31 | British investor making the stock market accessible for everyone-Documenting the journey openly | £130k → £200k | Sharing what we weren’t taught at school

Joined April 2023

- Tweets 23,942

- Following 179

- Followers 34,845

- Likes 5,792

1,424 Photos and videos

Pinned Tweet

May 30

MAY PORTFOLIO UPDATE

Grab a coffee - there’s a lot to go through but WHAT a month!!

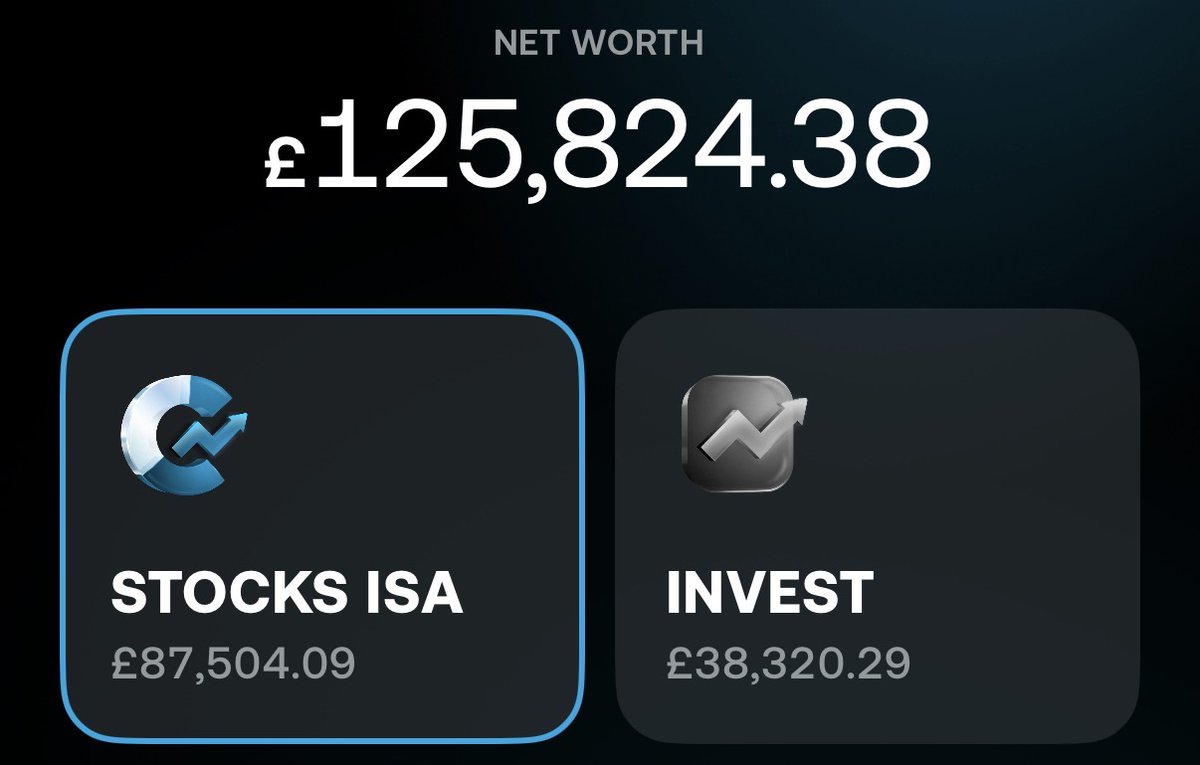

Total portfolio gain = £8700

Closing Value = £125,825 (£6000 in cash)

