fermacell® gypsum fibreboards and fermacell® Therm25™ dry screed elements have achieved C2C Certified® FullScope and C2C Certified® Material Health at Silver level in accordance with Version 4.1...

( @JamesHardieUK )

specifier-select.co.uk/post/…

#Contractors #Architects #Building

56

Jun 15

fermacell® gypsum fibreboards and fermacell® Therm25™ dry screed elements have achieved C2C Certified® FullScope and C2C Certified® Material Health at Silver level in accordance with Version 4.1...

( @JamesHardieUK )

xtrabuild.co.uk/post/fermace…

#Contractors #Architects #Building

1

63

fermacell® gypsum fibreboards and fermacell® Therm25™ dry screed elements have achieved C2C Certified® FullScope and C2C Certified® Material Health at Silver level in accordance with Version 4.1...

( @JamesHardieUK )

atbnews.co.uk/post/fermacell…

#Contractors #Architects #Building

62

fermacell® gypsum fibreboards and fermacell® Therm25™ dry screed elements have achieved C2C Certified® FullScope and C2C Certified® Material Health at Silver level in accordance with Version 4.1...

( @JamesHardieUK )

buildinginnovationsnews.co.u…

#Contractors #Architects #Building

73

fermacell® gypsum fibreboards and fermacell® Therm25™ dry screed elements have achieved C2C Certified® FullScope and C2C Certified® Material Health at Silver level in accordance with Version 4.1...

( @JamesHardieUK )

brickwork-bulletin.co.uk/pos… #Contractors #Architects #Building

69

fermacell® gypsum fibreboards and fermacell® Therm25™ dry screed elements have achieved C2C Certified® FullScope and C2C Certified® Material Health at Silver level in accordance with Version 4.1...

( @JamesHardieUK )

brickwork-bulletin.co.uk/pos…

#Contractors #Architects #Building

72

fermacell® gypsum fibreboards and fermacell® Therm25™ dry screed elements have achieved C2C Certified® FullScope and C2C Certified® Material Health at Silver level in accordance with Version 4.1...

( @JamesHardieUK )

brickwork-bulletin.co.uk/pos…

#Contractors #Architects #Building

66

Jun 9

blankSLATE: Behind-The-Scenes 001

the pod behind the pod!

BTS, VLOGS, and everything you don't see from the listener side - fullSCOPE Tier ONLY (Watch in full)

Watch here 🎥: patreon.com/blankSLATEHQ

3

7

1,905

Jan 8

Wazz'up GME 2019 activist gang? Part 1: Hestia, Ancora (also being involved in $BBBY/ $BBBYQ, $BIG & others) and the Edgewater Technology ( $EDGW ) sale raising the question whether preeminent proxy advisory like Institutional Shareholder Services interfere with incumbent management flaws but not with shareholders value destruction by certain activists?

This is not financial advice; do your own research

Topics:

* Intro

* 2016-2018 $EDGW: takeover with Ancora Advisors and merger with $ALYAF

* 2017: Ancora stating the events

* 2017: Edgewater adds to these events and strongly opposes Ancora and warns shareholders

* 2017: Proxy fight; fact checking the claims

* 2017: The proxy vote; or how to change your mind completely in a few days (deadline February 20, 2017)

* 2018: $EDGW sale was really bad for shareholders

* 2016-2018 $EDGW: sale conclusion and open questions

* 2016-2018 $EDGW: Answers and hypotheses

* Checking Ancora's track record with ISS

* Concluding with hypotheses regarding shareholder value destruction and outlook

** Intro **

When Burry came back for $GME after years, it was wonderful looking back.

We took a look at his track record in general (see x.com/beyond_mythos/status/1…) as well as compared $GME's state with and without the activist gangs changes (see x.com/beyond_mythos/status/2…).

In his post "Foundations: The Big Short Squeeze" from 12/16/25 he said "as result of Hestia and Permit, and then my pressure, GameStop bought back 38.1 million shares". Thus, why shouldn't we look at their track record too?

First let us take a look at Hestia Capital Partners, namely Wolf Kurt James.

Surely, you'll immediately feel comfortable reading "Mr. Wolf also has experience working as a consultant both with Deloitte Consulting from September 1995 until September 1998 and The Boston Consulting Group during the summer of 2001".

