Venture Capital Funds for RIAs | Pre-IPO Stock Research | AG Dillon & Co

Joined September 2011

- Tweets 3,317

- Following 1,284

- Followers 1,761

- Likes 2,307

2,418 Photos and videos

Pinned Tweet

Apr 25

THE CAP TABLE - APR 22, 2026

"No one has any compute = AI data centers are a great investment (in our opinion)"

Link to watch video = youtube.com/watch?v=hArtSgwr…

Aaron Ross and I started this podcast a few weeks back. Mr. Ross is a super sharp guy and I highly recommend folks reach out to him if you're interested in his pre-IPO stock research or care to learn more about the pre-IPO stock asset class. You can contact Aaron at aaron.ross@rosspreipo.com.

Our discussion this week focused on AI data centers. The single most underappreciated dynamic in markets today ... in my opinion ... is the compute shortage powering artificial intelligence. Roughly 30% to 50% of US data centers are currently running behind schedule, while demand continues to compound at a pace few investors fully appreciate. Heavy users of Claude, ChatGPT, and Grok are routinely hitting daily usage caps before noon. Software developers have begun launching autonomous coding agents that run uninterrupted for 13 days at a time, then immediately queuing the next job behind it. Inside major enterprises, executives are starting to ration tokens across departments the way they once allocated headcount. Within the next 24 months, we expect virtually every white collar worker to have automated agents executing tasks in the background of their day, and at that point the global compute demand curve becomes staggering very quickly. Compute is on track to become one of the most strategically important commodities on the planet, and we would not be surprised to see a tradable futures market for AI compute "tokens" emerge within the next several years.

For investors, this points directly at the AI infrastructure layer: semiconductors, data centers, and electricity production. These are the picks and shovels of the buildout, and on a risk adjusted basis we view the setup as one of the most compelling in the market today. Compute access is also reshaping competitive dynamics among the model providers themselves. Anthropic currently leads on model quality but remains constrained by its reliance on hyperscaler capacity. OpenAI has absorbed meaningful dilution to fund its own buildout, though that proprietary compute may translate directly into faster revenue growth from here. xAI's Colossus cluster in Tennessee, now home to 555,000 GPUs, gives Elon Musk's team more proprietary compute than Anthropic and OpenAI combined, and the company has already begun selling capacity to third parties such as Cursor (...although it was later announced this week that SpaceX/xAI is going to buy Cursor for $60 billion). On the private side, the names we are watching most closely include the Neocloud operators (Lambda Labs, Together AI, Crusoe, Nscale, Vast, Fermi), the inference specialists (GroqCloud, Cerebras), and the orchestration layer (Baseten, Fireworks AI). Our screening framework is straightforward: we want AI infrastructure companies with a strategic partnership with Nvidia and Nvidia on the cap table as an investor. Check those two boxes, and the setup gets very interesting.

2

754

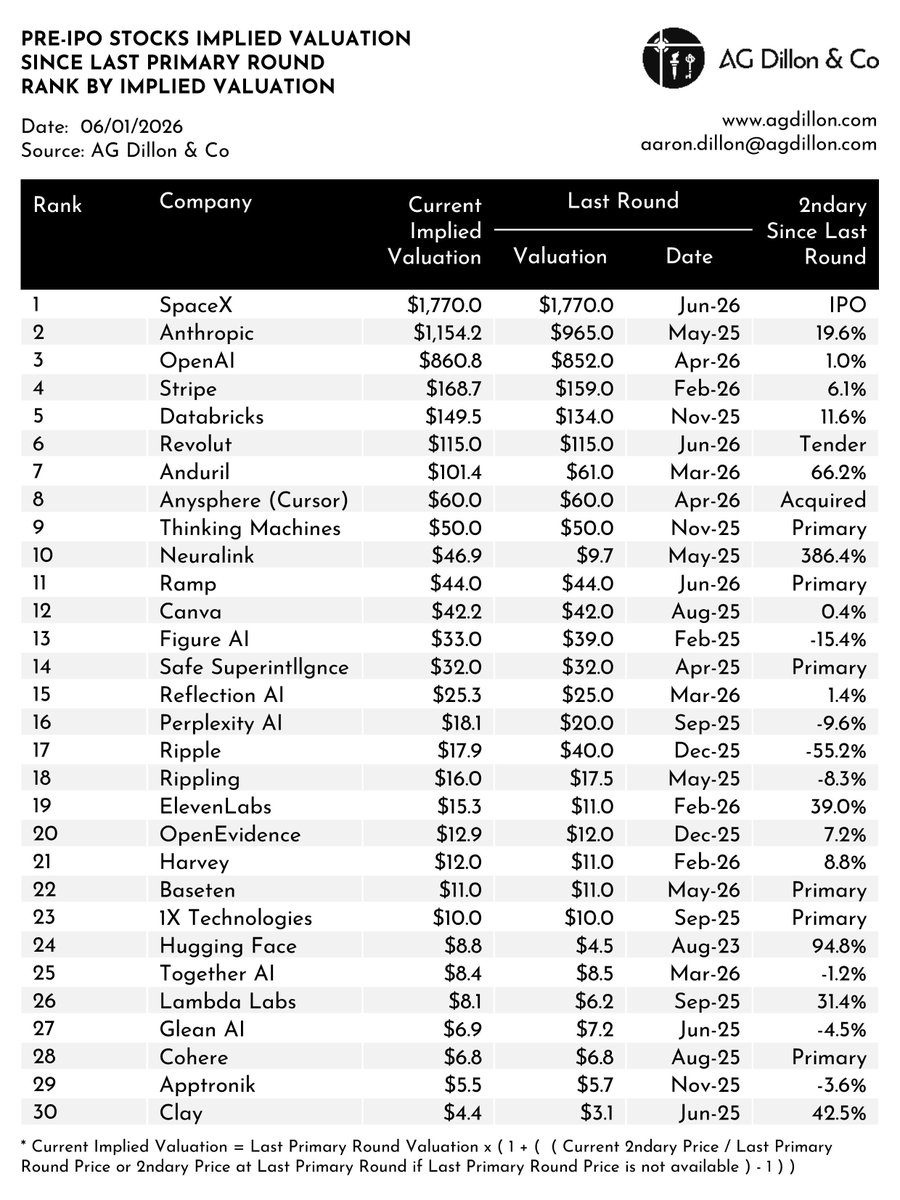

Pre-IPO Stock Secondary Market Valuation | as of Jun 1, 2026 | Download full report = agdillon.com/reports

