Strategic infrastructure for the tokenized world. Committed to the secure, decentralized operation of the TX Network and the global democratization of asset own

Joined March 2023

- Tweets 640

- Following 360

- Followers 684

- Likes 118

30 Photos and videos

007TX Validator retweeted

Jun 12

🔥BREAKING: Wall Street successfully tests 5-second Treasury settlements on the XRP Ledger.

A new cross-border tokenized redemption pilot was just completed by a powerhouse lineup:

🔹 JPMorgan

🔹 Mastercard

🔹 @OndoFinance

🔹 @Ripple

By cutting settlement times down from 3–5 business days to a mere 5 seconds, this test highlights the massive efficiency gains tokenization brings to traditional banking rails.

85

822

3,256

81,845

This is a very important step in the right direction. No institution will be ready to use TX and Solotex until the #txecosystem demonstrate (not just say that it is) complaint. Could not be prouder of the progress the team has gone. For those not aware, Part-2 is when the system demonstrates compliance for a given period of time (not just a snapshot which is what happens on Part-1)

Jun 6

Further demonstration of the #txecosystem team’s commitment to providing the safest institutional-grade rails for compliant #RWA #tokenization. Completing Part I shows all necessary security controls are in place, and Part II will confirm their functionality over time.

4

9

48

2,611

RT @jaebersole1: Further demonstration of the #txecosystem team’s commitment to providing the safest institutional-grade rails for complian…

51

RT @MikeMcC1uskey: For fintechs partnering with institutions in a regulated environment, having the right processes, procedures, and system…

53

007TX Validator retweeted

Jun 5

tx is now SOC 2 Type I compliant.

This milestone reflects the controls and standards institutions expect from their partners, and a commitment to compliance-first infrastructure.

Institutional trust starts with meeting that bar. It's what tx is built on.

32

84

235

21,371

007TX Validator retweeted

Jun 2

🇺🇸 LATEST: The SEC has elevated digital assets to a strategic priority in its five-year roadmap through 2030.

It calls for clearer crypto rules, tokenization support, and a framework for staking and onchain markets.

60

188

1,062

38,045

007TX Validator retweeted

Jun 2

🚨 JUST IN: #Ripple expands its Washington, D.C. presence with a new office 🇺🇸

8

106

658

13,420

007TX Validator retweeted

Jun 2

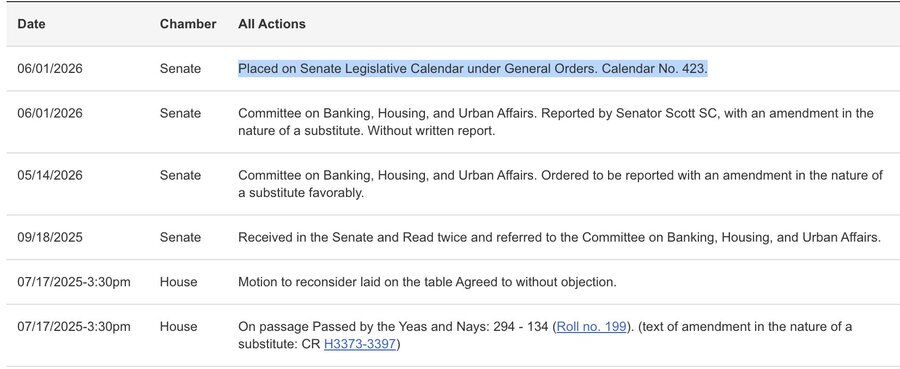

🚨HUGE: The CLARITY Act has now been added to the U.S. Senate Legislative Calendar.

51

139

969

28,850

Friends, it is happening.....I know that patience sometimes is painful but nobody can deny things are progressing in the right direction

Jun 1

🚨HUGE: SWIFT confirms over 50 major banks will implement CRYPTO rails for cross-border payments.

Bank of America, JP Morgan, Deutsche Bank, Bank of China and SBI are among the banks backing the initiative, with over 25 set to begin processing payments by June.

Swift handles over $150 TRILLION annually.

