Joined March 2026

- Tweets 1,005

- Following 274

- Followers 646

- Likes 4,418

207 Photos and videos

Everyone’s looking at the chip layer of AI. GPUs, custom ASICs, the names everyone already knows. There’s a layer underneath all of that, and you can’t build around it no matter how good your chips are.

Every AI cluster has two physical problems that have nothing to do with compute power. Getting the GPUs connected to each other and to the rest of the data center, and getting rid of the heat they generate. Power consumption per rack keeps climbing and the heat that comes with it climbs right along with it. Neither of these is optional. You can have the fastest chip in the world and it does nothing if it can’t talk to the rest of the cluster or if it melts.

The cooling numbers are what caught my attention. The whole industry is in the middle of a shift away from traditional air cooling toward liquid cooling, where coolant runs directly to the chip instead of relying on fans pushing air across a heatsink. Adoption in new data center builds was under 5% in 2023. It’s projected to hit 35-40% by 2026. The reason is simple. Air cooling tops out around 30-50kW per rack. Blackwell class racks are pushing well past that. Once you cross that threshold, liquid cooling isn’t a premium upgrade anymore. It’s the only option that works. The data center liquid cooling market is sitting around ~$5-6B in 2026 and multiple forecasts put it at ~$27-38B by 2033, roughly 25-30% CAGR depending on the source.

On the cabling and connectivity side, this is the part that’s been building for longer and is now showing up in earnings. Copper physically cannot carry the bandwidth modern AI workloads need beyond very short distances. 400G and 800G per lane requirements mean fiber has to go everywhere, inside racks, between racks, between buildings. This is already showing up in real numbers, not projections.

And this is the number that ties it together for me. Hyperscaler capex for 2026 is sitting around $330B, and roughly 40% of that flows to physical infrastructure rather than silicon. Cooling, power, networking, real estate. That’s not a small slice. And consensus estimates for hyperscaler capex have undershot actuals for two straight years running.

Everyone’s watching the chips. The actual bottleneck is in the plumbing. Most of these names trade at a fraction of the multiples the chip names command, despite facing the same demand curve.

3

193

Jun 8

$OCC Optical Cable just reported Q2 FY2026 and the number that matters most is the one at the bottom.

Net income positive ~$1.1M. The company just turned profitable.

Revenue hit $22.2M, up 26.6% year over year. That’s not the same trajectory as Q1’s 4.4% growth. Something accelerated. The company said it plainly on the call. Enterprise, data center, and severe duty markets drove the increase. Gross margin expanded again to 34.2% from 32.7% last quarter and 29.4% a year ago. Manufacturing operating leverage is kicking in, meaning every incremental dollar of revenue is dropping more to the bottom line than before.

The data center acceleration is the part worth understanding. On the Q1 call three months ago, management said they were seeing increased quotes and orders in the data center sector particularly in January and expected it to grow through the year. Q2 just proved that out. Revenue up 26.6% with data center explicitly called out as a driver. That’s not coincidence. That’s AI infrastructure buildout pulling fiber optic cable demand with it.

Here’s the part most people miss about $OCC specifically. AI data centers aren’t just about GPUs. Every GPU cluster needs fiber optic cabling to connect servers within racks, racks within rows, rows within buildings, and buildings across campuses. The bandwidth demands at 400G and 800G per lane mean you can’t use copper beyond very short distances. You need fiber everywhere. $OCC makes exactly that, across enterprise, data center, military, industrial, and harsh environment applications.

The Lightera strategic partnership is also worth watching. Lightera took a 7.24% stake in OCC and the collaboration is designed to expand product offerings and market reach. CEO said on the Q2 call they’re confident in OCC’s ability to capitalize on momentum in the second half of the year. Stock is still small cap and thinly traded. Cash position was tight at $126K at the end of Q1. The profitability in Q2 helps but this isn’t a fortress balance sheet. Still early.

But a fiber optic cable manufacturer turning profitable for the first time in years, with data center explicitly driving the acceleration, right in the middle of the largest AI infrastructure buildout in history. That’s a setup that doesn’t come around often in a small cap.

5

1

9

1,993

Jun 8

SpaceX ( $SPCX )IPO is June 12. One week away. And right now there are six funds that already hold SpaceX pre IPO. But they’re very different trades depending on what you’re actually trying to own.

$NASA (Tema Space Innovators ETF) is the most talked about. Launched March 30, 2026, crossed $2.48B in AUM in under three months. #SpaceX exposure through an SPV at roughly 6.5% of the portfolio, implying a SpaceX market cap of $1.51 trillion. Pure-play space economy, actively managed, 42 holdings including Rocket Lab $RKLB at 10.6%, AST SpaceMobile $ASTS at 6.6%, Planet Labs $PL at 6.5%, Intuitive Machines $LUNR at 6.2%, Firefly Aerospace $FLY at 5.1%.

$XOVR (ERShares Private-Public Crossover ETF) has the highest SpaceX concentration at roughly 14.4%, implying a valuation around $1.55 trillion. VC Growth ETF, not a space ETF. SpaceX is the headline holding but the mandate covers other private and public category-defining companies.

$DXYZ (Destiny Tech100) is a closed end fund holding a concentrated portfolio of private tech companies. SpaceX is one of the top positions alongside other pre IPO names like OpenAI and Anthropic.

$RONB (Baron First Principles ETF) holds SpaceX direct shares alongside a diversified portfolio of growth companies. Less concentrated on space specifically but meaningful SpaceX exposure through actual shares rather than an SPV.

$VCX (Fundrise Innovation Fund) is a non-traded vehicle giving retail access to late stage private companies including SpaceX. Less liquid than the others.

$AGIX (KraneShares AI & Technology ETF) has smaller SpaceX exposure within an AI focused portfolio. SpaceX here is a supporting position, not the main thesis.

One thing most people are missing about all of these. When SpaceX lists on June 12 under $SPCX on Nasdaq, the lockup period kicks in for at least six months. These funds don’t immediately convert to public shares. The IPO hype is already priced into them to some degree.

SpaceX is targeting $135 per share, raising $75 billion at a $1.75 trillion valuation. Largest IPO in history. Price set June 11, first trade June 12.

