Specialized Recruiting for Financial Planners & Advisors. RIAs | Broker/Dealers | Wirehouses | Family Offices

Joined November 2025

- Tweets 927

- Following 126

- Followers 1,713

- Likes 1,881

47 Photos and videos

Pinned Tweet

Pinned for anyone new here:

We’re a recruiting firm focused exclusively on financial planners and financial advisors.

We help:

- advisors explore new opportunities confidentially

- firms hire some of the best talent in the industry

If you’d like to join our talent network or discuss hiring needs, you can find everything here:

linktr.ee/FinancialAdvisorRe…

1

2

10

7,604

If I were a younger supporting advisor or financial planner trying to make the jump to the lead advisor role, this is exactly how I’d do it.

Develop the system. The system is your leverage that unlocks opportunities nobody else in your same spot will get.

You could get there by the end of the year if you start now

Most firms would love to recruit a wealth advisor with a large book of business.

That isn't exactly breaking news.

But here's what many younger advisors don't realize:

You don't need a massive book to create opportunities for yourself.

You need a repeatable process for bringing in quality clients.

The industry places a huge premium on advisors who know how to grow.

Not just advisors who already have.

I've seen financial planners and associate advisors create tremendous career opportunities for themselves simply because they demonstrated an ability to consistently bring in new relationships.

Even if the book is still relatively small.

Why?

Because firms know assets can be accumulated over time.

The harder skill to find is someone who can go out and earn a client's trust.

There are a lot of firms out there looking for people who know how to fish.

Not just people who already have the fish.

18

5,116

Most firms would love to recruit a wealth advisor with a large book of business.

That isn't exactly breaking news.

But here's what many younger advisors don't realize:

You don't need a massive book to create opportunities for yourself.

You need a repeatable process for bringing in quality clients.

The industry places a huge premium on advisors who know how to grow.

Not just advisors who already have.

I've seen financial planners and associate advisors create tremendous career opportunities for themselves simply because they demonstrated an ability to consistently bring in new relationships.

Even if the book is still relatively small.

Why?

Because firms know assets can be accumulated over time.

The harder skill to find is someone who can go out and earn a client's trust.

There are a lot of firms out there looking for people who know how to fish.

Not just people who already have the fish.

