A global leader in crowdsourced U.S. investment research, powered by one of the largest and most vibrant investor communities.

Joined March 2009

- Tweets 1,080,624

- Following 231

- Followers 331,745

- Likes 3,762

825 Photos and videos

Jun 12

Geopolitical raw material supply chains are re-weighting semiconductor valuations. AXT Inc. $AXTI advanced 10% today following reports of potential Chinese export restrictions on indium phosphide, a vital compound for optical data center interconnects.

THE CRITICAL SUBSTRATE CRUNCH:

GEOPOLITICAL EDGE: AXT utilizes a highly specialized, vertically integrated supply chain, holding strategic stakes in Chinese raw material firms to safeguard essential wafer production inputs.

BULLISH PRICE TARGETS: Wedbush analysts models massive potential trade tailwinds, reiterating an OUTPERFORM rating and an aggressive $93 price target.

PRICING POWER CONTEXT: Wedbush highlights that any acceleration in export license approvals or a spike in wafer spot market pricing could drive substantial consensus revenue estimate upgrades.

QUANT PERFORMANCE: Balancing structural supply chain risks against near-term commodity tailwinds, Seeking Alpha's automated scoring systems flag the stock as a steady HOLD.

By holding integrated supplier assets directly inside China's processing perimeter, AXT is positioning its high-purity wafer output as a vital bottleneck for the high-bandwidth optical computing landscape.

With Wedbush setting a $93 price target on AXT following potential Chinese export caps on indium phosphide, do you think $AXTI's local supplier model will shelter it or expose it to more friction?

1

2

4

4,115

Jun 12

Even an emphatic top-and-bottom-line earnings beat isn't enough to calm nervous software investors during executive handoffs. Adobe $ADBE shares slid over 6% today following its fiscal Q2 print.

THE STRONG FUNDAMENTALS VS. LEADERSHIP DISCONNECT:

THE DEMAND ENGINE: Quarterly revenue grew 13% year-over-year to $6.62 billion, beating out consensus models thanks to sticky, high-margin enterprise AI adoption.

THE OUTLOOK LIFT: Management confidently hoisted its full-year earnings target, projecting an updated full-year revenue midpoint of $26.55 billion and robust EPS guidance of $24.45.

THE SURPRISE EXIT: Capital momentum faced immediate friction as the company announced the sudden departure of CFO Dan Durn. Executive Steve Day will temporarily take the financial reins as interim CFO.

QUANT PERFORMANCE: Disregarding the leadership noise to focus on underlying structural growth, Seeking Alpha’s automated systems rate $ADBE a firm BUY on elite profitability marks.

By clearing financial targets while navigating vital leadership realignments, Adobe is working to stabilize its operational base as AI monetization goes mainstream.

With Adobe falling 6% on its CFO exit despite raising its full-year revenue target to $26.55B, does this leadership shuffle create a buying opportunity or do you expect more volatility ahead?

2

9

4,385

Jun 12

Want stock price growth but refuse to give up your dividend income? 📈💰

Nicole Benjamin and Steven Cress break down the ultimate dual-threat strategy for long-term investors: the newly launched Quant Growth & Income Portfolio (QGI).

The QGI Playbook:

- 🎯 The Dual Focus: Explicitly engineered for investors who refuse to choose between capital appreciation and strong dividend yields.

- 🛡️ The Dividend Guardrail: Proprietary safety algorithms actively look for dividend consistency and growth metrics to completely avoid yield traps.

- ⚙️ Proven Core Engine: Powered by the exact same quantitative system that drives AlphaPix, now optimized to isolate high-conviction dividend payers.

Steven’s Take: "If anyone is interested in both income and capital appreciation, this would be the product for them."

🔻Read the full article below

#DividendInvesting #PassiveIncome #StockMarket #QuantStrategies #QGI #SeekingAlpha

2

1

4

4,060

Jun 12

3

2,686

Jun 11

The enterprise software layer is redefining how corporations monetize artificial intelligence. Palantir $PLTR CEO Alex Karp warns that enterprise clients are growing increasingly dissatisfied with raw frontier AI labs over excessive token consumption.

