Paylaşımlarım yatırım tavsiyesi değildir; yalnızca kendi fikir ve stratejilerimi yansıtır. Yatırım kararı alıyorsanız, bu tamamen sizin sorumluluğunuzdadır.

Joined March 2021

- Tweets 2,340

- Following 1,077

- Followers 7,445

- Likes 8,618

499 Photos and videos

Ace ♤ retweeted

May 21

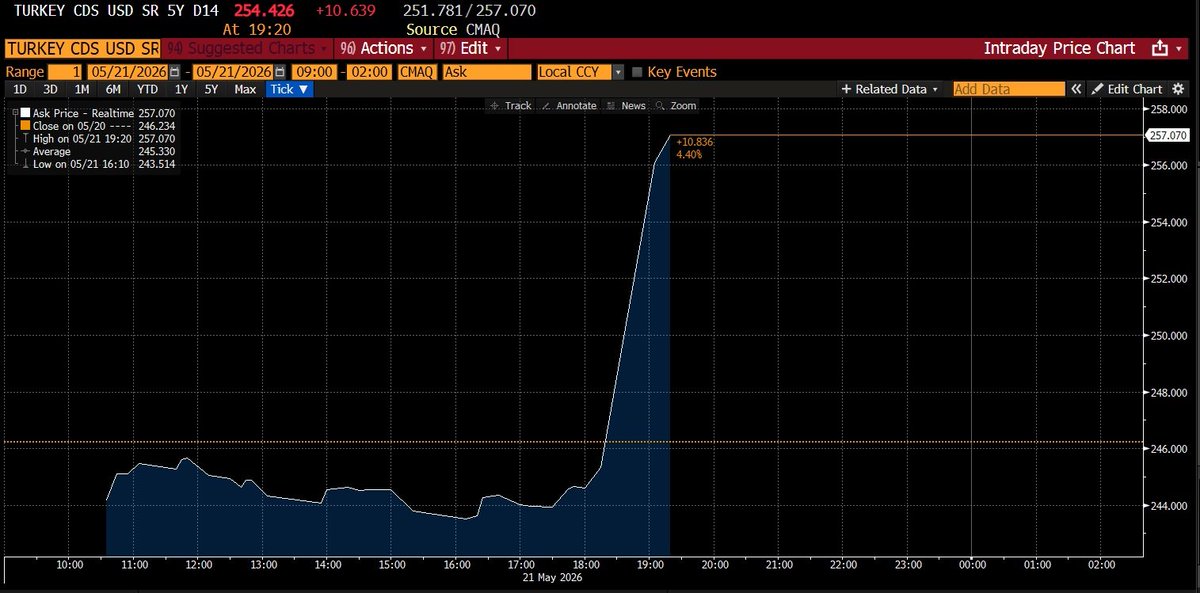

CDS, bir ülkenin borcunu ödeyememe riskine karşı piyasanın talep ettiği sigorta primidir. Risk algısı arttığında CDS yükselir, azaldığında düşer.

Kabaca bunu, bankadan kredi çekmek istediğinizde size dayatılan hayat sigortası gibi düşünebilirsiniz. Yaşınız veya sağlık durumunuzla ilgili bir risk varsa sigorta poliçe ücretleri de artar. Ülkede yolunda gitmeyen bir şeyler olduğunda CDS’in arttığı gibi.

Aslında bu, ülkenin itibarını gösteren parametrelerden biri olarak da düşünülebilir. Yükseliyorsa, itibarınızı sarsan bir şeyler yapıyorsunuz demektir.

13

39

87

13,684

Ace ♤ retweeted

May 21

Demokrasi ve hukukun olmadığı ülkelerin para biriminin değeri pul olur.

Çünkü bunların olmadığı ülkelerde ne ekonomi yönetimine ne de devlet kurumlarına güven kalır.