For pure space economy exposure with SpaceX embedded, $NASA. For maximum SpaceX concentration, $XOVR. For pre IPO tech broadly, $DXYZ. For a diversified growth fund with direct SpaceX shares, $RONB. For AI infrastructure with SpaceX on the side, $AGIX. Same story, very different bets. Know which one you’re actually making. 😉

1

2

11

2,790

Jun 5

$ABCL CFO Andrew Booth at Jefferies yesterday calling ABCL635 a potential blockbuster drug during the NK3R Q&A. CFOs at major healthcare conferences don’t use that word by accident.

Think about the context. Veozah launched with a Black Box Warning for liver toxicity and still pulled $234M in 9 months in a market that’s still building. Bayer’s Lynkuet is projecting ~$1B in annual sales. Both are small molecules with real limitations. #ABCL635 came back from Phase 1 with zero liver toxicity across all doses from 30mg to 900mg, a half life of 24 days supporting once monthly dosing, and clean target engagement. The dosing headroom Astellas never had is sitting right there.

You don’t say blockbuster in a room full of institutional investors unless you mean it. They know what Veozah did with a Black Box Warning. They know what Lynkuet is projecting. And they’re saying ABCL635 is positioned to compete in that same $6B market with a cleaner profile and more room to push efficacy.

Goldman at 4.3M shares. Baker Bros at 10.8%. Insider purchase after the data. Stifel raised to $8. Cantor initiated Overweight. JonesResearch at $11. And now the CFO calling it a blockbuster at Jefferies. Q3 topline data is still the moment. But the people who know this drug best keep ending up at😉 x.com/blorrior/status/206259…

3

12

122

16,961

Jun 3

$MXL up 10% today and the reason is worth understanding properly.

Most people have been watching MaxLinear as an optical interconnect story. Keystone PAM4 DSP inside 400G and 800G transceivers. Rushmore targeting 1.6T. That part of the story has been playing out exactly as expected.

But today’s news is about something different. MaxLinear and Los Alamos National Laboratory just announced a collaboration on hardware accelerated OpenZFS storage for large scale HPC environments. The numbers from the joint development are pretty striking. 39x speedup for writes. 7x for reads. Against NVMe flash-based infrastructure.

Los Alamos isn’t a typical customer to validate against. This is a federally funded national security lab running nuclear weapons simulation, climate modeling, and some of the most demanding supercomputing workloads on the planet. If Panther performs at LANL scale, it performs anywhere.

The CEO said it plainly on the Q1 call. 60% of data center spend is in memory. Slow memory access quietly kills inference performance at scale. That’s the problem Panther is designed to solve, and today Los Alamos just publicly confirmed it works.

Panther revenue is expected to at least double in 2026 versus 2025. The optical interconnect story was already the first growth leg. Storage acceleration is the second one, and it just got a national security lab’s seal of approval.

Both markets are accelerating at the same time, and both are running on $MXL silicon.

May 14

$MXL keeps adding to the story.

Trinity platform just dropped today. URX850 SoC delivering carrier-grade bidirectional wireless backhaul at up to 10Gbps. What used to require multiple separate components, switching, QoS, wireless link aggregation, encryption, and timing functions, now sits on a single chip. Bharti Airtel, one of India’s largest carriers, is already on record saying they’ve been waiting for exactly this kind of integration.

The part worth understanding is that this has nothing to do with the optical interconnect story I was posting about earlier. That’s data centers. This is cell towers connecting to core networks. Two completely separate markets, both accelerating, both running on $MXL silicon.

Keystone PAM4 DSP for 400G and 800G optical transceivers in AI data centers. Rushmore targeting 1.6T. Panther going after memory latency. And now Trinity for 5G wireless backhaul at 10Gbps. The product roadmap keeps expanding into infrastructure layers that aren’t slowing down.

OEM products based on Trinity expected H1 2027. URX850 already deployed globally across major carrier networks. Available now.

This is what a picks and shovels position in multiple infrastructure cycles looks like.

🔗maxlinear.com/news/press-rel…

2

13

2,736

Jun 2

A lot has changed since this post $LWLG. And a lot hasn’t. When I wrote this in April, GlobalFoundries and Tower were the foundry story. $TSMC was not yet in the picture. One Fortune Global 500 customer was at Stage 3.

Four Fortune Global 500 companies are now at Stage 3. One became four. CEO Yves has said publicly that roughly 80% of Stage 3s eventually advance to Stage 4, which is where volume production begins. And right now, $LWLG is actively negotiating High Volume terms with at least one of those Fortune 500 customers, with H2 2027 as the production timeline target.

The foundry story also expanded. GF and Tower were already in. TSMC PDK integration is now on deck. GF, Tower, and TSMC combined represent the vast majority of global silicon photonics production capacity. Getting Perkinamine into all three means any photonics designer at any of those fabs can now design around it without switching foundries.

Cash hit $100M by May 11, up from $75.1M on March 31. That $25M increase during the quarter lines up with wafer run timing. Full silicon photonics wafer runs take 12 to 16 weeks. If runs launched in January are tracking for June delivery, the tape-out data is coming soon.

The honest risks haven’t changed either. Revenue is still essentially zero, $29,000 in Q1. The stock has pulled back significantly from the $18.71 52-week high to the $11 range, which tells you this is a highly volatile pre commercial name. Stage 3 doesn’t guarantee Stage 4. The 20% of Stage 3s that don’t advance are a real outcome to consider. And the tape-out data, when it comes, will be the next major read on whether the technology performs in real foundry conditions at the specs customers actually need.

The original thesis was exactly this. Not the headlines. Whether the tech ends up inside real systems. Four Fortune 500 customers at Stage 3, TSMC coming online, and High Volume negotiations underway is as close to that confirmation as you get before revenue shows up.

Still watching. 😉

Apr 12

I started buying $LWLG about a year ago, and it’s already up around 10x.

The risk is still there though. That hasn’t changed.

It’s still early, not proven at scale, and revenue hasn’t caught up yet.

But what has changed is the progress.

For a long time it felt like one of those “cool tech, but when does it actually happen” stories. Lately that’s starting to shift.

They’re not just talking about the tech anymore. It’s starting to show up inside real foundry flows like GlobalFoundries and Tower.

Once something gets into a PDK and shows up in tape outs, it’s a totally different ballgame. People can actually start designing around it.

On top of that, some customers are moving past early testing and getting closer to real products.

That’s what I’m really watching.

Not the headlines. Just whether this tech actually ends up inside real systems.

So what exactly is $LWLG’s technology?