5

451

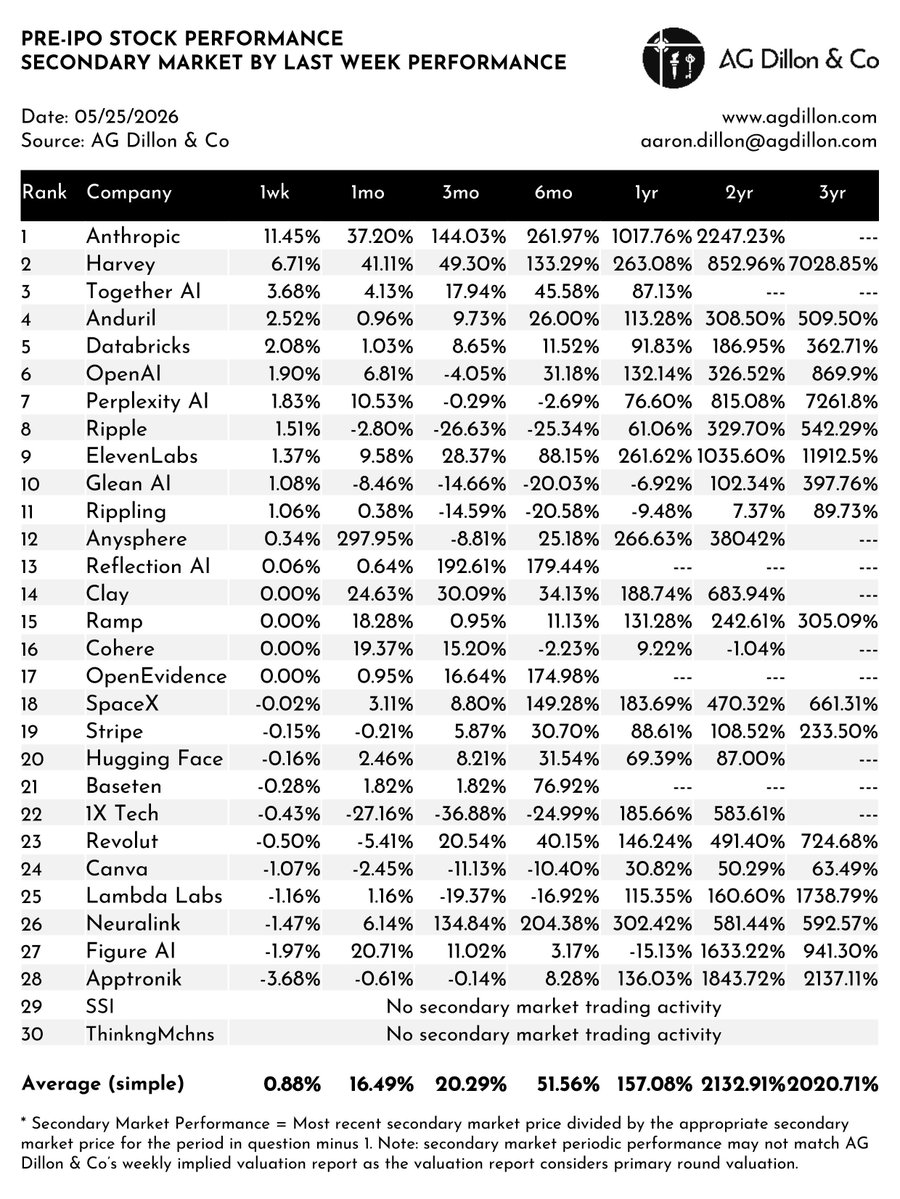

Pre-IPO Stock Secondary Market Performance | as of Jun 1, 2026 | Download full report = agdillon.com/reports

225

May 29

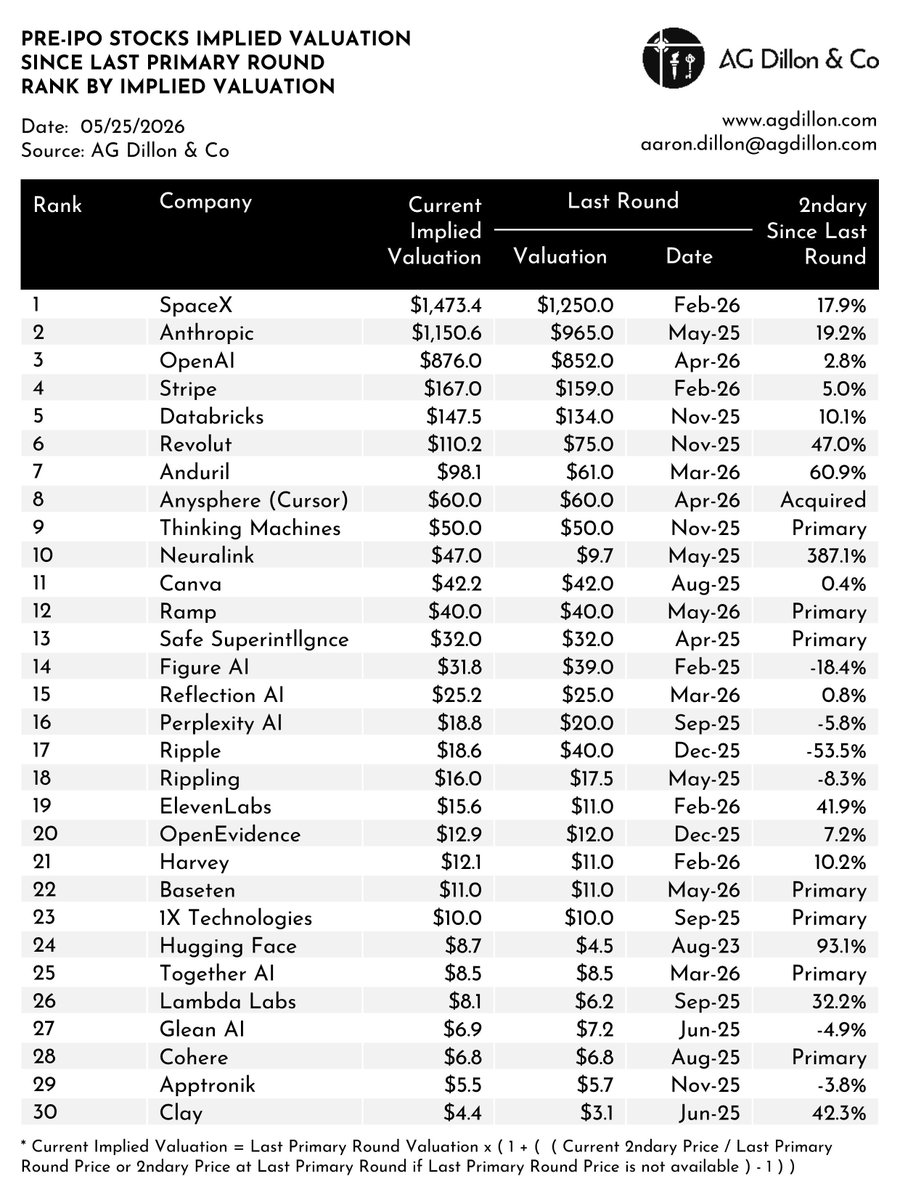

Pre-IPO Stock Secondary Market Valuations | as of May 25, 2026 | Download full report = agdillon.com/reports

2

290

May 29

Pre-IPO Stock Secondary Market Performance | as of May 25, 2026 | Download full report = agdillon.com/reports

