"Kingdom of daylight’s dauphin, dapple-dawn-drawn Falcon, in his riding” Crypto

Joined November 2024

- Tweets 380

- Following 605

- Followers 85

- Likes 1,047

109 Photos and videos

Pinned Tweet

19 Jan 2025

With $Trump sucking liquidity from the markets, Pendle is undervalued and has an attractive price currently. With an appetite for DeFAI and #RWA – Pendle’s yield opportunities will whet the appetite of AI Agents and Boros is going to be the catalyst that changes the direction of $Pendle forever. #Pendle

11 Jan 2025

5

2

21

3,696

uni v4 hook tokens on eth and base is something to watch 👀

10

wait until the 5th series of the tv show Industry, trading perp equities on Hyperliquid on a Sunday eve front-running the Monday market open from Harper's hotel room HF and trading on-chain options to hedge her long vol vehicles hyperliquidd

1

26

Jun 12

genuinely scandalous how many Irish bais are flogging trading courses on tiktok. €250/month sub. only income they're making is from people signing up lmao. moonlighting in contemporary digital ireland is very much alive, gotta love the be your own boss babe narrative

34

Jun 12

I wish you could short hardware wallets. Ledger Nano X battery, max leverage. what a piece of shit

1

1

120

Jun 12

bull run starts when Bitboy Ben makes a come back and shills the shit out of hyperliquid:native

46

Jun 12

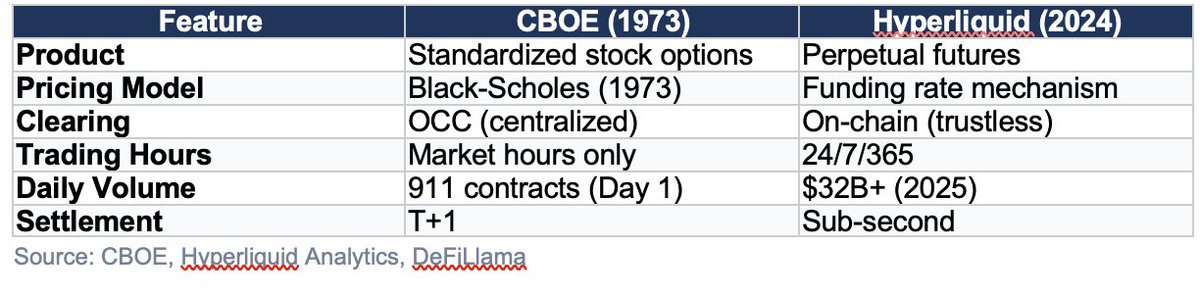

Bet on Protocols Integrating Perps, Equities and Stablecoins.

TL;DR: The winning protocol is the one that gives institutions a full derivatives desk on chain. Perps to take directional and basis risk. Options to express and sell vol. Funding rate markets to hedge the carry. Stablecoins as the unified collateral. Whoever stitches these into one composable stack captures the flow.

1/

Everyone is watching token prices. The real story is structural. Over the past two months three stress events taught me the same lesson: the protocols worth betting on are the ones stitching perps, equities and stablecoins into a single yield layer.

2/

Start with the map. Pendle sits in the middle of DeFi. It does not originate yield. It aggregates yield from other sources and splits it into fixed (Principal Tokens) and floating (Yield Tokens). Think of it as the venue where every kind of yield gets packaged and traded.

3/

What kinds of yield? Three are converging right now, and that convergence is the whole bet.

Perp funding rates.

Equity dividends.

Stablecoin and RWA cashflows.

All three are landing on the same middle layer.

4/

Perps stablecoins first. Ethena's sUSDe is a stablecoin whose yield is the funding rate from perpetual futures. It became the single largest category on Pendle, over 54% of TVL at peak. A stablecoin powered entirely by perp market structure.

5/

Equities stablecoins next. The newer category is Strategy backed. apxUSD, apyUSD, USDat, sUSDat. These are stablecoins whose yield comes from Strategy's preferred equity dividends (STRC, around 11 per cent annualised). TradFi equity cashflow, routed on chain, wrapped as a stable.