Thread🧵👇

1

1

12

2,507

Jun 1

When I wrote about $OPTT in April, it was 1 buoy in the water off San Diego. One DHS contract. One proof point.

Today $OPTT announced it’s actively expanding defense engagement efforts in Europe. Let me show you what’s happened in between.

Five concurrent PowerBuoy deployments in the U.S. now. Three for DHS, one for the U.S. Navy, one for a research institution. Three WAM-Vs and a PowerBuoy operating in the UAE. Active deployments in Greece and Taiwan. All three PowerBuoys simultaneously transmitting real time data from offshore at depths exceeding 1,000m, integrated directly into #Anduril ’s Lattice platform. Autonomous docking and charging demo completed. And today, formal European defense engagement expansion announced.

Here’s the honest read on this. The market is still looking at $OPTT as a small loss making marine company. The financials are still rough, the pipeline is real but uncontracted revenue, and the stock is thinly traded. That’s not nothing and I’m not going to pretend the risks aren’t there.

But the company itself has moved. Quietly and steadily, from one research buoy to a multi continent autonomous maritime network running live for DHS, Navy, UAE defense customers, and now actively pursuing European defense contracts. That’s not the same company the market is pricing.

I keep thinking about $ONDS. When it was trading under $1, nobody was paying attention. The backlog was building, the defense relationships were forming, and the market still saw a small drone company losing money. Then the revenue hit, the contracts closed, and the re-rating came fast. The pattern isn’t identical but the dynamic is familiar.

If $OPTT closes one or two European defense contracts, the conversation changes. NATO nations are actively increasing maritime security spending right now, and the technology they need, persistent autonomous offshore surveillance with no crew and no fuel, is exactly what @OceanPowerTech builds. That’s not a coincidence. That’s positioning.

🔗proactiveinvestors.com/compa…

Apr 20

Yes, this is $OPTT. And what’s happening here is a lot more interesting than just a Coast Guard surveillance story.

@OceanPowerTech Ocean Power Technologies just deployed its first PowerBuoy under a $6.5M DHS contract off the California coast last week. Each buoy sits offshore indefinitely, self powered by wave energy, feeding sensor data into Anduril’s Lattice command and control system alongside surveillance towers already in the water. No shore cables. No fuel. No crew. Just persistent eyes on the ocean running continuously.

The part most people miss is the architecture. $OPTT isn’t just selling hardware to the government. It’s becoming a node in a defense intelligence network that #Anduril is building. Every buoy feeds into Lattice, and the more buoys go in the water, the more valuable the whole network gets. You don’t really replace that once it’s built in.

And the use case isn’t going anywhere either. Migrant smuggling, drug trafficking, adversarial maritime activity off the U.S. coastline. The Coast Guard can’t put manned assets everywhere. Wave-powered buoys that run indefinitely and feed straight into AI driven command systems are a pretty obvious answer to that problem, and nobody else is really doing this at scale.

Backlog up 165% year over year to ~$19.9M. Pipeline sitting at ~$163.9M. First buoy in the water last week. Financials are still a mess, but the #Anduril integration is what makes this story different from a typical small defense contractor.

2

3

42

7,333

Jun 1

$ABCL has been quietly recovering and the more I sit with this company, the more I think the market is still underestimating what’s actually here.

Let me be honest about why I feel this way, because it’s not just the Phase 1 data or the Q3 catalyst, though both matter enormously.

It’s the management.

Carl Hansen founded this company, still runs it, and owns 20.9% of the outstanding shares. That’s a founder with 20.9% of his own company on the line. When he said on the May 11 earnings call that the Phase 1 data showing robust NK3R target engagement at well-tolerated doses with a pharmacokinetic profile supporting once monthly dosing makes him confident heading into Phase 2, that’s not investor relations language. That’s a scientist who spent years building a platform talking about his own molecule.

The financial discipline also reflects that. Q1 revenue of $8.3M, almost double year over year and well ahead of estimates. Loss per share of $0.14 beat the $0.17 consensus. Net loss narrowed. R&D investment increased. Cash and liquidity at $655M with current ratio of 10.2 and minimal debt. For a clinical stage biotech, this is a company being run carefully and thoughtfully, not burning recklessly toward a single bet.

And the institutional read keeps getting stronger. Goldman accumulated 4.3M shares in a single quarter. Baker Bros increased from 9.1% to 10.8% the day before the Phase 1 readout. An insider made a fresh purchase on May 18, after the data was already out. Cantor Fitzgerald initiated Overweight. Evan Seigerman reiterated Buy. Analyst consensus around $8-9 against a stock that’s been recovering from well below that.

A drug discovery engine with 203 clinical programs and 14 molecules in clinical stage, and ABCL635 is just the most advanced one right now. AI driven discovery that helped develop bamlanivimab in under 90 days during COVID. The platform generates value whether or not any single program succeeds.

Phase 2 topline data Q3 2026. $6 billion addressable market with no clean non hormonal solution. A management team with real skin in the game. And a stock that’s been quietly proving the accumulation thesis right.

LONG🚀😉#ABCL

May 21

$ABCL Called the accumulation phase. The stock is coming back.

When I posted about treating the post-Phase 1 sell off as an opportunity, the thesis was simple. The data wasn’t bad. The market just wanted efficacy numbers that Phase 1 isn’t designed to deliver. Everything that actually mattered came back clean.

And since then the story has only gotten stronger.

Phase 1 data confirmed zero liver toxicity across all doses from 30mg to 900mg. Zero serious adverse events. Strong NK3R target engagement confirmed. Half life of approximately 24 days supporting once monthly dosing. Phase 2 already enrolling. Q3 topline data on track.

Then on May 18, an insider made a fresh share purchase. Goldman sitting on 4.3M shares. Baker Bros increased from 9.1% to 10.8% the day before the readout. Cantor Fitzgerald initiated Overweight. Evan Seigerman reiterated Buy with $7 price target citing strong Phase 1 data and platform strength. Analyst consensus sitting around $9.00 against a current price that’s been recovering.

Revenue doubled year over year in Q1. Net loss narrowed. $655M in liquidity. Four programs in clinical or IND enabling stage. ABCL575 Phase 1 data coming H2 2026. The pipeline isn’t #ABCL635 alone.

Q3 is still the moment. The setup going into it keeps getting cleaner. 😉

4

7

72

5,732

May 28

This is the next chapter for $DMRC, and it's a meaningful one.