1

205

May 21

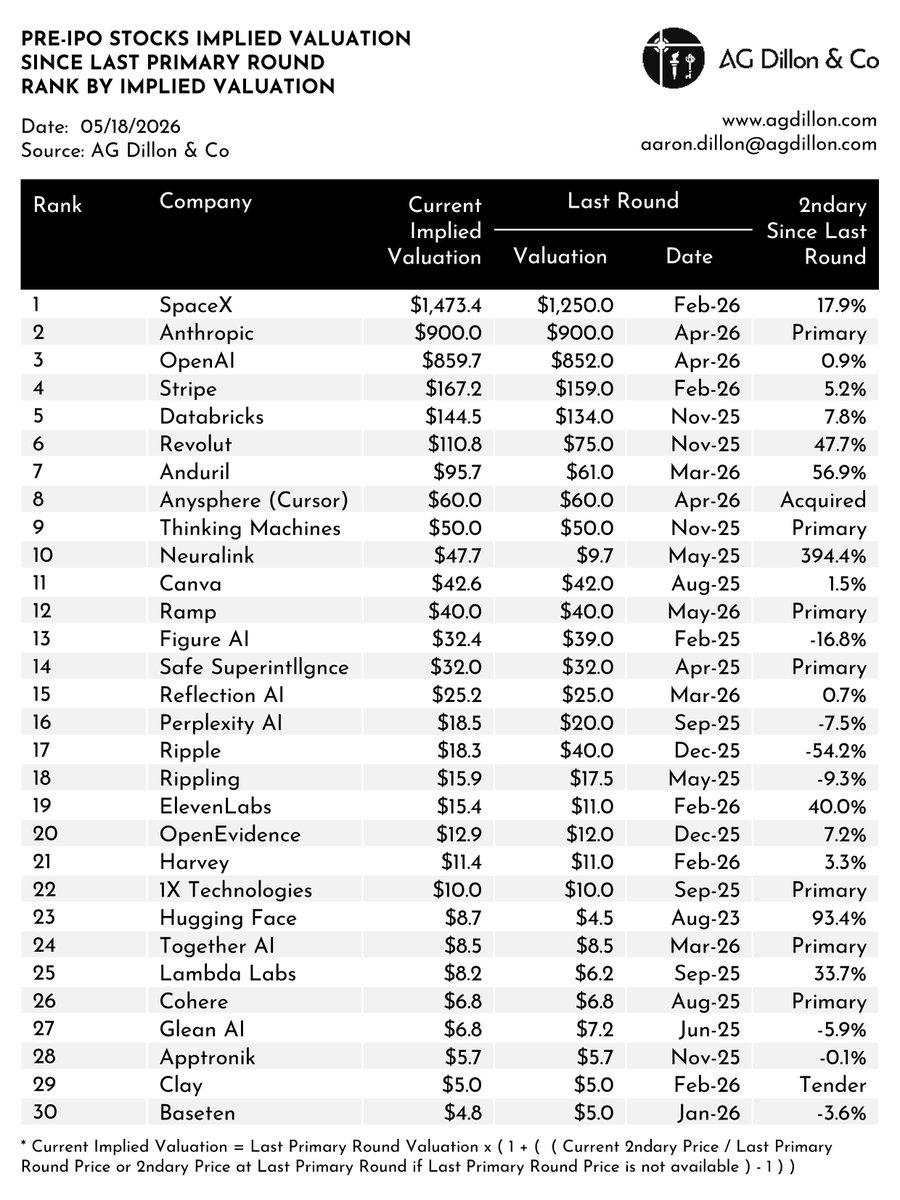

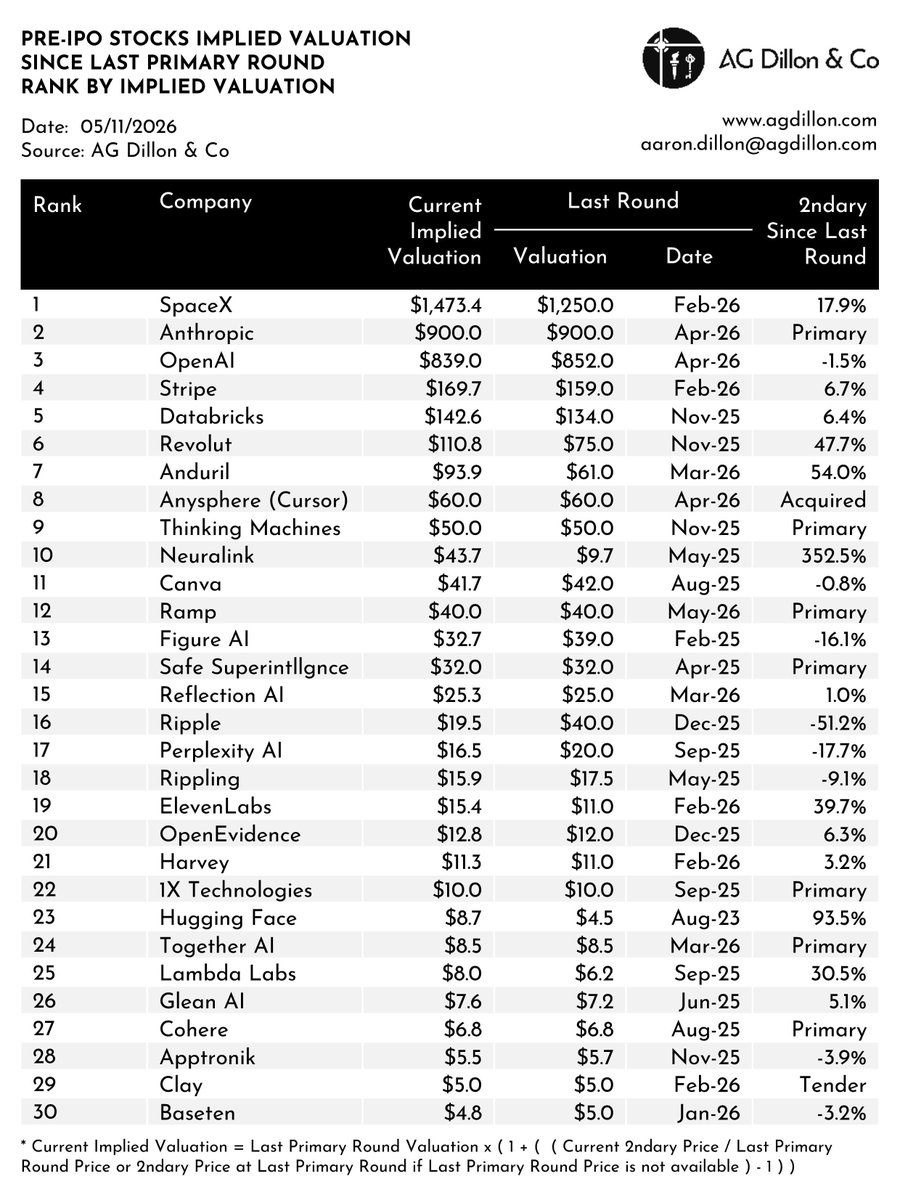

Pre-IPO Stock Secondary Market Valuations | as of May 18, 2026 | Download full report = agdillon.com/reports

