el mundo si sería hermoso si muse hiciera ub remake de showbiz y origin of simmetry pero con screams

Jun 14

such an ugly world

such a beautiful world

31

World chat

Ho conosciuto tante persone lituane portoghesi russe e serbe con le quali ci siamo scambiati lettere ed anche regali 😅

Da Mosca ho ricevuto cioccolata

Una sciarpa del CSKA mosca che ancora conservo.

E il CD dei Muse

Origin of simmetry😘

Che ancora adoro

29

te amo mi flaco hermoso hoy me emborracho en origin of simmetry por vos

4

70

Do not blame yourself… the “David” show perfection of forms and simmetry… in reiassance, the genital dimension are kept smaller to keep the Vatican quiet… anyway, Italian reinassance give to the world, art, crafts, architecture, poetry, and a culture that make history around the world… have large genitals and low IQ, never left a mark in history.

5

4,659

May 24

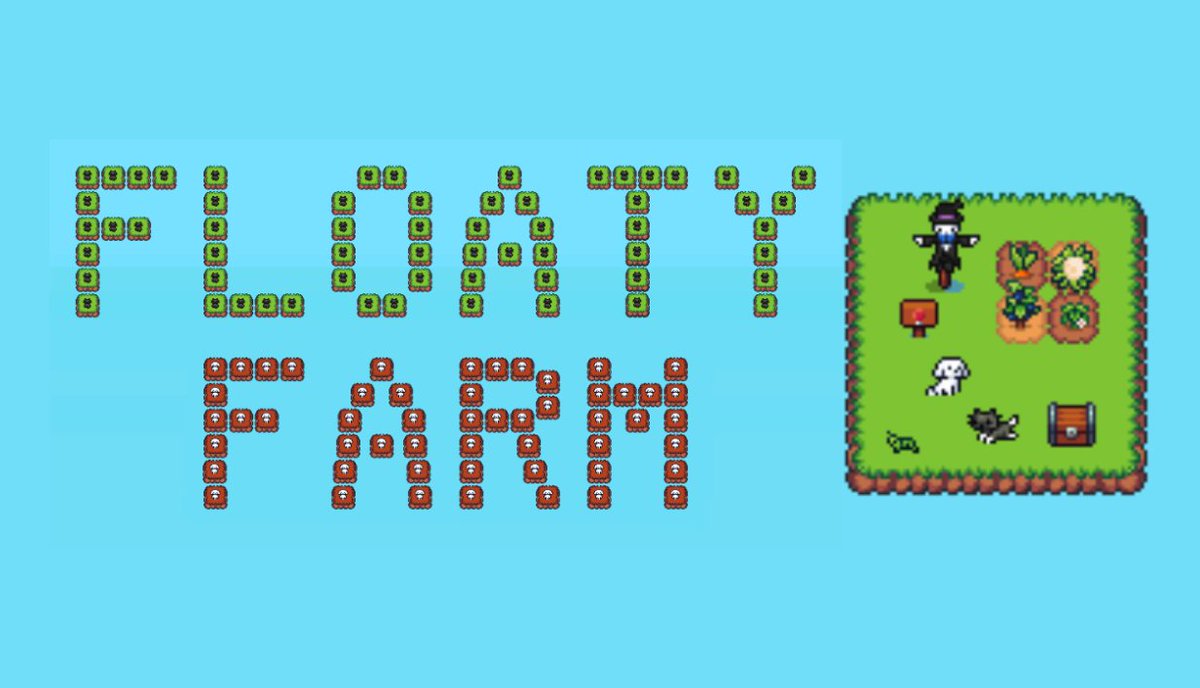

I believe you don't need to have the most stylized art for the Steam capsule, is better to represent the game in it.

That's why I like the one I made for Floaty Farm, it reflects the pixel art, simmetry and simplicity of the game.

