alignment precision, and qualification by BEL, ISRO, and EU defence primes.

- The company is strategically aligned with India's semiconductor priorities through MEITY programmes and Make in India initiatives.

Disc: Information provided in this tweet can be inaccurate, verify through the source in reply before making any investment decision.

Preview 👇 (First 4 out of 25 pages)

3

8

46

3,351

Jun 10

IZMO Ltd has released its corporate presentation highlighting its dual business engines: Digital SaaS & Semiconductors. The Digital division, with 3,000 dealers & 1,000 FrogData AI deployments across 22 countries, serves as a stable cashflow engine. The Semiconductor division, izmo Microsystems, focuses on Design , ATMP, Silicon Photonics & Optical Transceivers, with an integrated SiPh line and adjacent optical transceiver expansion. The company plans to leverage its profitable SaaS business to fund semiconductor growth in a capital-efficient manner.

📊 IZMO LTD | 🏷️ General

🌐 Details: wegro.app/cY9ikg

⚡️Instant stock alerts on WhatsApp - Try FREE 👉 wegro.app/go

1

194

Jun 8

IZMO Ltd - Q4FY26 | Concall Insights

Financial Highlights

•Q4FY26 consolidated revenue grew 82.5% YoY and 84.7% QoQ to INR109.16 crores, highest quarterly revenue in company history

•FY26 consolidated revenue increased 26.8% YoY to INR284.88 crores

•FY26 consolidated net profit stood at INR47.56 crores, broadly stable YoY despite investment phase in izmoMicro

•Q4FY26 net profit came at INR17.3 crores with strong YoY improvement

•Growth driven by izmoMicro order execution, automotive software client additions and FrogData expansion

Revenue

•izmoMicro revenue expected at INR45-50 crores in FY27 versus ~INR18-19 crores in FY26

•Current izmoMicro order book stands at ~INR40-60 crores with additional INR100 crores opportunity pipeline

•Current order book execution timeline estimated at around 9 months

•Automotive Solutions business maintained strong OEM partnerships across global markets

•FrogData continued strong traction in U.S. dealership fixed operations and AI analytics market

Margins

•FY27 EBITDA margin guidance indicated at 20%-25% range

•Long-term blended EBITDA margin expected to exceed 30% with semiconductor scale-up

•Silicon photonics packaging EBITDA margins expected at 35% levels

•AI-driven software automation improving development efficiency and reducing costs

•Margin improvement expected as izmoMicro revenues scale while cost structure remains relatively fixed

Business Expansion

•IZMO operates across 22 countries serving automotive OEMs, dealers, AI infrastructure, defense and space sectors

•Geronimo acquisition continued adding OEM and dealer clients in Germany and Central Europe

•Ford partnership expanded through FordDirect’s The Shop marketplace across U.S. dealer network

•New Germany subsidiary established to drive European semiconductor expansion

•izmoMicro joined Silicon Saxony semiconductor cluster to strengthen European ecosystem access

Capex

•Company planning ~INR150 crores fund raise primarily for semiconductor expansion

•~INR125 crores capex planned towards packaging capacity expansion and technology infrastructure

•Expanded packaging facility expected operational by FY28 with revenue contribution from Q2/Q3 FY28

•Current packaging facility supports ~INR150 crores topline capacity

•Post expansion semiconductor packaging capacity can support ~INR1,200 crores topline potential

Strategy

•Company achieved breakthrough in 32-channel silicon photonics packaging with sub-2 decibel insertion loss

•IZMO positioned as India’s only player in silicon photonics packaging and advanced 3D packaging

•AI-first strategy implemented with internal LLM infrastructure powering software products

•Strategic collaboration established with IIT Madras under MeitY silicon photonics initiative

•Partnerships with Alcyon Photonics and CCRAFT strengthening end-to-end semiconductor packaging ecosystem

Semiconductor Business

•Strong demand visibility from AI hyperscalers, telecom, defense, space and automotive sectors

•Defense electronics emerged as largest opportunity segment for izmoMicro

•Several global customers shifting advanced packaging work from overseas to India

•Silicon photonics market opportunity estimated at ~$30 billion globally with rapid growth outlook

•Packaging economics highly attractive with silicon photonics packaging contributing up to 80% of chip value

Other Key Updates

•Company selected as photonic IC packaging partner for MeitY-supported IIT Madras initiative

•Defense supply contracts transitioned from design phase to recurring revenue streams

•Government semiconductor incentives under ISM 1 and ISM 2 schemes expected to support growth