4

5

33

2,172

I am becoming very excited about the launch of the marketplace. Also, I love this image (the golden nuggets TX on the pan..). I thought it was very smart advertising.

Jun 1

Real-world assets are scattered across markets, platforms, and rails.

tx brings them into one marketplace, so building an onchain portfolio does not require digging across disconnected systems.

4

7

46

2,265

007TX Validator retweeted

May 27

Real world assets deserve a purpose-built destination.

One app. Every asset class. All in your pocket.

Stay tuned for more details.

39

92

223

14,351

007TX Validator retweeted

Jun 1

Citibank estimates that if 10% of everyday U.S. investors switch to digital trading platforms, it could create $2.6T in demand for tokenized stocks.

Access and distribution are just as important as issuance.

That's the market tx is building toward.

INSIGHT: @Citi projects the tokenized securities market will grow from $17B today to $5.5T by 2030.

18

46

155

9,684

May 20

RT @MikeMcC1uskey: Today, @txEcosystem met with the SEC to discuss the future of tokenized RWAs and blockchain-powered capital markets.

We…

124

May 20

RT @txEcosystem: tx leadership was fortunate to meet with SEC Crypto Task Force staff today.

The tx team presented materials focused on th…

82

007TX Validator retweeted

May 20

⚖️NEW: Trump orders Fed to grant crypto firms DIRECT access to master accounts.

This could let crypto firms move money more like banks instead of depending on banks to do it for them.

133

610

2,599

125,201

007TX Validator retweeted

May 19

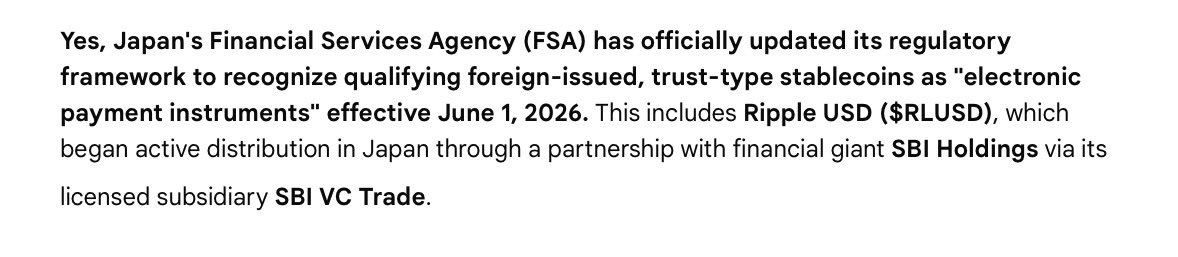

🚨Japan OFFICIALLY Recognizes $RLUSD As Digital Payment Method From June 🇯🇵🔥

$XRP has been previously recognized as “financial asset” in Japan. 🚀

May 19

JUST IN: 🇯🇵 Japan officially recognizes foreign-issued crypto stablecoins as legal electronic payment methods starting June 1.

8

67

496

24,801

INSIGHT: President Trump signs an executive order directing the Federal Reserve to review crypto and fintech firms' access to payment accounts and services, ordering regulators to identify and remove barriers to entry within three months.

127

403

1,769

102,837

007TX Validator retweeted

May 20

Hypothetical: $TX Tokenizing a Portion of NYSE

NYSE (part of ICE) has announced plans for tokenized securities platforms (24/7 trading, instant settlement, stablecoin funding), but these are likely on regulated, permissioned infrastructure—not directly on public chains like tx.

This scenario assumes tx captures significant value as the underlying blockchain/infrastructure or fee-capturing layer for tokenized NYSE-listed equities (or a "portion" of the market).

**Key context for simulation**:

- NYSE-listed market cap: ~$28–45 trillion (part of broader U.S. equities ~$69T ).

- Current tokenized RWAs: ~$30–35B on-chain (mostly treasuries/credit).

- Projections: Tokenized assets could reach $2–16T by 2030 (optimistic up to $30T by 2034), with equities as a major category if regulations allow broad adoption.