When I posted about Digimarc @digimarc a while back, the thesis was about AI-generated content, the EU AI Act mandate, and a company that had been quietly building the trust infrastructure for decades. What just got announced takes that thesis into a completely new direction that I didn't fully anticipate.

Autonomous Al agents are the next wave. Not Al that helps humans write or create, but AI that actually executes tasks independently.

Books flights, processes contracts, makes decisions, interacts with other systems without a human in the loop. The problem nobody has fully solved yet is how you verify what those agents are doing. Is this action authorized? Is this content authentic? Did a legitimate system generate this output or was it tampered with?

That's exactly what Digimarc just announced infrastructure for. Provenance and verification for autonomous AI workflows. The same digital watermarking IP they've deployed for 30 years in currencies and physical products, now applied to the layer that validates what AI agents are actually doing and whether it can be trusted.

And this isn't just a press release. The Q1 earnings call CEO said plainly that enterprises will require an ultra-scalable way to verify what is real, authentic and authorized as AI systems become more autonomous, and that idea is gaining widespread acceptance. Pilot programs are already running. They're already in conversations with the U.S. government through the SOFWERX Field Forward Technology Sprint, which is a defense rapid prototyping program. That's not a company guessing at a market. That's a company being pulled into it.

The May 15 holding company reorganization completed cleanly. Still trades as $DMRC on Nasdaq.

Revenue is still small, $7.6M in Q1, and down year over year from two contract losses. The numbers are still ahead of the story. But subscription gross margin hit 90%. The platform itself is highly profitable once customers are on it.

Thirty years of watermarking IP. C2PA co chair. EU AI Act compliance mandate already in force. And now the first provenance infrastructure purpose-built for autonomous AI agents. The market hasn't caught up to what this company is becoming yet.

🔗businesswire.com/news/home/2…

Apr 7

Everyone’s chasing semiconductors, space, and AI right now, and honestly same, I’ve been deep in all of it. But there’s one company I keep coming back to quietly, one that’s building something in a completely different direction. That’s $DMRC Digimarc, and let me explain why it’s been on my radar.

They do digital watermarking. Embedding invisible identification into content so you can prove what it is, where it came from, and whether it’s been tampered with. They’ve been doing this for nearly 30 years, and one of their longest running deployments is with a consortium of the world’s central banks to deter currency counterfeiting. Not a new idea for them at all.

And honestly the reason this feels more urgent now is pretty obvious when you think about it. AI generated content is everywhere, deepfakes, synthetic images, AI written text, and the question of is this real is getting harder to answer every single day. Digital watermarking is one of the most viable solutions to that problem at scale, and $DMRC has been quietly building the infrastructure for exactly this for decades without much fanfare.

The 2026 piece is worth paying attention to though. The EU AI Act comes into full force in May 2026, and it mandates watermarking and labeling of AI generated content across the board. Non compliance means fines up to 15 million EUR or 3% of global annual turnover, whichever is higher. This applies to any AI company operating in Europe, which is basically everyone.

What kind of got me was this part. $DMRC developed the industry’s first digital watermarking solution compliant with C2PA 2.1, the standard the industry is converging around, and they co-chair the watermarking task force for that standard. So they’re not just selling into this space, they’re literally at the table where the rules are being written. That’s a different kind of positioning.

The honest risk is the financials are still rough. Small cap, still burning cash, stock has been quiet for a while. The story is ahead of the numbers right now. But regulation moving in this direction with $DMRC sitting at the center of the standard, that’s not nothing. Staying on my watchlist for sure.

1

1

12

667

May 27

SpaceX’s IPO is coming, and the capital flowing into the space sector right now is real. But not all space stocks are created equal, and $RDW Redwire is the name I keep coming back to as the most structurally interesting play in this wave. And I’m not just watching, I’m holding. And the reason I keep coming back to $RDW specifically isn’t just momentum.

Most space stocks are betting on a future that hasn’t arrived yet. Redwire is different because they’re already embedded in the infrastructure that makes space happen today. Their Roll Out Solar Array technology powers the International Space Station, NASA’s Gateway lunar platform, and commercial satellites. When #SpaceX launches, Redwire solar arrays are often on the payload. If SpaceX scales to the launch cadence they’re targeting, the demand for Redwire’s hardware doesn’t speculate about the future. It compounds with every mission.

The MANUS robotic lunar arm for the European Space Agency just completed testing and delivery. Docking systems contract with The Exploration Company, eight figures. Space Force $1.8B Andromeda IDIQ access. In space 3D printing capability that nobody else has at commercial scale. Redwire is building the physical layer that every space economy participant actually needs to operate.

The defense side is also stacking fast. A NATO ally just awarded a multi-year, high eight figure Penguin Mk3 UAS contract. The U.S. Army added a $15M follow-on Stalker UAS order, the third in eight months. Defense and space both accelerating simultaneously under the same roof.

Q1 2026 revenue hit $96.97M, up 57.9% year over year. Record contracted backlog of $498.1M.

The revenue growth is real.

The honest risks are significant.

Q1 missed both EPS and revenue estimates. Gross margin is only 5.2%. The company is still deeply unprofitable. And after a 90% move in May alone, the stock is now trading well above analyst consensus of $14.44. This is a volatile momentum name, not a value play.

But the SpaceX IPO doesn’t just bring attention to the sector. It brings sustained capital and sustained launch volume to an ecosystem where Redwire holds the physical infrastructure. Owning a rocket stock is a bet on launches. Owning RDW is a bet on everything those rockets need to carry.

Holding @Redwire $RDW and watching this one closely as the space economy buildout accelerates. 😉

Mar 24

This looks small but I think it matters more than it seems for $RDW.

The ~$12.8M is not the story. What stands out is this is both a first sale and a standard component selection.

First sale means ELSA actually made it into a real program. For new space hardware that is usually the hardest step. But being baselined inside Moog’s METEOR platform is the bigger signal.

It does not guarantee revenue, but it creates a path. Every time that platform is used ELSA now has a seat at the table. That is very different from a one off contract.

Technically this lines up with where the market is going. Higher power density lower mass faster production. That is exactly what large satellite constellations and defense systems need.

From an investment perspective this is not about a single contract. It is about positioning inside a platform, and that is where repeat revenue starts to show up.

Feels like Redwire is starting to move from selling parts to getting embedded inside systems.

Market might be missing that.

$RDW

1

12

2,899

May 26

$HLIT Harmonic has been running since the Q1 earnings drop and the story behind it is worth understanding.