THE DEEP INTEGRATION PLAYBOOK:

THE MODEL FRUSTRATION: As developers like OpenAI and Anthropic gear up for high-profile public market debuts, Karp highlights a growing corporate pushback against simple, token-heavy chat interfaces.

WORKFLOW OVER LLMS: The enterprise thesis hinges on deep system integration. True business optimization requires wiring intelligence directly into legacy data pipelines and concrete operational workflows.

SCALE & MOMENTUM: Commanding a massive market capitalization that clears $312 billion, Palantir is leveraging its structural first-mover advantage to capture long-term enterprise software market share.

QUANT PERFORMANCE: Fueled by accelerating customer counts and aggressive commercial AIP adoption, Seeking Alpha's automated data flags the core stock as a definitive BUY.

By moving past the chatbot hype cycle to build the foundational architecture of corporate AI execution, Palantir is cementing an unassailable data moat.

With Alex Karp pointing out major corporate frustration with token-heavy AI models, do you think $PLTR's enterprise workflow integration gives it a permanent edge as foundation labs head to the public markets?

3

1

7

3,166

Jun 11

The structural narrative around custom chip fabrication is experiencing a massive shift. Intel $INTC advanced 6% today after Bank of America rolled out a rare post-earnings double upgrade to a conviction BUY.

THE ARCHITECTURAL MOAT EXPANSION:

THE RE-RATING: Shifting all the way from Underperform to Buy, BofA analyst Vivek Arya aggressively hoisted his price target to $135 from $96.

THE ENGINE: The turnaround thesis hinges on robust enterprise demand for high-density advanced packaging services and the deployment of localized, agentic AI-capable desktop and server CPUs.

EARNINGS EXPANSION: BofA models Intel's baseline structural earnings power surging to $6 per share over the multi-year cycle, vastly out-pacing the Street’s cautious $3 to $4 estimates.

QUANT PERFORMANCE: Reflecting immediate operational friction across the foundry buildout timeline, Seeking Alpha's automated scoring systems maintain a steady HOLD.

By scaling up commercial packaging capacity underneath next-gen device cycles, Intel is attempting to capture premium market share as the compute landscape decentralizes.

With Bank of America issuing a rare double upgrade on Intel to $135, do you think $INTC has officially cleared its operational cyclical bottom or are the foundry execution risks still too high?

6

2,941

Jun 11

Massive capital deployment plans are introducing near-term turbulence for cloud architecture leaders. Oracle $ORCL shares tumbled 12% following its post-earnings print, logging its steepest single-day selloff since late 2025.

THE PRICE VOLATILITY VS. COMPUTE INSULATION:

THE CAPEX SHOCK: Market participants reacted negatively to management's bold $95 billion capital expenditure layout mapped for FY2027, sparking short-term debt and liquidity concerns.

THE SALES ACCELERATION: Despite the market pullback, underlying demand indicators are hitting record numbers. Oracle’s total sales backlog exploded by an incredible $85 billion sequentially.

PREPAYMENT SHIELD: Mitigating core balance sheet funding friction, the software pioneer has already secured over $25 billion in liquid upfront cash prepayments from corporate hyperscale clients.

QUANT PERFORMANCE: Prioritizing unyielding enterprise demand for infrastructure clusters over immediate infrastructure deployment costs, Seeking Alpha's automated data rates $ORCL a firm BUY.

By using aggressive near-term leverage to build out data center capacity, Oracle is betting that locking in long-term AI training workloads will yield supreme equity returns over the decade.

With Oracle's $85B backlog growth keeping its Buy rating intact despite a 12% stock drop on CapEx fears, do you think the infrastructure spend is a smart long-term land grab or an expensive risk?