1

17

6,441

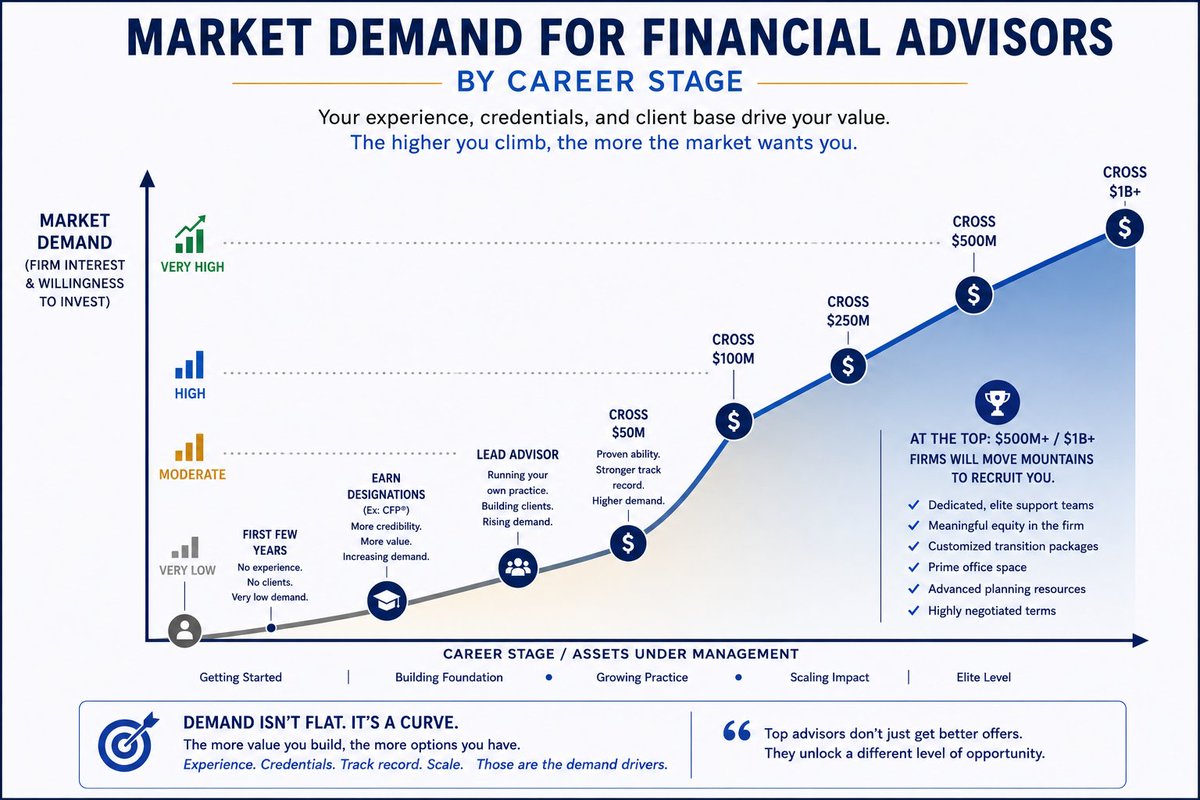

There are a handful of milestones that completely change the trajectory of a financial advisor's career.

One of the biggest is crossing $1M in annual revenue.

Not because it's a nice round number.

Because it unlocks opportunities that simply aren't available to most advisors below that level.

This is where the headline recruiting deals start showing up.

This is where meaningful equity conversations become possible.

On the RIA side of the industry, a $1M advisor often has enough scale that their book can be used as part of an equity negotiation.

An advisor operating independently may eventually sell their practice for a 6x-8x EBITDA multiple.

But when that same book is contributed into a larger enterprise, the economics can look very different.

10x, 12x, or even higher multiples aren't uncommon for larger firms.

The broker-dealer side presents a different, but equally interesting, opportunity.

At this level of production, firms may be willing to offer transition packages worth 3x, 4x, or more of trailing 12-month revenue.

The point isn't that every advisor should make a move once they hit $1M.

It's that the menu of options changes.

More ownership opportunities.

More recruiting interest.

More leverage.

More ways to create wealth.

For many advisors, $1M in revenue isn't the finish line.

It's the point where entirely new doors start opening.

17

3,920

One of the most common questions I get from wealth advisors is:

“How big does my book need to be before firms start taking an interest in me?”

The answer varies by firm, but it’s usually lower than most advisors think.

If you have $20M in AUM, there are plenty of firms that would be interested in having a conversation.

This is one of the most unique environments I've ever seen for wealth advisors considering a move.

Not only are there more business models than ever before...

The market itself has created some interesting opportunities.

We're coming off three consecutive strong years, and many client accounts are at or near all-time highs.

That matters because advisor economics are often tied directly to the size of the book.

On the RIA side, established advisors often negotiate for equity when joining a new firm.

In many cases, the size of the advisor's book helps determine the size of their ownership stake.

Larger book.

Larger contribution.

Potentially larger equity opportunity.

The broker-dealer side presents a different, but equally interesting, opportunity.

Many firms are aggressively competing for quality advisors and are willing to offer significant transition packages to attract them.

Depending on the size of the practice, those deals can be substantial.

What's interesting is that advisors today often have multiple paths to create wealth.

Some may prioritize ownership and enterprise value.

Others may prioritize transition compensation.

Others may find a way to participate in both.

The wealth management industry has always rewarded successful advisors.

But there are moments when market conditions create opportunities that simply don't exist in other environments.

This feels like one of those moments.

1

12

7,302

The wealth management industry is in the middle of one of the largest consolidation waves it has ever seen.

But the large consolidators aren't immune from the same two challenges every wealth management firm faces:

Attracting and retaining next-generation talent.

And generating organic growth.

The roll-up strategy is relatively straightforward.

Acquire firms from advisors nearing retirement.

Add scale.

Create operational efficiencies.

The challenge is that many of those retiring advisors were also the primary growth engines of their firms.

They spent decades building relationships and bringing in new clients.

Now they're leaving.

At the same time, many next-generation advisors at acquired firms had little or no equity before the acquisition.

And after the acquisition, they often find themselves competing against independent firms that can offer more attractive economics.

That's a difficult balancing act.

The consolidator needs to generate a return on a business purchased at historically high multiples.