Q1 2026 numbers came in way ahead of expectations. Revenue $121.7M against analyst estimates of $104.3M, a 16.7% beat. Broadband revenue up 43% year over year. Rest of Market broadband up 78%. Backlog and deferred revenue hit $582.1M, up 87% from a year ago. Net income per share $0.17, well past the $0.11 to $0.12 guidance range. Operating profit from continuing operations $26M against ~$18-20M guidance. Full year 2026 broadband revenue guidance raised to ~$475-495M. Every number beat, and then guidance went up on top of it.

The numbers are only half the story though.The company is selling its video business for $145M in cash, expected to close Q2. Once that’s done, $HLIT becomes a pure-play broadband infrastructure company. The cOS software platform virtualizes cable access, running DOCSIS 4.0 deployments for cable operators transitioning from legacy hardware to software-defined networks. Infrastructure that used to require dedicated physical equipment now runs on standard servers. Lower capex for the operator, recurring software revenue for Harmonic.

Customer concentration risk is also quietly disappearing. Rest-of-Market bookings are now over 50% of the total, meaning the business is no longer dependent on one or two large cable operators. That’s a different business risk profile than what the stock has been priced as.

On May 19, Harmonic announced the SeaStar Optical Node enabling cost-effective broadband expansion in brownfield MDU environments. DNA Finland already deploying it to reach multi-dwelling units that fiber couldn’t previously reach economically. New addressable market opening up.

Analyst moves post earnings: Rosenblatt raised target to $20, Buy. Needham raised to $18, Buy. Northland raised to $15, Outperform. Jefferies raised to $15, Hold. $200M buyback authorization also in place.

Honest risks. Insider selling continues, a company director flagged intention to sell 32K shares. Gross margin guidance of 50-51.5% is pressured by memory costs. GF Value flags it as overvalued at current levels. Three-year revenue CAGR of roughly -17% is the overhang the bull case has to work through.

A company pivoting from hardware heavy video into pure play software defined broadband with 43% revenue growth, a record backlog, and multiple analysts lifting targets. That re rating doesn’t feel done yet.

1

8

1,092

May 21

$ABCL Called the accumulation phase. The stock is coming back.

When I posted about treating the post-Phase 1 sell off as an opportunity, the thesis was simple. The data wasn’t bad. The market just wanted efficacy numbers that Phase 1 isn’t designed to deliver. Everything that actually mattered came back clean.

And since then the story has only gotten stronger.

Phase 1 data confirmed zero liver toxicity across all doses from 30mg to 900mg. Zero serious adverse events. Strong NK3R target engagement confirmed. Half life of approximately 24 days supporting once monthly dosing. Phase 2 already enrolling. Q3 topline data on track.

Then on May 18, an insider made a fresh share purchase. Goldman sitting on 4.3M shares. Baker Bros increased from 9.1% to 10.8% the day before the readout. Cantor Fitzgerald initiated Overweight. Evan Seigerman reiterated Buy with $7 price target citing strong Phase 1 data and platform strength. Analyst consensus sitting around $9.00 against a current price that’s been recovering.

Revenue doubled year over year in Q1. Net loss narrowed. $655M in liquidity. Four programs in clinical or IND enabling stage. ABCL575 Phase 1 data coming H2 2026. The pipeline isn’t #ABCL635 alone.

Q3 is still the moment. The setup going into it keeps getting cleaner. 😉

May 18

$ABCL dropped Phase 1 data and the stock sold off. I think that’s a mistake.

ABCL635 hit every single checkpoint Phase 1 is supposed to hit.

No liver toxicity at any dose. Zero serious adverse events. Testosterone suppression confirming strong NK3R target engagement. Half life of approximately 24 days, which is exactly what you need to support once monthly subcutaneous dosing.

The pharmacokinetic profile came back clean. The tolerability profile came back clean. The company immediately advanced into Phase 2 on the strength of this data.

The market sold it because Phase 1 doesn’t come with efficacy numbers. That’s a different thing from the data being bad. Phase 1 confirmation is what makes Phase 2 credible, and that’s exactly what this was.

The piece that keeps coming back to me is the hepatotoxicity comparison. Veozah, the only approved oral NK3R drug, has a Black Box Warning for liver toxicity and still pulled $234M in 9 months. ABCL635 showed zero liver enzyme elevations across all doses tested from 30mg to 900mg in the Phase 1 data released last week. That’s the dosing headroom that Astellas never had. If higher doses are safe, you can push efficacy further than Veozah ever could.

Goldman sitting on 4.3M shares. Baker Bros increased from 9.1% to 10.8% the day before the readout. These people saw the data before we did. They added going into the announcement.

$655M in liquidity. EPS beat. Revenue beat. Phase 1 cleared. Phase 2 on track for Q3.

The sell off gave us a better entry on a story that actually got cleaner this week, not worse. Treating this as an accumulation phase.

5

6

42

10,065

May 21

$INFQ up 22% in premarket today and the reason is significant.

The Trump administration just announced $2 billion in grants to nine quantum computing companies, with the U.S. government taking minority equity stakes in each. Infleqtion is getting $100M. This isn’t a research grant. This is the federal government formally declaring quantum computing a national security priority and taking ownership stakes in the companies it believes will define the sector.

The grant headline is grabbing attention but there’s been a lot building underneath it.

One week ago, Q1 results came in with record revenue of $9.5M, up 14% year over year. Full year 2026 guidance raised to at least ~$40M. $569M in cash, zero debt. And on May 20, Infleqtion announced new technical breakthroughs on its neutral-atom platform, including 99.73% entangling fidelity and becoming one of the only companies to demonstrate a real-world application using logical qubits. The 30 logical qubit target for 2026 is still on track.

On May 13, Infleqtion introduced Quantum Spectrum, described as the first fundamental shift in RF sensing architecture in decades. That’s the sensing business, the part that’s already generating revenue while the computing roadmap matures.

The structural position hasn’t changed. $NVDA selected $INFQ twice across two separate partner categories for the Ising AI models. Citi at $20 price target. BTIG bullish. 12month analyst target $21, currently trading around $10-11 before today’s move.

Government money, technical breakthroughs, record revenue, raised guidance, and NVIDIA’s fingerprints all over the platform. The pieces keep connecting.

Apr 20

$INFQ has been running hard this week and the reason is pretty clear once you dig in.