1

2

10

3,271

Jun 11

The capital intensity of the artificial intelligence server boom is hitting an unprecedented scale. Super Micro Computer $SMCI has officially priced its massive dual-tranche equity offerings to bring in roughly $4.9 billion in immediate liquidity.

THE MASSIVE LIQUIDITY RAMP:

THE TRANSACTION DETAILS: Supermicro priced 45.45 million common shares at a flat $27.50 each, alongside a concurrent sale of 75 million mandatory convertible preferred depositary shares carrying a fixed 7.0% yield.

FUNDING THE BACKLOG: The net proceeds are being deployed to purchase premium silicon and thermal equipment necessary to build out an astronomical $39 billion backlog in advanced AI server orders booked by 20 foundational customers.

CAPITAL VS. DILUTION: While the sudden influx of shares introduces near-term equity dilution, it provides the critical liquid cash runway required to fulfill custom liquid-cooled rack systems at scale.

QUANT PERFORMANCE: Factoring in heavy near-term working capital friction against explosive top-line delivery guidance, Seeking Alpha's automated scoring models rate the stock a steady HOLD.

By using public equity markets to directly weaponize its supply chain, Supermicro is aiming to rapidly convert its historic order backlog into recognized hardware revenue.

With Supermicro pricing a massive $4.9B dual offering to bankroll its $39B AI server backlog, do you think this aggressive dilution clears a profitable runway or does it flag persistent cash flow strains?