•AI infrastructure demand and hyperscaler data center investments creating strong photonics demand

•Quantum packaging collaboration underway with IIT ecosystem for future deep-tech opportunities

4

502

Jun 8

IZMO Limited announced record-breaking Q4 FY26 financial results, with consolidated revenue reaching ₹109.16 Cr, an 82.5% year-on-year (YoY) & 84.7% quarter-on-quarter (QoQ) increase. Net profit for the quarter was ₹17.3 Cr. For the full year FY26, consolidated revenue stood at ₹284.88 Cr, a 26.8% YoY growth. 📈

Key highlights from the earnings call:

𝗕𝘂𝘀𝗶𝗻𝗲𝘀𝘀 𝗣𝗲𝗿𝗳𝗼𝗿𝗺𝗮𝗻𝗰𝗲 & 𝗘𝘅𝗽𝗮𝗻𝘀𝗶𝗼𝗻:

- 𝗢𝘃𝗲𝗿𝗮𝗹𝗹 𝗚𝗿𝗼𝘄𝘁𝗵: FY26 was a year of 'landmark achievements' with global footprint expansion in automotive technology & deepened AI capabilities.

- 𝗶𝘇𝗺𝗼𝘀𝘁𝗼𝗰𝗸: Redesigned portal gained traction, enhancing user experience & opening new customer segments.

- 𝗶𝘇𝗺𝗼𝗰𝗮𝗿𝘀: Deepened OEM relationships in Europe (e.g., Stellantis rollout) & sustained organic client additions in the U.S.

- 𝗙𝗿𝗼𝗴𝗗𝗮𝘁𝗮: Decision intelligence tools saw rapid growth with a >93% gross revenue retention rate. Partnership with FordDirect expands reach.

- 𝗔𝗜 𝗜𝗻𝘁𝗲𝗴𝗿𝗮𝘁𝗶𝗼𝗻: Launched an 'AI factory' for in-house AI-based software development, building AI into the core of all products.

𝗜𝘇𝗺𝗼𝗺𝗶𝗰𝗿𝗼 - 𝗦𝗲𝗺𝗶𝗰𝗼𝗻𝗱𝘂𝗰𝘁𝗼𝗿 𝗙𝗼𝗰𝘂𝘀:

- 𝗕𝗿𝗲𝗮𝗸𝘁𝗵𝗿𝗼𝘂𝗴𝗵: Achieved a breakthrough in silicon photonics packaging with a 32-channel high-density platform, positioning India globally.

- 𝗠𝗮𝗿𝗸𝗲𝘁 𝗢𝗽𝗽𝗼𝗿𝘁𝘂𝗻𝗶𝘁𝘆: Critical for AI data centers, with significant demand expected from hyperscaler investments in India (>$3 lakh Cr).

- 𝗢𝗿𝗱𝗲𝗿 𝗕𝗼𝗼𝗸: Secured an order book of ₹60 Cr with visibility of over ₹100 Cr in the next 12-18 months.

- 𝗗𝗲𝗳𝗲𝗻𝘀𝗲 𝗦𝗲𝗰𝘁𝗼𝗿 𝗘𝗻𝘁𝗿𝘆: Strategic entry into India's defense electronics sector, securing ongoing defense supply contracts.

- 𝗚𝗹𝗼𝗯𝗮𝗹 𝗘𝘅𝗽𝗮𝗻𝘀𝗶𝗼𝗻: Established a new subsidiary in Germany & joined Silicon Saxony, enhancing European market access.

- 𝗙𝗬27 𝗢𝘂𝘁𝗹𝗼𝗼𝗸: Targeting ₹45-50 Cr revenue for izmomicro in FY27.

- 𝗖𝗮𝗽𝗮𝗰𝗶𝘁𝘆 𝗘𝘅𝗽𝗮𝗻𝘀𝗶𝗼𝗻: Plans to raise ₹150 Cr (approx. ₹125 Cr for capex) to expand capacity from ₹150 Cr to ₹1,200 Cr.

- 𝗙𝘂𝘁𝘂𝗿𝗲 𝗣𝗿𝗼𝗷𝗲𝗰𝘁𝗶𝗼𝗻𝘀: Expects ₹1,200 Cr to ₹1,500 Cr revenue from izmomicro in 5 years.