We find his first SEC filing for 2010-01-25, a sale of unregistered securities (sec.gov/Archives/edgar/data/…). He sold $800k to 4 investors. Which rose to $3.4m and 11 investors during 7 financing rounds in 2016 and 2025 $32m with 45 investors (sec.gov/edgar/search/#/dateR…). His first action which we will discuss in part 1 here is the sale (or merger) of Edgewater Technology ($EDGW) from 2016 to 2018.

** 2016-2018 $EDGW: takeover with Ancora Advisors and merger with $ALYAF **

Together with Ancora Advisors (Frederick DiSanto) and some others (see sec.gov/Archives/edgar/data/…) they invested into EDGEWATER TECHNOLOGY INC and both among two more become nominees for the board. Both were on the board from February 16, 2017 (sec.gov/Archives/edgar/data/…) until November, 2018 (sec.gov/Archives/edgar/data/…). In 2015 the company had acquired three consulting companies (M2 Dynamics, Zero2Ten, Branchbird LLC) leading to a very diverse customer base with 670 customers in 2016 with the five largest only accounting for 15.2% of service revenue. With services like C-level strategy consulting, IT consulting, products and services they got very deep knowledge about their customers and as speculation, while harming fiduciary duty, this knowledge could be seen as a very valuable asset for competitors.

Hypothetically, in theory and just as a thought experiment, this could be used as intelligence for competitors and thus be of high interest for those. However interesting this might be, we won't extend on this here because its not the point of this post.

On November 1, 2018, Edgewater Technology, Inc. ($EDGW) and Alithya Group inc. (private) merged into "New Alithya" ($ALYAF), (sec.gov/Archives/edgar/data/…).

And here it gets spicy. There was a very public proxy fight where the board opposed Ancora.

** 2017: Ancora stating the events **

* April 2015: First investment by Ancora

* Apr 2016: "Ancora intends to seek the replacement of the incumbent members of the Board, other than the two independent directors added in March 2016" [Paul E. Flynn, Paul Guzzi, Michael R. Loeb and Wayne Wilson]

* Oct 2016: "Ancora's views regarding sale of the Company in pieces or in whole and ways the Company"

(sec.gov/Archives/edgar/data/…)

* Dec 2016: "issuance of a press release announcing Ancora’s filing of the Preliminary Consent Statement in order to allow stockholders to reconstitute the Board" [Matthew Carpenter, Frederick DiSanto, Jeffrey L. Rutherford and Kurtis J. Wolf]

* Jan 2017: "Edgewater [...] established the close of business on January 11, 2017, as the record date to determine the stockholders entitled to [vote]."

(timeline and 5 proposals: sec.gov/Archives/edgar/data/…)

** 2017: Edgewater adds to these events and strongly opposes Ancora and warns shareholders **

* March 2016: "[In a settlement agreement with Lone Star Value Management, LLC] the Company expanded the size of the Board of Directors [...] from six to eight directors and appointed [...] Timothy Whelan and Stephen Bova."

* June 2016: "[...] Ancora, contacted Ms. Singleton and requested one board seat to provide a fresh outlook and represent the Edgewater shareholders. Ms. Singleton communicated to Mr. Chadwick that Mr. Whelan and Mr. Bova were recently appointed to the Board to provide a fresh outlook, and that, even if Edgewater were amenable to additional directors, the Settlement Agreement restricted Edgewater from making additional appointments [...]."

* Nov/Dec 2016: very detailed timeline of how Edgewater tried to tell Ancora, they reject their requests.

(sec.gov/Archives/edgar/data/…)

January 10, 2017, Edgewater states in an investor presentation for the proxy vote (sec.gov/Archives/edgar/data/…) that:

* Ancora replacing senior leadership would cause significant distraction and disrupt the strategic plan (p. 5)

* "Despite seeking Board control, Ancora has not offered any specifics on how its nominees would create shareholder value, especially, if they are unable to sell the company" (p. 6)

* "Ancora is a short-term investor" [Which was proven true, after its sale in 2018] (p. 6)

* S. Singleton and D. Clancey own 12.8% in $EDGW, aligning their interests with the shareholders. (p. 6) [I see RC approving this statement]

* They show a solid 6.2% revenue CAGR, 63% institutional holdings [84,8% including management], [but admittedly, their reported operating income/EBIT margin for 2016 was ~2%, but their cash flow from operating activities was at 6% of revenue and looks solid over the past years] (p. 10).

