Simon Brown retweeted

Jun 11

MTBPS will be on 21 October 2026, and the session may start at 10am.

But whips are still discussing the early start.

1

3

7

3,536

Jun 11

Are we in that much? That we have to start early because this MTBPS will continue well into the night?

Jun 11

MTBPS will be on 21 October 2026, and the session may start at 10am.

But whips are still discussing the early start.

11

May 14

Previous Finance MECs (e.g., Lebogang Maile) have held media briefings on budgets, municipal finances, MTBPS, and state of entities, but these were typically at the Gauteng Legislature, hotels, or official venues.

No widespread reports surface of prior Finance Department media briefings specifically inside a hostel like Dube. It represents a shift towards more community-based communication on fiscal matters.

#EFFInGovernment

May 14

PICTURES| During the media briefing at Dube Hostel in Soweto, MEC of Finance @DungaLeko announced intensified interventions to address unpaid invoices, revenue leakages and financial challenges affecting municipalities and provincial departments.

#GrowingGautengTogether

2

18

91

8,199

Feb 26

STATEMENT | LATEST BUDGET BENEFITS THE BETTER-OFF, SQUEEZES THE POOR

While infrastructure spending grows modestly, it is insufficient to reverse years of underinvestment and risks further commodifying essential services through expanded public-private partnerships.

The Budget prioritises fiscal consolidation and debt metrics over employment creation, redistribution, and structural reform. Without embedding fiscal policy in a developmental macroeconomic framework, South Africa will remain trapped in stagnation, rising inequality, and unmet constitutional rights.The 2026 Budget was a chance to break with a decade of austerity and invest in transformative growth. Instead, it entrenches the status quo. Real non-interest spending declines, per capita spending falls, and critical sectors, education, healthcare and social protection, remain underfunded. Meanwhile, projected growth averages just 1.8%, locking South Africa into a low-growth, high-unemployment path.

Key concerns include: Cuts in real public spending, including declining per-learner education funding and lower per-user health expenditure than in 2019/20.

Shrinking social protection, with the SRD grant unfunded in the outer years of the MTBPS and tighter grant cancellations, despite deepening food insecurity.

Tax relief for higher-income earners, including inflation-adjusted personal income tax brackets and medical tax credits, foregoing billions that could strengthen public services.

Full statement available here

iej.org.za/press-room/statem…

Statement | Latest budget benefits the better-off, squeezes the poor - mailchi.mp/iej.org.za/statem…

9

14

1,733

Feb 25

In my world, this budget gets a 4 maybe 5/10

Excuse the grammar, am writing this on the fly

1) Budget deficit at 4.5% dropping to only 4.0% in 2026/27. I would have expected a sharper dip than this, and I need to look at the expenditure line items, but I do see they have removed the plans to increase tax rates............at least for now which detracted from the expected dip.

2) Debt/GDP rising well above our expectations of a dip, and frustrating to see a repeat of the usual adjusting the ratio higher year after year. We need to decide whether this government is genuinely serious about any fiscal consolidation

3) The fiscal anchor appears to be too loose to be useful. A "principles-based" fiscal anchor sounds like ideological claptrap and will only be announced at the MTBPS, so has no bearing on the here and now

4) Projected declines in the net borrowing requirements and the ramp up in redemptions should be welcomed, but they are just forecasts and we have to wait and see whether the current jump in the debt/GDP ratio and the disappointingly buoyant budget deficit allows for this. That said, reduced issuance is a positive and we like redemptions or paying down debt

5) budget deficits further out have been revised upwards, despite the improved tax collections, higher commodity prices and lower interest rates, implying that they I need to identify where an upward adjustment to spending is coming from

6) Commitment to spending R1.07trln is good news, but as yet we have seen no evidence in the GFCF numbers and there was no headlines on infrastructure bonds, which is a pity, because they might've been well received in the current environment. We retain a wait and see approach, to see whether Operation Vulindlela gains more traction

7) GDP growth was revised up to 1.6% for 2026 and 1.8% for 2027, which is also slightly disappointing.