NVIDIA just launched Ising earlier this week. It is the world’s first open-source AI models built specifically for quantum computing. They’re designed for quantum processor calibration and error correction decoding, and they’re running 2.5x faster and 3x more accurate than traditional methods.

Out of all the quantum companies NVIDIA highlighted, Infleqtion was the only one that showed up on both the calibration list and the decoding list. Citron Research jumped on it right away, calling it the most obvious mispricing in the entire quantum space right now. Their point was simple. Rigetti ($RGTI), which has roughly twice the market cap of $INFQ, didn’t make NVIDIA’s list at all. On top of that, Citi initiated coverage this week with a Buy rating and a $20 price target. The stock went from $9.81 at the end of March to an all time high of $21.28 on Friday. Basically an 80% run in under three weeks.

Most pure play quantum companies are still betting entirely on a future that hasn’t arrived yet. $INFQ is structurally different, and I think most people still haven’t fully clocked it. More on that below 🧵👇

2

2

9

1,415

May 20

Most people are looking at $TE and seeing a stock that’s down 27% year to date despite record quarterly EBITDA. I’m looking at it differently.

G2_Austin is the first major U.S. solar cell fab of its kind. 2.1 GW Phase 1. Concrete works started in April. First structural steel going up this month. Construction timeline unchanged. Engineering team finalized the full Issued for Construction package in early May. They’re not pitching a vision. They’re pouring concrete.

Q1 numbers backed that up. Record net income from continuing operations of ~$3.9M. Record Adjusted EBITDA of ~$9.1M. Revenue $177.65M beating estimates. G1_Dallas running and producing while G2 goes up simultaneously. 2026 production guidance of 3.1 to 4.2 GW maintained.

The remaining piece is the ~$225M Phase 1 financing, targeting Q2 completion. That’s the near term overhang keeping the stock where it is. But Situational Awareness LP just disclosed a stake, and analyst fair value is sitting at $8.90 against a current price around $5.67.

America needs domestic solar manufacturing that isn’t dependent on foreign supply chains. T1 is building exactly that in Texas. Every beam going up is a data point the market hasn’t priced in yet.

Every beam. Every day. Real progress. G2_Austin.

America needs more energy infrastructure, and it’s being built right here.

1

6

764

May 18

$ABCL dropped Phase 1 data and the stock sold off. I think that’s a mistake.

ABCL635 hit every single checkpoint Phase 1 is supposed to hit.

No liver toxicity at any dose. Zero serious adverse events. Testosterone suppression confirming strong NK3R target engagement. Half life of approximately 24 days, which is exactly what you need to support once monthly subcutaneous dosing.

The pharmacokinetic profile came back clean. The tolerability profile came back clean. The company immediately advanced into Phase 2 on the strength of this data.

The market sold it because Phase 1 doesn’t come with efficacy numbers. That’s a different thing from the data being bad. Phase 1 confirmation is what makes Phase 2 credible, and that’s exactly what this was.

The piece that keeps coming back to me is the hepatotoxicity comparison. Veozah, the only approved oral NK3R drug, has a Black Box Warning for liver toxicity and still pulled $234M in 9 months. ABCL635 showed zero liver enzyme elevations across all doses tested from 30mg to 900mg in the Phase 1 data released last week. That’s the dosing headroom that Astellas never had. If higher doses are safe, you can push efficacy further than Veozah ever could.

Goldman sitting on 4.3M shares. Baker Bros increased from 9.1% to 10.8% the day before the readout. These people saw the data before we did. They added going into the announcement.

$655M in liquidity. EPS beat. Revenue beat. Phase 1 cleared. Phase 2 on track for Q3.

The sell off gave us a better entry on a story that actually got cleaner this week, not worse. Treating this as an accumulation phase.

May 11

$ABCL This is the context that matters going into today’s Phase 1 readout.

Veozah, a Black Box Warning for hepatotoxicity and all, pulled $234M in 9 months in a market that’s still building. That’s not the ceiling, that’s what a drug with a Black Box Warning can do in a brand new market. The liver warning forced Astellas to cap the dose at 45mg even though Phase 2 data showed higher doses delivered better efficacy. They left effectiveness on the table because the compound itself was toxic, not the target.

If #ABCL635 comes back with clean safety today, that changes the dosing calculus entirely. An antibody mechanism that hits the same NK3R target without the hepatotoxicity risk could theoretically be dosed higher and deliver meaningfully better efficacy than Veozah ever could. That’s a meaningfully better drug in the same market, not just a slightly cleaner version.

Is most of the upside priced in right now? Maybe. Probably some of it. But I’ve been in this stock long enough to know that a down move on data, if it comes, would be an opportunity, not a reason to leave. The science here is real. The team is real. The platform behind ABCL635 has already proven it can move from discovery to clinic at a pace traditional pharma can’t match.

Whatever happens today, I’m not going anywhere. This is a company I trust, and that’s honestly the only thing that matters when you’re holding through a binary event.😉

6

4

84

13,211

May 14

$MXL keeps adding to the story.

Trinity platform just dropped today. URX850 SoC delivering carrier-grade bidirectional wireless backhaul at up to 10Gbps. What used to require multiple separate components, switching, QoS, wireless link aggregation, encryption, and timing functions, now sits on a single chip. Bharti Airtel, one of India’s largest carriers, is already on record saying they’ve been waiting for exactly this kind of integration.

The part worth understanding is that this has nothing to do with the optical interconnect story I was posting about earlier. That’s data centers. This is cell towers connecting to core networks. Two completely separate markets, both accelerating, both running on $MXL silicon.

Keystone PAM4 DSP for 400G and 800G optical transceivers in AI data centers. Rushmore targeting 1.6T. Panther going after memory latency. And now Trinity for 5G wireless backhaul at 10Gbps. The product roadmap keeps expanding into infrastructure layers that aren’t slowing down.

OEM products based on Trinity expected H1 2027. URX850 already deployed globally across major carrier networks. Available now.

This is what a picks and shovels position in multiple infrastructure cycles looks like.

🔗maxlinear.com/news/press-rel…

May 4

Called this one. Back when I posted about $MXL, it wasn’t getting a lot of attention outside of people already tracking the optical interconnect space. The Q1 numbers changed that conversation fast.

