Microgrants for bold and ambitious student founders.

Joined February 2025

- Tweets 563

- Following 8

- Followers 501

- Likes 471

67 Photos and videos

3F VC retweeted

Jun 13

Meet the members of Proxima:

Anindyadeep (@anindyadeeps) is building Litefold. LiteFold combines physics-based simulation and AI to accelerate the design and validation of drug candidates in silico.

Their leading product is Rosalind: An AI Co-Scientist for Life Sciences.

4

8

53

5,234

3F VC retweeted

Jun 12

If you like the AI space want to understand the stack at a deeper level, do give this a read:

3f.vc/reports/ai-stack

1

1

10

144

3F VC retweeted

Jun 12

Would you all be interested in this?

If we can get 10–20 people to show up for the livestream, @karansehgal47 and I would be more than happy to do this for every report.

Can't we have a tbpn style 1 hr block from you 2 fav tag team, where you discuss many good useful info. Can we?

4

3

14

824

3F VC retweeted

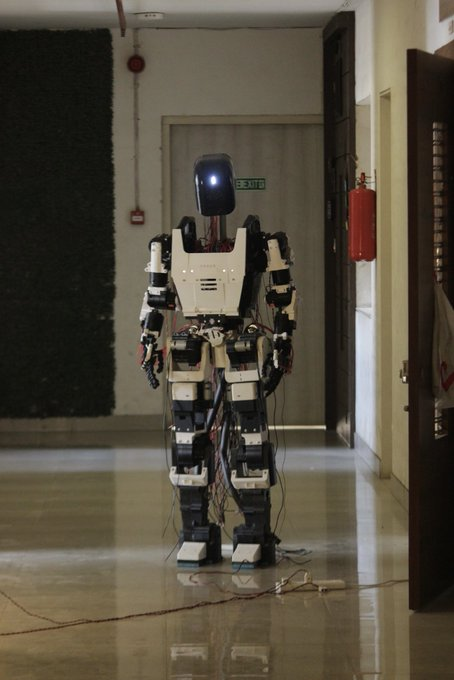

Jun 11

Meet the members of Proxima:

Aryan Wagh (@ironwagh) is building Vanar Robots, an indigenous robotics firm solving for general-purpose humanoid robotics. From a living room. On almost no capital.

They build everything in-house: actuators, manipulators, software. Not general-purpose imported parts, but components built specifically for the mechanical strain that comes from running a robot for hours on end in harsh conditions.

9

32

289

23,432

Communities are quietly becoming startup infrastructure.

They help founders move through trust faster: early users, feedback, hires, investors, and intros.

The strongest startup ecosystems will be built around dense networks that help people hire, raise, and grow.

3f.vc/article/communities-as…

1

2

7

179

Startups grow inside networks of trust.

Communities help founders find early users, hire, learn faster, raise capital, and build market credibility.

That is why communities are becoming startup infrastructure.

3f.vc/article/communities-as…

2

1

3

123

Industries fueled by passion are the hardest ones to crack.

We figured this out while working on our specialty coffee report. At first, coffee looked like a simple market to map. Beans move from farms to roasters to cafes to consumers. Margins should be visible. Winners should be obvious. But the deeper we went, the less it behaved like a normal consumer category. Everyone in the chain cared too much.

That sounds like a good thing. Passion creates better products, better stories, and more loyal customers. But it also makes the market harder to read. A cafe owner may accept worse economics because they love the craft. A roaster may obsess over a microlot that will never scale. A customer may spend ₹400 on a pour over every week but refuse to buy a ₹5,000 grinder. Rational behavior exists, but it is hidden under taste, identity, ritual, and pride.

This is why these markets punish outsiders. You cannot just enter with capital, branding, or distribution and expect to win. The real rules are tribal. People care about origin, processing, equipment, water, technique, and the person behind the bar. They can smell shortcuts quickly. In passion markets, the customer is not only buying the product. They are buying proof that you respect the thing as much as they do.