The next-generation advisor is evaluating compensation, ownership opportunities, career trajectory, and long-term upside.

Meanwhile, the firm's future growth increasingly depends on that next generation.

This is why I think the biggest challenge facing many large wealth management firms over the next decade isn't acquisitions.

It's figuring out how to retain and incentivize the people who will drive the next wave of growth.

Buying growth and creating growth are two very different skill sets.

1

2

23

4,083

This is one of the most unique environments I've ever seen for wealth advisors considering a move.

Not only are there more business models than ever before...

The market itself has created some interesting opportunities.

We're coming off three consecutive strong years, and many client accounts are at or near all-time highs.

That matters because advisor economics are often tied directly to the size of the book.

On the RIA side, established advisors often negotiate for equity when joining a new firm.

In many cases, the size of the advisor's book helps determine the size of their ownership stake.

Larger book.

Larger contribution.

Potentially larger equity opportunity.

The broker-dealer side presents a different, but equally interesting, opportunity.

Many firms are aggressively competing for quality advisors and are willing to offer significant transition packages to attract them.

Depending on the size of the practice, those deals can be substantial.

What's interesting is that advisors today often have multiple paths to create wealth.

Some may prioritize ownership and enterprise value.

Others may prioritize transition compensation.

Others may find a way to participate in both.

The wealth management industry has always rewarded successful advisors.

But there are moments when market conditions create opportunities that simply don't exist in other environments.

This feels like one of those moments.

8

8,809

“Collaborative” is a key term in the definition of financial planning. Good advisors do not start allocating clients’ money into investments the clients do not understand. They take the time to educate, explain, and make sure clients are comfortable with the strategy and risks involved.

Are there bad actors in the industry? Absolutely, especially around professional athletes. It is unfortunate. But there are also outstanding advisors who provide enormous value to their clients through guidance, planning, and long term stewardship of wealth.

Chad Ochocinco says he saved 83% of his $49,000,000 NFL salary and refuses to let financial advisors who "never made it" tell him what to do with it

"You don't know who to tell no to. You got all these investment people. You know how many horror stories there are about NFL players that invest in companies?"

"The best investment person is yourself. Do your homework. You don't need all these people because if they knew… name one investment person that's in a position that's rich"

"Don't tell me how to handle my money when you haven't made it yet, to give me an example of what I should do. We put our money in too many people's hands. You don't know what's going on"

2

13

6,715

I sincerely hope this works out for these SpaceX employees, but if I were a betting man, I’d guess that 30 or fewer will still be with the same firm by 2030.

BREAKING: More than 100 current and former SpaceX employees (worth up to $5 billion) unionized to secure low-fees wealth management services from Chicago-based RIA Choreo

1

29

8,652

I have this conversation with a lot of next-generation financial advisors.

They're trying to decide whether buying equity in their current firm makes sense.

Here's what I always tell them:

At some point, the owner is going to face a decision.

Sell internally to employees.

Or sell externally to a strategic buyer.

The economics are often very different.

A strategic buyer may pay significantly more, provide immediate liquidity, and remove much of the risk for the seller.

An internal succession often means a lower price and more uncertainty.

I'm not saying internal successions don't happen.

They do.

But they are becoming increasingly rare.

That's why the first question I'd ask isn't about valuation.

It's about intent.

What does the owner actually want?

The firms that successfully transition internally are usually led by owners who have been vocal about that plan for years.

And more importantly, their actions match their words.

Internal successions are rarely built through a single transaction when the owner is ready to retire.

They're usually built over time.

Gradually transferring ownership.

Bringing the next generation into decision-making.

And creating alignment long before an exit is on the horizon.