1

2

11

3,816

Jun 11

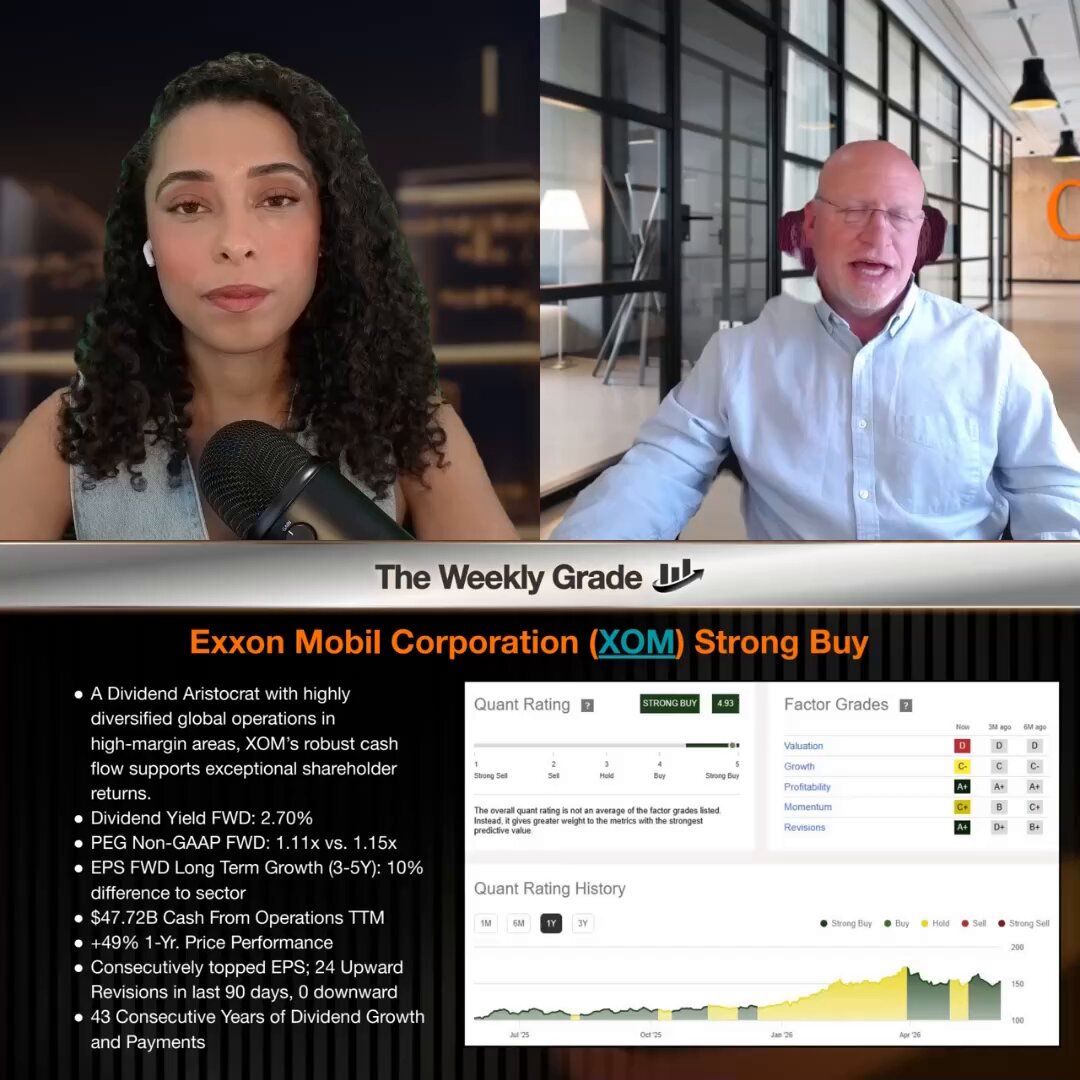

Exxon Mobil: Why Wall Street Changed Its Mind 📊

Exxon Mobil ($XOM) has 43 years of consistent dividend payments under its belt, but a massive shift in the underlying data points to even more upside ahead. @CressTopStocks joins Nicole Benjamin to reveal the sector-relative metrics flashing a huge green light for the energy giant.

The Reality Check:

- Analyst Reversal: Exxon’s analyst revision grade skyrocketed from a "D " to a near-perfect "A " in just 90 days as Wall Street floods it with upgrades.

- Sector Dominance: While its valuation looks average, Exxon's profitability grade completely crushes its energy sector peers.

- The Growth Driver: Analysts are aggressively upgrading earnings estimates for $XOM at a faster pace than the rest of the sector.

- Steven’s Take: "Analysts have really changed their mind... where most are revising their earnings estimates up and very few are taking it down".

#Investing #StockMarket #ExxonMobil #XOM #EnergySector #SeekingAlpha

🔻 Watch the full breakdown on Seeking Alpha below!

1

3

6

4,272

Jun 11

1

3

2,844

Jun 10

The unsupervised ride-hailing era is hitting real-world traffic. Tesla $TSLA has officially expanded its driverless Robotaxi geofence to blanket the entire Austin metro, but fresh operational testing from Bloomberg reveals early scaling friction.

THE INFRASTRUCTURE DEPLOYMENT REALITY:

THE FLEET LIMIT: Reviewing public Texas DMV filings, data shows Tesla has deployed just 59 active unsupervised vehicles to cover the massive 245-square-mile territory.

APP ROADBLOCKS: Bloomberg field tests highlighted prolonged software glitches, pick-up inaccuracies, and "Texas-sized" wait times stretching past 30 minutes due to tight fleet capacity constraints.

WALL STREET WATCH: CFRA Research analyst Garrett Nelson noted the active vehicle count lands well short of even bearish baseline models, highlighting the vast operational gap between Tesla and Alphabet’s multi-thousand vehicle Waymo network.

QUANT PERFORMANCE: Balancing structural auto margin recovery trajectories against a massive premium multiple, Seeking Alpha’s automated systems flag the equity as a steady HOLD.

By prioritizing highly controlled, driverless validation cycles over raw vehicle volume, Tesla is treating its current Texas footprint as an engineering lab before unlocking massive localized scale.

With Bloomberg highlighting long wait times across Tesla's 59-car Austin Robotaxi fleet, do you think this deliberate, slow-rolling approach preserves critical safety boundaries or is the slow vehicle scaling letting autonomous rivals pull too far ahead?