10

24

56

14,005

Ace ♤ retweeted

Apr 22

En büyük kazançlar, herkesin korktuğu dönemlerde yapılan doğru hamlelerden çıkar.

Eğer bugün $BTC, $ETH, $SOL gibi güçlü ve oturmuş projelere yatırımınız varsa, muhtemelen bundan bir kazanç elde edersiniz.

Eğer yatırımınızı ilk fırsatta realize etmek yerine daha uzun vadeli bir stratejiye dönüştürürseniz, belki de bu yatırım kazançtan öte hayatınızı değiştirecek bir şeye evrilebilir.

Çünkü dünya genelinde kripto varlıklara yönelik düzenlemelerin artması, sektörün artık görmezden gelinemeyecek bir noktaya geldiğini gösteriyor.

24

47

76

21,059

Daha iyi yok gerçekten.

Mar 31

Güzel dalga geçmişler.

Daha önce de söylemiştim ama galiba ne demek istediğim tam anlaşılmadı. @Chain_GPT sadece bir launchpad değil, çok daha fazlası. Hatta CEO’su ile ilk görüştüğümde, launchpad’in ekosistemin çok küçük bir parçası olduğunu söylemişti ve anlaşılan o ki bu doğru.

O yüzden $CGPT'ye inanıyorum.

Aşağıda da binlerce dolarlık akıllı kontrat denetim hizmetlerinin, ChainGPT AI Hub V2 ile 100 dolar gibi komik bir rakama yapılabildiğini ve bunun da denetim firmalarında bir miktar endişe yarattığını üzülerek anlatmışlar 🤣

5

68

Bu savaş diğerlerine benzemiyor. Çünkü tüm ülke ekonomilerini doğrudan etkileyebilecek bir faktöre sahip: Hürmüz Boğazı.

Mar 30

Teknik analizler, MA’lar, cart curt… şu an o kadar anlamsız ki. Kardeşim, bu savaş bitmeden piyasaların düzelme şansı yok. Sen istediğin kadar analiz yap.

Ama işin güzel yanı, bunun eninde sonunda düzelecek olması. Sanki hiç gelmeyecekmiş gibi hissettirse de gelecek.

Bu benim 3. ayı sezonum ve evet, piyasa bir şekilde hep toparlıyor.

4

86

Ace ♤ retweeted

Mar 25

Bilmiyorum, ben milleti temsil eden birinden daha iyi bir hitabet beklerdim. Niyeti iyi olsa da konuyu toparlamakta zorlanmış gibi.

Ayrıca mecliste kimsenin de dinlediğini zannetmiyorum; meclisin durumu da ortada. AKP–MHP ne derse o.

Zaten bu şartlarda neden meclis varsa.. .

Mar 25

Yeni Yol Partisi Milletvekili Sadullah Kısacık:

"Kriptonun da bir felsefesi var"

"Bu yasa bu şekliyle geçerse balinalar varlıklarını global platformlara taşır"

16

23

97

20,794

Ace ♤ retweeted

Mar 24

Bir sonraki döngünün hikayesini, ETF onayı almış ve alma potansiyeli olan altcoinler yazacak.

Çünkü SEC tarafından onaylanmış bir ETF’e kurumsal para rahatça girebilir.

Bu da ETF olan altcoinlerde daha fazla likidite, daha fazla görünürlük ve daha büyük fiyat hareketleri demek.

27

37

76

16,768

Ace ♤ retweeted

Mar 10

Brolar, size yakında ödüllü AMA gerçekleştireceğimiz #PRISM projesinden bahsetmek istiyorum.

OpenEden, FalconX ve Monarq Asset Management tarafından geliştirilen PRISM, on-chain getiri tarafında çok stratejili bir portföy modeli sunuyor.

Çoğu on-chain getiri ürünü tek bir stratejiye dayanır. O strateji zayıfladığında getiriler de aynı şekilde düşer. Fakat PRISM’de işler biraz farklı.

