Contracted Controller Accountant, Speaker, and Founder of TBX Trial Balance Exporter for QuickBooks Desktop #TBX

Joined September 2013

- Tweets 2,712

- Following 1,550

- Followers 940

- Likes 6,430

368 Photos and videos

Apr 16

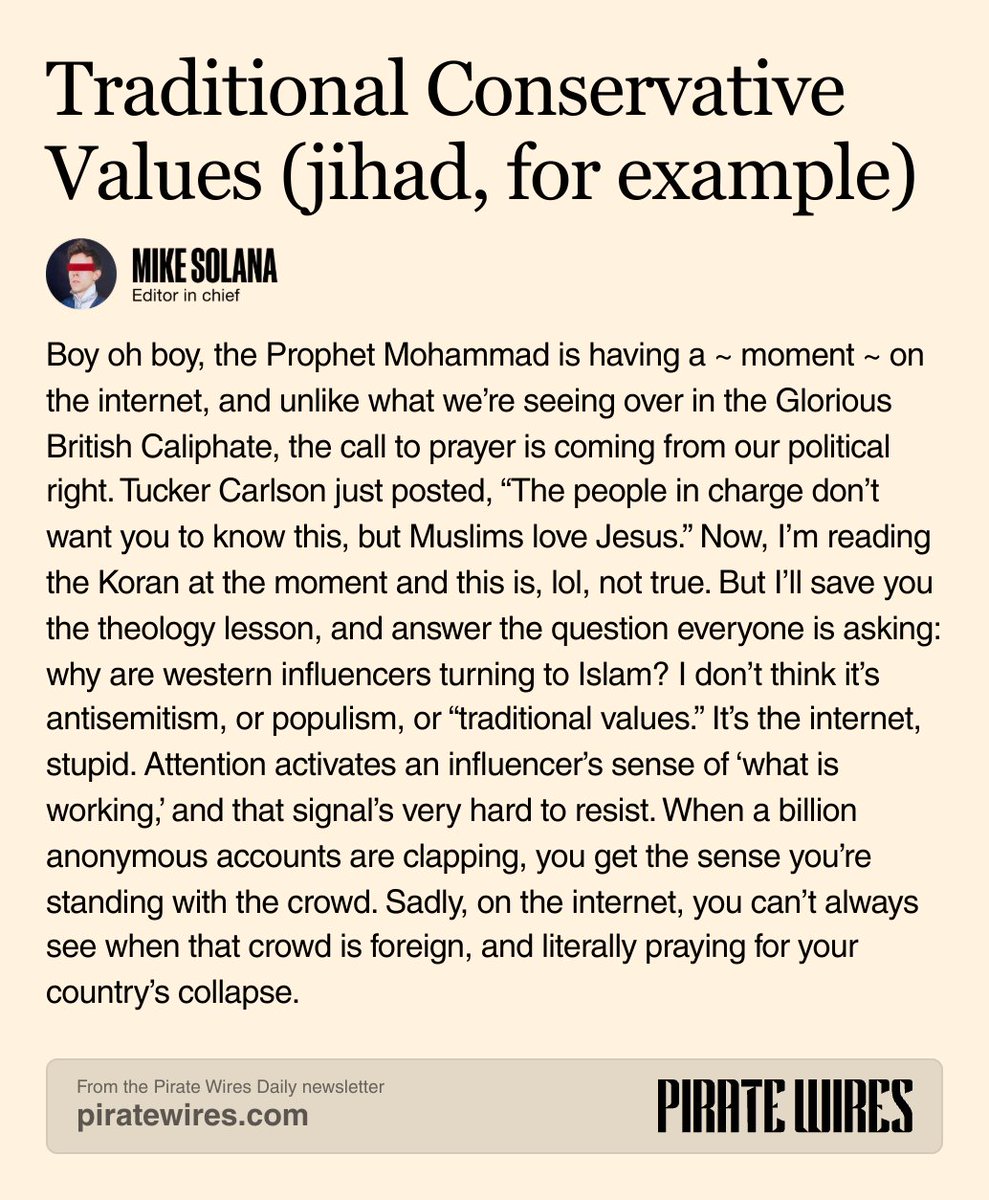

Americans praising and converting to Islam makes no sense to me. No Tucker, they don’t “love” Jesus.

