Joined January 2026

- Tweets 268

- Following 50

- Followers 64

- Likes 30

10 Photos and videos

Pinned Tweet

May 29

What you will find in the Adverse Model is a rigorous mathematical approach and full transparency on winners and losers, everything gets timestamped and recorded. We take pride in wins and losses.

🚩We are not going after fast money

🚩We are not going after getting famous

🚩We are expressing auditable macro positions in global asset classes for educational and risk management purposes

check us out adversegroup.com/en

1

5

726

🚨 ALERT - €/$ EUR-USD

SHORT confirmed by the Adverse model

📍 Trigger: 1.1648

📊 Adverse Interval: 1.1569–1.1650

Bearish bias confirmed by Adverse Interval analysis.

#EURUSD #Forex #AdverseSignal #Trading

#research #notfinancialadvice

14

Jun 11

$UNH is a very good pick IMO, especially in a market that chops.

I am using it to stabilize my growth portfolio. It still has significant upside but it's behaving like a safe haven on down days.

I am looking for opportunities to increase my stake in it

83

Jun 11

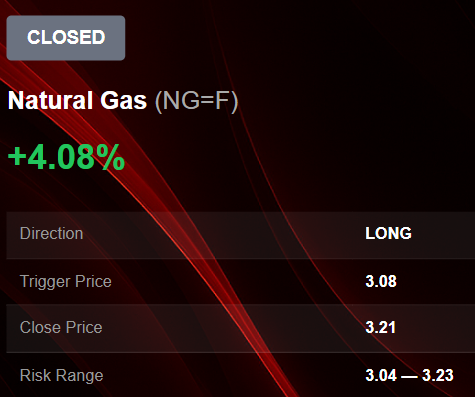

Long #NGAS at 3.08 Model driven with stop loss at 2.96.

The Model doesn't know what to buy today

54

Jun 11

Rationalizing on $PCT after yesterday bloodbath:

1) The timing of the filing was a disaster. It literally couldn't have been worse. They announced it during a week of full-blown market panic, with a massive OpEx expiration on Friday.

2) They may be brilliant plastic nerds, but for the love of God, their communication around corporate finance actions has been amateurish, to put it mildly, every single time. They seem to completely ignore market dynamics, and that's simply not going to work. Trillion-dollar companies pay close attention to the timing of offerings and capital raises, while PCT appears to think it can just wing it. This is something that will need to be addressed sooner rather than later with the right hire.

3) On the positive side, we all knew they only had roughly 3–4 quarters of cash runway left. The new capital raise gives them the flexibility to continue investing in ongoing projects without risking a liquidity crunch.

4) The 215M 2030 notes represented a significant overhang, and they managed to eliminate that burden on reasonably fair terms.

5) This deal puts enormous pressure on 2Q results. I expect the stock to remain pinned in the $8–9 range for a while, but if we don't see a meaningful revenue acceleration soon, it could drop to $5 in the blink of an eye.

@Mike_Taylor1972 @PureCycleTech

4

1

49

6,364

Jun 10

It is the worst possible timing for this mixed shelf from $PCT... it is a big middle finger to existing shareholders after a 30% drop in 7 days

8

1

12

2,835

Jun 10

🏁 CLOSE - 🇺🇸 Russell 2000

Long position closed by the Adverse model

📍 Exit: 2899

📊 Adverse Interval: 2800–2944

🟢 P&L: 0.46%

Take Profit · Risk Management

Profit taken for risk management purposes.

📈 Track record: adversegroup.com/track-recor…

#Russell2000 #SmallCap #AdverseSignal #Trading

#research #notfinancialadvice

1

1

230

Jun 10

This is why it is important to risk manage positions, especially those with an ugly start such as the one above

49

Jun 9

The main thing I see is a big fat rotation taking place with Real Estate, Healthcare and Staples beeing the main beneficiaries.

That kind of action surely doesn't look like rate hike expectations are popping off.

I suspect somebody knows something and CPI will be cooler than expected or at least that's what those sector rotations are hinting at.

Hopefully my bonds come back from the dead then.

76

Jun 9

Our Intervals are amazing and it's a shame that there isn't more people using them.

Nailed the bottom for the bounce today as well and made a very profitable scalp on sp500.

59

Jun 9

🏁 CLOSE - ₿ Bitcoin

Short position closed by the Adverse model

📍 Exit: 61170

📊 Adverse Interval: 61853–65755

🟢 P&L: 3.81%

Take Profit · Risk Management

Profit taken for risk management purposes.

📈 Track record: adversegroup.com/track-recor…

#Bitcoin #BTC #Crypto #AdverseSignal #Trading

#research #notfinancialadvice

1

2

92

Jun 8

🚨 ALERT - ₿ Bitcoin

SHORT confirmed by the Adverse model

📍 Trigger: 63500

📊 Adverse Interval: 59878–63622

Bearish bias confirmed by Adverse Interval analysis.

#Bitcoin #BTC #Crypto #AdverseSignal #Trading

#research #notfinancialadvice

50

Jun 6

I increased my position in $PCT yesterday at 12.50

This stock is the only "disproportionate" bet I have.

Around 15% of my total net worth is in this thing after the last run it had with a DCA of 7.5.

The thesis is simple, they are the only player in the world with and FDA approval for polypropylene recycling. Meanwhile they are in the early stages of investing in Europe and Thailand.

Their technology could become compelling to reduce plastic waste globally, but it is important to state clearly that it won't happen overnight.

It will take years for them to build production lines around the world, find customers, scale up fast enough.

They will also face serious cash flow issues if they don't start selling significant amounts from Ironton in the next 6-9 months, but the tech and the business plan is rock solid. I will gladly take a 0 if the plan fails.

Everything that matters now is execution, good luck to the management team.

3

12

1,013

Jun 7

I am not sure I understand the reasoning there sorry man, I will gladly deep dive with you if you pull up the numbers behind that assumption

1

63