Seleucia _Mersin retweeted

Equality is about ensuring everyone has the tools to build their future, not just the chance to try. EquityNow EqualRights 🎉 🌺

1

1

4

PumaNFT retweeted

Jun 9

Trading alone was never the end state.

The future is connected.

One account. Every market.

Waitlist now open.

rewards.pear.trade

13,024

14,585

12,528

337,353

Cat Peterson 🇺🇸 🇺🇦🌈 retweeted

According to published reports, it looks like the Iran war only accomplished a promise of future negotiations about Iran’s nuclear program. And to think Obama had a deal about Iran’s nuclear program with on site inspections without a needless war. @realDonaldTrump is an idiot.

1

4

11

110

Hunter Prey

Hunter Prey Nanaba Scorpee retweeted

🚨🇫🇷 Manu Koné on his future: “I am focused on the World Cup. After that, we will see what happens”, told Gazzetta.

572

447

8,685

309,104

mpreg abortion☆ ς(•💋•.) retweeted

Its funny because its not impossible to fix at all. It would take ages, and we would all be dead and future generations would replace us, but its possible still. we will never see it fixed in our life time unless we found some magic cure but we could start with nuclear power

Jun 12

117

4,479

41,423

517,227

Absolutely agree, proactive security is the only way forward. Love that @quipnetwork is tackling future risks head-on with this dual-layer approach.

The power is in your hands. 🗳️

At InterLink, we believe true decentralization means giving the wheel to the people who matter most—our community.

The future staking ratio isn't being decided behind closed doors. Your voice, your vote, your future. 🌐

#InterLink #ITLG #ITL

Mugure retweeted

Study the past if you would define the future. ~ Confucius.

A reminder that remembering history is crucial for understanding where we are, and headed to in the name of Affordable Housing.

The writing was and remains on the wall. Amalize tu aende.

#RutoMustGo

31

41

1,487

Success is near. 针孔摄像头 Success is a journey.

Don’t stop until you’re proud. 探花手机 Keep faith in yourself.

The best is yet to come. 考试设备 Forget the past, focus on the future.

Stay consistent. 点盟科技 Keep climbing.

Invariant Perspective retweeted

Xi Jinping is betting China's future on a wild paradox: a hyper-innovative tech engine built on top of a collapsing domestic economy.

A definitive report by The Economist titled "China is innovative. Its economy is a mess. Which matters more?" exposes how Beijing has become completely obsessed with winning a high-tech "space race" against the United States. Driven by this fixation, billions of dollars are flooding into frontier industries like electric vehicles, advanced batteries, and artificial intelligence, with leadership treating technological self-reliance as the ultimate shield against Western containment.

But as The Economist details from reporting deep inside the provinces, outside of these glossy tech corridors, the real economy is in a structural tailspin. Local government debt is spiraling out of control, the crucial property market has imploded, and domestic consumer confidence remains stubbornly flat. These spectacular tech advances are bleeding into some rural areas, but they simply aren't generating enough broad-based productivity or income gains to rescue an entire nation choked by old-economy decay.

This unprecedented contradiction sets up a high-stakes race that will ultimately define the 21st-century global balance of power. Can a narrow corridor of brilliant engineering scale up fast enough to save the country before its massive debt and property traps drag everything down? As Beijing forces its empire to run on this volatile dual track of supreme innovation and structural mess, the rest of the world is left waiting to see which side wins out.