* "Ancora's Interests are NOT aligned with Edgewater shareholders" [see page 28 and following for missing qualifications and missing plan].

* [My opinion: Overall Edgewater's strategy and past success looks compelling to me and Ancora missing plan or even their missing stated intention, beside selling the company, wouldn't look compelling to me if I was a long-term shareholder. Though some points of Ancora about the company performance are valid.]

(sec.gov/Archives/edgar/data/…)

In summary, we see Edgewater's management clearly opposing Ancora.

** 2017: Proxy fight; fact checking the claims **

Before Ancora made any public claims of underperformance of Edgewater, Ancora very clearly states on April 29, 2016 that they intent Edgewater entirely to be sold (sec.gov/Archives/edgar/data/…).

Since they didn't state any other plan, but concentrated on the company performance we can rather safely assume hat all voting shareholders were aware of their intentions and would in hindsight rate Ancora by the outcome of the sale of the company.

We'll list each claim, the counter argument and who is in my opinion more right. This is debatable since I in some cases argue against conventional wisdom.

1. Ancora: Stock underperformance vs. peers/market (1/3/10-year periods)

* Counter (Edgewater): 5-year TSR 153% outperforms some peers; peer group mismatched (e.g., includes non-comparable large firms like IBM).

* More true: Ancora; data shows underperformance in cited periods; 5-year boosted by low 2012 base from prior decline.

2. Ancora: High SG&A expenses (>50% above peers, ~29-33% of revenue)

* Counter (Edgewater): Peer group invalid; focus on revenue growth ( 24% 2012-2016 > peer median).

* More true: Ancora; verified SG&A ~29% in 2015 vs. IT peers median ~23-24%; erodes margins.

3. Ancora: Declining consultant utilization (e.g., 70.8% in 2015, down YoY)

* Counter (Edgewater): Operational progress via acquisitions; partial 2016 targets met (revenue up 10%).

* More true: Ancora; filings confirm decline from 75.8%; below industry benchmarks ~75-80%.

4. Ancora: Excessive exec comp (~$17M cumulative, 90% of EBIT)

* Counter (Edgewater): 91% say-on-pay approval; essential for talent retention; renewed agreements valid.

* More true: Edgewater; Indeed high % relative to weak EBIT, but 91% say-on-pay and high equity

5. Ancora: Inadequate company sale review (narrow focus on whole-company sales, no breakup explored)

* Counter (Edgewater): Thorough (contacted 66 parties, 11-month process); stand-alone best for value.

More true: Debatable, since a lot or even most of M&A activities don't add value for shareholders (hbr.org/2020/03/dont-make-th…).

6. Ancora: Board lacks independence (6/8 with >10-year tenures)

* Counter (Edgewater): Directors qualified via governance process; added independents in 2016.

* More true: Debatable, in my opinion the outcome should be way more important than a higher board turnover. ISS guidelines suggests <= 9 years, which in my opinion might rather add short-term thinking and thus harm shareholders.

7. Ancora: Poor acquisition track record (e.g., Fullscope embezzlement, offsetting legacy decline)

* Counter (Edgewater): Successful overall; revenue 734% since 2004, Fullscope 177% since 2009; embezzlement settled June 2014 with >95% recovery from escrow.

* More true: Edgewater; verified growth and settlement; embezzlement resolved without major loss.

8. Ancora: Negative free cash flow due to acquisitions (~$104M costs)

* Counter (Edgewater): Positive ops cash flow $51.3M since 2002; actual acquisition costs $83.7M, not $104M.

* More true: Edgewater; distinguishes ops cash from investments; Ancora overstated costs.

9. Edgewater: Ancora's nominees lack thorough selection, driven by self-interest

* Counter (Ancora): Nominees qualified (e.g., DiSanto's finance expertise); aim to enhance value for all.

* More true: Edgewater; partial—activist-led, but ISS endorsed two as adding value; standard for proxies.

10. Edgewater: Stand-alone strategy best post-review

* Counter (Ancora): Review flawed, no results despite pressure.

* More true: Debatable, see point 5

11. Edgewater: Partial 2016 performance targets met (revenue exceeded)

* Counter (Ancora): Overall sub-par margins/EBITDA.

