Financial data and software for global funds and corporates investing in Africa. Request a demo: bit.ly/3r9Akb2

Joined October 2014

- Tweets 106,082

- Following 22

- Followers 124,395

- Likes 6,195

3,216 Photos and videos

Pinned Tweet

Feb 24

2025 was an interesting year for African PE: volumes softened, value held, and strategy evolved.

Our new Private Capital Activity Report breaks down where capital concentrated, how deal structures shifted, and what this signals for 2026.

Download the full report here to learn more ➡️ stears.co/info/2025-private-…

11

15

4,912

Stears retweeted

Jun 3

IT’S OFFICIAL. 🚨

Stears just secured $450,000 in catalytic funding from Cascador.

If you want to invest in Africa, build in Africa, or govern Africa, you need reliable data. Preston Ideh and the Stears team have been building that infrastructure since 2017. Today Cascador backed them to take it further across the continent.

Congratulations Preston 🎉 @StearsData

#CascadorPitchDay2026

5

20

885

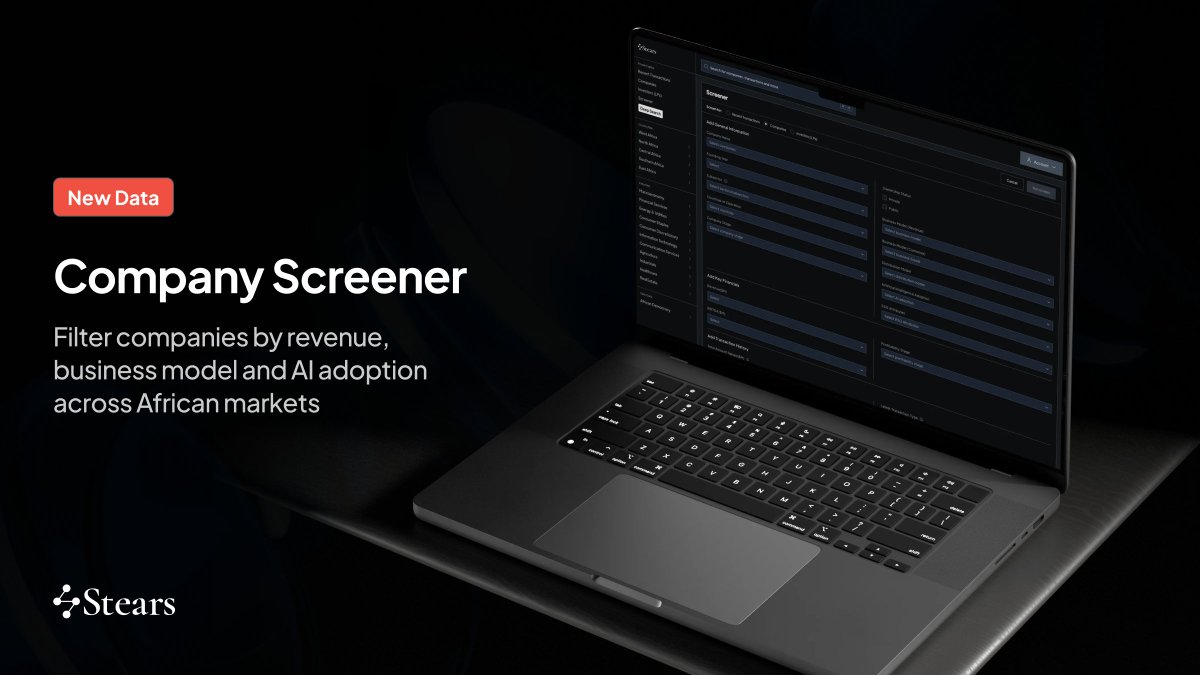

Apr 21

Sourcing the right companies in African markets that fit your strategy can be quite challenging. The Stears Company Screener lets you go from a broad market scan to a targeted shortlist in seconds.

Less time scanning. More time on the right opportunities.