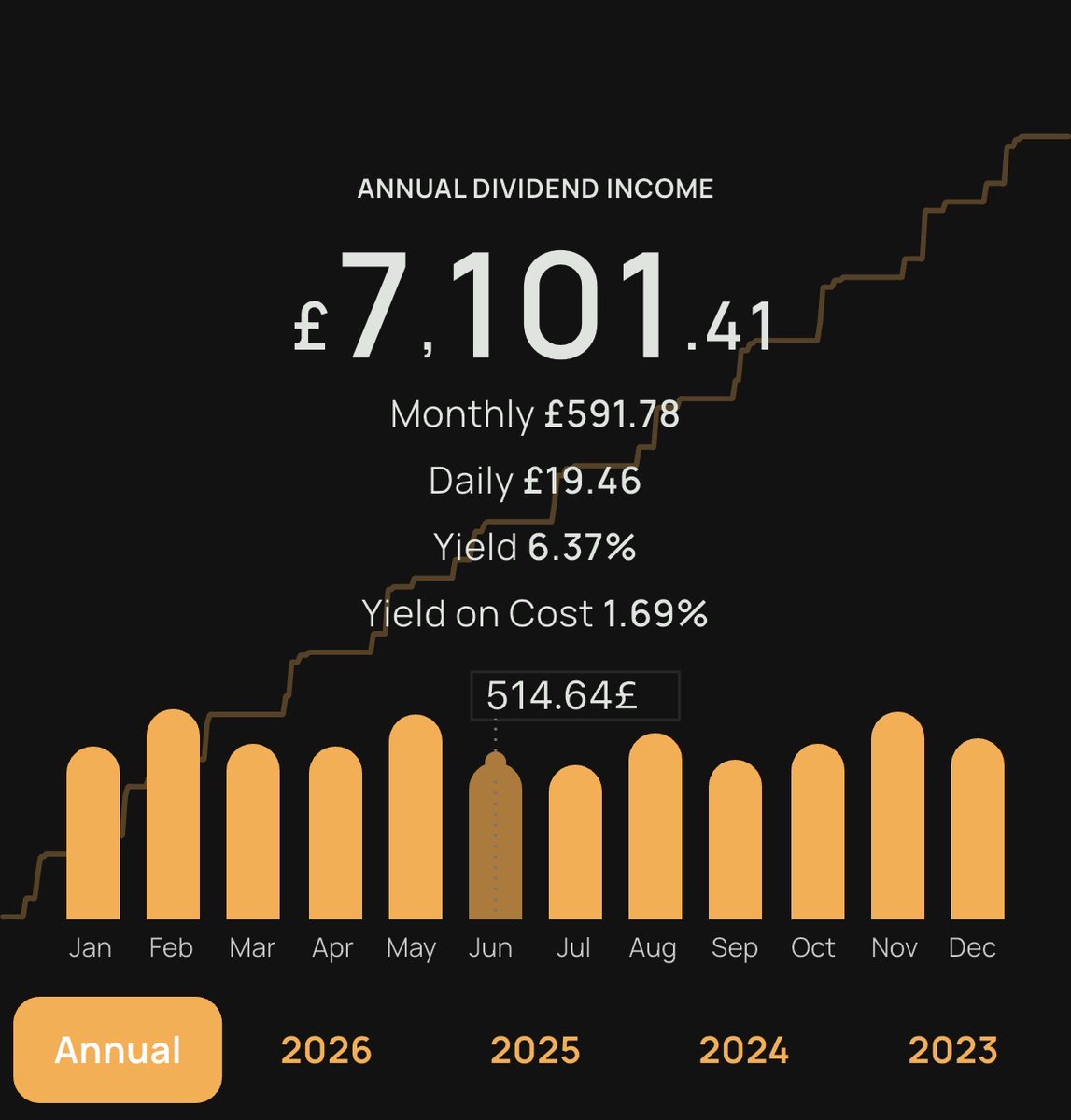

Total dividends earnt = £542 - All reinvested back into my main pie. I’ll put pie links at the bottom where you can see % split of each ETF/stock.

Dividends came from $JEQP $AAIF $SLVI $GLDE $GOOO $TSLD

So, firstly we hit an all time high for the stocks and shares ISA (£87,851). I’m pushing for £100,000 in the ISA before next April, which I think is doable with the addition of my new boost pie (shall explain lower). I have used all £20,000 allowance so the target is going to have to be achieved from reinvesting dividends earnt and capital growth. All depends on what Donny decides though...

I started a new smaller cap growth pie which I plan to DCA into from dividends earnt as well as deposits I make. I think this will be a great addition to act as a side boost.

The pie includes some good names (jn my opinion):

Boost pie: $GRRR $HIVE $MNTS $NBIS $ONDS $OUST $NOW $SIDU $SIVE $TE

I sold all my 131,000 Dogecoin. I had initially planned to hold it until SpaceX IPO but with the market performing as well as it is, that capital should be put to work. I have circa £6200 in the boost pie in my general invest account at the time of writing. Hopefully this is way higher at the end of June!