𝗙𝗶𝗻𝗮𝗻𝗰𝗶𝗮𝗹𝘀 & 𝗚𝘂𝗶𝗱𝗮𝗻𝗰𝗲:

- 𝗠𝗮𝗿𝗴𝗶𝗻𝘀: Expects EBITDA margins to improve to 20-25% in FY27 & 30% in FY28, driven by izmomicro's growth & new plant.

- 𝗙𝘂𝗻𝗱𝗶𝗻𝗴: In process of raising ₹150 Cr via equity-cum-debt for capex.

- 𝗧𝗿𝗮𝗱𝗲 𝗥𝗲𝗰𝗲𝗶𝘃𝗮𝗯𝗹𝗲𝘀: Stood at ₹129 Cr in Q4 FY26 (100-110 days), considered normal for large clients like Hertz & Stellantis.

𝗡𝗼𝘁𝗮𝗯𝗹𝗲 𝗤&𝗔 𝗣𝗼𝗶𝗻𝘁𝘀:

- 𝗢𝘁𝗵𝗲𝗿 𝗘𝘅𝗽𝗲𝗻𝘀𝗲𝘀: Jump in Q4 was due to a special project with pass-through revenue; expected to decrease going forward.

- 𝗦𝗶𝗹𝗶𝗰𝗼𝗻 𝗣𝗵𝗼𝘁𝗼𝗻𝗶𝗰𝘀 𝗧𝗔𝗠: Globally estimated at $30 billion, growing to $80 billion.

- 𝗖𝗼𝗺𝗽𝗲𝘁𝗶𝘁𝗶𝗼𝗻: No direct competition in India for izmomicro's advanced packaging; international competition exists from Korean, US, & Taiwanese companies.

- 𝗙𝘂𝗻𝗱𝗶𝗻𝗴 𝗡𝗲𝗲𝗱𝘀: Requires ₹100-150 Cr for packaging capability expansion, with funding in process.

- 𝗖𝗼𝗹𝗹𝗮𝗯𝗼𝗿𝗮𝘁𝗶𝗼𝗻: Partnerships with CCRAFT & Alcyon Photonics are expected to contribute meaningful revenue in FY27.

- 𝗠𝗼𝘁𝗼𝗿 𝗕𝘂𝘀𝗶𝗻𝗲𝘀𝘀: Commercial production is underway for a previously announced motor with orders already secured.

📊 IZMO LTD | 🏷️ Earnings Call Transcript

🌐 Details: wegro.app/OV4vjz

⚡️Instant stock alerts on WhatsApp - Try FREE 👉 wegro.app/go

1

1

220

Jun 7

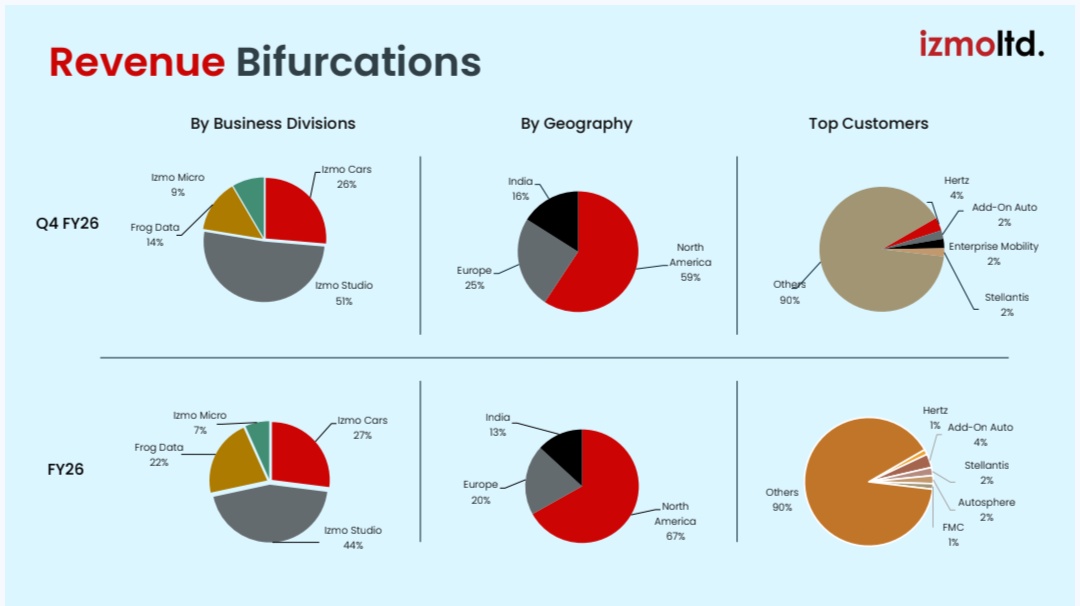

2/ IZMO today operates 4 biz

📸 Izmo Studio

💻 Izmo Cars

📊 FrogData

🔬 Izmo Micro

The first three provide stable, recurring software revenues.