2

7

307

May 21

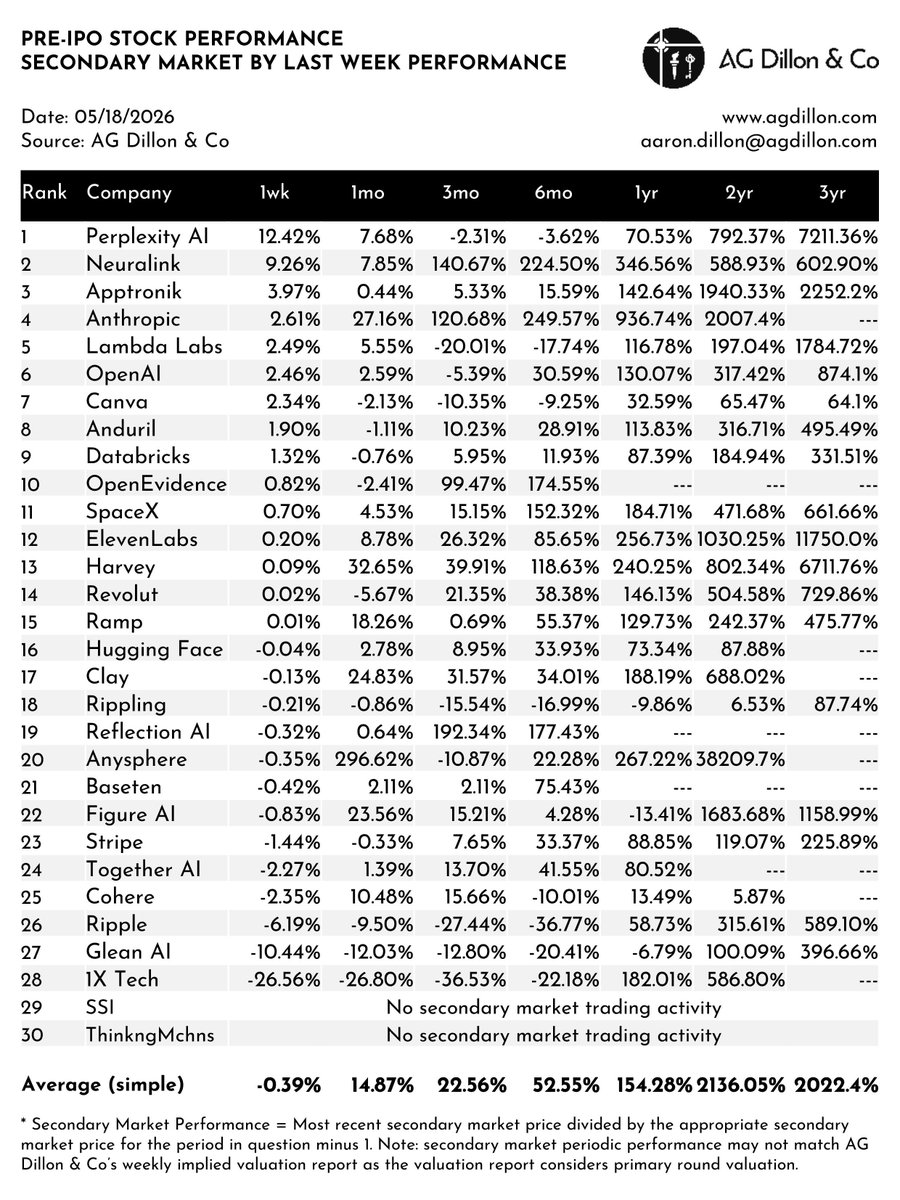

Pre-IPO Stock Secondary Market Performance | as of May 18, 2026 | Download full report = agdillon.com/reports

1

266

May 15

Pre-IPO Stock Secondary Market Valuations | as of May 11, 2026 | Download full report = agdillon.com/reports

1

3

299

May 15

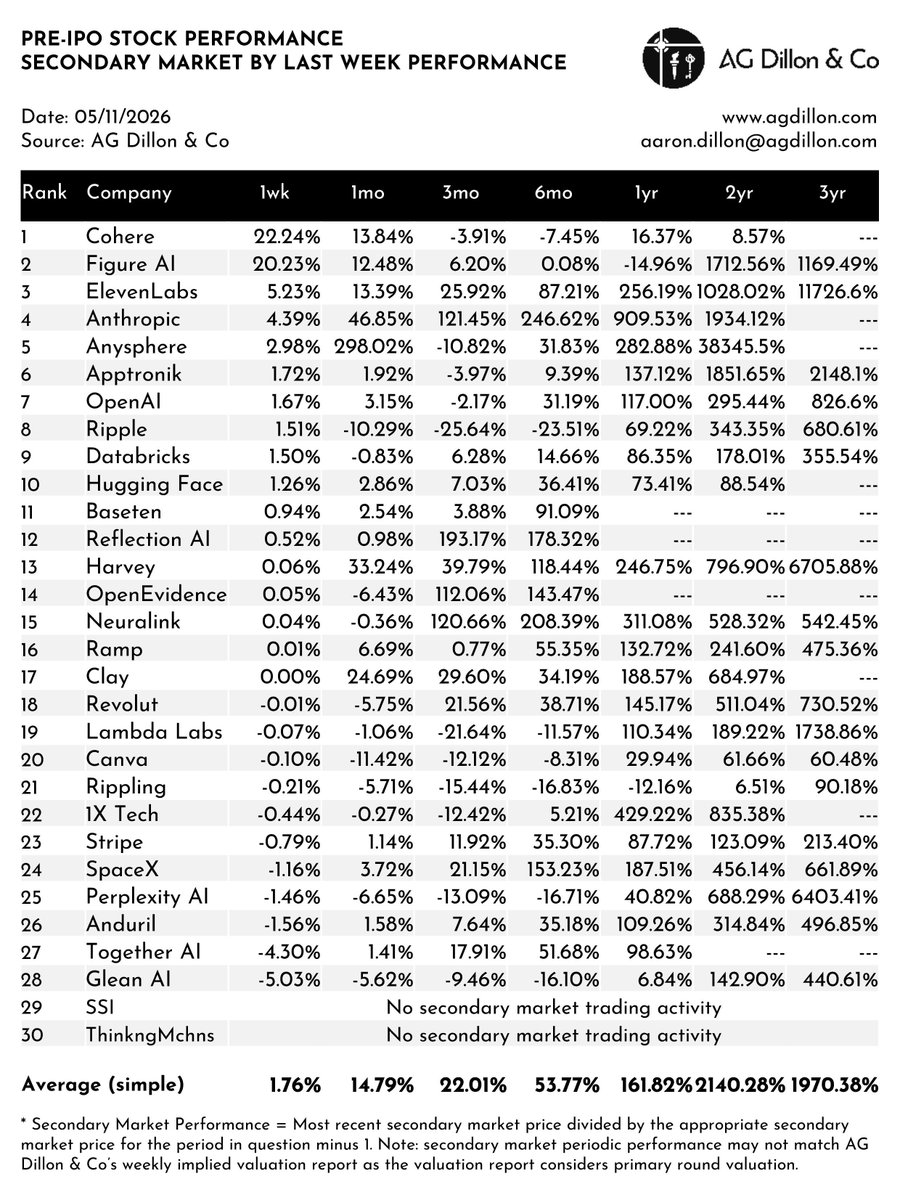

Pre-IPO Stock Secondary Market Performance | as of May 11, 2026 | Download full report = agdillon.com/reports