4

1,019

MUSE regresa al Dramatismo Espacial con 'HEXAGONS'! 💫

¡Ya disponible en plataformas digitales! ✅

🔹Spotify: goo.su/fYYjXcY

🔹Apple Music: goo.su/JAAax

🔹Amazon Music: goo.su/cYFkk

🔹Deezer: goo.su/Ngk6e

🔹TIDAL: goo.su/ukLzX

🔹YouTube: goo.su/J6h9Y

Este cuarto tema de su nuevo nuevo álbum, 'The WOW! SIGNAL', trae de regreso a un Muse más 'Old School', con una atmósfera espacial que nos transporta 25 años atrás, a la era de su álbum 'Origin Of Simmetry'. 💥

¿Qué les ha parecido? 👀

-

#museband

5

3

31

711

May 19

Face simmetry is unreal 🔥🥰 #CharlieFleming

May 19

Metro Style Magazine Picks the Filipina Actresses Poised for Stardom.

Fyang Smith

Kai Montinola

Ashtine Olviga

Caprice Cayetano

Carmelle Collado

Bianca De Vera

Krystal Mejes

Hyacinth Callado

Charlie Fleming

Lella Ford

1

8

43

2,053

May 14

There's no simmetry, indeed: @idf terrorists have killed many more innocent civilians than Hamas ever did.

And everyone knows it.

Today I instructed my legal advisers to consider the harshest legal action against The New York Times and Nicholas Kristof.

They defamed the soldiers of Israel and perpetuated a blood libel about rape, trying to create a false symmetry between the genocidal terrorists of Hamas and Israel’s valiant soldiers.

Under my leadership, Israel will not be silent.

We will fight these lies in the court of public opinion and in the court of law.

Truth will prevail.

1

17

113

2,075

May 12

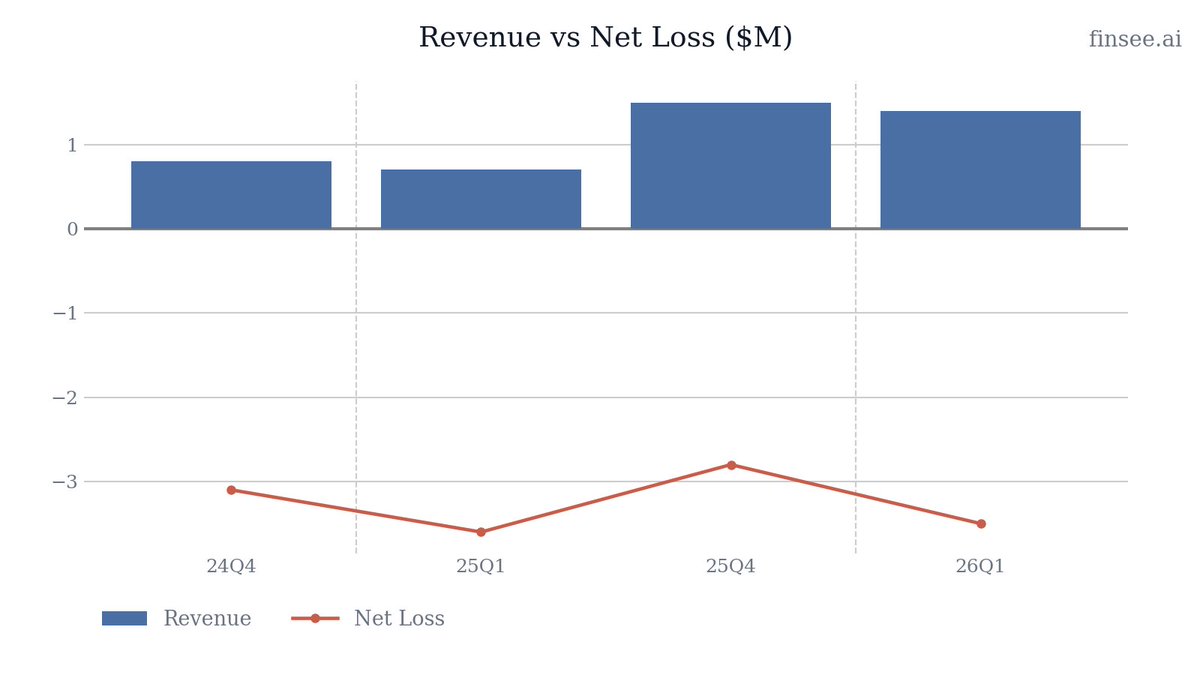

$TNON Q1 2026 earnings: YoY Growth Remains Strong, But Sequential Momentum Stalls