The opportunity is still real. In fact, it may be better because of this difficulty. But the best companies in such industries usually do not begin by trying to look big. They begin by earning trust in one small corner. They make one tool, one roast, one cafe format, one supply chain layer, or one ritual meaningfully better. Passion makes the market harder to crack, but it also protects the people who crack it honestly.

1

5

195

Read more: 3f.vc/reports/specialty-coff…

1

3

73

Glad to see founders build and share in public.

Jun 4

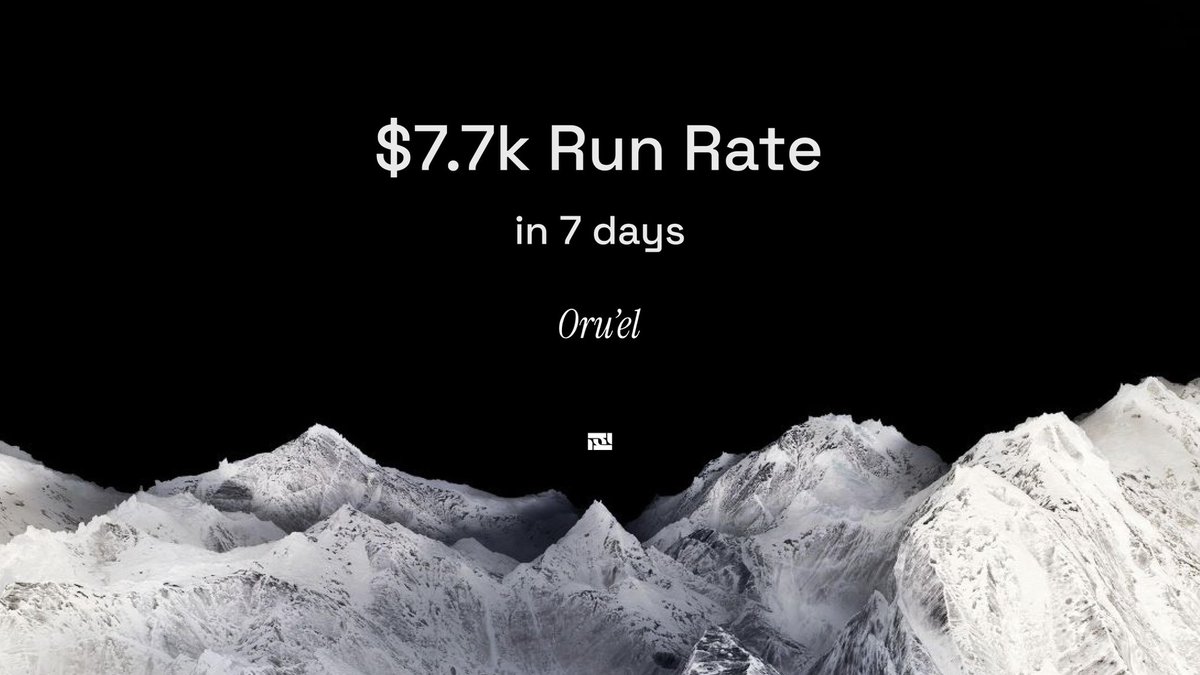

7 days 7.7k Run Rate Private Beta == Too much Drama

Oru'el began a private beta with a set number of handpicked researchers, engineers, startups and organisations about a week ago.

Yesterday, we crossed $7.7k in Monthly Run Rate during the first 7 days of the Private Beta.

Was this easy? lol. As a matter of fact, we got a bank account on the last day before our GST permit was gone. We were waiting for it else we couldn't actually sell. Not mentioning that we are juggling 3 payment gateways bank transfers.

The funny part? We neither own GPUs nor sell compute. We sell one thing that everyone loves to claim in the industry but can't prove. SLAs, or to be bluntly put, Job Completion Guarantee (and a few more gaps the industry ignores).

It took 5mo of playing around to figure that the buyer must change. Sell to the teams already paying for compute, the ones bleeding 60% of their time to this problem.

Our internal research team (one person) led by @chastronomic and Internal Product team (one person) @nihipap ran days and nights.