1

380

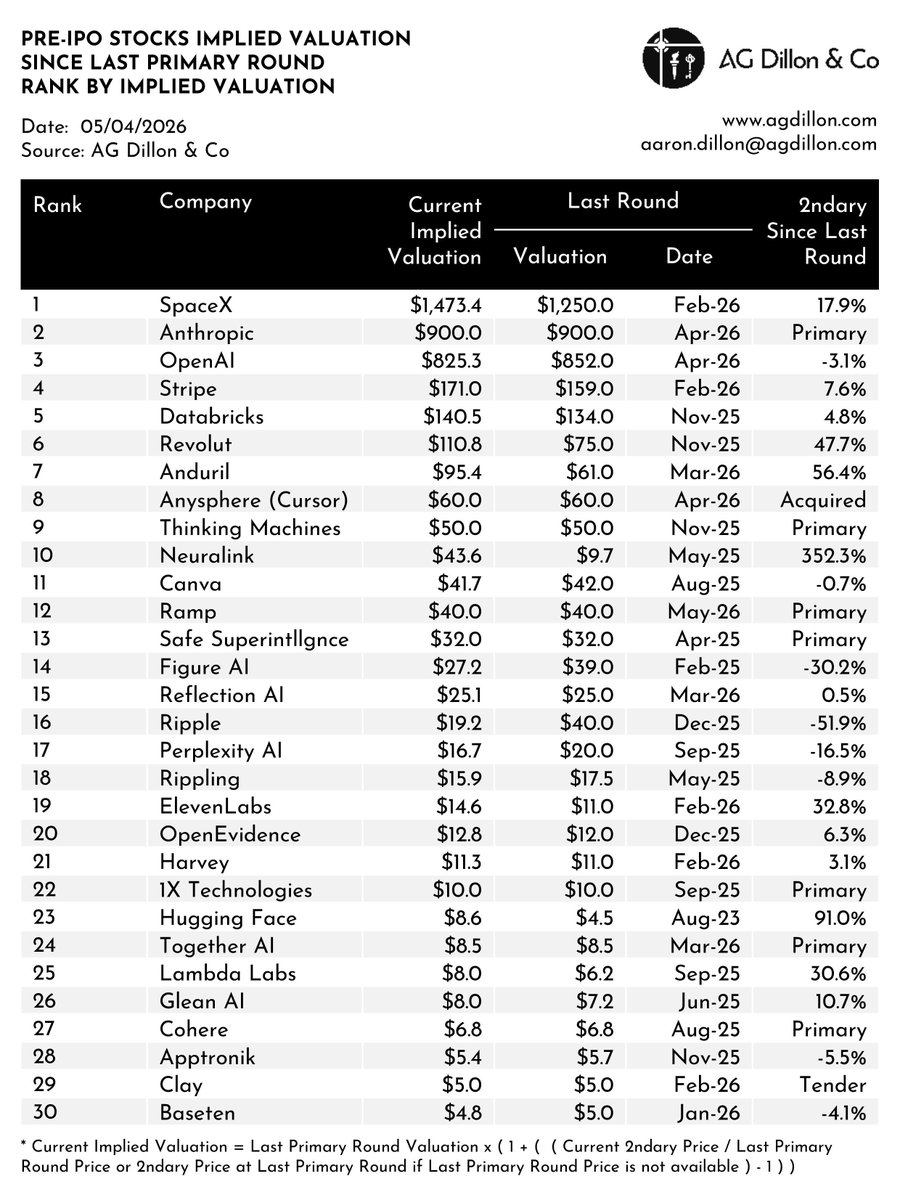

Pre-IPO Stock Secondary Market Valuations | as of May 4, 2026 | Download full report = agdillon.com/reports

300

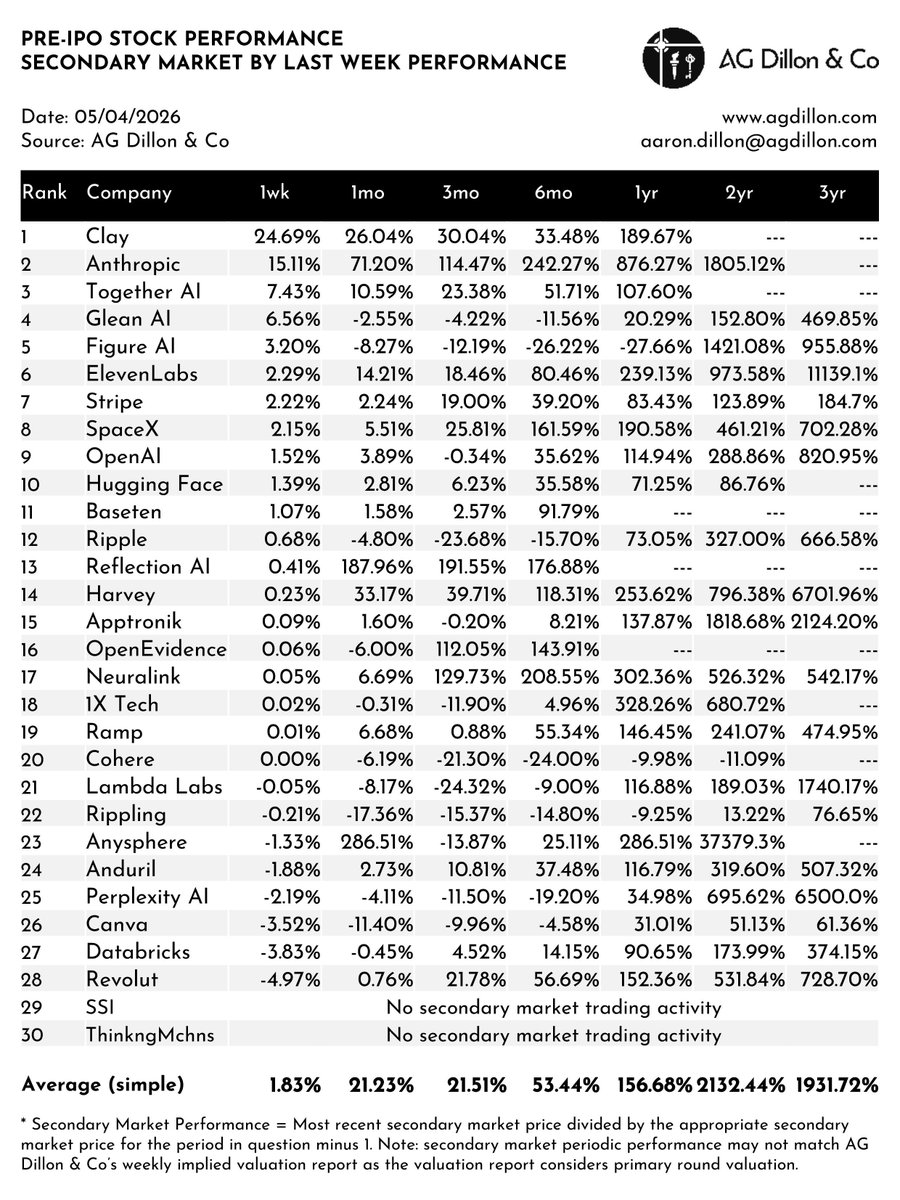

Pre-IPO Stock Secondary Market Performance | as of May 4, 2026 | Download full report = agdillon.com/reports