18

Apr 9

What good is the daily @Truist Fraud Inspector if the check images will not render?! This is the second MONTH that the images just spin. I've tried different computers and browsers. I am forced to go to the activity list instead of the fraud detector page to search for the new checks and click, click, clicking to find their image. Calling and reporting this was horrible. You have no messaging available inside of the website while logged in. NO support other than the 1-800 number. It took forever answering a HUGE list of security questions to prove that I had an account with Truist. Why? I'm reporting an issue with your website. All that, just for someone to say, "Ok, I'll report it." Then nothing. Worthless. Am I the only one in the whole country having an issue?

I only have until 2 pm to read every single check and approve them and it was FAST when done with the Fraud Inspector. I quickly clicked on each check, which opened the image, and then hopped to the top and scrolled down and read them quickly. Now I click, click, click..

Hi there. We're sorry to hear you may have been a victim of fraud and understand how frustrating these situations can be. While Truist has many security measures in place to help protect your accounts, 1/3

157

𝕊𝕒𝕣𝕒 𝕃𝕒𝕚𝕕𝕝𝕒𝕨 - 𝕋𝔹𝕏 retweeted

Apr 2

Madden Orlovsky had a heartfelt message for his family and friends in honor of World Autism Awareness Day 🥹

This was a special moment for all of us at ESPN. Thanks, Madden and @danorlovsky7 ❤️

909

5,716

37,469

5,119,747

Mar 21

“All we want is a nap”. Amen

Mar 20

This millennial would like Gen X to sit down. Does he understand what would happen to the world if we decided to do that??

Take a listen to this response.

It is perfection! 👌🏼

51

Mar 21

What the hell @QuickBooks @IntuitAccts @Intuit ? Yet ANOTHER USELESS “improvement” of a hard to read mixed-font. Forcing us to export to Excel or buy a reporting add-on. FIRE your developers! Stop wasting our time on dumb $%^O*%T. Please stop A/B testing in a live program! Find other guinea pigs. It is a horrible way to run a SAAS company. Another reason that companies are chomping at the bit for a decent replacement to raise its head. Why don’t you see that you are pushing customers away? The arrogance and lack of listing to customers is off the chart.

2

4

212

Mar 18

What good is the daily @Truist Fraud Inspector if the check images will not render? This is the second week of searching for the checks and click, click, clicking to find their image on the activity list instead of the fraud detector page.

1

160

Mar 18

Make it stop. Investigate every single state.

Mar 17

🚨 Here is the full 40 minutes of my crew and I exposing California fraud, Minnesota was big but California is even bigger... We uncovered over $170,000,000 in fraud as these fraudsters live in luxury with no consequences. Like it and share it, the fraud must STOP.

We ALL work way too hard and pay too much in taxes for this to be happening. These fraudsters have been able to defraud American taxpayers for years without any pushback from the public and politicians.

It is time to EXPOSE IT ALL and end America's fraud crisis.

27

Mar 14

Something positive today! Smile.

Mar 14

Love in its purest form: wife helps her blind husband follow their son's game, recounting each play with caresses on his back.

This is genuinely heartwarming! ❤️

37

𝕊𝕒𝕣𝕒 𝕃𝕒𝕚𝕕𝕝𝕒𝕨 - 𝕋𝔹𝕏 retweeted

Feb 6

This is great parenting.

We need more of this.

142

369

3,982

103,156

30 Dec 2025

What if your clients could capture and organize (non-AR) check receipts and deposits in a way that makes YOUR job easier and THEIR burden lighter?

Tell me - What is painful about gathering deposit information and entering Sales Receipts and customers/donors?

📢 CALLING QUICKBOOKS PUBLIC BOOKKEEPERS/ACCOUNTANTS FIRM OWNERS

I'm building ReceiptLogic for check-heavy industries (nonprofits, membership orgs, property management). The idea: streamline the whole process from receipt image, coding, to QuickBooks posting.

Could this work? I need to validate pain points and get feedback on a working prototype.

🎯 LOOKING TO CHAT WITH 5-10 people who:

✓ Work with clients processing >50 (non-AR) checks monthly in QuickBooks

✓ Currently deal with manual Sales Receipt entry or deposit customer lists

✓ Understand pain points for clients, bookkeepers/accountants, AND auditors

💰 IF YOU FIT THE ABOVE - I'M OFFERING:

→ $50 Amazon gift card for 20-25 minutes of your time

→ Early look at the prototype

→ Zoom call (camera optional)

This is pure research—no sales pitch. Just want to know if I'm solving real problems or wasting my time! Comment or Message if this fits you!