Izmo Micro is the new growth engine.

FY26 revenue mix:

Studio 44%

Cars 27%

FrogData 22%

Micro 7%

1

2

972

📢 izmo Ltd.

BSE: 532341

Potential Impact: Positive

Q3 & 9M FY26 Investor Presentation

1. Company presented its Q3 & 9M FY26 investor update.

2. Management highlights continued progress and stable performance across key markets.

3. Revenue remained stable at Rs. 59.1 cr in Q3 FY26.

4. EBITDA (excluding other income) grew 70% YoY to Rs. 14.1 cr, and PAT increased 93.1% to Rs. 11.7 cr in Q3 FY26.

5. Partnerships with Ford Direct for AI-driven service operations solutions through FrogData were highlighted.

6. Izmo Micro's order book is growing stronger from diverse sectors.

7. Development of a 3D SiP module for space payload camera electronics and headway in silicon photonics packaging through IIT Madras partnership were mentioned.

8. Key updates include izmo Micro's advanced space electronics packaging, FrogData's partnership with FordDirect, izmostock's new global portal, and izmo AI Factory.

9. Business divisions include izmostock, izmoauto, frogdata, and izmomicro.

10. Financial highlights show consistent revenue and EBITDA growth.

#izmo #StockMarket #Updates

⚠️ Disclaimer: This update is for informational & educational purposes only, sourced from public announcements. Not investment advice. I am not SEBI registered.

📡 This channel provides real-time updates as and when announced on BSE.

🔔 Follow to stay updated!

2

250

Jan 27

IZMO Limited

Izmo Ltd's FrogData partners with FordDirect, USA, enhancing dealership service operations via 'The Shop' marketplace for Ford & Lincoln retailers. No specific order value mentioned.

MCap: 968.17 Cr. CMP: 647.45

#IZMO #Breaking #FlashStox #StockMarket

2

504

Company: IZMO

Update Type: Press Release 📰 | Sentiment: Positive 🟢

Summary: Izmo Ltd’s FrogData division has partnered with FordDirect to join 'The Shop,' a curated marketplace for Ford and Lincoln dealers. This integration provides Izmo direct access to the Ford dealer network, offering its AI-driven FixedOps analytics and service marketing suites to improve dealership profitability.