1

4

3,686

Jun 10

The foundation of digital commerce is expanding beyond human interaction. Mastercard $MA has officially launched Agent Pay for Machines (AP4M), a new payment rail built for autonomous AI agents to transact and settle programmatically at machine speed.

THE MACHINE-TO-MACHINE PAYMENTS SUPERCYCLE:

THE CAPABILITIES: AP4M introduces digital credentialing via Verifiable Intent, programmatic spending caps, and continuous, background microtransactions—even handling values worth fractions of a cent.

THE ECOSYSTEM MOAT: Over 30 industry leaders have signed on as launch partners to establish universal rules and scale adoption, including Stripe, Cloudflare, Coinbase, Ripple, and Adyen.

MULTI-RAIL SETTLEMENT: To bypass expensive legacy constraints, the infrastructure natively integrates card networks and bank accounts with stablecoin clearing assets like USDC and PYUSD.

QUANT PERFORMANCE: Commanding a $437.5 billion market capitalization at a stock price of $489.94, Seeking Alpha's automated data flags the company as an unambiguous STRONG BUY.

By building the primary monetary layer under the agentic economy, Mastercard is locking down a massive, high-margin transactional ecosystem before autonomous software commerce goes mainstream.

With Mastercard launching its AP4M network to power automated machine-to-machine payments, do you think this first-mover advantage across AI rails will expand $MA's competitive moat against traditional banking rivals?

3

1

6

2,873

Jun 10

The quick-service drive-thru coffee space is locking in premium market share. Dutch Bros $BROS has been crowned the top SMID-cap investment idea at TD Cowen as analysts double down on the high-growth beverage chain.

THE DRIVE-THRU MONETIZATION STORY:

THE PRICE TARGET: TD Cowen reiterated its conviction BUY rating on the stock, holding a bullish $73.00 price target on positive restaurant sector sales revisions.

TROUGH MULTIPLES: Trading at 19.0x EV/EBITDA, the stock sits right near its historical floor of 18.1x, creating what analysts view as a stark valuation disconnect given its active 28% top-line expansion.

COFFEE VS. FOOD REVENUE: Growth is accelerating ahead of expectations, driven by the middle innings of its mobile app ordering push and a high-margin hot food rollout expected to clear management's initial targets.

COMPETITIVE INFRASTRUCTURE: Despite operating in competitive pockets of Texas alongside fast-growing drive-thru chains like 7 Brew, data shows Dutch Bros is successfully consolidating regional market share.

QUANT PERFORMANCE: Fueled by superior traffic trends and store rollout productivity, Seeking Alpha's automated scoring systems rate $BROS a firm STRONG BUY.

By turning high-velocity coffee and custom energy drink menus into a highly scalable drive-thru infrastructure model, Dutch Bros is out-pacing legacy casual dining networks.

With TD Cowen naming Dutch Bros its top SMID-cap pick and sticking to a $73 target, do you think $BROS can maintain its rapid growth trajectory or will mounting competition cool down the momentum?

7

3,231

Jun 10

The commercial freight landscape is experiencing a massive competitive pivot. Amazon $AMZN has officially opened its nationwide Less-Than-Truckload freight service to all external businesses, taking direct aim at legacy delivery giants.

THE SUPPLY CHAIN RE-ENGINEERING:

THE LOGISTICS OVERHAUL: Operating under Amazon Supply Chain Services , the network handles commercial partial loads from 150 to 15,000 pounds, delivering nationwide to third-party warehouses, retail partners, and independent distributors.

INDUSTRY SHOCKWAVES: The announcement sent immediate structural tremors through the industrial sector, triggering notable stock selloffs across legacy regional carriers like Old Dominion, FedEx, and XPO.

MONETIZING SCALABILITY: Backed by a massive active fleet of over 80,000 trailers and 24,000 intermodal containers, Amazon is effectively turning its core internal logistics layout into a standalone B2B enterprise service.