* More true: Edgewater; verified revenue up ~8-10% YoY, but EBITDA missed.

Summarizing I would follow Ancora with: 1. Stock underperformance, 2. High SG&A expenses, 3. Declining consultant utilization

I would discuss: 5. Company sale (combined with 10), 6. Board independence

And I would rather go with Edgewater: 4. exec comp, 7. acquisition track record, 8. free cash flow, 9. Acora's nominees, 11. 2016 performance targets

While we could have a philosophical discussion about what the purpose of a company is, let us for now say it is the shareholder value, reflected by the operational income, equity and stock price.

** 2017: The proxy vote; or how to change your mind completely in a few days (deadline February 20, 2017) **

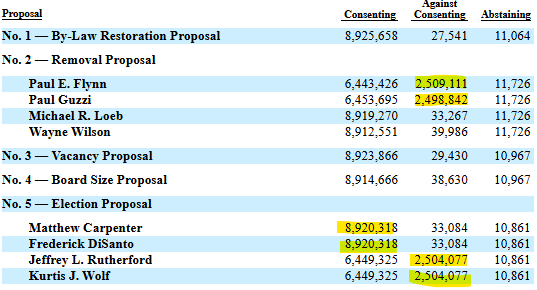

David and Sherly own 1.7m shares (12.8% of the company) and together the 12 directors and executive officers own 3.1m shares (21.8% of the company, see "Stock Ownership of Directors and Management" in sec.gov/Archives/edgar/data/…).

Now, here it gets interesting.

Total shares outstanding were 12,880,356. Roughly 3.8-4m shares weren't voted, assuming those were non-voting retail investors and institutions because of lack of interest, information or whatsoever. A majority (over 6.44 million) votes were required for a proposal to go through. Here are the voting results:

(sec.gov/Archives/edgar/data/…)

* GAMCO Investors and Dimensional Fund Advisors Inc together owned 24.7% together during the vote (sec.gov/Archives/edgar/data/…) and were invested since 2002 (sec.gov/Archives/edgar/data/…), together with the Edgewater management 46.5%.

* With barely above the 6.44m threshold, Paul E. Flynn and Paul Guzzi got removed as well as Jeffrey L. Rutherford and Kurtis J. Wolf got elected. That was close for Ancora. Maybe we'll look at this in more depth in the future.

* Who aligned apparently nearly all the institutional owners and how? Especially, as we've seen above Ancora seemed to be pretty much the worse choice for long-term shareholder.

[sec.gov/Archives/edgar/data/…]

* With almost certainty we can say that the management did vote, especially as we see those 2.5m vote blocks shifting between consenting and against.

* With almost certainty we can say that the Edgewater management changed their minds within days about Ancora, as they with near certainty voted for DiSanto's who they heavily opposed before, right? Why?

Shirley and David left the company in March 2017, getting a lump-sum severance payment of $1.4 million for Shirley and $1.2 million for David. Interestingly, they didn't file for a sale of their stock, which means they took a position in $ALYA after the merger. After the merger their position was around 2% of $ALYAF and they could have sold without any public notice. If they would have sold to the open market directly after the merger, they would have made $5.4m and $5.7m respectively. Which is less as if they would have sold when leaving the company.

Interestingly, Lone Star board members were the only pre-Ancora board members who stayed with the company until the merger (sec.gov/Archives/edgar/data/…). We heard of Lone Star before, didn't we? But that's for another post.