**Value capture assumptions** (highly speculative; real outcomes depend on adoption, competition from NYSE's own platform/Nasdaq/others, regulation, and tx's execution):

- **Fees/utility model**: TX could capture transaction/gas fees, staking for security, issuance fees, or governance value from tokenized volume/TVL. Compare to other L1s (e.g., SOL/ETH capture via fees token demand).

- Conservative: tx powers 1–5% of tokenized equities (e.g., niche or international access).

- Bull: tx becomes a leading public chain for compliant RWAs, capturing 10% via network effects.

### Simulated Price Potential (Rough Scenarios)

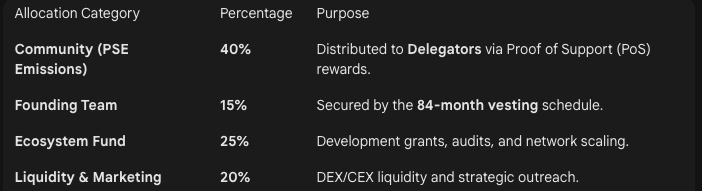

Assume TVL/ tokenized volume on tx drives demand for TX (staking, fees, speculation). Current price ~$0.008, circ. supply ~4.3B. Emissions dilute over time, so models focus on effective valuation.

1. **Base Case (Modest Adoption, 2030)**: $100–500B tokenized on tx (e.g., portion of early RWA growth).

- TX captures value like a mid-tier RWA chain (e.g., via 0.1–1% fees staking yields).

- Implied market cap: $1–5B (comparable to current mid-cap L1s with RWA focus).

- **Price range**: $0.20 – $1 (20–100x from current, assuming some dilution offset by growth/burns).

- Rationale: Matches current RWA momentum but limited NYSE penetration.

2. **Bull Case (Significant Portion of NYSE Tokenized)**: $1–5T tokenized equities/RWAs on tx (e.g., 5–10% of NYSE or broader U.S. equities shift on-chain).

- High utility: Fees from high-volume trading/settlement, staking for security, premium for compliance.

- Implied market cap: $10–50B (like top RWA plays or L1s today, scaled up).

- **Price range**: $2 – $10 (250–1,200x), or higher in euphoria (FDV $100B if hype).

- PSE emissions: Gradual release supports staking yields (potentially 10–30% APY early), attracting capital but creating sell pressure—mitigated if demand grows faster.

3. **Extreme Bull (Dominant Tokenization OS)**: tx captures 10–20% of multi-trillion tokenized market.

- Market cap $50–200B (comparable to today's major L1s if RWAs explode).

- **Price**: $10 – $50 (massive upside, but low probability due to competition from traditional players like NYSE/ICE).

**Risks and Caveats**:

- **Dilution**: PSE unlocks ~1/84 of 100B monthly—long-term inflation unless offset by demand/burns.

- Competition: NYSE's own platform, other chains (Ethereum, Solana), or permissioned solutions could dominate.

- Regulation: Tokenized stocks face hurdles (SEC, custody, fungibility).

- Execution: tx must deliver marketplace, liquidity, and adoption.

- Valuation not guaranteed: Crypto tokens often trade on narrative/speculation more than fundamentals.

This is a **speculative simulation** based on public projections—not financial advice. Actual price depends on execution, macro, and market sentiment. DYOR, consider volatility, and note RWAs are early-stage. If tx successfully positions for even a slice of NYSE-scale tokenization, upside could be substantial given its low current valuation.

May 19

Today, @txEcosystem met with the SEC to discuss the future of tokenized RWAs and blockchain-powered capital markets.

We shared TX’s vision for compliance-first infrastructure supporting regulated financial assets onchain through licensed partners.

The next era of finance will be built onchain.

4

7

51

2,715

May 19

Cannot get more bullish @txEcosystem

May 19

🚨BREAKING:

SEC CHAIR PAUL ATKINS SAYS “ALL U.S. MARKETS WILL BE ON-CHAIN WITHIN TWO YEARS”

IT'S COMING!

3

7

43

1,617