Request a trial: bit.ly/4sNgtYL

3

746

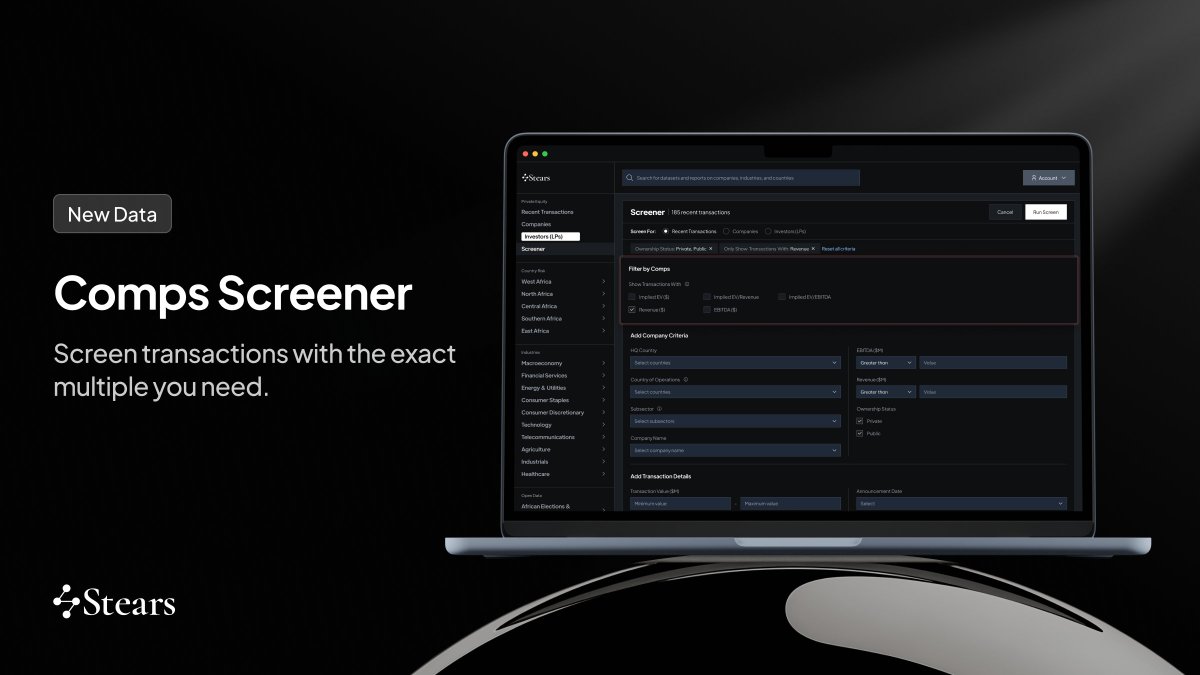

Apr 9

The Stears Comps Screener now filters by exact comparable data points.

Select Implied EV, EV/Revenue, or EV/EBITDA. Every result contains the multiple you're looking for.

Cleaner comps. Faster. Built on African market data.

Live now. bit.ly/4c072jF

1

1

660

Apr 2

Valuation benchmarks for African private markets are now live on Stears. The standard move when pricing an African deal has been to pull US, European or Asian comps and apply a discount. That discount is a guess. There's no data behind it.

