Founder @prometheusmacro

Joined December 2024

- Tweets 9,295

- Following 696

- Followers 7,535

- Likes 5,250

794 Photos and videos

Pinned Tweet

3 Dec 2024

Alright, let’s do this twitter thing.

1/ I started @prometheusmacro in 2020 as a free blog to develop and share my ideas on macro and investing. Fast forward to today and Prometheus is a fast growing macro research firm servicing some of the biggest institutions in the world…

7

4

82

78,589

@aahan_prometheus retweeted

For years, buybacks have been a tailwind for stocks.

On the latest First Principles, @dampedspring breaks down what happens when that tailwind runs into a wave of new issuance.

🎙️bit.ly/4xwX8i0

🍏bit.ly/4gtOsCS

We discuss:

☑️ What happens when buybacks turn into issuance

☑️ The funding of AI CapEx

☑️ How dissaving and the wealth effect are supporting the economy

☑️ Why falling oil may shift inflation rather than end it

☑️ How Fed policy might change under Warsh

1

4

13

13,727

🔥🔥🔥

Third in our monthly series with Excess Return team and me. Enjoy.

2

731

GM

(Say it back)

It’s time to have a conversation about bonds

4

22

2,123

0.4 sharpe

19h

Jeff DeGraaf, who does a lot of good quant work, mentioning that number one signal for recognizing when the momentum unwind is imminent is the behavior of credit spreads (I assume he means widening)

2

26

14,109

FYI this was published last week

2

12

2,036

@aahan_prometheus retweeted

Yes… a super interesting CHART CRIME

4

1

12

1,742

Interesting

3

1

23

8,414

At a macro level investors are rarely *forced* to buy stocks.

But more often than not, they are forced to sell them (vol, drawdown, risk etc).

Provide those forced sellers some liquidity and you do decently well.