#nonprofit #CFO #accounting #TaxTwitter #quickbooks #CRM

88

🤔

6,987

38,191

297,306

31,540,744

𝕊𝕒𝕣𝕒 𝕃𝕒𝕚𝕕𝕝𝕒𝕨 - 𝕋𝔹𝕏 retweeted

1 Nov 2025

"40 Years Ago, A Cholesterol Level Of 300 Was Perfectly Fine & It's Perfectly Fine Today."

Barbara O'Neill

"Now We Are Told We Can't Go Above 190"...Every Time They Lower The Numbers, Millions More People 'Need' Statin Drugs.

That's Not Healthcare, That's A Strategy For Profit.

93 million Americans are currently on Statin drugs, making the pharmaceutical industry a yearly profit of $22 Billion dollars.

As of 2025,Statins have now reached all age levels, the FDA has approved Statin drug therapy to children 8yrs old & over.

The goal of the famous Framingham Heart Study was to prove that cholesterol causes heart disease. The study failed miserably...in fact it proved the opposite.

The findings of the study actually shows that when cholesterol is lowered...mortality INCREASES. In the 30 year follow-up study published in 1987, the authors reported that ‘For each 1 mg/dl drop in total cholesterol per year, there was an 11% increase in coronary & total mortality’.

World renowned Lipidologist, Dr Uffe Ravnskov, in the largest systematic review of 19 cohort studies including more than 68,000 people (>60 years of age), found that those with the highest LDL-C levels lived the longest. The higher your LDL, the longer you live.

Dr Ravnskov stated, "Treatment with a statin is an iatrogenic mitochondrial disease...a physician caused death."

"Physician's have broken their oath to 'first do no harm' by prescribing deadly cholesterol lowering statins that cause Parkinson's Disease, Alzheimer's, Chronic Fatigue, Cardiomyopathy, Diabetes, Fibromyalgia, Kidney Disease, Heart Failure, Multiple Sclerosis, Epilepsy & much more."

Cholesterol is the building block to every cell membrane & lowering it harms every cell in the body. There are no benefits in taking a cholesterol lowering statin.

The brain is supposed to be rich in fat & cholesterol for optimal cognitive ability & protection from neurodegenerative disease.

Statins cross the blood brain barrier & inhibit the brain from having its optimal ratios of 60% fat & 25% cholesterol.

Statins cause a multitude of side effects that will cause a low quality of life. Statins do not lower Cardiovascular Disease, Stroke, Heart Attack or Mortality.

Statin Medications Cause The Following Chronic Conditions...

Aphasia

Dementia

Alzheimer's Disease

Cancer

Pancreatitis

Parkinson's Disease

Muscle Tearing & Pain

Fatigue & Weakness

Neuropathy

Hormone Deficiency

Brain Damage

MS Multiple Sclerosis

Depression & Suicidality

Liver Damage

New Onset Type 2 Diabetes

Heart Failure

Vertigo

Cognitive Impairment

ALS (Lou Gehrig's Disease)