PRISM’de birden fazla getiri kaynağı bulunuyor:

➥ Cash-and-carry arbitrajı

➥ Kurumsal karşı taraflara aşırı teminatlı kredi

➥ On-chain getiri platformları

➥ ABD tahvili destekli tokenize RWA’lar

Amaç; farklı piyasa döngülerinde daha istikrarlı getiri sağlamak ve kripto fiyatlarıyla düşük korelasyon yakalamak.

Portföy yönetimi ise FalconX’in nicel varlık yönetimi kolu olan Monarq tarafından yapılıyor.

Kısacası bu model, tek bir stratejiye bağlı getiri yerine çeşitlendirilmiş gelir kaynakları, disiplinli likidite yönetimi ve aktif risk kontrolüne dayanıyor.

Detaylı anlatım burada 👇🏼

55

75

112

17,855

Ace ♤ retweeted

Mar 5

Arz oylaması tamamlandı.

Artık 2.1 milyardan fazla $APT olmayacak. Ancak bu tek başına yeterli değil.

Sıradaki adımlar:

➥ Gaz ücretlerinin 10 kata kadar artırılması ve elde edilen gelirlerin yakılması.

➥ Enflasyonun (dolaşıma düzenli giren token miktarının) %5.22’den %2.6’ya düşürülmesi.

Bunların gerçekleşmesi hâlinde fiyat üzerinde mutlaka bir etkisi olacaktır.

Aptos Proposal #183: Hard Supply Cap: 2.1 Billion APT has passed.

Now awaiting execution, stay tuned for more updates:

governance.aptosfoundation.o…

26

59

99

17,965

When we look at $BTC on the weekly chart, it’s hard to argue that the uptrend has been broken. RSI has also moved into the oversold zone.

Around May, I expect the U.S. midterm election economy to kick in, a change in the Federal Reserve chair, and more aggressive rate cuts than currently signaled.

This process reminds me somewhat of the Covid period. As you may recall, the economy climbed out of the Covid slump largely through the stimulus money Trump distributed directly to citizens. Today, I believe Trump will take similar steps to strengthen his position ahead of the midterms and will move to support and stabilize the markets.

1

5

113

Seeing the OKX CEO’s post about Binance and the APY rates being offered for $USDe immediately brought the #LUNA crisis to mind.

If you’ve been in the market for a while, you’ll remember this. There was an algorithmic stablecoin tied to LUNA: UST (TerraUSD). More precisely, its backing was not a traditional reserve, but rather LUNA’s market value and an arbitrage mechanism.

Right before the collapse, UST was offering APY rates well above the market average. These yields, primarily provided through the Anchor protocol, were extremely attractive to anyone looking for passive income. Major exchanges like Bybit made access to these returns very easy, which caused liquidity to flow into the system at a rapid pace.

Honestly, even back then, the whole setup didn’t make much sense to me. Despite many content creators enthusiastically promoting it, I stayed away. In hindsight, that was the right call—because the collapse came very quickly.

UST’s collateral was not a reserve in the conventional sense; as mentioned above, it relied on LUNA’s market capitalization. The system was built around a mint-and-burn mechanism designed to maintain UST’s 1-dollar peg. But once large amounts of UST started being sold on the market or withdrawn from the protocol, the peg broke.

From that point on, the arbitrage mechanism worked in reverse: more LUNA was minted, and as LUNA’s price fell, the system’s ability to support UST weakened even further.

What followed was the now-infamous “death spiral.” The peg was completely lost, LUNA’s supply spiraled out of control, and the system effectively collapsed.

That experience taught me a very clear lesson:

If a stablecoin is offering unusually high APY, the first thing to examine is where that yield comes from and how it’s generated. The collateral structure, sustainability, and how the system behaves under stress are just as important as the headline return.