8) Consolidated government expenditure is expected to grow to R2.89trln from 2,58trln in 2025/26, which represents a 12% increase over 3 years. This reflects expenditure growth above inflation, suggesting that fiscal discipline is not well anchored.

1

2

250

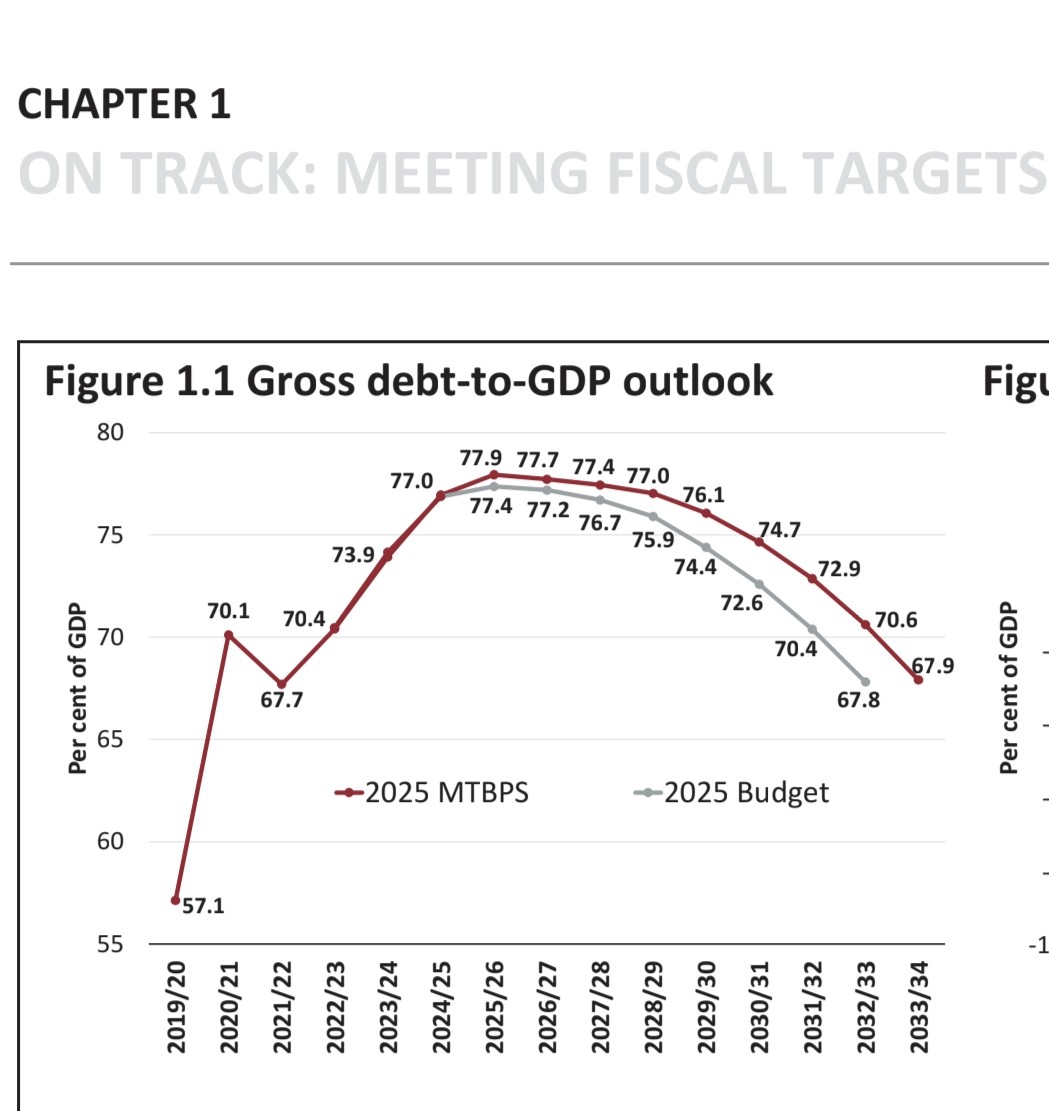

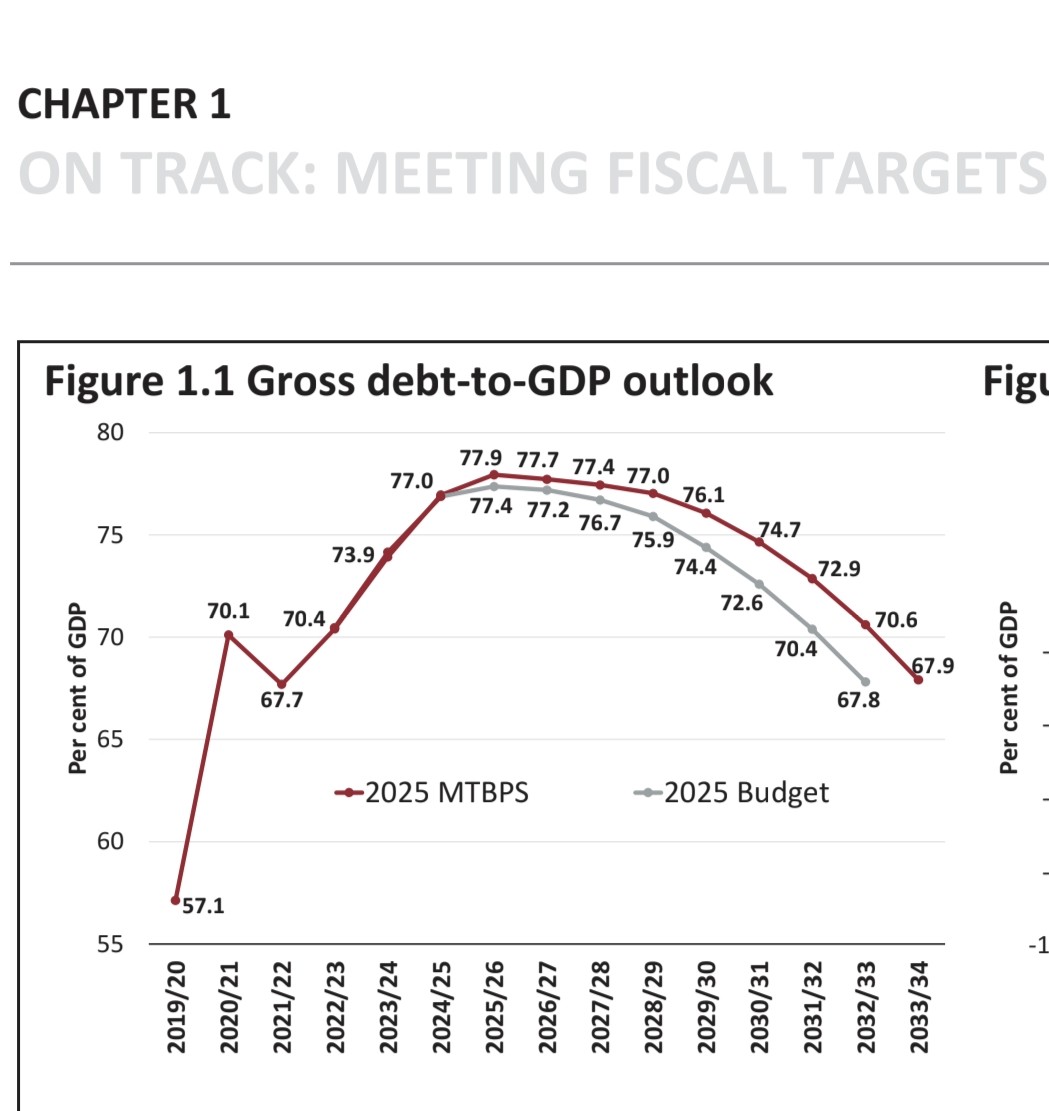

Fiscal consolidation (austerity) is failing to stabilize debt, dismally.