QUANT PERFORMANCE: Capitalizing on this unparalleled infrastructure moat and a $2.63 trillion market cap, Seeking Alpha's automated scoring models rate $AMZN a clear STRONG BUY.

By weaponizing three decades of proprietary fulfillment tech to absorb outside commercial shipping volumes, Amazon is positioning its network as the primary transport backbone of the modern economy.

2

2,905

Jun 10

Macro price pressures are accelerating. The fresh May Consumer Price Index metrics printed hotter than anticipated, showing consumer price inflation climbing 4.2% year-over-year.

THE BREAKDOWN ON STICKY PRICES:

ACCELERATING PACE: The 4.2% headline figure marks a distinct acceleration from the 3.8% annual clip logged in April, complicating the near-term economic path.

ENERGY SHOCK: Volatile energy costs spiked 3.9% during the month, proving to be the primary culprit by driving over 60% of the total headline increase.

THE CORE CORE TRUTH: Core CPI—excluding food and energy—ticked up to 2.9%, signaling that underlying inflationary momentum remains stubborn across services.

POLICY DIRECTION: As inflation lines drift further from the Federal Reserve’s stated 2.0% sweet spot, swap markets are rapidly repricing the probability of upcoming interest rate cuts.

With energy costs propelling headline inflation to 4.2% in May, do you think the Federal Reserve will be forced to keep interest rates higher for the rest of the year?

$spy $qqq

4

2,918

Jun 9

The neurodegenerative pipeline space is consolidating around precision therapeutics. Eli Lilly $LLY has inked a massive licensing partnership with Swedish biotech AlzeCure Pharma to secure global rights to their preclinical Alzheimer's pipeline.

THE BIOPHARMA BLOCKBUSTER:

THE CASH FLOW STRUCTURE: Lilly will deploy $10 million in initial upfront development capital, wrapping the alliance in a multi-stage milestone track that could clear $1 billion plus royalties.

PATHOLOGY UNDER THE HOOD: The collaborative efforts will build out the Alzstatin ACD680 project—an early-stage molecular modifier targeting the processing enzyme paths behind amyloid-beta aggregates.

PREVENTING BRAIN DAMAGE: By neutralizing these sticky, toxic amyloid-beta assemblies before they create structural plaque chains, the drug aims to preserve baseline cognitive functions.

QUANT METRICS: Reflecting secular dominance across obesity and neurology markets, Seeking Alpha’s automated scoring models rate the core stock a strong BUY.

By layering foundational, early-stage asset rights into its advanced internal clinical pipeline, Eli Lilly is building a defensive, long-term wall against legacy pharmaceutical rivals.

With Eli Lilly locking in a $1B deal with AlzeCure Pharma to advance its Alzstatin program, do you think this preclinical approach will successfully crack the Alzheimer's market, or are the medical clinical risks still too high?

4

3,606

Jun 9

Affluent consumer credit profiles are continuing to clear high macro hurdles. American Express $AXP shares ticked 1.9% higher today after leadership outlined a premium runway for core transaction volume.

THE CREDIT BALANCE MOAT:

THE VOLUME EXPANSION: CFO Christophe Le Cailleux noted that Q2 billing velocity is out-pacing a stellar Q1 performance, which stood as the platform's strongest credit acquisition window in three years.

THE FEE ENGINE: Sustained high-margin net card fee growth continues to buffer the top line, as premium card tier memberships show zero signs of cyclical degradation.

THE YIELD BACKDROP: Backed by a robust market capitalization of $213.1 billion, the financial giant pairs its defensive corporate structure with a dependable 1.09% dividend yield.

QUANT METRICS: Reflecting rock-solid consumer asset quality and premium pricing power, Seeking Alpha’s automated systems rate $AXP a clear BUY.

By anchoring its portfolio structure on ultra-premium consumers rather than subprime credit layers, American Express is successfully shifting past sticky inflationary drags.

With American Express reporting accelerating Q2 billing growth to lock in a clear Buy rating, do you think $AXP's high-end consumer base will keep it insulated if macro economic conditions cool down?