Now there is. Price with confidence: bit.ly/4m8EOXi

3

2

714

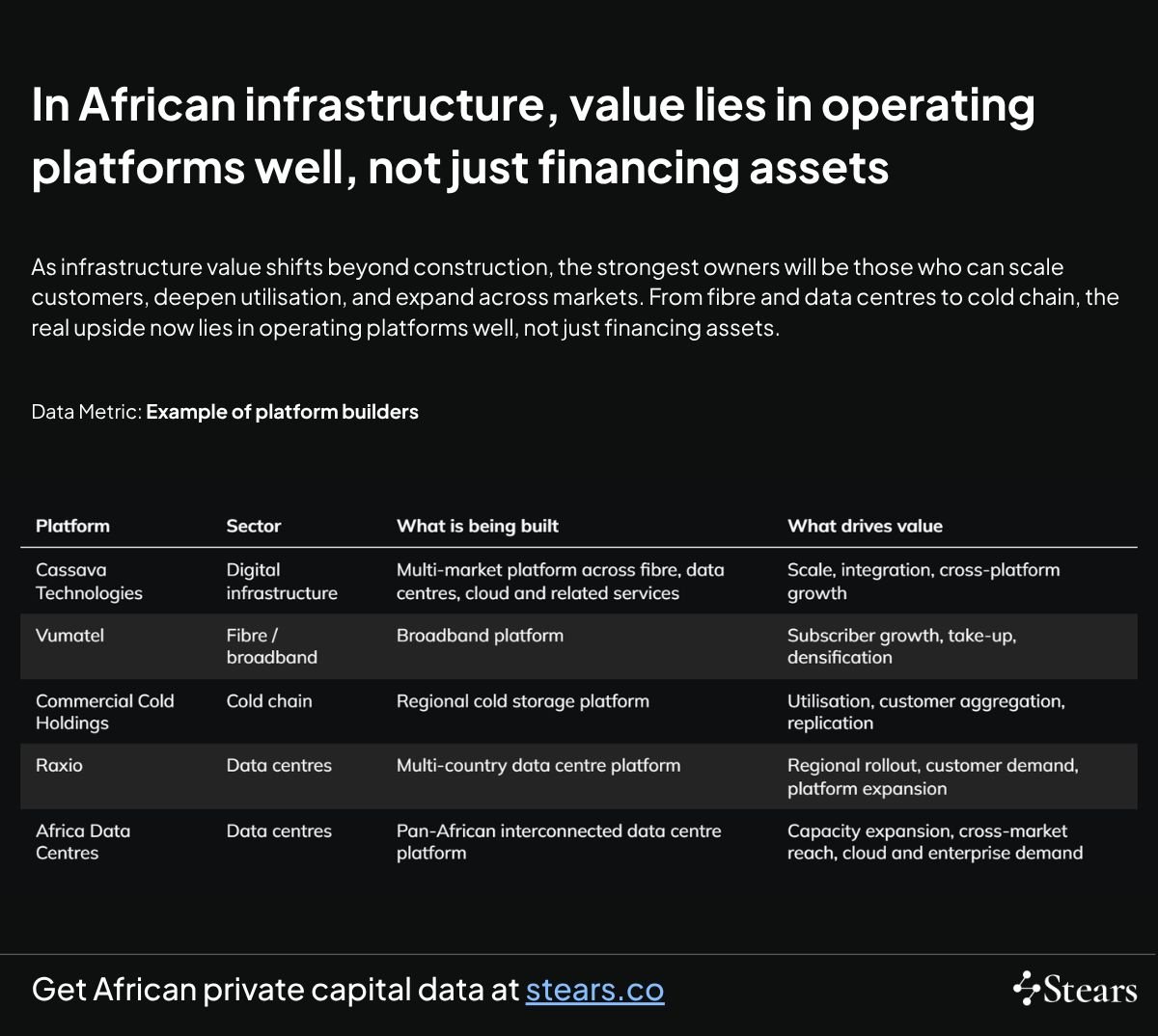

Mar 31

Africa’s infrastructure story is shifting from asset build-out to platform scale. Across fibre, cloud, data centres, and cold chain, value is increasingly driven by utilisation, customer growth, and regional expansion rather than construction alone. Returns may depend less on financing assets and more on building platforms well, with operators and platform builders playing a larger role and institutional capital positioned behind them.

See the signals shaping African infrastructure: share.hsforms.com/1Koufu6ZET…

2

516

Mar 30

Capital is still flowing into Africa, but pricing is shifting. Higher sovereign yields, concessional European financing, and local bank participation in energy infrastructure all point to a more selective market environment. See how investors are positioning: share.hsforms.com/1Koufu6ZET…