👇The Higher Your LDL, The Longer You Live👇

meddocsonline.org/annals-of-…

👇High Cholesterol Prevents Atherosclerosis👇

academic.oup.com/qjmed/artic…

👇Statins Extend Life Only 3.2 Days👇

pubmed.ncbi.nlm.nih.gov/2640…

Speaker: Barbara O'Neill, Naturopathic Nutritionist

Video: @healthsolutions

105

1,822

4,678

156,755

10 Nov 2025

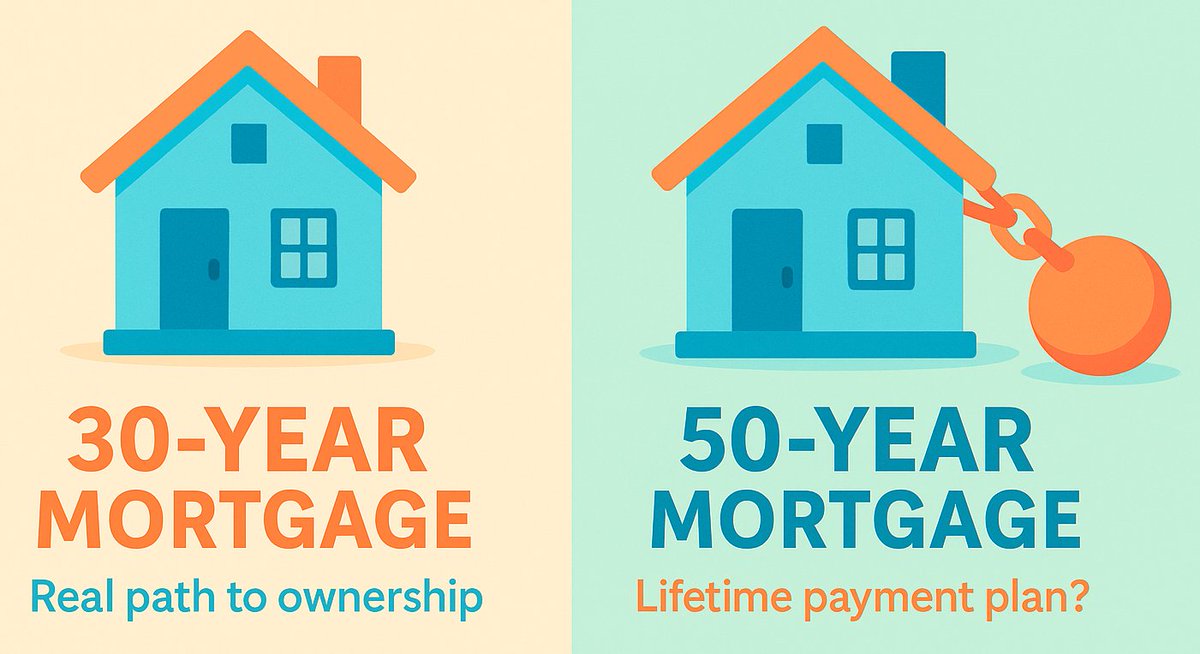

We’re in a real housing cost-of-living crisis. Food, rent, and home prices are brutal. Young adults are locked out of homeownership. So I actually like that this administration is at least trying new ideas — including the talk of a 50-year mortgage. Doing nothing isn’t working.

But here’s my concern: on paper, a 50-year loan looks great. Lower monthly payment, easier to “qualify.” In real life, in a world where people finance pizza (Holy new hell, it's a thing!) and only look at “Can I swing things this month?”, it can turn into a long-term debt trap. It is the same psychology car dealers use when they flash a low monthly payment instead of telling you what the car really costs or how many payments. (Pet peeve, Toyota)

The focus stays on today’s payment, not the total cost or how long you’re locked in. The real goal should be to own your home. Stretch that term to 50 years and you’re paying mostly interest for a long time before you even dent the principal.

I’m not anti-mortgage. Back when you could refi with no closing costs, (remember that?!) I restarted 30-year loans more than once for large projects such as a roof, HVAC, renovation and an addition. I chose 30-years to keep the REQUIRED payment low so if I got sick or lost income, I wouldn’t lose my house.

The difference? I had a clear plan: prepay the principal aggressively and enter retirement with no mortgage. My required payment was around $900; I actually pre-paid an additional $2,000–$2,500 a month and killed the mortgage well before my 60s.

So my take: experimenting with solutions is good. But a 50-year mortgage in a society that doesn’t teach basic money skills? It might help a small, disciplined minority — and quietly trap a lot of others in 50 years of payments.

37

5 Nov 2025

APP ALERT!!

Have you ever flipped through an online magazine and thought, “I wish I could do that with my PDFs”?

You can. 📖

I found an easy tool that does it: Flip Booklets. It turns PDFs into sleek, interactive flip books you can share with one link — perfect for training docs, my app manuals, and SOPs.

Easy to edit, inexpensive, always current, and professional!

👉 Affiliate link - because I love it! flipbooklets.com?aff=G7iAhYq…

25

𝕊𝕒𝕣𝕒 𝕃𝕒𝕚𝕕𝕝𝕒𝕨 - 𝕋𝔹𝕏 retweeted

21 Sep 2025

I listened to Erika Kirk’s full speech at the memorial, and I want to share a few thoughts that came to me while live streaming the event. This is not political.

First, I should say that I grew up as a Muslim in a Muslim country. I don’t know enough about Christianity to say if what I witnessed is rooted in faith or culture. But what struck me most was how, even though death is heavy and this was by nature a sad occasion, the entire event carried a celebratory spirit that honored life.

That contrast hit me deeply. In Islam, even though we believe that good people go to heaven, the relationship with God is taught through fear. Funerals are overwhelmingly sad, often filled with warnings of the terrifying first night in the grave. Growing up hearing that, and then witnessing people celebrate life, speak of God’s love, and remember someone through the impact he had on others; it felt so refreshing, so positive.