#ChinaEconomy #TechWar #Innovation #Macroeconomics #Geopolitics #TheEconomist

economist.com/finance-and-ec…

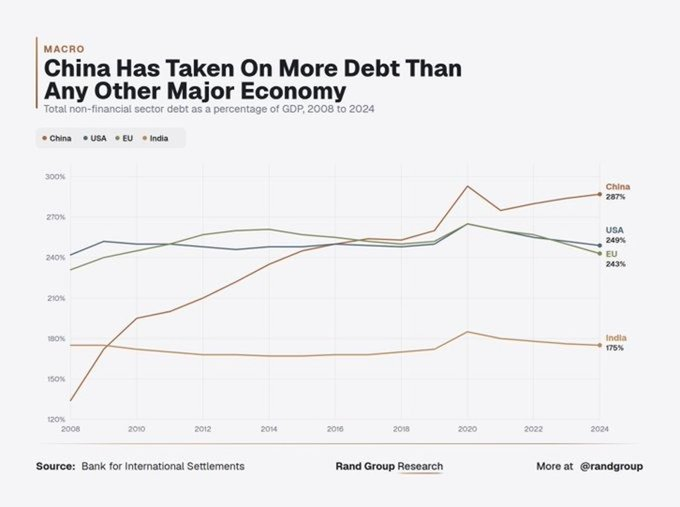

China has officially built the largest debt mountain in the developing world, and the foundation is beginning to crack. Data from the Bank for International Settlements (BIS) reveals that China's total non-financial sector debt has exploded to a staggering 287% of GDP. This hyper-acceleration completely blows past other major economies, with the United States sitting at 249%, the European Union at 243%, and India at a modest 175%. Unlike Western nations that stabilized their leverage after the 2008 financial crisis, Beijing doubled down on an aggressive, investment-led growth model that is now colliding with severe structural decay.

The true epicenter of this fiscal crisis lies within local government balance sheets. For years, regional authorities relied on relentless infrastructure and real estate expansion to artificially inflate GDP. Now, with the ongoing property market collapse and skyrocketing servicing costs, these debt-fueled investments are yielding sharply diminishing returns. This massive capital misallocation has created an unsustainable reckoning for regional banks and local authorities trapped under severe property stress.

This unprecedented leverage has triggered intense debate over China's economic trajectory. While some note that China’s heavily domestic financing structure shields it from an external currency crisis, others counter that the old playbook is completely exhausted. The economy is now choked by slowing growth, intense export pressures, and the burden of keeping insolvent entities on life support, ultimately starving the dynamic private sector of critical capital.

#ChinaEconomy #DebtCrisis #BISData #Macroeconomics #Finance #Geopolitics

3

21

56

3,225

Pabitra Sahoo🇮🇳🇮🇳 retweeted

KIIT School of Rural Management’s two-year MBA in Rural Management program is designed to develop professionals and future leaders to create meaningful impact for both organizations and rural communities. The program brings together students from diverse academic and socio-economic backgrounds, equipping them with the skills and perspective to excel in the evolving rural development landscape.

With over 60 recruiters visiting annually and competitive placement opportunities, the program serves as a gateway to specialized careers across the development sector, corporate domain, and government organizations.

Apply to us via KIITEE at kiitee.ac.in

#ksrmbbsr #RuralManagement #kiitee2026 #kiitmba

3

22

30

168

COOLADIL INC retweeted

Children are the future of any country

Chinese kids vs Indian kids

303

780

3,010

167,654

irob banks🕊️ retweeted

Jun 13

If she looking at Lord Future like that then she’s unfortunately already under his Genjutsu, we can only pray for her now.

321

3,915

50,127

1,943,826

15s

Exactly. It seems Africa had no forward thinking, which is vital for a 'future'

Africa will have 2.5 billion people by 2050. Where is all the food going to come from? Will Africa snap out of its centuries of floundering and shoulder the challenge, or will it be a chaotic, poverty trap, I wonder?

That's 85 to 90 people per square kilometer in sub-Saharan Africa compared to today, where it stands at 44 per sq km. Double trouble, perhaps.

Zambia has 2/3 rds of all fresh water in Southern Africa and land to feed millions if harnessed correctly. Zimbabwe and Mozambique, too, can produce huge variety and volume. South Africa today, though driest and least fertile off all, is the bread basket of the region due to the tenacity and skill of its current commercial farmers. Who are under permanent threat of either expropriation and / or violence and economic stresses.

There would have to be a total turnaround of political leadership and societal mindset shortly if this continent has any chance whatsoever of readying itself for the inevitable doubling of its population in the next quarter century.

Viresh Rajput retweeted

Jun 12

RWA in 2025:

"Tokenized Treasuries are the future."

RWA in 2027:

"What do you mean you don't own compute?"

55

2,765

891

9,486

Makaveli retweeted

Doc Rivers says the Spurs future is bright, but there’s no guarantees:

“I always go back to when Miami beat Oklahoma City. I remember Mike Breen saying on the air, “Well, Oklahoma City will be here every year.” It took them 20 years to get back. You know, you just can’t, you can never take things for granted. With trades, free agency, injuries, and I always use the band theories, you know, why aren’t there great bands that last forever because somebody gets jealous, somebody wants to be the man, and things change.”

(Via @stephenasmith)

62

194

2,790

496,408

TACHA🔱🇬🇭 🇳🇬 retweeted

13 Aug 2020

NOTE TO MY FUTURE ME;

I'm not you yet, but I'm trusting the PROCESS and I'm on my way 🔱🔱

•

•

#WeAreProudOfTacha

632

1,871

12,287