Revenue up 43% year over year to -$137.2M. Infrastructure segment, which is the optical connectivity piece, up 136% year over year and now the largest end market. Stock was the best performing IT name in April according to Seeking Alpha, with the top 10 IT performers delivering gains ranging from 71% to 336%, momentum concentrated in semiconductors, photonics, and power electronics as AI infrastructure buildout accelerated. $MXL was sitting at the top of that list.

Once you understand where MaxLinear actually sits in the stack, the move makes a lot of sense. They don’t make the transceiver. They make the semiconductor chips that go inside transceivers across multiple manufacturers. Whoever wins the transceiver market, $MXL supplies the silicon underneath. That’s not a bet on one customer or one design win. That’s a position in the layer that every optical interconnect solution depends on, and that layer is becoming more critical as AI clusters push bandwidth requirements to 800G and 1.6T.

And the analyst moves post-earnings aren’t small either. Price targets getting moved to 105% above current levels isn’t a minor adjustment. That’s the market catching up to a thesis that was already in the numbers for anyone paying attention.

Full year 2026 optical data center revenue guidance raised to $150M to -$170M. This isn’t a one quarter setup. Every major hyperscaler is still in the middle of a multi-year buildout and $MXL is in the supply chain for all of it. Still holding. Still watching. 🫣

1

15

5,639

May 14

$ONDS just dropped Q1 2026 results and every number came in ahead of expectations.

Revenue ~$50.1M. Analysts were expecting ~$38-40M. That’s a 25% beat on the high end of guidance. And compared to Q1 2025, revenue is up 1,065%. Not a typo. Ten times the revenue in one year.

The backlog is actually where it gets more interesting. Pro forma backlog hit $457M, up 570% from $68.3M at the end of 2025. That’s not organic momentum alone. That’s the Mistral acquisition bringing direct access to U.S. Army and Special Operations contract vehicles including a $982M IDIQ program for loitering munitions, World View adding stratospheric ISR capabilities, and global demand for autonomous drone and counter-UAS systems accelerating at the same time.

The pipeline is stacking faster than the revenue can recognize it.

The Palantir partnership is the piece I didn’t expect to see called out this prominently in the release. $ONDS and $PLTR co built something called SkyWeaver, an adaptive agentic AI platform at the edge that combines ONDS hardware and autonomy with Palantir’s data intelligence for rapid decision-making. The CEO described it as unique and symbiotic. When a defense autonomy company and Palantir are building shared operational systems together, that’s a different kind of relationship than a vendor contract.

The profitability timeline also got pulled forward. Product companies hit adjusted EBITDA positive in Q1, six months ahead of target. OAS profitability now expected Q1 2027 instead of Q3 2027. Management is running ahead of their own schedule, which doesn’t happen often.

Cash position sitting at $1.48 billion. Full year 2026 revenue target raised to at least $390M, representing roughly 670% year over year growth.

The honest risk is that adjusted EBITDA losses are expected to widen through Q2 as the company front-loads spending ahead of the H2 revenue ramp. Company wide profitability isn’t until Q1 2028. This is still a growth story, not a profitability story yet.

Still watching how fast the H2 ramp actually materializes. But the setup looks different than it did 90 days ago.

Been long since $0.80 and not going anywhere.✊💎

May 14

Ondas reported record Q1 2026 results with $50.1 million in revenue, raised its 2026 revenue target to at least $390 million, and expanded pro forma backlog to $457 million.

The quarter reflected accelerating demand across counter-UAS, ISR, and autonomous systems markets while advancing Ondas’ global operating platform and AI-enabled multi-domain ISR strategy. $ONDS

ondas.com/post/ondas-reports…

1

12

1,599

May 13

Called it on the thesis. Didn’t expect it to move this fast.

Since posting about $PENG, the stock has nearly doubled. Let me break down what actually drove it.

Q2 FY2026 revenue came in at $343M, beating estimates, and management doubled the full-year growth outlook from 6% to 12%. That guidance revision was the first real signal that the AI infrastructure pivot was showing up in the numbers. Then on May 10, a tripartite partnership with $AMD and Shell around AI powered data center capabilities dropped, and the stock jumped another 13% on the day. A golden cross technical formation added fuel as momentum traders piled in. Rosenblatt followed with a fresh price target and the stock ran to $52.85 after hours.

$PENG isn’t selling GPUs. They’re building the AI factories around them. Enterprise and sovereign AI customers need exactly that expertise, and the contract pipeline is starting to reflect it. And it’s exactly what I was pointing at when I first posted.

The honest risks are still there. Barclays downgraded to Equalweight. Advanced Computing momentum is slower than expected. Insider selling happened near the highs. P/E north of 54 is not cheap.

But the sovereign AI and enterprise buildout story hasn’t played out yet. This was the early innings.

Apr 30

$PENG Penguin Solutions is one of those companies that’s genuinely hard to explain in one sentence, and I think that’s part of why it’s still flying under the radar for a lot of people.

Think of $PENG as the company that takes $NVDA ’s GPUs and actually builds the AI cluster around them. The design, the architecture, the deployment, the ongoing management. The hardware is someone else’s. The expertise of putting it all together is theirs.

Here’s how I think about it. When a company, a government, a university, or a neocloud provider wants to build an AI cluster, they usually don’t have the in-house expertise to design, deploy, and operate it at scale. That’s where PENG comes in. 25 years of high performance computing experience, applied directly to AI factory buildouts. They handle the full stack, hardware selection, cluster architecture, deployment, and then ongoing managed services through their ICE ClusterWare platform. Over 3.3 billion hours of GPU runtime management under their belt. That’s not a number most companies can put on a slide.

What I keep coming back to is the customer diversification story. The AI infrastructure market spent the last two years being dominated by hyperscaler spending, lumpy, unpredictable, and concentrated. #PENG is actively pivoting toward enterprise, neocloud, and sovereign AI customers. Governments across Europe and the Middle East are building localized AI infrastructure to keep data within their borders. They can’t just call AWS. They need a partner who can design and operate the whole system. That’s a stickier customer profile than hyperscalers, and it compounds differently.

The software layer is the underappreciated piece. ICE ClusterWare is a proprietary cluster management platform purpose-built for AI workloads. That’s not commodity hardware reselling. It’s a software moat that generates managed service revenue on top of the hardware sale, and every dollar from managed services carries significantly higher margins than the hardware underneath it.

Q2 in early April showed revenue down year over year but net income up sharply and full year guidance raised to 12% growth. Goldman Sachs initiated with a Buy this morning. Barclays was already there. 8 analysts, Strong Buy consensus, average target around $28.