Second, I was profoundly moved by @MrsErikaKirk’s words. I cannot fathom the strength it takes to stand and deliver such a meaningful speech after losing the love of your life. But even more than that, the grace it takes to forgive the very person who destroyed your world. I cannot imagine myself standing on a stage, sending love to those who cheered your husband’s murder, or inviting others to spread God’s love in response because, as she said, “we do not respond to hate with hate.” That is powerful beyond words.

Again, I am ignorant when it comes to Christianity, but if this is what it truly embodies, then I am envious of those who get to experience that feeling.

10,397

17,830

128,787

5,249,700

14 Sep 2025

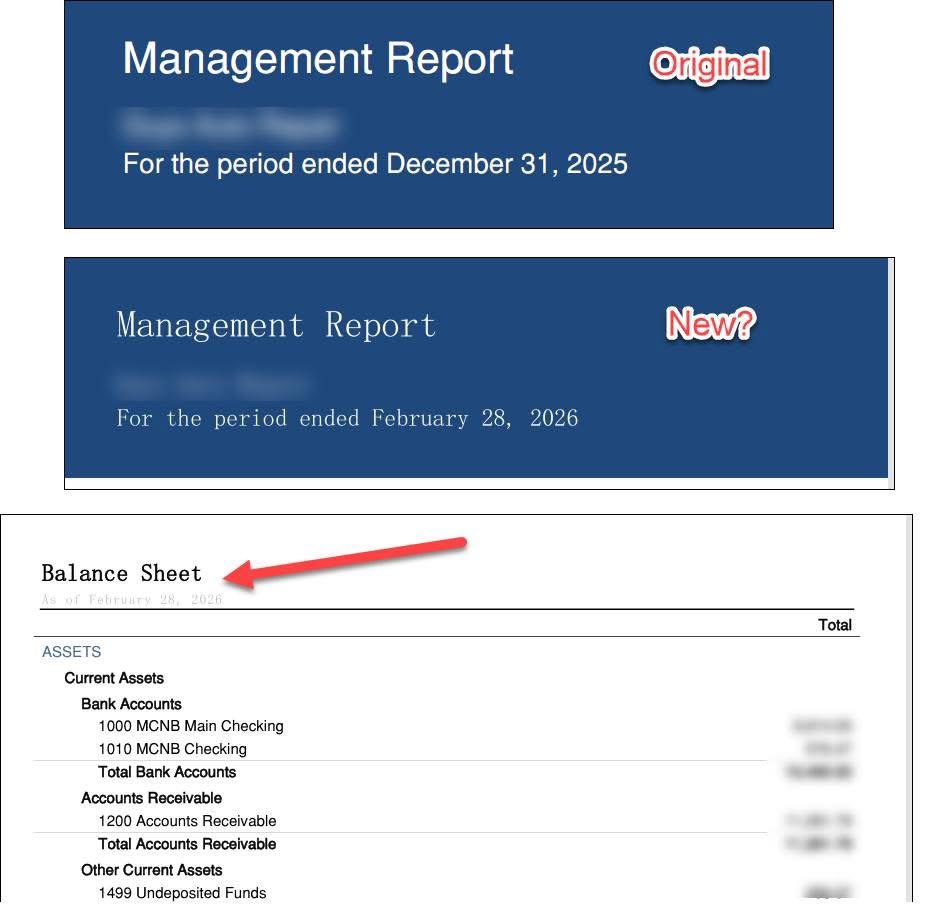

Growing out of QuickBooks Desktop is a win—but beware of losing your comparative financials.

That’s where TBX Trial Balance Exporter helps:

• Export monthly balances by class

• Create clean journal entries (CSV or IIF)

• Import into QBO, NetSuite, Sage Intacct & more

The fastest way to take your history with you 🚀

👉 tools.asbinc.net #CFO #DataMigration #ERP #Accounting #CPA

106

𝕊𝕒𝕣𝕒 𝕃𝕒𝕚𝕕𝕝𝕒𝕨 - 𝕋𝔹𝕏 retweeted

11 Sep 2025

Democrats are Losing EveryOne EveryWhere…

270

4,431

28,302

338,669

11 Sep 2025

Great advice.

11 Sep 2025

Social media guide:

Be vigilant in guarding your feelings, especially anger and despair.

Filter the information and posts you are ingesting. Focus on good, encouraging, positive things, while taking in important news as necessary.

Mute/block inflaming and provoking people.

169