16

2,705

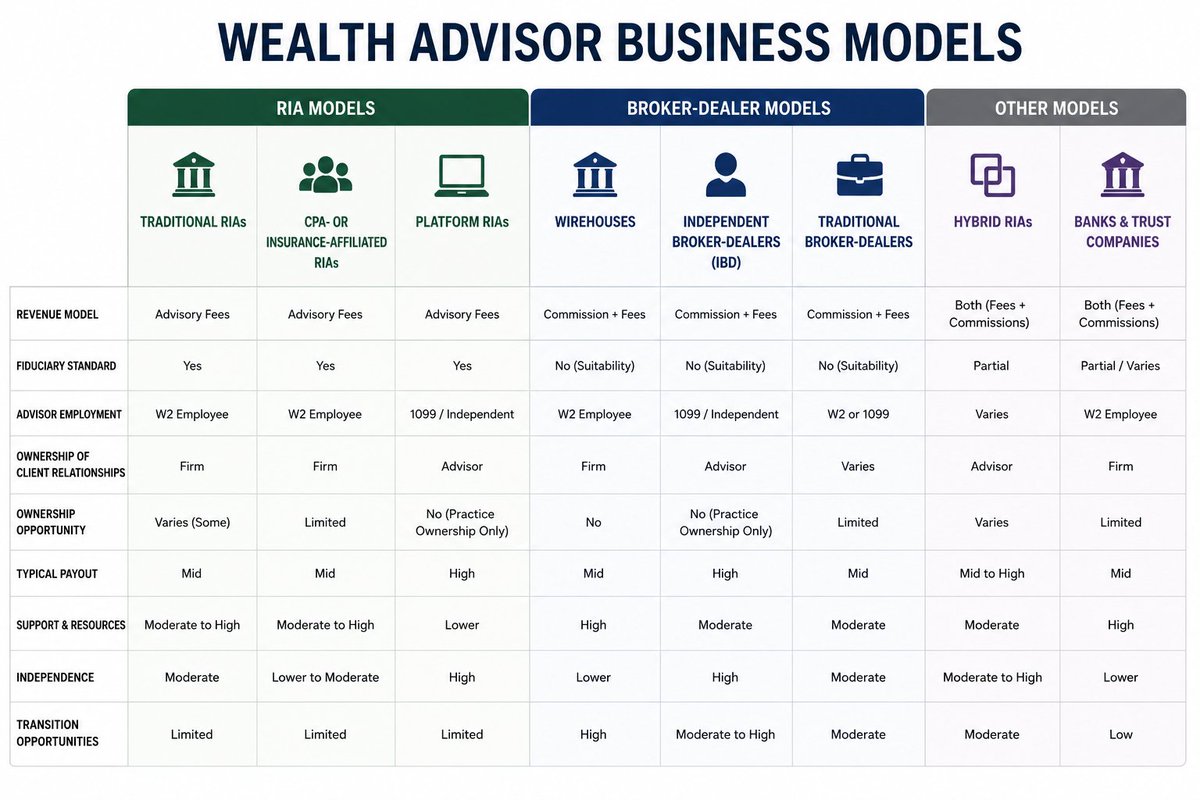

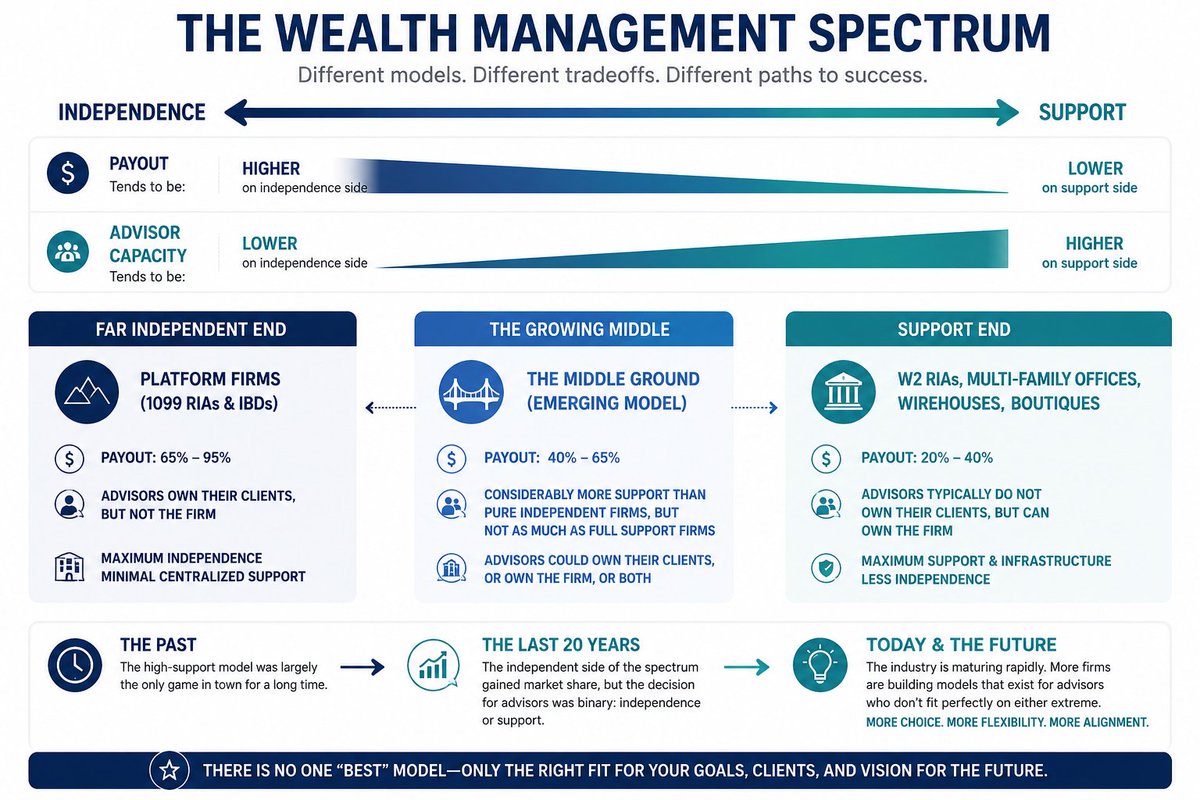

A lot of wealth advisors dream about owning their own firm one day.

What's unique about wealth management is that there are more paths to ownership than most people realize.

In many industries, your options are simple:

Start a business from scratch or remain an employee.

Wealth management is different.

There are several ways to capture many of the benefits of ownership without building everything from the ground up.