Tenon Medical reported strong year-over-year progress with Q1 2026 revenue surging 90% to $1.4 million and gross margins expanding 24 percentage points to 68.5%. However, beneath the bullish YoY narrative, sequential momentum has stalled. Revenue dipped slightly from Q4 2025's $1.5 million, and operating expenses crept back up to $4.2 million. This combination widened the net loss sequentially to $3.5 million. The company successfully closed a $4.3 million convertible note to extend its cash runway, but the lack of formal forward guidance and the sequential revenue deceleration raise questions about the immediate adoption curve of the newly launched SImmetry system.

Full article with charts - link in bio

🐂 𝐁𝐮𝐥𝐥 𝐂𝐚𝐬𝐞

• 𝐌𝐚𝐫𝐠𝐢𝐧 𝐏𝐫𝐨𝐟𝐢𝐥𝐞 𝐏𝐫𝐨𝐯𝐞𝐬 𝐎𝐩𝐞𝐫𝐚𝐭𝐢𝐧𝐠 𝐋𝐞𝐯𝐞𝐫𝐚𝐠𝐞 — Gross margin reached an impressive 68.5% (up from 44.5% a year ago), demonstrating that Tenon's manufacturing base can achieve highly profitable unit economics as production volume overhead is absorbed.

• 𝐃𝐮𝐚𝐥-𝐏𝐥𝐚𝐭𝐟𝐨𝐫𝐦 𝐒𝐭𝐫𝐚𝐭𝐞𝐠𝐲 𝐄𝐱𝐞𝐜𝐮𝐭𝐢𝐧𝐠 — The successful integration of the SImmetry system alongside the flagship Catamaran system is successfully transforming Tenon into a multi-solution provider, expanding its total addressable market to include lateral approach procedures.

🐻 𝐁𝐞𝐚𝐫 𝐂𝐚𝐬𝐞

• 𝐒𝐞𝐪𝐮𝐞𝐧𝐭𝐢𝐚𝐥 𝐃𝐞𝐜𝐞𝐥𝐞𝐫𝐚𝐭𝐢𝐨𝐧 — Despite management's optimism surrounding the SImmetry rollout, Q1 2026 revenue of $1.4M was a step backward from the $1.5M achieved in Q4 2025, suggesting a potentially choppy adoption curve.

• 𝐏𝐞𝐫𝐬𝐢𝐬𝐭𝐞𝐧𝐭 𝐂𝐚𝐬𝐡 𝐁𝐮𝐫𝐧 𝐑𝐞𝐪𝐮𝐢𝐫𝐞𝐬 𝐃𝐞𝐛𝐭 — With Q1 net losses expanding sequentially to $3.5M, the company was forced to introduce $3.5M in convertible note liabilities to the balance sheet, generating $176K in new interest expense for the quarter.

⚖️ 𝐕𝐞𝐫𝐝𝐢𝐜𝐭: ⚪

Neutral. While YoY metrics look spectacular on a percentage basis, the absolute dollar figures reveal a business that has temporarily plateaued sequentially while expenses continue to outpace gross profit by a significant margin.

𝐊𝐞𝐲 𝐓𝐡𝐞𝐦𝐞𝐬

🟢 𝐏𝐨𝐫𝐭𝐟𝐨𝐥𝐢𝐨 𝐄𝐱𝐩𝐚𝐧𝐬𝐢𝐨𝐧 𝐭𝐨 𝐌𝐮𝐥𝐭𝐢-𝐀𝐩𝐩𝐫𝐨𝐚𝐜𝐡 𝐂𝐚𝐩𝐚𝐛𝐢𝐥𝐢𝐭𝐢𝐞𝐬

The addition of the SImmetry SI Joint Fusion System is a critical growth catalyst. By offering both lateral (SImmetry ) and inferior-posterior (Catamaran) surgical approaches, the sales team can now cater to a much broader range of surgeon preferences, removing a key historical bottleneck to adoption.