In 2025 budget is was 77.4%, MTBPS revised the number up to 77.9%. Now, revised up to 78.9%.

Expect debt to worsen with primary budget surplus increasing & low inflation. IT IS ECONOMICS.

#budget2026

3

11

17

700

Feb 25

SPENDING PRIORITIES

Godongwana confirms that in 2026/27, government will spend R2.67 trillion.

"This spending includes a proposed R5 billion in the contingency reserve to cater to disasters declared since the MTBPS."

#BudgetSpeech2026

323

"We are on the path of stabilizing debt". He is a pathological liar.

In budget review 2022, they forecasted debt to GDP of 70% by 2024/25. Actual came out at 77%.

In budget review 2025, they forecasted 77.4%, then MTBPS 2025 revised that up to 77.9.

🤭🤭

3

11

19

307

Feb 12

A lot of politicians have been saying 'we will look to the Budget later this month for the $$ that'll pay for #SONA2026 pledges', but @CyrilRamaphosa said we must wait till the #MTBPS in October

This should be properly communicated

1

3

500

MKP, EFF and the ANC (🤨) must reject budget review 2026:

1. It'll be a rehash of 2016 budget that missed its targets consistently.

2. MTBPS 2025 has already shown missed debt to GDP ratio, higher ave interest rates & higher share of interest payments despite primary surplus.

1

4

10

764

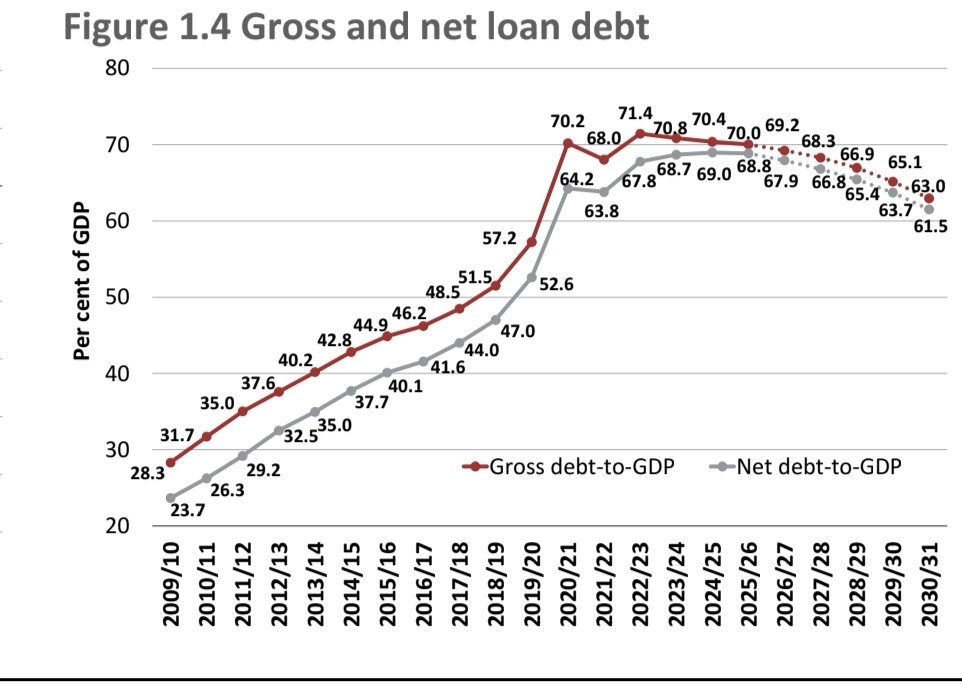

See fig 1.1 below. Ignore 2020 & 2021. NB how debt to GDP ratio rise sharply from FY23 to FY 24.