6/

This is the part people underrate. STRC dividends are structurally independent of crypto. No funding rate exposure. No restaking mechanics. No correlation to ETH. A genuinely orthogonal yield source sitting inside a crypto native protocol.

7/

Then perps plus equities. Oil perps on Hyperliquid and trade.xyz (HIP-3 markets) let you trade WTI and Brent on chain. The oracle tracks front month CME futures. When the contract rolls, the price drops by the full calendar spread. A predictable, structural repricing.

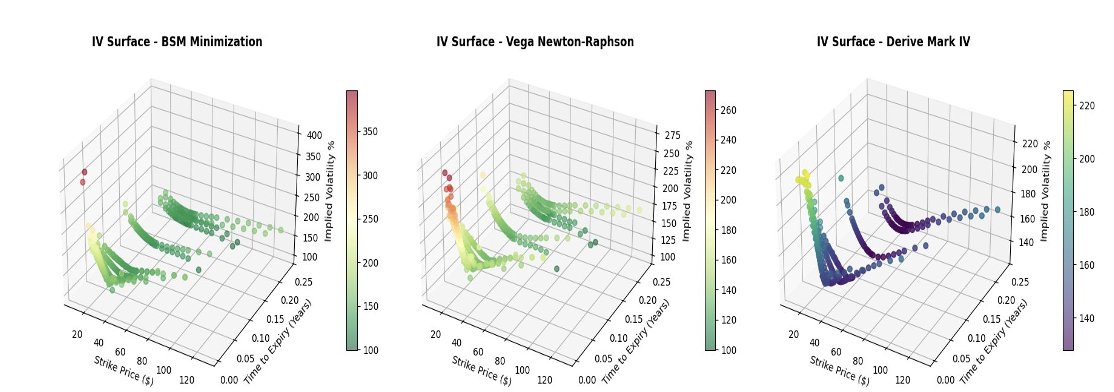

And the options leg is maturing too. Derive runs options, perps and structured products on its own chain. Early 2026 saw a real surge, options crossing 1 billion in open interest and overtaking perps.

The HYPE maturities on Boros line up with the HYPE options maturities on Derive. When a funding rate market and an options market start sharing an expiry calendar, you are watching a single derivatives stack form across protocols.

8/

In late March and early April oil went into extreme backwardation. Front month around 115, next month around 100. A 15 dollar spread that the perp oracle would mechanically give up at the roll. Traders front ran it by shorting, and funding went deeply negative, down toward minus 300 to minus 400 per cent.

9/

Negative funding means shorts pay longs. So the trade was elegant. Long the oil perp to collect the funding. Hedge the price with CME futures. You get paid to hold a delta neutral position. Perps had become an institutional basis trade venue.

10/

But floating funding is volatile and can flip against you. Enter Boros, Pendle's funding rate market. You buy a Yield Unit, pay a fixed implied rate locked at entry, and receive the floating funding. It turns an uncertain funding stream into a fixed locked in carry.

11/

So look at what just happened. Boros is the hedging layer for the perp funding that backs the biggest stablecoin category on Pendle (Ethena). And the same tool lets oil desks lock in carry on equity linked commodity perps. Perps, equities and stablecoins, one stack.

12/

This is the bet. Not on any single asset. On the protocols that aggregate the convergence. Pendle tokenises the yield from all three. Boros hedges the perp leg. STRC drags equity cashflow on chain. Whoever owns the middle captures the fees.

13/

The data backs the rotation. STRC backed assets went from 8.8 per cent of Pendle TVL in mid April to 22.9 per cent by 8 May to 39.9 per cent by 30 May. In six weeks it went from a sliver to the single largest category, overtaking Ethena which fell from 54.5 to 25 per cent.

14/

That rotation held through real stress. The Kelp rsETH exploit drained 292 million in April. The 7 May sUSDe rollover failed, with around 83 per cent of a 381 million position exiting. Through both, Strategy backed assets kept taking inflows. Orthogonal yield did its job.