9

1,098

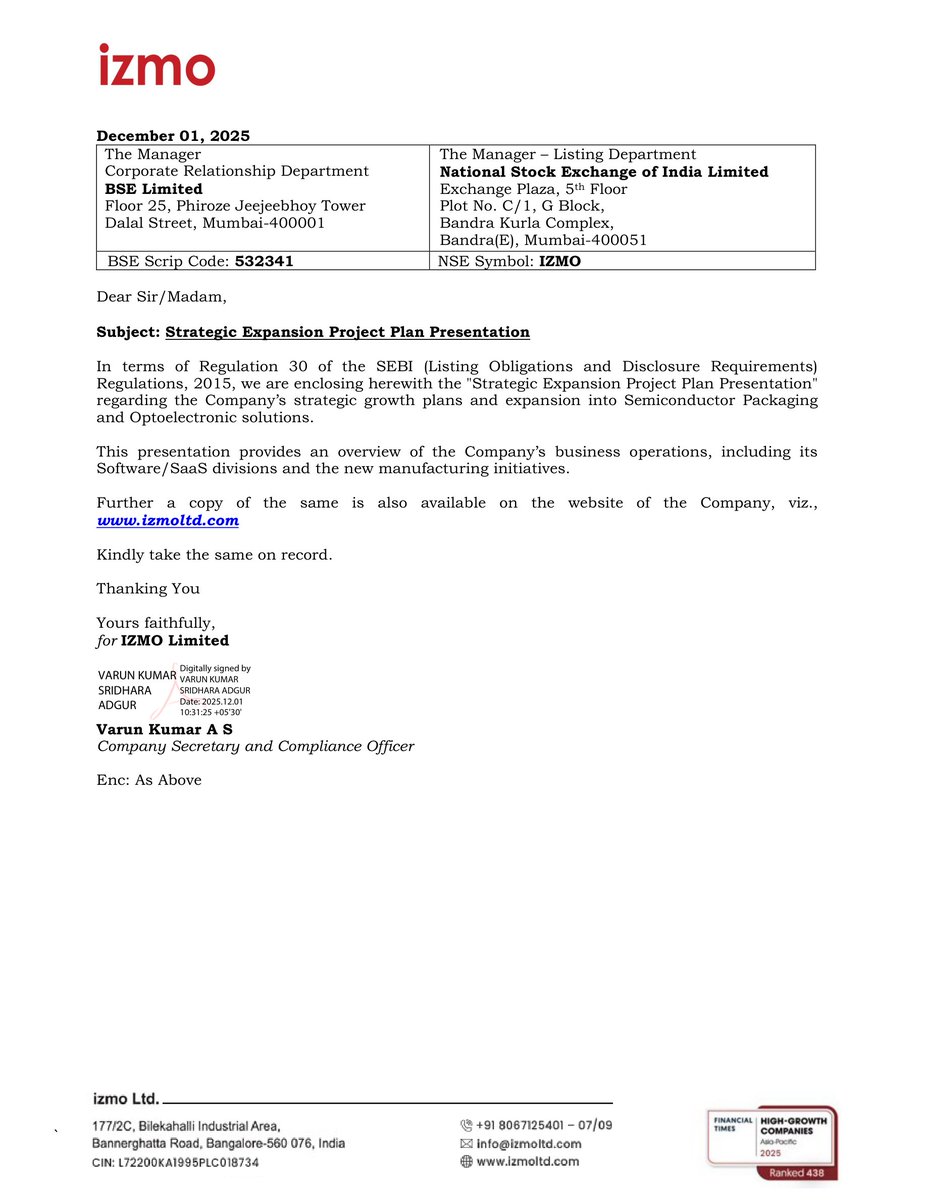

1 Dec 2025

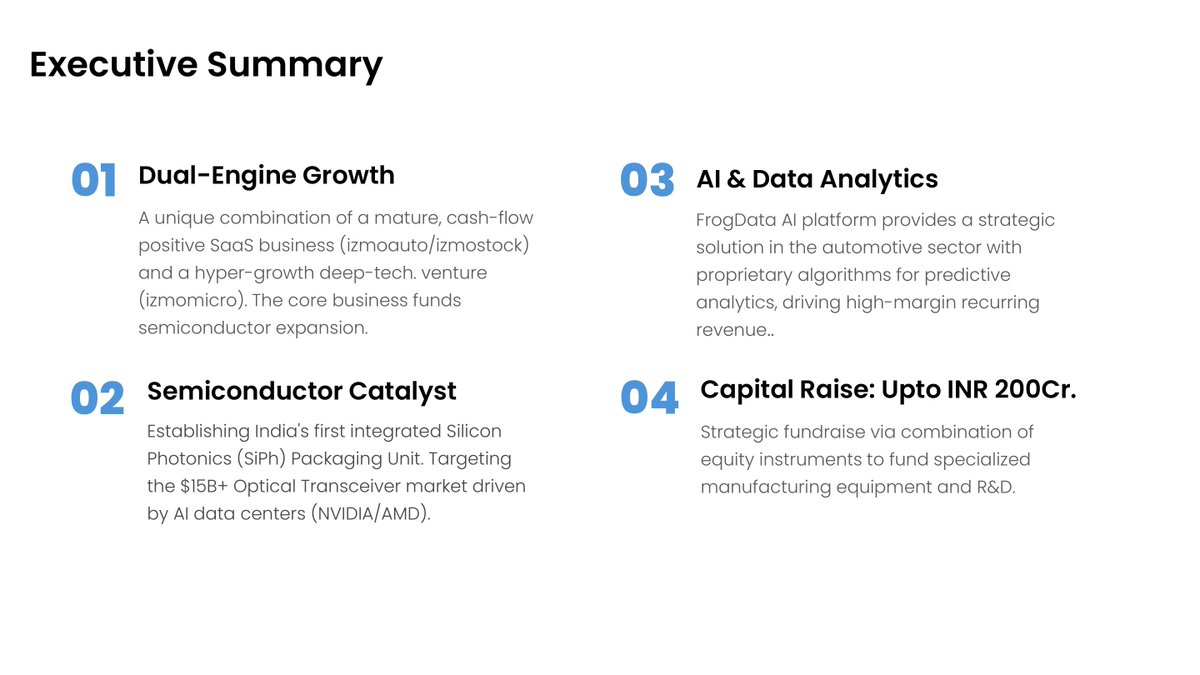

💡 IZMO unveils ₹200 Cr expansion plan into Silicon Photonics & Optical Transceivers

👉🏻 Company to raise up to ₹200 crore to fund semiconductor packaging, silicon photonics & high-speed optical transceiver manufacturing.