NB the gray line in FY26. In Feb 2025, NT forecasted D/GDP of 77.4%. MTBPS revised it to 77.9%.

NB this upward revision is unexplained. You can foresee the outcomes in Feb 2026. 🤨

1

3

5

220

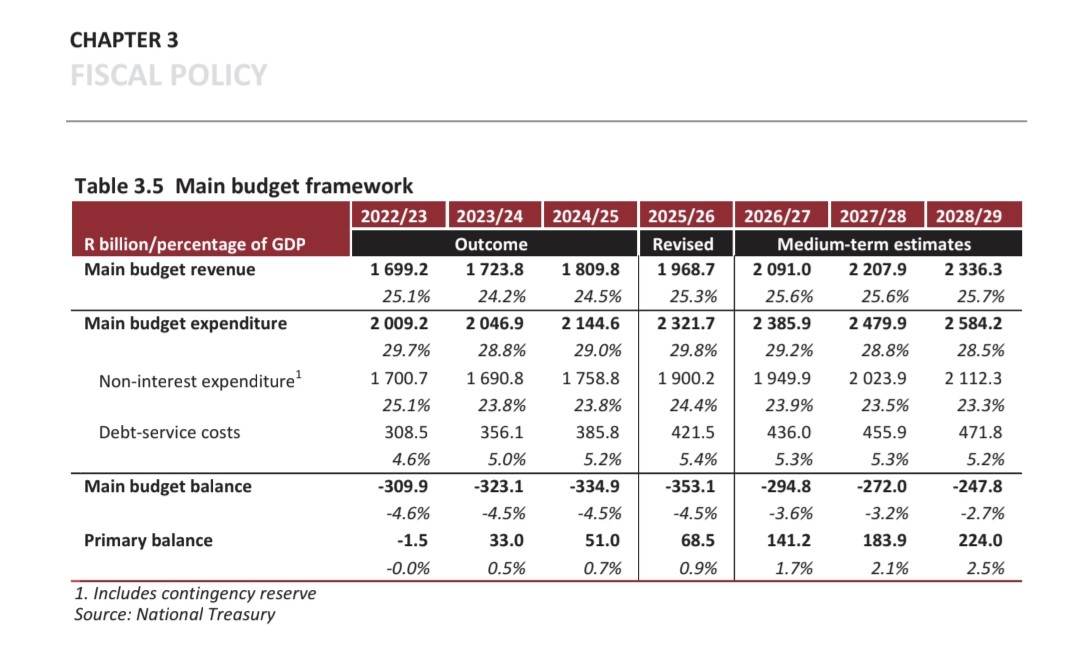

Get your calculator, let's analyze MTBPS:

Divide Debt service costs by Main Budget expenditure 4 all the years. NB how debt service costs contribution to expenditure ⬆️ as surplus ⬆️. For unexplained reasons, NT expect this fiscal policy failure to stop over the MTEF.

🧵🧵🧵

1

10

11

1,644

♦️Must Read♦️

EFF Statement on the 2025 Medium-Term Budget Policy Statement Adjustment Debates

—We vehemently reject this policy change, not only because of its complete failure to consult Parliament and society, but also because the MTBPS is irrelevant, misplaced, and fundamentally incoherent. It offers no meaningful analysis or response to global geopolitical developments that directly shape South Africa’s economic and political

reality.

This silence is particularly reckless amid escalating imperial aggression by the United States against sovereign nations such as Venezuela and Cuba through sanctions and economic warfare.

2

27

62

3,921

Jan 9

🎙️“There’s nothing that stops a bullet like a job.”

Watch as we unpack why job creation is central to tackling crime, how the 2025 MTBPS shapes SA’s future, and why the DA’s Economic Inclusion for All Bill matters.