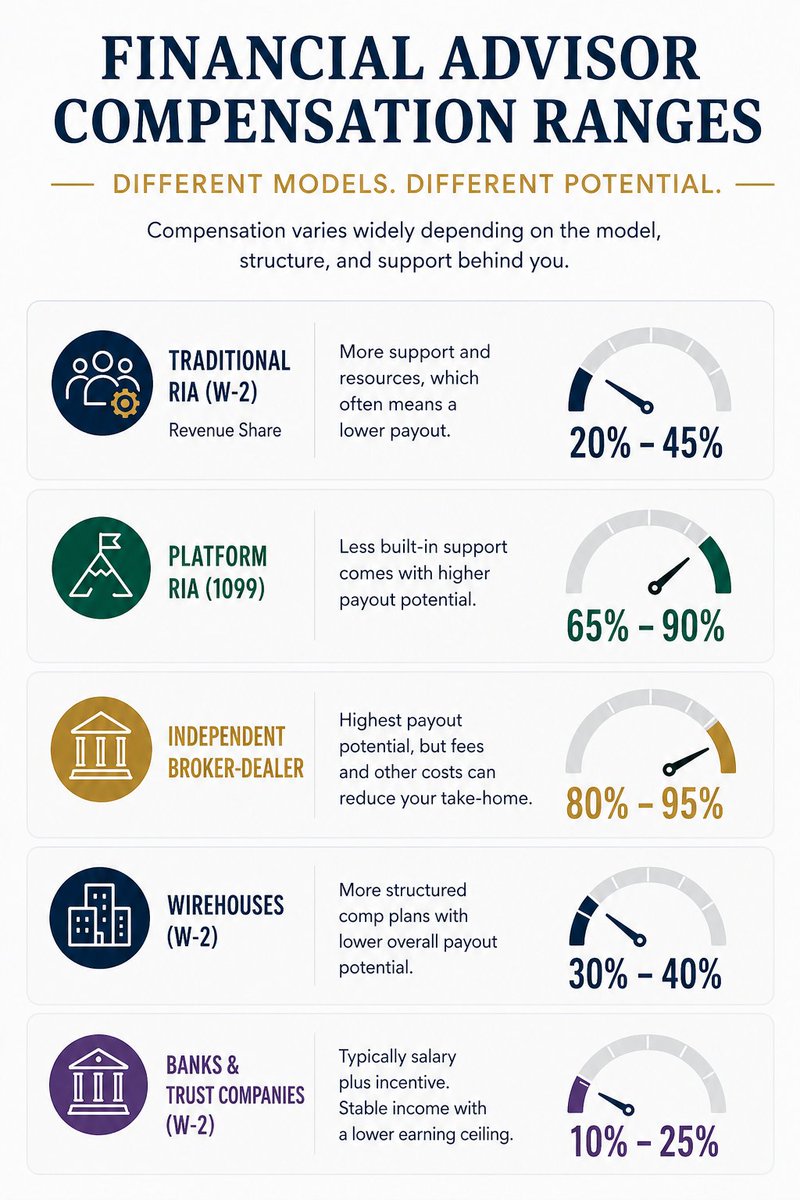

Independent broker-dealers allow advisors to own their client relationships, often operate under their own brand, and typically offer payouts in the 80%-95% range.

Platform RIAs and hybrid RIAs can provide similar benefits while often offering additional flexibility around marketing, technology, and service offerings.

There are even firms today like XPYN whose entire business is helping advisors launch and operate their own firms.

In other words, ownership isn't necessarily a binary decision anymore.

There is a spectrum.

That said, I still think there are situations where starting a firm from scratch makes complete sense.

One is when you want to build an enterprise rather than simply run a practice.

You want to hire advisors.

Develop leadership.

Build a brand.

And create something that can eventually operate beyond your own client relationships.

The other is when you serve a highly specialized clientele and need every aspect of the business designed around their needs.

Sometimes the existing platforms simply aren't built for what you're trying to create.

The good news is that advisors today have more options than ever before.

The challenge is figuring out which ownership path best aligns with what you're actually trying to build.

3

12

3,193

A career as a wealth advisor can be extremely rewarding and lucrative.

But there are certain situations that don't allow that potential to be fully realized.

The one that kills me to see the most is when an advisor spends their entire career on a fixed salary or a low payout structure (15%-25%) with no equity opportunity.

A low payout can make a lot of sense for equity partners.

The firm retains more revenue.

That capital can be used to hire staff, improve technology, make acquisitions, and expand the business.

If the advisor participates in the growth of the firm's enterprise value, there is a clear tradeoff.

But I struggle to understand why anyone would accept a fixed salary or a low payout over an entire career if there is no meaningful ownership opportunity attached to it.

The places I tend to see this most often are banks, trust companies, next-generation advisors at broker-dealer affiliated firms, and increasingly some next-generation advisors at PE-backed RIAs.

Money isn't everything.

But it is amazing how many advisors I come across who could potentially be earning 2x or 3x more, have significantly better long-term upside, and in some cases provide clients with a broader service offering.