4

7

238

Ace ♤ retweeted

Jan 25

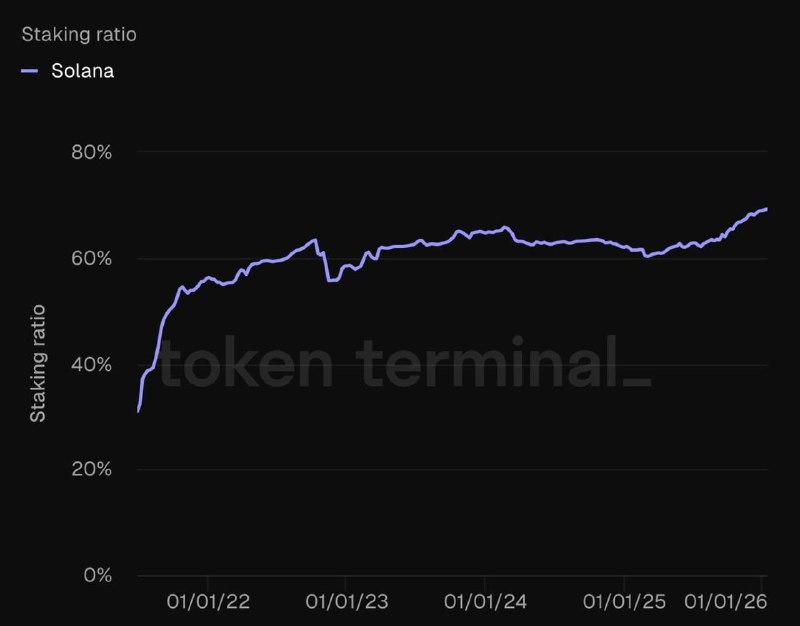

$SOL staking oranı p’e dayanmış durumda.

Bu, yatırımcının #Solana ekosistemine olan inancını ve güvenini açık şekilde gösteriyor. Aynı zamanda son derece bullish bir veri.

Şöyle özetleyeyim: Neredeyse her projede staking özelliği var ama bu piyasa değerine sahip, üstelik 11 ETF’i bulunan bir L1 projesinde p gibi bir staking oranı görmek pek mümkün değil. Bu, Solana’ya olan uzun vadeli bağlılığın çok net bir göstergesi.

Yeri gelmişken şunu da söylemekte fayda var: Bireysel kullanıcıların zahmetsizce ~ %5,4 APR ile stake edebileceği Binance'in $BNSOL ürününü de incelemenizi tavsiye ederim. Elinizde tuttuğunuz SOL’ler için en pratik ve görece en yüksek staking getirilerinden birini sunuyor.

🟨 binance.com/en/solana-stakin…

Üstelik bunu yaparken SOL likiditenizi de kullanmanız mümkün. Bu açıdan sistem oldukça esnek. Stake ettiğiniz token’ları talep ettiğinizde, 2-3 gün içinde biriken ödülleriyle birlikte geri alabiliyorsunuz.

#İşbirliği değildir.

45

53

98

21,318

Market makerlar kaybetti.

Fonlar ve retail ciddi zarar etti.

Proje ekipleri bile kasalarını yedi.

Fonlar riskten kaçtı, borç alınan token’lar satıldı, proje ekipleri de olası satış dalgasına karşı cash’e dönmeye başladı.

Ortada tek bir kötü haber yoktu ama senaryolar fiyatlandı.

Likidite çekildi, satışlar üst üste bindi ve piyasa bugünkü sıkışık hale geldi.

2025 Q4 güzel anılmıyorsun canım 🥲

7

13

221

Değerli metallerden çıkan paranın kriptoya aktığı, savaşların bittiği ve herkesin mutlu bir yıl geçirdiği bir yıl dileğiyle… Mutlu Noeller. 🎄

31 Dec 2025

2023’ten beri çok verimli bir yıl göremedim. Umarım 2026 hepimiz için bir teselli olur.