Ajith sprained his ankle, got his wisdom tooth removed and got food poisoning during this duration while Nihith had to move back to hyderabad and worked 16 hours a day continuously for 3 weeks before the platform was live.

We have identified two crucial segments where compute scarcity hits them like a truck to the wall but haven't been catered to at all. No one serves them properly.

I am aware the post leaves questions like what exactly are these market segments, how do we guarantee job completions, what are the other gaps that are ignored, and a lot more, we will expand on them once the Private Beta is over.

Honoured. Grateful. Hopeful, as more shall come and must come. The private beta is still live. 3 more weeks.

Veer Bhogya Vasundhara.

2

5

499

3F VC retweeted

Jun 4

7 days 7.7k Run Rate Private Beta == Too much Drama

Oru'el began a private beta with a set number of handpicked researchers, engineers, startups and organisations about a week ago.

Yesterday, we crossed $7.7k in Monthly Run Rate during the first 7 days of the Private Beta.

Was this easy? lol. As a matter of fact, we got a bank account on the last day before our GST permit was gone. We were waiting for it else we couldn't actually sell. Not mentioning that we are juggling 3 payment gateways bank transfers.

The funny part? We neither own GPUs nor sell compute. We sell one thing that everyone loves to claim in the industry but can't prove. SLAs, or to be bluntly put, Job Completion Guarantee (and a few more gaps the industry ignores).

It took 5mo of playing around to figure that the buyer must change. Sell to the teams already paying for compute, the ones bleeding 60% of their time to this problem.

Our internal research team (one person) led by @chastronomic and Internal Product team (one person) @nihipap ran days and nights.

Ajith sprained his ankle, got his wisdom tooth removed and got food poisoning during this duration while Nihith had to move back to hyderabad and worked 16 hours a day continuously for 3 weeks before the platform was live.

We have identified two crucial segments where compute scarcity hits them like a truck to the wall but haven't been catered to at all. No one serves them properly.

I am aware the post leaves questions like what exactly are these market segments, how do we guarantee job completions, what are the other gaps that are ignored, and a lot more, we will expand on them once the Private Beta is over.

Honoured. Grateful. Hopeful, as more shall come and must come. The private beta is still live. 3 more weeks.

Veer Bhogya Vasundhara.

3

4

21

1,310

3F VC retweeted

Jun 4

We’ve all seen people nerd out on fancy coffee tasting notes and bright acidity.

@karansehgal47 and I spent the last month digging past the flavor talk. We decoded the numbers: farmgate prices, the harvest-to-cup chain, and where value moves and costs land for founders in India.