The honest risk is the transition period. Moving away from hyperscaler concentration toward enterprise and sovereign AI takes time, and the revenue line will be lumpy while that shift plays out.

But 25 years of HPC expertise, a proprietary software platform, managed services that compound over time, and a pivot toward sovereign AI and enterprise at exactly the moment those markets are accelerating. That’s the setup I’m watching.

10

1,380

May 11

$ABCL This is the context that matters going into today’s Phase 1 readout.

Veozah, a Black Box Warning for hepatotoxicity and all, pulled $234M in 9 months in a market that’s still building. That’s not the ceiling, that’s what a drug with a Black Box Warning can do in a brand new market. The liver warning forced Astellas to cap the dose at 45mg even though Phase 2 data showed higher doses delivered better efficacy. They left effectiveness on the table because the compound itself was toxic, not the target.

If #ABCL635 comes back with clean safety today, that changes the dosing calculus entirely. An antibody mechanism that hits the same NK3R target without the hepatotoxicity risk could theoretically be dosed higher and deliver meaningfully better efficacy than Veozah ever could. That’s a meaningfully better drug in the same market, not just a slightly cleaner version.

Is most of the upside priced in right now? Maybe. Probably some of it. But I’ve been in this stock long enough to know that a down move on data, if it comes, would be an opportunity, not a reason to leave. The science here is real. The team is real. The platform behind ABCL635 has already proven it can move from discovery to clinic at a pace traditional pharma can’t match.

Whatever happens today, I’m not going anywhere. This is a company I trust, and that’s honestly the only thing that matters when you’re holding through a binary event.😉

May 10

Tomorrow, $ABCL has its first Phase 1 readout for ABCL635. Most of the upside is priced in IMO. However, tomorrow's data will show: (i) if the mAb engages the target and it is not excluded by the blood-brain barrier; and (ii) preliminary safety which is very important (see below).

The next milestone will be efficacy. I am doing a long article about ABCL635 for after the ph1 readout, but I wanted to share something.

ABCL635 engages NK3r, same target as Fezolinetant (Veozah) from Astellas. The oral pill Veozah has made ~$234M in sales in the 9 months since launch in 2025, in a $4B VMS non-hormonal treatment market.

REMEMBER that this molecule has a BLACK BOX WARNING for Hepatotoxicity!!! AND $234M in 9 months!

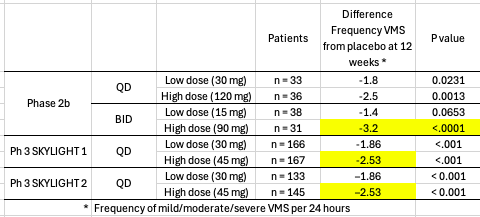

The table below shows the results from Fezolinetant in ph 2b and ph3s. In phase 2 they tested QD (one pill a day) vs BID (two pills a day) each at high and low doses (30 and 120 mg for QD and 15 and 90 for BID).

The endpoint was the difference in VMS frequency from baseline at 12 weeks. This means the reduction of episodes that the woman had of hot flashes compared to baseline (w/o the treatment). Example: -3 is better than -1, since -3 means they experienced 3 episodes less than baseline, while -1 means they experienced only 1 less.

The trend is clear for ph2 and ph3. The molecule clearly works and engages the target (p-value < 0.05 in most cases) and higher doses resulted in fewer VMS episodes. GOOD!!

However, they chose 45 mg of Fezolinetant for the Veozah pill, even if ph2 showed more reduction of VMS episodes at higher doses, WHY?? Higher dosage = Hepatotoxicity.

🚨My point: THERE IS A LOT OF EFFICIACY LEFT ON THE TABLE for ABCL635!!!

The hepatotoxicity is most probably due to the Fezolinetant compound, not the NK3r target engaged. IF this is true and ABCL635 doesn't have toxicity and is safe, AbCellera could trial a safer higher dosing resulting in HIGHER EFFICACY!!

If ABCL635 is safer and has more efficacy than Fezolinetant they would only compete over how convenient it is to have one pill a day or one shot a month, that is not up to me to decide.

But still, it will be a clear contender for the $6B non-hormonal treatment VMS market projected for 2030 and could maaaaaaaaaybe prey on the Hormone replacement therapy market of $26.5B by 2030. Big IF, I know, but there is a good chance.

6

1

38

15,703

May 11

$MRAM Everspin Technologies hit a 52-week high of $23.10 on Friday, and the stock is up about 266% over the past year. Most people haven’t come across this one yet. Worth changing that.

Everspin makes MRAM,

Magnetoresistive Random Access Memory. The simplest way to explain it is this. Your computer has two kinds of memory. DRAM is fast but forgets everything when the power goes out. Flash storage remembers everything but is slow to write. MRAM does both. It writes at near-DRAM speeds and remembers everything when the power cuts. Unlike flash, it doesn’t wear out after millions of write cycles. It also works at extreme temperatures and survives radiation. That combination doesn’t exist anywhere else in memory today, which is why aerospace, defense, industrial, and data center applications have been quietly adopting it.

Three things happened in April that changed the growth trajectory.

First, Everspin signed a 10-year manufacturing agreement with Microchip Technology to produce MRAM and TMR sensor products at Microchip’s Oregon fab. ITAR-capable, onshore U.S. production, first products shipping H2 2027. That’s supply chain security for defense customers who can’t rely on overseas fabs.

Second, a $40 million, 30-month subcontract with Amentum Services under a U.S. Navy microelectronics RDT&E program. Toggle MRAM process technology going directly into the U.S. defense supply chain.

Third, Q1 2026 results beat expectations. Revenue $14.87M vs $14.60M estimate. Needham raised their price target to $18.50 and maintained Buy.

The honest risks are real. CEO and CFO sold a combined $796K in stock in early May. Q2 guidance is soft, EPS range of $0.000 to $0.030. The stock is trading above the analyst consensus of $18.50, meaning a lot of execution has to go right from here. P/E of 2,532 tells you this is a story stock, not a value stock.

But the underlying thesis is hard to ignore. AI inference needs memory that is fast and persistent at the same time. Defense procurement is actively pulling MRAM into hardened systems. And Everspin is the only publicly traded pure play MRAM company in the world. If this technology gets the adoption cycle it’s been building toward, there’s nothing else to own in this specific bet.

3

2

14

4,185