I have also started building some long term positions in Rolls Royce and Lockheed. Ive thought about adding Northrop too. My reasoning is I essentially want exposure to the big, government contracted companies that are constantly improving propulsion systems. I think we are going to see a breakthrough in propulsion soon.

Top gainers for the month:

Vaneck Space Innovators: 41%

Vaneck Semiconductors: 26%

Vaneck Quantum Computing: 23%

Some of the single stocks in the boost pie have done silly returns but I’ve not held them all for a month straight yet so won’t include in the above.

One I am really excited about is Sivers Semiconductors. I have 362 shares and now that earnings have happened, hopefully it continues to rip up. The companies pipeline looks strong.

Boost pie: trading212.com/pies/ltzntt0a…

Main pie: trading212.com/pies/ltzntt0a…

A few things I am thinking about doing but am yet undecided: Thinning down or even removing SP500 and going all in on All World as well as thinning down ETF exposure generally and adding more capital to single stocks. I shall keep everyone in the loop.

June plan:

- Deposit as much as I can from my salary, hopefully £300-400 and add this to the boost pie.

- Reinvest Dividends into the boost pie.

- Hope Donny keeps his mouth shut and we get another month like May!!

As always, I’ve no idea what I’m doing and if anyone has questions, fire them at me.

I honestly love the community we've got here. Every now and then I get tagged in a post by someone saying I've inspired them to start investing which honestly amazes me that I have an impact - so thank you to anyone that has liked, commented, shared etc. It really means a lot.

Let's keep this rolling gang!

35

4

192

63,401

£10,000 sitting in a savings account.

Here's the most tax efficient way to deploy it.

Priority order:

→ 3 months expenses in easy access savings first. Non negotiable.

→ Remaining £6-7k straight into Stocks & Shares ISA. → Buy VWRP or VUAG. Global or US index fund.

→ If under 40: £4,000 into LISA first. Government adds £1,000 instantly.

→ Automate £200/month going forward. Never stop.

What not to do:

→ Leave it in a current account earning nothing

→ Put it all in crypto

→ Wait for the perfect moment

£10,000 invested today at 10%:

→ Worth £174,000 in 30 years.

The best time to deploy it was yesterday.

The second best time is today.

8

32

3,819

Well said

Jun 12

Owning a £400,000 house with a £350,000 mortgage in the UK in 2026 means signing a 25-year contract to give the bank around £2,050 a month, in exchange for the right to maintain a building you'll spend another £4,000 a year keeping dry, warm and structurally sound.

At a 5% fixed rate, the total interest over the life of the mortgage is around £264,000. The total mortgage cost ends up at roughly £614,000.

The price tag on the front door says £400K. The actual cost of living in it for 25 years is closer to £750K, before council tax, repairs, insurance and the new boiler.

This is what the country has been calling 'getting on the ladder.'