The wealth management industry has never offered more career paths than it does today.

Which is why understanding the economics of your business model matters so much.

Over 20 or 30 years, small differences in compensation and ownership can turn into very large differences in outcomes.

2

24

4,461

This one right here

Jun 8

Picking up the phone and calling (vs texting or emailing) is the most high leverage thing a millenial or gen z can do in the business world.

11

2,555

I always chuckle when an advisor tells me they think their pay is going up because their firm is selling to a PE-backed consolidator.

“This firm has a ton of money behind it.”

True.

But that money isn’t sitting there waiting to increase advisor compensation.

It’s there to fund acquisitions.

The investment thesis is usually built on buying firms, creating scale, and expanding margins. Not handing out raises to the existing staff of acquired firms.

If anything, the pressure often runs in the opposite direction.

2

1

15

3,433

One of the toughest transition points in a financial advisor's career is moving from an associate or planner role into a lead advisor role.

Specifically:

How do you get enough clients to generate a living wage?

Historically, there was really only one path.

You left your support role, your income dropped dramatically (or disappeared altogether), and you raced to build a book before running out of time or money.

It was a leap of faith.

Today, the landscape is changing.

More firms are creating structured pathways for next-generation advisors.

Some are offering salary support or draw arrangements that gradually phase out as an advisor builds their client base and recurring revenue.

These opportunities become much more realistic once an advisor has some traction.

And increasingly, younger advisors are getting there.

Many spend years working as financial planners or associate advisors on senior advisors' books while slowly developing relationships of their own.

By the time they're ready to make a move, it's not uncommon to see them bringing $10M, $15M, or even $25M in assets under management.

That's where the market gets interesting.

The demand for advisors with clients has always been strong.

But over the last few years, the biggest increase in demand may be for younger advisors with $10M–$25M AUM.