1

3

503

Mar 27

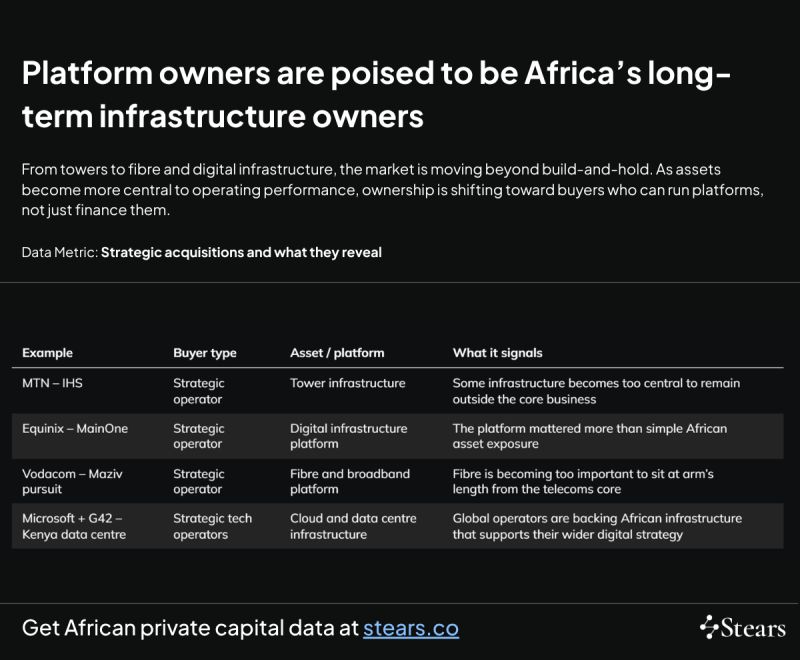

African infrastructure is moving into new hands. MTN’s move to regain control of IHS signals a broader shift in ownership across towers, fibre, and digital platforms from financial sponsors to strategic operators building long-term platforms.

Understand who will own African infrastructure next: share.hsforms.com/1Koufu6ZET…

5

9

835

Mar 25

We are live at the PEVCA Policy Capital Summit 2026, showcasing how Stears provides private capital investors, advisers, and institutions with structured intelligence on African markets — covering transactions, macro trends, and sector dynamics.

See how leading teams evaluate opportunities with greater precision.

share.hsforms.com/1Koufu6ZET…

1

1

486

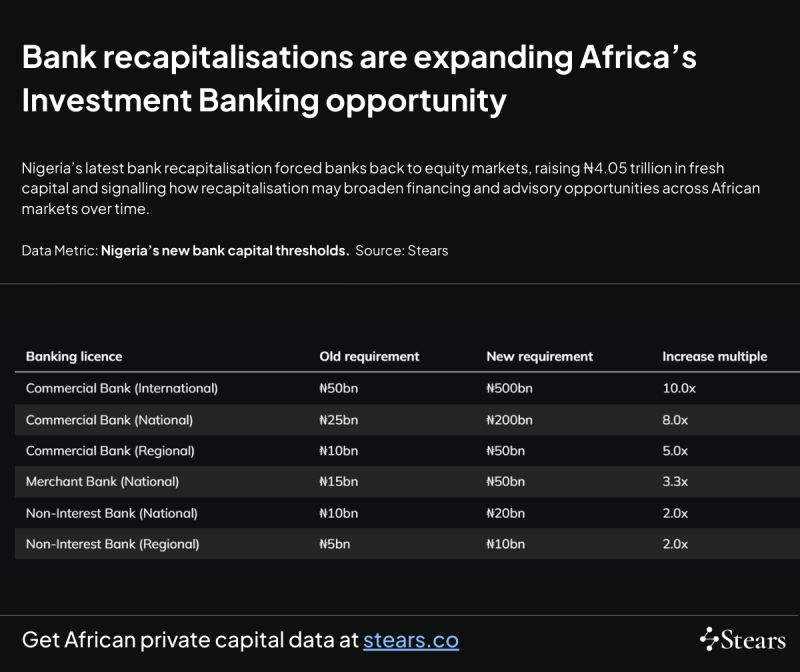

Mar 13

Nigeria’s bank recapitalisation is quietly testing the depth of its capital markets. After the Central Bank raised minimum capital thresholds in 2024, banks mobilised ₦4.05tn (~$2.9bn) in new equity within two years, with 30 of 33 banks meeting the requirement by March 2026. Nigeria’s equity market may be able to absorb more large-scale issuance than recent non-bank deal flow suggests.