15/

Now the honest risk, because integration cuts both ways. Stitching perps, equities and stablecoins into one protocol means one protocol now carries cross domain risk. An equity dividend cycle, a perp funding squeeze and a lending market shock can all hit through different doors.

16/

We saw exactly that. The largest single Pendle outflow during the rsETH stress was apyUSD, an equity backed stable with zero rsETH exposure. The shock travelled through shared Aave lending rails, not direct exposure. Integration concentrates contagion as much as it concentrates yield.

17/

There is also a recurring trap in this whole stack. Reported numbers lie. Gated APY readings showing zero. Implied funding diverging from realized. The edge, and the danger, lives in the gap between the printed number and on chain truth.

18/

So the thesis in one line. The next phase of DeFi is not a new asset. It is the convergence of perps, equities and stablecoins onto a single tokenised yield layer, and the protocols that aggregate and hedge that convergence are the ones to watch.

19/

Pendle is the aggregator. Boros is the hedge. STRC is the bridge to equities. Ethena is the bridge to perps. The bet is that this middle layer keeps eating, and that funding rate is the new variable that decides who wins.

3

179

Jun 8

Bull Posting $Pendle

1. Stress is a fee event. Every unwind and forced rollover routes through Pendle's AMM and pays fees. It printed its highest-revenue epoch of the year into the rsETH panic. It does not need a calm market to earn.

2. No longer a single-yield bet. Ethena fell 54.5% to ~25% of TVL and Pendle absorbed an 83% exit of a $381M position without a fee-base collapse. It can lose its biggest category and keep working.

3. Yield from outside crypto. The Strategy complex grew 8.8% to ~40% of TVL in six weeks. Now down ~28% in 11 days under STRC stress, so I am watching closely. But the structural point holds: Pendle can rotate its yield base.

4. Buybacks, not a floor. Revenue funds biweekly open-market PENDLE buybacks, confirmed on chain.

5. The winners tap markets outside crypto. HYPE worked because it brought TradFi equity perps on chain. Pendle is doing the same across products: STRC (TradFi preferred equity), USDai (GPU-collateral backed), and Boros, which opens up funding rate trading on TradFi names like NVDA and Brent. The structural bet is simple: products bridging real-world markets into DeFi are the ones that win, and Pendle is positioned across them.

My filter for winners: 1) real revenue 2) token buyback 3) RWA access 4) stablecoin access 5) TradFi equity access. Pendle is one of the few that ticks every box.

If you believe perps become the pivotal derivative and TradFi equity & stablecoins keep getting adopted, the trade is HYPE and PENDLE. HYPE for the perp rails, PENDLE for the yield and equity layer.

Wait until PTs show up on neobanks like Revolut under bonds. Fixed on-chain yield next to traditional bonds in a retail app.