They have enough business to prove they can grow.

But they're still early enough in their careers to build something meaningful for decades.

For firms looking toward the future, that's a very attractive combination.

5

41

6,366

We are in interesting times.

Pay raises for job changers has consistently outpaced pay raises for job stayers since 2020.

Me walking into my boss's office to ask why the new hire makes 20k more than me

1

8

3,151

A lot of wealth advisors who want to be great focus on how to differentiate themselves from their peers.

And rightfully so.

But that doesn’t mean you need to reinvent the wheel for every aspect of your business.

There are a handful of habits that nearly every top advisor I speak with has in common.

The biggest one?

They treat their practice like a business, not just a job.

Most of them have a structured planning process. At least twice a year, they step back, evaluate where the business stands today, and map out where they want it to go over the next 12 months.

A good starting point is a simple spreadsheet of your current clients:

• Length of relationship

• Assets under management

• Revenue by client

• Clients at risk

• Growth opportunities

This is an exercise I often have advisors complete when they’re considering a move to a new firm as well.

The more organized and buttoned up your business is, the better your outcomes tend to be, whether you’re looking to grow where you are today or make a transition elsewhere.

I have a simple spreadsheet template for this process that I’m happy to share.

If you’re an advisor and would like a copy, send me a DM.

3

1

24

3,093

I have several friends in different industries looking for new jobs right now.

I asked how they were conducting their search.

The answer was the same for all of them.

Job boards.

LinkedIn, Indeed, ZipRecruiter, etc.

Not one of them had considered reaching out to a recruiter who specializes in their industry.

I'm obviously biased, but it also seems like a complete no-brainer.

Job boards are saturated with applicants, and increasingly, AI is making it easier than ever to spam applications into every listing.

Meanwhile, specialized recruiters typically have direct relationships with the decision-makers at the firms in your industry.

Recruiters spend all day hearing the good, the bad, and the ugly about the firms you're looking at.

One conversation can save you from having to research dozens of companies on your own.

And they'll usually have that conversation with you for free.

Nearly every industry has specialized recruiters.

There's everything to gain and nothing to lose.

14

2,224

Every once in a while, I talk to a wealth advisor who hasn't looked at the advisor market since before 2020.

They almost all have the same reaction.

It usually involves a few expletives.

The recruitment deals are nearly double what they remember.

Firms are offering higher payouts.

There are more equity opportunities than ever before.

And there are more business models available to advisors than at any point in the industry's history.

Most advisors are so busy serving clients and growing their practice that they don't realize how much the industry has changed around them.

Then one day they take a look at the market and realize the rules of the game have changed.

Whether you have any intention of moving firms or not, it pays to understand what is happening around you.

1

11

2,687

Couldn’t agree more.

The right team will always outperform the sum of its individual parts.

That’s why investing in human capital matters so much. It’s one of the few places where 1 1 can equal 3.

In the wealth management industry, developing the skill of identifying right-fit talent is what separates a practice from a business, and a business from an enterprise.

Jun 1

The best investment a business owner can make

Hiring the right people before you feel like you are ready and can afford to

Every time I've seen a business owner do this, they scaled faster and wished they did it sooner

Every time they waited until it felt comfortable, they left money on the table and had to rush into a hire and it didn't work out

9

2,992

“Why do the largest wealth advisors move firms?”

It’s a question I get all the time.

Most people assume the answer is money.

In my experience, that’s rarely the primary reason.

More often, it’s the accumulation of small frustrations over time.

A firm limits their ability to differentiate themselves in the marketplace.

Marketing ideas get watered down by compliance.

Decision-making moves slowly.

Every new initiative requires layers of approvals and exceptions.

Processes that were manageable when the business was smaller become obstacles as the practice grows.

At some point, these advisors realize they’re spending too much time navigating internal bureaucracy and not enough time serving clients or building their business.

The tipping point usually isn’t one major event.

It’s the realization that the friction has become a meaningful drag on growth, client experience, and their ability to execute their vision.

The largest advisor transitions I’ve seen weren’t driven by a bigger check.

They were driven by a desire for greater autonomy, faster execution, and a platform that better aligns with where the business is headed.

Money matters.

But freedom to build the business the way they believe it should be built often matters more.

3

8

1,942