210

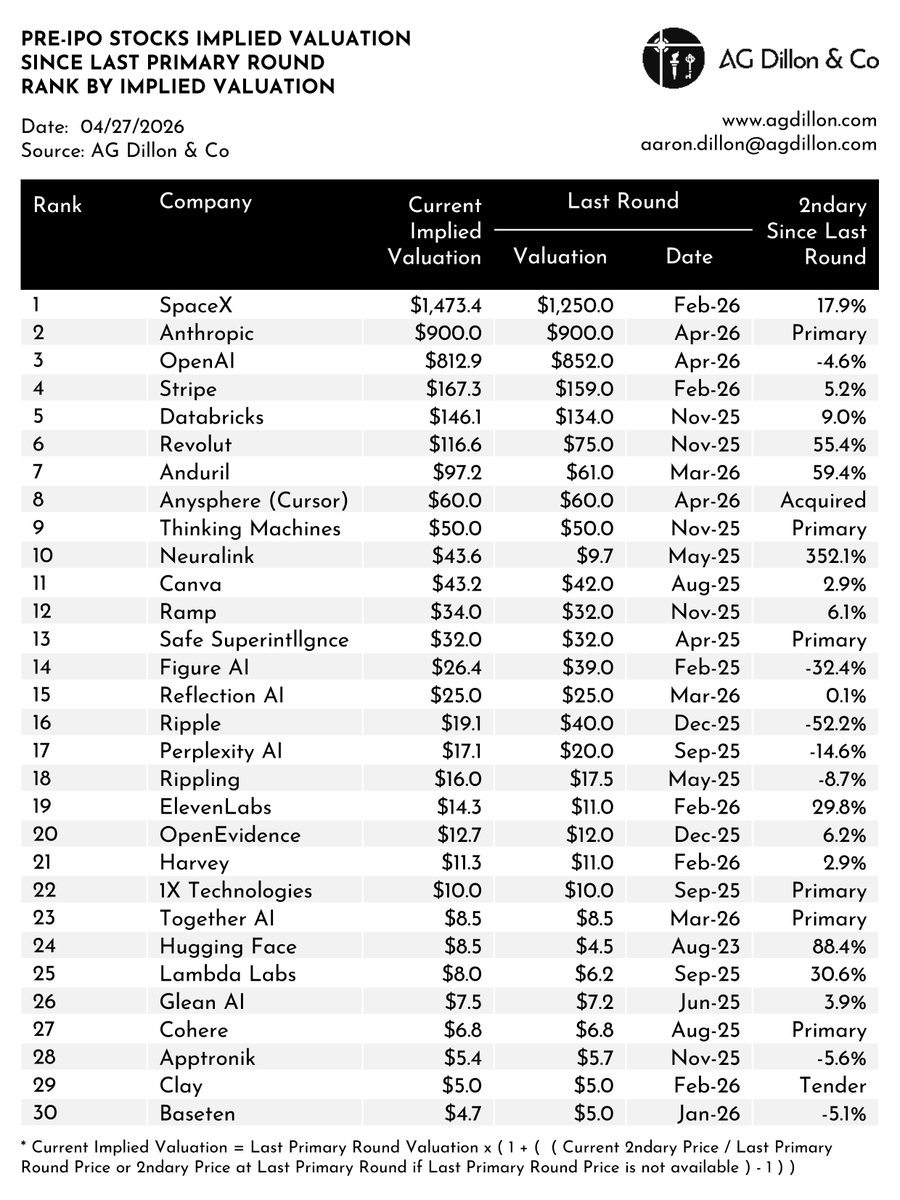

Pre-IPO Stock Secondary Market Valuations | as of Apr 27, 2026 | Download full report = agdillon.com/reports

1

1

249

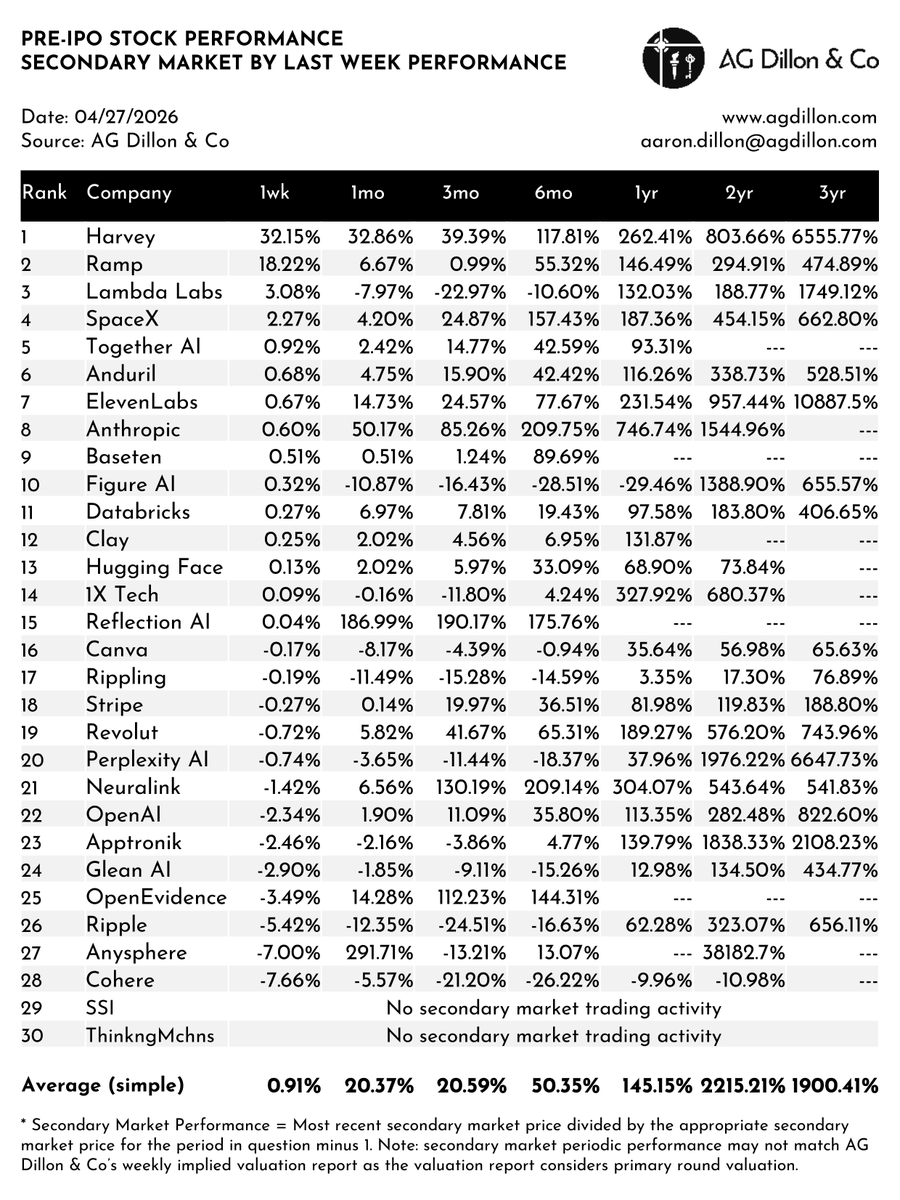

Pre-IPO Stock Secondary Market Performance | as of Apr 27, 2026 | Download full report = agdillon.com/reports