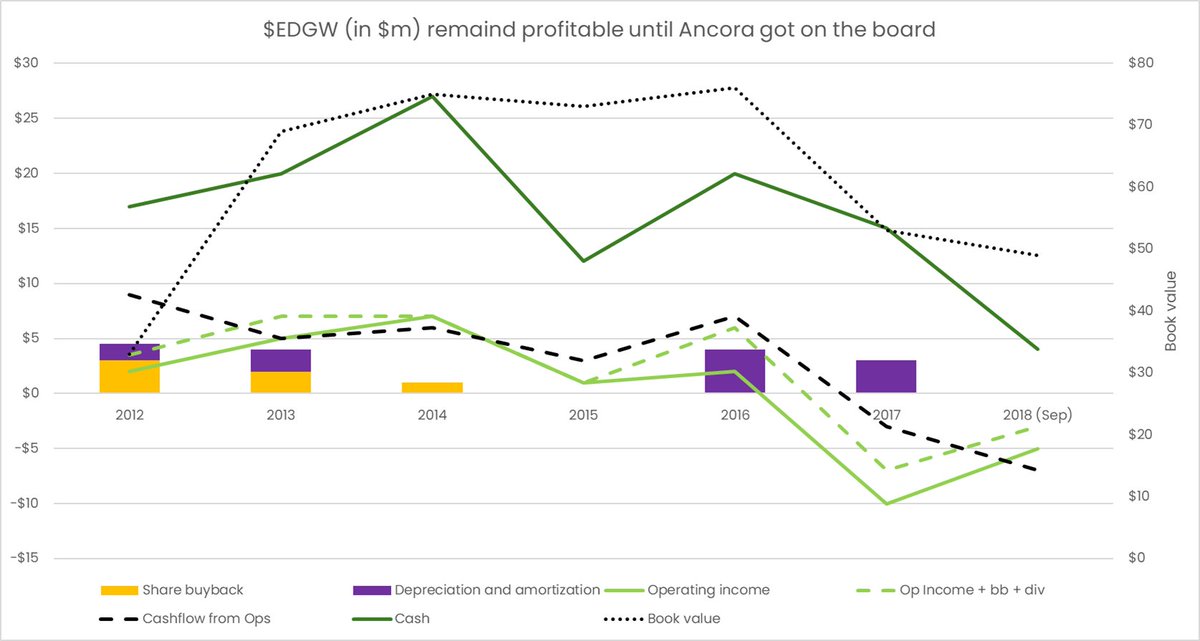

** 2018: $EDGW sale was really bad for shareholders **

During Ancora's time equity decreased 35% (76m in 2016, 53m in 2017 and 49m in 2018).

The merger adjusted stock price fell 68% from $7.44 year end 2016 (EDGW close adjusted (original ~$8.87 / 1.1918) to $2.35 in 2018 (ALYA close post-merger) and even 77% to $1.69 end of 2020.

Book value per share fell 45% 2016 to 2018 and 66% 2016 to 2020.

Hm.

** 2016-2018 $EDGW: sale conclusion and open questions **

* The incumbent Edgewater management was right in their assessment, that Ancora was short-term oriented and disrupted shareholder value **EVEN as they sold the company**, which leads us to

1. What was in for the institutions to change the majority vote against the incumbent management and for Ancora, who didn't provide any strategic plan for shareholder value beside the sale or a breakup?

2. How was at least part of the management convinced to vote in favor Ancora, just a few days later after they heavily opposed them?

3. If Ancora and institutions who voted for it knew it was about the sale of the company, why did they accept the company performance going south in 2017 and 2018 ending in a merger which disrupted shareholder and thus their own value?

4. Why are shareholders left holding the bag without any accountability? The only thing the SEC did was to ask Ancora for proof and they just changed things to "they beliefe...". But that's a more ethical question.

** 2016-2018 $EDGW: Answers and hypotheses **

1. Hypothetically, we can assume that support by the Institutional Shareholder Services shifted the vote in Ancora's favor and yet didn't voice any concerns when shareholder value eroded.

* We find that on January 30, 2017 GAMCO voices support for Ancora and explain, that "nominees will add value to the Issuer's Board" (sec.gov/Archives/edgar/data/…).

* February 7, 2017 the Institutional Shareholder Services (ISS) voices support for Ancora and explains a bit more in detail as GAMCO, namely SG&A as mentioned above, EBITDA result (but not mentioning cash flow from operations - which in my opinion looks good), tenure of the board, "the strategic review process" or better the sale of the company, lack of transparency and praising DiSanto's banking experience and Carpenter's IT experience.

* To be honest, I didn't hear of the Institutional Shareholder Services before. They have very strong influence on institutional shareholder votes in public companies: "[a]s the preeminent proxy advisory firm, ISS maintains a leading market position, holding an estimated 48% share of the U.S. proxy advice market for mutual funds as of 2021, advising on $26.8 trillion in assets from 144 fund families." (grokipedia.com/page/Institut…)

2. Maybe a big part was also the support of the ISS, but do you remember that Shirley and David didn't sell their shares? They could also have kept their $ALYAF stock, which went south afterwards, or they could hypothetically have sold it in a pre-agreed private sale. The latter could explain why they changed their votes in favor to Ancora, giving up Edgewater to someone they only thought very short-term focused and why they kept their stock after they left the company. That's only speculation, but maybe Ancora convincingly secured a majority vote with institutions. Thus let us check out, how things for shareholders went.