Herkese mutlu yıllar 🎄

9

139

$TTD on Binance Alpha is easily one of the most ambitious AI agents I’ve come across.

To be fair, plenty of AI agents can generate signals or run analysis on a crypto asset. But when it comes to actually executing trades, most of them hit a wall and ask for manual approval.

That’s not how things work at @tradetideAI_.

#Tradetide follows an execution-first approach.

Put simply:

While most AI bots say “here’s what you should do”, Tradetide aims to say “I’ll do the trade for you.” 🔥

I don’t know, that feels pretty slick to me.

What’s live today: enter a token or contract address and get real-time technical analysis, plus a backtesting infrastructure that lets you test strategies on historical data. So it’s not just ideas, it’s an attempt to answer “does this strategy actually work?” with data.

The roadmap is equally ambitious: agents that manage portfolios based on user-defined return targets and risk tolerance, a strategy marketplace, and eventually a network of fully autonomous alpha-generating agents.

And it’s not just a hollow story on the numbers side either: a community of 150k , tens of thousands of on-chain users, and a testnet that’s been active for months.

Bottom line: several people around me are already using these AI agents, and they’re definitely not random amateurs. If this catches your interest, I think it’s worth at least keeping on your radar.

18 Dec 2025

Binance Alpha will be the first platform to feature TradeTide (TTD) on December 20.

Eligible users can claim their airdrop using Binance Alpha Points on the Alpha Events page once trading opens. Further details will be announced soon.

Please stay tuned to Binance’s official channels for the latest updates.

1

2

297

Kazanan arkadaşları tebrik ediyorum 🤝

24 Dec 2025

Kazananları tebrik ederim

@Muhendis_ozgur

@Termoss13

@kndnemslmn99

@TapLadyyy

@Hudaiyolun

smpl.rs/g/LUTVEQ

5

166

Ace ♤ retweeted

20 Dec 2025

Binance Alpha’da yer alan $TTD, gördüğüm en iddialı AI Agent!

Aslına bakarsanız birçok AI ajanı bir kripto para hakkında size sinyal üretebilir, analizler yapabilir; fakat iş işlem yapmaya gelince orada tıkanır ve sizden manuel onay ister. Ama @tradetideAI_’da işler öyle yürümüyor. Çünkü #Tradetide execution-first yaklaşımını benimsemiş durumda.

Basitçe anlatmak gerekirse:

Birçok AI bot/ajan “ne yapılmalı?” derken, Tradetide “işlemi ben yaparım” demeye çalışıyor 🔥

Bilmiyorum, bana havalı geldi.

Şu an aktif olan tarafı; token ya da kontrat adresi girildiğinde canlı teknik analiz üretmesi ve stratejileri geçmiş veriler üzerinde test edebilen bir backtesting altyapısına sahip olması. Yani sadece fikir değil, “bu strateji gerçekten çalışıyor mu?” sorusuna veriyle cevap verme çabası var.

Yol haritası da son derece iddialı. Kullanıcının getiri hedefi ve risk toleransına göre portföy yöneten agent’lar, strateji pazaryeri ve uzun vadede otonom çalışan bir alpha agent ağı hedefleniyor.

Rakamlar tarafında da tamamen boş bir hikâye yok: 150 binin üzerinde topluluk, on binlerce on-chain kullanıcı ve aylardır aktif bir testnet süreci var.

Özetle, benim çevremde bu AI ajanlarını kullanan birçok kişi var ve bunlar öyle hiç de boş adamlar değil. Hâliyle ilginizi çekiyorsa, en azından takip etmekte fayda var diye düşünüyorum.

18 Dec 2025

Binance Alpha will be the first platform to feature TradeTide (TTD) on December 20.

Eligible users can claim their airdrop using Binance Alpha Points on the Alpha Events page once trading opens. Further details will be announced soon.

Please stay tuned to Binance’s official channels for the latest updates.

70

91

152

24,351