2,695

Jun 9

The consumer artificial intelligence ecosystem is locking in its defining software gateways. Apple $AAPL shares are drawing heavy volume post-WWDC after officially embedding Google Gemini models into a deeply re-architected version of Siri.

THE INTELLIGENCE MONETIZATION SCALE:

THE UPGRADE BUMP: Applauding the consumer feature stack, Morgan Stanley aggressively lifted its stock price target to an Overweight-rated $360 from $330.

VALUE CREATION LOOP: Wedbush analysts model that active monetization from systemic premium services and third-party integrations could expand equity values by $75 to $100 per share.

THE SUBSCRIPTION LEVER: JPMorgan notes that while local edge execution remains free, deep contextual cloud computing will likely drive massive upgrades across premium iCloud tiers starting this Fall.

THE HOLD DISCONNECT: Keeping an alternative view, Jefferies maintained a HOLD on structural supply constraints and data privacy access limitations.

By layering foundational large language models directly into the operating system level, Apple is engineering a high-margin upgrade supercycle for its global global hardware network.

With Apple leveraging Google Gemini to fuel a massive Siri overhaul and hitting a $360 target from Morgan Stanley, do you think this consumer tech refresh cycle will break through Near-Term supply headwinds?

1

2

3,423

Jun 8

The corporate battle over encryption and state-sponsored espionage is returning to federal court. Meta $META has filed a contempt order against Israeli spyware firm NSO Group for violating a permanent injunction protecting WhatsApp users.

THE DIGITAL PERIMETER DEFENSE:

THE INJUNCTION BREACH: Meta claims its internal threat intelligence network detected and disrupted a fresh wave of localized NSO-linked "one-click" social engineering campaigns.

CONTEXT & CLASH: The legal escalation comes after NSO was found liable for exploiting cloud communication channels to deploy its Pegasus spyware arrays into 1,400 global devices.

INFRASTRUCTURE FOOTPRINT: Backed by a $1.51 trillion market capitalization, the social media giant is sharing malicious threat indicators with global security researchers to neutralize the domains.

QUANT METRICS: Seeking Alpha’s automated systems remain steady at a HOLD, balancing the platform's pristine high-margin A profitability footprint against an F valuation grade.

By moving to penalize non-compliant offensive cyber intelligence firms via federal courts, Meta is attempting to establish a binding legal liability frame for commercial spyware vendors.

With Meta dragging NSO Group back to court for violating its permanent WhatsApp injunction, do you think aggressive big tech litigation can successfully curb commercial spyware or are platforms structurally vulnerable?

1

7

3,292

Jun 8

Corporate crypto treasury aggregation is hitting an unprecedented scale. Bitmine Immersion Technologies $BMNR advanced 7.7% today after unveiling a massive $9.6 billion composite asset treasury.

THE ACCUMULATION ENGINE:

THE DIP BUY: Seizing on a macro market pullback, Bitmine scooped up an extra 126,971 ETH in just seven days, deploying roughly $213 million in liquid cash.

REVENUE FOOTPRINT: The company’s total position has ballooned to 5,543,872 ETH, meaning a single public company now controls an astronomical 4.59% of the global Ethereum supply.

THE STAKING INCOME: Utilizing its proprietary "MAVAN" validator network, Bitmine projects it will generate over $270 million in annualized high-margin staking rewards.

QUANT SEGMENT: Brushing off the massive digital vault expansion, Seeking Alpha’s automated systems rate the stock a STRONG SELL on steep pre-revenue valuation metrics.

By aggressively out-pacing corporate peers in raw token velocity, Bitmine is establishing an unassailable financial gateway to the on-chain economy.

With Bitmine buying the dip to secure 4.59% of the entire global Ethereum supply, do you think this massive $9.6B crypto treasury makes $BMNR an essential asset or does the Quant "Strong Sell" highlight too much risk?

1

5

3,329