👉🏻 Setting up India’s first integrated Silicon Photonics packaging unit targeting the booming AI data-centre market.

👉🏻 New ultra-low-power optical transceivers planned (400G → scalable to 800G & 1.6T).

👉🏻 Core SaaS businesses (izmoauto, izmostock, FrogData) continue to generate stable ARR to support deep-tech expansion.

👉🏻 Strong tech moat with DSIR-recognised R&D unit exclusive IIT-Madras photonics partnership.

#IZMO #Semiconductors #Photonics #AIDataCenters #OpticalTransceivers

4

17

1,360

1 Dec 2025

🚀 IZMO Ltd. Pioneers India’s First Silicon Photonics Packaging Unit, Eyes $15B AI Data Center Market | MCap 1,347.74 Cr

- IZMO is establishing India’s first integrated Silicon Photonics (SiPh) Packaging Unit, targeting the $15B Optical Transceiver market driven by AI data centers.

- Plans to launch Optical Transceivers in Q1 2026, targeting India, APAC, and European markets.

- Projects a strong 30% CAGR in India for 400G modules.

- Operates a dual-engine model: mature SaaS (izmoauto/izmostock) and hyper-growth deep-tech (izmomicro).

- FrogData AI platform drives high-margin recurring revenue in the automotive sector.

- Global footprint across 22 countries with clients like Stellantis, Ford, Renault, BEL, and IIT Madras.

- Strategic partnership with IIT Madras (CPPICS) for Silicon Photonics R&D.

- izmostock is the world’s largest automotive stock library (Hertz, Avis, Europcar).

- izmoauto serves 3,000 global dealers with a multilingual digital retail platform.

- Management team boasts decades of expertise in tech, automotive, and semiconductors.

Complete Source: bseindia.com/xml-data/corpfi…

Disc: Information provided in this tweet can be inaccurate, verify through the source before making any investment decision.

Preview 👇 (First 4 out of 30 pages)