10

13

51

11,741

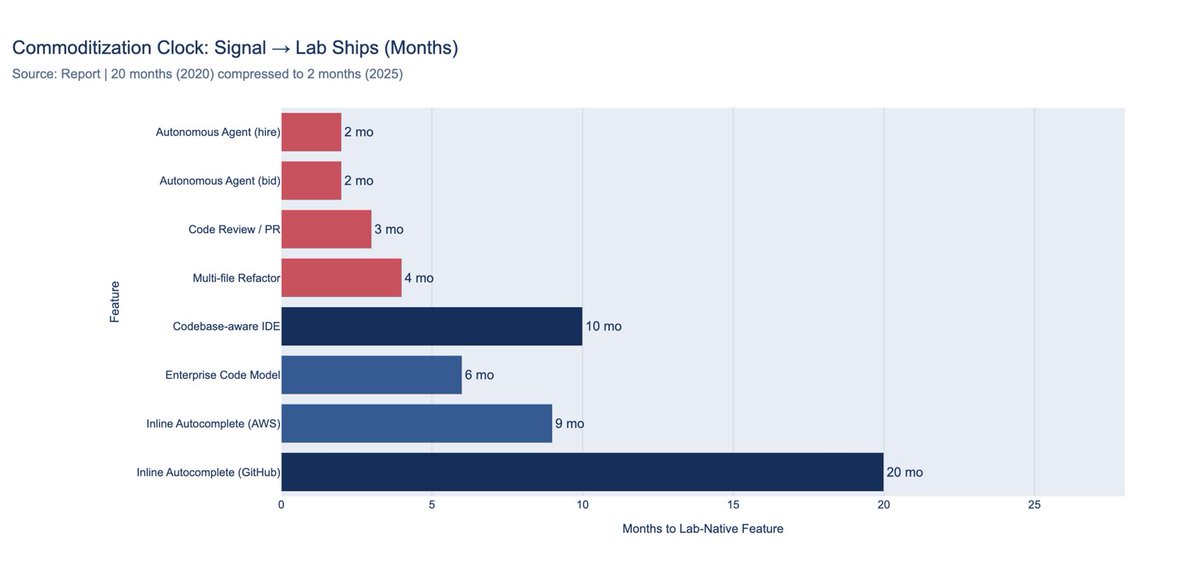

The Commoditization Clock

The most dangerous thing about building software in 2026 is that you can now measure exactly how much time you have before a lab ships your product as a feature. In 2020, when GitHub and OpenAI announced their partnership, it took 20 months for Copilot to reach general availability. By 2025, when Cursor acquired Graphite for over $290 million, Anthropic had native code review live in three months. The gap between a startup signaling value and a lab shipping a replacement has compressed from 20 months to one fiscal quarter. That is not a trend. That is a new law of nature for anyone building software on top of foundation models.

The reason the clock accelerated has nothing to do with labs getting smarter. It is that your fundraising announcement and your acquisition disclosures are now product roadmaps. The moment Cursor paid acquisition prices for Graphite, it told Anthropic two things: code review is the next high-value workflow step, and developers will pay transaction-level pricing for it. Anthropic did not need a product discovery process. Cursor ran it for them. Every round you raise, every acqui-hire you make, every feature you ship that gets press coverage is a prioritization signal for a team with 200 engineers and infinite compute sitting one layer below you in the stack.

The math at the model layer makes this worse than it looks. OpenAI earns 33% gross margins. Anthropic earns roughly 40%. Salesforce earns 75%. Adobe earns 88%. AI model companies are running on manufacturing economics, not software economics, which means every lab is under structural pressure to capture more of the application-layer margin before their own unit economics stabilize. When Anthropic observed Claude Code users repurposing the tool for non-technical workflows, they built and shipped Cowork in approximately ten days. They did not plan it. They watched their own usage data, saw a market, and shipped. Your traction is their market research.

The vibe coding layer is the fastest proof of how this plays out at scale. Lovable claimed $400 million ARR in February 2026. Working backward from their own reported figures, 180,000 paying customers at a blended rate between $12.50 and $25 per month implies annualized revenue of $27 to $54 million, not $400 million. The entire category runs on three simultaneous subsidies: labs pricing API access at adoption rates to drive market share, platforms extending that subsidy through discounts and free tiers, and VC capital absorbing the difference. The growth rates are real. The profitability is deferred and contingent on enterprise conversion accelerating before consumer churn catches up, API pricing staying stable, and labs deciding the application-layer margin is not worth taking directly. That last assumption is the one that fails first, every time.

The founders who come out of this are the ones who stop thinking about features and start thinking about what computer scientists call load-bearing infrastructure. Cursor's $29.3 billion valuation is a bet that VS Code familiarity and Fortune 500 procurement cycles create switching costs that outlast model commoditization. That might be right. But the developers have already moved. Claude Code sits at 46% most-loved among developers versus Cursor at 19%, and enterprises follow developers, always, just later. The only genuine protection in this environment is becoming so entangled in a specific customer's actual workflow that switching to a lab-native product feels like a regression, not an upgrade. Distribution compounds. So does commoditization. The question is which one compounds faster for your specific product. Most founders are betting on the wrong one.

7

1

5

512

3F VC retweeted

🚨Founders - These 4 minutes can save you in future.

Here's a quick breakdown of anti-dilution, ESOP Pool creation and Investor Consent matters:

youtu.be/KvngSS2n594?si=g0pr…

1

1

1

106