🎥 Watch the #DApodcast here: youtu.be/VLFlOe0d6_M?si=lVXM…

1

17

43

2,382

Sjoe! The Rand Is Flying but Investors Are Leaving — What’s Really Going On? 🚀💔 ~ South Africa’s Investment Paradox: When Strong Markets Can’t Mask Weak Governance 📉⚖️ ~ The Unsigned Reform That Could Decide South Africa’s Economic Future ✍🏽⏳

Sjoe! There are moments when even the most optimistic South African stops, looks around, and lets out a quiet, exhausted "Sjoe!" – that word we use when surprise, admiration, shock, and relief all collide at once. In 2025, the rand ended the year up ~12-13%, closing around ~16.66-16.68 ZAR/USD, the JSE All Share Index climbed ~30.28% to 113,938 by mid-December, and headlines cheered a "resurgent economy" under the Government of National Unity.

Yet foreign direct investment limped along at $5.2-6 billion for the third straight year, Africa attracted $97 billion in 2024 while we watched from the sidelines, and seven major international companies – from IG Group to Norton Rose Fulbright – either packed up entirely or dramatically scaled back. Meanwhile, Transalloys, the country's last manganese smelter, announced it might cut 600 jobs because electricity costs twice as much as in competing nations, leaving only two of five furnaces running.

This is the paradox at the heart of South Africa today: A land blessed with ~75% of the world's manganese reserves, vast platinum wealth, a sophisticated financial system, and 63.96 million resilient people, yet trapped in a cycle where internal governance failures and external pressures drive capital away and industries to the brink.

The central claim is straightforward but painful: Cadre deployment's corrosive legacy – the ANC's system of placing loyalists in key public roles – remains the primary structural barrier to investment, compounded by corruption, energy crises, crime, policy uncertainty, and global competition.

President Ramaphosa's reform agenda, symbolized by the Public Service Amendment Bill passed by Parliament on December 3, 2025, but still unsigned as of early 2026, represents a potential turning point – a gamble that could professionalise the public service or, if delayed further, deepen the stagnation.

To prove this, we build a network of cumulative evidence from economics (IMF growth forecasts at 1.3%, debt-to-GDP projections at 78.4% for 2025/26), history (Zondo Commission's R500 billion state capture findings), geopolitics (Chinese steel dumping with ~116 million tons exported annualized, Trump's 30% tariffs), and social sciences (68.1% poverty rate, World Bank 2025; unemployment at 31.9% in Q3 2025, Stats SA).

These fields converge on a falsifiable truth: If the bill is signed and implemented with merit-based hiring, FDI and growth could rise; persistent delays or weak enforcement will see more exits and crises like Transalloys.

Like a beloved old bakkie that still turns heads but struggles to climb the hill because the engine's clogged with years of bad fuel, South Africa has the bodywork to impress – but the internals need urgent attention.

Stirring Questions:

How can a nation with such natural wealth and financial sophistication raise the alarm when FDI remains so stubbornly low?

If the rand's gains are partly global (USD weakness from Fed cuts), why do some stories focus only on local triumphs?

With the Public Service Amendment Bill unsigned into 2026, how might further delays compound the risks already driving company exits?

These questions matter together because they shift from passive observation to active scrutiny, reminding South Africans that the story of our economy is not just numbers on a screen, but choices that affect every family table.

Context

To understand the paradox, start with the essentials. Cadre deployment is the ANC's long-standing practice – informal from 1994, formalized at the 1997 Mafikeng Conference – of appointing party loyalists to public positions to advance transformation goals. It successfully increased black representation in state-owned enterprises from 10% in 1994 to 60% by 2025 (Politicsweb, 2025), aiming to align governance with liberation ideals like social grants for 18 million citizens.