273

Apr 25

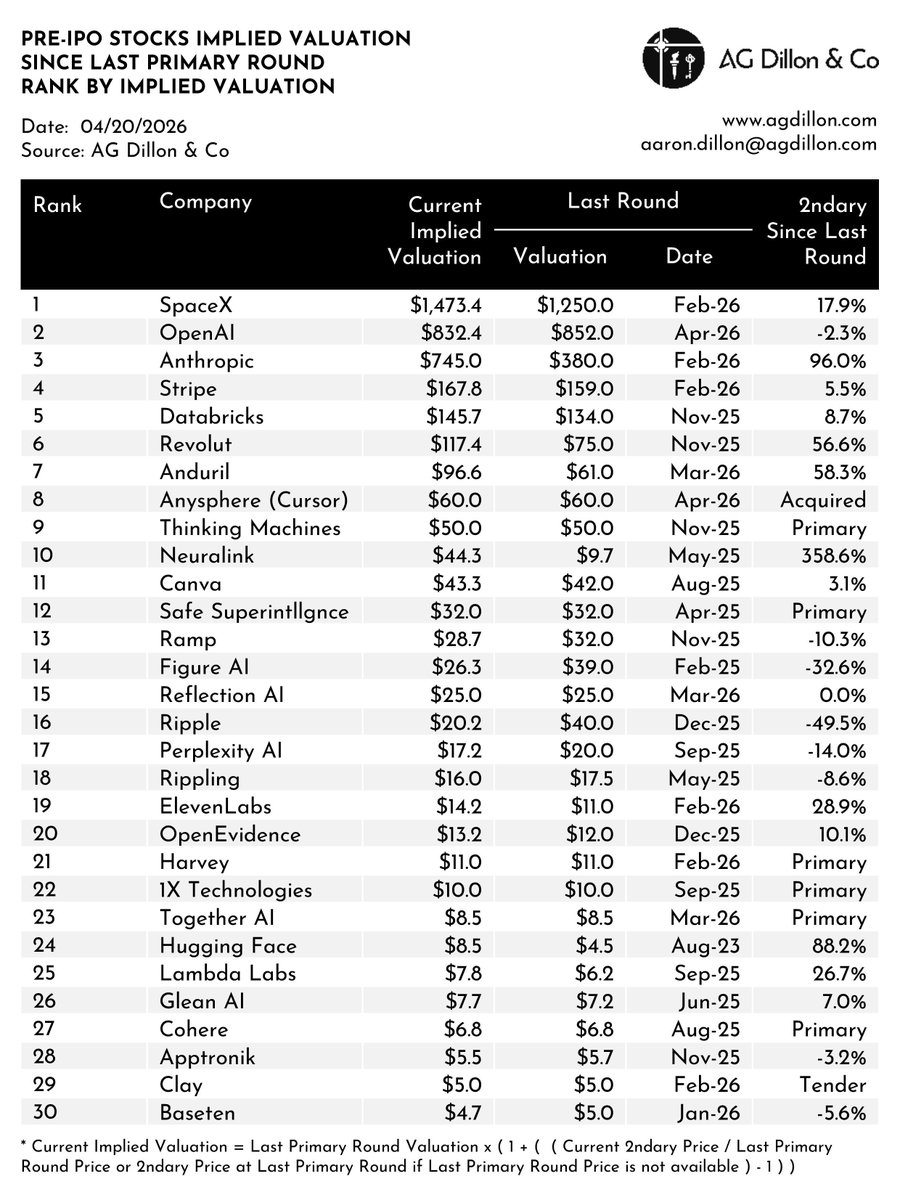

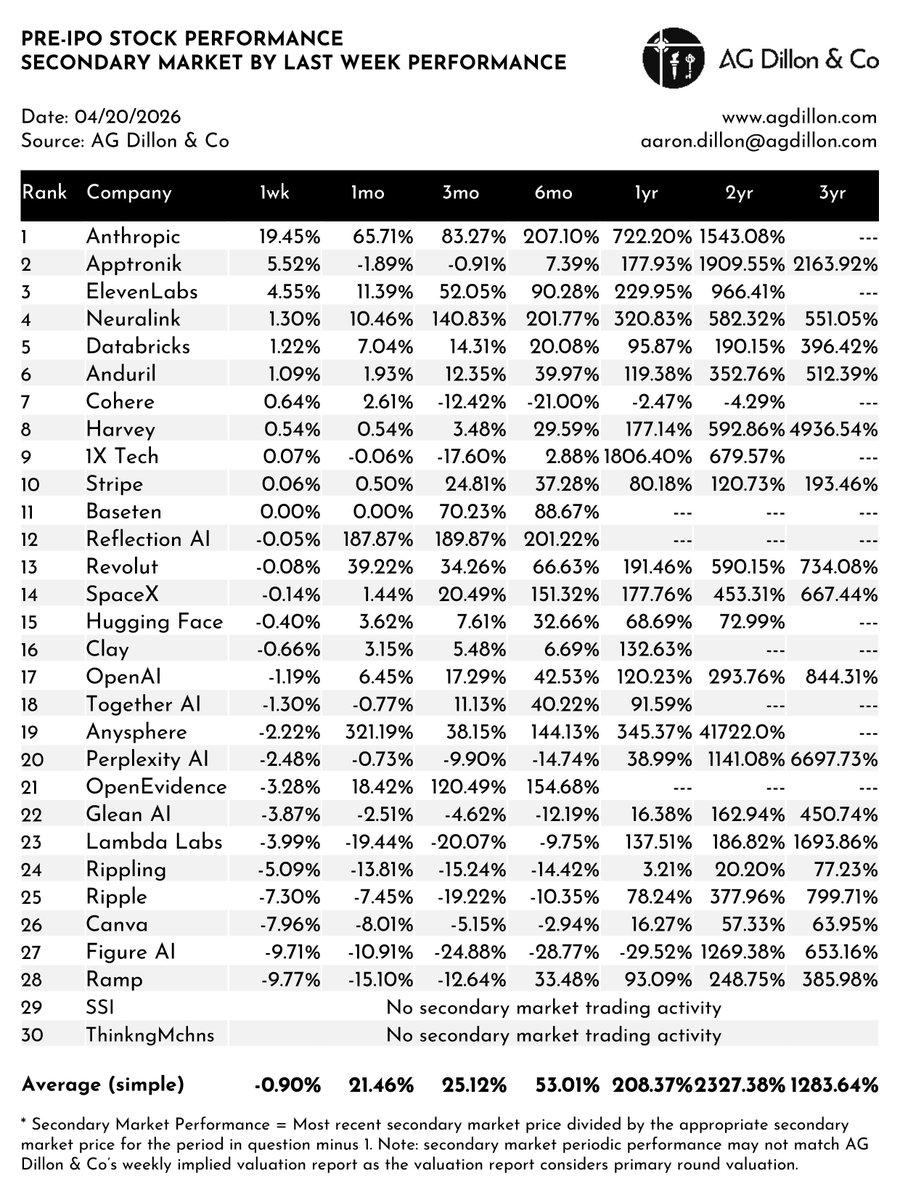

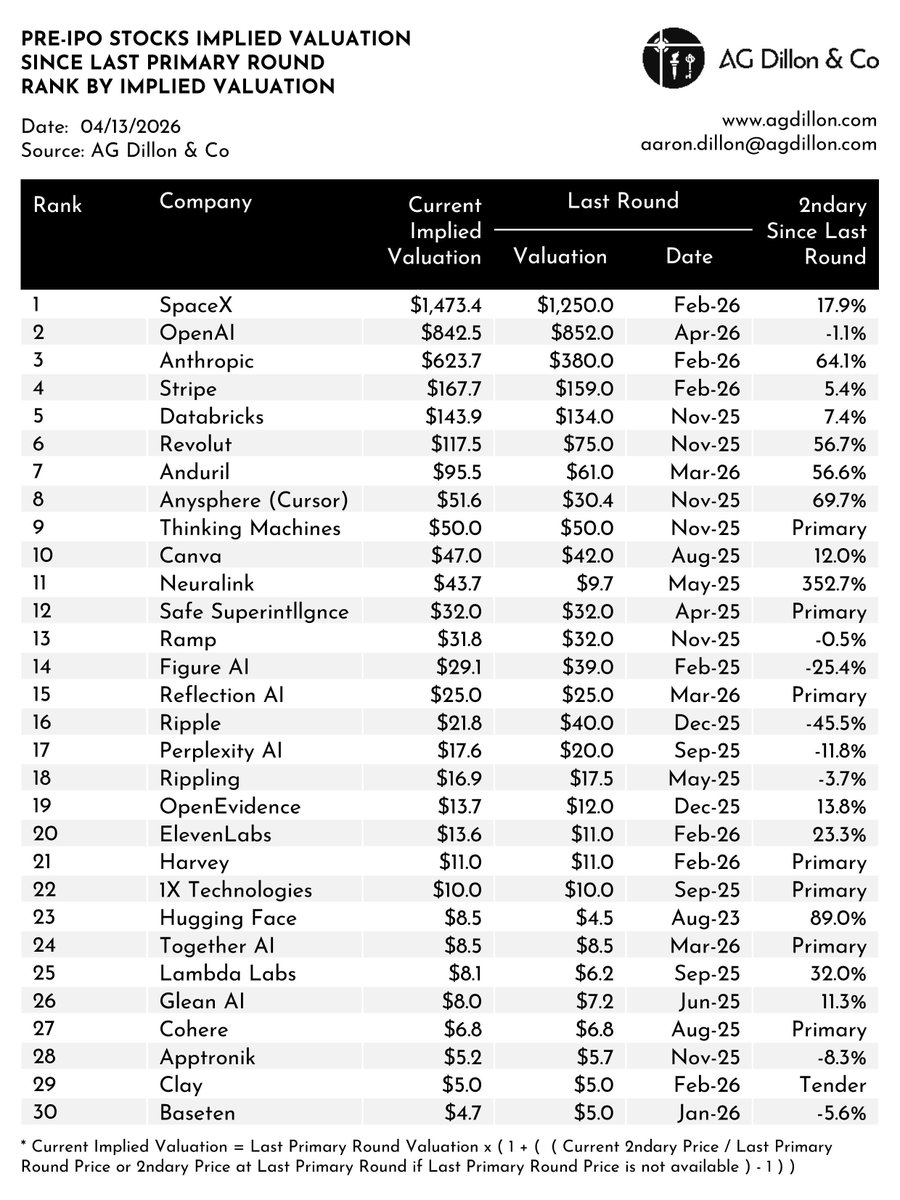

Pre-IPO Stock Secondary Market Valuations | as of Apr 20, 2026 | Download full report = agdillon.com/reports

1

1

2

375

Apr 25

Pre-IPO Stock Secondary Market Performance | as of Apr 20, 2026 | Download full report = agdillon.com/reports

2

260

Apr 17

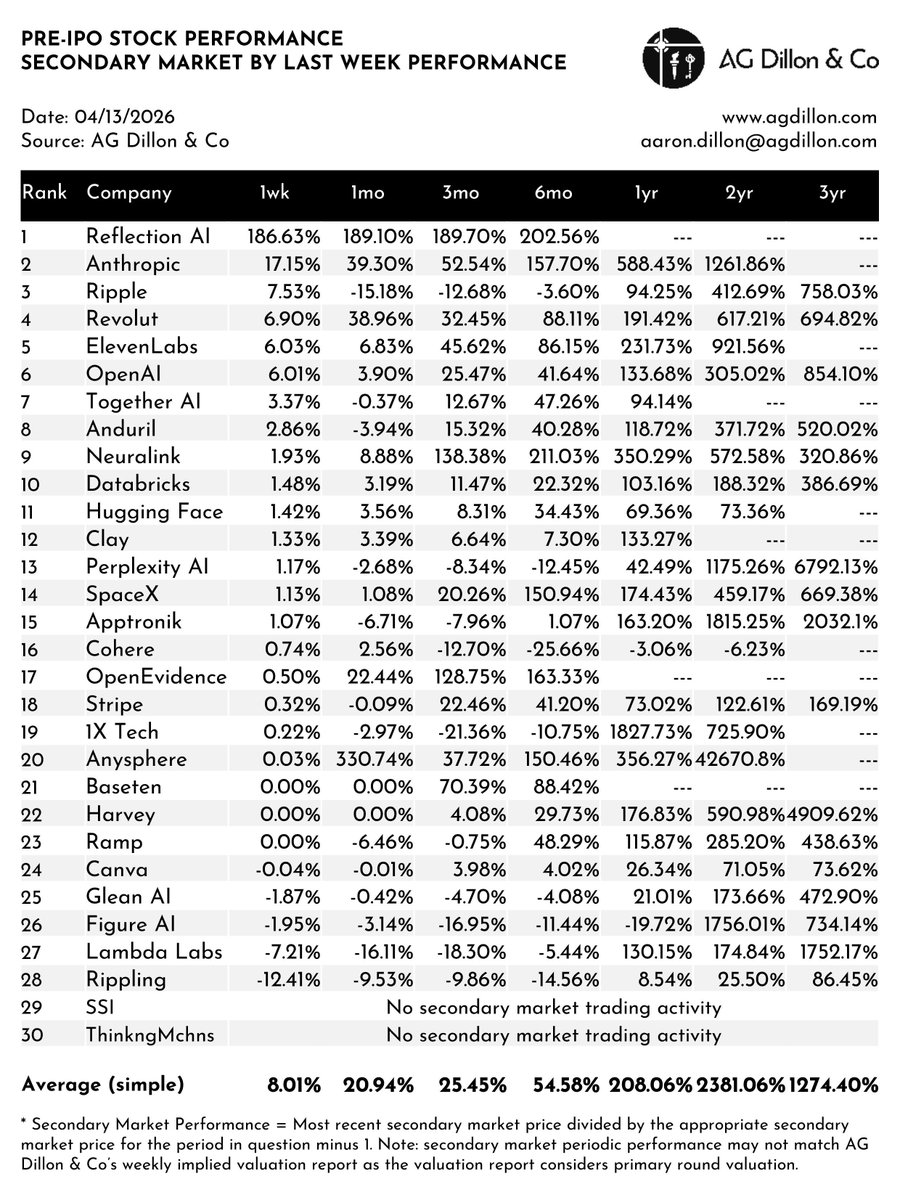

Pre-IPO Stock Secondary Market Valuations | as of Apr 13, 2026 | Download full report = agdillon.com/reports

3

455

Apr 17

Pre-IPO Stock Secondary Market Performance | as of Apr 13, 2026 | Download full report = agdillon.com/reports

1

2,776

Apr 16

Revolut in Talks to Acquire Turkish Neobank FUPS | Download full report = agdillon.com/insights

• In discussions to acquire FUPS, a Turkish neobank founded in 2018 offering money transfers, bill payments, ATM withdrawals, and card services; deal requires BDDK regulatory approval

• Revolut has been building Turkish infrastructure since 2024, appointing a country director and head of strategy and operations

• Turkey flagged internally as a high-priority market due to its young, tech-forward population

• A completed deal would mark a significant milestone in Revolut's global expansion across multiple regulated continents