7

1

33

45,745

🤣🤣 what on earth

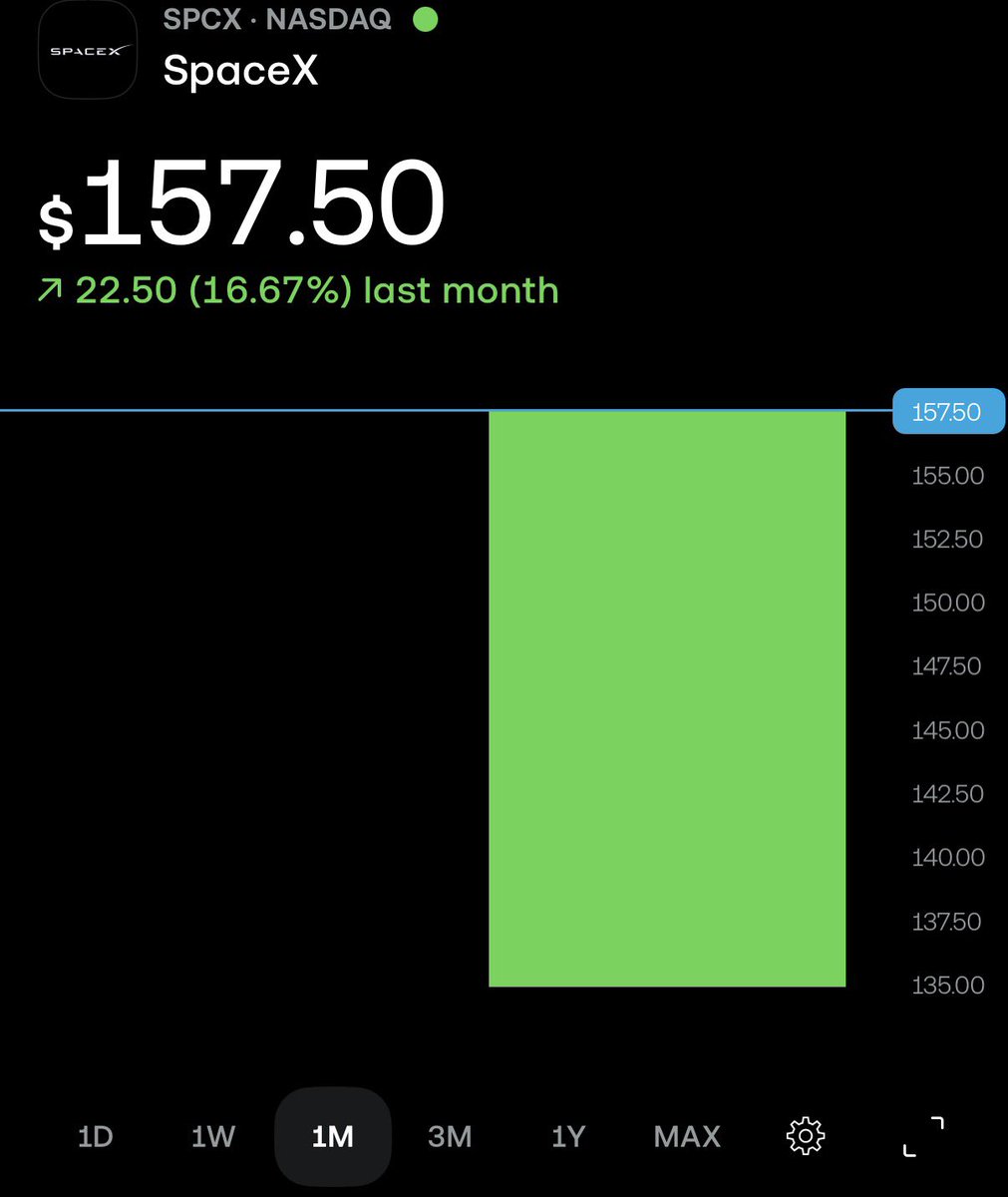

SpaceX $SPCX beats Nvidia's record for largest stock market cap increase in a single day, adding over $350,000,000,000 after its IPO.

10

49

9,498

Emerging markets.

Two words that confuse most beginner investors.

Plain English:

Developing economies with fast growing stock markets. Higher risk. Higher potential reward.

Examples: China. India. Brazil. South Africa. Taiwan. Mexico.

Why invest in them?

India GDP growing at 6-7% annually vs UK at 1-2%

Middle class expanding rapidly across Asia

Demographics favour growth. Young populations. Rising incomes.

The risks:

Political instability

Currency volatility

Less regulatory protection

Liquidity issues in smaller markets

Most beginner investors get enough emerging market exposure through VWRP. 10% allocation automatically.

Enough to benefit. Not enough to hurt badly if they struggle.

13

1

37

8,032

MONDAY GOD CANDLE APPROACHES

21h

JUST IN: 🇺🇸🇮🇷 Pakistan's Prime Minister expects US-Iran deal to be finalized within the next 24 hours.

18

51

5,463

To everyone stating currency risk is still an issue with GBP - yep you're absolutely correct. The point I'm getting at is for us British folk, we're usually better off buying GBP funds and not USD

Jun 13

You invest in the S&P 500 in your ISA.

The S&P 500 goes up 10%.

Your return in GBP? Maybe 7%.

Welcome to currency risk.