🟢 𝐆𝐫𝐨𝐬𝐬 𝐌𝐚𝐫𝐠𝐢𝐧 𝐒𝐭𝐚𝐛𝐢𝐥𝐢𝐳𝐚𝐭𝐢𝐨𝐧 [NEW]

Gross margins are stabilizing near the 70% threshold. At 68.5% in Q1 2026, up 24 points YoY, the company is proving its thesis that higher top-line revenue will quickly absorb fixed production overhead. If revenue growth resumes, gross profit flow-through will be substantial.

⚪ 𝐀𝐠𝐠𝐫𝐞𝐬𝐬𝐢𝐯𝐞 𝐏𝐡𝐲𝐬𝐢𝐜𝐢𝐚𝐧 𝐓𝐫𝐚𝐢𝐧𝐢𝐧𝐠 𝐚𝐧𝐝 𝐂𝐞𝐧𝐭𝐞𝐫 𝐨𝐟 𝐄𝐱𝐜𝐞𝐥𝐥𝐞𝐧𝐜𝐞

Adoption is directly correlated to training. Tenon hosted 21 physicians in targeted sessions in Q1 (following 24 in Q4 2025) and recently opened a new Center of Excellence Training Center in Tampa, FL, to accelerate onboarding in the Eastern Region.

🔴 𝐒𝐞𝐪𝐮𝐞𝐧𝐭𝐢𝐚𝐥 𝐑𝐞𝐯𝐞𝐧𝐮𝐞 𝐂𝐨𝐧𝐭𝐫𝐚𝐝𝐢𝐜𝐭𝐬 𝐆𝐫𝐨𝐰𝐭𝐡 𝐍𝐚𝐫𝐫𝐚𝐭𝐢𝐯𝐞 [NEW]

Management cites 'early returns on the strategy' and 'commercial momentum,' yet revenue fell from $1.5M in Q4 2025 to $1.4M in Q1 2026. If the SImmetry alpha launch 'exceeded all expectations' in Q4, the lack of sequential top-line growth in Q1 raises red flags about seasonality or plateauing utilization among early adopters.

🔴 𝐎𝐩𝐞𝐫𝐚𝐭𝐢𝐧𝐠 𝐄𝐱𝐩𝐞𝐧𝐬𝐞 𝐂𝐫𝐞𝐞𝐩 [NEW]

During the Q4 call, management suggested the $3.9M OpEx level was a 'good baseline' for modeling. However, Q1 2026 OpEx immediately jumped to $4.2M, driven largely by Sales & Marketing expenses ($1.86M) to support the SImmetry rollout. This operating deleverage widened the net loss sequentially.

🔴 𝐋𝐚𝐜𝐤 𝐨𝐟 𝐅𝐨𝐫𝐰𝐚𝐫𝐝 𝐆𝐮𝐢𝐝𝐚𝐧𝐜𝐞

Management continues to withhold specific revenue or margin guidance for the fiscal year. Given the early stage of commercialization, the lack of management commitments leaves investors blind to expected cash burn and run-rate projections for the remainder of 2026.

🟢 𝐅𝐨𝐫𝐭𝐢𝐟𝐢𝐜𝐚𝐭𝐢𝐨𝐧 𝐨𝐟 𝐈𝐧𝐭𝐞𝐥𝐥𝐞𝐜𝐭𝐮𝐚𝐥 𝐏𝐫𝐨𝐩𝐞𝐫𝐭𝐲 [NEW]

Tenon secured multiple Notices of Allowance from the USPTO in Q1, further defending its technology stack. The portfolio now boasts 29 issued U. S. patents and 9 international patents, providing a deep protective moat around both the Catamaran and SImmetry architectures against larger orthopedic competitors.