3. We also don't see directly how GAMCO and other institutions made money with the deal. But we can assume they would have complained or try to act against the new board if they weren't happy with the outcome. Thus, can we assume their incentives weren't aligned with shareholders?

** Checking Ancora's track record with ISS **

4. Instead of providing an answer here, I'll list you some companies Ancora was invested and got support from ISS for later research:

* 2006: $MACE "Ancora has also noted that both leading independent proxy advisory services, Institutional Shareholder Services ("ISS") and Glass Lewis also recommended voting to WITHHOLD on certain directors." (sec.gov/Archives/edgar/data/…)

* 2015: $RUSHA "Ancora Advisors LLC announced today that Institutional Shareholder Services (“ISS”) is recommending shareholders vote in favor of the proposal to collapse Rush Enterprises, Inc.’s (NASDAQ: RUSHA, RUSHB) dual-class share structure" (sec.gov/Archives/edgar/data/…)

* 2015: $SFLY Shutterfly "In recent weeks, the Shutterfly board of directors has endeavored to demonstrate that it is shareholder friendly, despite receiving a corporate governance rating from ISS prior to its 2014 annual meeting of 9 out of 10, with 10 being the worst" (sec.gov/Archives/edgar/data/…)

* 2016: Edgewater

* 2019: $BBBYQ Bed Bath & Beyond [bankrupted 2023] "ISS has given the quality score here of eight. That’s a little bit better than the last two years where it was at the highest risk at ten." (sec.gov/Archives/edgar/data/…)

* 2021: $BCOR BLUCORA INC "ISS Recommends Blucora Stockholders Vote For Boardroom Change on Ancora’s WHITE Proxy Card" (sec.gov/Archives/edgar/data/…)

* 2022: $SPTN SpartanNash Co "We are not alone in finding issue with the Company’s executive compensation plan. In its evaluation of the Company’s executive compensation plan for the 2021 Annual Meeting, Institutional Shareholder Services Inc. (ISS) noted its concern, highlighting Mr. Sarsam’s high compensation [...]" (sec.gov/Archives/edgar/data/…)

* 2023/24: $PBI Pitney Bowes, oh here we find Hestia again: "[o]n January 31, 2024, Pitney Bowes [...] entered into a Cooperation Agreement [...] with Hestia Capital Partners" and they promise to only vote in accordance to Glass, Lewis and ISS (sec.gov/Archives/edgar/data/…)

* 2024: $NSC NORFOLK SOUTHERN CORP "Ohio-based Ancora Holdings Group, LLC (collectively with its affiliates, “Ancora” or “we”), which owns a large equity stake in Norfolk Southern Corporation (NYSE: NSC) (“Norfolk Southern” or the “Company”), today announced that all three independent proxy advisory firms – Institutional Shareholder Services Inc. (“ISS”), Glass, Lewis & Co. (“Glass Lewis”), and Egan-Jones Ratings Company (“Egan-Jones”) – have now recommended that Norfolk Southern shareholders vote “FOR” significant boardroom change at the Company’s upcoming Annual Meeting of Shareholders [...]" (sec.gov/Archives/edgar/data/…)

We further find Ancora in $KOHL, $BIG and many other companies.

Looking back and evaluating the change in share price, change in book value we get the following table:

We see that more likely than not stock price and, or book value decreased significantly (we should add revenue, EBITDA later). In case of the mergers, either the company performance worsened or shareholders were left out. Positive examples are only two of eleven, being $RUSHA (from 2015) as well as recently $NSC (2024). Those following my posts probably won't ask for a control group to verify the results - but maybe I'll do proper statistics at some time. I guess Proxy advisory firms should.