Corruption, as defined by Transparency International, is the abuse of power for private gain, seen in irregular expenditures and the R500 billion lost to state capture (Zondo Commission, 2022). The issue is profound: In a population of 63.96 million (IMF, 2025), these intertwined systems contribute to FDI stagnation at $5.2-6 billion annually (2023-2025), while Africa attracted $97 billion in 2024 (UNCTAD, 2025).

Views differ: Supporters see cadreism as essential redress; critics view it as patronage enabling inefficiency (R520 billion SOE bailouts since 2010, National Treasury, 2025). Neutral analyses note debt servicing at R385.6 billion (~16% of R2.4 trillion budget) and growth at 1.3% barely outpacing population (IMF, 2025).

For ordinary people, it's lived reality: Unemployment at 31.9% in Q3 2025 (Stats SA, 2025), poverty at 68.1% (World Bank, 2025), Gini 0.63 (Statista, 2025), crime with safety index rank 145th (25.4 score, Numbeo, 2025) and ~70% assaults unreported (Stats SA, 2025). External pressures like Chinese dumping and US tariffs add weight. The unsigned Public Service Amendment Bill – intended to limit political interference in appointments – sits as a symbol of hesitation.

Stirring Questions:

Why does a system designed for equity raise concerns when poverty remains at 68.1%?

If cadreism's benefits are assumed without testing alternatives, what hybrid models could balance transformation and competence?

With global competition intensifying, how do domestic delays risk further marginalisation?

These questions are important collectively because they connect policy to people, turning abstract debates into urgent calls for change that honour both history and future.

Evidence Network

Economic Evidence: The Quiet Erosion of Prosperity

Economics provides the stark ledger: South Africa's per capita GDP contracted -0.3% in 2025 – the only country globally (IMF, October 2025), with real household incomes down 15-18% since 2010, equating to R5,000-9,000 less annually per person (SARB, 2025). Debt servicing consumes R385.6 billion (~16% of R2.4 trillion budget), crowding out social spending amid 78.4% debt-to-GDP projections for 2025/26 (National Treasury, 2025). FDI remains $5.2-6 billion, far from regional peers (UNCTAD, 2025).

Cadre-linked inefficiencies in SOEs demand R520 billion bailouts since 2010, while energy crises cost ~R100-150 billion in 2025 (down from R300 billion peaks, FTI Consulting/MKRI, 2025). This deters investors (governance top risk, EY/RMB surveys), fueling offshore flows ~14-20% up in 2025 (ASISA, 2025).

Picture a household budget stretched thin: Grants erode in value while bailouts drain the pot. Some may try to point to international pressures: Africa's surge isolates local factors. This economic strain flows into history's legacy.

Historical Evidence: From Liberation Tool to Entrenched Burden

History traces cadreism's journey: Emerging post-1994 to break apartheid's hold, formalized 1997 for "revolutionary discipline" (ANC, 1997), it boosted equity (black SOE roles from 10% to 60%). But Zuma's era (2009-2018) weaponized it for R500 billion capture, debt from 27% to 53% GDP (Zondo Commission, 2022). Ramaphosa's renewal promised change, but irregularities persist (~30% audited entities, ~R87 billion municipal values 2021-2024, AGSA, 2025).

This legacy repels FDI, with "lost decade" 0.8% growth forgoing R800 billion taxes (Investec estimates, 2025). Like a bridge built strong but weakened by poor maintenance, early gains sour. Some claim equity justifies – but stagnant poverty (68.1%) disproves.

Geopolitical Evidence: The World Knocking at a Fragile Door

Geopolitics compounds the strain: China's 15-25% steel undercuts (~116 million tons exported annualized) swell deficits (~R20 billion steel, ~R162 billion overall first 10 months 2025, SARS/ITAC, 2025), while Trump's 30% tariffs since August 2025 disrupt (Reuters, 2025). BRICS Rio's 126 commitments (July 2025) contrast 90% Chinese FOCAC contracts (Carnegie, 2025).