𝐎𝐭𝐡𝐞𝐫 𝐊𝐏𝐈𝐬

𝐂𝐚𝐬𝐡 𝐚𝐧𝐝 𝐂𝐚𝐬𝐡 𝐄𝐪𝐮𝐢𝐯𝐚𝐥𝐞𝐧𝐭𝐬: $4.6 million

Up from $3.8M at year-end 2025. This increase was purely driven by the $4.3M gross proceeds from the senior convertible note private placement in March 2026. Without this financing, the company would have ended the quarter critically low on cash.

𝐈𝐧𝐭𝐞𝐫𝐞𝐬𝐭 𝐄𝐱𝐩𝐞𝐧𝐬𝐞: $176,000

Reversing from zero. The company operated entirely debt-free at the end of 2025. The introduction of the convertible note now saddles the P&L with interest expenses, a new headwind for achieving net profitability.

𝐒𝐚𝐥𝐞𝐬 𝐚𝐧𝐝 𝐌𝐚𝐫𝐤𝐞𝐭𝐢𝐧𝐠 𝐄𝐱𝐩𝐞𝐧𝐬𝐞: $1.86 million

Accelerating. S&M increased from $1.65M in Q1 2025 to $1.86M in Q1 2026. This reflects the aggressive commercial expansion, new hires in the Eastern Region, and the costs associated with the SImmetry launch.

𝐊𝐞𝐲 𝐐𝐮𝐞𝐬𝐭𝐢𝐨𝐧𝐬

𝐒𝐞𝐪𝐮𝐞𝐧𝐭𝐢𝐚𝐥 𝐑𝐞𝐯𝐞𝐧𝐮𝐞 𝐃𝐢𝐬𝐜𝐨𝐧𝐧𝐞𝐜𝐭

With the full commercial integration of SImmetry and the addition of 21 newly trained physicians in Q1, why did top-line revenue decline sequentially from $1.5M in Q4 2025 to $1.4M in Q1 2026?

𝐎𝐩𝐞𝐫𝐚𝐭𝐢𝐧𝐠 𝐄𝐱𝐩𝐞𝐧𝐬𝐞 𝐓𝐫𝐚𝐣𝐞𝐜𝐭𝐨𝐫𝐲

Management previously noted Q4's $3.9M OpEx as a solid baseline for 2026, yet Q1 came in at $4.2M. Should investors view $4.2M as the new quarterly floor as Eastern Region sales leadership expands?

𝐂𝐨𝐧𝐯𝐞𝐫𝐭𝐢𝐛𝐥𝐞 𝐍𝐨𝐭𝐞 𝐃𝐲𝐧𝐚𝐦𝐢𝐜𝐬

Can you provide more color on the conversion terms of the new $4.3M senior notes, and what metrics would trigger conversion versus repayment?

1

2

489

Apr 24

THE SIMMETRY, THE REPETITION OF SHAPES AND JUMPS FROM LIGHT TO SHADE The name Atrani comes from the Latin word atrum, which means rocky place, gloomy. campanica.blogspot.com/2026/…

----

#AmalfiCoast #Atrani #village

1

2

39

Apr 8

Showbiz:

Origin of Simmetry:

Absolution:

Black Holes:

The Resistance:

The 2nd Law:

Drones:

Simulation Theory:

Will of The People:

🚨 POLÊMICA

Pra você 🫵 qual a pior música de cada álbum do Muse? Vamos todos julgar o gosto alheio!!

Abaixo a escolha dos adms:

2

2

118

Apr 4

There is no doubt.

The beautiul face, the... simmetry.

Perfection

3

1

155

14,439

Apr 1

i made editable the simmetry of the head and a the other side of the pose morph doesnt work

i also made editable the hypernurbs and now i got weird polygons

PLEASE HELP😖

2

4

24

848

I love your body it's perfect and with well simmetry

3

114