Request a trial to track the capital flows shaping African markets. bit.ly/4lx5gd0

1

2

787

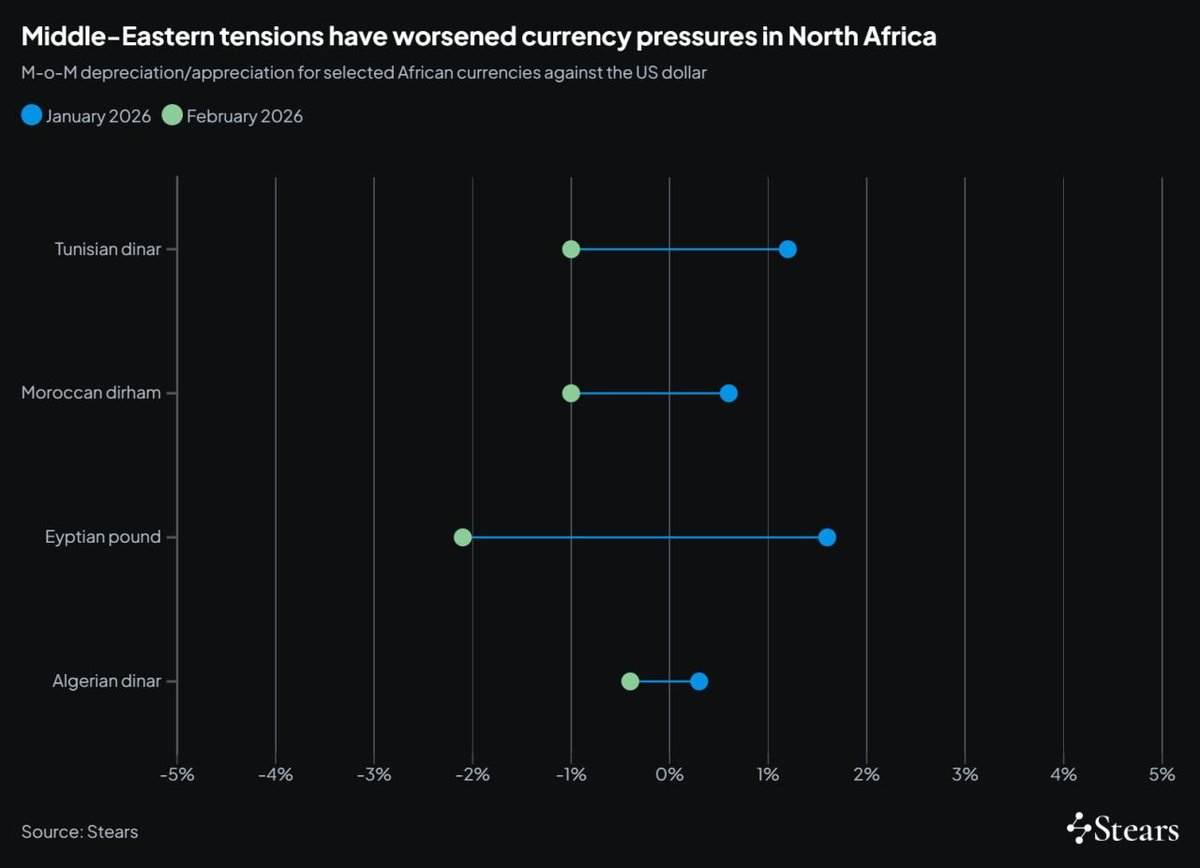

Mar 13

North Africa’s capital flows are becoming more differentiated. Amidst tensions, Egypt captured ~69% of disclosed deals in February, reinforcing its role as the region’s capital hub. Meanwhile, Morocco is attracting new industrial investment, including Safran’s €280m aerospace facility, while Algeria and Tunisia push digital infrastructure reforms.

We break down the capital flows, sectors and deal dynamics on Stears.

Request a trial: bit.ly/4lx5gd0

3

1

478

Mar 6

AfCFTA may be Africa’s most important economic experiment in decades.

54 countries are lowering tariffs on ~90% of goods while tackling non-tariff barriers.

Early results we expect include

• Border clearance times falling on major corridors

• Logistics costs declining

• Intra-African trade rising to 14.9%

Source: Stears Research.

Read more: share.hsforms.com/1Koufu6ZET…

4

8

562

Mar 5

Last week, we analysed medical equipment in Southern & North Africa.

This week: East & West Africa.

Medical equipment across these regions remains largely import-dependent, making distributors, rather than manufacturers, the strategic entry point.