31

2,271

@aahan_prometheus retweeted

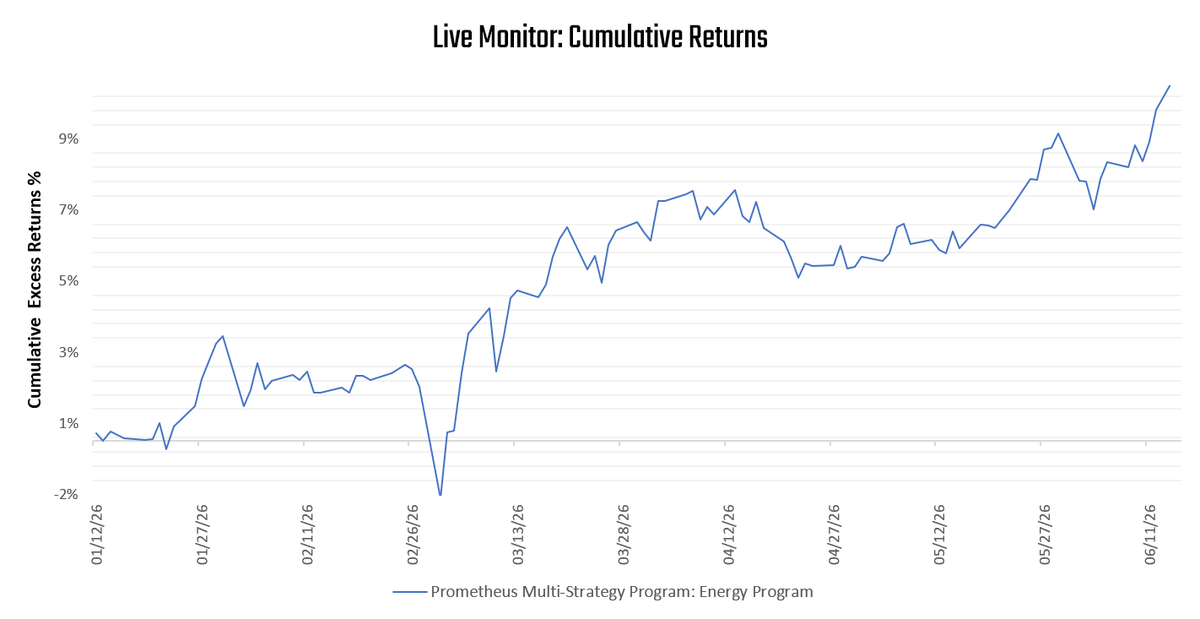

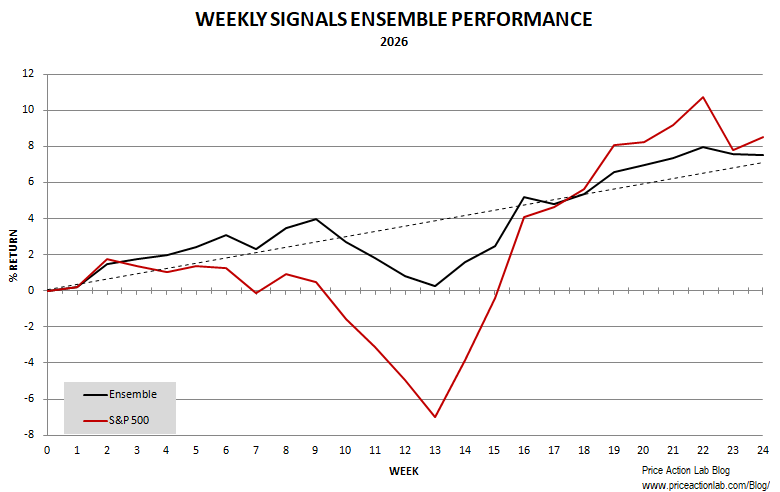

Jun 15

Weekly Signals update for subscribers. YTD Sharpe ratio 2.5, MAR 2.1. Link in reply 👇

Jun 13

Weekly Signals update for subs. YTD Sharpe ratio 2.5, MAR 2.1. Link in reply 👇

1

1

1,100

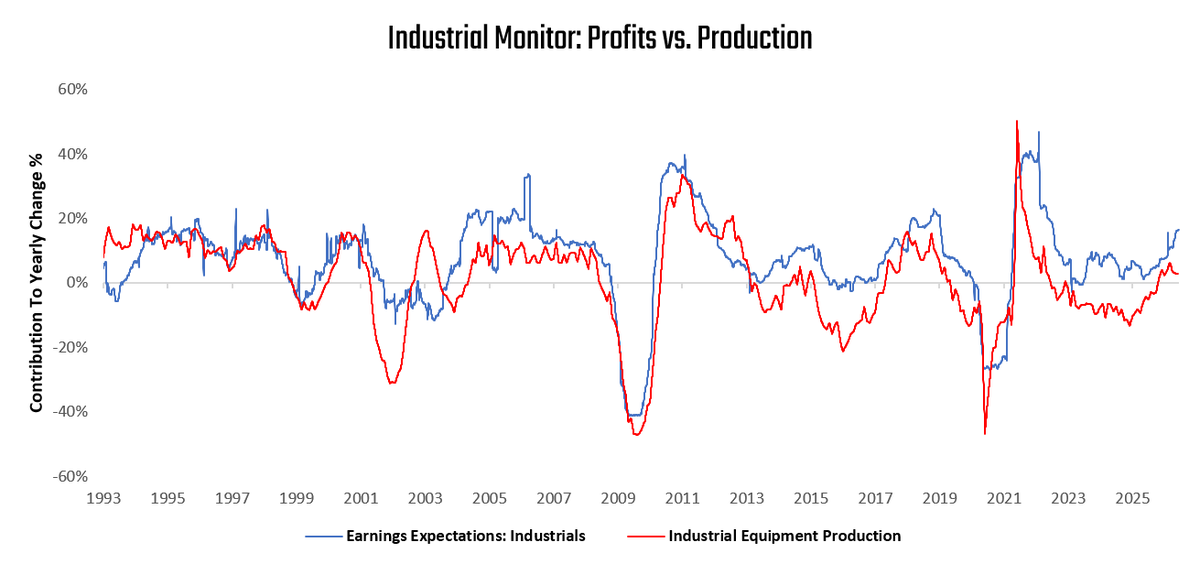

The latest industrial production shows some signs of potential slowing for industrial equities. Nothing big.

Meanwhile, earnings momentum for the industrial sector remains very high.

Not a force to fight

1

14

1,530

Equity signal cut in half.

Crude still going, but should have stops for a speculative reversal

Top 🤖

Long S&P

Short Crude

1

22

4,228

Okay fine

I'll promote my oil analyst to associate PM

He's on the phone with my oil analyst

(trying to poach him)