5

405

Jun 8

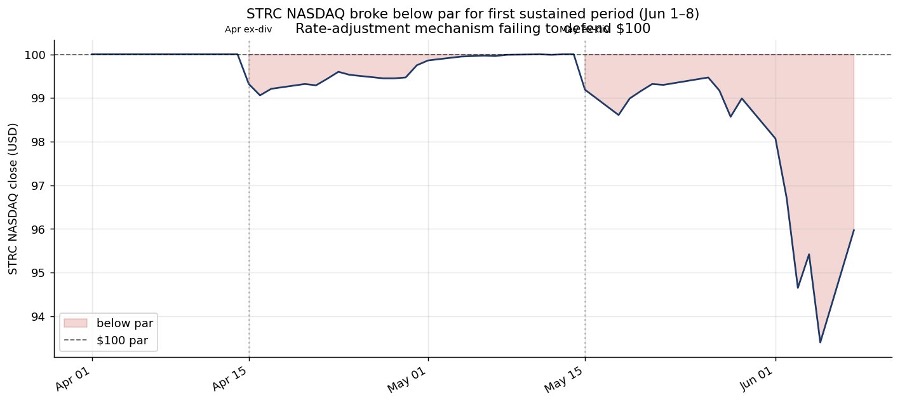

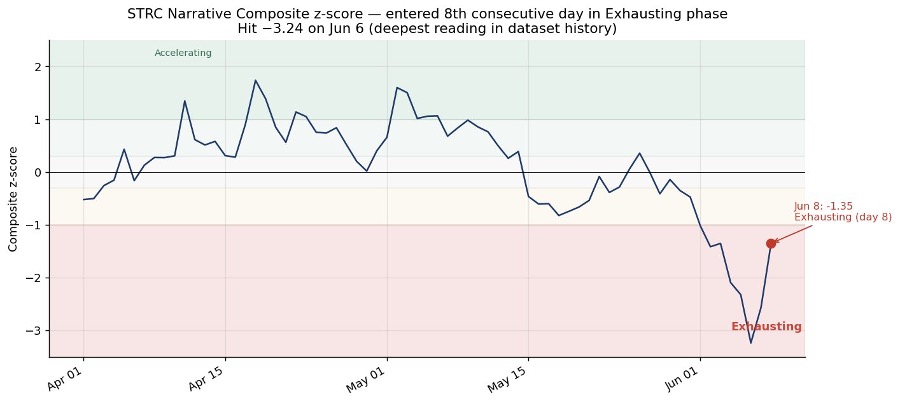

STRC just broke par for the first time in my dataset, and Pendle is where it's showing up

The prevailing read on STRC right now is that this is a stress test, not a collapse. I run a model on the STRC complex, and here is why I think some of those readings are wrong. The mechanism that makes “stress test, not collapse” true has just broken.

1

64

Jun 8

STRC has held below par for a full week, $94–96, with a $93.40 low on Jun 5. First sustained break of $10. The auto-adjusting dividend reset is supposed to defend par. This week it didn’t. Either MSTR can’t raise the rate fast enough or the market doesn’t believe it can pay one. That’s the load-bearing assumption under the whole stack.

2

60

Jun 8

And capital isn’t waiting around. STRC category TVL on Pendle went $528M to $381M in 11 days (−28%), rotating back into less narrative-dependent RWASo the right question isn’t only whether Strategy can keep raising capital over the next 6–12 months. That’s the long-runquestion. The near-term test is dated and 10 days out: ~$413M of STRC TVL matures Jun 18. A clean roll = the rotation holds. A mass exit below 25% share = the narrative is structurally over. That’s where this gets decided.

76

Jun 8

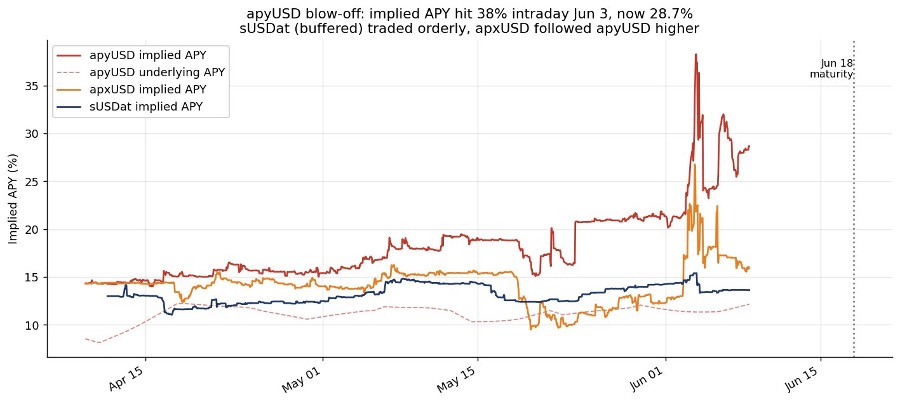

sUSDat implied APY (navy) barely moved, up ~120bp from its peak, orderly. apyUSD (red) blew off to ~29%, with a 38.3% intraday spike on Jun 3, around 1,650bp over its ~12% underlying.

The reason is mechanical: sUSDat carries a dividend-receivable buffer that absorbs STRC mark-to-market. apyUSD has no buffer, so it’s direct exposure to the synthetic-dollar price. So the complex isn’t uniformly stressed; it’s the non-buffered legs repricing while the buffered ones stay calm. Saturn’s structure is doing exactly what it was built to do.

1

49