Demand is concentrated in Nigeria, Kenya, and Tanzania, and capital is flowing toward platforms with regulatory depth, servicing networks, and OEM partnerships.

If you’re underwriting healthcare infrastructure exposure, request a Stears trial for deeper analysis: share.hsforms.com/1Koufu6ZET…

2

440

Mar 3

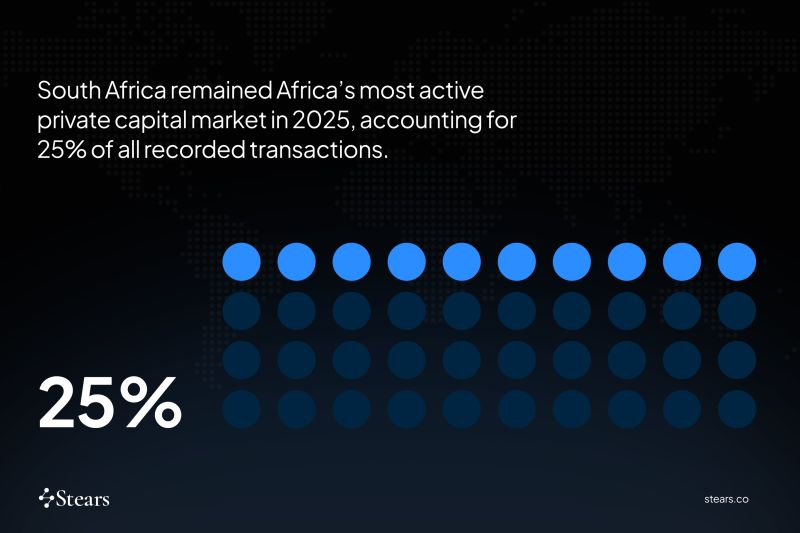

25% of Africa’s recorded private capital deals in 2025 happened in South Africa.

That concentration tells you something.

Regulatory depth deal maturity scalable assets = capital gravity.

Activity is clustering around:

• Telecoms & fibre

• Visible exit pathways

• Expanding private debt markets

For GPs, it’s a proving ground.

For LPs, it’s the reference market.

Source: Stears Research.

Benchmark capital inflows and sector concentration in our 2025 report.

Download here: stears.co/info/2025-private-…

2

459

Mar 3

West Africa is quietly engineering funding optionality.

Benin’s $500m sukuk drew $3.9bn in orders, priced alongside a Eurobond reopening.

Nigeria’s six domestic sukuk issuances since 2017 have lifted outstanding stock to ₦1.29tn by September 2025.

This is not symbolic diversification.

It reflects segmentation of the global capital pool, expanding the investor base beyond traditional EM-dedicated funds and accessing pools structurally restricted from holding conventional debt.

For sovereign issuers, that reshapes refinancing risk and demand resilience.

Source: Stears Research.

For deeper sovereign funding and capital flow intelligence, request trial access: share.hsforms.com/1Koufu6ZET…