1

2

4

1,146

9 Sep 2025

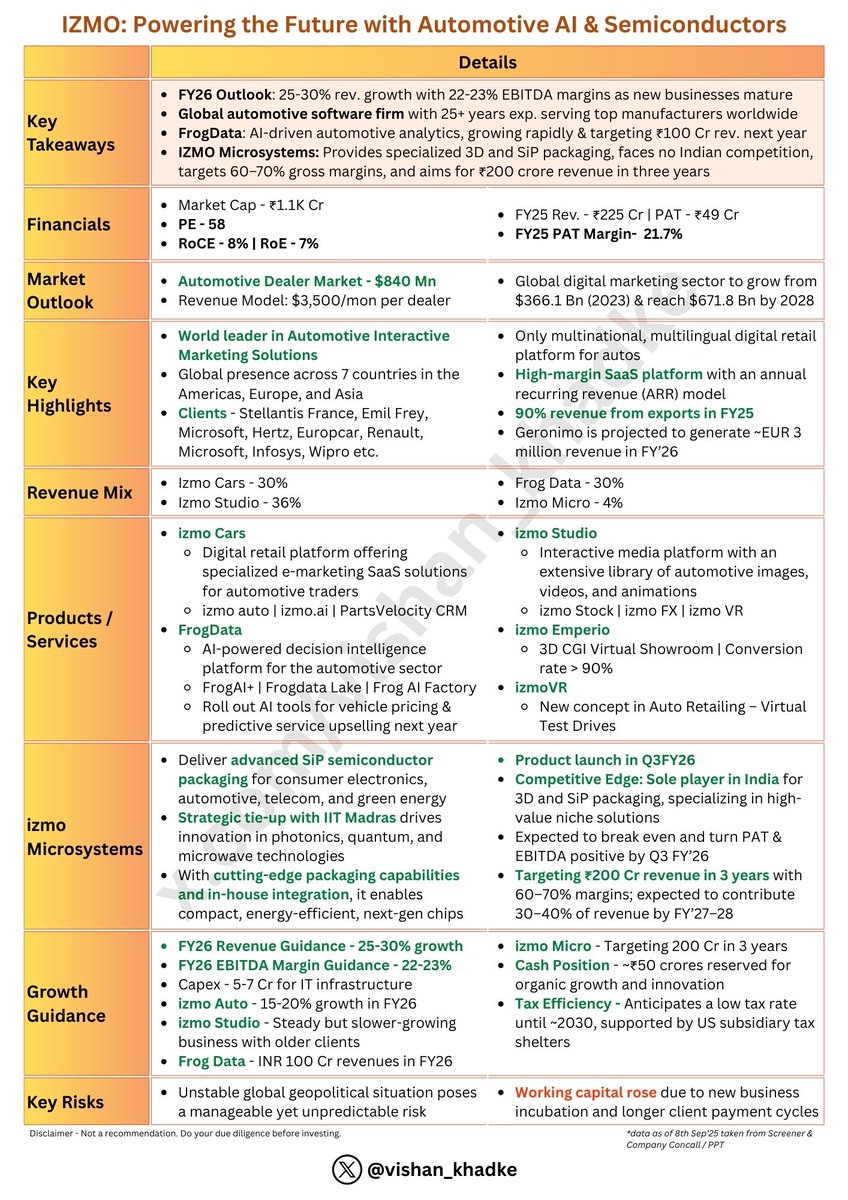

Izmo - Powering the Future with Automotive AI and Semiconductors 🚀

💡 Want more one-pagers like this? Follow 👉 @vishan_khadke

[ Trades at FY26 PE - 29x ]

🟩 Global Leadership & Client Base

• World leader in automotive interactive marketing, with presence across 7 countries spanning the Americas, Europe, and Asia

• Clients: Stellantis, France; Emil Frey; Microsoft; Hertz; Europcar; Renault; Microsoft; Infosys; Wipro

🟩 Scalable SaaS Platform

• Only multinational, multilingual digital retail SaaS platform for auto dealers globally

• High-margin SaaS model with annual recurring revenue (ARR) and over 90% revenue derived from exports in FY25

🟩 Innovation & Diverse Revenue Mix

• Multiple product lines: izmo Cars, izmo Studio, FrogData (AI analytics), izmoVR (virtual retail), and izmo Microsystems (SiP packaging)

• Focus on AI-driven analytics, virtual showrooms, and advanced semiconductor packaging for automotive and consumer tech

🟩 Strong Growth Potential

• FY26 revenue growth guidance of 25-30%, with EBITDA margins of 22-23%

• Product mix enhancements and new launches expected to drive future PAT & margin expansion, targeting ₹200 Cr revenue in 3 years

✅️ Strategic Edge

• Sole Indian player in advanced 3D and SiP packaging, partnering with IIT Madras for photonics, quantum, and microwave innovation

• Competitive positioning in high-value automotive digital marketing and interactive solutions

⚠️ Key Risks

• Geopolitical uncertainty: Global instability may pose unpredictable risks.

• Working capital rise: Longer client payment cycles due to new business incubation impact liquidity.

📈 Financial Projections (Conservative)

• Revenues (assumed 30% growth)

▪︎ FY26 - 290 Cr

• EBITDA (22% margin assumed)

▪︎ FY26 - 64 Cr

• PAT (assumed interest and depreciation as 18 Cr and tax rate of 10%)

▪︎ FY26 - 41 Cr, PE - 29

For more details, please read the one-pager attached 👇

Disclaimer - No recommendation. Do your due diligence before investing.