** Concluding with hypotheses regarding shareholder value destruction and outlook **

The result allow to form the following hypotheses:

* Certain activist gangs (Ancora, Macellum, Mithaq, Hestia and more) acting on no morals and destruct shareholder value, very likely for their benefit (see moral framework here: x.com/beyond_mythos/status/2…)

* Proxy advisory firms rather support activist gangs, stating real concerns but ironically don't interfere value destructing in the progress, this is a fundamental flaw with a focus on governance, seemingly neglecting the outcome for long-term shareholders

While this post started with Michael Burry and Hestia Capital, we took a huge detour looking at Ancora and the Edgewater sale in detail. We checked on Ancora's past but should come back to Ancora's present campaigns (e.g., CSX CEO replacement, Americold review) Hestia ( $PBI ) and Permit ( $QVCA ) with their more recent investments. Also we should expand on other activist investors and evaluate their work like Lone Star, Merlin.

It seems like Elon Musk is completely right: "[f]raud will keep rising unless stopped" (x.com/elonmusk/status/200564…). Until then, true long-term shareholder activists like Ryan Cohen will remain the exception.

1

1

4

2,217

11 Nov 2025

Tbh my anxiety constantly haunts me and ngl i dont know if anyone cares for Sammy lore that much so i only post when i see it.

Like only 2 people have a fullscope of how much lore she has.

10 Nov 2025

idk who needs to hear this but if you have ocs or are writing something or anything like that STOP BEING MYSTERIOUS it does you no favors

3

5

248

6 Oct 2025

Saw all the charlos videos and came to stake his claim.

Roberto teto merhi - the orginal, the fullscope, the endgame - carlos sainz wag

4

635

DeepBot watches everything so you don’t have to, then sends you the moment to strike.

🔗 Go to deepbot.pro to find out more

DeepBot & DeepBot PRO: Your Unfair Advantage.

$DEEPAI #DeepBot #DeepBotPRO #FullScope #MarketEdge #TradingPower

2

7

1,448

I wish people really realized it fullscope how old this planet is so much history well never know about, but we assume that our time is the best. It’s just most current.

11

3,673

26 Dec 2024

A Panic Room for everyone in your gaudy 80s mansion that you don't live in and wasn't burglarized. BTW, why is he still doing his pod from the old house? Fullscope, Premium, A&A Mgmt, 13 Mgmt - low IQ and petulant. dailymail.co.uk/tvshowbiz/ar…

1

10

2,306

7 Nov 2024

Ormiston partner with Kite Trust in Fullscope. Kite Trust are all over MH in the East of England.

I don't hold out much hope for vulnerable kids, SEND or otherwise, to be protected from the incursion of the genderborg into schools & MH services.

fullscopecollaboration.org.u…

7 Nov 2024

Oh dear lord. He can't even get his Trusts safeguarding policy to comply with KCSIE 24.

1

3

6

182

15 Oct 2024

Fullscope went to Westminster! Shortlisted for an NHS Parliamentary Award for our co-created film about self-harm, Ask Me How I Am, in the mental health category. Didn't win but it was great to be there with 2 of the young people who worked with us (& 👶), and celebrate together

3

55

11 Oct 2024

𝐅𝐮𝐥𝐥𝐒𝐜𝐨𝐩𝐞 𝐅𝐫𝐞𝐞𝐥𝐚𝐧𝐜𝐞𝐫 𝐢𝐬 𝐚𝐧 𝐚𝐥𝐥-𝐢𝐧-𝐨𝐧𝐞 𝐛𝐮𝐬𝐢𝐧𝐞𝐬𝐬 𝐭𝐨𝐨𝐥 𝐈 𝐫𝐞𝐥𝐲 𝐨𝐧 𝐚𝐧𝐝 𝐭𝐫𝐮𝐬𝐭; I am delighted to have secured my yearly subscription before the price increase

@ben_fullscope @fullscopefree

#freelancer #virtualassistant

2

2

76

29 Sep 2024

Fullscope, Travis's team, freshman, not smarter than a 4th grader. Cue Tree Paine.....

3

469

29 Sep 2024

Taylor isn't dating Travis. Any BUA is for delulu fans. She's in contract w/ the Chiefs/NFL and makes big money pretending to date him and play drunk cheerleader. The 'fake doc' was sophomoric PR Stunt by Fullscope / Tree to flex and hit headlines. They're laughingstocks.

2

1

584

14 Sep 2024

No disrespect Sasha, but Fullscope is all D-list and reality TV show people. Yes, the jocks are D-list by Hollywood standards.

6

315