4

10

865

Feb 26

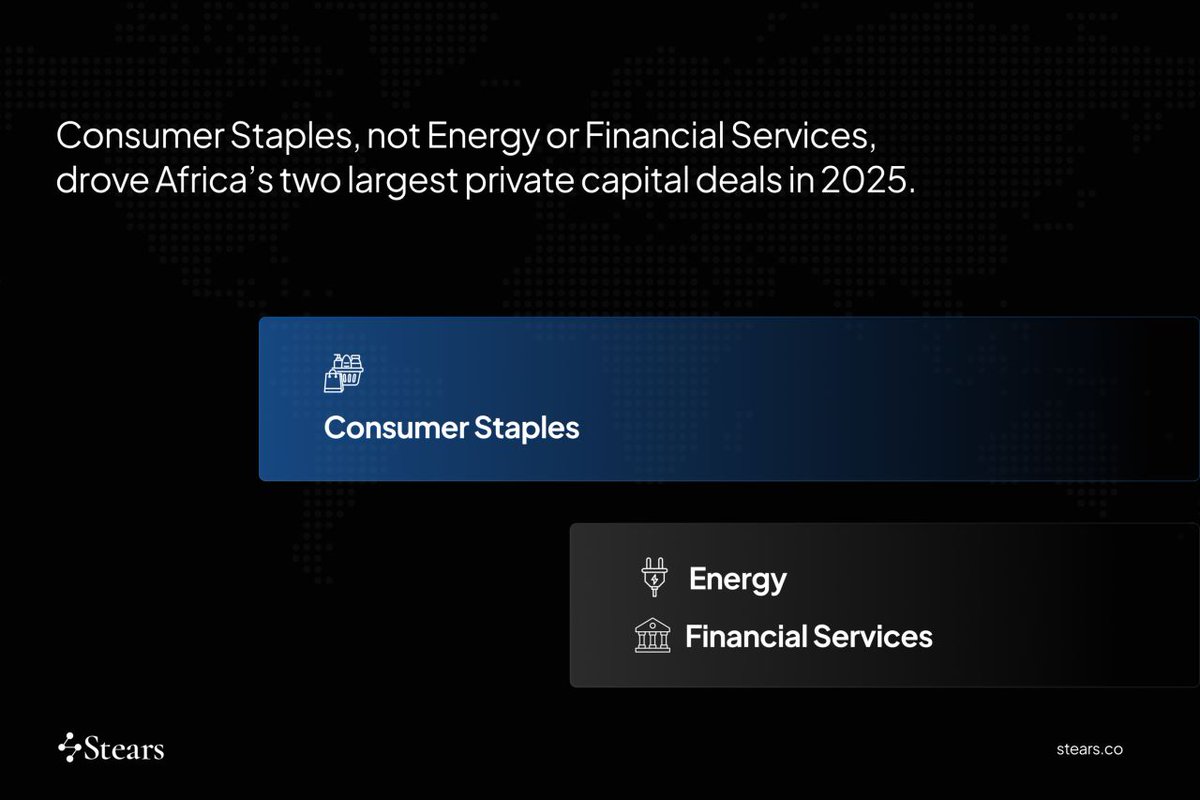

Consumer Staples took the deal crown in 2025.

For the first time, it outpaced Energy and Financial Services in anchoring Africa’s two largest private capital deals.

From @CocaCola HBC’s CCBA acquisition to Asahi and @Diageo_NA portfolio reshuffles, capital is backing African demand for the long haul.

See where capital is rotating next ➡️stears.co/info/2025-private-…

#FMCG #ConsumerDemand #AfricaMarkets #DealFlowAnalysis

2

4

598

Feb 25

The real moat in African medical equipment isn’t the hardware, it’s the route to market.

This industry is split into four structurally different channels:

• Public procurement

• Private hospital networks

• Independent clinics & labs

• Donor-funded programmes

Each carries a different margin profile, working capital cycle, and payment risk.

For LPs and GPs, this isn’t academic.

Channel strategy determines cash conversion, risk exposure, and exit optionality.

Valuation isn’t driven by topline growth alone it’s channel mix, OEM positioning, and service depth.

The winners will integrate lifecycle services, scale regionally, and build recurring revenue engines.

Access the full proprietary African healthcare investment data here➡️ share.hsforms.com/1Koufu6ZET…

1

1

343

Feb 25

Africa’s capacity to absorb multi-billion-dollar deals just shifted.

In 2025, five transactions topped $2bn.

In 2024, only one did.

Global capital is rotating from early-stage risk to scaled, de-risked platforms.

Source: Stears Research, 2025 Private Capital in Africa Activity Report

Track where the next billion-dollar deal will land → shorturl.at/vnMTb

#MegaDeals #PrivateEquityAfrica #StrategicCapital #FrontierMarkets

3

3

472

1 May 2025

Africa’s private capital data—now at your fingertips. Stears is the only data platform built exclusively for Africa’s private capital market. Get instant access to company data, financials, transaction histories, macro trends & exclusive insights across 54 countries. Request a trial today: share.hsforms.com/1Koufu6ZET… #AVCA2025 #StearsData

1

3

11

2,691

27 Feb 2025

With Egypt's inflation near 15% in 2024, down from a 30% peak, IMF reforms are boosting investor optimism. Discover what else is buoying investor sentiment in the Africa Capital in 2025 report: bit.ly/3Qs8q2V

1

1

7

2,430