Intersecting cadre inefficiencies, these make beneficiation unviable (Transalloys 2/5 furnaces, 600 jobs threatened; Glencore/Samancor cuts). Like neighbors borrowing tools but returning broken, alliances strain. Some may refute "win-win": Defaults elsewhere expose risks.

Social Evidence: The Human Faces Behind the Figures

Social data humanizes: Unemployment 31.9% Q3 2025 (Stats SA, 2025), poverty 68.1% (World Bank, 2025), Gini 0.63 (Statista, 2025), crime index 5th highest (74.6 score, Numbeo, 2025), ~70% assaults unreported (Stats SA, 2025).

Synthesis

The evidence—from economic erosion (IMF/SARB, 2025), historical devolution (Zondo, 2022), geopolitical strains (ITAC/Carnegie, 2025), social scars (World Bank/Stats SA, 2025)—coalesces: Cadreism's legacy, unsigned reforms, and compounded pressures chain potential. Consilience strong: Sources align on falsifiable path—if bill signed/enforced, merit gains; delays perpetuate exits/crises.

Envision breakthrough: Ramaphosa signs, heads hire on skill—SOEs stabilize, power costs negotiated, beneficiation revives. Step by step: Pilots blend equity/merit; poverty eases, FDI flows. It is a vision of renewed institutions—renewal.

Objections

Cadreism essential for transformation—empathize with redress fears, but hybrids achieve equity with growth (IMF comparisons).

Globals dominate—fair, but Africa's surge isolates internals (UNCTAD, 2025).

Delays political necessity—valid GNU binds, but urgency outweighs (CDE, 2025).

Conclusion

The evidence network proves cadreism and corruption, compounded by delays and pressures, drive South Africa's investment paradox, with the unsigned bill pivotal. South Africans, demand signature, scrutiny, merit—forge renewal. What if decisive step ignites surge? The evidence network proves cadreism's legacy and reform delays perpetuate South Africa's FDI stagnation and industry crises with undeniable evidence.

#SjoeNews 😮🗞️

#SjoeEconomy 😵💫💰

#UnsignedAndUnbothered ✍🏽🙃

#FDIWhereAreYou 👀💸

#CadreChaos 🎭🔥

#RainbowNationRealityCheck 🌈⚠️

#MarketsUpJobsDown 📈⬇️

#PowerCutsAndPolicyCuts ⚡📄

#GovernanceGoneWild 🤯🏛️

#EconomicEish 😬💥

#StillWaitingForReform ⏳😩

#SouthAfricaPlotTwist 🇿🇦🎬

#SjoeButMakeItSerious 😮📉

#InvestmentParadoxUnlocked 🔓💸

References (APA style)

African National Congress. (1997). Mafikeng conference resolutions. ANC.

Auditor-General of South Africa. (2025). Annual audit reports. AGSA.

Carnegie Endowment for International Peace. (2025). BRICS and FOCAC analysis. Carnegie.

Centre for Development and Enterprise. (2025). Unemployment catastrophe. CDE.

International Monetary Fund. (2025). World economic outlook. IMF.

International Trade Administration Commission. (2025). Steel dumping finding. ITAC.

National Treasury. (2025). Budget/MTBPS. National Treasury.

Numbeo. (2025). Crime/safety index. Numbeo.

Parliament of South Africa. (2025). Bills tracker. Parliament.

Politicsweb. (2025). SOE statistics. Politicsweb.

Reuters. (2025). Tariff/exit reports. Reuters.

South African Reserve Bank. (2025). Estimates. SARB.

Statistics South Africa. (2025). Labour/crime data. Stats SA.

Statista. (2025). Gini/debt. Statista.

United Nations Conference on Trade and Development. (2025). Investment report. UNCTAD.

World Bank. (2025). Poverty reports. World Bank.

Zondo Commission. (2022). State capture report. Judicial Commission.

1

1

2

1,519