@ptj_official plz dont

1

10

1,540

This could be us

But you playin

1

12

1,727

Beep boop

Top 🤖

Long S&P

Short Crude

1

13

2,134

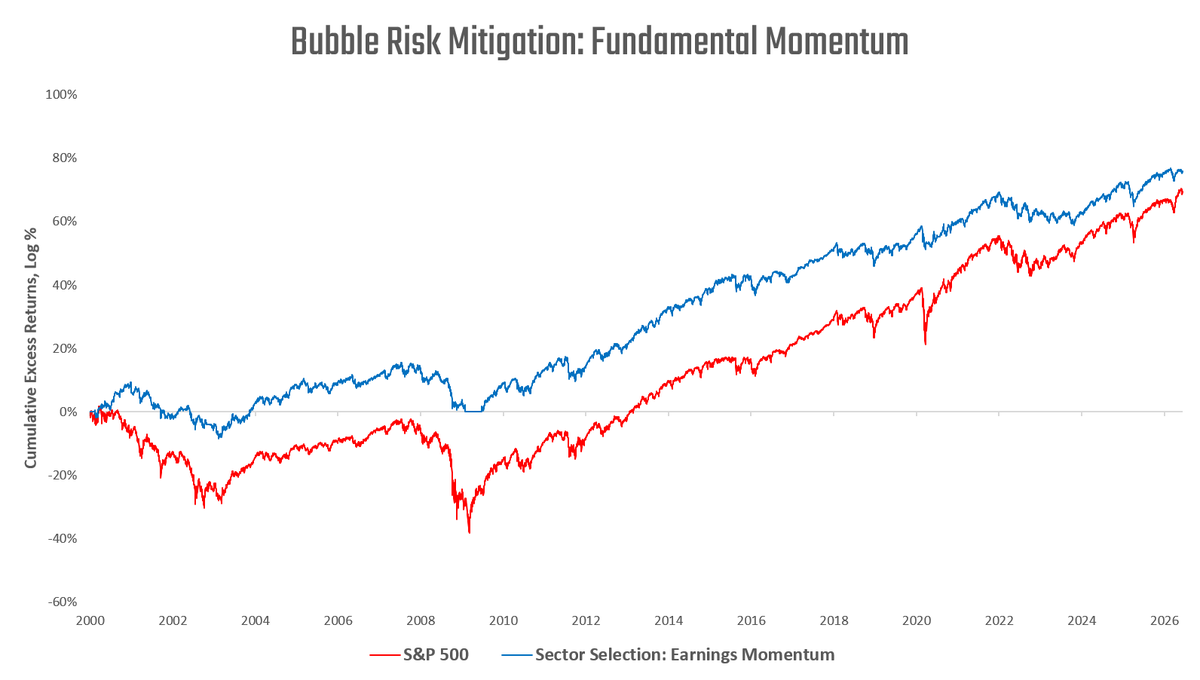

Worried about a bubble?

There are many things you can do.

One of those things is to keep a very careful watch of earnings momentum. You pick how you define that.

When it falls, exit the sector. In a true bubble, you'll find you exit almost all sectors in succession:

3

47

2,757

@aahan_prometheus retweeted

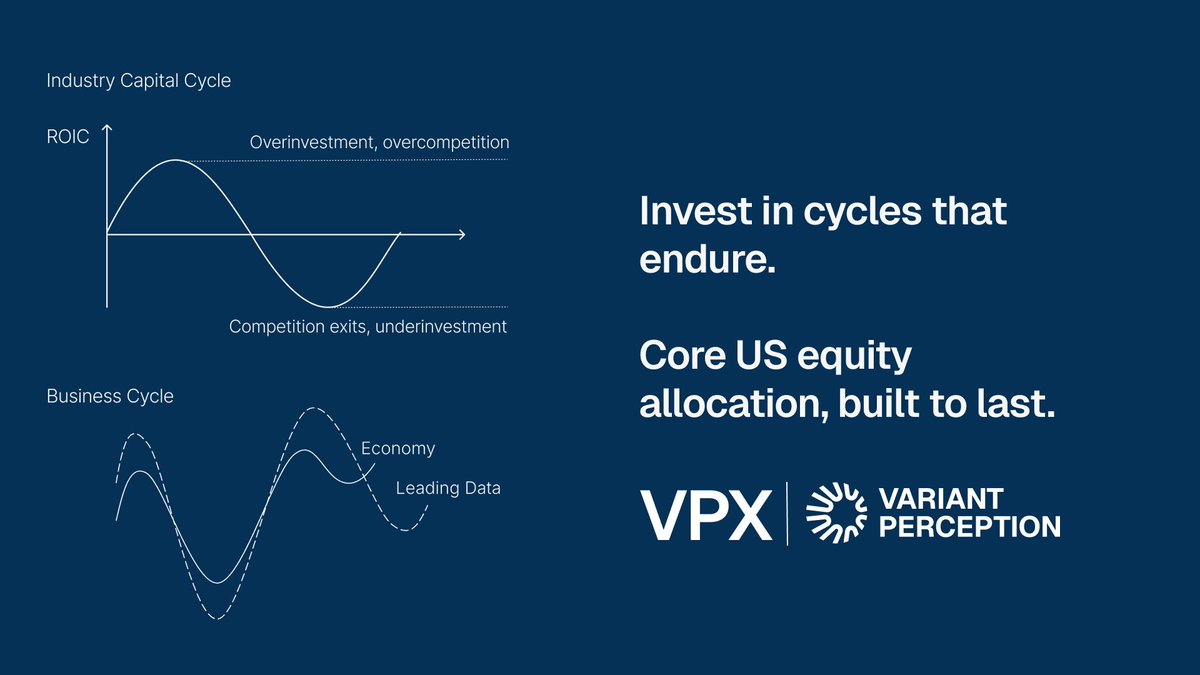

Invest in cycles that endure. The rhythm of markets is shaped by the Business Cycle and Industry Capital Cycles.

We analyze the capital cycle seeking to identify where earnings attract competition (reducing profits) or where competition exits (increasing profits). We combine this with Leading Data on the economy to manage business cycle risk.

$VPX is a cycle-aware core equity allocation, built to last.

1

2

8

1,889