If you liked the content, please Like | Repost | Bookmark 😀

@deepak4748 @Dynamicinvstr

#Izmo

25 Aug 2025

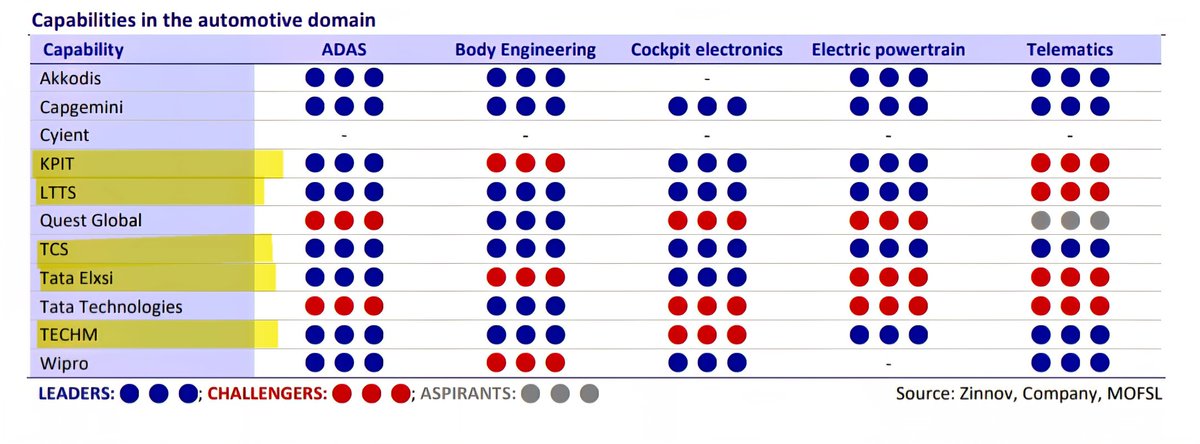

Auto Tech - TCS, KPIT, LTTS, Tech Mahindra & Tata Elxsi are best positioned for next-gen auto tech growth.

13

15

119

25,613

22 Aug 2025

🚀 IZMO Ltd Reports 19% Revenue Growth in Q1 FY26, Expands into Germany & Launches AI Innovations | MCap 872.13 Cr

- Revenue grew 19% YoY to Rs. 56.5 crores in Q1 FY26.

- Added 88 new clients in the US and 27 in Europe/UK this quarter.

- Entered the German market, leveraging Geronimo and Izmo Microsystems (IMPL).

- Launched Izmostock’s global portal and an Automotive AI Factory.

- Gross revenue retention rate stands strong at 98.5%.

- FY25 annual highlights: 20.27% growth in total income (Rs. 224.61 Cr) and 87.64% PAT growth (Rs. 48.88 Cr).

- EBITDA (ex-other income) grew 4% YoY to Rs. 9.7 Cr in Q1 FY26; PAT at Rs. 6.0 Cr.

- One-time German market/IMPL expenses impacted margins.

- Strategic R&D focus: izmoVR, izmo.ai, and partnership with IIT Madras for semiconductor solutions.

- Core divisions: izmo Cars (retail), Frogdata (AI), izmo Studio (media).

Complete Source: bseindia.com/xml-data/corpfi…

Disc: Information provided in this tweet can be inaccurate, verify through the source before making any investment decision.

Preview 👇 (First 4 out of 35 pages)

2

1,152

20 Feb 2025

Company: IZMO

Update Type: Investor Presentation

Summary: Expanding client base, FrogData AI growth, 3D semiconductor packaging, Izmo Microsystems operational ramp, Geronimo integration, US, Europe market expansion[0].

12

1,795

11 Dec 2024

It can go up even more due to Frogdata and sentiments around their Semiconductor subsidiary and become 2x from here!! But yes, entry at this point can be risky!!

1

2

444

10 Dec 2024

Thanks for posting these insights! It’s always great to see updates like this.I have done a fundamental analysis and found the following factors interesting.

[1] Core Divisions: IZMO Limited operates through three main divisions: IZMO Studio, which offers interactive media solutions; IZMO Auto, a digital retail and CRM platform; and FrogData, focusing on AI and data intelligence for the automotive sector.

[2] Recent Acquisition: The company recently acquired Geronimo Web, a UK-based digital marketing leader for auto dealers, which expands IZMO's client base in Europe and Latin America, including onboarding Ford as a new client. This acquisition is expected to contribute ₹30-35 crores in revenue over the next year.

[3] Spanish-Language Platform Launch: IZMO has launched a Spanish-language platform, autogozo.com, targeting the Hispanic automotive market in the US. Over 2,000 dealers have signed up, tapping into a market valued at $220 billion.

[4] Financial Performance: For Q2 FY25, IZMO reported revenues of ₹58.55 crores, marking a 30.83% year-on-year increase, with a PAT of ₹29.9 crores compared to ₹5.12 crores in Q2 FY24, benefiting from a one-time property sale gain.

[5] Growth Expectations: The company anticipates significant growth in its FrogData division, projecting a 25%-30% increase in H2 FY25 and aiming for 50%-75% year-on-year growth over the next two years. Additionally, revenue from its semiconductor business is expected to reach ₹30-40 crores by FY26.

[6] Strategic Focus on R&D: IZMO maintains an annual R&D budget of ₹20-25 crores to support product development and innovation, with management projecting an average growth rate of 25%-30% year-on-year based on favorable market conditions and internal capabilities.

No Buy/Sell recommendation.

If you've found this helpful, show some love with a kind REPOST and LIKE! @FunTech_Founder

2

312