363

Apr 16

Harvey Study Exposes "Mobile AI Gap" as Legal Professionals Preview Mobile App | Download full report = agdillon.com/insights

• Survey of 200 legal professionals globally: 90% use smartphones for work and 86% rely on mobile as their primary away-from-desk tool - but only 20% use AI on a smartphone and 5% on a tablet

• 80% use AI at least weekly, yet three-quarters still access it primarily on a laptop or desktop

• Harvey coined the disconnect the "mobile AI gap" and released the study alongside a preview of its own mobile app to close that gap

• Primary valuation: $11.0B (Feb/Mar 2026 primary round)

1

239

Apr 16

OpenEvidence Embeds AI Directly into Epic EHR at Mount Sinai's 48,000-Person System | Download full report = agdillon.com/insights

• Launched Dotflows, a reusable natural language prompt system letting clinicians trigger structured workflows (e.g., .discharge, .prior_auth) and share them via a community library

• Mount Sinai Health System (7 hospitals, 48,000 employees) will embed OpenEvidence directly into Epic EHR - the first enterprise-scale deployment extending access to physicians, nurses, and pharmacists

• Platform is trusted by hundreds of thousands of verified clinicians across the US

• Secondary market valuation: $13.6B ( 13.2% vs. Dec 2025 round)

240