Here's what happens:

Your fund is priced in USD. When the pound strengthens against the dollar your returns shrink. When the pound weakens your returns grow.

You can be right about the market. And still underperform because of currencies.

The fix for UK investors:

→ Buy GBP denominated funds. VUAG not VOO.

→ UCITS regulated. LSE listed.

→ No currency conversion eating your returns silently.

Same index. Same companies. Right wrapper.

13

54

45,724

Most people retire poor because:

• They optimise for now, not later

• They think small amounts don't matter

• They wait for the "right time"

£200/month at 25 beats £600/month at 40.

11

1

43

12,432

Sivers finished the week strong. The company AGM is on Monday where hopefully we may get some potential NASDAQ listing news. Let’s wait and see. $SIVE

9

46

7,308

Ever wonder why your UK portfolio moves when US markets open? Here's why.

The S&P 500 contains companies generating revenue in every country on earth. Apple. Microsoft. Amazon. Google. Nvidia.

When Wall Street sneezes the entire world catches a cold.

US markets represent roughly 60% of global stock market value. When they move everything moves with them.

Your VWRP or VUAG tracks US companies. Even your FTSE 100 funds react to US sentiment.

This isn't a flaw. It's just how interconnected global markets are.

The good news? US markets go up more than they go down. Long term that interconnection works in your favour.

3

4

41

11,897

Jun 13

You invest in the S&P 500 in your ISA.

The S&P 500 goes up 10%.

Your return in GBP? Maybe 7%.

Welcome to currency risk.

Here's what happens:

Your fund is priced in USD. When the pound strengthens against the dollar your returns shrink. When the pound weakens your returns grow.

You can be right about the market. And still underperform because of currencies.

The fix for UK investors:

→ Buy GBP denominated funds. VUAG not VOO.

→ UCITS regulated. LSE listed.

→ No currency conversion eating your returns silently.

Same index. Same companies. Right wrapper.

40

6

302

97,878

Jun 12

Incredibly we ended the week green. What a week lol. Excited for next week!

15

1

66

10,027

Jun 12

My guess would be Space X pumps for some weeks then slowly bleeds down over the next 6 months.

30

2

95

23,728

Jun 12

Volatility is terrifying.

For long term investors it's just noise.

The S&P 500 since 1928:

→ Falls 10% roughly every 11 months

→ Falls 20% roughly every 4 years

→ Falls 30% roughly every decade

Every single time it recovered. Every single time it hit new all time highs.

The investor who stayed invested through every drop? Never lost money over any 20 year period. Ever.

Volatility isn't risk for long term investors. It's the price of admission for extraordinary returns. The investors who can't stomach the drops never experience the highs.

14

5

57

21,142

Jun 12

The Federal Reserve sets US interest rates.

You're a UK investor. Why should you care?

Because it moves everything you own.

When Fed raises rates:

→ Borrowing costs rise globally

→ Growth stocks get hammered

→ REITs suffer

→ Your portfolio drops

When Fed cuts rates:

→ Borrowing gets cheaper

→ Growth stocks rally

→ REITs recover

→ Your portfolio rises

The Fed doesn't manage your ISA. But it might as well.

5

1

14

4,035

Jun 12

Me monitoring the situation from the sideline

17

4

94

13,329

Jun 12

The other week I made a call to ditch $VUAG (S&P 500).

Replaced it with VWRP (FTSE All-World) SMGB (Semiconductors). Both of which I already held but I’ve just sized up the positions.

Genuinely one of the better portfolio decisions I’ve made in my opinion.

Why?

VWRP gives me every major global company across every geography - US, Europe, Asia, emerging markets. True diversification, not just “US tech with extra steps.”

SMGB gives me concentrated exposure to the actual infrastructure layer which I believe every single industry is going to be reliant on. TSMC, Nvidia, ASML, Broadcom, AMD. The companies that everything else depends on.

Between the two, I’ve got every major name that matters AND genuine geographic diversification AND a direct line into the semiconductor supercycle.

The S&P 500 was just US large caps with heavy tech concentration anyway.

This feels like the same exposure, minus the blind spots, plus the conviction.

Anyone else made similar moves away from the standard S&P 500/Nasdaq trackers recently?”

38

5

123

24,457